Recession-Hard/Soft Landing

Our Portfolio Allocation Summary for September 2025.

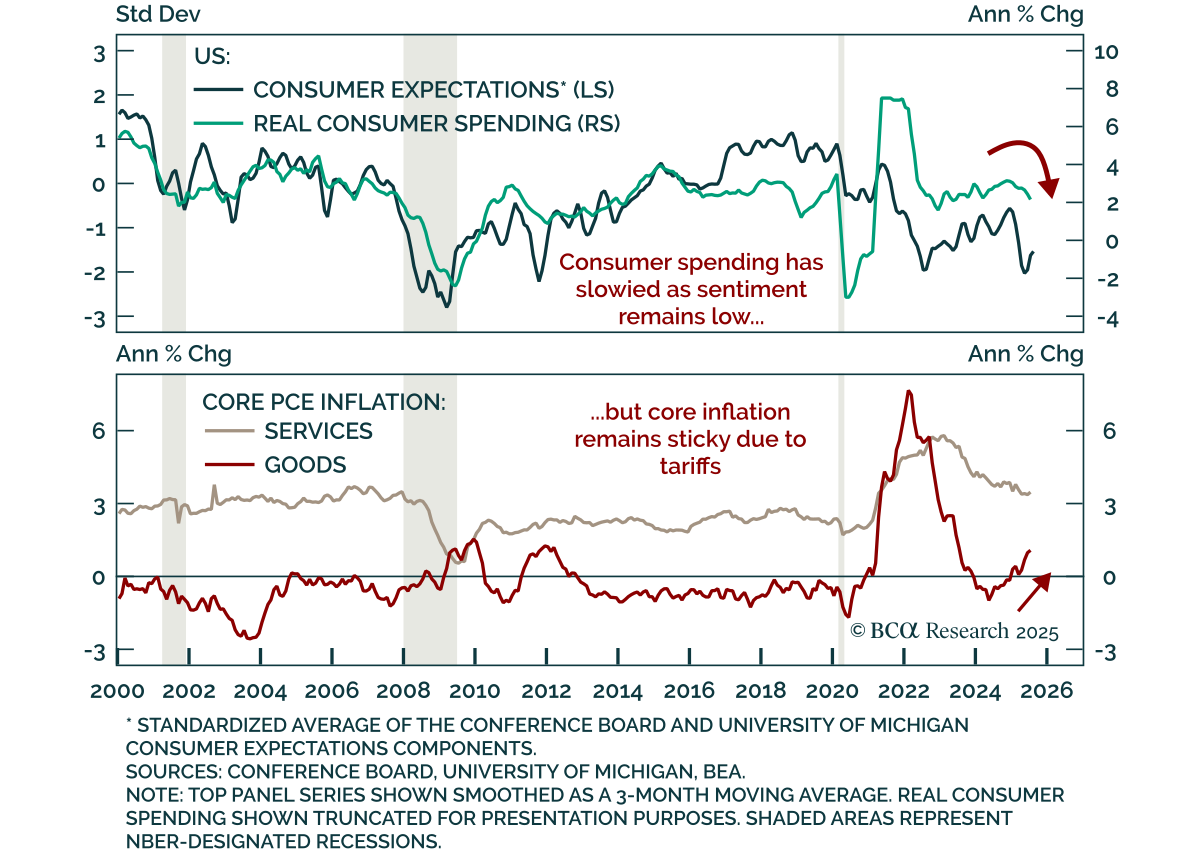

July income and spending data confirmed resilient consumption and sticky inflation, however, slowing labor momentum keeps us defensive. Real personal spending increased 0.3% m/m. Personal income rose 0.4% m/m, with real income ex-transfer payments…

Powell’s Jackson Hole speech was misread, and points to cautious dovishness. Some commentators called it hawkish, others suggested the Fed abandoned its 2% target. Neither is accurate. Central bank communication is rarely binary; it operates across…

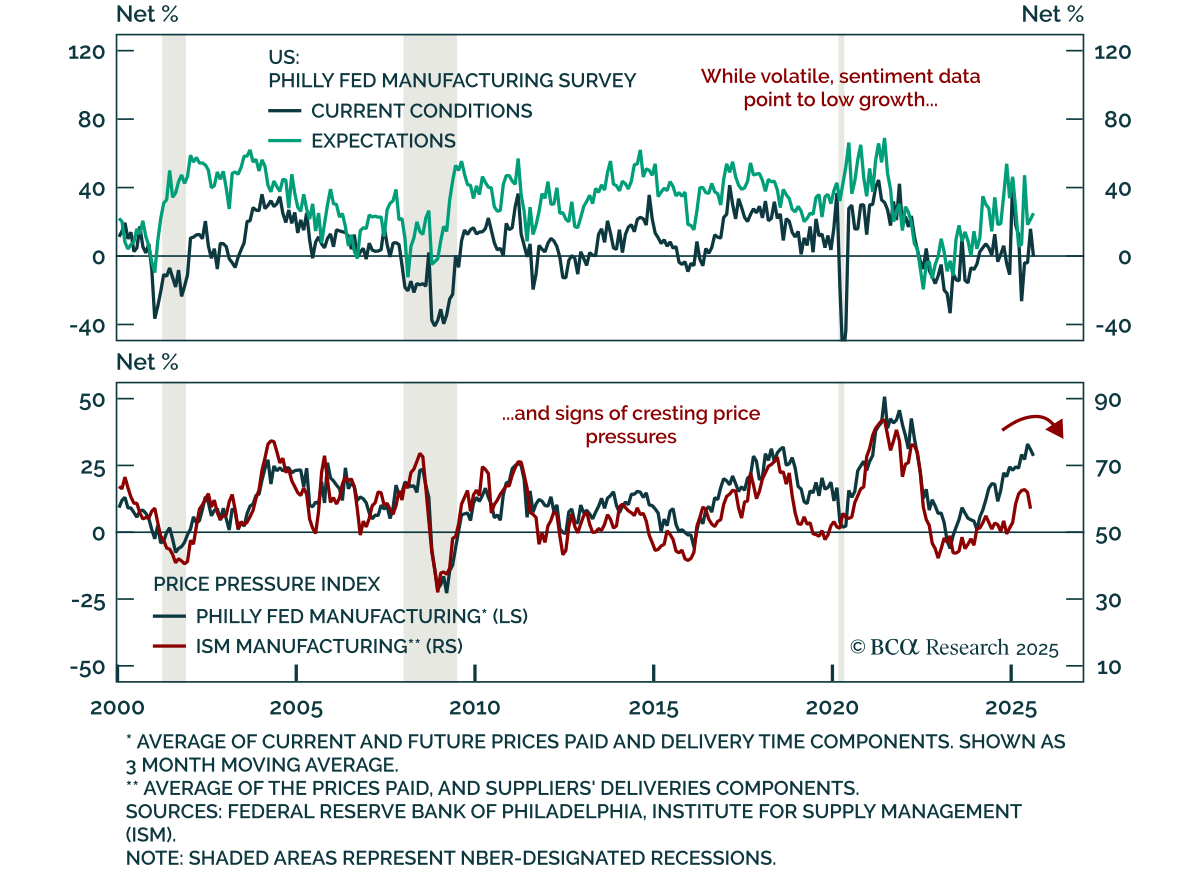

The Philly Fed’s August dip confirms persistent US manufacturing weakness and sends a disinflationary impulse. The index fell to -0.3 from 15.9 in July, with shipments, employment, and new orders all declining, the latter slipping into contraction.…

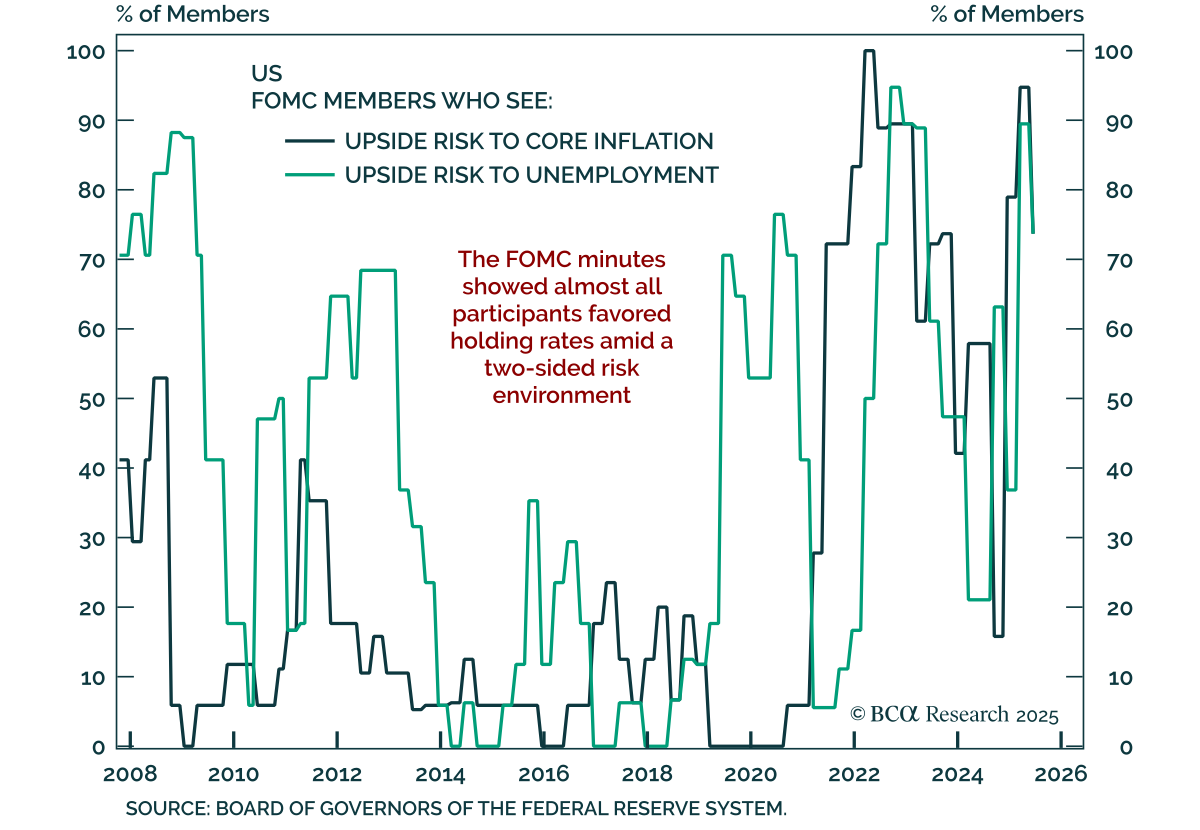

FOMC minutes showed broad support to hold in July, but the committee remains divided between proactive doves and reactive hawks. “Almost all members” favored leaving the funds rate unchanged, though two dissented for an immediate 25 bps cut. Doves want…

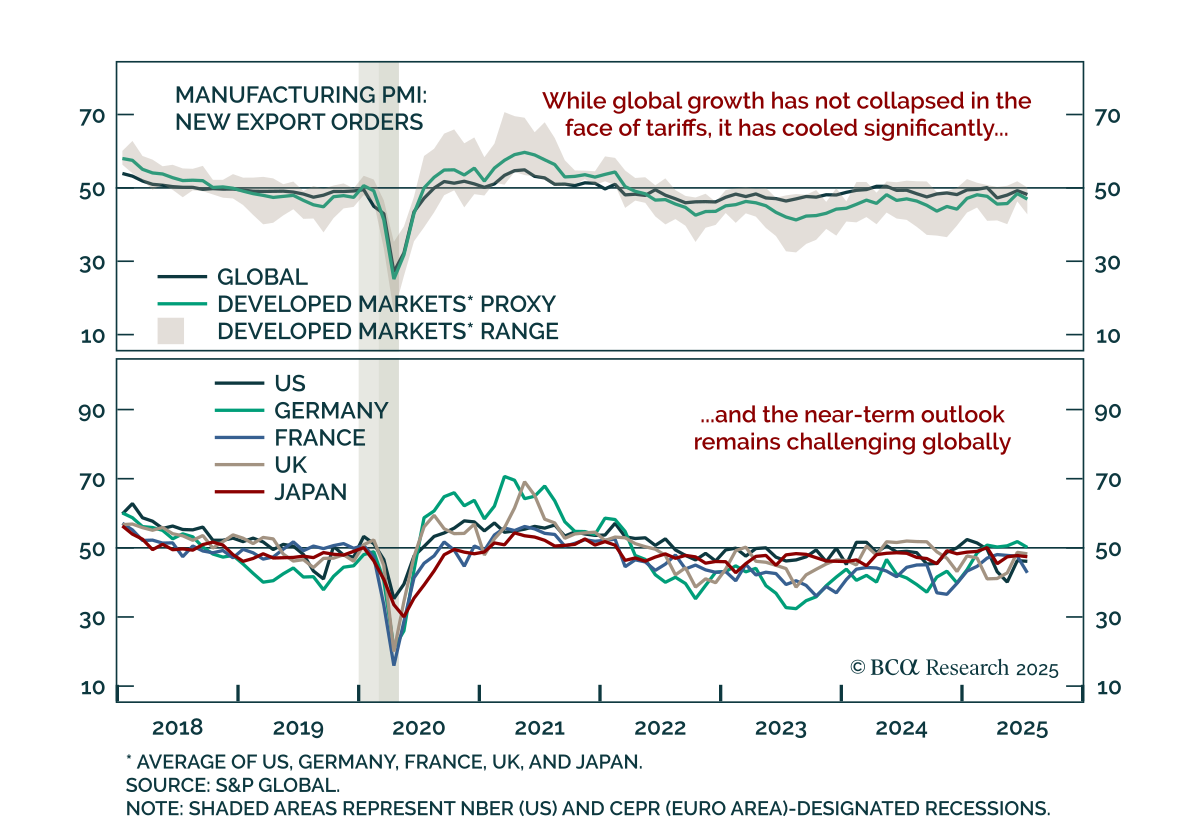

In response to trade uncertainty, global growth is cooling but not collapsing, supporting a cautious near-term view on risk assets. Trade disruption earlier this year raised fears of a global recession, but the data so far point to deceleration, not…

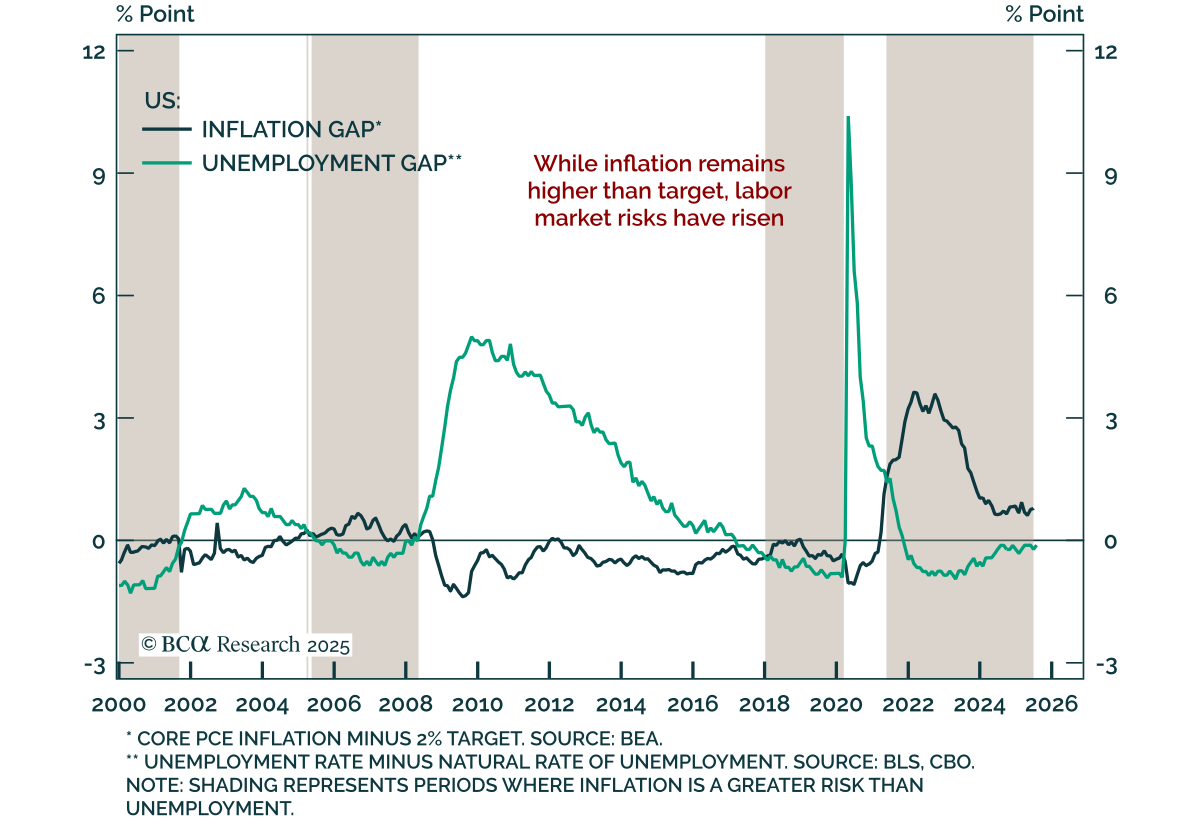

We maintain our 12-month US recession probability at 60%. However, until the “whites of the recession’s eyes” are more clearly visible, we would refrain from moving to a fully defensive stance.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

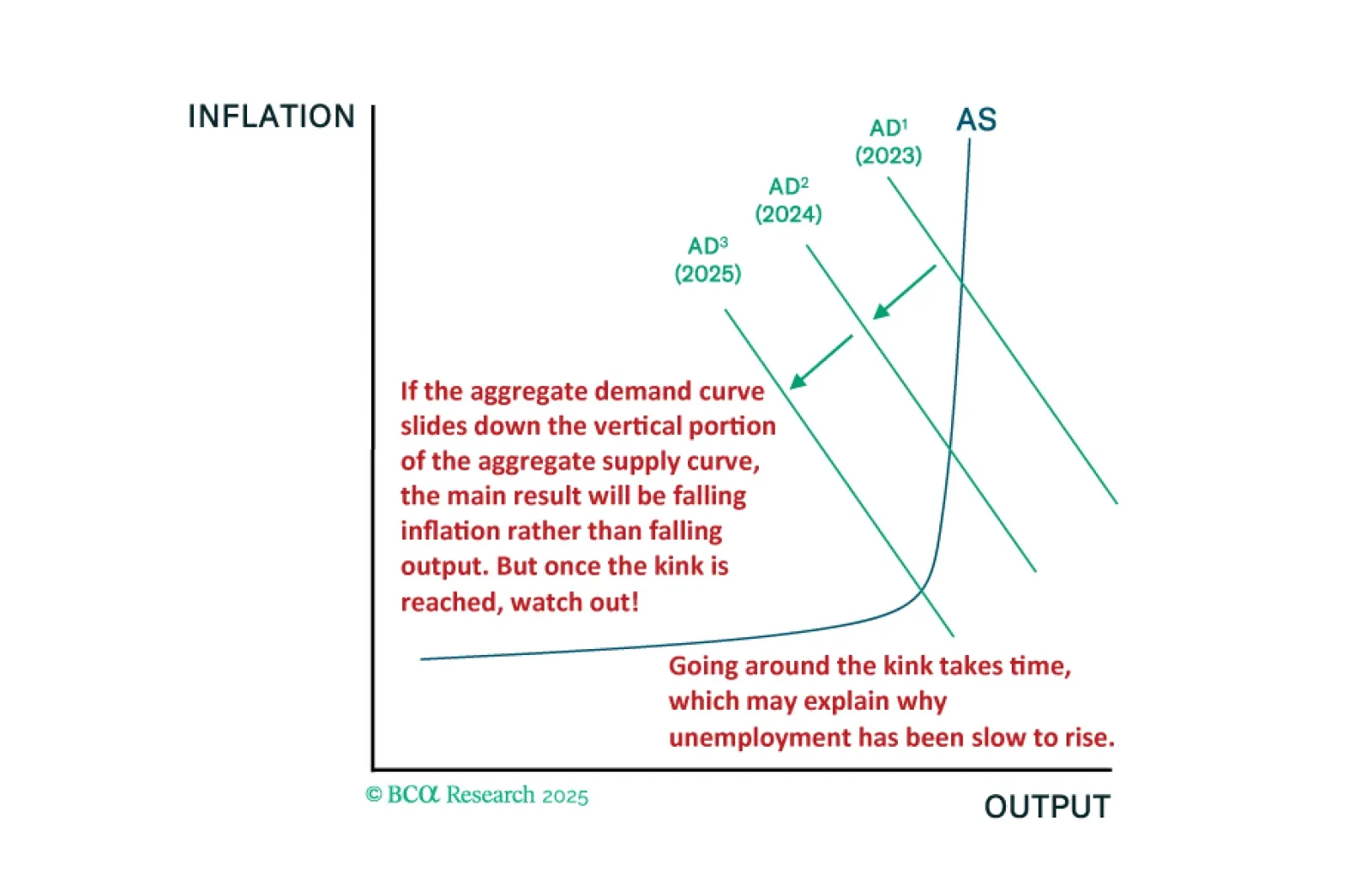

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

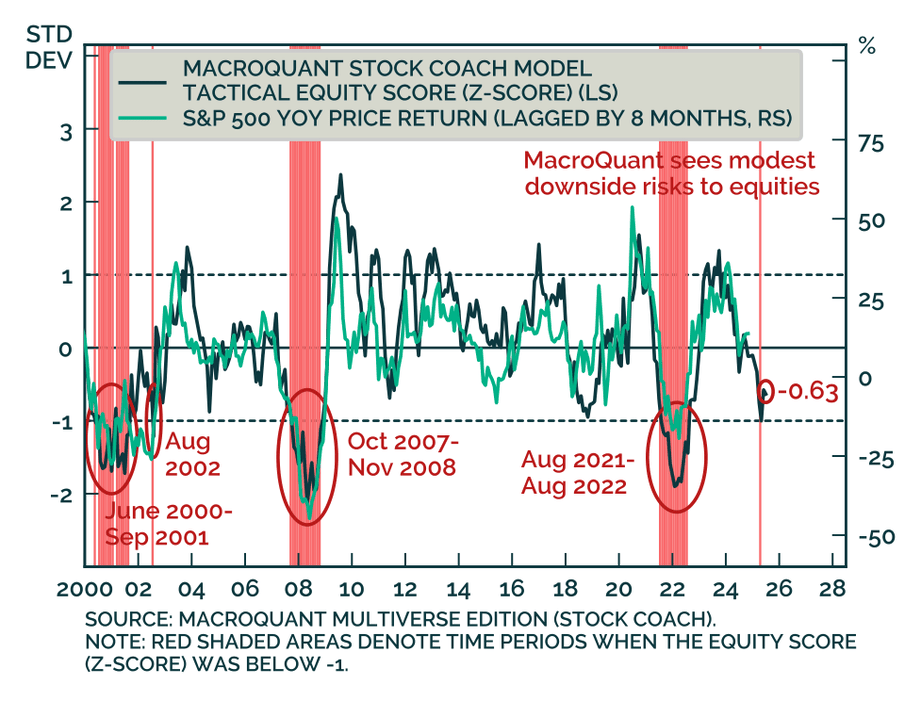

MacroQuant’s equity model points to mild downside risks for the S&P 500, supporting a modest equity underweight. Our Chart Of The Week comes from Chanhyuck Lee, from our Global Investment Strategy team. MacroQuant’s Stock Coach model, which…