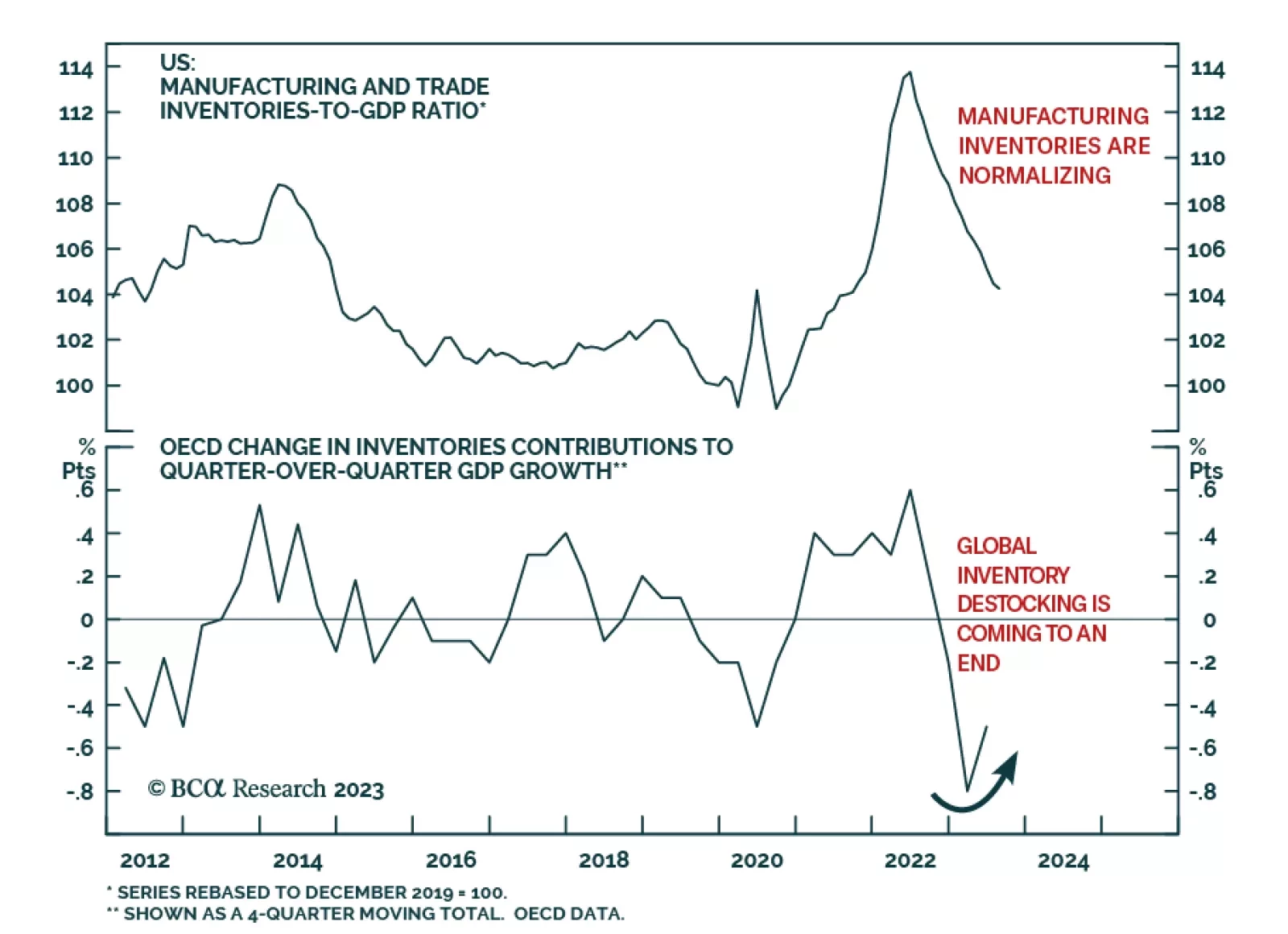

Recession-Hard/Soft Landing

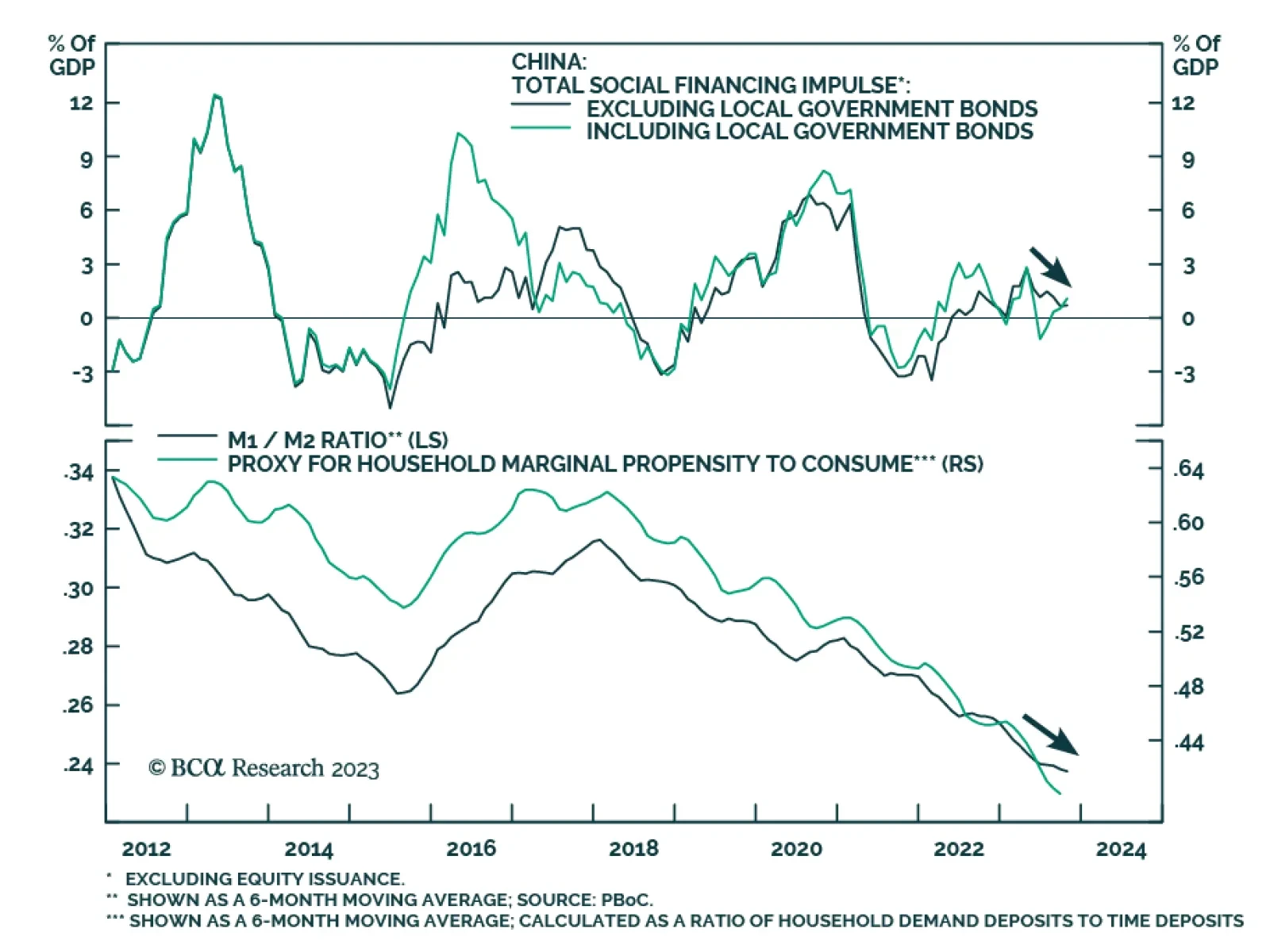

China's money and credit data remained weak in October. New total social financing amounted to RMB 1.85 trillion – less than the RMB 1.95 trillion anticipated and below the prior month's increase of RMB 4.12 trillion. Similarly, loans extended by banks fell…

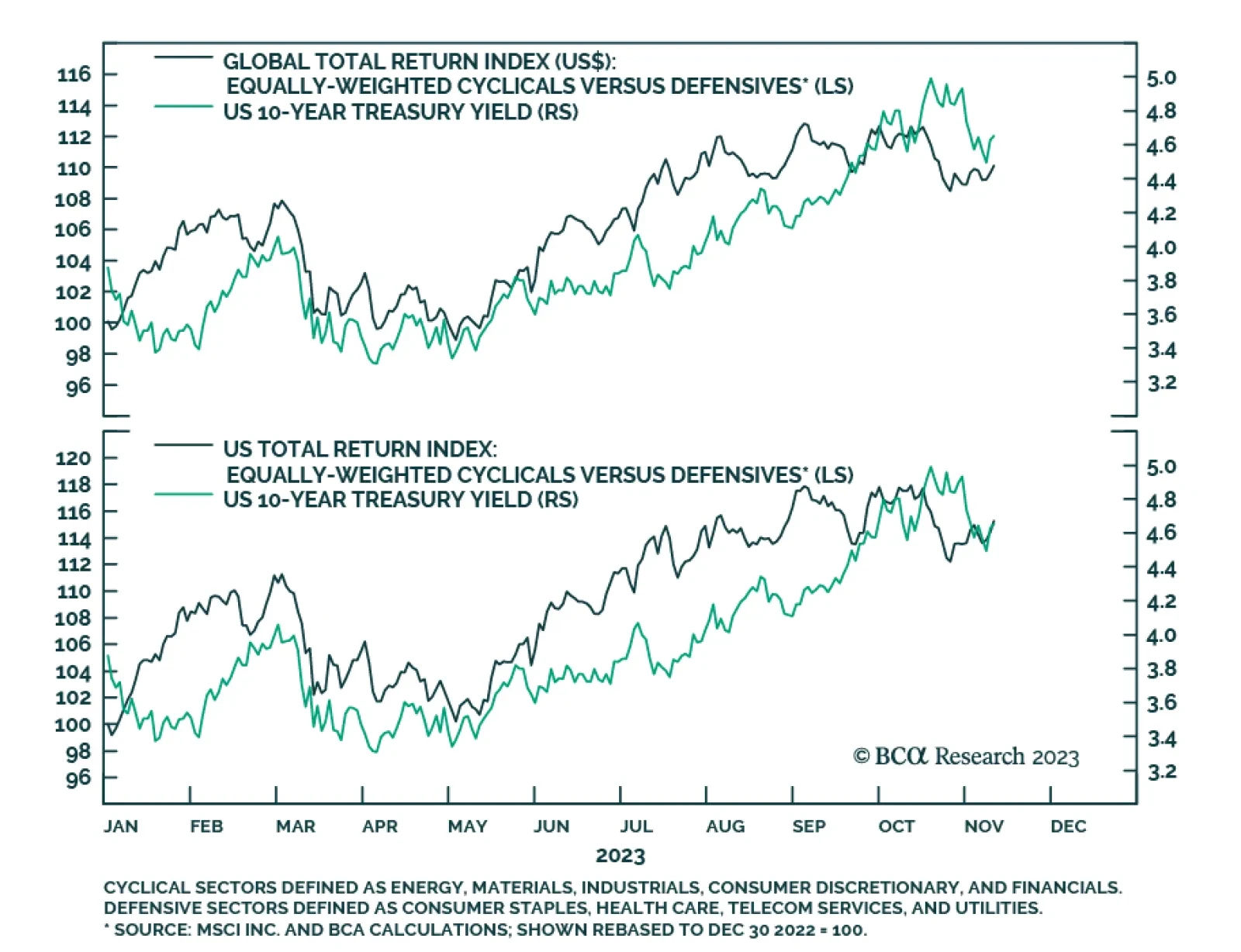

Our equally weighted global cyclical equity index has outperformed equally weighted defensives for most of this year. By October 17, this outperformance stood at about 12.6%. This outperformance is consistent with US Treasury market dynamics. The relative…

BCA Research's Global Investment Strategy service assigns 25% odds of the recession starting in 2025 or later. Our colleagues continue to think that the US will succumb to a recession in 2024, probably in the second half of the year. They see the…

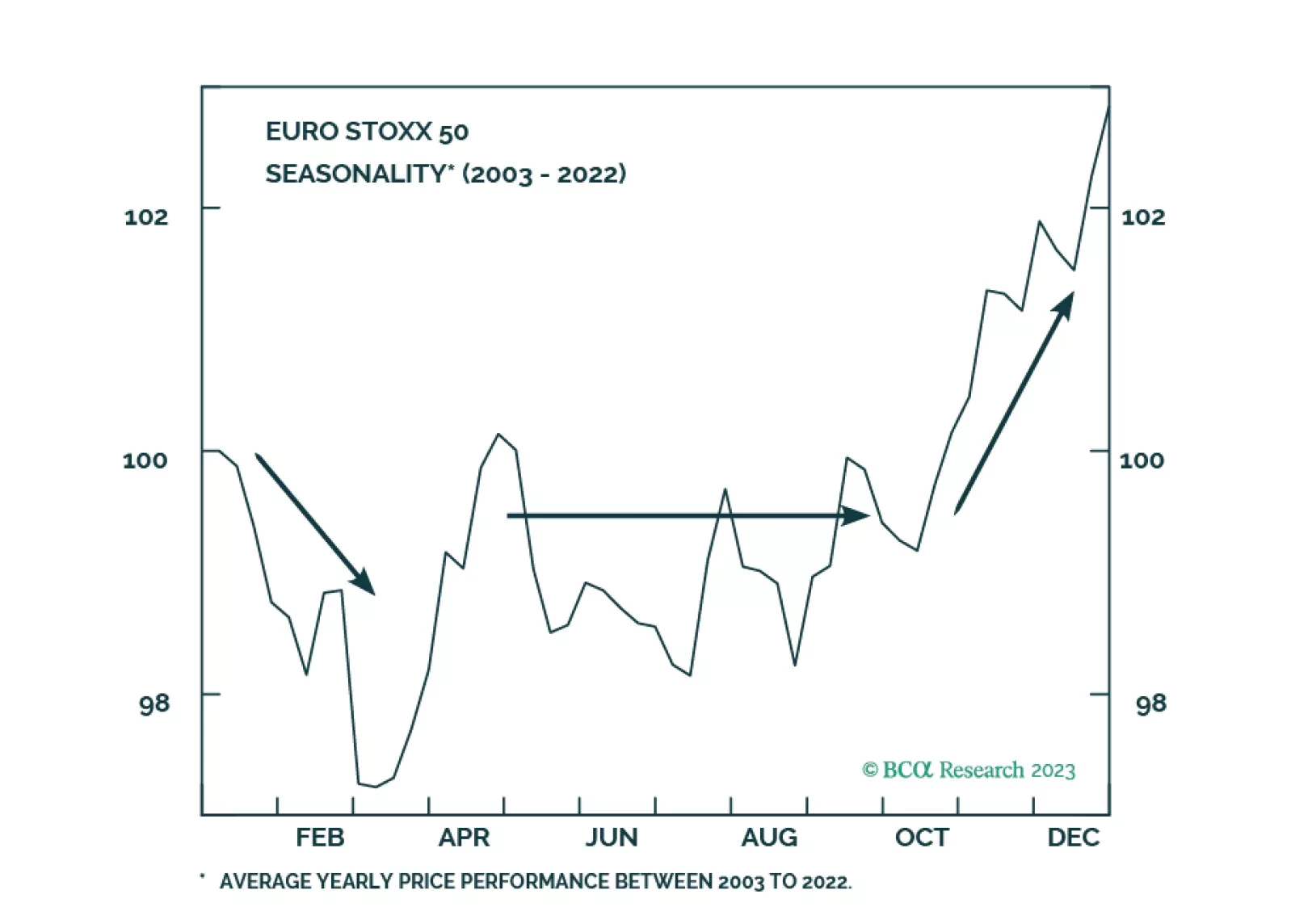

European markets have room to rebound in the coming weeks, however, a recession looms. What are the lessons from history that investors can use to position themselves under these conditions?

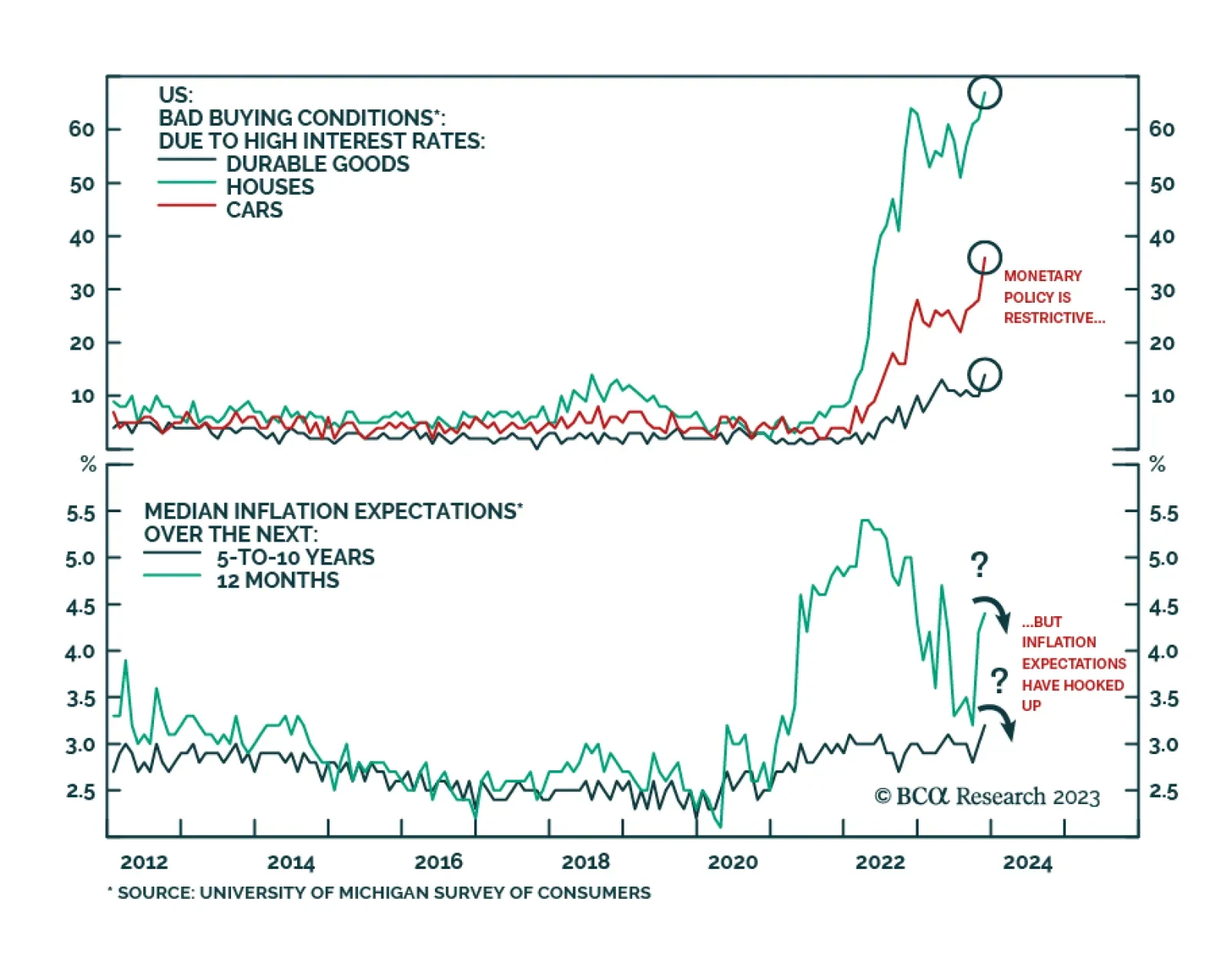

The preliminary release for the University of Michigan’s Consumer Survey sent a pessimistic signal about consumer sentiment on Friday. The headline index fell from 63.8 to 60.4 in November, below expectations of a marginal decrease to 63.7. Declines in both…

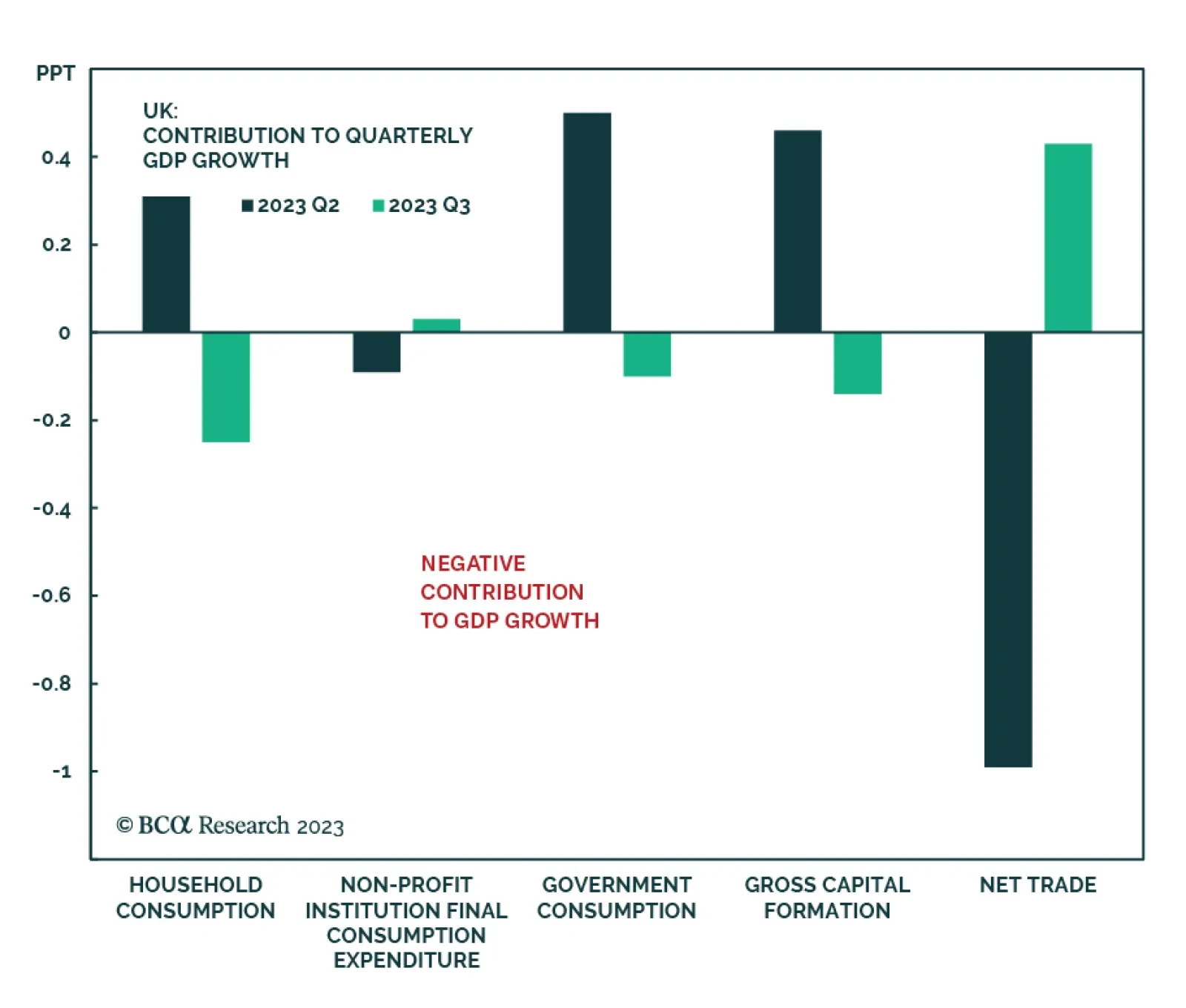

The UK economy stagnated in Q3 – a deterioration from the minor 0.2% q/q expansion in the prior quarter. Although the Q3 figure is slightly better than anticipations of a 0.1% q/q contraction, the details of the report are generally weak. Consumption dropped…

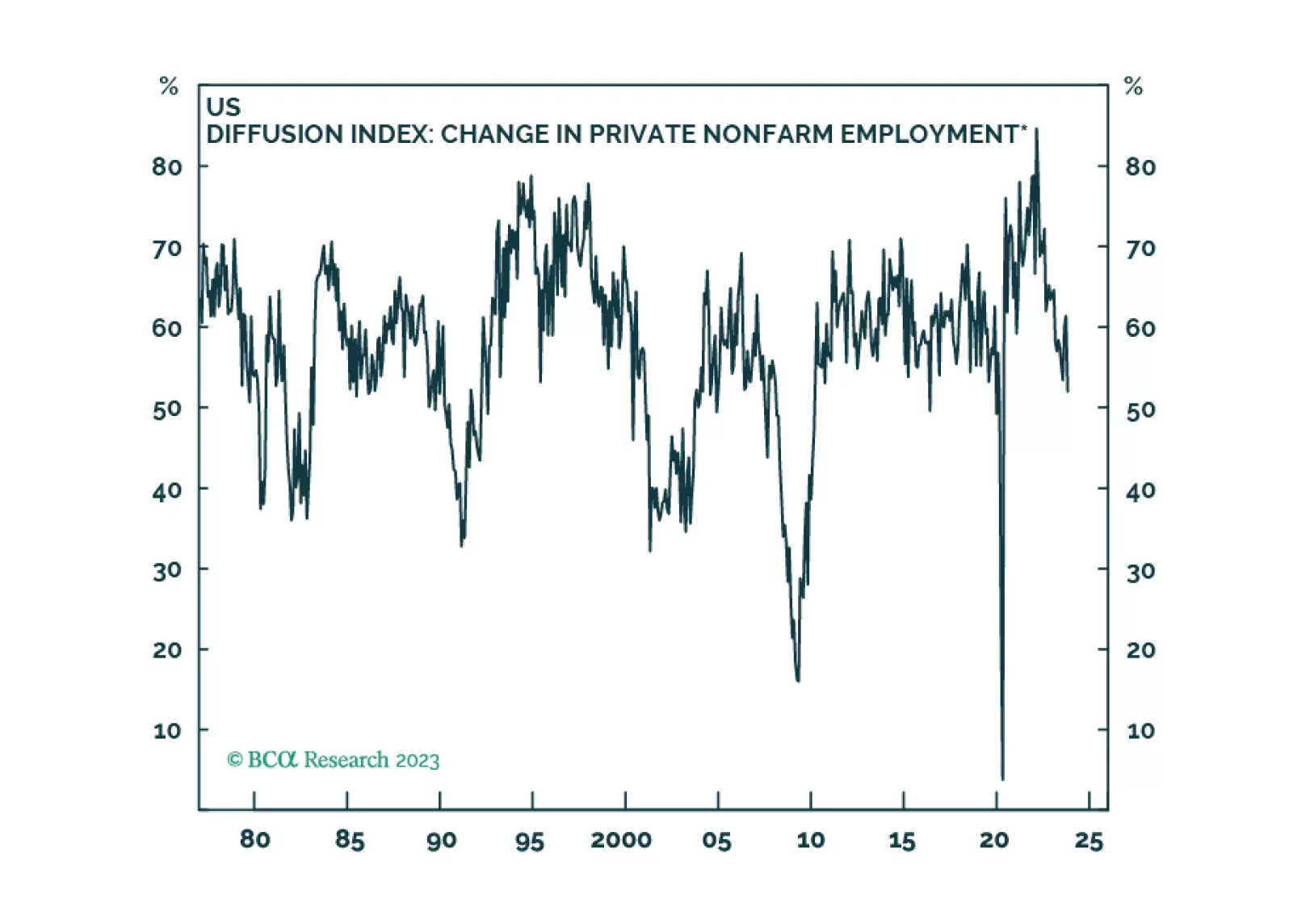

Labor markets are softening in most developed economies, as is usually the case in the lead-up to recessions. Our base case is that the global recession will begin in the second half of 2024, but we will be monitoring our MacroQuant model on a daily basis for confirmation.

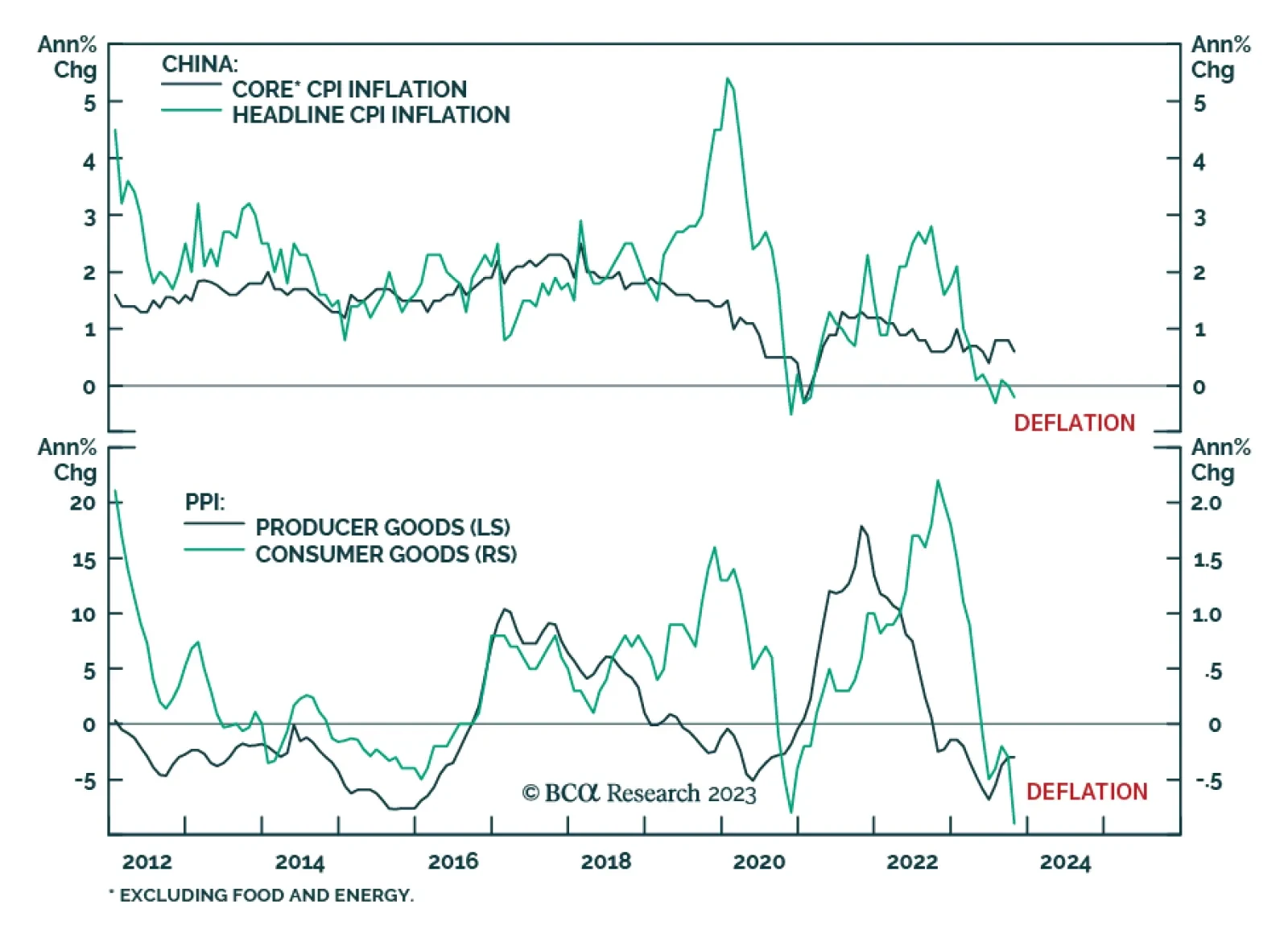

China's CPI and PPI inflation release for October indicates that deflationary pressures continue to dominate the domestic economy. After remaining unchanged in September, consumer prices declined by 0.2% y/y last month, falling below consensus estimates of a…

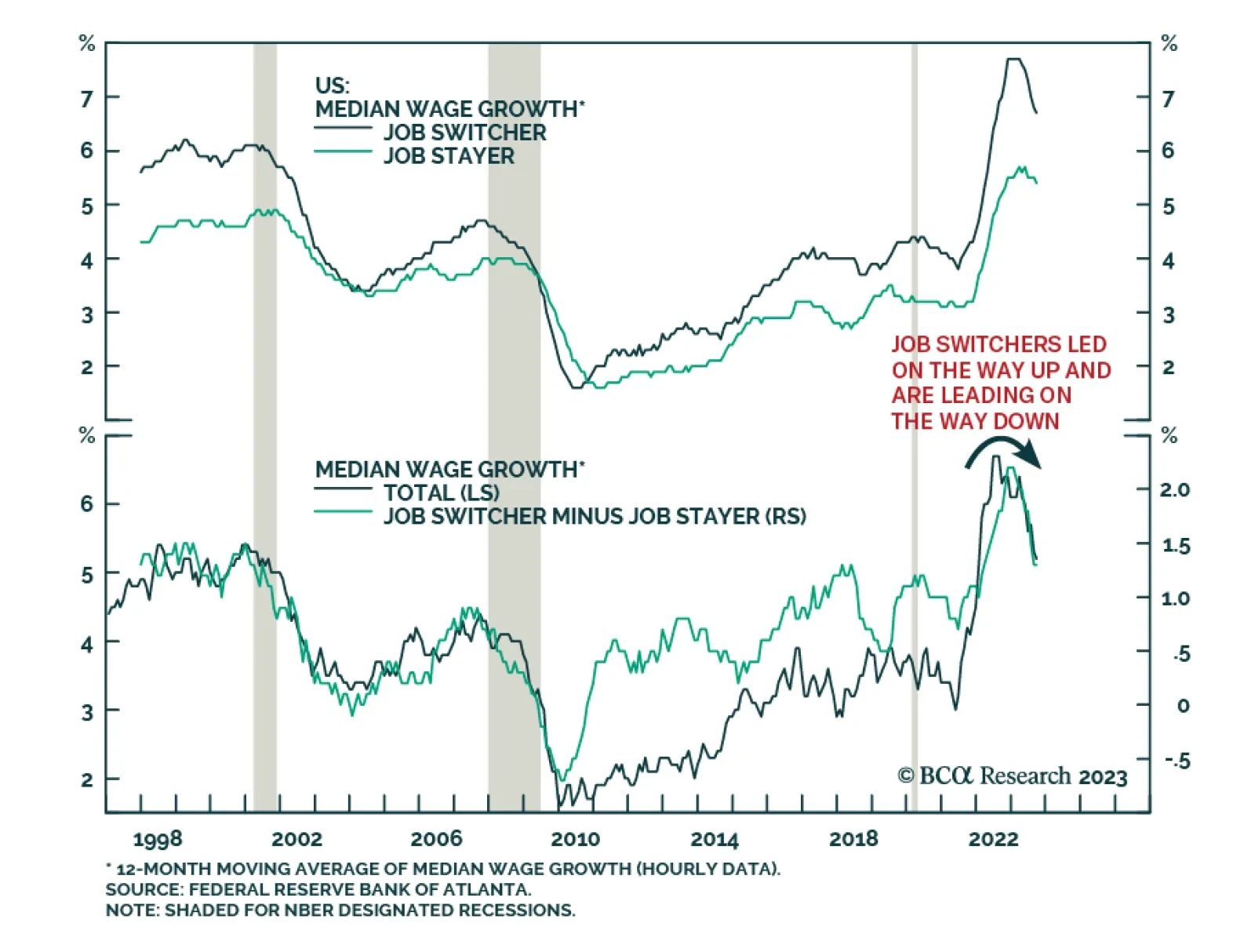

After surging in H2 2021/H1 2022, the Atlanta Fed's Wage Growth Tracker has been on a general downtrend for over a year. The latest reading of 5.2% in October – albeit unchanged from September – is considerably below the peak of 6.7% just over a year ago.…

According to BCA Research’s Counterpoint service, the ECB is the central bank that poses the lowest risk of repeating the mistakes of the 1970s and letting inflation expectations unanchor. One reason is the ECB’s inherited Germanic anti-inflation DNA. Even…