Recession-Hard/Soft Landing

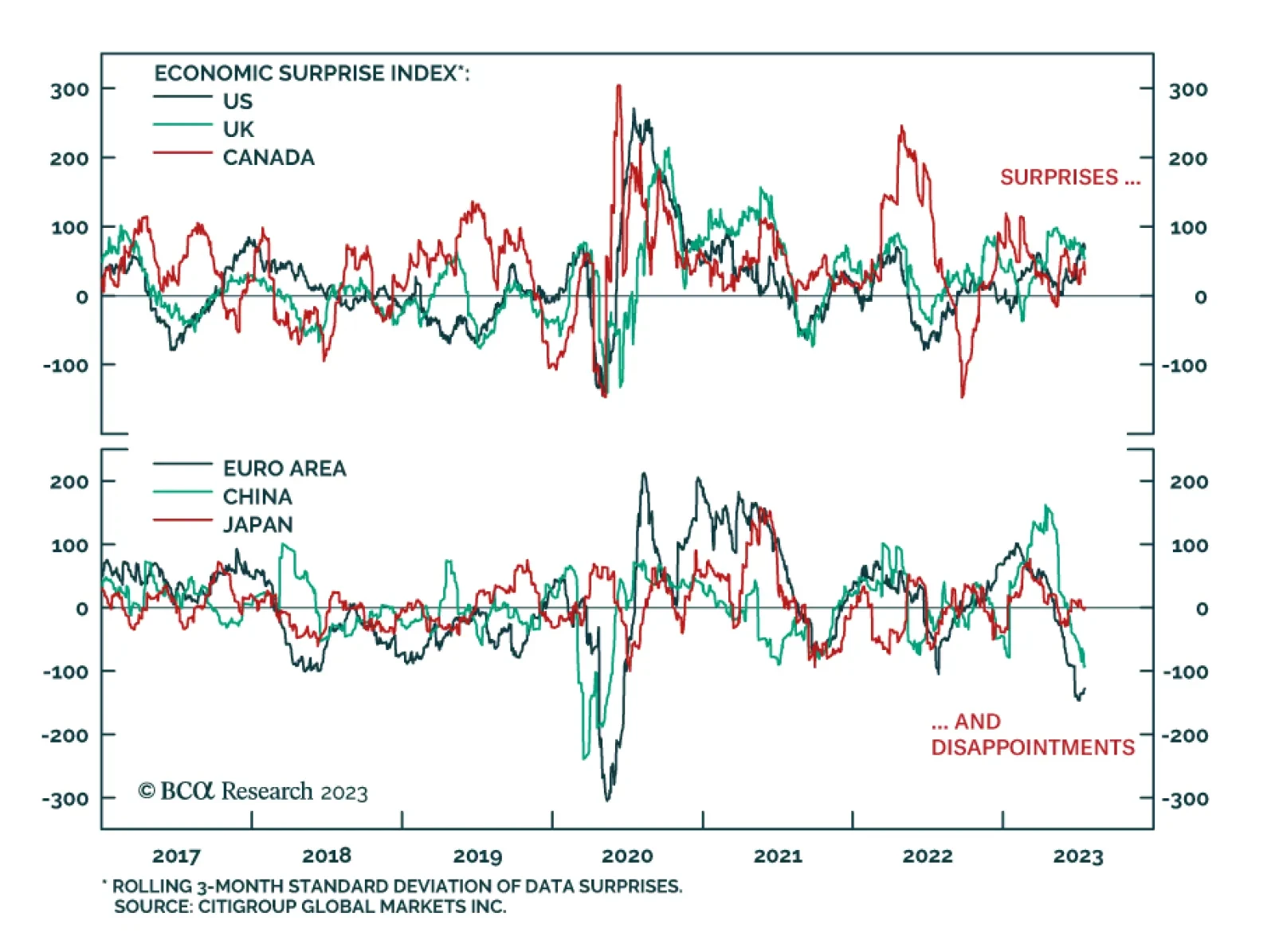

Citigroup’s global economic surprise index has fallen sharply over the past few months and is now slightly negative – indicating that economic data have surprised to the downside. Yet beneath the surface, there is a dichotomy across major global economies.…

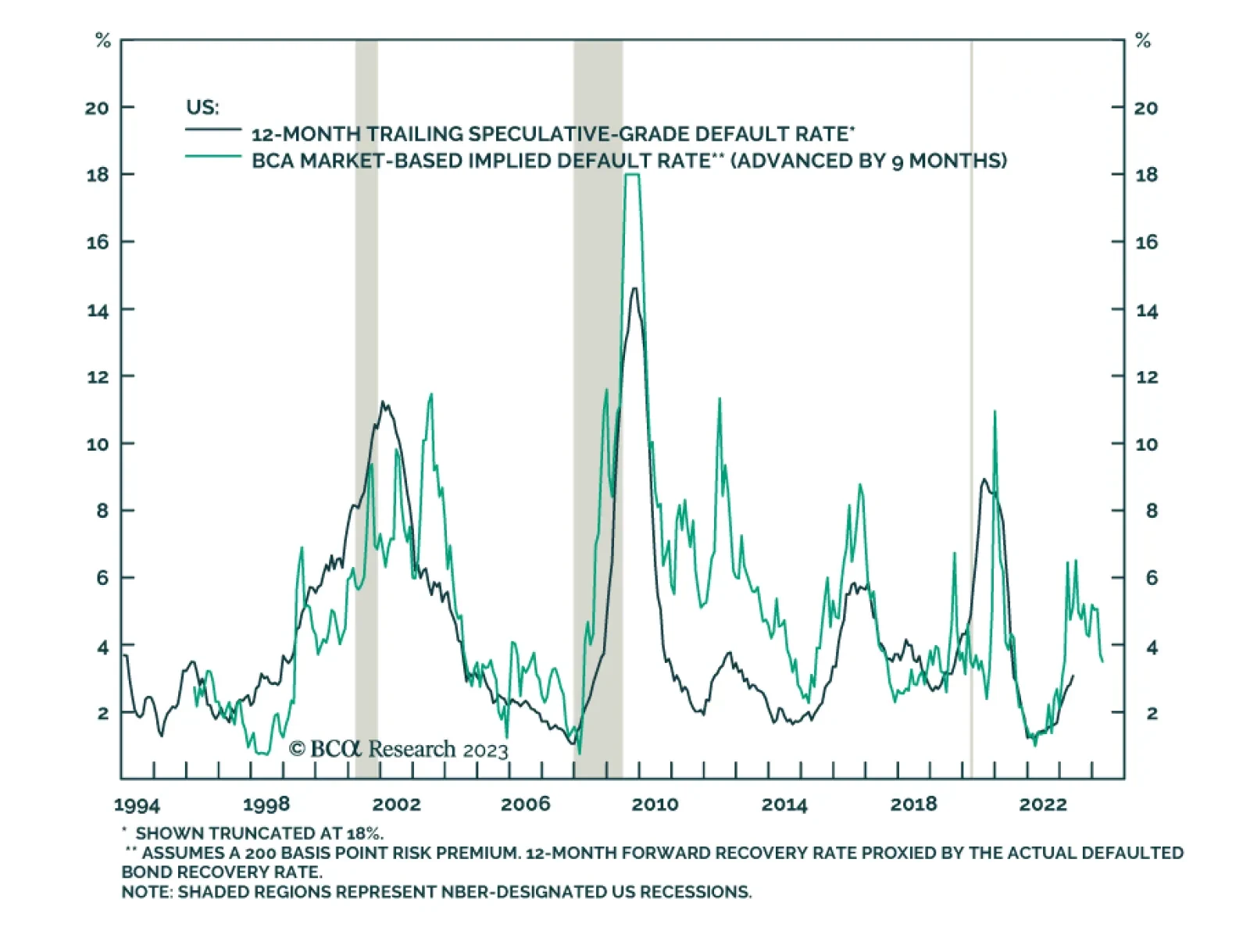

US speculative-grade corporate bond (junk) spreads rose significantly last year in response to a sharp increase in US interest rates and widespread concerns about a US recession. Junk spreads have since come in from their mid-2022 peak, and now trade below…

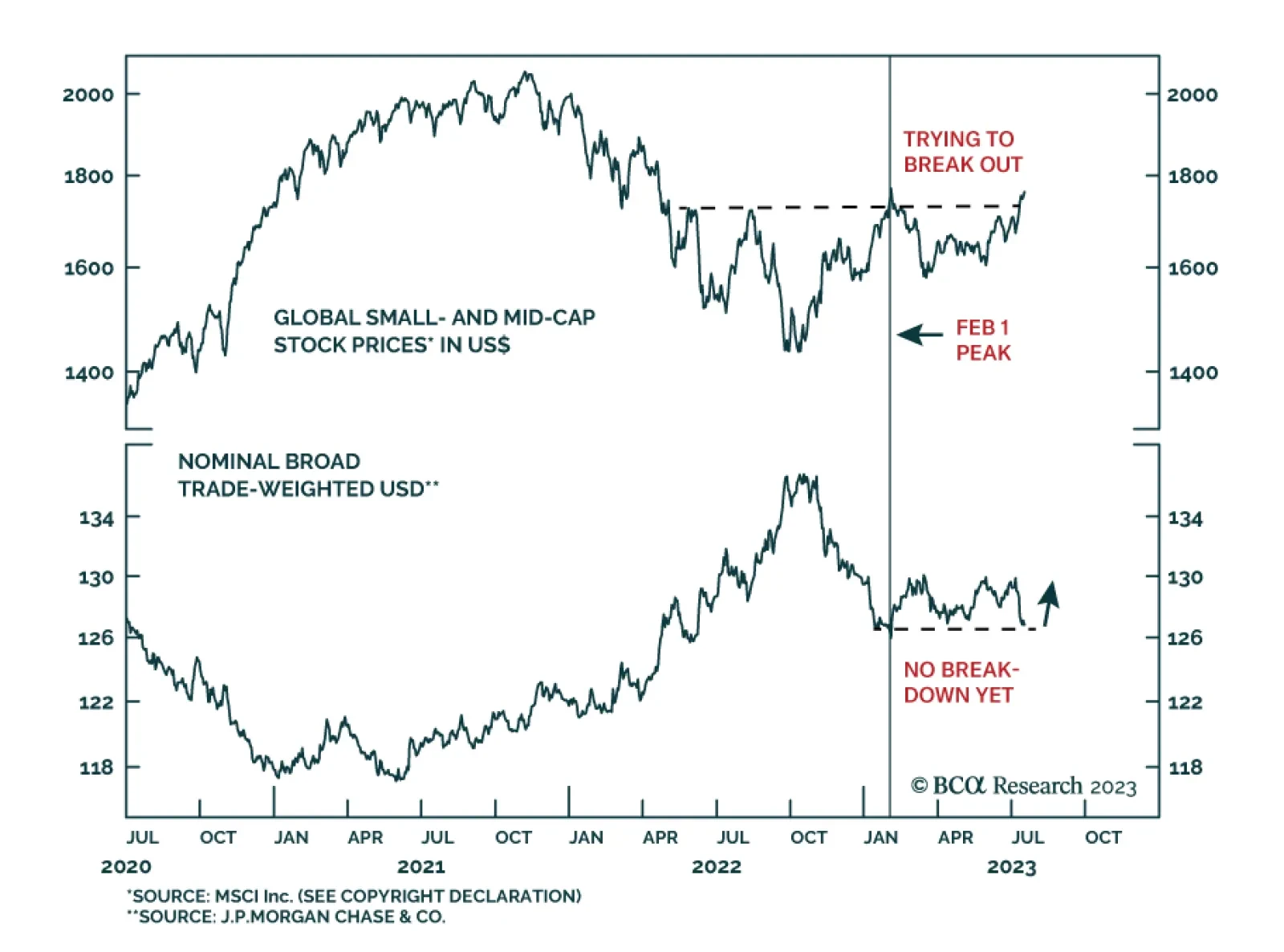

BCA Research’s Emerging Markets Strategy service concludes that the failure of EM stocks, Asian currencies and commodities to stage a broad-based outperformance is consistent with their macro thesis that global trade/manufacturing – the main driver of EM –…

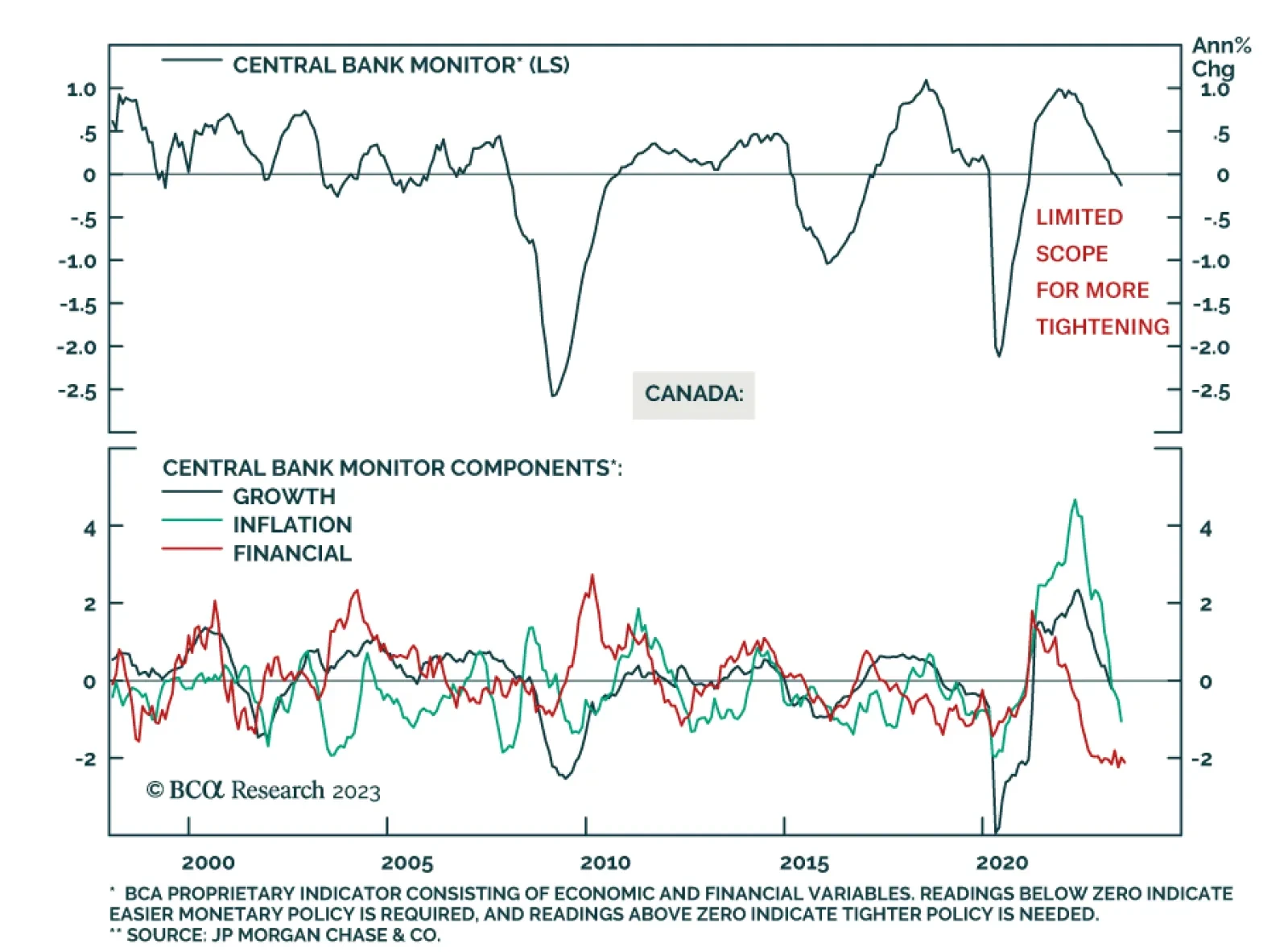

Canada’s CPI release showed headline CPI inflation cooled from 3.4% y/y to 2.8% in June – below estimates calling for a less pronounced moderation to 3.0% y/y. This marks inflation’s first return to the Bank of Canada’s 1%-3% percent inflation target range…

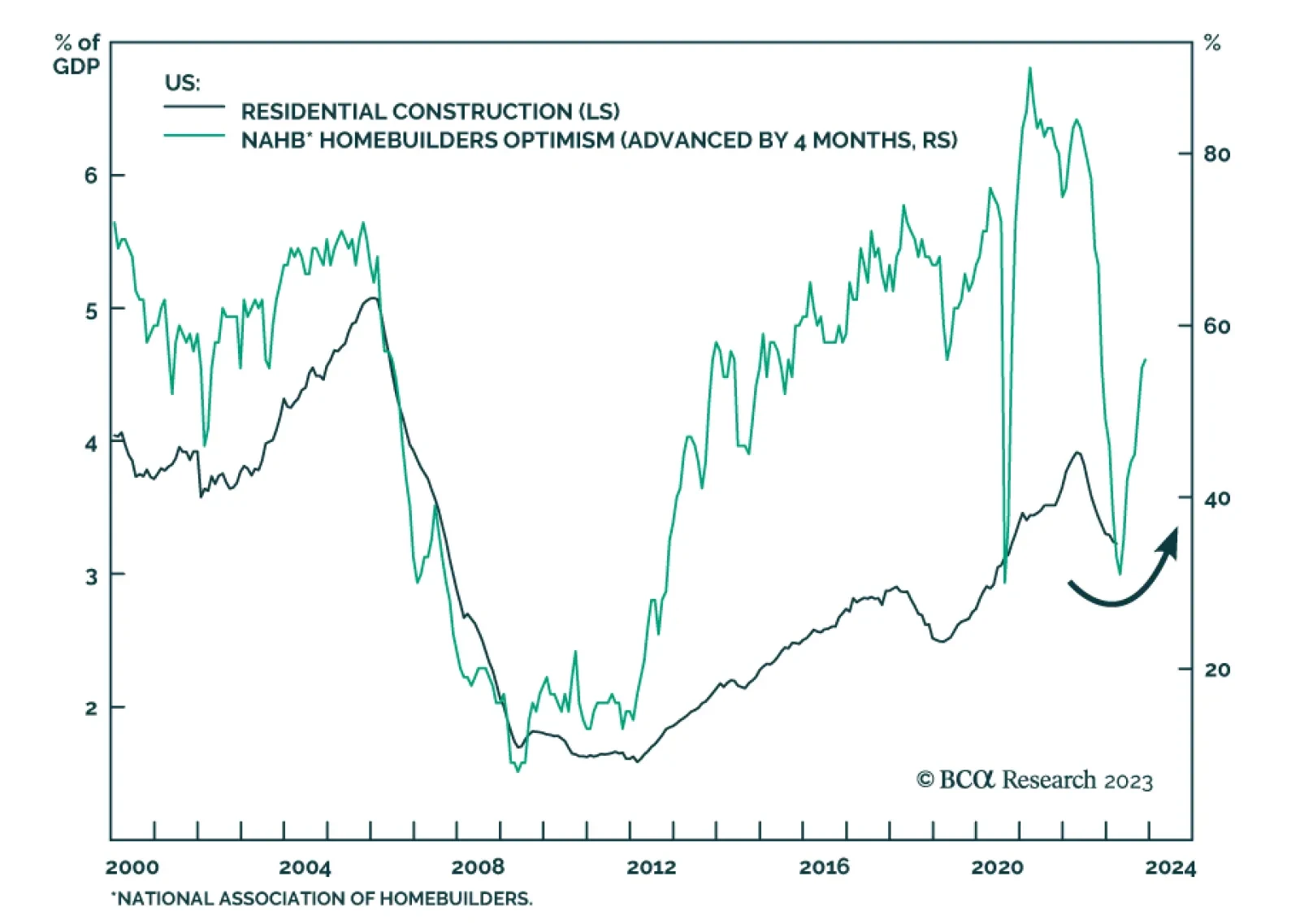

Results of the NAHB survey shows US homebuilder sentiment inched further above 50 to a 13-month high of 56 in July. Its ongoing rise above 50 indicates that net sentiment is becoming increasingly favorable. That said, homebuilders pared back some optimism…

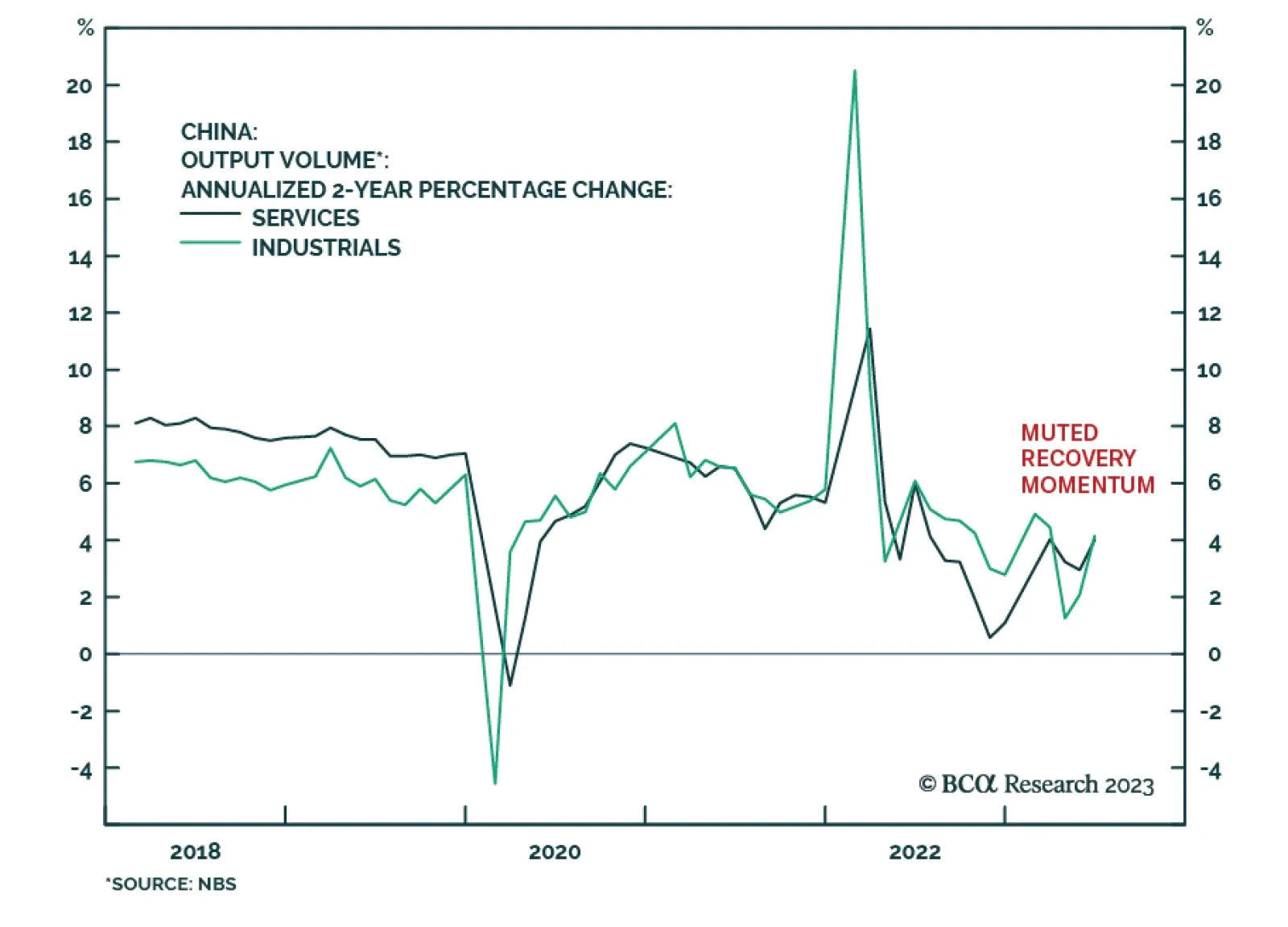

On the surface, the latest batch of Chinese economic data released on Monday shows a deterioration in consumer spending with retail sales growth slowing sharply from 12.7% y/y to 3.1% y/y in June – slightly below consensus estimates of 3.3% y/y. In addition,…

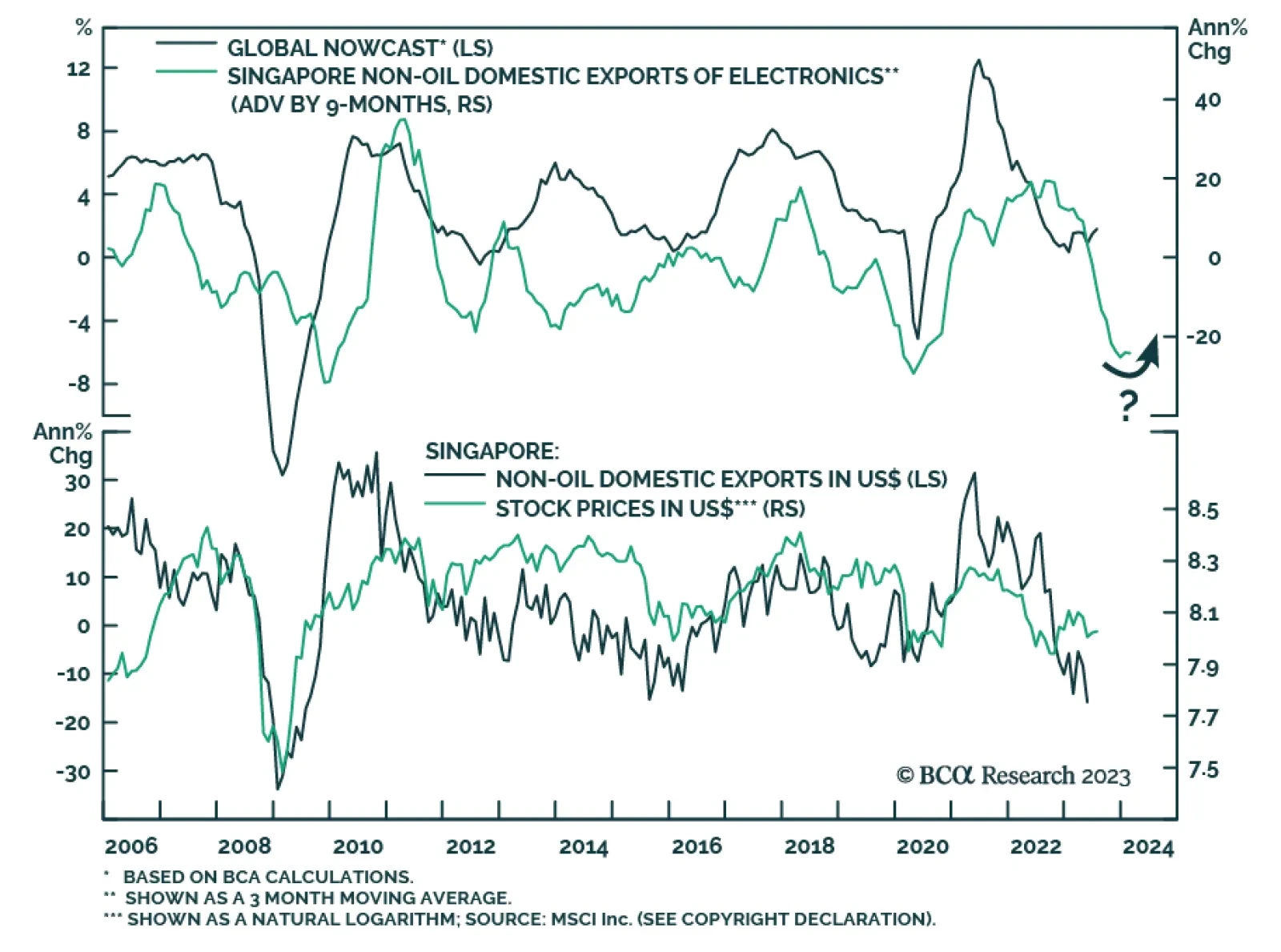

Singapore’s trade data continue to send a pessimistic signal about global manufacturing conditions. The year-over-year contraction in non-oil domestic exports (NODX) deepened to -15.5% y/y in June from -14.8% y/y – marking the ninth consecutive month of…

In the first five months of the year, optimism about GAI (generative AI) drove a narrow rally in US equities. The three sectors that contain companies that are most exposed to this dynamic were the only ones that experienced price gains. IT, Communication…

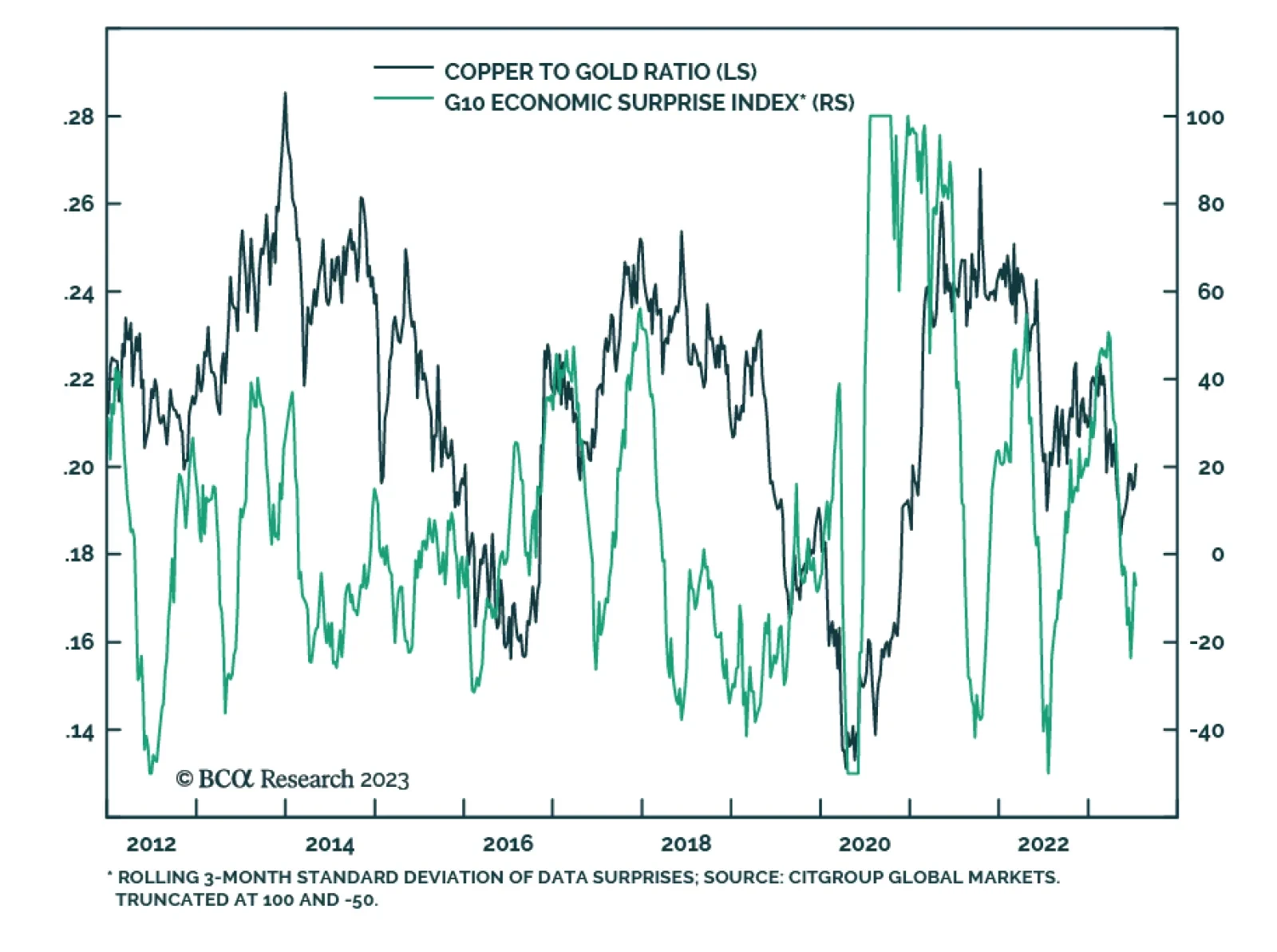

Copper rallied to a two-month high by the end of last week. Importantly, this move did not occur in isolation. It coincides with greater optimism about the prospects of a soft landing. Indeed, the US economic surprise index is solidly in positive territory…

Stocks fare best when there is plenty of slack in the economy and growth is strong and getting stronger. The good news is that the economic growth score for the US in our MacroQuant model is above its historic average. The bad news is that US economy is operating with little slack and sentiment is getting complacent. We recommend that investors maintain a modest overweight to equities for the time being but look to get more defensive later this year or in early 2024.