Recession-Hard/Soft Landing

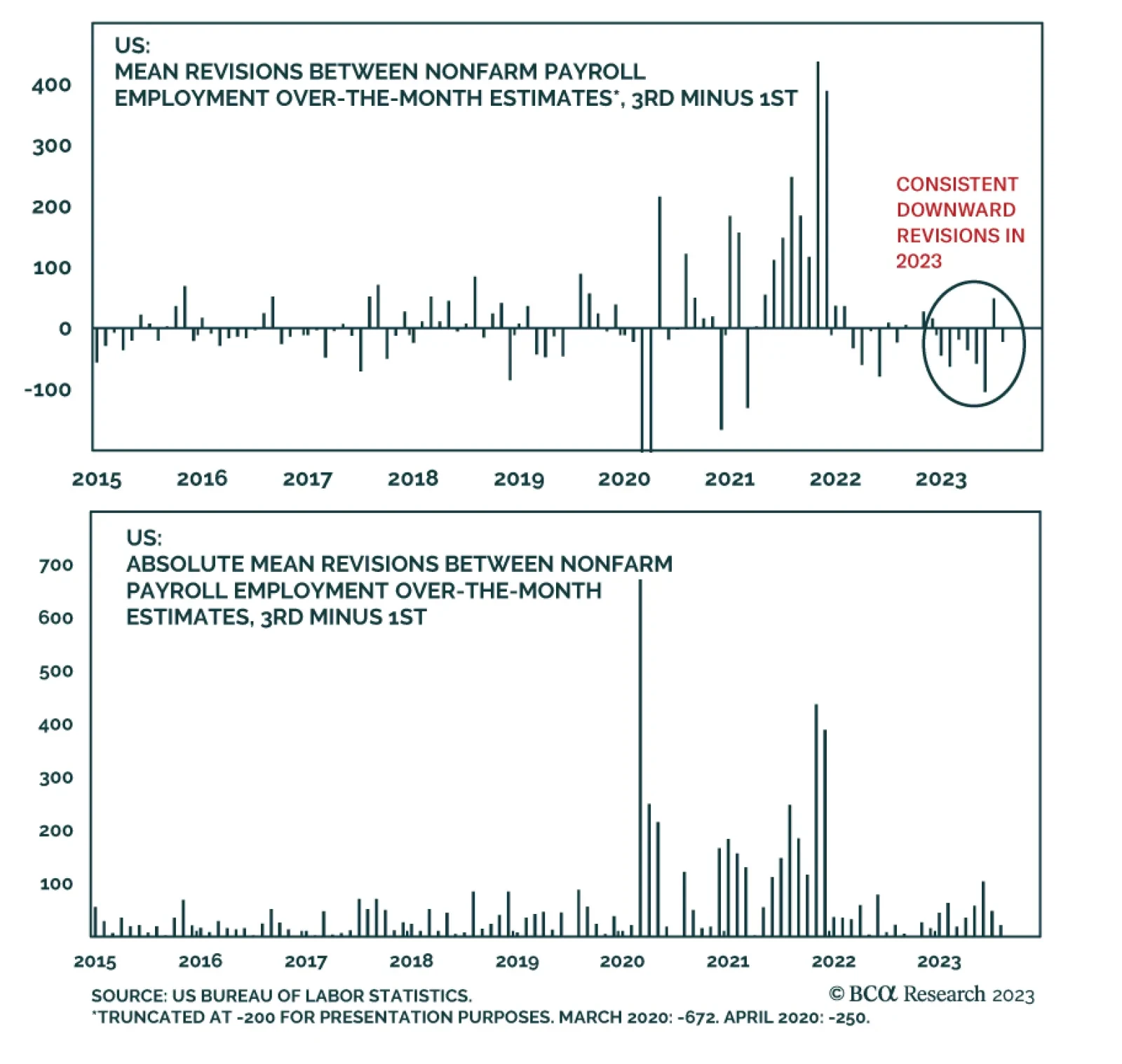

The US nonfarm payroll report is an important monthly data release that investors scrutinize for updates on the state of the US labor market and economy more broadly. In the current context, the updates help gauge whether the US economy is heading toward…

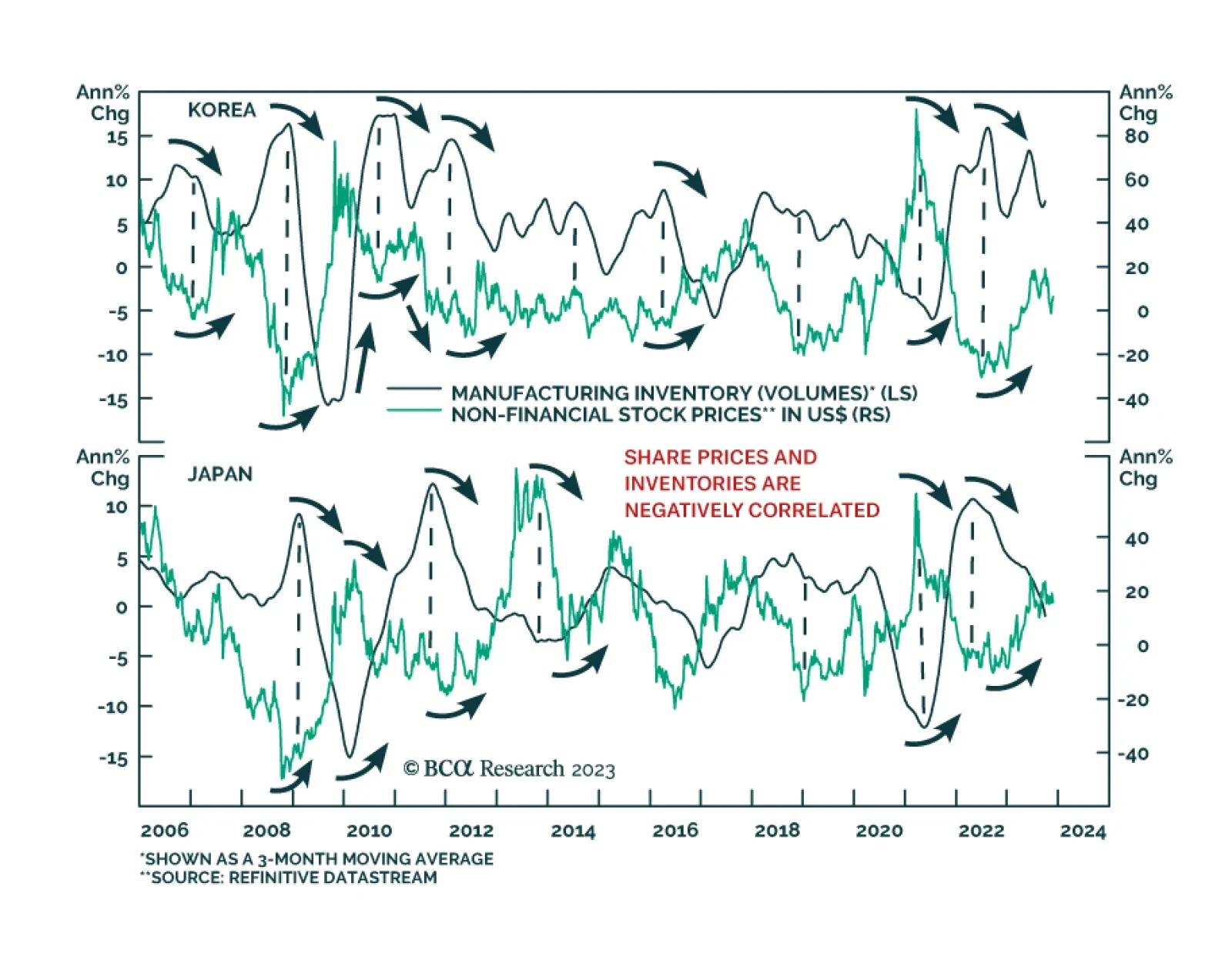

According to BCA Research's Emerging Markets Strategy service, investors should focus on fluctuations in final demand rather than inventories. A common narrative endorsed by many market participants is that inventory restocking worldwide will support the…

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

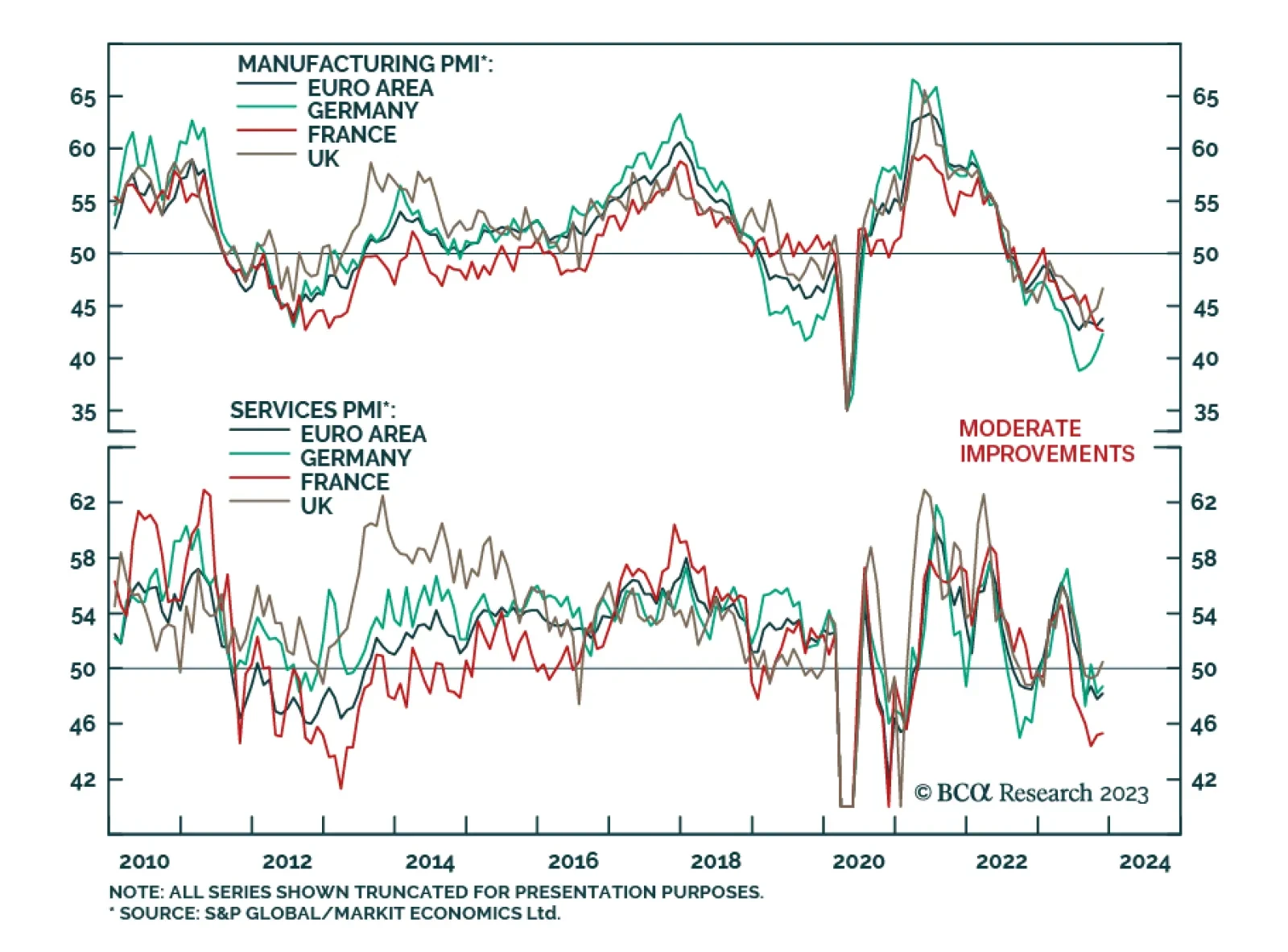

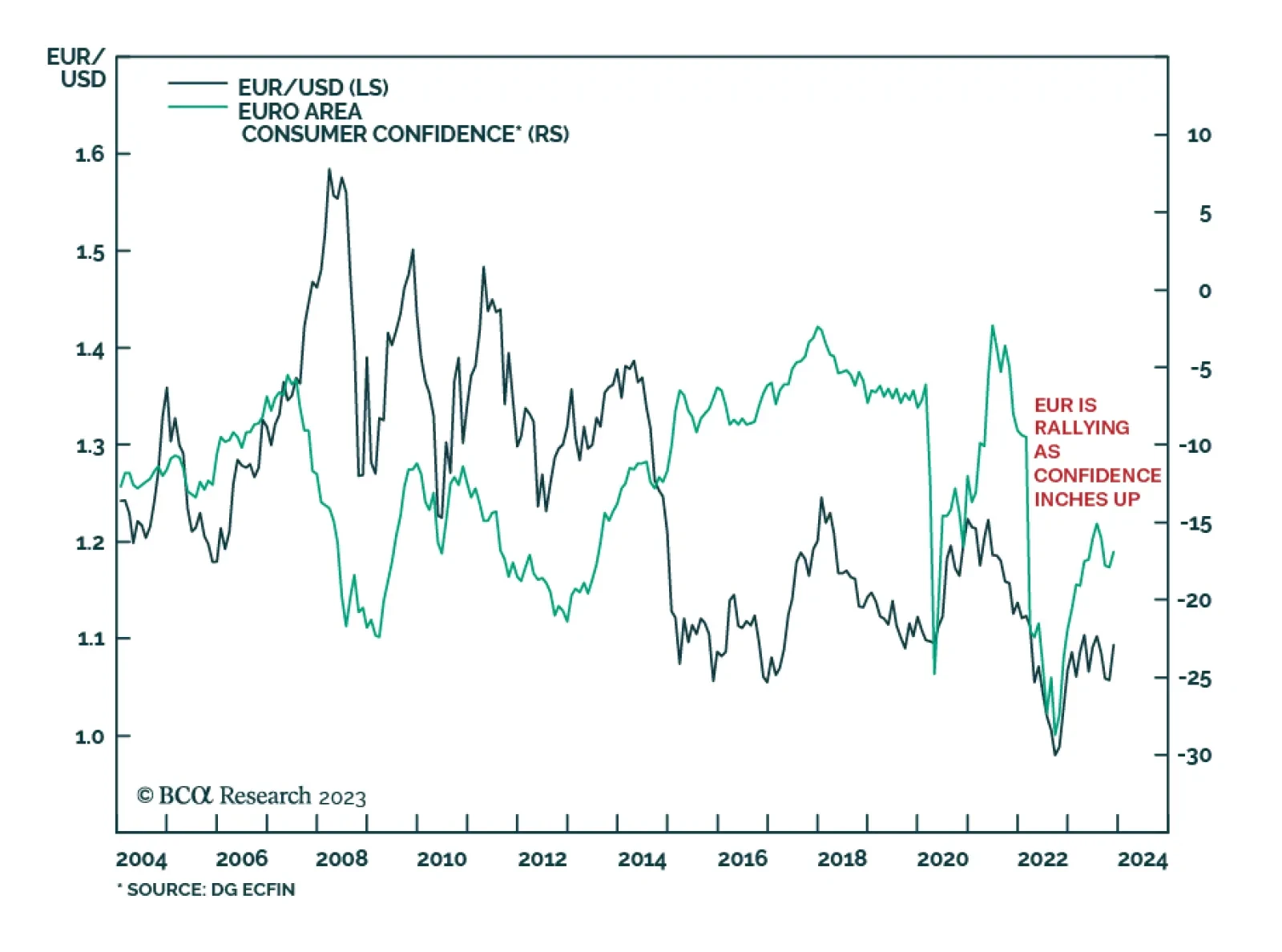

European flash PMI estimates for November sent a slightly less pessimistic signal on Thursday. The Eurozone composite PMI climbed by 0.6 points to 47.1, beating expectations of a more muted increase to 46.8. Notably, both the manufacturing and services…

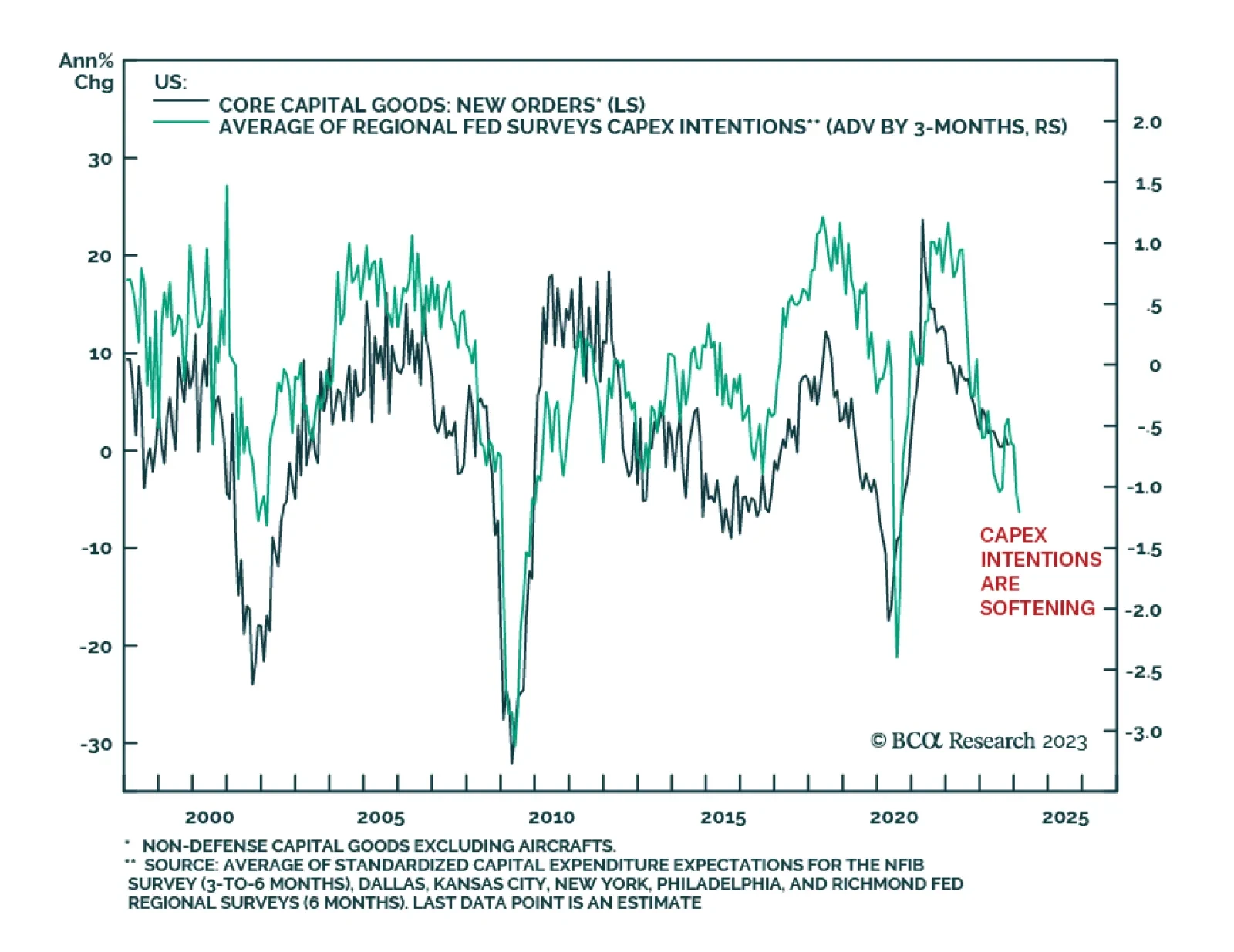

US durable goods orders delivered a negative surprise on Wednesday. New orders for manufactured durable goods dropped by 5.4% m/m in October, below consensus estimates of a 3.2% m/m decline. Moreover, the September increase was revised down slightly to 4.0%…

Confidence is on the mend in the Euro Area. The rebounding ZEW growth expectations index reveals that investors are becoming more optimistic. The German IFO's business climate index inched higher in October for the first time since April, suggesting that…

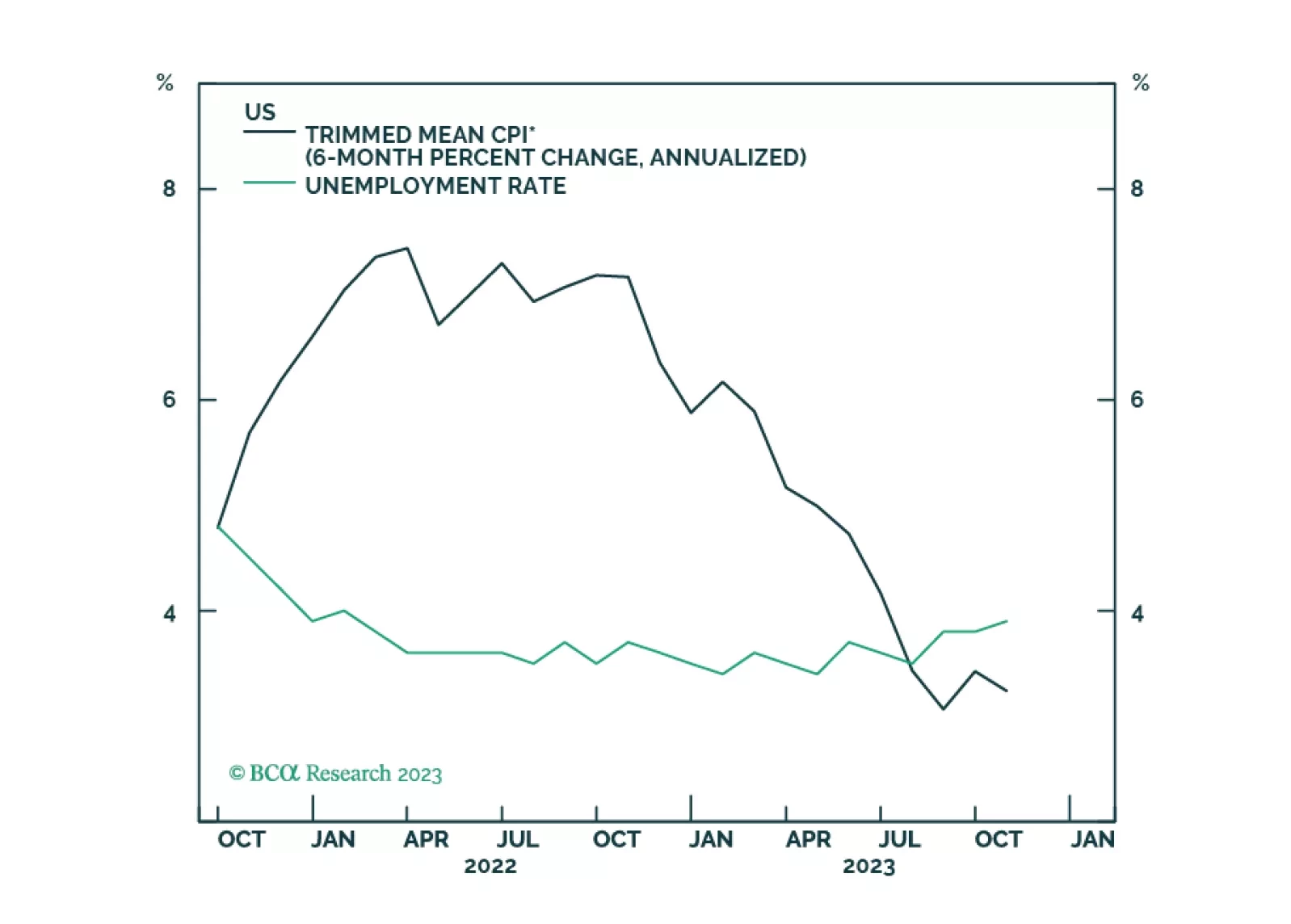

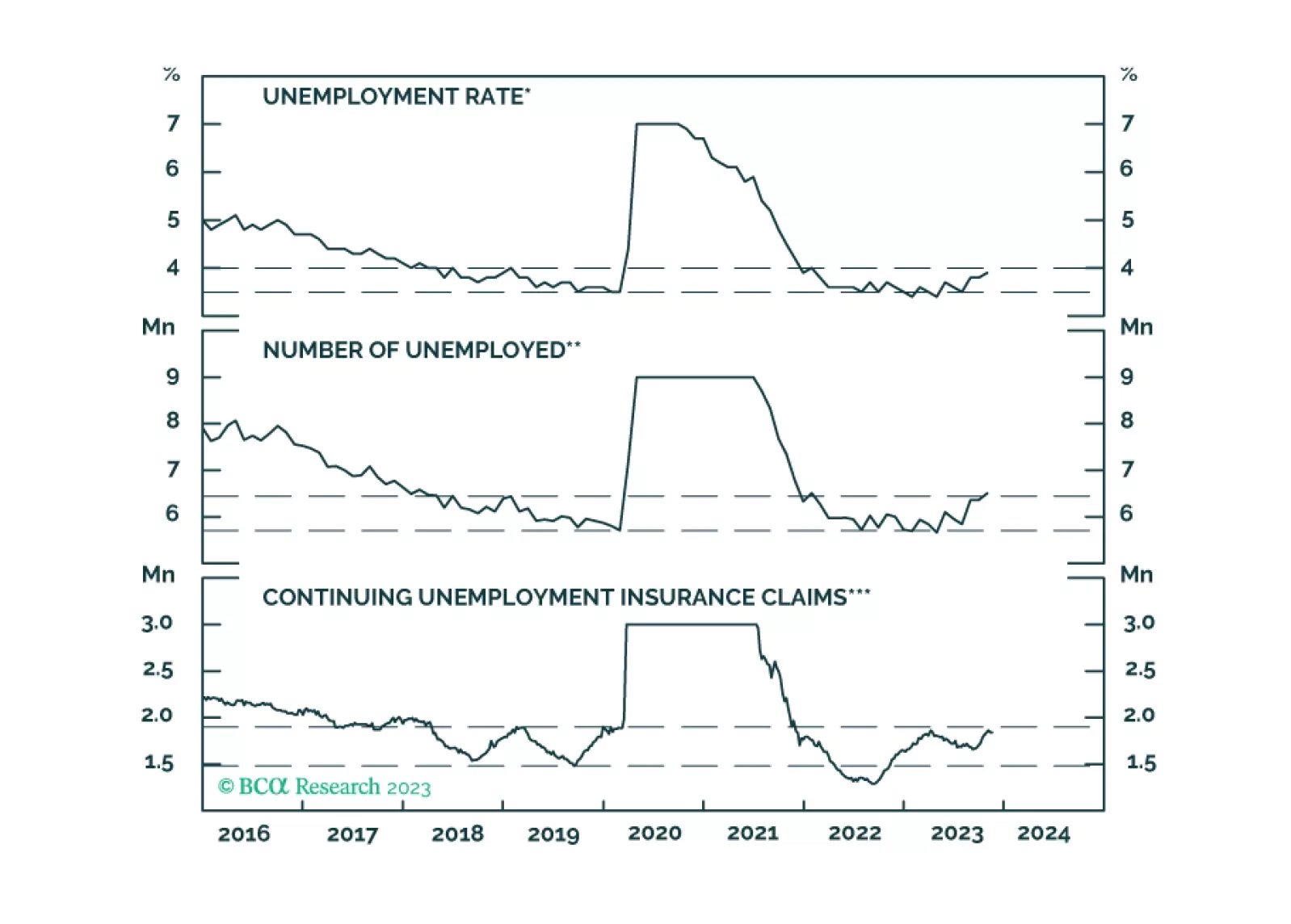

We investigate the recent increase in unemployment with the goal of determining whether it is flagging an imminent US recession.

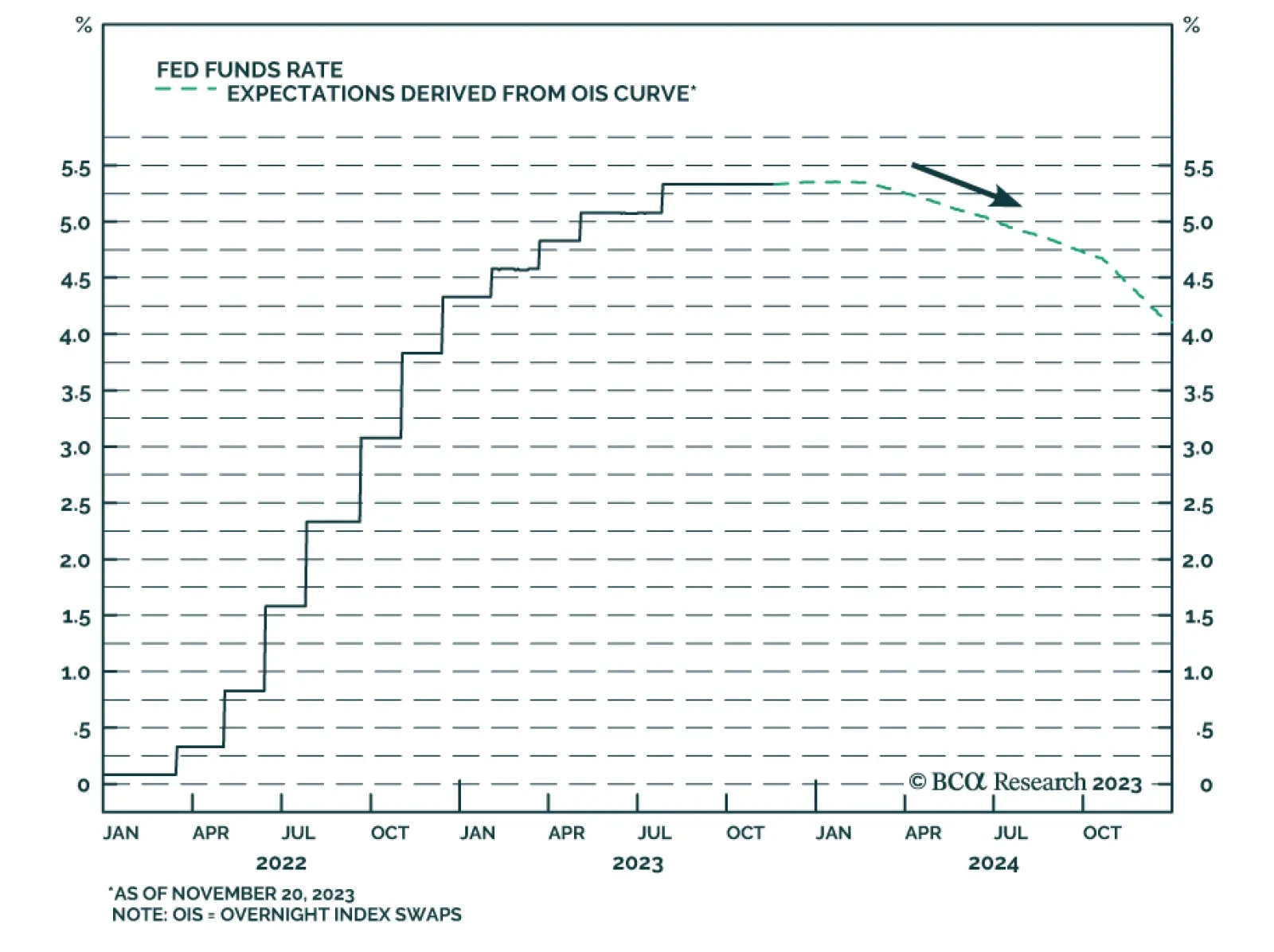

The minutes of the Fed's latest FOMC meeting revealed that there is a consensus among policymakers to proceed carefully. Another rate increase is appropriate only if "incoming inflation indicated that progress toward the Committee's inflation objective was…

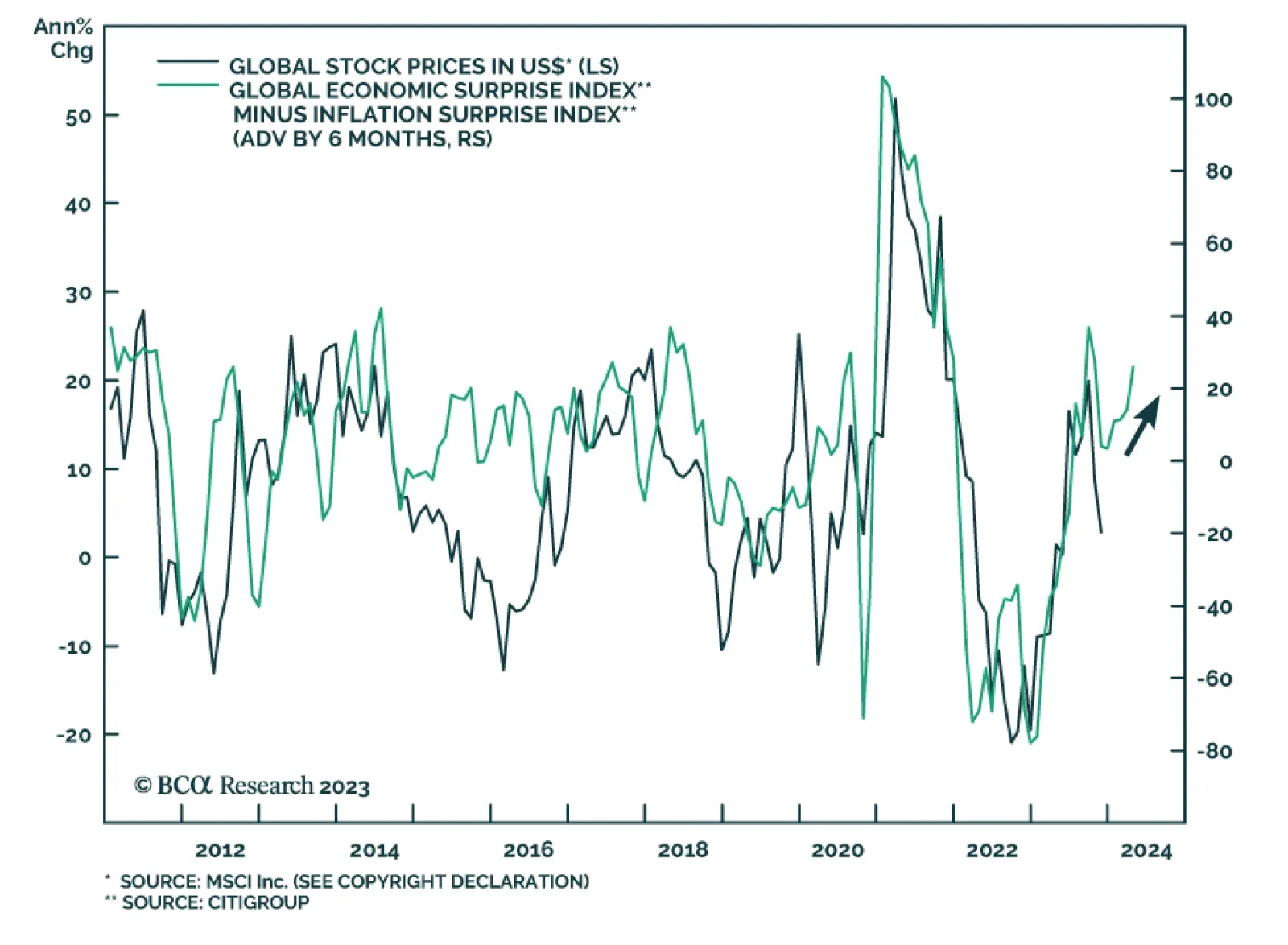

After dipping into negative territory between June and early August, the Global Economic Surprise Index has since rebounded, signalling an improvement in economic momentum. Initially, this rebound was isolated to the US. However, the trend has been broadening…

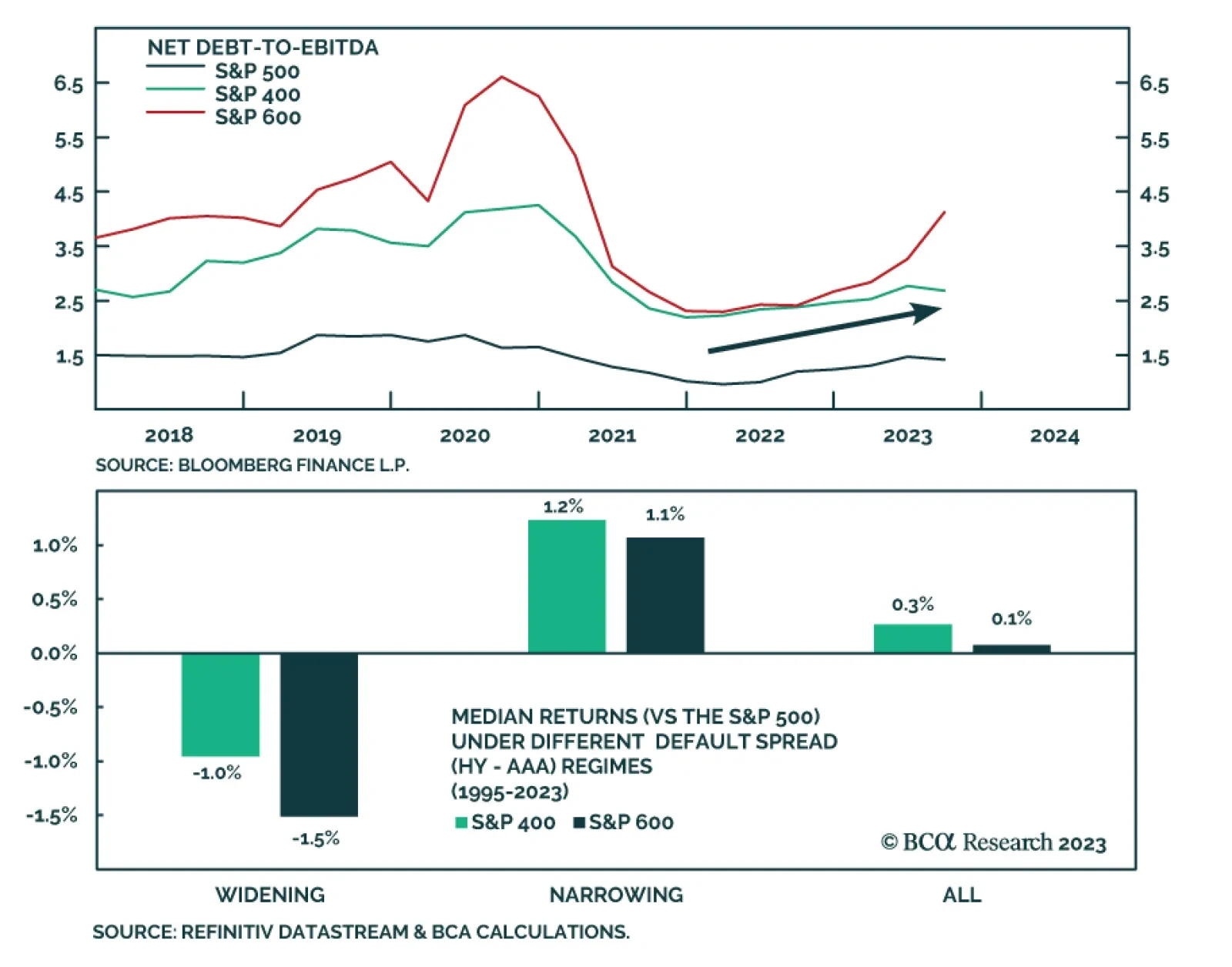

According to BCA Research's US Equity Strategy service, mid-caps underperform when spreads widen, although less so than Small as they are more financially robust and have better credit ratings. Small is the most leveraged relative to income (EBITDA) and…