Recession-Hard/Soft Landing

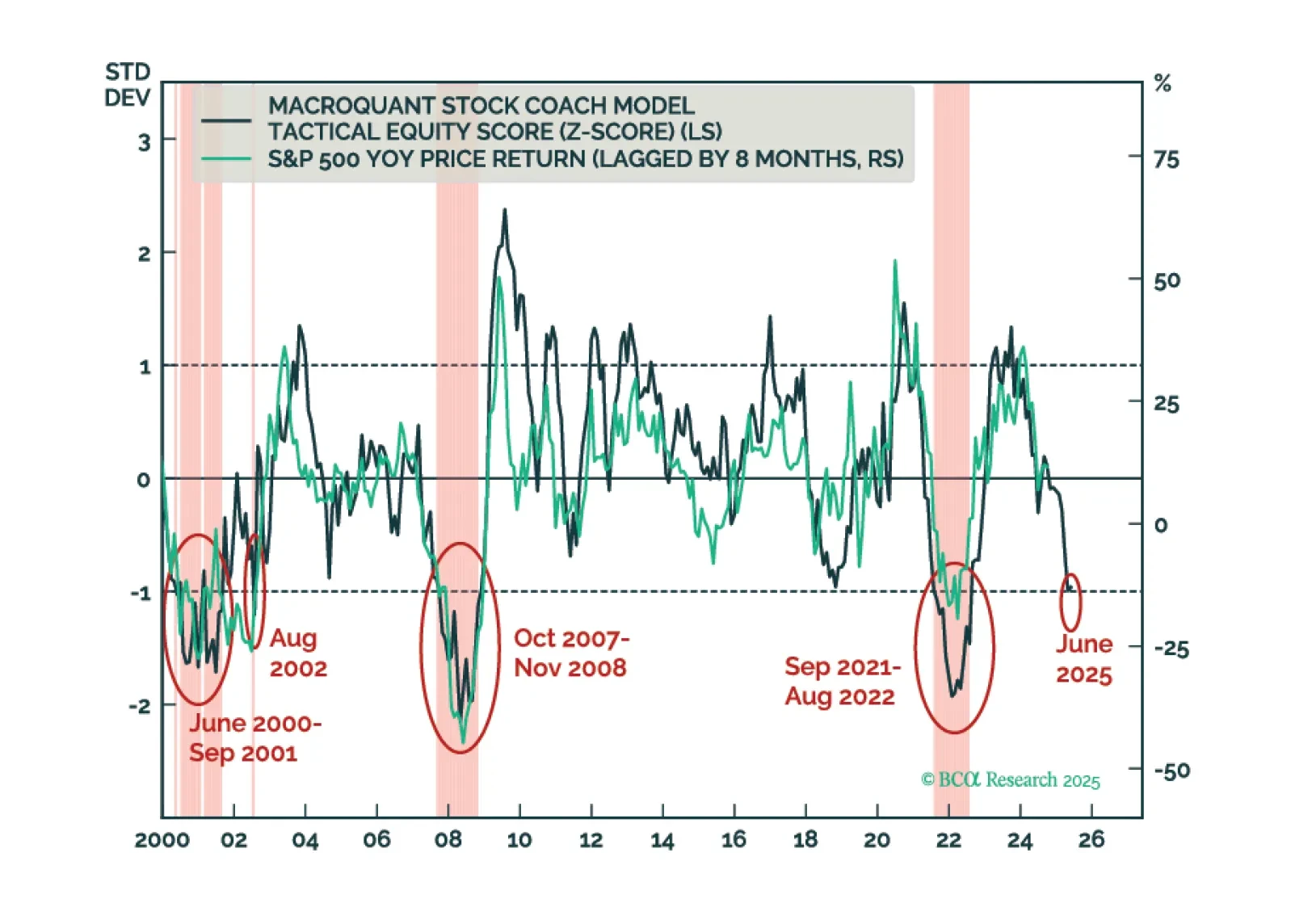

We will abandon our recession call if US economic data show clear signs of stabilization over the summer months. For now, that has not happened. Maintain a modest underweight to stocks but look to get more defensive if MacroQuant’s equity z-score falls below -1.

Our Portfolio Allocation Summary for July 2025.

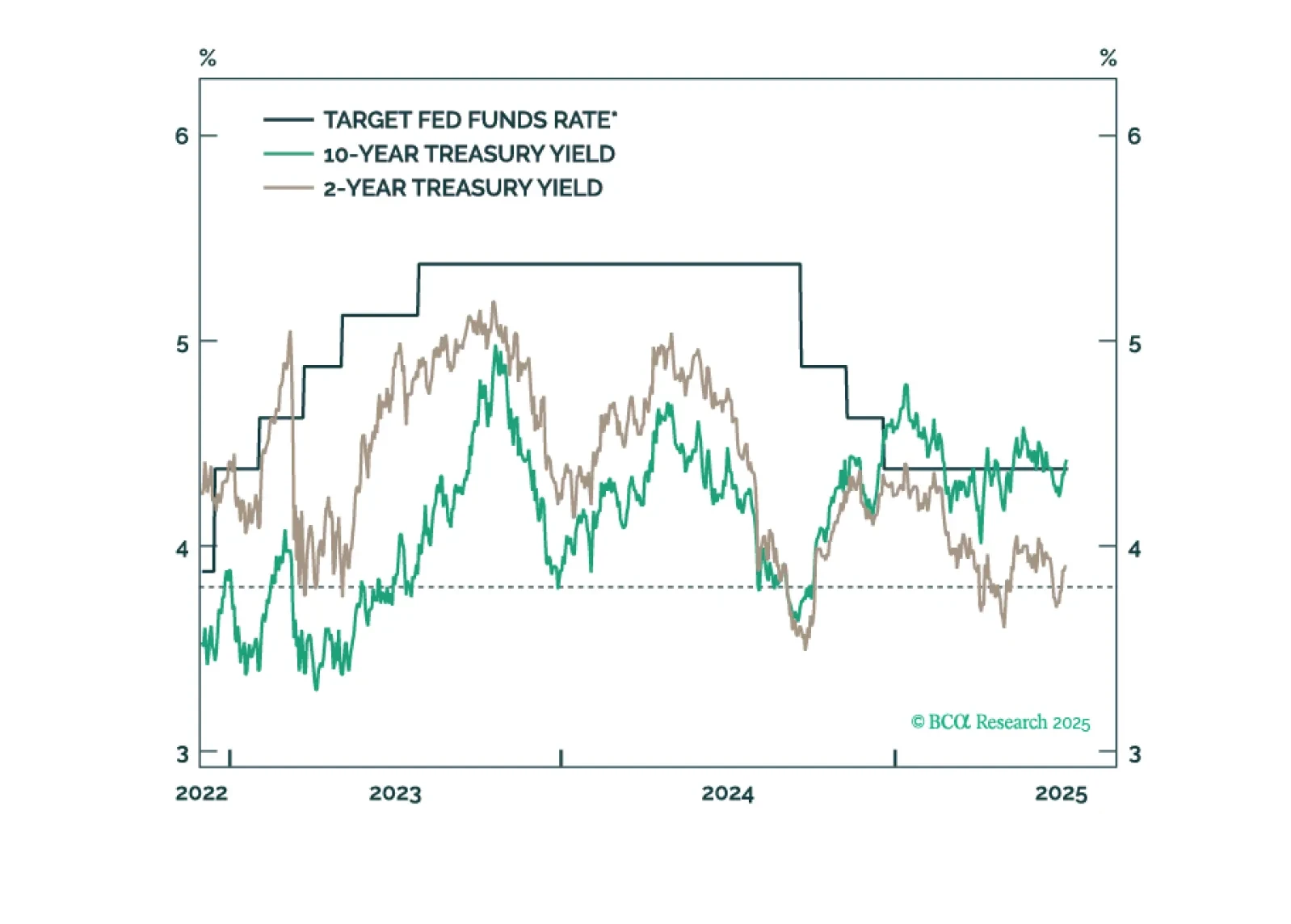

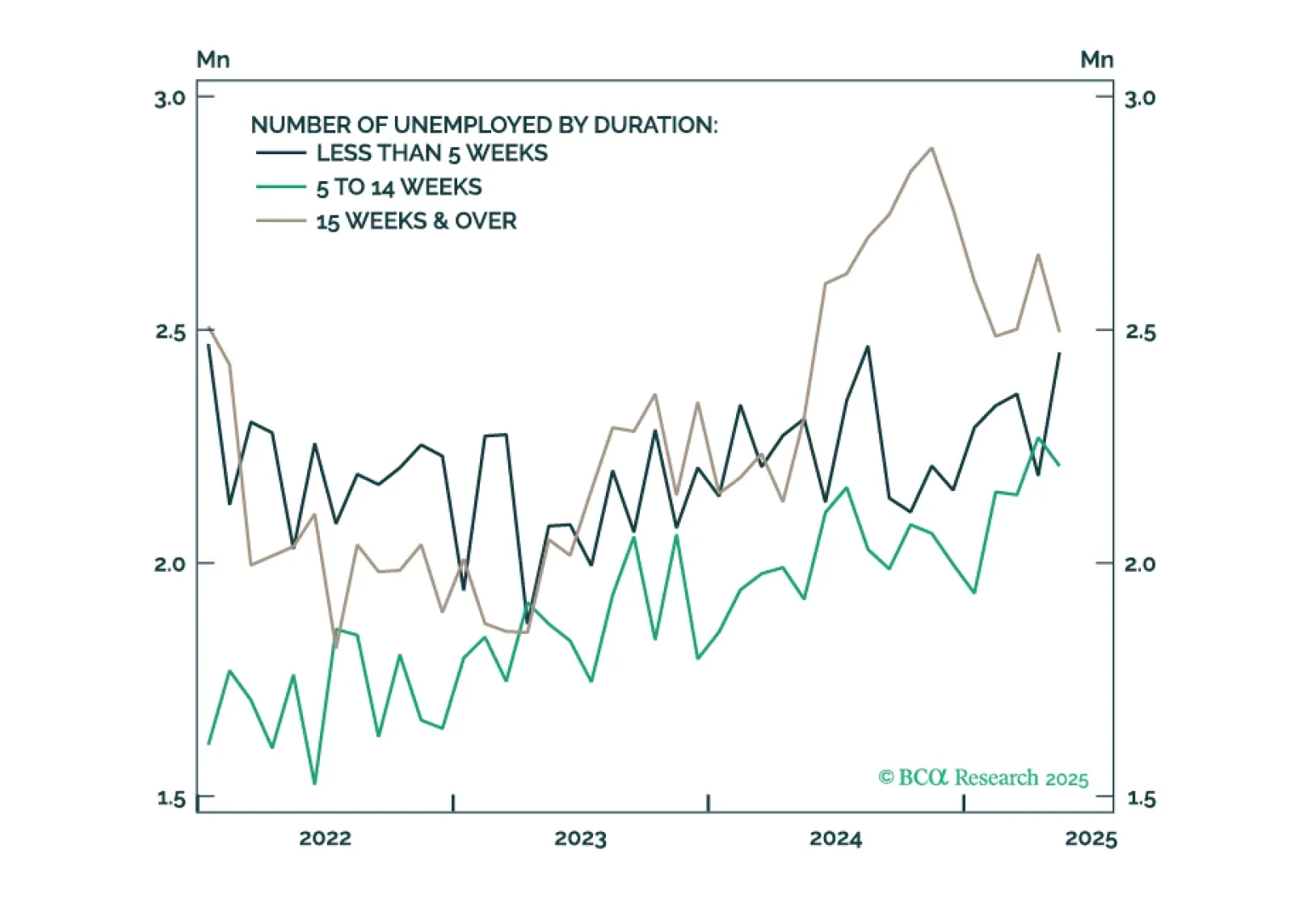

June’s employment report showed a tick down in the unemployment rate, an improvement that rules out a Fed rate cut later this month.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.

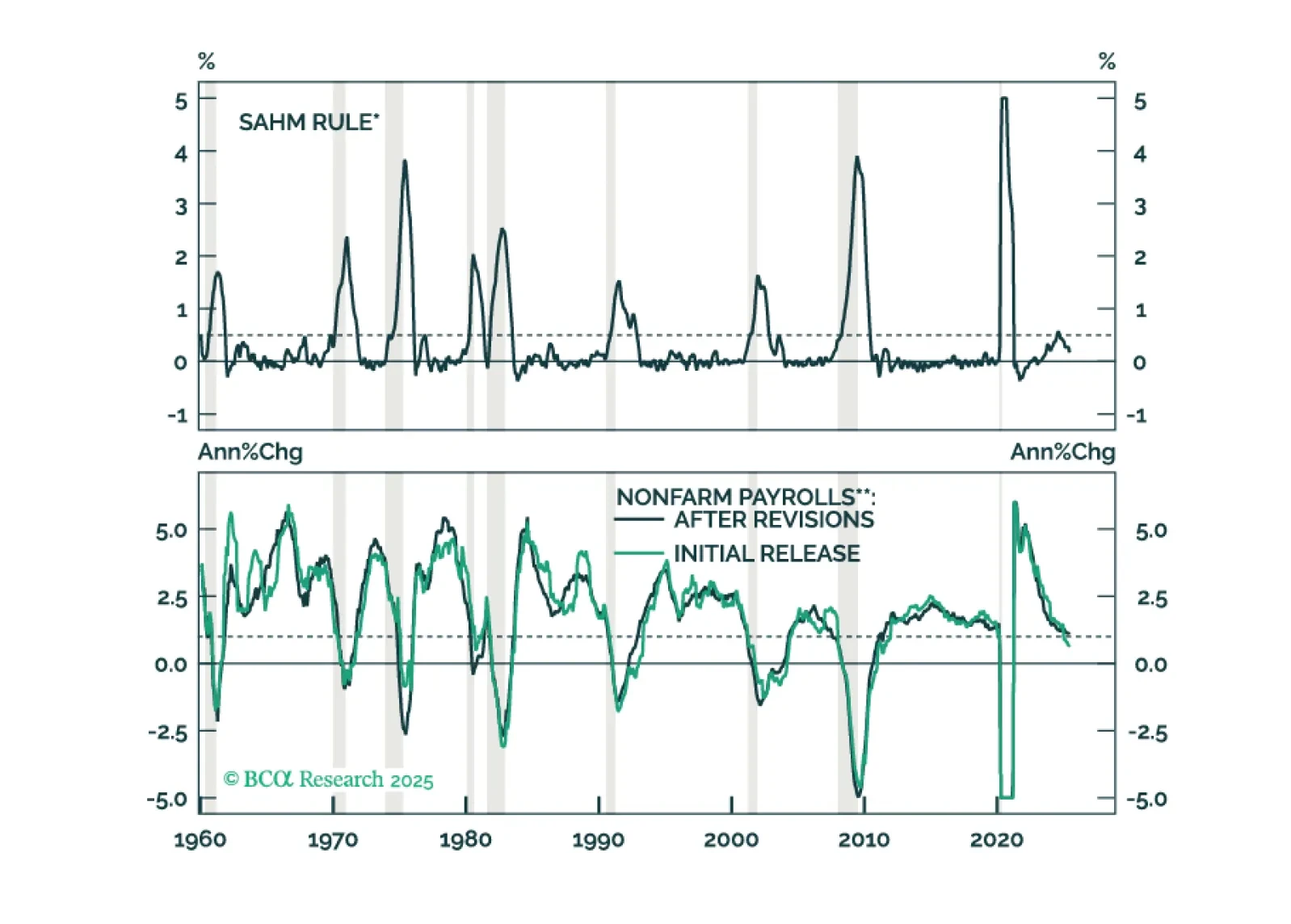

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.

Our Portfolio Allocation Summary for June 2025.

In this report, we take stock of the Q1 2025 earnings season. Corporate commentary and forward guidance provide valuable insights into the state of the economy, tariff mitigation strategies, and consumer spending.

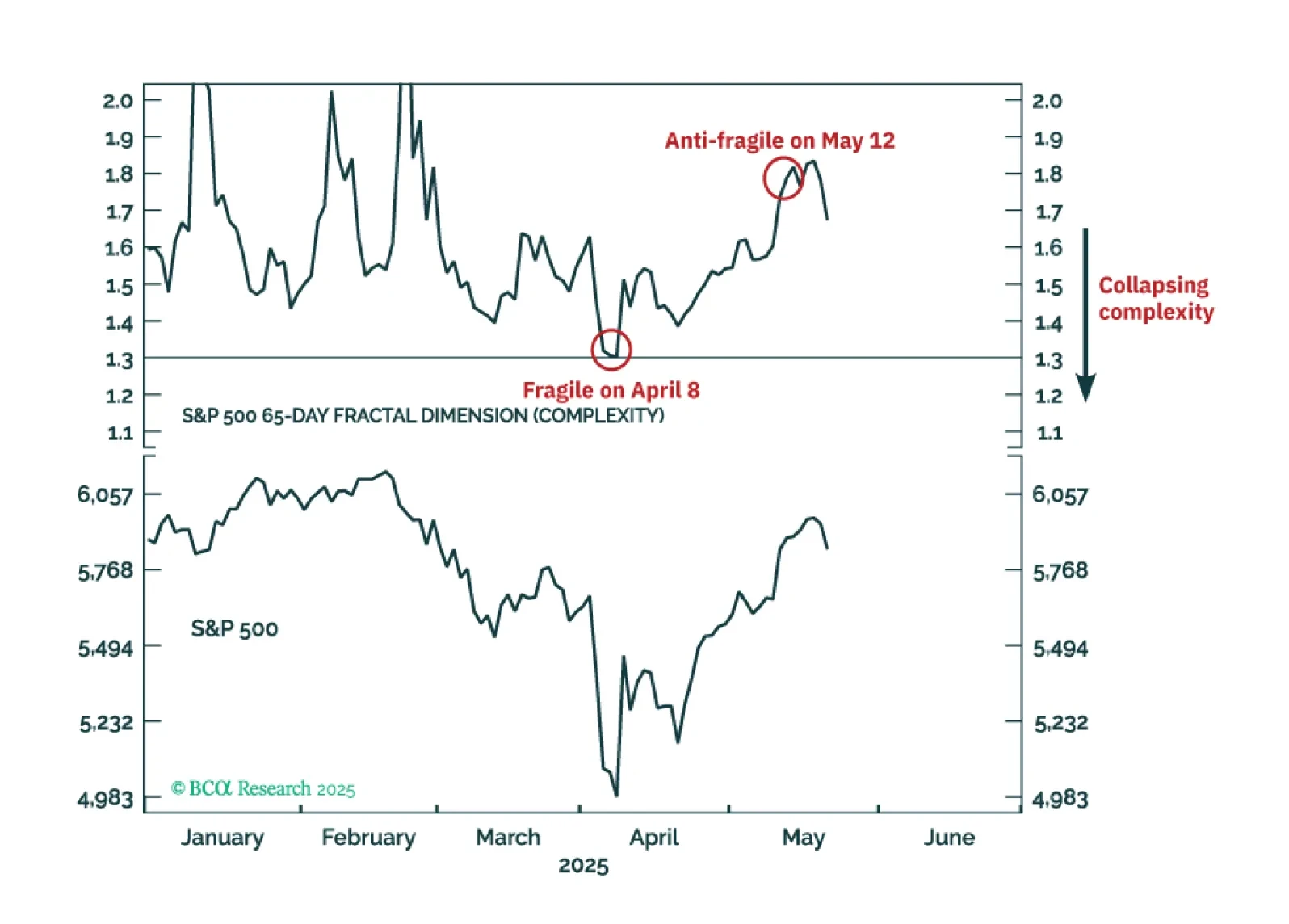

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.