Sectors

Highlights The (earnings) yield premium on tech stocks versus the 10-year bond yield is at its 2.5 percent lower threshold that has signalled four previous market fragilities. Additionally, the 65-day fractal structure of stocks versus bonds has collapsed, signalling a high probability of an exhaustion or correction over the next 65 days. Likewise, the 130-day fractal structure of bitcoin has also collapsed, signalling a high probability of an exhaustion or correction over the next 130 days. Bond yields are unlikely to go much higher; they are likely to go lower. Prefer utilities within the value segment, and prefer healthcare within the growth segment. Offices and bricks-and-mortar retail will never fully reopen. This will devastate the jobs market once the protection from government-funded furlough schemes winds down in 2021. Feature The pandemic will ease in 2021, and with it many of the restrictions on our lives. Yet when it comes to the economy and investment, the great reopening narrative for 2021 is misleading because the world economy has already largely reopened. We quickly learned that, with some adaptations, like working from home, and doing our shopping online, almost all economic activity can resume during a raging global pandemic. As a result, global profits have already rebounded very strongly (Chart of the Week). Chart of the WeekGlobal Profits Have Already Rebounded Very Strongly

Global Profits Have Already Rebounded Very Strongly

Global Profits Have Already Rebounded Very Strongly

Manufacturing is fully open. Construction is fully open. Industrial production is fully open. Finance and most services are fully open. Looking at the world’s two largest economies, China is already beyond its pre-pandemic levels of output (Chart I-2), while the US is a mere 0.9 percent below (based on the Atlanta Fed Nowcast of 2.6 percent growth in the fourth quarter)1 (Chart I-3). Chart I-2The Chinese Economy Has Already Rebounded

The Chinese Economy Has Already Rebounded

The Chinese Economy Has Already Rebounded

Chart I-3The US Economy Has Already ##br##Rebounded

The US Economy Has Already Rebounded

The US Economy Has Already Rebounded

Offices And Bricks-And-Mortar Retail Will Never Fully Reopen In the great reopening narrative, the end of the pandemic will allow the full reopening of offices, shops, restaurants, bars, travel and leisure. But will former office workers flock back to their offices full-time, or even majority-time? Will consumers flock back to bricks-and-mortar retailers? Will firms flock back to the same extent of business travel? Our high conviction answers are no, no, and no. The reason we will not go back to the pre-pandemic way of doing things is because we have found a better way of doing things. Obviously, we will relish our re-found ability to go on holiday and to meet our fellow humans in the flesh. But do we really need to meet our co-workers every day, or even most days? Do we really need to do our shopping in person every time, or even most times? Do we really need to visit the overseas office every quarter? In 2021 and beyond, we will continue to work, shop, and interact more remotely, not because a pandemic forces us to, but because it improves the quality of our personal and working lives. It improves our standard of living. In 2021 and beyond, we will continue to work, shop, and interact more remotely. Unfortunately, there will be collateral damage. As working from home becomes mainstream, the ecosystem of city centre bars, restaurants, and shops that rely on office workers will wither. This ecosystem’s large footprint can be illustrated by a remarkable fact: the pre-pandemic populations of both Manhattan and central London were 2 million people greater during the weekday daytime than during the night-time. Likewise, as online shopping becomes the default, bricks-and-mortar retailing will go into terminal decline. This is significant because retail employs 10 percent of all workers in the US and the UK, the majority in bricks-and-mortar retail outlets. In the same way, more online meetings and fewer business trips means less employment in the travel and accommodation sectors. The common thread connecting retail and accommodation and food services is that they produce relatively little output, but account for a lot of jobs – in fact, just 8 percent of output but 20 percent of all jobs (Table I-1). Table I-1Retail Plus Accommodation And Food Services Account For 8 Percent Of Output But 20 Percent Of Jobs

Stocks Are Vulnerable… And So Is Bitcoin

Stocks Are Vulnerable… And So Is Bitcoin

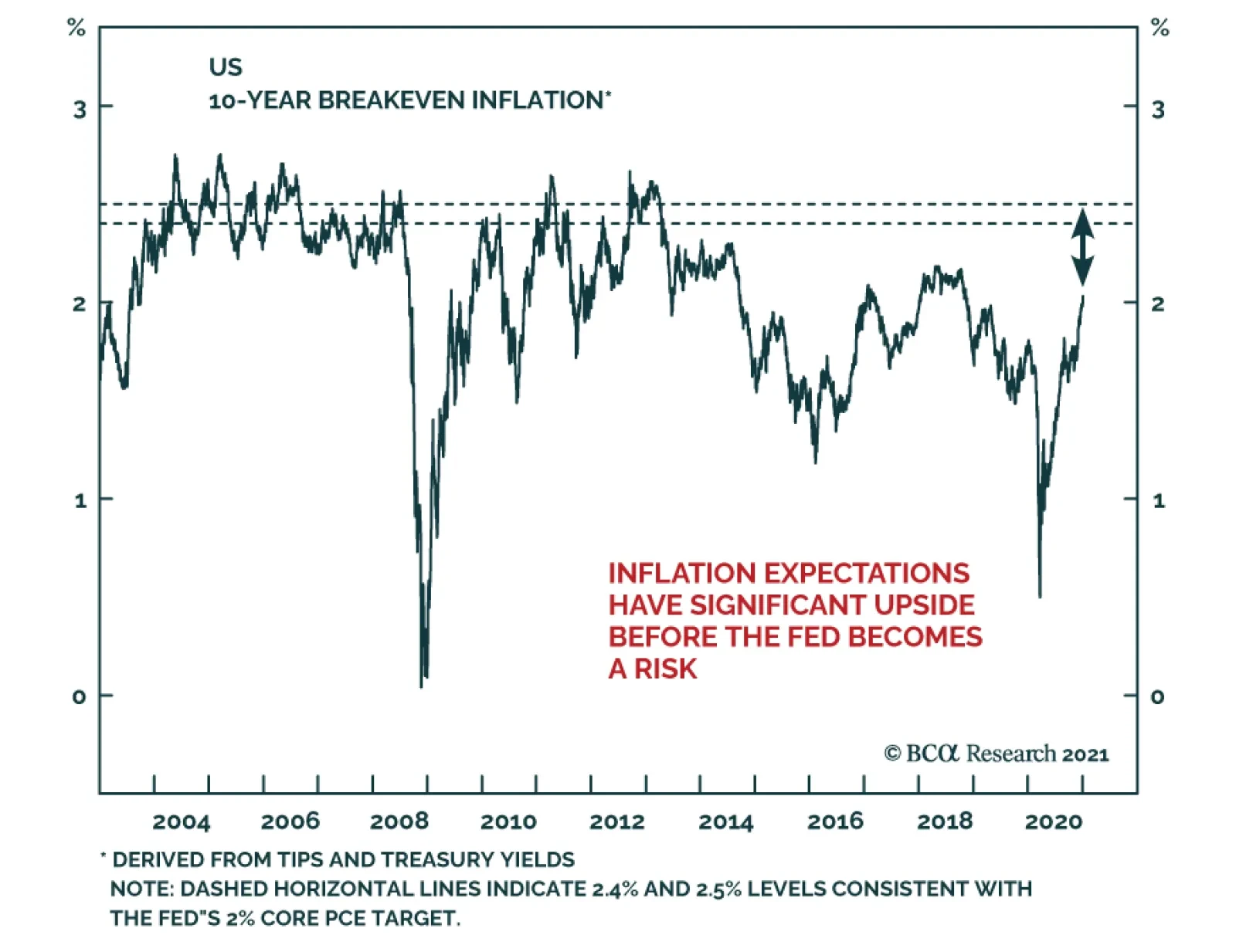

Hence, as these sectors wither, the good news is that the impact on economic output will be modest. The bad news is that the ultimate impact on the jobs market will be devastating. Crucially, this ultimate impact on the jobs market will only be felt once the protection from government-funded furlough schemes winds down in 2021. In time, a dynamic economy will redeploy the army of shop assistants, city centre bar and restaurant staff, and cabin crew into fast growing sectors such as healthcare and education. But a process that requires retraining and reskilling will take years not months. During this long adjustment, there is likely to be huge slack in developed economy labour markets. Given that central banks are now explicitly targeting labour market slack, these central banks will be forced to keep nominal bond yields at ultra-low levels for a very long time. The Near-Term Constraint On Bond Yields In the near term, there is an even greater force holding bond yields in check, and that force is something that central banks also explicitly target – financial stability. Higher bond yields would imperil financial stability. The global stock market is at an all-time high because valuations stand 25 percent higher than a year ago (Chart I-4). Valuations have surged because bond yields have collapsed (Chart I-5), but even relative to these ultra-low bond yields, technology sector valuations are now stretched. Chart I-4The Global Stock Market Is At An All-Time High Because Valuations Are 25 Percent Higher

The Global Stock Market Is At An All-Time High Because Valuations Are 25 Percent Higher

The Global Stock Market Is At An All-Time High Because Valuations Are 25 Percent Higher

Chart I-5Valuations Are 25 Percent Higher Because Bond Yields Have Collapsed

Valuations Are 25 Percent Higher Because Bond Yields Have Collapsed

Valuations Are 25 Percent Higher Because Bond Yields Have Collapsed

The (earnings) yield premium on tech stocks versus the 10-year bond yield is at its 2.5 percent lower threshold that has signalled four previous market fragilities. These previous market fragilities resulted in an exhaustion, or worse, a correction in the stock market in February 2018, October 2018, April 2019, and January 2020. Just as important, these points of fragility signalled that bond yields were approaching a major or minor peak (Chart I-6). Chart I-6Tech Stock Valuations Are Fragile

Tech Stock Valuations Are Fragile

Tech Stock Valuations Are Fragile

Hence, in the early part of 2021 at least, steer towards investments that will benefit from a backing down of bond yields. This means avoiding value stocks as an aggregate, because value cannot outperform growth unless bond yields are rising (Chart I-7). However, it also means avoiding growth stocks in aggregate as the fragility lies in tech stock valuations. Chart I-7Value Cannot Outperform Growth Unless Bond Yields Are Rising

Value Cannot Outperform Growth Unless Bond Yields Are Rising

Value Cannot Outperform Growth Unless Bond Yields Are Rising

A good strategy is to prefer utilities within the value segment, given that utilities benefit from lower bond yields (Chart I-8). And prefer healthcare within the growth segment, given the sector’s more reasonable valuation. Chart I-8Banks Cannot Outperform Utilities Unless Bond Yields Are Rising

Banks Cannot Outperform Utilities Unless Bond Yields Are Rising

Banks Cannot Outperform Utilities Unless Bond Yields Are Rising

Stocks Are Vulnerable… And So Is Bitcoin Manias occur in markets when marginal buyers keep flooding in at a higher and higher price. (Likewise, panics occur when marginal sellers keep flooding in at a lower and lower price.) The supply of marginal buyers fuelling the strong uptrend tends to come from longer-term investors who are uncharacteristically behaving like short-term momentum traders for fear of missing out on the rally. For example, an investor with a 130-day investment horizon shouldn’t buy because of a one-day price increase. If he does, then his investment horizon has shrunk to 1-day. In this example, the strong uptrend will run out of fuel when the 130-day investors who are fuelling it are all in. This is defined by the 130-day fractal structure of the investment collapsing, meaning that its 130-day fractal dimension has reached its lower bound. If someone now puts on a sell order, there are no more 130-day horizon investors available to be the marginal buyer at the current price. Having sucked in all the 130-day investors, an investor with an even longer horizon, say 260 days, must step in as the marginal buyer. The likely outcome is a price correction because the longer-term investor is likely to buy only when a lower price satisfies his value compass. The other possibility is that the 260-day investor joins the uptrend, becoming a marginal buyer at the current price, adding more fuel to the mania. This is the less likely outcome because the longer that an investor’s horizon is, the more faithful he is likely to be to his valuation compass. Nevertheless, sometimes the valuation compass goes awry because of structural shifts or massive intervention by policymakers, allowing the trend to continue. The above describes the basis of our proprietary fractal trading system. In a nutshell, when the fractal structure of an investment collapses, the probability of a trend reversal increases sharply, and the probability of a trend continuation decreases sharply. Right now, the 65-day fractal structure of stocks versus bonds has collapsed, signalling a high probability of an exhaustion or correction over the next 65 days (see final section). Likewise, the 130-day fractal structure of bitcoin has also collapsed, signalling a high probability of an exhaustion or correction over the next 130 days (Chart I-9). Chart I-9The 130-Day Fractal Structure Of Bitcoin Has Collapsed

Bitcoin

Bitcoin

To be clear, these rallies can continue uninterrupted if longer-term investors join the bandwagon. But this would require them to discard their valuation compasses. Hence, on balance, we think that this is the lower probability outcome. Also, to be clear, the long-term direction of both stocks versus bonds and bitcoin is up. The vulnerability we refer to is of a tactical pullback within a structural uptrend. An Excellent Year For The Fractal Trading System Among our most recent trades, overweight Portugal versus Italy achieved its 7 percent profit target, and underweight Australian construction materials (James Hardie, Lendlease, and Boral) achieved its 6 percent profit target. This takes the 2020 win ratio to a very pleasing 63 percent, comprising 18.4 winning trades versus 11 losing trades. Using a position size that delivers 2 percent for a win (and -2 percent for a loss), this equates to a 2020 return of 15 percent with a worst drawdown of -6 percent. By comparison, the MSCI All Country World index delivered a similar return of 17 percent but with a much more severe worst drawdown of -34 percent. 63 percent is a great win ratio. 63 percent is a great win ratio, but our aim is to reach 70 percent. To this end we are preparing several enhancements to the system which we will unveil in the coming weeks. Stay tuned. Fractal Trading System* As already discussed, we are targeting a tactical pullback in the MSCI All Country World Index versus the 30-year T-bond. The profit-target and symmetrical stop-loss are set at 5.8 percent. Chart I-10

MSCI All-Country World Vs. 30-Year T-Bond

MSCI All-Country World Vs. 30-Year T-Bond

The rolling 12-month win ratio now stands at 63 percent. When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 The GDP rebound creates a dissonance. If GDP is indicating a largely recovered economy, but our lives feel far from normal, is GDP really a good measure or objective for our wellbeing? We will leave a deeper discussion of this to a later date. Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Dear Client, I am writing as the US Capitol goes under lockdown to tell you about a new development at BCA Research. Since you are a subscriber of Geopolitical Strategy, we wanted you to be the first to know. This month we are launching a new sister service, US Political Strategy, which will expand and deepen our coverage of investment-relevant US domestic political risks and opportunities. Over the past decade, we at Geopolitical Strategy have worked hard to craft an analytical framework that incorporates policy insights into the investment process in a systematic and data-dependent way. We have learned a lot from your input and have refined our method, while also building new quantitative models and indicators to supplement our qualitative, theme-based coverage. While our method served us well in 2020, the frantic US election cycle often caused clients to lament that US politics had begun to crowd out our traditional focus on truly global themes and trends. We concurred. Therefore we have decided to expand our team and deepen our coverage. With a series of new hires, we are now better positioned to provide greater depth on US markets in US Political Strategy while redoubling our traditional global sweep in the pages of Geopolitical Strategy. Going forward, US Political Strategy will cover executive orders, Capitol Hill, federal agencies, regulatory risk, the Supreme Court, emerging socioeconomic trends, and their impacts on key US sectors and assets. It will be BCA Research’s newest premium investment strategy service and will include the full gamut of weekly reports, special reports, webcasts, and client conferences. Meanwhile Geopolitical Strategy will return to its core competency of geopolitics writ large – including the US in its global impacts, but diving deeper into the politics and markets of China, Europe, India, Japan, Russia, the Middle East, and select emerging markets. Both strategies will utilize our proprietary analytical framework, which relies on data-driven assessments of the “checks and balances” that shape policy outcomes (i.e. comparing constraints versus preferences). As you know best, we are agnostic about political parties, transparent about conviction levels and scenario probabilities, and solely focused on getting the market calls right. To this end, we offer you a complimentary trial subscription of US Political Strategy. We aim to become an integral part of your work flow – separating the wheat from the chaff in the political and geopolitical sphere so that you can focus on honing your investment process. We know you will be pleased to see Geopolitical Strategy return to its roots – and we hope you will consider diving deeper with us into US politics and markets. We look forward to hearing from you. Happy New Year! All very best, Matt Gertken, Vice President BCA Research The outgoing Trump administration is powerless to stop the presidential transition and the US military and security forces will not participate in any “coup.” Investors should buy the dip if social instability affects the markets between now and President-elect Joe Biden’s Inauguration Day. Democrats have achieved a sweep of US government with two victories in Georgia’s Senate election. The Biden administration is no longer destined for paralysis. Investors no longer need fear a premature tightening of US fiscal policy. Fiscal thrust will expand by around 6.9% of GDP more than it otherwise would have in FY2021 and contract by 12.3% of GDP in FY2022. Democrats will partly repeal the Trump tax cuts to pay for new spending programs, including an expansion and entrenchment of Obamacare. Big Tech is the most exposed to the combination of higher corporate taxes and inflation expectations. Investors should go long risk assets and reflation plays on a 12-month basis. We recommend value over growth stocks, materials over tech, TIPS over nominal treasuries, infrastructure plays, and municipal bonds. The special US Senate elections in Georgia produced a two-seat victory for Democrats on January 5 and have thus given the Democratic Party de facto control of the Senate.Financial markets have awaited this election with bated breath. The “reflation trade” – bets on economic recovery on the back of ultra-dovish monetary and fiscal policy – had taken a pause for the election. There was a slight setback in treasury yields and the outperformance of cyclical, small cap, and value stocks, which rallied sharply after the November 3 general election (Chart 1). The Democratic victory ensures that US corporate and individual taxes will go up – triggering a one-off drop in earnings per share of about 11%, according to our US Equity Strategist Anastasios Avgeriou (Table 1). But it also brings more proactive fiscal policy. Since the Democrats project larger new spending programs financed by tax hikes, the big takeaway is that the US economic recovery will gain momentum and will not be undermined by premature fiscal tightening. Chart 1Markets Will Look Through Unrest To Reflation

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Table 1What EPS Hit To Expect?

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 2Democrats Won Georgia Seats, US Senate

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Republicans Snatch Defeat From Jaws Of Victory The results of the Georgia runoffs, at the latest count, are shown in Chart 2. Republican Senator David Perdue has not yet officially lost the race, as votes are still being tallied, but he trails his Democratic challenger Jon Ossoff by 16,370 votes. This is a gap that is unlikely to be changed by subsequent vote disputes or recounts (though it is possible and the results are not yet declared as we go to press). President-elect Joe Biden only lost 1,274 votes to President Trump when ballots were recounted by hand in November. The Democratic victory offers some slight consolation for opinion pollsters who underestimated Republicans in the general election in certain states. Opinion polls had shown a dead heat in both of Georgia’s races, with Republican Senators Perdue and Kelly Loeffler deviating by 1.4% and 0.4% respectively from their support rate in the average of polls in December. Democratic challengers Jon Ossoff and Raphael Warnock differed by 1.3% and 2.3% from their final polling (Charts 3A & 3B). Chart 3AOpinion Pollsters Did Better …

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 3B… In Georgia Runoffs

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

By comparison, in the November 3 general election, polls underestimated Perdue by 1.3% and overestimated Warnock by 5.3% (Chart 4). On the whole, the election shows that state-level opinion polling can improve to address new challenges. Our quantitative Senate election model had given Republicans a 78% chance of winning Georgia. This they did in the first round of the election, but conditions have changed since November 3, namely due to President Trump’s refusal to concede the election after the Electoral College voted on December 14.1 Our model is based on structural factors so it did not distinguish between the two Senate candidates in the same state. For the whole election, the model predicted that Democrats would win a net of three seats, resulting in a Republican majority of 51-49. Today we see that the model only missed two states: Maine and Georgia. But Georgia has made all the difference, with the result to be 50-50, for Vice President Kamala Harris to break the tie (Chart 5). Chart 4Ossoff In Line With Polls, Warnock Slightly Beat

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 5Our Quant Model Missed Maine And Georgia – And Georgia Carries Two Seats To Turn The Senate

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

COVID-19 likely took a further toll on Republican support in the interim between the two election rounds. The third wave of the COVID-19 pandemic has not peaked in the US or the Peach State. While the number of cases has spiked in Georgia as elsewhere, the number of deaths has not yet followed (Chart 6). Chart 6COVID-19 Surged Since November

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Lame Duck Trump Risk Before proceeding to the policy impacts of the apparent Democratic sweep of both executive and legislative branches, a word must be said about the presidential transition and President Trump’s final 14 days in office. First, the Joint Session of Congress to count the Electoral College ballots to certify the election of the new US president has been interrupted as we go to press. There is zero chance that protesters storming the proceedings will change the outcome of the election. The counting of the electoral votes can be interrupted for debate; it will be reconvened. Disputes over the vote could theoretically become meaningful if Republicans controlled both the House and the Senate, as the combined voice of the legislature could challenge the legitimacy of a state’s electoral votes. But today the Republicans only control the Senate, and while some will press isolated challenges, based on legal disputes of variable merit, these challenges will not gain traction in the Senate let alone in the Democratic-controlled House. What did the US learn from this controversial election? US political polarization is reaching extreme peaks which are putting strain on the formal political system, but Trump lacks the strength in key government bodies to overturn the election. Second, there was no willingness of state legislatures to challenge their state executives on the vote results. This has to do with the evidence upon which challenges could be lodged, but there is also a built-in constraint. Any state legislature whose ruling party opposes the popular result will by definition put its own popular support in jeopardy in the next election. Third, the Supreme Court largely washed its hands of state-level disputes settled by state-level courts. Historically, the Supreme Court never played a role in presidential elections. The year 2000 was an exception, as the high court said at the time. The 2020 election has established a high bar for any future Supreme Court involvement, though someday it will likely be called on to weigh in. Hysteria regarding the conservative leaning on the court – which is now a three-seat gap – was misplaced. The three Supreme Court justices appointed by Trump took no partisan or interventionist role. Nevertheless, the court’s conservative leaning will be one of the Trump administration’s biggest legacies. The marginal judge in controversial cases is now more conservative and will take a larger role given that Democrats now have a greater ability to pass legislation by taking the Senate. President Trump is still in office for 14 days. There is zero chance of a successful military coup or anything of the sort in a republic in which institutions are strong and the military swears allegiance to the constitution. Attempts to oppose the Electoral College and Congress will be opposed – and ultimately they will be met with an overwhelming reassertion of the rule of law. All ten of the surviving secretaries of defense of the United States have signed an open letter saying that the election results should no longer be resisted and that any defense officials who try to involve the military in settling electoral disputes could be criminally liable.2 With Trump’s options for contesting the election foreclosed, he will turn to signing a flurry of executive orders to cement his legacy. His primary legacy is the US confrontation with China, so he will continue to impose sanctions on China on the way out, posing a tactical risk to equity prices. The business community will be slow to comply, however, so the next administration will set China policy. There is a small possibility that Trump will order economic or even military action against Iran or any other state that provokes the United States. But Trump is opposed to foreign wars and the bureaucracy would obstruct any major actions that do not conform with national interests. Basically, Trump’s final 14 days may pose a downside risk to equities that have rallied sharply since the November 9 vaccine announcement but we are long equities and reflation plays. Sweeps Just As Good For Stocks As Gridlock The balance of power in Congress is shown in Chart 7. The majorities are extremely thin, which means that although Democrats now have control, there will remain high uncertainty over the passage of legislation, at least until the 2022 midterm elections. Investors can now draw three solid conclusions about the makeup of US government from the 2020 election: The White House’s political capital has substantially improved – President-elect Joe Biden no longer faces a divided Congress. He won by a 4.5% popular margin (51.4% of the total), bringing the popular and electoral vote back into alignment. He will have a higher net approval rating than Trump in general, and household sentiment, business sentiment, and economic conditions will improve from depressed, pandemic-stricken levels over the course of his term. The Senate is evenly split but Democrats will pass some major legislation – Thin margins in the Senate make it hard to pass legislation in general. However, the budget reconciliation process enables laws to pass with a simple majority if they involve fiscal matters. Hence, Democrats will be able to legislate additional COVID relief and social support that they were not able to pass in the end-of-year budget bill. They can pass a reconciliation bill for fiscal 2022 as well. They will focus on economic recovery followed by expanding and entrenching the Affordable Care Act (Obamacare). We fully expect a partial repeal of Trump’s Tax Cut and Jobs Act, if not initially then later in the year. Democrats only have a five-seat majority in the House of Representatives – Democrats will vote with their party and thus 222 seats is enough to maintain a working majority. But the most radical parts of the agenda, such as the Green New Deal, will be hard to pass. Chart 7Democrats Control Both Houses

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

With the thinnest possible margin, the Senate has a highly unreliable balance of power. Table 2 shows top three Republicans and Democrats in terms of age, centrist ideology, and independent mentality. Four senators are above the age of 85 – they can vote freely and could also retire or pass away. Centrist and maverick senators will carry enormous weight as they will provide the decisive votes. The obvious example is Senator Joe Manchin of West Virginia, who has opposed the far-left wing of his party on critical issues such as the Green New Deal, defunding the police, and the filibuster. Table 2The Senate Will Hinge On These Senators

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

The Democrats could conceivably muster the 51 votes to eliminate the filibuster, which requires a 60-vote majority to pass most legislation, but it will be very difficult. Senators Dianne Feinstein (D, CA), Angus King (I, ME), Kyrsten Sinema (D, AZ), Jon Tester (D, MT), and Manchin are all skeptical of revoking this critical hurdle to Senate legislation.3 We would not rule it out, however. The US has reached a point of “peak polarization” in which surprises should be expected. By the same token, Republican Senators Lisa Murkowski and Susan Collins often vote against their party. Collins just won yet another tough race in Maine due to her ability to bridge the partisan gap. There are also mavericks like Rand Paul – and Ted Cruz will have to rethink his populist strategy given his thin margins of victory and the Trump-induced Republican defeat in the South. Not shown are other moderates who will be eager to cross the political aisle, such as Senator Mitt Romney of Utah. None of the above means Democrats will fail to raise taxes. All Democrats voted against Trump’s Tax Cut and Jobs Act, which did not end up being popular or politically beneficial for the Republicans. The Democratic base is fired up and mobilized by Trump to pursue its core agenda of increasing the government role in US society and the economy and redressing various imbalances and disparities. This requires revenue, especially if it is to be done with only 51 votes via the budget reconciliation process. The two Democratic senators from Arizona are vulnerable, but they will toe the party line because Trump and the GOP were out of step with the median voter. Moreover, Arizonians voted for higher taxes in a state ballot measure in November. Since 1980, gridlocked government has resulted in higher average annual returns on the S&P500. But since 1949, single-party sweeps have slightly edged out gridlocked governments in stock returns, though the results are about the same (Chart 8). The point is that gridlock makes it hard for government to get big things done. Sometimes that is positive for markets, sometimes not. The macro backdrop is what matters. The Federal Reserve is unlikely to start tightening until late 2022 at earliest and fiscal thrust in 2021-22 will be more expansionary now that the Democrats have control of the Senate. This policy backdrop is negative for the dollar and positive for risk assets, especially equity sectors that will suffer least from impending corporate tax hikes, such as energy, industrials, consumer staples, materials, and financials. Chart 8Sweeps Don’t Always Underperform Gridlock

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Meanwhile, Biden will have far less trouble getting his cabinet and judicial appointments through the Senate (Appendix). His appointees so far reflect his desire to return the US to “rule by experts,” as opposed to Trump’s disruptive style of personal rule. Investors will cheer the return to technocrats and predictable policymaking even if they later relearn that experts make gigantic mistakes too. Fiscal Policy Outlook The critical feature of the Trump administration was the COVID-19 pandemic, which sent the US budget deficit soaring to World War II levels relative to GDP. In the coming years, the change in the budget deficit (fiscal thrust) will necessarily be negative, dragging on growth rates (Chart 9). Fiscal policy determines how heavy and abrupt that drag will be. Chart 9US Budget Deficit Surged – Pace Of Normalization Matters

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 10 presents four scenarios that we adjusted based on data from the Congressional Budget Office. The baseline would see an extraordinary 6.7% of GDP contraction in the budget deficit that would kill the recovery, which the Georgia outcome has now rendered irrelevant. The “Republican Status Quo” scenario is now the minimum. Chart 10Democratic Sweep Suggests Big Fiscal Thrust In FY2021 And Less Contraction FY2022

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

The “Democratic Status Quo” scenario assumes that the $600 per household rebate will be increased to $2,000 per family and that the remaining $2.5 trillion of the Democrats’ proposed HEROES Act will be enacted. The “Democratic High” scenario adds Biden’s $5.6 trillion policy agenda on top of the Democratic status quo, supercharging the economic recovery with a fiscal bonanza. Biden will not achieve all of this, so the reality will lie somewhere between the solid blue and dotted blue lines. This Democratic status quo implies a 6.9% of GDP expansion of the deficit in FY2021. It also implies that the deficit will contract by 12.3% of GDP in FY2022, instead of 13.5% in the Republican status quo scenario. The economic recovery will be better supported. So, too, will the Fed’s timeline for rate hikes – but the Fed’s new strategy of average inflation targeting shows that it is targeting an inflation overshoot. So the threat of Fed liftoff is not immediate. The longer the extraordinary fiscal largesse is maintained, the greater the impact on inflation expectations and the more upward pressure on bond yields (Chart 11). Big Tech will be the one to suffer while Big Banks, industrials, materials, and energy will benefit. Chart 11Bond Bearish Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Our US Political Risk Matrix There is no correlation between fiscal thrust and equity returns. This is true whether we consider the broad market, cyclicals/defensives, value/growth stocks, or small/large caps (Chart 12). Normally, fiscal thrust surges when recessions and bear markets occur, leading to volatility in asset prices. However, in the new monetary policy context, the risk is to the upside for the above-mentioned sectors, styles, and segments. Looking at sector performance before and after the November 3 election and November 9 vaccine announcement, there has been a clear shift from pandemic losers to pandemic winners. Big Tech and Consumer Discretionary (Amazon) thrived during the period before the vaccine, while value stocks (industrials, energy, financials) suffered the most from the lockdowns. These trends have reversed, with energy and financials outperforming the market since November (Chart 13). The Biden administration poses regulatory risks for Big Oil and arguably Big Banks, but these will come into play after the market has priced in economic normalization and the emerging consensus in favor of monetary-fiscal policy coordination, which is very positive for these sectors. Chart 12Fiscal Thrust Not Correlated With Stocks

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Chart 13Energy And Financials Turned Around With Vaccine

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

In the case of energy, as stated above, the Biden administration will still struggle to get anything resembling the Green New Deal approved in Congress. Nevertheless, environmental regulation will expand and piecemeal measures to promote research and development, renewables, electric vehicles, and other green initiatives may pass. Large cap energy firms are capable of adjusting to this kind of transition. Coal companies are obviously losers. In the case of financials, Biden’s record is not unfriendly to the financial industry. His nominee for Treasury Secretary, former Fed Chair Janet Yellen, approved of the relaxation of some of its more stringent financial regulations under the Trump administration. Big Banks are no longer the target of popular animus like they were after the 2008 financial crisis – in that regard they have given way to Big Tech. Our US Investment Strategist Doug Peta argues that the Democratic sweep will smother any gathering momentum in personal loan defaults, which would help banks outperform the broad market. Biden’s regulatory approach to Big Tech will be measured, as the Obama administration’s alliance with Silicon Valley persists, but tech stands to suffer the most from higher taxes, especially a minimum corporate tax rate. With a unified Congress, it is also now possible that new legislation could expand tech regulation. There is a bipartisan consensus emerging on tech regulation so Republican votes can be garnered. Tech thrives on growth-scarce, disinflationary environments whereas the latest developments are positive for inflation expectations. In the recent lead-up to the Georgia vote, industrials, financials, and consumer discretionary stocks have not benefited much, even though they should (Chart 14). These are investment opportunities. Chart 14Upside For Energy And Financials Despite Regulatory Risk

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

In our Political Risk Matrix, we establish these views as our baseline political tilts, to be applied to the BCA Research House View of our US Equity Strategy. The results are shown in Table 3. When equity sectors become technically stretched, the political impacts will become more salient. Table 3US Political Risk Matrix

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Investment Takeaways Over the past few years our sister Geopolitical Strategy has written extensively about “Civil War Lite,” “Peak Polarization,” and contested elections in the United States. We will dive deeper into these themes and issues in forthcoming reports, but for now suffice it to say that extremist events will galvanize the majority of the nation behind the new administration while also driving politicians of both stripes to use pork-barrel spending to try to stabilize the country. Congress will err on the side of providing too much fiscal stimulus just as surely as the Fed is bent on erring on the side of providing too much monetary stimulus. That means reflation, which will ultimately boost stocks in 2021. We also expect stocks to outperform government bonds, at least on a tactical 3-6 month timeframe. As the above makes clear, we prefer value stocks over growth stocks. Specifically we favor cyclical plays like materials over the big five of Google, Apple, Amazon, Microsoft, and Facebook. An infrastructure bill was one of the few legislative options for the Biden administration under gridlock, now it is even more likely. Infrastructure is popular and both presidential candidates competed to see who could offer the bigger plan. Moreover, what Biden cannot achieve under the rubric of climate policy he can try to achieve under the rubric of infrastructure. The BCA US Infrastructure Basket correlates with the US budget deficit as well as growth in China/EM and we recommend investors pursue similar plays. In the fixed income space, Treasury inflation protected securities (TIPS) are likely to continue outperforming nominal, duration-matched government bonds. Our US Bond Strategist Ryan Swift is on alert to downgrade this recommendation, but the change in US government configuration at least motivates a tactical overweight in TIPS. The chances of US state and local governments receiving fiscal support – previously denied by the GOP Senate – has increased so we will also go long municipal bonds relative to treasuries. Matt Gertken Vice President US Political Strategy mattg@bcaresearch.com Appendix Table A1Biden’s Cabinet Position Appointments

Buy Reflation Plays On Georgia’s Blue Sweep

Buy Reflation Plays On Georgia’s Blue Sweep

Footnotes 1 Perdue defeated Ossoff on November 3 but fell short of the 50% threshold to avoid a second round; meanwhile the cumulative Republican vote in the multi-candidate special election outnumbered the cumulative Democratic vote on November 3. 2 Ashton Carter, Dick Cheney, William Cohen, et al, “All 10 living former defense secretaries: Involving the military in election disputes would cross into dangerous territory,” Washington Post, January 3, 2021, washingtonpost.com. 3 Jordain Carney, “Filibuster fight looms if Democrats retake Senate,” The Hill, August 25, 2020, thehill.com.

According to BCA Research’s Global Asset Allocation Strategy service, a rapid rollout of vaccines means that the economy should be on track to return to near-normality by the second half of 2021. Therefore, the key thing for investors to think about is what…

In our "Millennials Are Not Coming Of Age; They Are Already Here” Special Report where we first created the BCA Millennial Basket we mentioned that “we would not hesitate to add other sharing economy stocks, including Airbnb and Uber, to this basket should they become investable.” We did eventually add UBER to the basket, which replaced FB on December 13, 2019. Today, in light of the recent Airbnb IPO, we are compelled to make another substitution. We are banking all the TSLA gains and removing it from our millennial basket as the S&P is adding it in the S&P 500. And, we are reinvesting the funds into ABNB and rebalance all the stocks in the millennial basket back to a 10% weight for each of the constituents. The main reason behind the substitution is because the easy money has already been made in TSLA, but not in ABNB (Chart 1). In other words, now that TSLA is worth as much as all the other car manufacturers in the world put together, it is difficult to continue rising at the same frenetic pace of the past few years. In contrast, were ABNB to follow a similar trajectory and rise to a similar stardom to TSLA, then there is a long runway ahead for this new IPO. Our Millennial Basket is currently up 137% in absolute terms, and 77% in relative to S&P 500 terms, since the June 11 2018 inception (Chart 2). Recently, we also instituted an 18% rolling stop that we plan to obey it. Chart 1

Replace TSLA with ABNB In The Millennial Equity Basket

Replace TSLA with ABNB In The Millennial Equity Basket

Chart 2

Replace TSLA with ABNB In The Millennial Equity Basket

Replace TSLA with ABNB In The Millennial Equity Basket

Bottom Line: ABNB takes TSLA’s seat in our Millennial Basket.

Many investors feel that the Phillips Curve has failed to predict weak inflation over the past decade. But this perception is due to a singular focus on the economic slack component of the modern-day version of the curve to the exclusion of inflation expectations, and a failure to fully consider the lasting impact of sustained periods of a negative output gap on those expectations. In addition, many investors tend to downplay the long-term balance sheet impact of two episodes of excesses and savings/capital misallocations on the relationship between the stance of monetary policy and the output gap, via a persistently negative shock to aggregate demand and a reduced sensitivity of economic activity to interest rates. The COVID-19 pandemic was certainly a major economic shock. But for now, it seems like this was a sharp income statement recession, not a balance-sheet recession. This fact, along with lower odds of negative supply-side shocks and several structural factors, suggest that inflation will be higher over the next ten years than it has over the past decade. Investors looking to protect against potentially higher inflation should look primarily to commodities, cyclical stocks, and US farmland. Gold is likely to remain well supported over the coming few years, but rich valuation suggests the long-term outlook for the yellow metal is poor. A hybrid TIPS/currency portfolio has historically been strongly correlated with the price of gold, and may provide investors with long-term protection against inflation – at a better price. Introduction Chart II-1A Surge In Long-Dated Inflation Expectations

A Surge In Long-Dated Inflation Expectations

A Surge In Long-Dated Inflation Expectations

The pandemic, and the corresponding fiscal and monetary response is challenging the low-inflation outlook of many market participants. Chart II-1 highlights that long-dated market-based inflation expectations have surged past their pre-COVID levels after collapsing to the lowest-ever level in March. The shift in thinking about inflation has partly been a response to an extraordinary rise in government spending in many countries. But Chart II-1 shows that long-dated expectations in the US were mostly trendless from April to June as Federal support was distributed, and instead rose sharply in July and August in the lead-up to the Fed’s official shift to an average inflation targeting regime. This new dawn for US monetary policy has been prompted not just by the pandemic, but also by the extended period of below-target inflation over the past decade. In this report, we review how the past ten-year episode of low inflation can be successfully explained through the lens of the expectations-augmented (i.e. “modern-day”) Phillips Curve. Many investors fail to fully appreciate the impact that inflation expectations have on driving actual inflation, as well as the cumulative impact of two major capital and savings misallocations over the past 25 years on the responsiveness of demand to interest rates and on the level of inflation expectations. Using the modern-day Phillips Curve as a guide, we present several reasons in favor of the view that inflation will be higher over the next decade than over the past ten years. Finally, we conclude with an assessment of several ways for investors to protect their portfolios from rising inflation. Revisiting The “Modern-Day” Phillips Curve The original Phillips Curve, as formulated by New Zealand economist William Phillips in the late 1950s, described a negative relationship between the unemployment rate and the pace of wage growth. Given the close correlation between wage and overall price growth at the time, the Phillips Curve was soon extended and generalized to describe an inverse relationship between labor market slack and overall price inflation. Chart II-2Rising Unemployment And Inflation Challenged The Original Phillips Curve

Rising Unemployment And Inflation Challenged The Original Phillips Curve

Rising Unemployment And Inflation Challenged The Original Phillips Curve

However, the experience of rising inflation alongside high unemployment from the late 1960s to the late 1970s underscored that prices are also importantly determined by inflation expectations and shocks to the supply-side of the economy (Chart II-2). In the 1980s and 1990s, the Federal Reserve’s success at reigning in inflation was achieved not only by raising interest rates to punishingly high levels, but also by sharply altering consumer, business, and investor expectations about future prices. The experience of the late 1960s and 1970s led to a revised form of the Phillips Curve, dubbed the “expectations-augmented” or “modern” version. As an equation, the modern Phillips Curve is described today by Fed officials, in terms of core inflation, as follows: πct = β1πet + β2πct-1 + β3πct-2 - β4SLACKt + β5IMPt + εt where: πct = Core inflation today πet = Expectations of inflation πct-n = Lagged core inflation SLACKt = Slack in the economy IMPt = Imported goods prices εt = Other shocks to prices Described verbally, this framework suggests that “economic slack, changes in imported goods prices, and idiosyncratic shocks all cause core inflation to deviate from its longer-term trend that is ultimately determined by long-run inflation expectations.1” This framework can easily be extended to headline inflation by adding changes in food and energy prices. In most formal models of the economy in use today, the modern Phillips Curve is combined with the New Keynesian demand function to describe business cycles: Yt = Y*t – β(r-r*) + εt where: Yt = Real GDP Y*t = Real potential GDP r = The real interest rate r* = The neutral rate of interest εt = Other shocks to output This equation posits that differences in the real interest rate from its neutral level, along with idiosyncratic shocks to demand, cause real GDP to deviate from potential output. Abstracting from import prices and idiosyncratic shocks, these two equations tell a simple and intuitive story of how the economy generally works: The stance of monetary policy determines the output gap and, The output gap, along with inflation expectations, determine inflation. The Modern-Day Phillips Curve: The Pre-2000 Experience This above view of inflation and demand was strongly accepted by investors before the 2008 global financial crisis, but the decade-long period of generally below-target inflation has caused a crisis of faith in the idea of the Phillips Curve. Charts II-3 and II-4 show the historical record of the New Keynesian demand function and the modern-day Phillips Curve, using five-year averages of the data in question to smooth out the impact of short-term and idiosyncratic effects. We use nominal GDP growth as our long-run proxy for the neutral rate of interest,2 the US Congressional Budget Office’s (CBO) estimate of potential GDP to determine the output gap, and a proprietary measure of inflation expectations based on an adaptive expectations framework3 (Chart II-5). Chart II-3With Just Two Exceptions, Monetary Policy Strongly Explained Demand Before 2000

With Just Two Exceptions, Monetary Policy Strongly Explained Demand Before 2000

With Just Two Exceptions, Monetary Policy Strongly Explained Demand Before 2000

Chart II-4Similarly, Pre-2000 The Output Gap Generally Explained Unexpected Inflation

Similarly, Pre-2000 The Output Gap Generally Explained Unexpected Inflation

Similarly, Pre-2000 The Output Gap Generally Explained Unexpected Inflation

Chart II-3 shows that until 1999, the stance of monetary policy was highly predictive of the output gap over a five-year period, with just two exceptions where major structural forces were at play: the late 1970s, and the second half of the 1990s. In the case of the former, the disruptive effect of persistently high inflation negatively impacted output growth despite easy monetary policy, and in the latter case, economic activity was modestly stronger than what interest rates would have implied due to the beneficial impact of the technologically-driven productivity boom of that decade. Similarly, Chart II-4 shows that until 1999 there was a good relationship between the output gap and the deviation in inflation from expectations, again with the late 1970s and late 1990s as exceptions. Along with the beneficial supply-side effects of the disinflationary tech boom, persistent import price weakness (via dollar strength) seems to have also played a role in suppressing inflation in the late 1990s (Chart II-6). Chart II-5The Expectations Component Of The Modern Phillips Curve, Visualized

The Expectations Component Of The Modern Phillips Curve, Visualized

The Expectations Component Of The Modern Phillips Curve, Visualized

Chart II-6A Strong Dollar Also Played A Role In Suppressing Inflation During The 1990s

A Strong Dollar Also Played A Role In Suppressing Inflation During The 1990s

A Strong Dollar Also Played A Role In Suppressing Inflation During The 1990s

The Modern-Day Phillips Curve Post-2000 Following 2000, deviations between the monetary policy stance, the output gap, and inflation become more prominent, particularly after 2008. As we will illustrate below, these deviations are more apparent on the demand side. In the case of inflation, the question should be why inflation was not even lower in the years immediately following the global financial crisis. On both the demand and inflation side, these deviations are explainable, and in a way that helps us determine future inflation. Charts II-7 and II-8 show the same series as in Charts II-3 and II-4, but focused on the post-2000 period. From 2000-2007, Chart II-8 shows that the relationship between the output gap and the deviation in inflation from expectations was not particularly anomalous. The output gap was negative from the end of the 2001 recession until the beginning of 2006, and inflation was correspondingly below expectations on average for the cycle. Chart II-7Post-2000, The Output Gap Decoupled From The Monetary Policy Stance

Post-2000, The Output Gap Decoupled From The Monetary Policy Stance

Post-2000, The Output Gap Decoupled From The Monetary Policy Stance

Chart II-8Since The GFC, The Real Mystery Is Why Inflation Has Been So Strong

Since The GFC, The Real Mystery Is Why Inflation Has Been So Strong

Since The GFC, The Real Mystery Is Why Inflation Has Been So Strong

Chart II-7 shows that the anomaly during that cycle was in the relationship between the output gap and the stance of monetary policy. Monetary policy was the easiest it had been in two decades, yet the output gap was negative for several years following the recession. Larry Summers pointedly cited this divergence in his revival of the secular stagnation theory in November 2013, arguing that it was strong evidence that excess savings were depressing aggregate demand via a lower neutral rate of interest and that this effect pre-dated the financial crisis. Why was demand so weak during that period? Chart II-9 compares the annualized per capita growth in the expenditure components of GDP during the 2001-2007 expansion to the 1991-2001 period. The chart shows that all components of GDP were lower than during the 1991-2001 period, with investment – the most interest rate sensitive component of GDP – showing up as particularly weak. On the surface, this supports the idea of structural factors weighing heavily on the neutral rate, rendering monetary policy less easy than investors would otherwise expect. But Chart II-9 treats the 2001-2007 years as one period, ignoring what happened over the course of the expansion. Chart II-10 repeats the exercise shown in Chart II-9 from Q1 2001 to Q3 2005, and highlights that the annualized growth in per capita residential investment was much stronger than it was during the 1991-2001 period – and nonresidential fixed investment was much weaker. Spending on goods was roughly the same, which is impressive considering that the late 1990s experienced a productivity boom and robust wage growth. All the negative contribution to growth from residential investment during the 2001-2007 expansion came after Q3 2005, as the housing market bubble burst in response to rising interest rates. In short, Chart II-10 highlights that there was a strong relationship between easy monetary policy and the demand for housing, but that this was not true for the corporate sector. Chart II-9Looking At The Whole 2001-2007 Period, Investment Was Extremely Weak

January 2021

January 2021

Chart II-10Housing Absolutely Responded To Easy Monetary Policy

January 2021

January 2021

Explaining Weak CAPEX Growth In The Early 2000s This leads us to ask why CAPEX was so weak during the 2001-2007 period. In addition to changes in interest rates, business investment is strongly influenced by expectations of consumer demand and corporate profitability. Chart II-11 shows that real nonresidential fixed investment and as-reported earnings moved in lockstep during the period, and that this delayed corporate-sector recovery also impacted the pace of hiring. Weak expectations for consumer spending do not appear to be the culprit. Chart II-12 highlights that while real personal consumption expenditure growth fell during the recession, spending did not contract (as it had done during the previous recession) and capital expenditures fell much more than what real PCE would have implied. Chart II-11Post-2001, Persistently Weak Profits Led To Weak Investment And Jobs Growth

Post-2001, Persistently Weak Profits Led To Weak Investment And Jobs Growth

Post-2001, Persistently Weak Profits Led To Weak Investment And Jobs Growth

Chart II-12CAPEX Was Much Weaker In 2002 Than Justified By Consumer Spending

CAPEX Was Much Weaker In 2002 Than Justified By Consumer Spending

CAPEX Was Much Weaker In 2002 Than Justified By Consumer Spending

Instead, persistently weak CAPEX in the early 2000s appears to be best explained by the damaging impact of corporate excesses that built up during the dot-com bubble. The Sarbanes-Oxley Act of 2002 was passed in response to a series of corporate accounting frauds that came to light in the wake of the bubble, but in many cases had been occurring for several years. Chart II-13 highlights that widespread write-offs badly impacted earnings quality and the growth in the asset value of equipment and intellectual property products (IPP), both of which only began to improve again in early 2003. This occurred alongside an outright contraction in real investment in IPP as investors lost faith in company financial statements and heavily scrutinized corporate spending. Chart II-14highlights that a contraction in IP spending was a huge change from the double-digit pace of growth that occurred in the late 1990s. Chart II-13The Damaging Impact Of Corporate Excesses

The Damaging Impact Of Corporate Excesses

The Damaging Impact Of Corporate Excesses

Chart II-14A Near-Unprecedented Collapse In IPP Investment Followed The Tech Bubble

A Near-Unprecedented Collapse In IPP Investment Followed The Tech Bubble

A Near-Unprecedented Collapse In IPP Investment Followed The Tech Bubble

In addition, corporate sector indebtedness also appears to have played a role in driving weak investment in the early 2000s. While the interest burden of nonfinancial corporate debt was not as high in 2000 as it was in the early 1990s, Chart II-15 highlights that debt to operating income surged in the late 1990s – which likely caused investors already skeptical about company financial statements to impose a period of elevated capital discipline on corporate managers following the recession. Chart II-16 shows that while the peak in the 12-month trailing corporate bond default rate in January 2002 was similar to that of the early 90s, it was meaningfully higher on average in the lead-up to and following the recession. Chart II-15The Late-1990s Saw A Major Increase In Corporate Debt

The Late-1990s Saw A Major Increase In Corporate Debt

The Late-1990s Saw A Major Increase In Corporate Debt

Chart II-16Above-Average Corporate Defaults Before And After The 2001 Recession

Above-Average Corporate Defaults Before And After The 2001 Recession

Above-Average Corporate Defaults Before And After The 2001 Recession

To summarize, Charts II-10-16 underscore that management excesses, governance failures, and elevated debt in the corporate sector in the 1990s were the root cause of the seeming divergence between monetary policy and the output gap from 2001 to 2007. This was, unfortunately, the first of two major savings/capital misallocations that have occurred in the US over the past 25 years. Explaining The Post-GFC Experience In the early 2000s, the Federal Reserve was faced with a decision between two monetary policy paths: one that was appropriate for the corporate sector, and one that was appropriate for the household sector. The Fed chose the former, and it inadvertently contributed to the second major savings/capital misallocation to occur over the past 25 years: the enormous debt-driven bubble in US housing that culminated into the global financial crisis (GFC) of 2007-2009. Chart II-17It Is No Mystery Why Demand And Inflation Were Weak Last Cycle

It Is No Mystery Why Demand And Inflation Were Weak Last Cycle

It Is No Mystery Why Demand And Inflation Were Weak Last Cycle

As a result, 2007 to 2013/2014 was a mirror image of the early 2000s. Unlike previous post-war downturns, the GFC precipitated a balance-sheet recession that deeply affected homeowners and the financial system. This lasting damage led to a multi-year household deleveraging process, which substantially lowered the responsiveness of the economy to stimulative monetary policy. On a year-over-year basis, Chart II-17 shows that total nominal household mortgage credit growth was continuously negative for six and a half years, from Q4 2008 until Q2 2015, underscoring that the large divergence during this period between the stance of monetary policy and the output gap should not, in any way, be surprising to investors. And this is even before accounting for the negative impact of the euro area sovereign debt crisis and double-dip recession, or the persistent fiscal drag in nearly every advanced economy last cycle. What is surprising about the post-GFC experience is that inflation was not substantially weaker than it was, which is ironic considering that the secular stagnation narrative was revived to help explain below-target inflation. Chart II-8 showed that actual inflation steadily improved versus expected inflation alongside the closing of the output gap and the decline in the unemployment rate, but that it was much stronger than the output gap would have implied – particularly during the early phase of the economic recovery. It is still an open question as to why this occurred. A weak dollar and a strong recovery in oil prices likely helped support consumer prices, but we doubt that these two factors alone explain the discrepancy. A more credible answer is that expectations stayed very well anchored due to the Fed’s strong record of maintaining low and stable inflation (thus preventing a disinflationary spiral). In addition, the fact that the Fed actively communicated to the public during the early recovery years that a large part of its objective was to prevent deflation may have helped support prices. For example, in a CBS interview following the Fed’s November 2010 decision to engage in a second round of quantitative easing (“QE2”), then-Chair Bernanke prominently tied the decision to the fact that “inflation is very, very low.” When asked whether additional rounds of easing might be required, Bernanke responded that it was “certainly possible” and again cited inflation as a core consideration. Chart II-18Rising US Oil Production Caused The Massive 2014 Oil Price Shock

Rising US Oil Production Caused The Massive 2014 Oil Price Shock

Rising US Oil Production Caused The Massive 2014 Oil Price Shock

While inflation did not ultimately fall relative to expectations post-GFC as much as the output gap would have implied, the long-lasting weakness in demand left expectations vulnerable to exogenous shocks. In 2014, such a shock occurred: oil prices collapsed almost exactly at the point that US tight oil production crossed the four-million-barrels-per-day mark (Chart II-18), a level of output that many experts had previously believed would not be attainable (or would roughly mark the peak in production). We view this event as a truly exogenous shock to prices, given that research & development of shale technology had been ongoing since the late 1970s and only happened to finally gain traction around 2010. Chart II-19 shows that the 2014 oil price collapse caused a clear break lower in our measure of inflation expectations, to the lowest value recorded since the 1940s. This break also occurred in market-based expectations of inflation, such as long-dated CPI swap rates and TIPS breakeven inflation rates, and surveys of consumer inflation expectations (Chart II-20). This decline in inflation expectations meant that the output gap needed to be above zero in order for the Fed to hit its 2% target (absent any upwards shock to prices), and that the meaningful acceleration of inflation from 2016 to 2018 should actually be viewed as inflation “outperformance” because its long-term trend had been lowered by the earlier downward shift in expectations. Chart II-19The 2014 Oil Price Shock Collapsed Inflation Expectations...

The 2014 Oil Price Shock Collapsed Inflation Expectations...

The 2014 Oil Price Shock Collapsed Inflation Expectations...

Chart II-20...No Matter What Inflation Expectations Measure Is Used

...No Matter What Inflation Expectations Measure Is Used

...No Matter What Inflation Expectations Measure Is Used

The Modern-Day Phillips Curve: Key Takeaways Based on the evidence presented above, we see the perceived “failure” of the Phillips Curve to predict weak inflation over the past decade as being due to: A singular focus on the output gap/slack component of the modern Phillips Curve, to the exclusion of expectations A failure to fully consider the lasting impact of sustained periods of a negative output gap on expectations Downplaying the long-term balance-sheet impact of two episodes of excesses and savings/capital misallocations on the relationship between the stance of monetary policy and the output gap, via a persistently negative shock to aggregate demand and a reduced sensitivity of economic activity to interest rates. One crucial takeaway from the modern-day Phillips Curve equation presented above is that if inflation expectations are largely formed based on the experience of past inflation, then inflation is ultimately determined by three dimensions of the output gap: whether it is rising or falling, whether it is above or below zero, and how long it has been above or below zero. The extended period of below-potential output over the past two decades, accelerated recently by a major negative shock to energy prices, has now lowered inflation expectations to a point that merely reaching the Fed’s target constitutes inflation “outperformance.” This realization, made even more urgent by the COVID-19 pandemic, has strongly motivated the Fed’s official shift to an average inflation targeting regime. That shift does not suggest that the Fed is moving away from the modern-day Phillips Curve framework; rather, the Fed’s new policy is aimed at closing the output gap as quickly as possible in order to prevent a renewed decline in inflation expectations (and thus inflation itself) from another long period of activity running below its potential. The Outlook For Inflation While the Fed has shifted its policy to prefer higher inflation, that does not necessarily mean it will get it. Why is it likely to happen this time, if the last economic cycle featured such a large divergence between monetary policy and the output gap? Chart II-21Above-Target Inflation Is Not Imminent

Above-Target Inflation Is Not Imminent

Above-Target Inflation Is Not Imminent

First, to clarify, we do not believe that above-target inflation is imminent. The COVID-19 pandemic was an extreme event, and even given the very substantial recovery in the labor market, the unemployment rate remains almost 2½ percentage points above the Congressional Budget long-run estimate of NAIRU (Chart II-21). But based on our analysis of the modern-day Phillips Curve presented above, there are at least four main reasons to expect that inflation may be higher on average over the next ten years than over the past decade. Reason #1: This Appears To Be A Sharp Income Statement Recession, Not A Balance-Sheet Recession We highlighted above the importance of savings/capital misallocations in driving a gap between monetary policy and the output gap over the past two decades, but this recession was obviously not sparked by such an event. The onset of the pandemic came following a long period of US household sector deleveraging which, while painful, helped restore consumer balance sheets. Chart II-22 highlights that household debt to disposable income had fallen back to 2001 levels at the onset of the pandemic, and the interest burden of debt servicing had fallen to a 40-year low. From a wealth perspective, Chart II-23 highlights that total household liabilities to net worth have fallen below where they were at the peak of the housing market boom in 2005 for almost all income groups, and that a decline in leverage has been particularly noteworthy for the lowest income group since mid-2016. Chart II-22Households Have Repaired Their Balance Sheets...

Households Have Repaired Their Balance Sheets...

Households Have Repaired Their Balance Sheets...

Chart II-23...Across Almost All Income Brackets

...Across Almost All Income Brackets

...Across Almost All Income Brackets

Total credit to the nonfinancial corporate sector rose significantly relative to GDP over the course of the last cycle, but subpar growth in real nonresidential fixed investment and a rise in share buybacks highlight that this debt went largely to fund changes in capital structure rather than increased productive capacity. Chart II-24 highlights that corporate sector interest payments as a percentage of operating income are low relative to history, and they do not seem to be necessarily dependent on extremely low government bond yields.4 Finally, the corporate bond default rate may have already peaked (Chart II-25) and the percentage of jobs permanently lost looks more like 2001 than 2007 (Chart II-26), signaling that a prolonged balance-sheet recession is unlikely. Chart II-24Corporate Sector Debt Is Currently High, But Affordable

Corporate Sector Debt Is Currently High, But Affordable

Corporate Sector Debt Is Currently High, But Affordable

Chart II-25Corporate Defaults Have Already Peaked

Corporate Defaults Have Already Peaked

Corporate Defaults Have Already Peaked

Chart II-26So Far, Permanent Job Losses Look Like The 2001 Recession, Not 2007/2008

So Far, Permanent Job Losses Look Like The 2001 Recession, Not 2007/2008

So Far, Permanent Job Losses Look Like The 2001 Recession, Not 2007/2008

The bottom line is that while the pandemic has not yet been resolved and that major and permanent economic damage cannot be ruled out, the absence of “balance-sheet dynamics” is likely to eventually lead to a stronger responsiveness of demand for goods and services to what is set to be an extraordinarily easy monetary policy stance for at least another two years. Reason #2: The Fed May Be Able To Jawbone Inflation Higher The Fed’s public commitment to set interest rates in a way that will generate moderately above-target inflation is highly reminiscent of its defense of quantitative easing in the early phase of the last economic expansion, and (in the opposite fashion) of Paul Volker’s campaign in the 1980s against the “self-fulfilling prophecy” of inflation. From 2008-2014, the Fed explicitly linked the odds of future bond buying to the pace of actual inflation in its public statements. On its own, this was not enough to cause inflation to rise, but we highlighted above that it may have contributed to the fact that inflation expectations did not collapse. Chart II-1 on page 12 showed that long-dated market-based expectations for inflation have already been impacted by the Fed’s regime shift, suggesting decent odds that Fed policy will contribute to self-fulfilling price increases if the US economy does indeed avoid “balance-sheet dynamics” as a result of the pandemic. Reason #3: The Odds Of Negative Supply Shocks Are Lower Than In The Past We noted above the impact that energy price shocks and large typically exchange-rate driven changes in import prices can have on inflation, with the 2014 oil price collapse serving as the most vivid recent example. On both fronts, a value perspective suggests that the odds of negative shocks to inflation over the coming few years from oil and the dollar are lower than they have been in the past. Chart II-27 shows that the cost of global energy consumption as a share of GDP has fallen below its median since 1970, and Chart II-28 highlights that the US dollar is comparatively expensive relative to other currencies – which raises the bar for further gains. Stable-to-higher oil prices alongside a flat-to-weak dollar implies reflationary rather than disinflationary pressure. Chart II-27Massive, Downward Shocks To Oil Prices Are Now Less Likely

Massive, Downward Shocks To Oil Prices Are Now Less Likely

Massive, Downward Shocks To Oil Prices Are Now Less Likely

Chart II-28Valuation Favors A Declining Dollar, Which Is Inflationary

January 2021

January 2021

Reason #4: Structural Factors In addition to the cyclical arguments noted above, my colleague Peter Berezin, BCA’s Chief Global Strategist, has also highlighted several structural arguments in favor of higher inflation. Chart II-29 highlights that the world support ratio, calculated as the number of workers relative to the number of consumers, peaked early last decade after rising for nearly 40 years. This suggests that output will fall relative to spending the coming several years, which should have the effect of boosting prices. Chart II-30 also highlights that globalization is on the back foot, with the ratio of trade-to-output having moved sideways for more than a decade. Since the early 1990s, rising global trade intensity has corresponded with very low goods prices in many countries, and the end of this trend reduces the impact of a factor that has been weighing on consumer prices globally over the past two decades. Chart II-29Less Production Relative To Consumption Is Inflationary

Less Production Relative To Consumption Is Inflationary

Less Production Relative To Consumption Is Inflationary

Chart II-30Trade Is Not Suppressing Prices As Much As It Used To

Trade Is Not Suppressing Prices As Much As It Used To

Trade Is Not Suppressing Prices As Much As It Used To

Positioning For Eventually Higher Inflation Below we present an assessment of several potential candidates across the major asset classes that investors can use to protect their portfolios from rising inflation once it emerges. We conclude with a new trade idea that may provide investors with inflation protection at a better valuation profile than more traditional inflation hedges. Fixed-Income Within fixed-income, inflation-linked bonds and derivatives (such as CPI swaps) are the obvious choice for investors seeking inflation protection. Inflation-linked bonds are much better played relative to nominal equivalents, as inflation expectations make up the difference between nominal and inflation-linked yields. But Table II-1 shows that 5-10 year TIPS are also likely to provide positive absolute returns over the coming year even in a scenario where 10-year Treasury yields are rising, so long as real yields do not account for the vast majority of the increase. Barring a major and positive change in the long-term economic outlook over the coming year, our sense is that the Fed would act to cap any outsized increase in real yields and that TIPS remain an attractive long-only option until the Fed becomes sufficiently comfortable with the inflation outlook. Table II-1TIPS Will Earn Positive Absolute Returns Next Year Barring A Surge In Real Yields

January 2021

January 2021

Commodities Commodities are arguably the most traditional inflation hedge, and are likely to provide investors with superior risk-adjusted returns in an environment where inflation expectations are rising. Our Commodity & Energy Strategy service is positive on gold, and recently argued that Brent crude prices are likely to average between $65-$70/barrel between 2021-2025.5 Chart II-31Gold Is Expensive And Long-Term Returns May Be Poor

Gold Is Expensive And Long-Term Returns May Be Poor

Gold Is Expensive And Long-Term Returns May Be Poor

One caveat about gold is that, unlike oil prices, it appears to be quite expensive relative to its history. Since gold does not provide investors with a cash flow, over time real (or inflation-adjusted) prices should ultimately be mean-reverting unless real production costs steadily trend higher. Chart II-31 highlights that the real price of gold is already sky-high and well above its historical average. Over a ten-year time horizon, gold prices fell meaningfully following the last two occasions where real gold prices reached current levels, suggesting that the long-term outlook for gold returns is poor. However, over the coming few years, gold prices are likely to remain well supported given our economic outlook, the Fed’s new monetary policy regime, and the consistently negative correlation between real yields and the US dollar and gold prices. As such, we would recommend gold as a hedge against the fear of inflation, which is likely to increase over the cyclical horizon. Equities We provide two perspectives on how equity investors may be able to protect themselves against rising inflation. The first is simply to favor cyclical versus defensive sectors. The former is likely to continue to benefit next year in response to a strengthening economy as COVID-19 vaccines are progressively distributed, and historically cyclical sectors have tended to outperform during periods of rising inflation. In addition, my colleague Anastasios Avgeriou, BCA’s Equity Strategist, presented Table II-2 in a June Special Report,6 and it highlights that cyclical sectors (plus health care) have enjoyed positive relative returns on average during periods of rising inflation. Table II-2S&P 500 Sector Performance During Inflationary Periods

January 2021

January 2021