Recession-Hard/Soft Landing

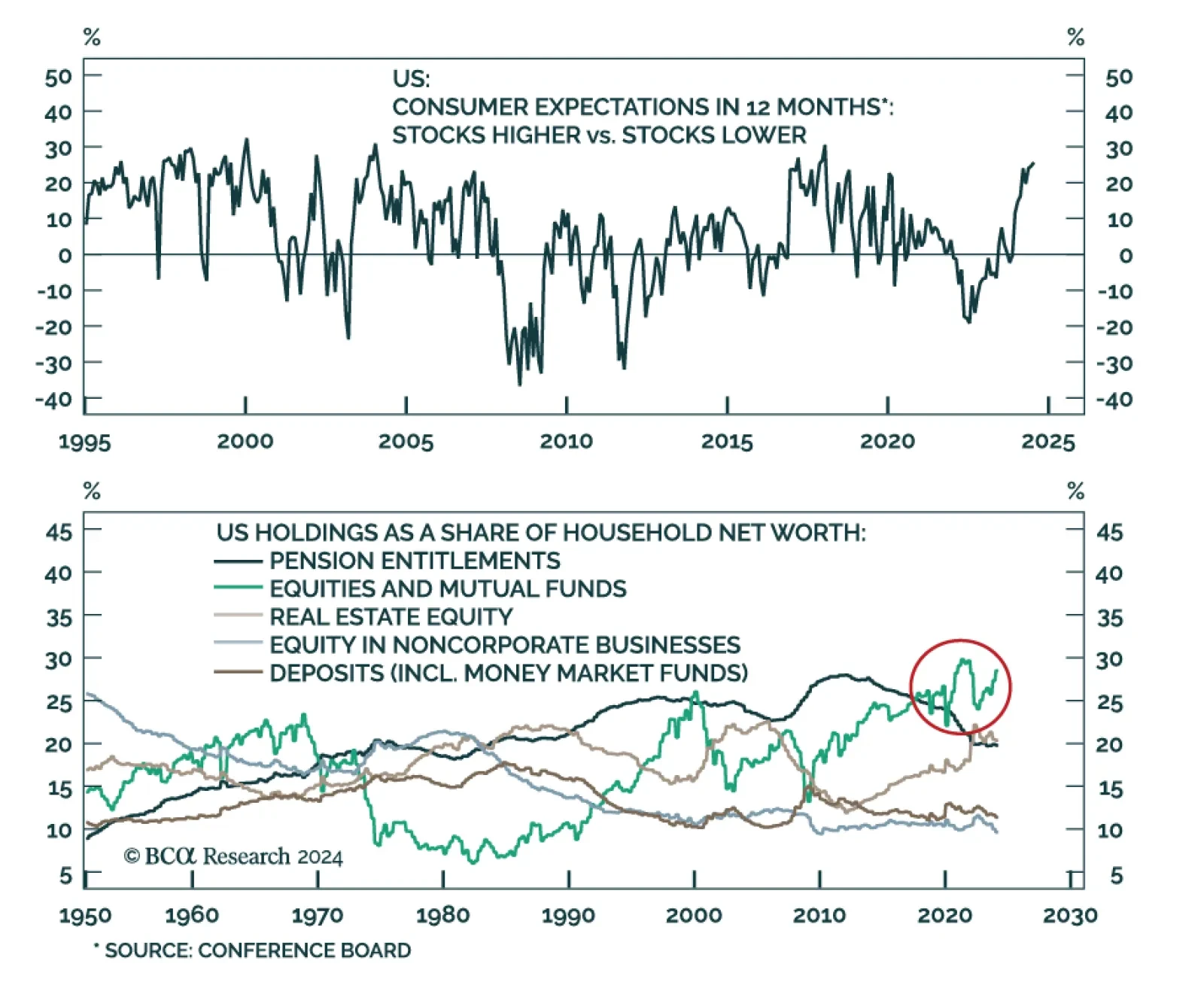

The latest Conference Board measure of consumer confidence suggested that consumers were increasingly downbeat about current economic conditions. Notably, their fading optimism about labor market conditions drove the jobs-plentiful-minus-hard-to-get measure…

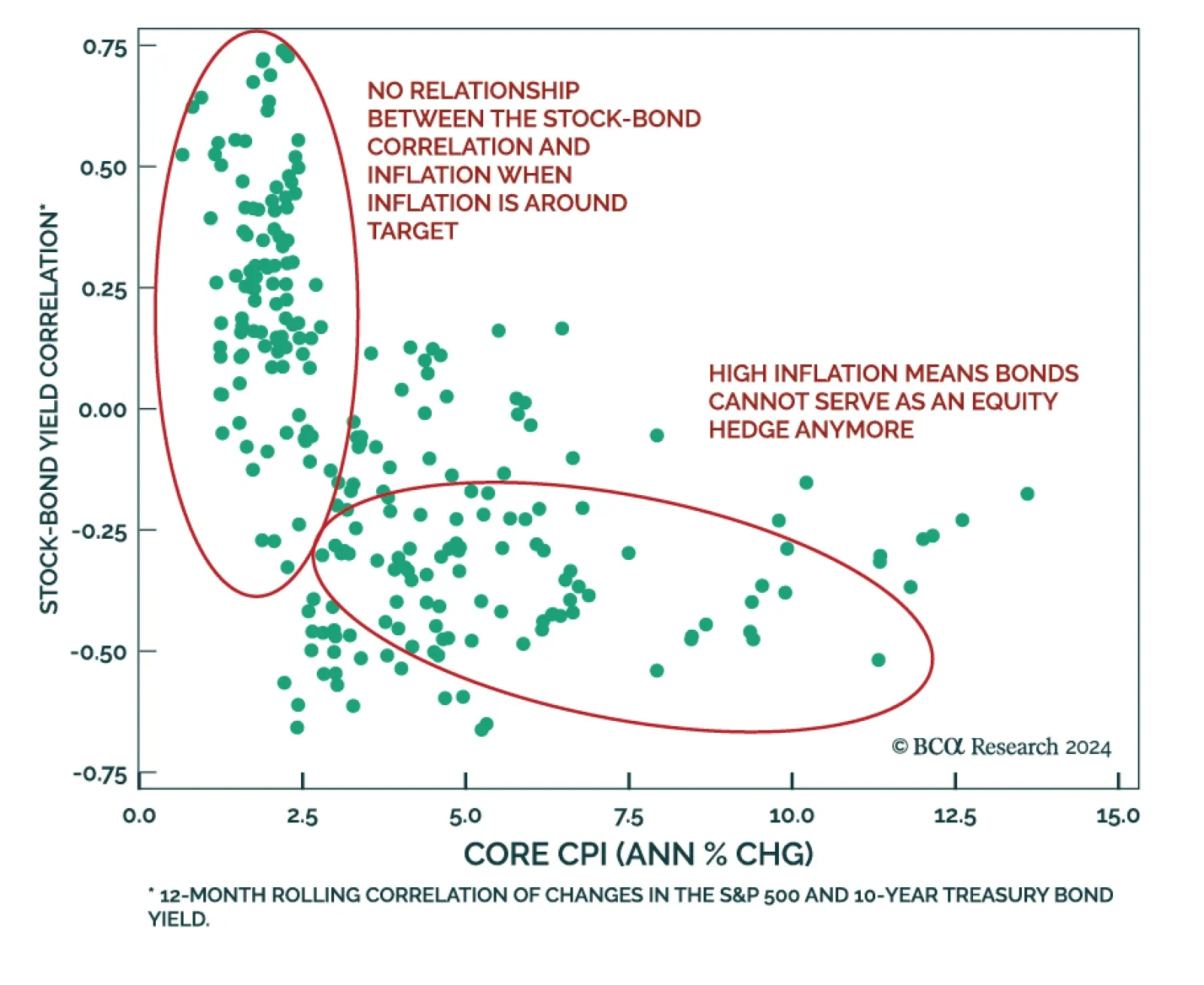

According to BCA Research’s Global Asset Allocation service, while the market action of the past few weeks is pointing to a return to a negative stock-bond correlation, more prints will be needed to confirm things are getting back to normal. The post-COVID…

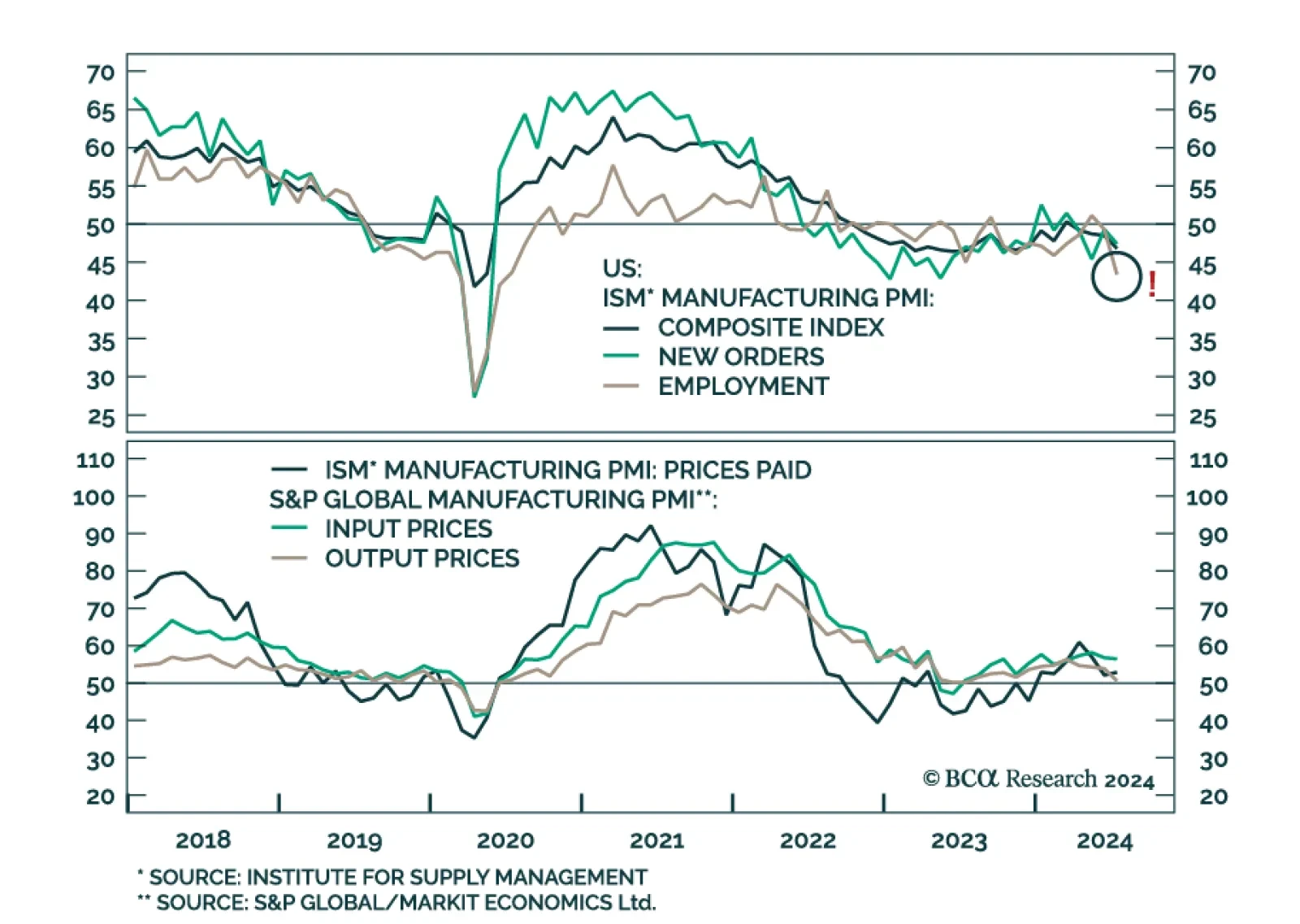

The ISM Manufacturing PMI disappointed in July. The headline index declined at a faster pace, from 48.5 to 46.8, disappointing expectations and extending a four-month contraction streak. Details were uninspiring. New orders dipped to 47.4 from 49.3,…

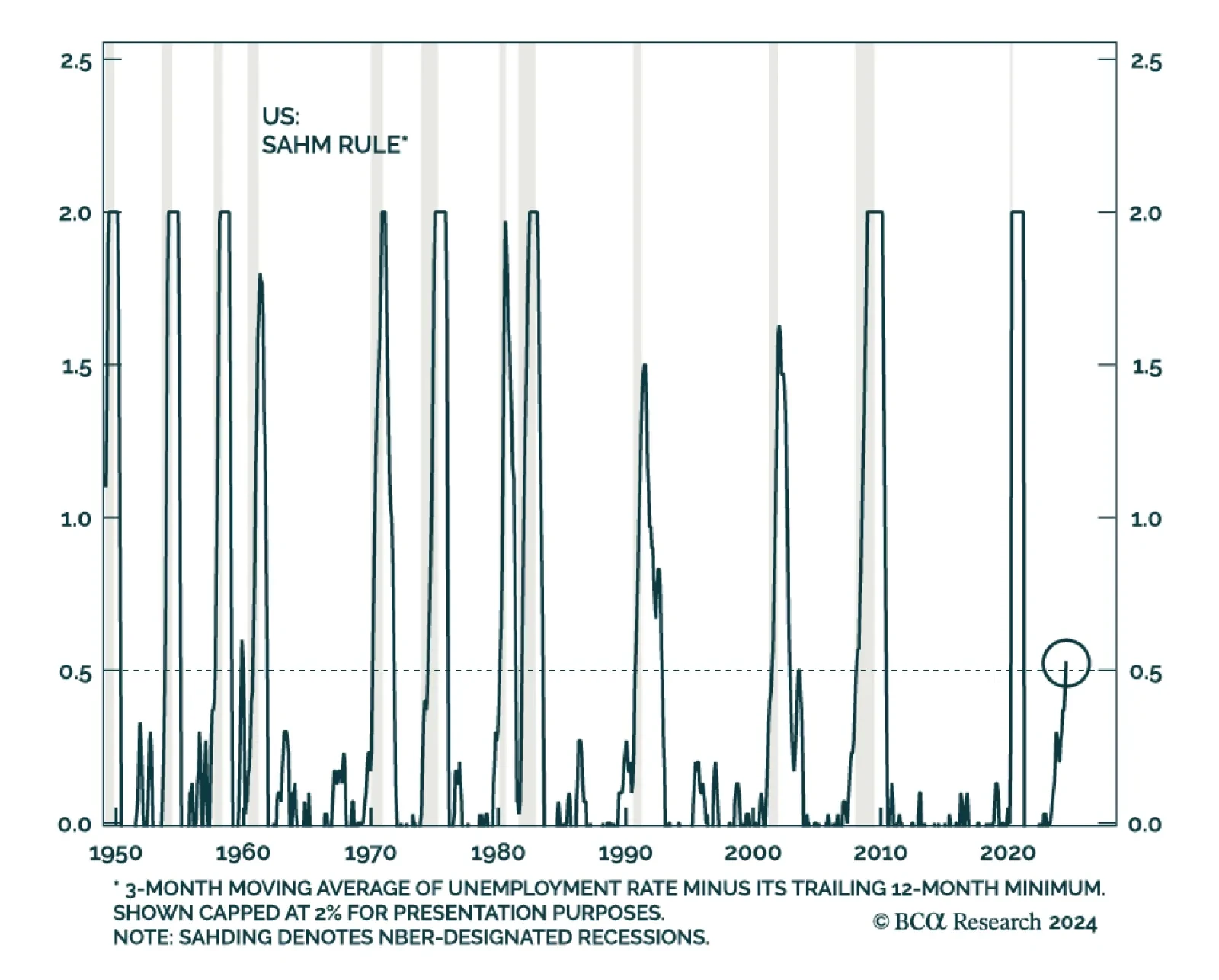

The Sahm Rule – a widely watched real-time recession indicator – signals the early stages of a recession when the 3-month moving average of the unemployment rate rises at least half a percentage point above its past 12-month low. The surprise rise in the…

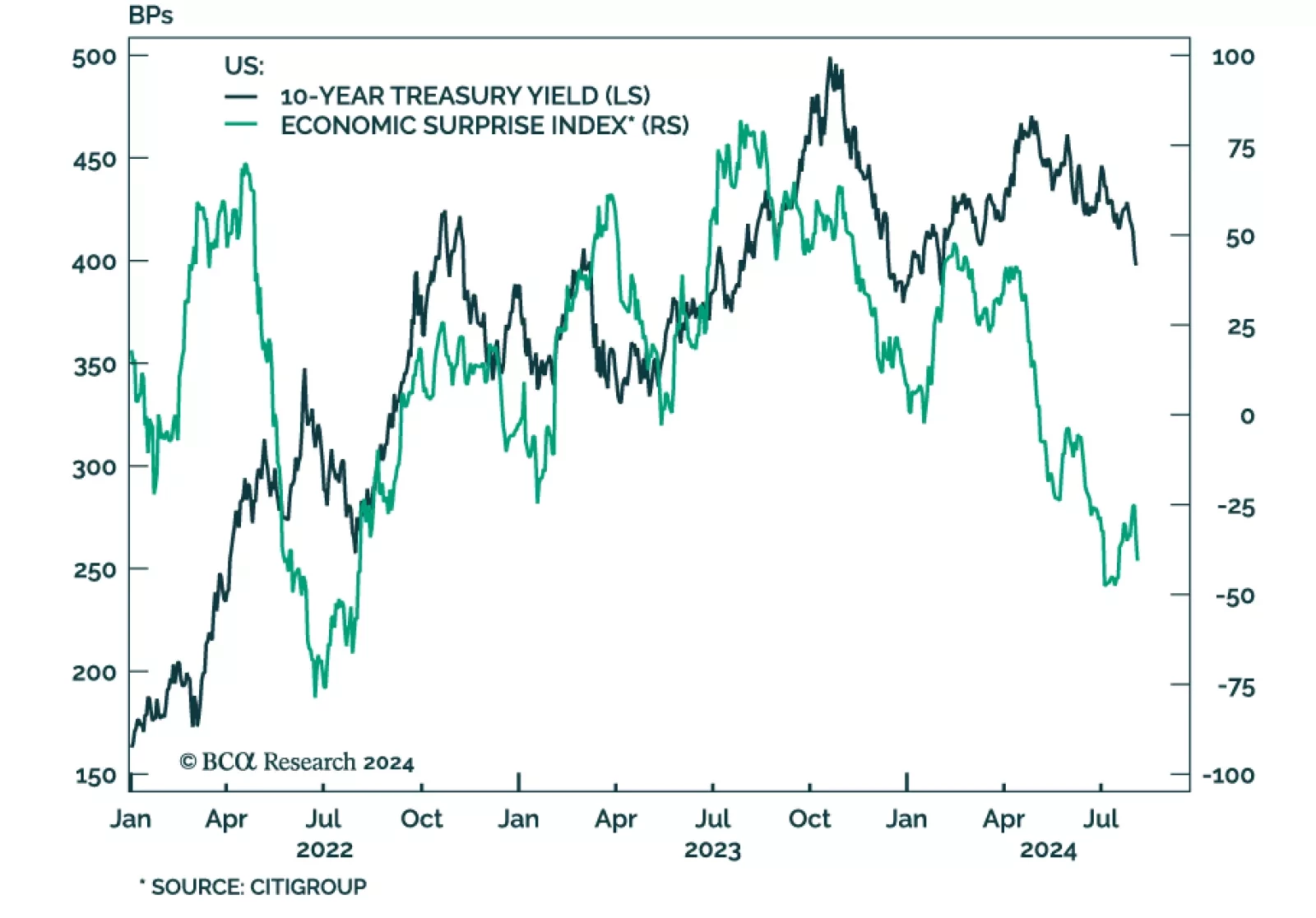

A decisive risk-off mood dominated markets at the end of last week, amid disappointing payrolls, tech earnings and manufacturing PMIs. The Nasdaq and other tech-heavy stock markets such as Japan, Korea and Taiwan led the equity declines. Other pro-cyclical…

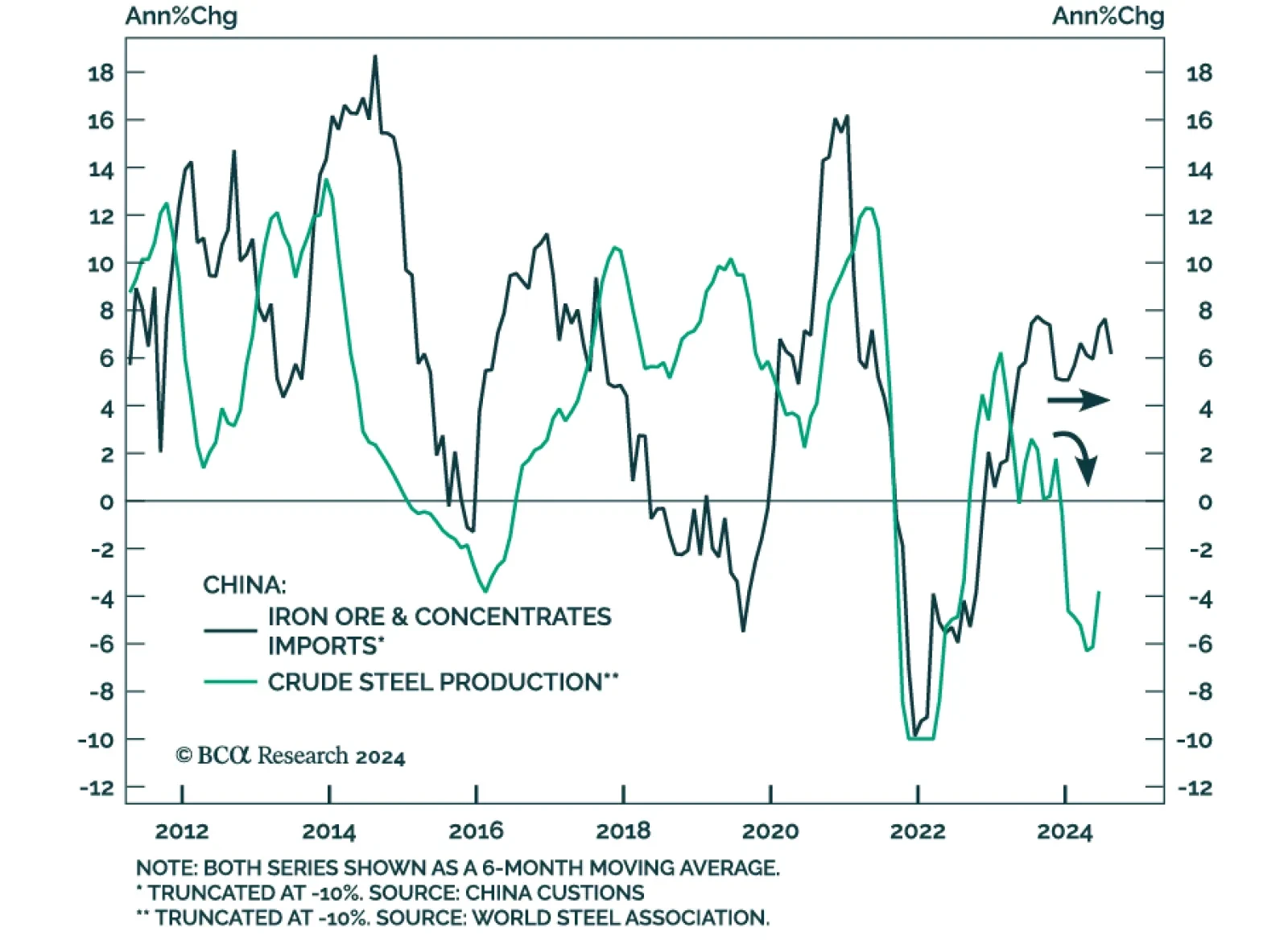

According to BCA Research’s Commodity & Energy Strategy service, robust iron ore imports are sending a false signal about steel demand. Instead, these supplies are being used to restock inventories. By the end of last year, iron ore stocks at Chinese…

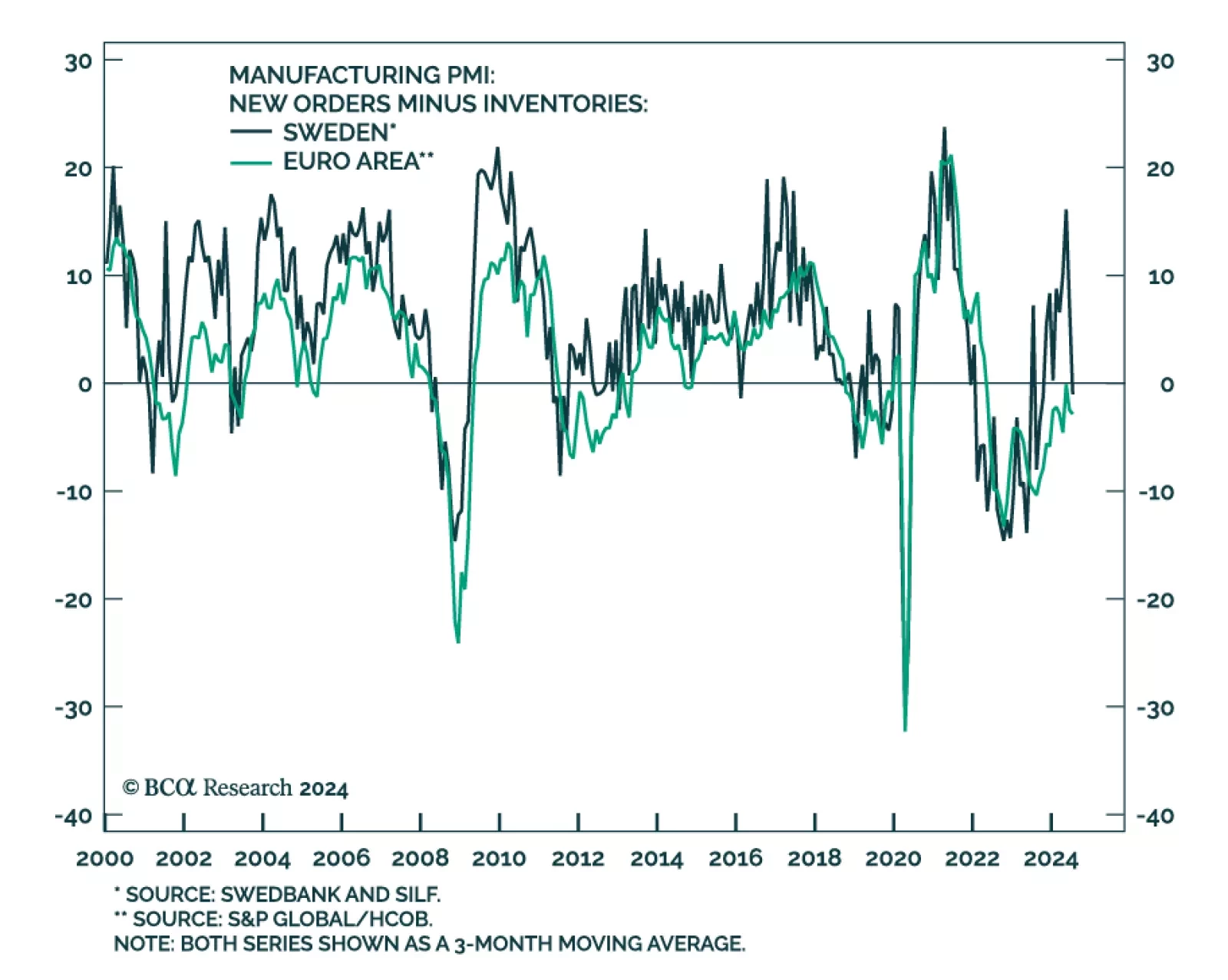

Sweden’s manufacturing PMI started contracting in July, plummeting from 53 to 49.2, falling far short of expectations that growth would broaden. Weakness was broad-based. Notably, new orders and new export orders plunged a whopping 15.1 and 8.7 points in…

According to BCA Research’s Global Asset Allocation service, there are clear signs that growth is weakening. BCA’s Global Nowcast has been slowing for three months. Behind this slowdown is the fact that the US consumer – the biggest factor keeping growth…

Eurozone headline CPI inflation unexpectedly accelerated in July, from 2.5% y/y to 2.6%. Core CPI remained stable at 2.9% despite expectations it would ease. EU Harmonized CPI accelerated in the regions’ three largest economies, surprising by a large margin…

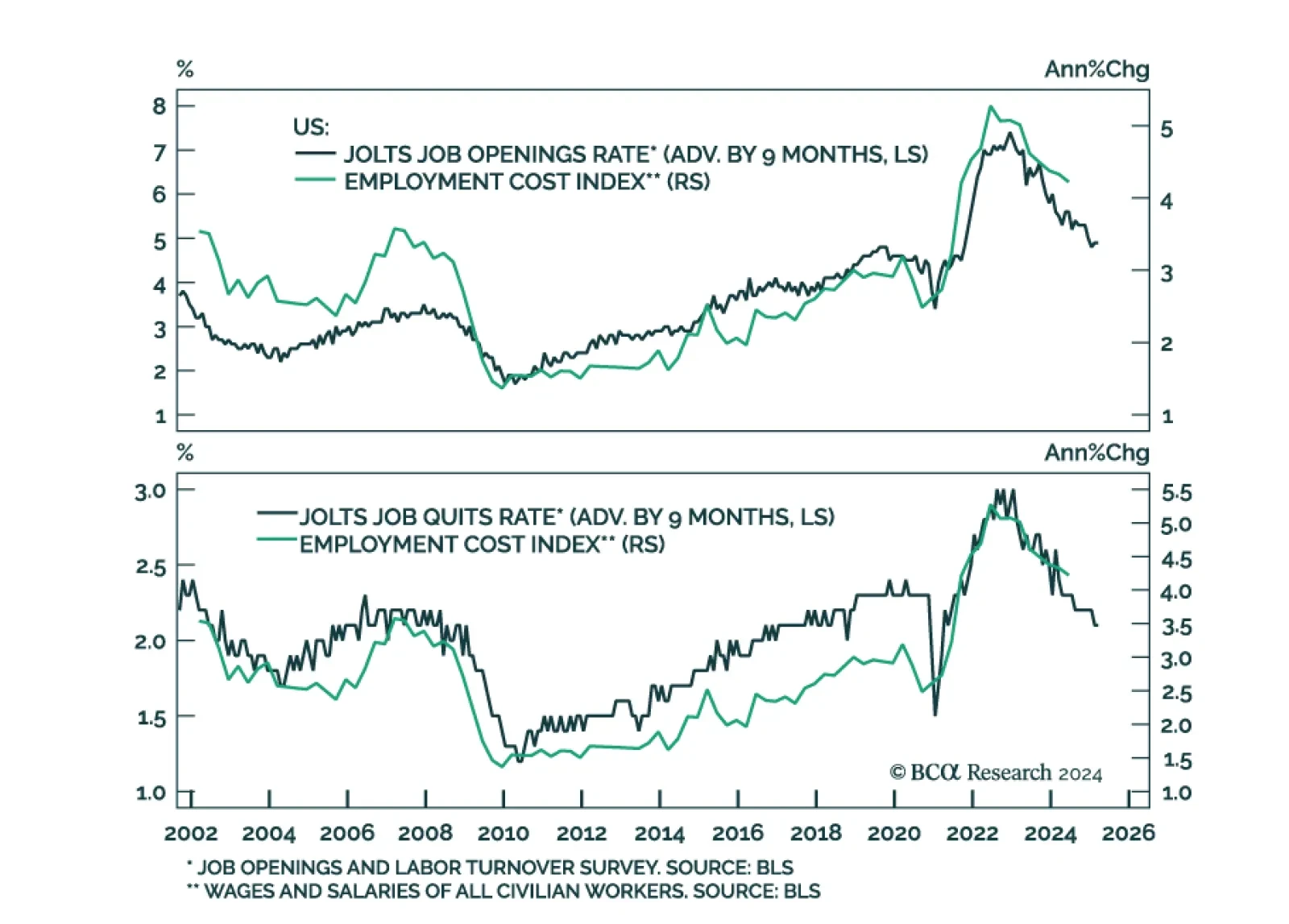

FOMC members unanimously voted in favor of keeping rates on hold in July but signaled that a September cut is on the table. Inflationary pressures have indeed continued to ease over the past several months. Notably, the Employment Cost Index (ECI) – the…