Recession-Hard/Soft Landing

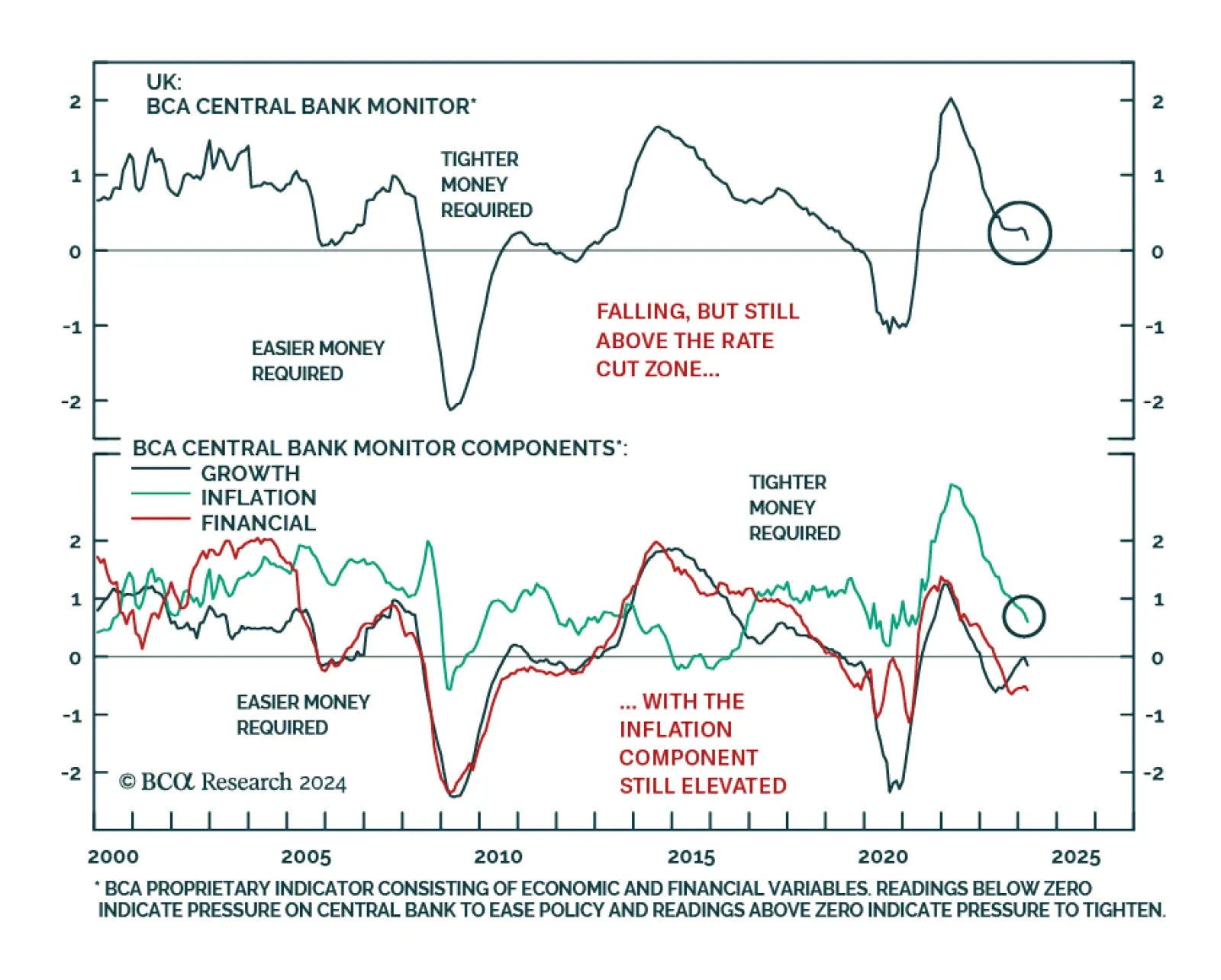

According to BCA Research’s Global Fixed Income Strategy service, a hard landing is the only way to solve the UK inflation problem. Sticky inflation and lingering inflation pressures have made the BoE’s job much more challenging. The UK economy weakened in…

The advanced estimates for US real GDP suggest that economic growth slowed meaningfully from 3.4% in Q4 2023 to 1.6% in Q1 2024 on an annualized basis, significantly below expectations of 2.5%. That said, the details of the report were less gloomy. While…

Equity markets reacted negatively to the preliminary Q1 US GDP on Thursday, with the S&P 500 shedding 0.5%. Meanwhile, the 10-year Treasury yield rose 6 bps in response to the stronger-than-expected core PCE inflation print for Q1. Importantly,…

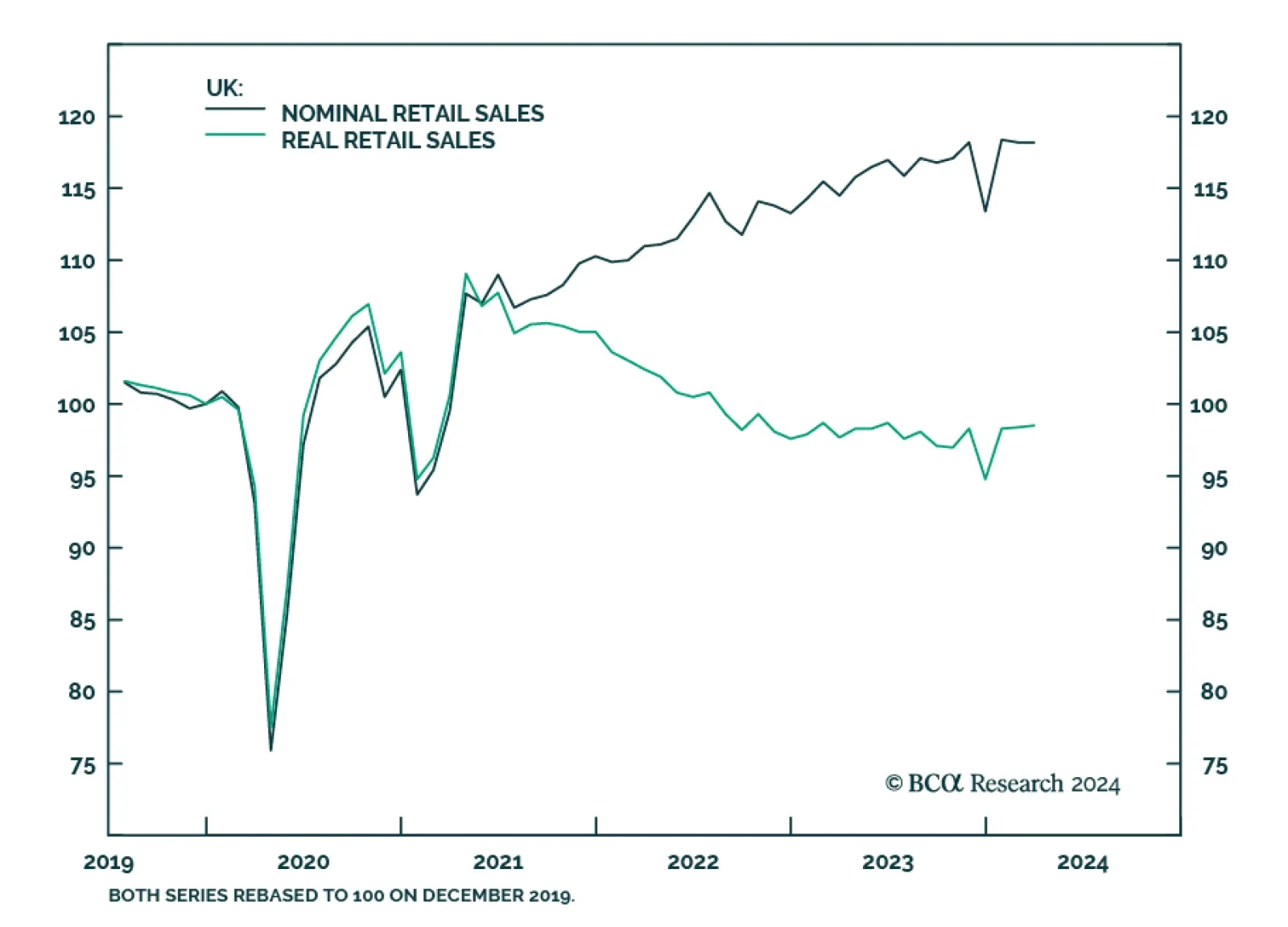

UK retail sales volumes were flat in March, a decrease from the 0.1% growth registered in February and disappointing expectations of a 0.3% m/m increase. The details were mixed, with automotive fuel and non-food stores sales volumes…

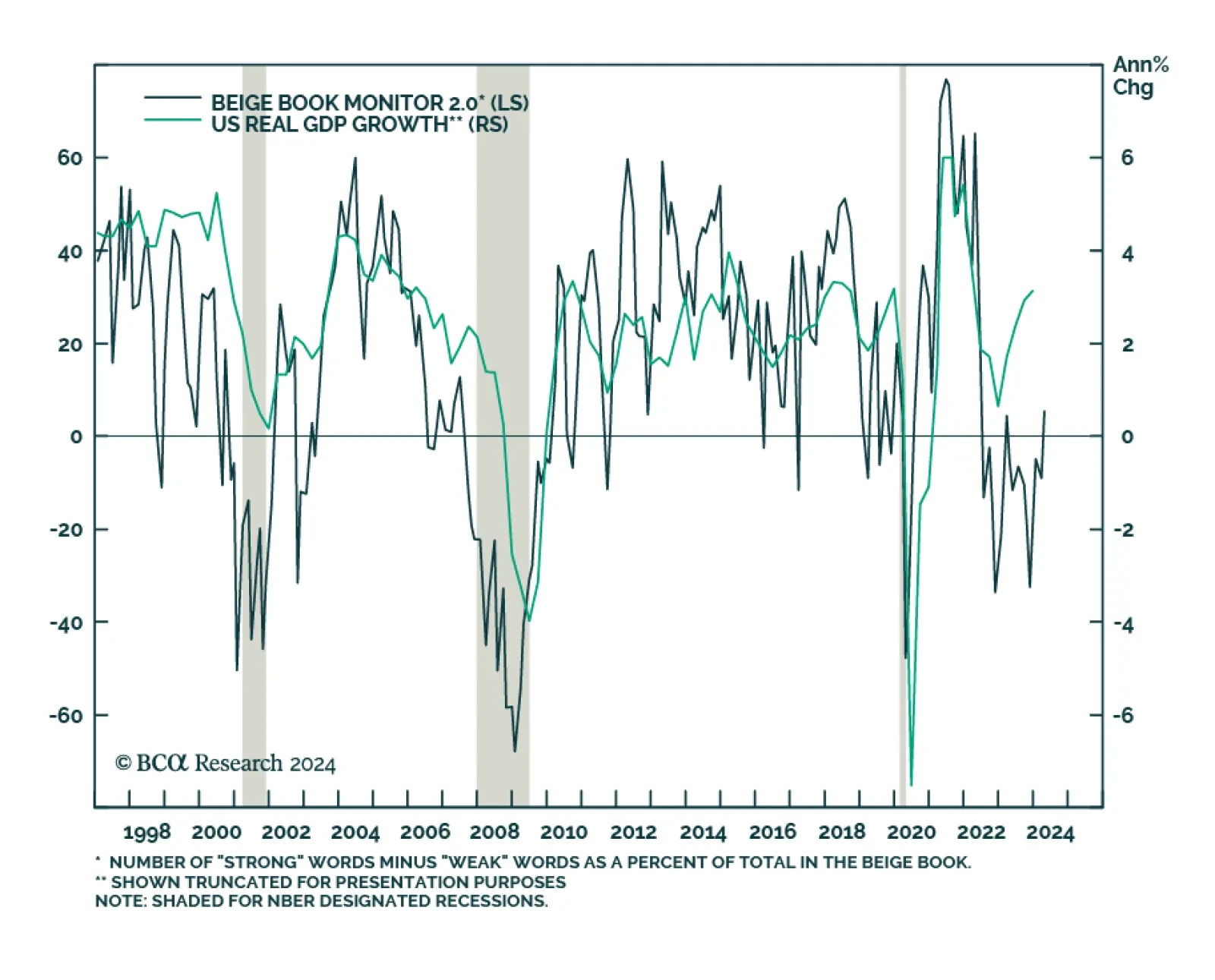

BCA’s US Beige Book Monitor – an indicator we use to gauge changes in the language of the Fed’s Beige Book report and which historically tracks US GDP growth – has improved in April. Nevertheless — and despite March's hot retail sales and February's…

This year’s rise in commodity prices represents a blow-off rally rather than the start of a durable bull market. The global economy is heading for a recession. Stocks, commodities, and other risk assets are vulnerable.

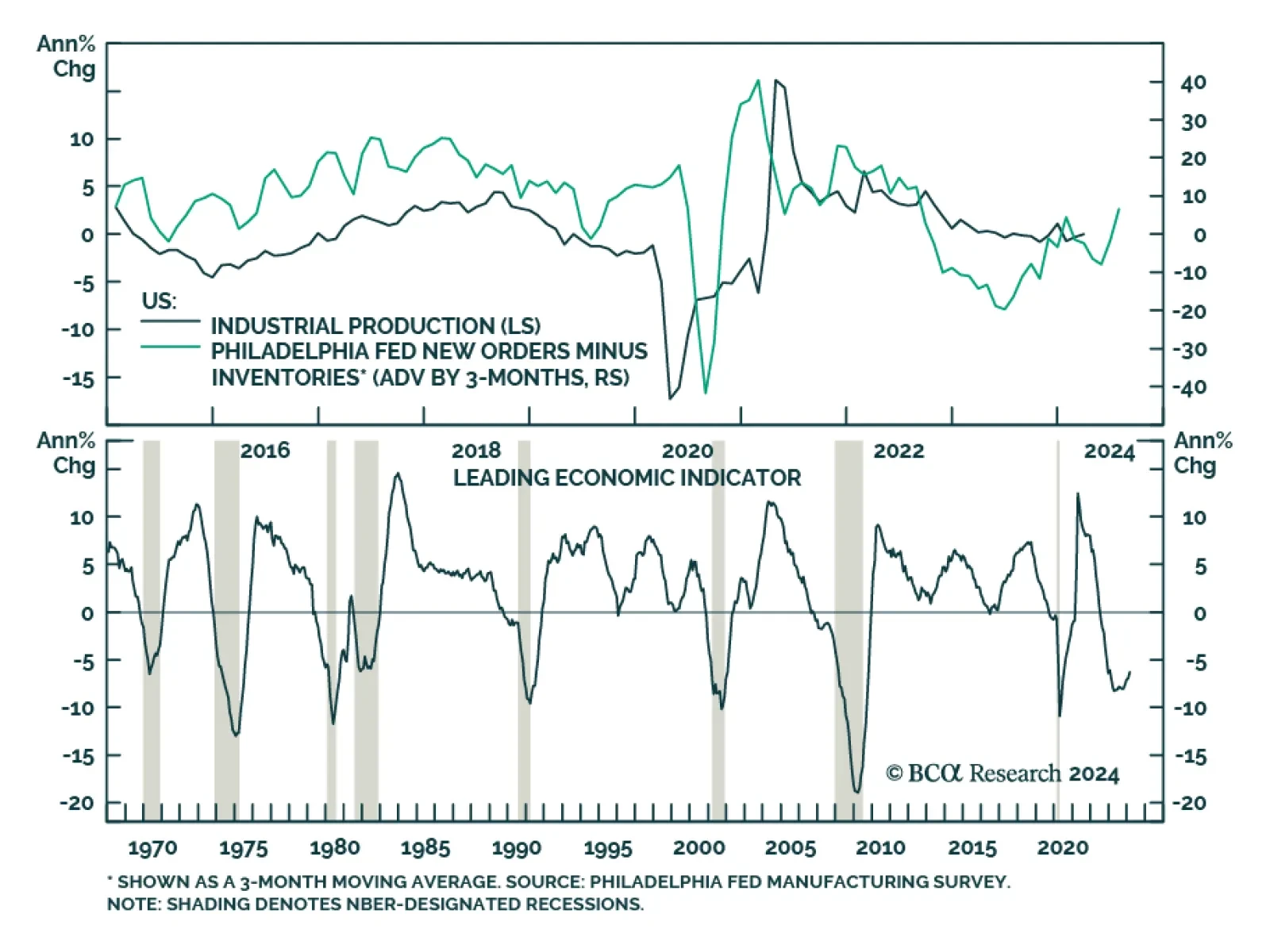

The headline Philadelphia Fed manufacturing survey for April delivered a positive surprise on Thursday, increasing from 3.2 to a twelve-month high of 15.5 and beating expectations it would soften to 2.0. Measures of demand improved with new orders and…

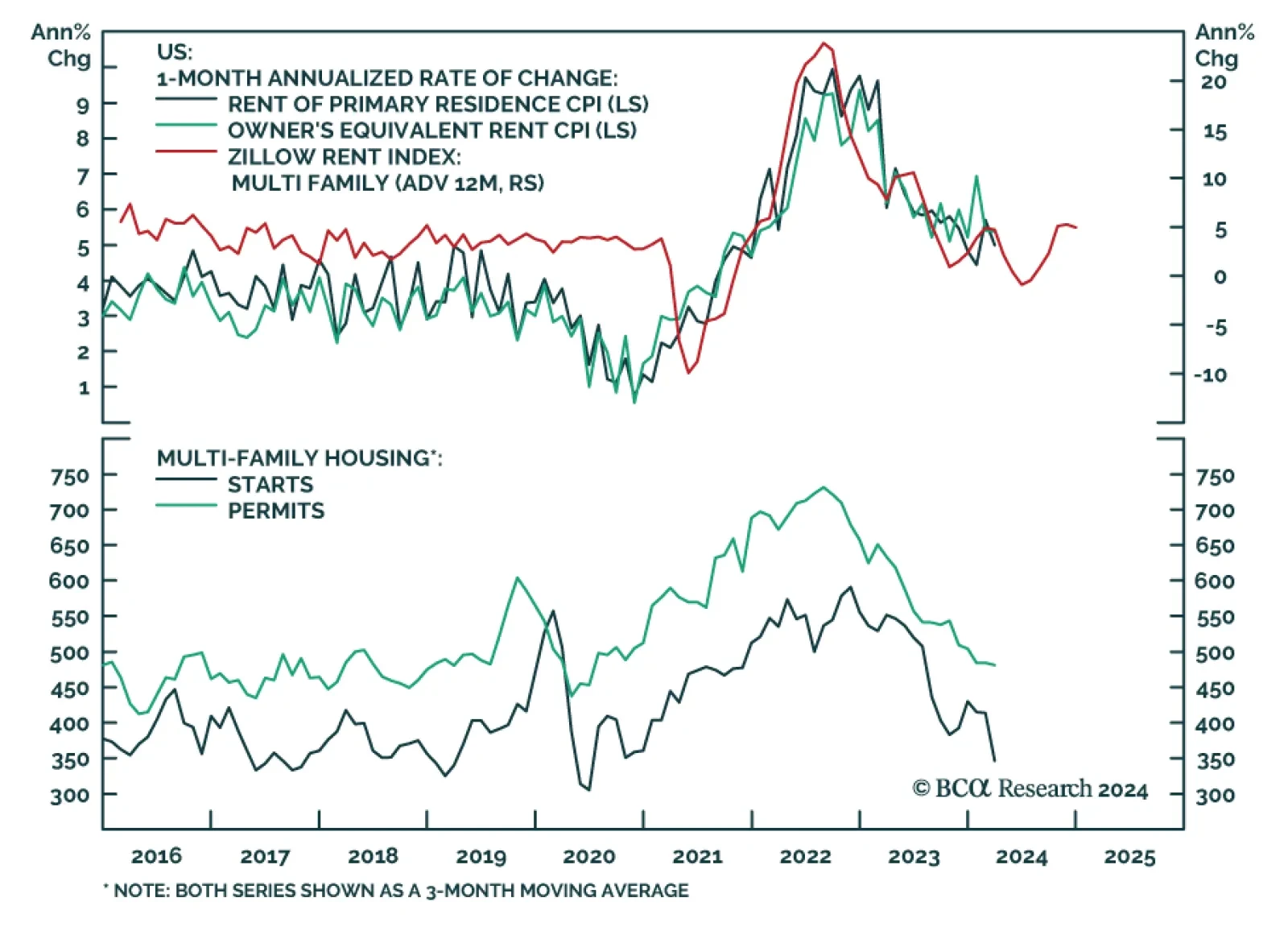

Developments in US multi-family housing are particularly relevant for the inflation outlook since they inform the future direction of shelter inflation – an important component of CPI inflation. Indeed, the Zillow multi-family rent index leads moves in the…

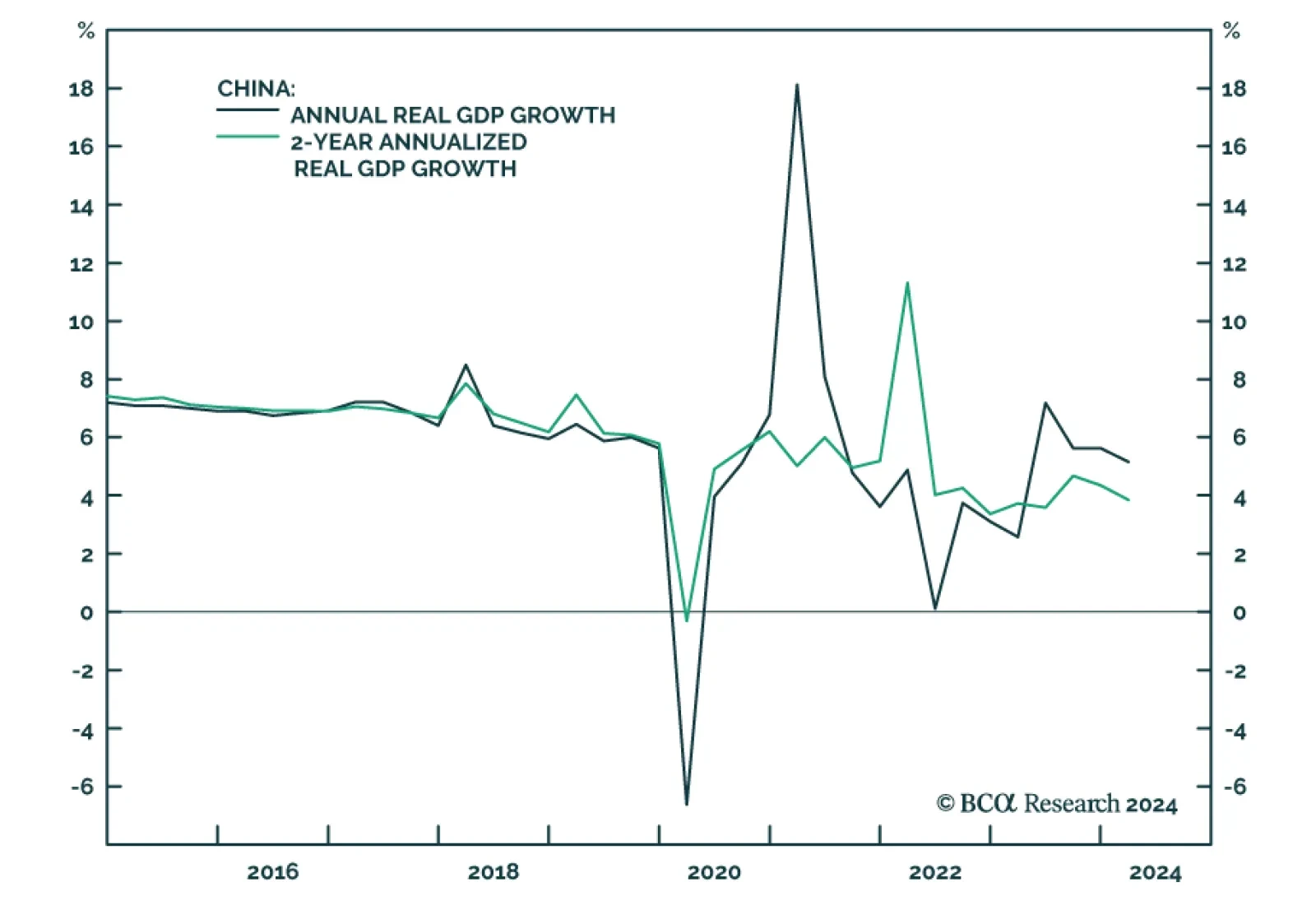

Chinese economic data releases painted a mixed picture of domestic conditions on Tuesday. Chinese real GDP growth accelerated from 5.2% y/y to 5.3% y/y in Q1 2024, beating expectations of 4.8% and suggesting that economic momentum improved at the start of…

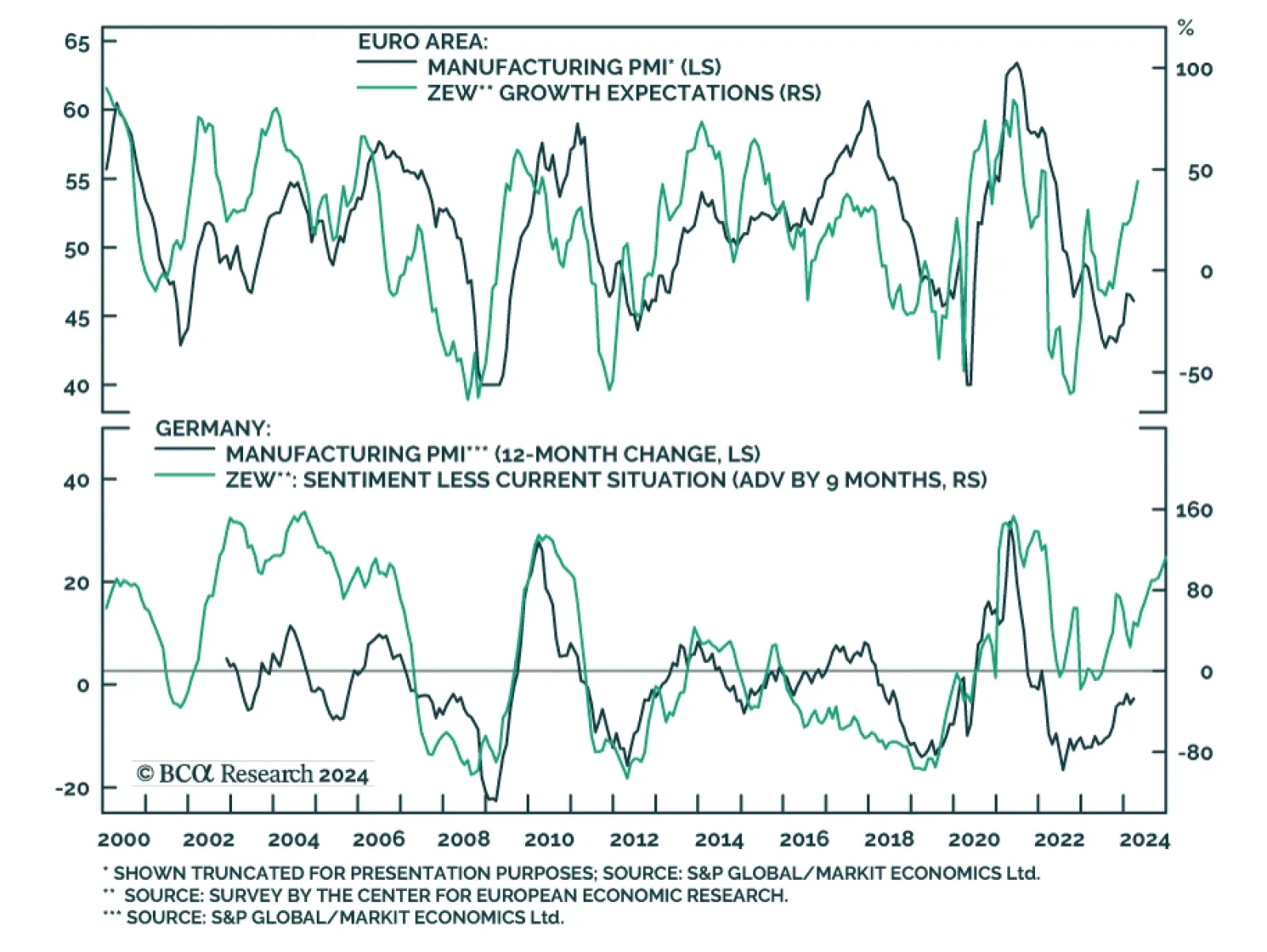

Optimism about the future continues to boost investor confidence in the Euro Area. The ZEW Expectations series for the Eurozone (+10.4 to 43.9) and Germany (+11.2 to 42.9) surged and are now both at their highest in 26 months. Although investors’…