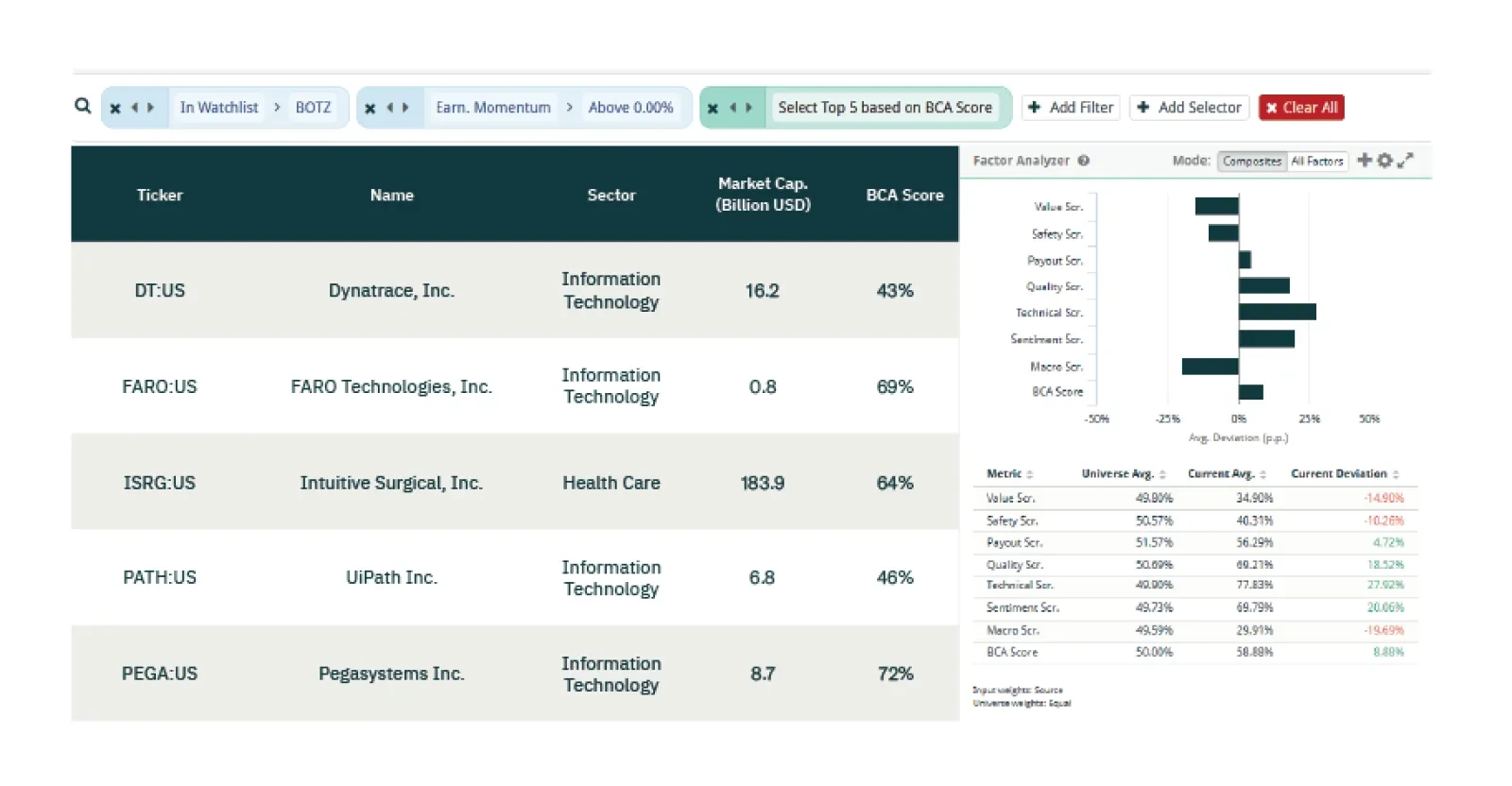

Dear Client,In this special issue we present the first commentary for the BCA Research US High-Quality Stock Selection strategy, which represents the next evolution of the Equity Analyzer service.The strategy, constructed exclusively using the Equity Analyzer toolset, provides reliable exposure to high-quality US securities through the BCA Score factor model, while maintaining sector neutrality relative to the US market.Most importantly, the underlying portfolio is now offered through BCA Research Investment Solutions, which provides turn-key and directing-indexing implementations of our quantitative signals. This solution marks the most accurate and practical implementation of our equity factor model to-date.For more information about the strategy, including historical performance metrics, or, to learn how to incorporate this service into your investment process, please contact investmentsolutions@bcaresearch.com.Performance RecapThe US equity market regained its composure in month of December 2021, with investors seeing through the rapidly spreading but seemingly less pathogenic Omicron variant. The US High-Quality strategy (USHQ), which closely tracks movement in the SPDR S&P 500 ETF (SPY, approx. 90% correlation since inception), also had a strong month, with an outperformance of 0.49% relative to SPY.1 Since last quarter, strategy performance has been mostly in line with the US market (Chart 1), with modest downside protection and lower daily return volatility (Table 1), which are typical characteristics of the strategy.Returning to the most recent month of trading (December 2021), we are reminded that tech and health care continue to have a major influence on total returns given their weight in the US market. The USHQ portfolio was able to gain ground against SPY through outperformance in 8 out of 11 GICS Level 1 sectors, namely in tech and health care (Chart 2). Within SPY, mega-cap symbols continued to provide strong contributions2 with AAPL, TSLA, FB, MA, and UNH leading the pack. Downside impact was muted, with ADBE being the top detractor. The USHQ strategy had solid breadth across constituents, with a few holdings standing out in tech and health care. The top/bottom 10 contributors for the month of December are shown in Table 2A and Table 2B. Table 12021Q4 Statistics* At the current juncture, US equities are experiencing increased volatility due in part to a hawkish tone from the Federal Reserve. The latest set of FOMC minutes point to a mid-march liftoff date. This comes amid sustained inflationary pressures and a move towards maximum employment in the US. Not surprisingly, the market has corrected slightly against this backdrop. As of end-of-day January 11, 2022, USHQ is down -0.3% MTD vs -1.7% for SPY.Factor BreakdownIn this section we examine the current factor landscape for the USHQ portfolio, SPY, and the broad US equity universe.The current factor exposure for the USHQ portfolio and SPY is shown in Chart 3. It is up to date as of the latest portfolio rebalance (Jan 3, 2021). The methodology is similar to that used by the Factor Analyzer widget on the Equity Analyzer (EA) platform. We define the composite factor exposure as the difference between the portfolio or fund-weighted average factor score and the average score of our stock universe. In this case the stock universe consists of the top 1000 US stocks according to market cap. Composite factor scores are obtained from the EA platform and range from 0% to 100%.The portfolio will tend to have a positive factor exposure on most factors as it holds the top ranking stocks in each sector according to the BCA Score. The factor exposure of SPY will vary from month to month depending on the evolution of the market. In the ideal environment, the strategy should have positive BCA Score exposure relative to the market index. Practically speaking, this provides verification that the strategy is correctly tilted towards the factors we deem important for managing market risk.The values in Chart 4 can be interpreted as the difference between the dark green bars and light green bars in Chart 3. This month, we observe that the valuation gap between the portfolio and SPY has narrowed relative to last month. This was mainly due to a drop in the Value Score of USHQ, which can be explained by a significant price appreciation in the strategy's tech holdings. Increased exposure to Technicals for USHQ and SPY indicate that both are increasingly weighted towards firms with strong momentum over the past 12 months.When considering the broad US equity universe on an equal-weighted basis, it’s clear that the composite Value factor has experienced a resurgence over the past month (Chart 5). The BCA Score metric has remained robust over the same period, with the core model components outperforming on a long/short basis. The current factor landscape reflects a switch to an environment of rising interest rates, as seen by the movement of the 10-year Treasury yield. Based on a previous study of factor performance in different rate environments, the outlook for Quality factors remains strong, as we are currently in an environment of high3 and rising rates (Chart 6).Portfolio Constituents SummaryThis section provides information about the latest holdings in the portfolio as of last rebalance (Jan 3, 2021). The current sector composition is shown in Chart 7 with changes since last rebalance shown in parentheses. New positions in the portfolio are shown in Table 3A, and closed positions are shown in Table 3B. Movement of securities in and out of the portfolio is driven primarily by the level of the factor model ranking (BCA Score) at the time of rebalance.Specifically, positions are closed when the BCA Score drops below 70% and the Composite Macro Score is below 75%. The closed positions are replaced with high-ranking securities from the pool of top 1000 US stocks by market capitalization. Rebalancing occurs on the first trading day of each month. The number of securities in the portfolio currently sits at 55, with 5 stocks occupying each of the 11 GICS Level 1 sectors.Footnotes1 Calculated for the latest portfolio intra-rebalance period (2021-12-01 to 2022-01-03) using dividend-adjusted end-of-day pricing.2 Contribution defined as fund or portfolio-weighted return during the given month.3 As determined by our moving average (MA) cross indicators. Rates are considered “high” if the 3-month MA is above the 3-year MA.