Recession-Hard/Soft Landing

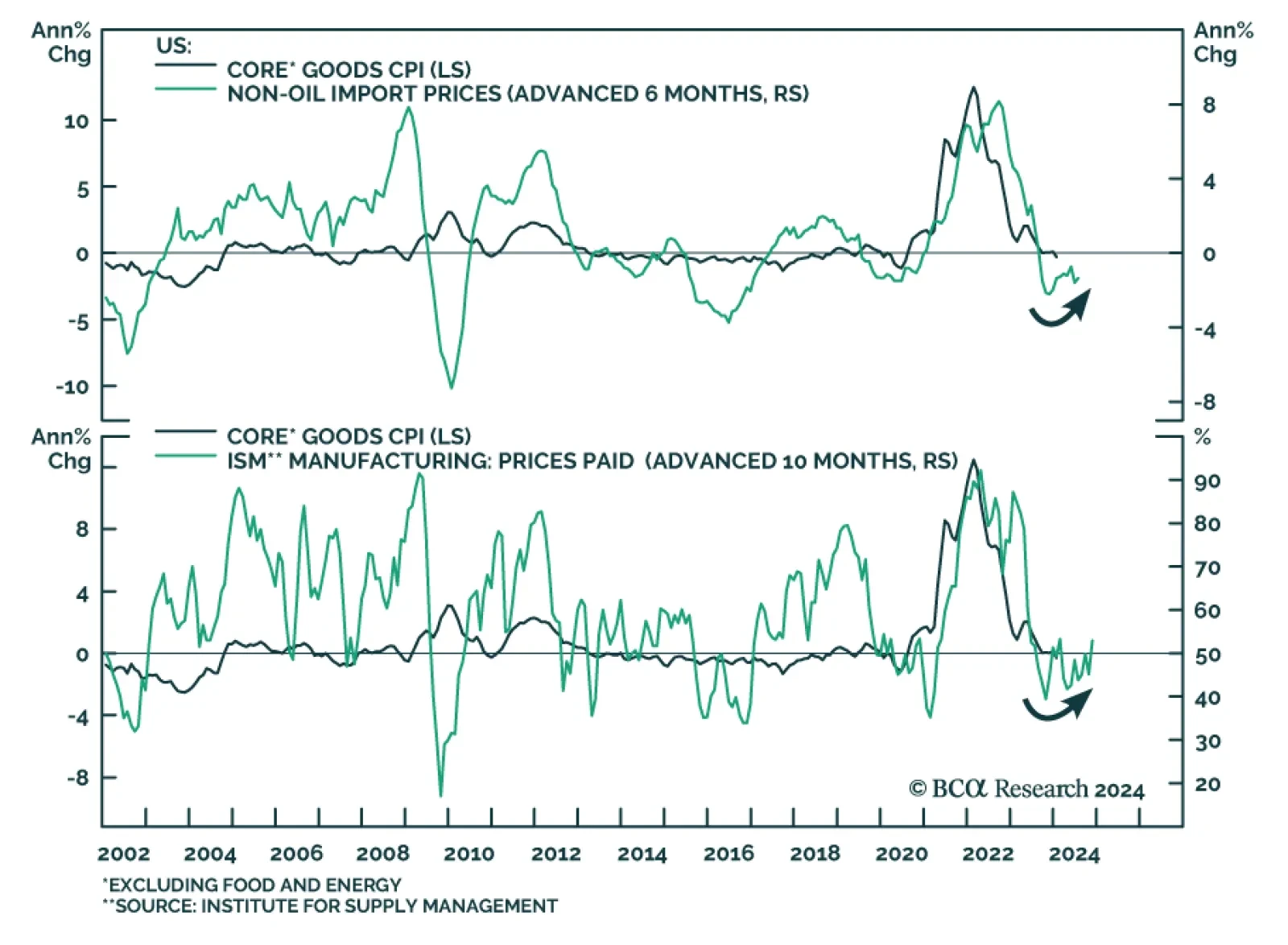

Much of the focus of investors concerned about lingering price pressures has been on services prices. There is good reason for that. Even though core CPI inflation remains relatively elevated at 3.9% y/y in January, core goods prices fell by 0.3% y/y and are…

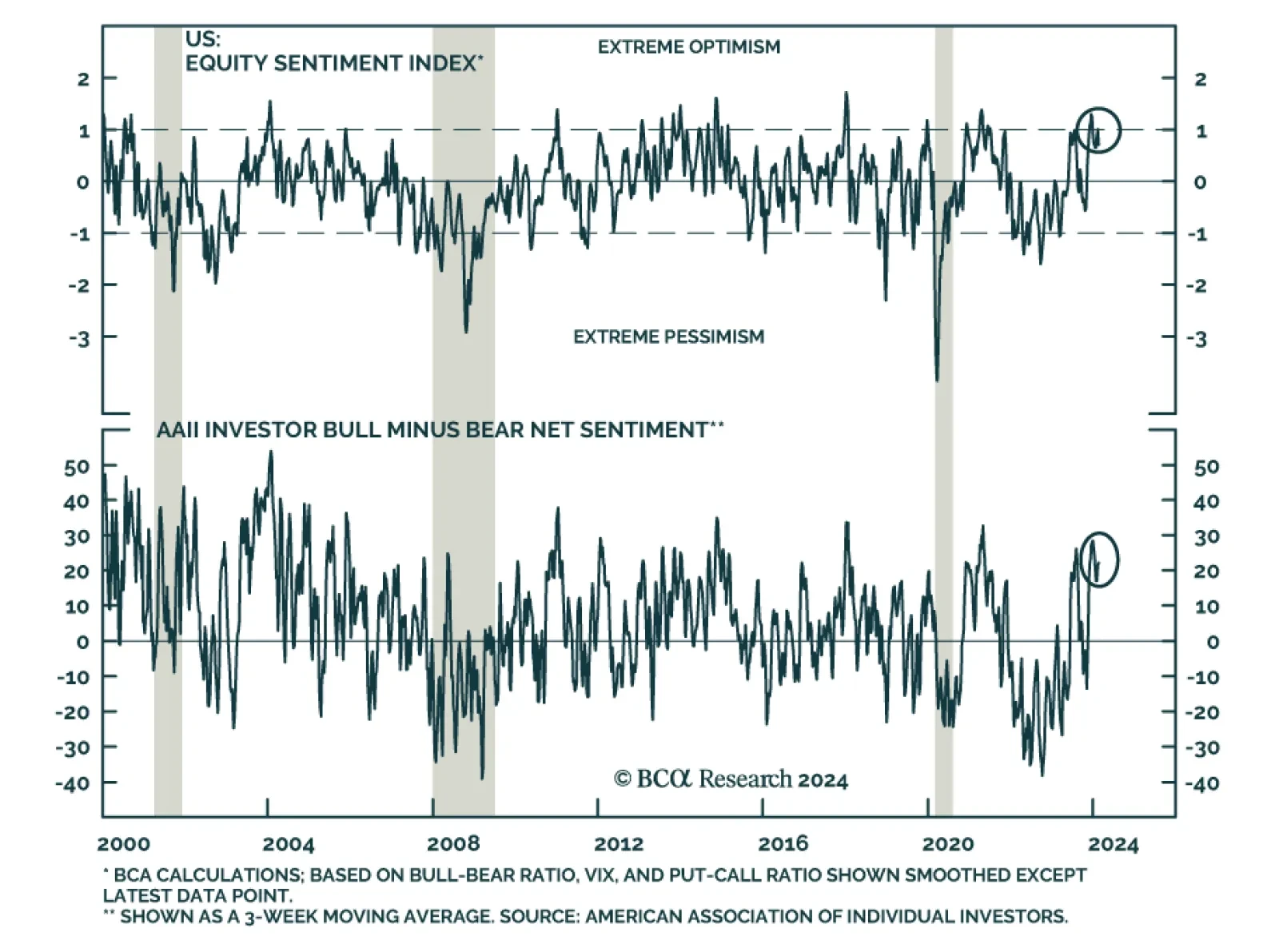

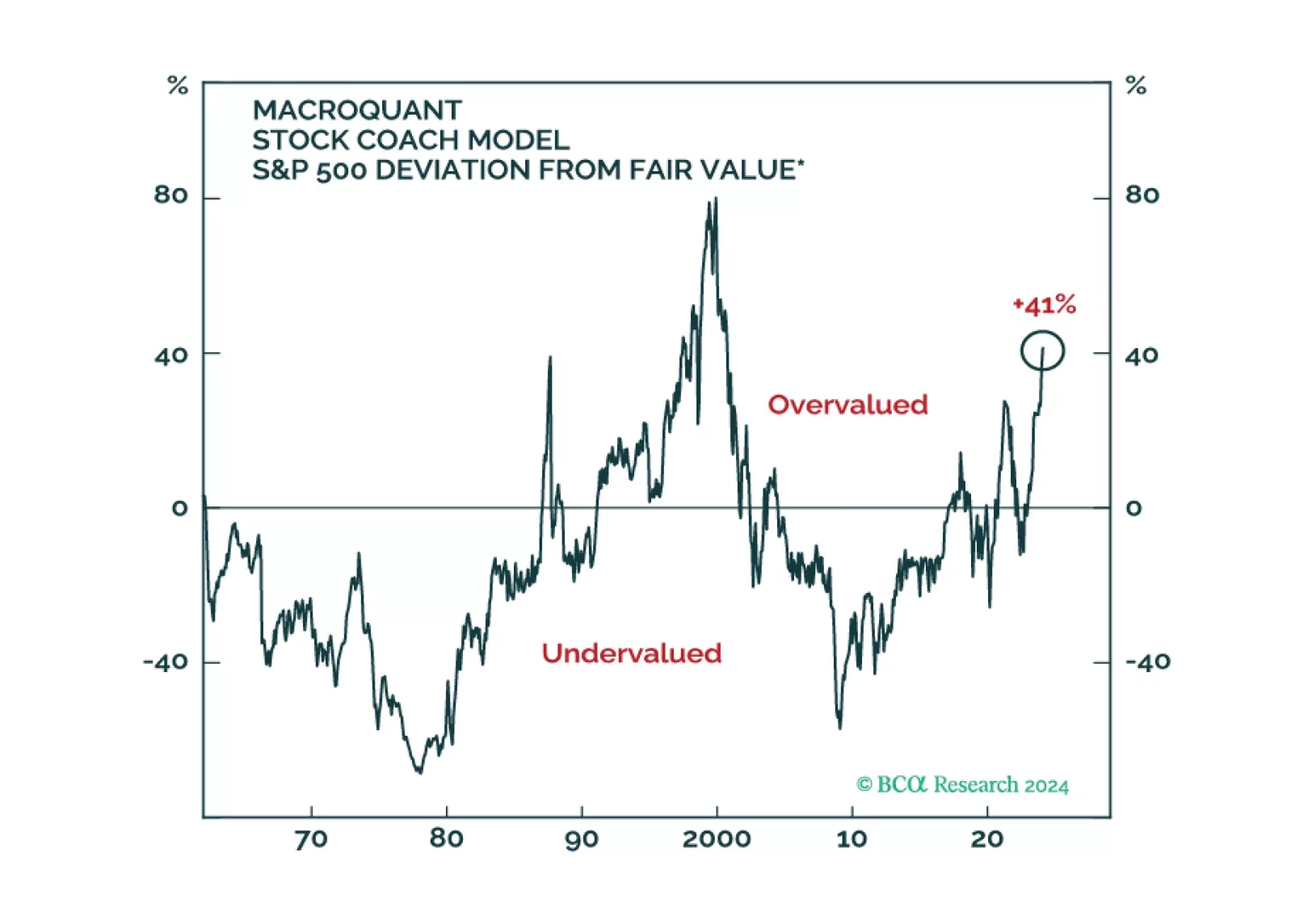

The S&P 500 forged a new all-time high last Thursday and ended the week with a 4.9% year-to-date gain, extending the rally that started in late-October. Interestingly, the recent increase comes even though investors have priced out a Fed rate cut in March…

Households have ramped up their cash holdings since the end of 2019, but the absence of an empirical link between cash and consumption leads us to believe that we’ve modestly overestimated the risk of consumer-driven overheating.

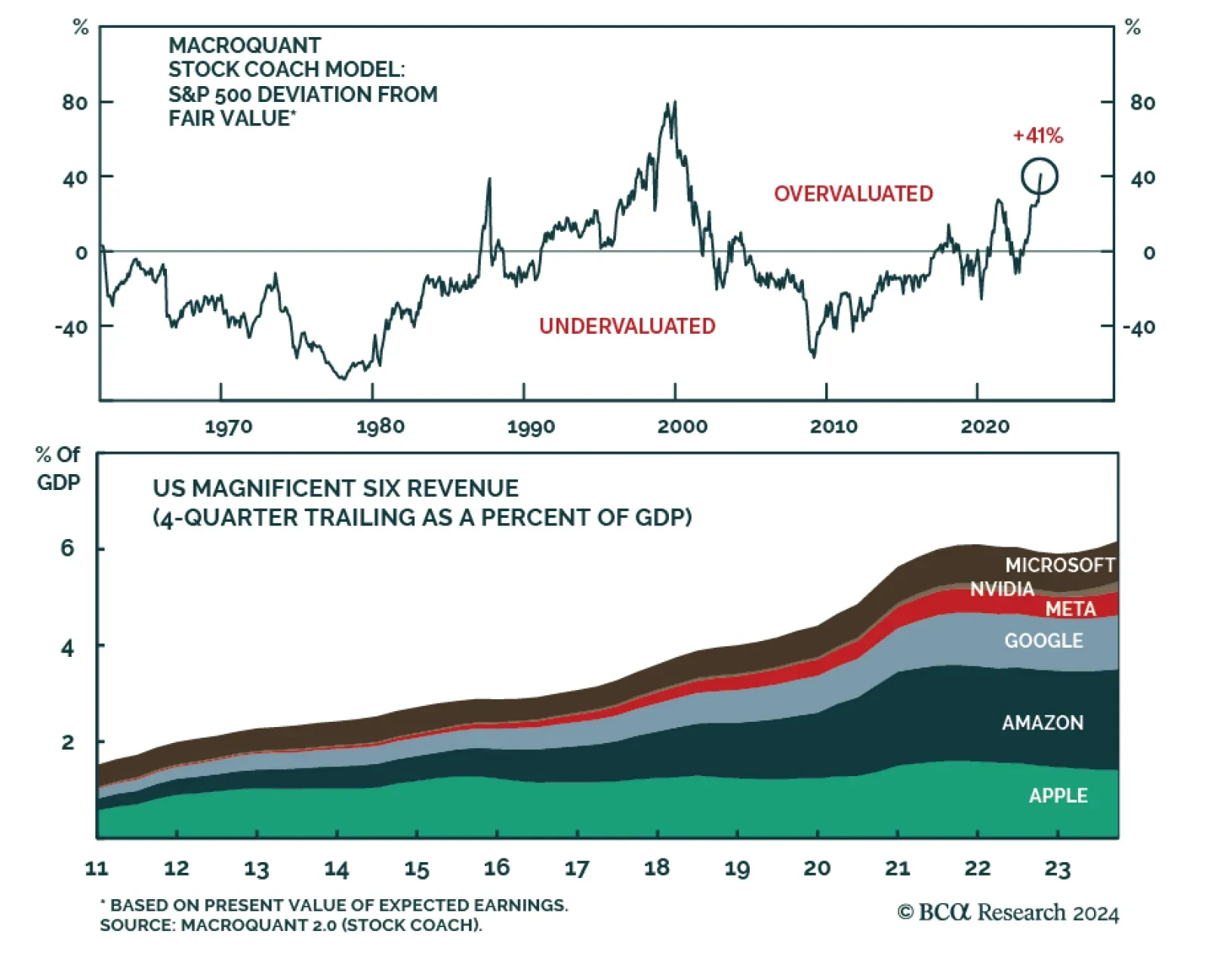

According to BCA Research’s Global Investment Strategy service, although the next recession is likely to be mild-to-moderate, the ensuing financial avalanche will be more severe. Valuations are highly stretched and hopes that today’s tech leaders will…

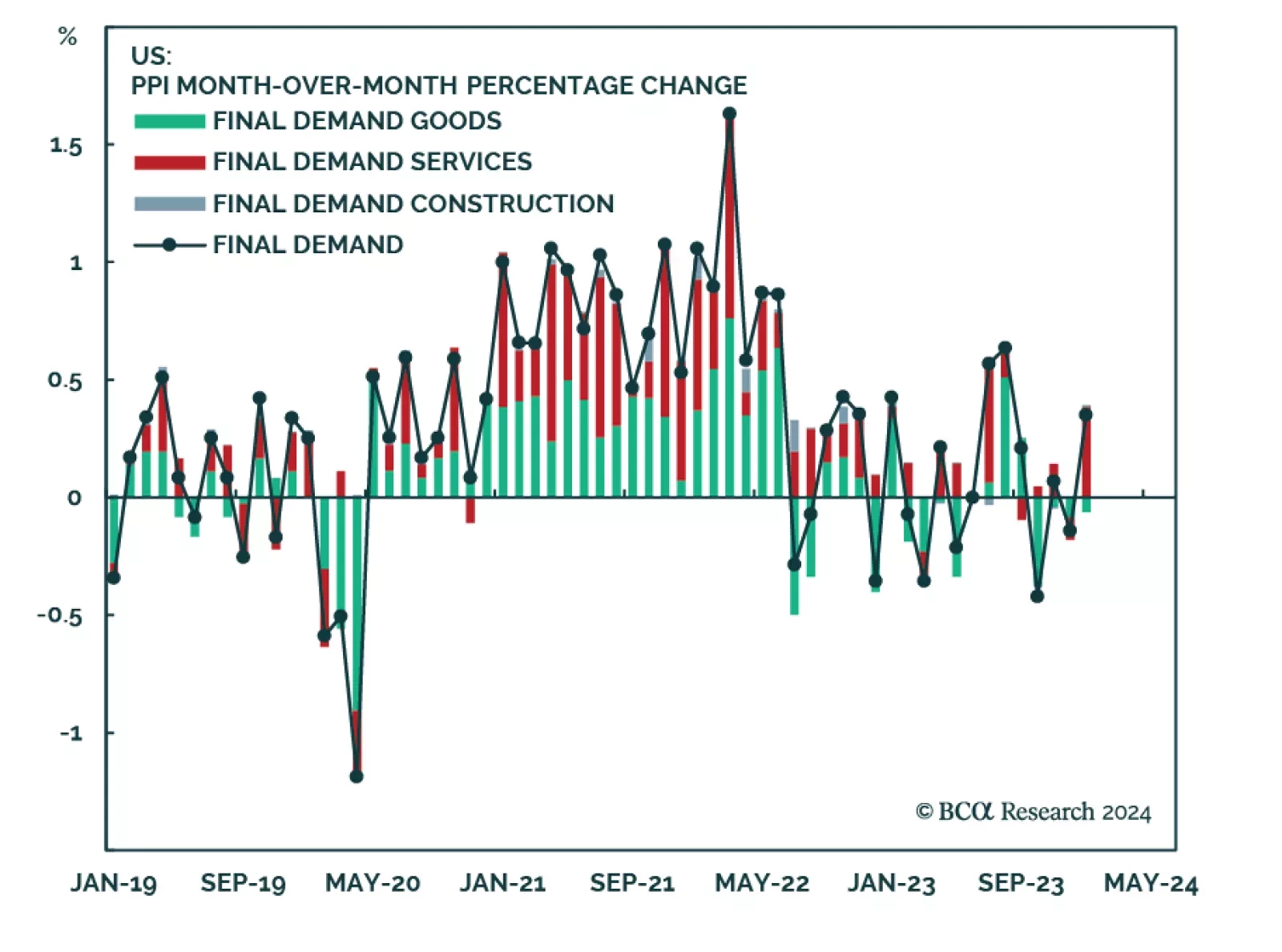

The hotter-than-anticipated US PPI report for January prompted a selloff in Treasuries on Friday. The monthly and annual changes in both the headline as well as the core measures of final demand PPI came in above expectations. Core PPI’s 0.5% m/m increase…

Recessions often begin seemingly out of the blue when the economy’s temperature falls enough to set in motion adverse feedback loops that cause unemployment to rise. We expect the US economy to suddenly freeze over towards the end of this year or in early 2025. For now, a benchmark allocation to equities is appropriate, but a more defensive stance will be necessary later this year.

According to BCA Research’s Emerging Markets Strategy service, the diminishing pace of disinflation in the US could pose a threat to US share prices in the near term. In the medium term, the key risk to US share prices is shrinking corporate profits. …

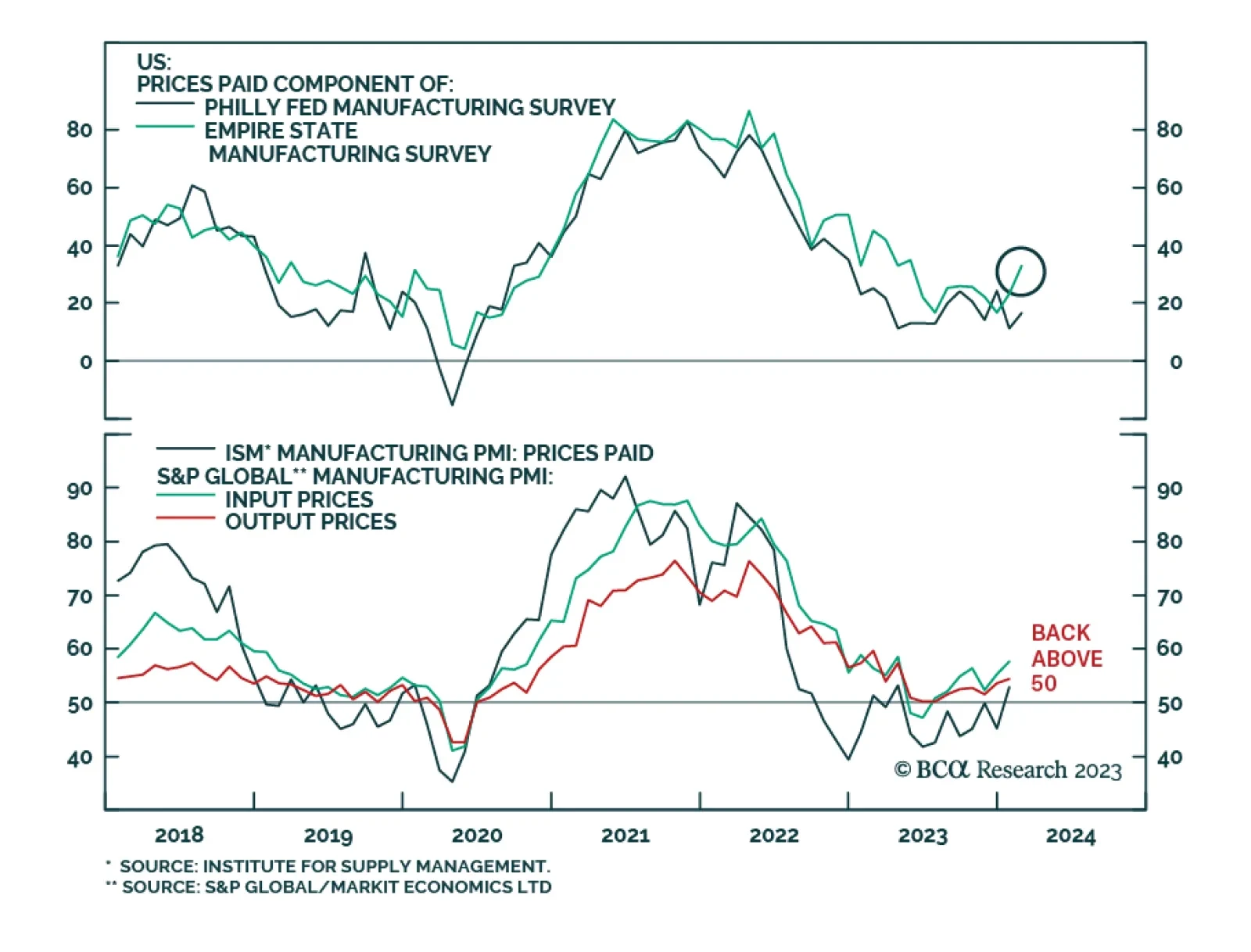

The first two regional fed manufacturing surveys for February delivered strong upside surprises. The New York Fed’s Empire Index surged from -43.7 to -2.4, unwinding its January slump. Similarly, the Philly Fed current activity index jumped by 15.8 points to…

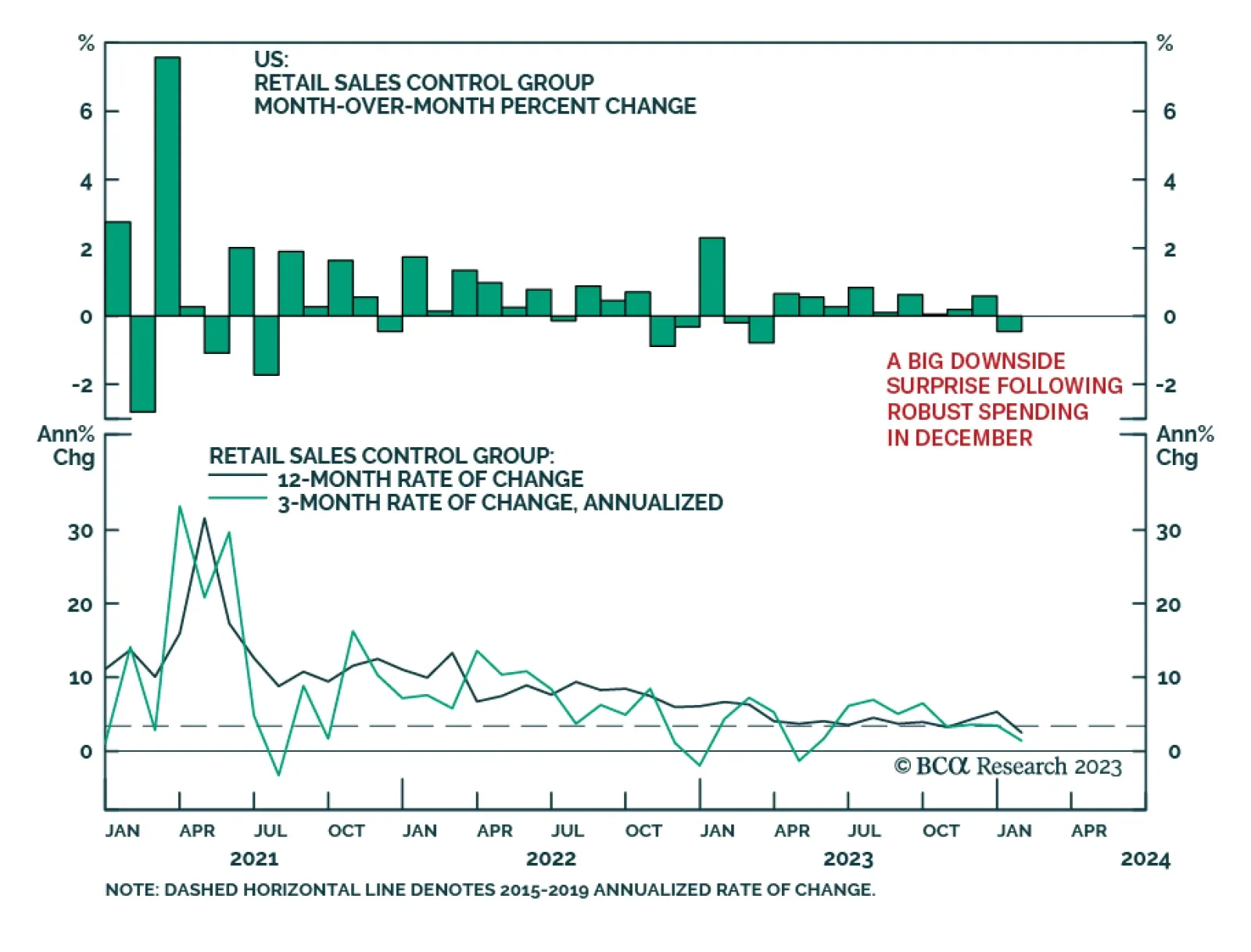

The US retail sales report for January delivered a disappointing message about consumer spending. The 0.8% m/m drop in overall retail sales was worse than expectations of a 0.2% m/m decline and marked the most severe monthly contraction since last March. The…

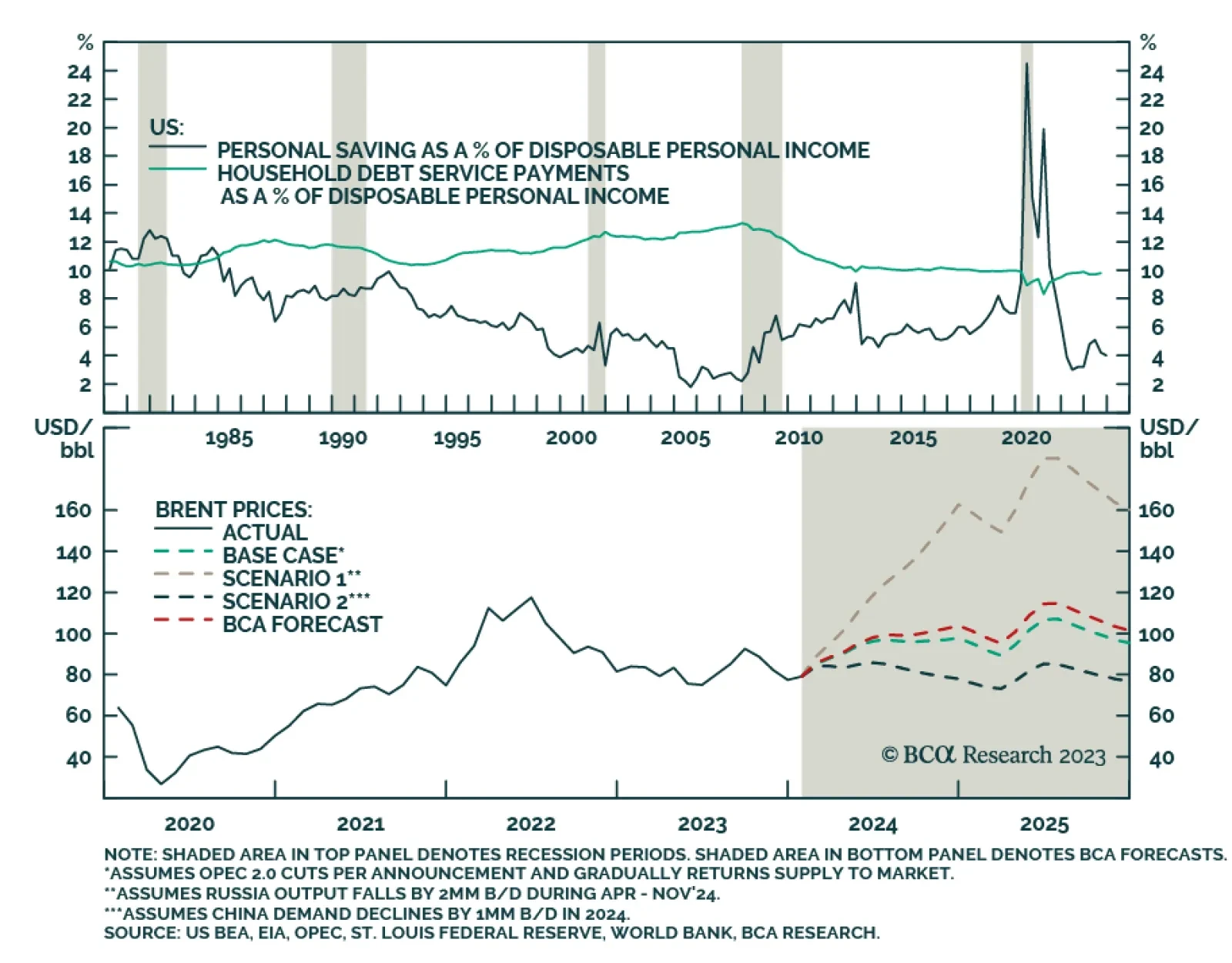

Our Commodity & Energy colleagues see oil markets balanced in the short run, which keeps their Brent price forecasts at $95/bbl and $105/bbl for 2024 and 2025. That said, they note the odds are increasing demand growth could surprise to the…