Recession-Hard/Soft Landing

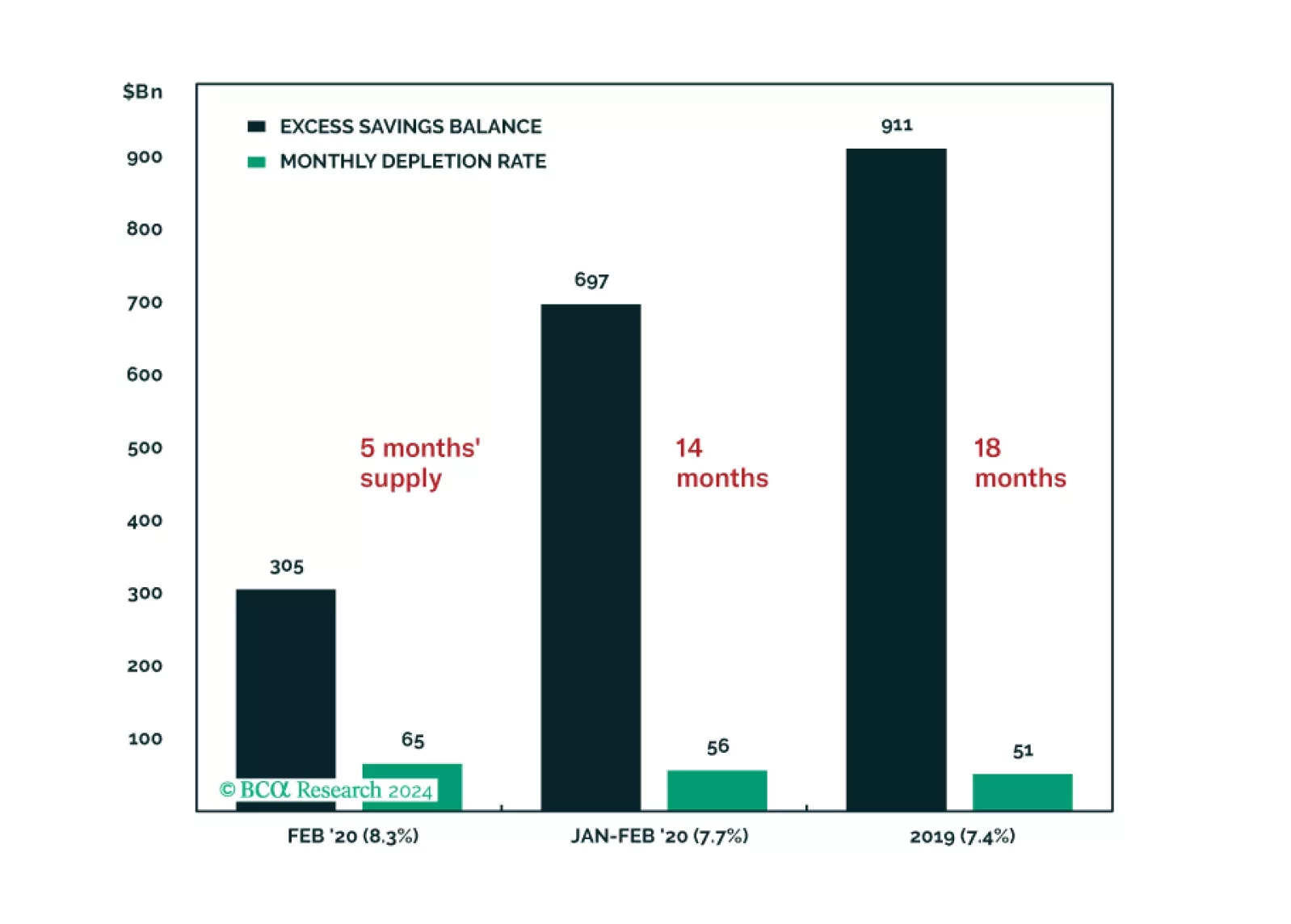

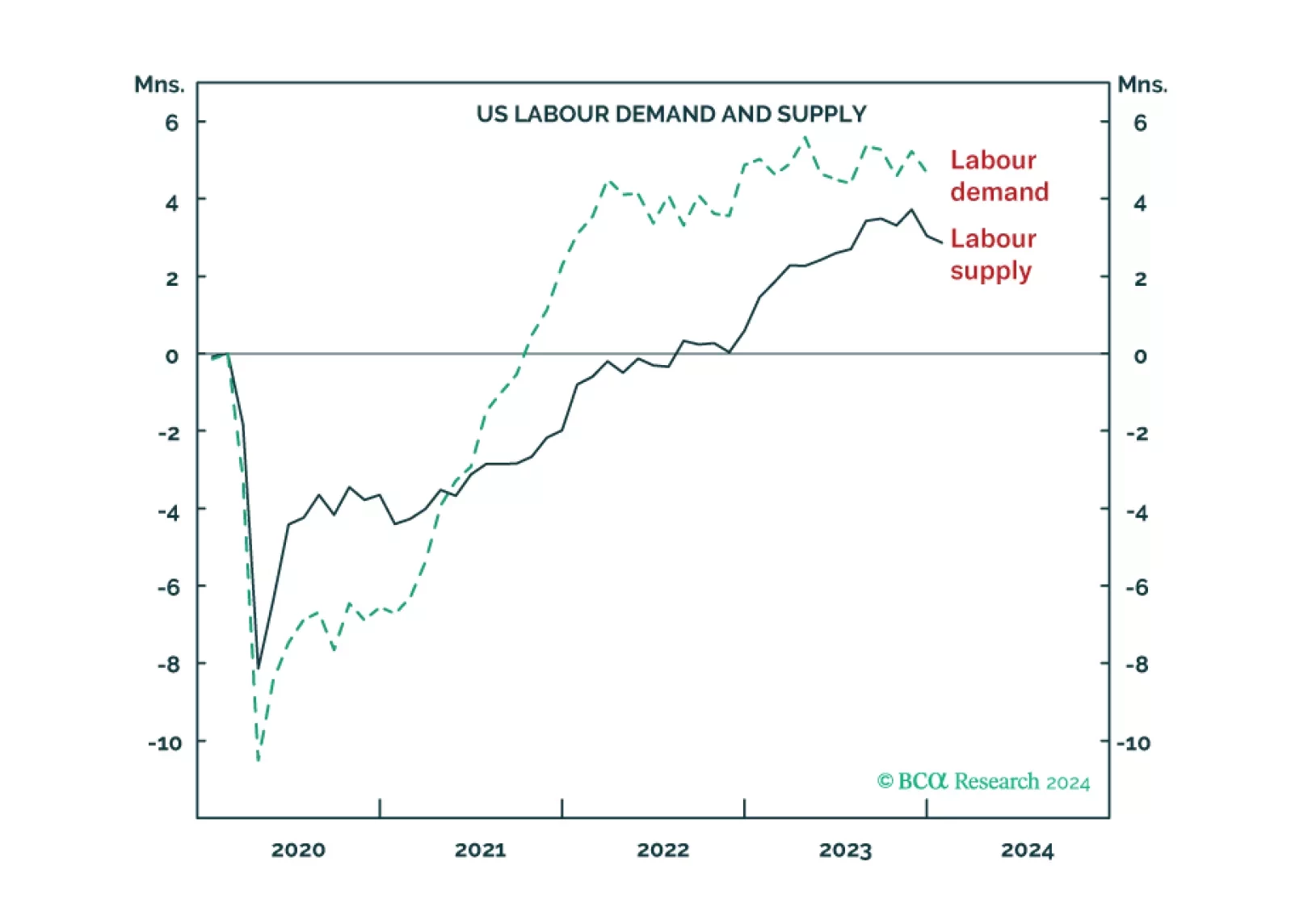

We feel as good about spurning the soft-landing narrative today as we did about spurning the recession narrative a year ago, but we are not giving into complacency. This week’s report looks at two key ways that we may be getting it wrong: by underestimating households’ asset support and the labor market’s durability. We remain tactically neutral but continue to look for opportunities to turn defensive.

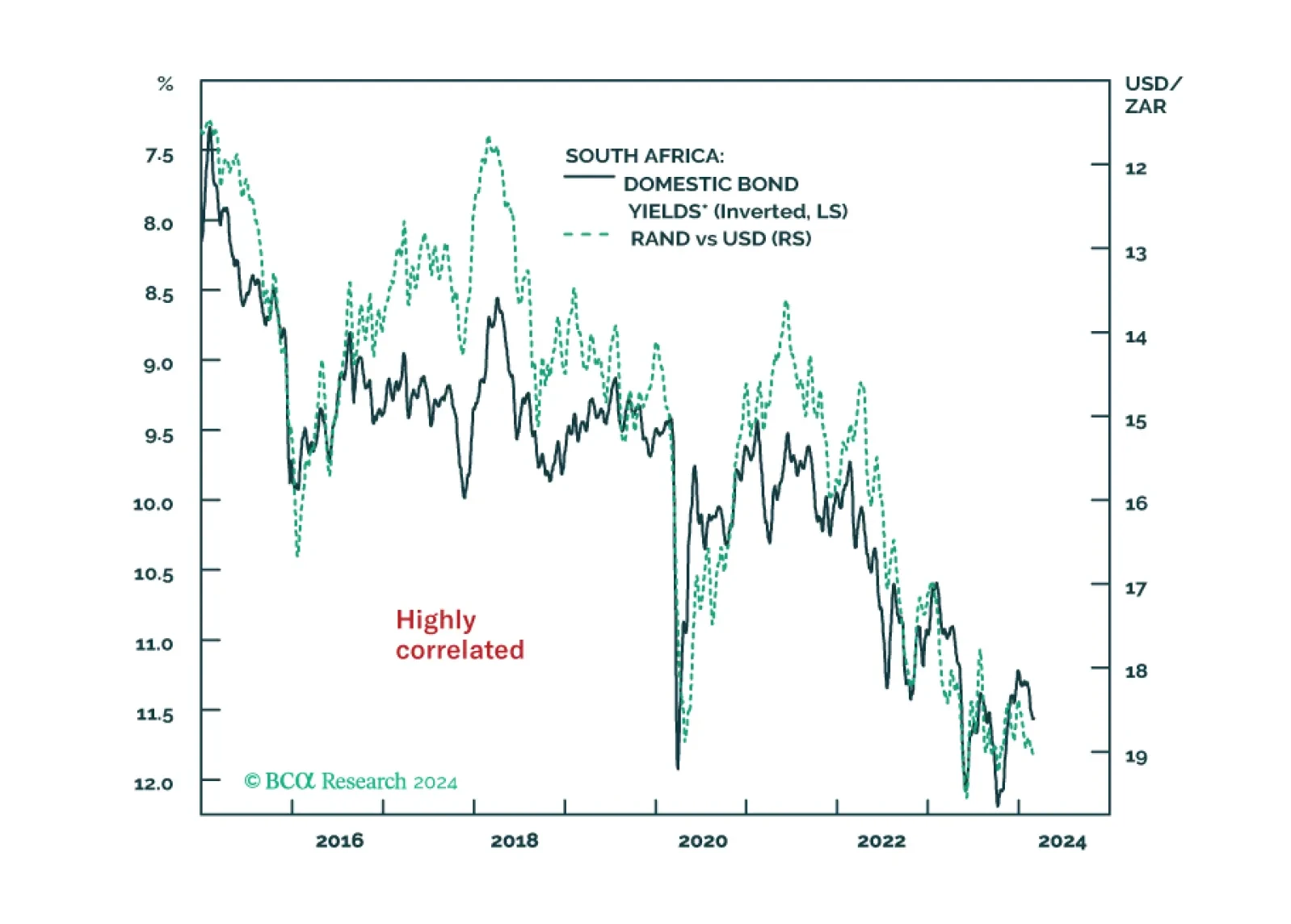

Despite the economy being on the verge of a recession, the South African Reserve Bank will not ease policy meaningfully. Doing so will accentuate the currency depreciation, which, in turn, will push up bond yields – an outcome the central bank would like to prevent.

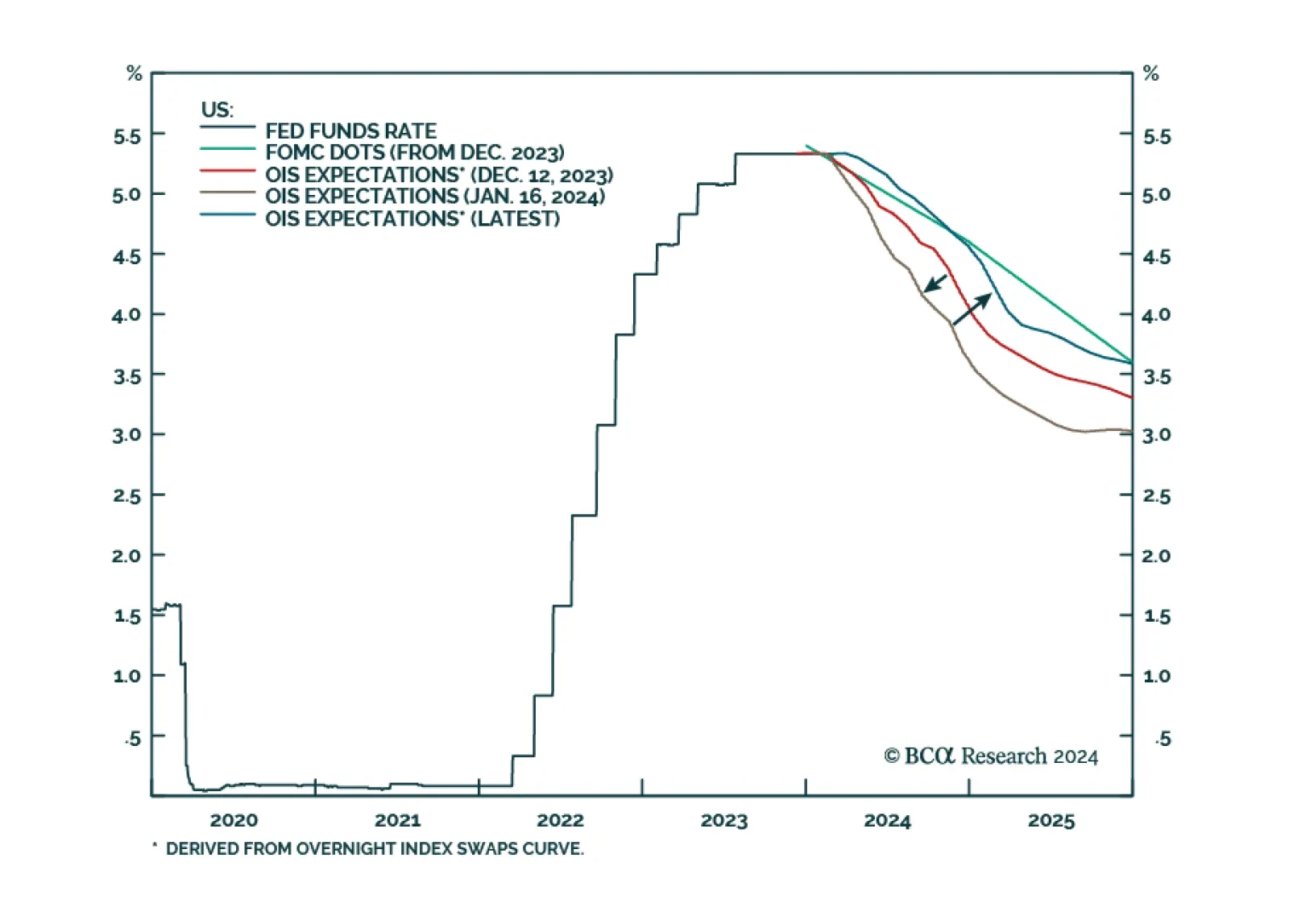

The US ‘immaculate disinflation’ has run its course, given that labour force participation is topping out. This leaves the Fed with a dilemma. Settle for price inflation stabilising at 3 percent, and cut rates early to avoid higher unemployment. Or, not cut rates early and go the final mile to 2 percent price inflation, at the risk of higher unemployment. We discuss which way the Fed is likely to tilt, and the investment implications. Plus: China is oversold while Japan is overbought.