Sectors

Highlights Global shortages of medical equipment – including medicines – are frontloaded until emergency production kicks in. As the crisis abates, political recriminations between the US and China will surge. The US will seek to minimize medical supply exposure to China going forward, a boon for India and Mexico. China has escaped the COVID-19 crisis with minimal impact on food supply. Pork prices are surging due to African Swine Flu, but meat is a luxury. Still, the “Misery Index” is spiking and this will increase social instability. Food insecurity, inflation, and large current account deficits suggest that emerging market currencies will remain under pressure. Turkey and South Africa stand to suffer while we remain overweight Malaysia. Feature Chart 1Collapse In Economic Activity

Collapse In Economic Activity

Collapse In Economic Activity

With a third of the world population under some form of lockdown, general activity in the world’s manufacturing powerhouses has collapsed (Chart 1). The breakdown is a double whammy on market fundamentals. On the supply side, government-mandated containment efforts force workers in non-essential services to stay home while, on the demand side, households confined to their homes are unable to spend. Acute demand for medical supplies is causing shortages, while supply disruptions threaten states that lack food security. While global monetary and fiscal stimulus will soften the blow (Chart 2), the economic shock is estimated to be a 2% contraction in real GDP for every month of strict isolation. If measures are extended beyond April, markets will sell and new stimulus will be applied. Already the US Congress is negotiating the $1-$2 trillion infrastructure package that we discussed in our March 4 report, and cash handouts will be ongoing. When the dust settles the political fallout will be massive. Authoritarian states like China and especially Iran will face greater challenges maintaining domestic stability. Democracies like Italy and the US, which lead the COVID-19 case count, are the most likely to experience a change in leadership (Chart 3). Initially the ruling parties of the democracies are receiving a bump in opinion polling, but this will fade as households will be worse off and will likely vent their grievances at the ballot box.

Chart 2

Chart 3

Until a vaccine or treatment is discovered, medical equipment and social distancing are the only weapons against the pandemic. National production is (rightly) being redirected from clothing and cars to masks and ventilators to meet the spike in demand. Will the supply shock cause shortages in food and medicine – essential goods for humankind? In this report we address the impact of COVID-19 on global supply security and assess the market implications. Medical Equipment Shortages Will Spur Protectionism

Chart

Policymakers are fighting today’s crisis with the tools of the 2008 crisis, but a lasting rebound in financial markets will depend on surmounting the pandemic, which is prerequisite to economic recovery (Table 1). As the US faces the peak of its COVID-19 outbreak, public health officials and doctors are raising the alarm on the shortage of medical supplies. A recent US Conference of Mayors survey reveals that out of the 38% of mayors who say they have received supplies from their state, 84.6% say they are inadequate (Chart 4). Italy serves as a warning: A reported 8% of the COVID-19 cases there are doctors and health professionals, often treating patients without gloves or with compromised protective gear. These workers are irreplaceable and when they succumb the virus cannot be contained. In the US, doctors and nurses are re-using masks and sometimes treating patients behind a mere curtain, highlighting the supply shortage. While the shortages are mainly driven by a surge in demand from both medical institutions and households, they also come from the supply side, particularly China. Factory closures and transportation disruptions in China earlier this year, coupled with Beijing’s government-mandated export curbs, reduced Chinese exports, a major source of US and global supplies (Chart 5).

Chart 4

Chart 5

Other countries have imposed restrictions on exports of products used in combating the spread of COVID-19. Following export restrictions by the French, German, and Czech governments in early March, the European Commission intervened on March 15 to ensure intra-EU trade. It also restricted exports of protective medical gear outside of the EU. At least 54 nations have imposed new export restrictions on medical supplies since the beginning of the year.1 Both European and Chinese measures will reduce supplies in the US, the top destination for most of these halted exports (Chart 6).

Chart 6

Thus it is no wonder that the Trump administration has rushed to cut import duties and boost domestic production. The administration has released strategic stockpiles and cut tariffs on Chinese medical equipment used to treat COVID-19. With the whole nation mobilized, supply kinks should improve greatly in April. After a debacle in rolling out test kits (Chart 7), the US is rapidly increasing its testing capabilities to manage the crisis, with over a million tests completed as of the end of March (Chart 8). Meanwhile a coalition of companies is taking shape to make face masks. The president has invoked the defense production act to force companies to make ventilators.

Chart 7

Chart 8

However, with the pandemic peaking in the US, the hardest-hit regions will continue experiencing shortages in the near term. Shortages are prompting public outcry against the US government for its failure to anticipate and redress supply chain vulnerabilities that were well known and warned against. A report in The New York Times tells how Mike Bowen, owner of Texas-based mask-maker Prestige Ameritech, has advised the past three presidents about the danger in the fact that the US imports 95% of its surgical masks. “Aside from sitting in front of the White House and lighting myself on fire, I feel like I’ve done everything I can,” he said. He is currently inundated with emergency orders from US hospitals. The same report tells of a company called Strong Manufacturers in North Carolina that had to cut production of masks because it depends on raw materials from Wuhan, China, where the virus originated.2 The Trump administration will suffer the initial public uproar, but the US government will also seek to reduce import dependency going forward, and it will likely deflect some of the blame by focusing on the supply risks posed by China. Beijing, for its part, is launching a propaganda campaign against the US to distract from its own failures at home (some officials have even blamed the US for the virus). Meanwhile it is cranking up production and shipping medical supplies to crisis hit areas like Italy to try to repair its global image after having given rise to the virus. In addition, the city of Shenzhen is sending 1.2 million N95 masks to the US on the New England Patriots’ team plane. Even Russia is sending small donations. But these moves work to propagandistic efforts in these countries and will ultimately shame the Americans into taking measures to improve self-sufficiency. Bottom Line: The most important supply shortage amid the global pandemic is that of medical equipment. While these shortages will abate sooner rather than later, the supply chain vulnerabilities they have exposed will trigger new policies of supply redundancy and import substitution. The US in particular will seek to reduce dependency on China. That COVID-19 is aggravating rather than reducing tensions between these states, despite China’s role as a key supplier in a time of need, highlights the secular nature of their rising tensions. The US-China Drug War Shortages of pharmaceuticals are also occurring, despite the fact that the primary pandemic response is necessarily “non-pharmaceutical” (e.g. social distancing). The US Food and Drug Administration (FDA) announced the first COVID-19 related drug shortage in the US on February 27. While the specific drug was not disclosed, the announcement notes that “the shortage is due to an issue with manufacturing of an active pharmaceutical ingredient used in the drug.”3 The FDA is monitoring 20 other (non-critical) drugs potentially at risk of shortages because the sole source is China. The global spread of the pandemic will increase these shortages. On March 3 India announced export restrictions on 26 drugs, including paracetamol and several antibiotics, due to supply disruptions caused by the Chinese shutdown. While Chinese economic activity has since picked up, India is now among the string of countries under a nationwide lockdown. Similar measures enforced across Europe will also hamper the production and transportation of these goods. The implication is that even if Chinese drugs return to market, supplies further down the chain and from alternative suppliers will take a hit. The risk that this will evolve into a drug shortage depends on the intensity of the outbreak. Drug companies generally hold 3-6 months’ worth of inventories. Consequently, while inventories are likely to draw as supplies are disrupted, consumers may not experience an outright shortage immediately. In the US, as with equipment and protective gear, the government’s strategic stockpile will buffer against shortfalls in supplies of critical drugs. COVID-19 is aggravating rather than reducing US-China tensions. Nevertheless the supply chain is getting caught up in the larger US-China strategic conflict. Even before the pandemic, the US-China trade war brought attention to the US’s vulnerabilities to China’s drug exports. This dispute is not limited to illicit drugs, as with China’s production of the opioid fentanyl, but also extends to mainstream medicines, as highlighted in the selection of public statements shown in Table 2.

Chart

Chart 9

How much does the US rely on China for medicine? According to FDA data, just over half of manufacturing facilities producing regulated drugs in finished dosage form for the US market are located abroad, with China’s share at 7% (Chart 9).4 The figures are higher for manufacturing facilities producing active pharmaceutical ingredients, though still not alarming – 72% of the facilities are located abroad, with 13% in China. Of course, high-level data understate China’s influence. The complex nature of global drug supply chains means that the source of finished dosage forms masks dependencies and dominance higher up the supply chain (Figure 1).

Chart

For instance, active pharmaceutical ingredients produced in Chinese facilities are used as intermediate goods by finished dosage facilities in India as well as China. The FDA reports that Indian finished dosage facilities rely on China for three-quarters of the active ingredients in their generic drug formulations, which are then exported to the US and the rest of the world. Any supply disruption in China – or any other major drug producer – will lead to shortages further down the supply chain.

Chart 10

Chinese influence becomes more apparent when the sample is restricted to generic prescription drugs. These are especially relevant because nearly 70% of Americans are on at least one prescription drug, of which more than 90% are dispensed in the generic form. In this case, 87% of ingredient manufacturers and 60% of finished dosage manufacturers are located outside the US, with 17% of ingredient facilities and 8% of dosage facilities in China (Chart 10). Of all the facilities that manufacture active ingredients that are listed on the World Health Organization’s Essential Medicines List – a compilation of drugs that are considered critical to the health system – 71% are located aboard with 15% located in China (Chart 11). Moreover, manufacturers are relatively inflexible when adapting to market conditions and shortages. Drug manufacturing facilities generally operate at above 80% of their capacity and are thus left with little immediate capacity to ramp up production in reaction to shortages elsewhere. In addition, manufacturers face challenges in changing ingredient suppliers – there is no centralized source of information on them, and additional FDA approvals are required. The US will look to reduce its dependency on China for its drug supplies regardless of 2020 election outcome. China also has overwhelming dominance in specific categories. The Council on Foreign Relations reports that China makes up 97% of the US antibiotics market.5 Other common drugs that are highly dependent on China for supplies include ibuprofen, acetaminophen, hydrocortisone, penicillin, and heparin (Chart 12).

Chart 11

Chart 12

Taking it all together, US vulnerability can be overstated. Consider the following: Of the 370 drugs on the Essential Medicines List that are marketed in the US, only three are produced solely in China. None of these three are used to treat top ten causes of death in the United States. Import substitution is uneconomical. Foreign companies, especially Chinese companies, are attractive due to their lower costs and lax regulations. While China’s influence extends higher up the supply chain, this is true for US markets as well as other consumer markets. While China can cut off the US from the finished dosages it supplies, it cannot do the same for the ingredients that are used by facilities in other countries and eventually make their way to the US in finished dosage form. Americans are demanding that drug prices be reduced and an obvious solution is looser controls on imports. The recent activation of the Defense Production Act shows that the US can take action to boost domestic production in emergencies. Nevertheless, China is growing conspicuous to the American public due to general trade tensions and COVID-19. As it moves up the value chain, it also threatens increasing competition for the US and its allies. Hence the US government will have a strategic reason to cap China’s influence that is also supported by corporate interests and popular opinion. This will lead to tense trade negotiations with China and meanwhile the US will seek alternative suppliers. China will not want to lose market share or leverage over the United States, so it may offer trade concessions at some point to keep the US engaged. Ultimately, however, strategic tensions will catalyze US policy moves to reduce the cost differential with China and promote its rivals. Pressure on China over its currency, regulatory standards, and scientific-technological acquisition will continue regardless of which party wins the White House in 2020. The Democrats would increase focus on China’s transparency and adherence to international standards, including labor and environmental standards. Both Republicans and Democrats will try to boost trade with allies. The key beneficiaries will be India, Southeast Asia, and the Americas. Taiwan’s importance will grow as a middle-man, but so will its vulnerability to strategic tensions. Bottom Line: The US and the rest of the world are suffering shortfalls of equipment necessary to combat COVID-19. There is also a risk of drug shortages stemming from supply disruptions and emergency protectionist policies. These shortages look to be manageable, but they have exposed national vulnerabilities that will be reduced in future via interventionist trade policies. While the US and Europe will ultimately manage the outbreak, the political fallout will be immense. The US will look to reduce its dependency on China. This will increase investment in non-China producers of active pharmaceutical ingredients, such as India and Mexico. The US tactics against China will vary according to the election result, but the strategic direction of diversifying away from China is clear and will have popular impetus in the wake of COVID-19. Food Security In addition to the challenges posed by COVID-19 on medical supplies, food – another essential good – also faces risk of shortages. China is a case in point. Food prices there were on the rise well before the COVID-19 outbreak, averaging 17.3% in the final quarter of 2019. However inflation was limited to pork and its substitutes – beef, lamb and poultry – and reflected a reduction in pork supplies on the back of the African Swine Flu outbreak. While year-on-year increases in the prices of pork and beef averaged 102.8% and 21.0%, respectively, grain, fresh vegetable, and fresh fruit prices averaged 0.6%, 1.5%, and -5.0% in Q42019 (Chart 13). Chart 13Chinese Inflation Has (Thus far) Been Contained To Pork

Chinese Inflation Has (Thus far) Been Contained To Pork

Chinese Inflation Has (Thus far) Been Contained To Pork

Chart 14China's Misery Index Is Spiking - A Political Liability

China's Misery Index Is Spiking - A Political Liability

China's Misery Index Is Spiking - A Political Liability

However China’s COVID-19 containment measures had a more broad-based impact on food supplies, threatening to push up China’s Misery Index (Chart 14). Travel restrictions, roadblocks, quarantined farm laborers, and risk-averse truck drivers introduced challenges not only in ensuring supplies were delivered to consumers, but also to daily farm activity and planting. The absence of farm inputs needed for planting such as seeds and fertilizer, and animal feed for livestock, was especially damaging in regions hardest hit by the pandemic. Livestock farmers already struggling with swine flu-related reductions in herd sizes were forced to prematurely cull starving animals, cutting the stock of chicken and hogs. Now as the country transitions out of its COVID-19 containment phase and moves toward normalizing activity (Chart 15), food security is top of the mind. Authorities are emphasizing the need to ensure sufficient food supplies and adopt policies to encourage production.6 This is especially important for crops due to be planted in the spring. Delayed or reduced plantings would weight on the quality and quantity of the crops, pushing prices up.

Chart 15

With food estimated to account for 19.9% of China’s CPI basket – 12.8% of which goes towards pork (Chart 16) – a prolonged food shortage, or a full-blown food crisis, would be extremely damaging to Chinese families and their pocketbooks.

Chart 16

However, apart from soybeans and to a lesser extent livestock, China’s inventories are well stocked (Chart 17) and are significantly higher than levels amid the 2006-2008 and 2010-2012 food crises. Inventories have been built up specifically to provide ammunition precisely in times of crisis. Corn and rice stocks are capable of covering consumption for nearly three quarters of a year, and wheat stocks exceeding a year’s worth of consumption. Thus, while not completely immune, China today is better able to weather a supply shock. Moreover, with the exception of soybeans, China is not overly dependent on imports for agricultural supplies (Chart 18).

Chart 17

Chart 18

As the COVID-19 epicenter shifts to the US and Europe, farmers there are beginning to face the same challenges. Reports of delays in the arrival of shipments of inputs such as fertilizer and seeds have prompted American farmers to prepare for the worst and order these goods ahead of time.

Chart 19

While these proactive measures will help reduce risks to supply, farmers in Europe and parts of the US who typically rely on migrant laborers will need to search for alternative laborers as the planting season nears. Just last week France’s agriculture minister asked hairdressers, waiters, florists, and others that find themselves unemployed to take up work in farms to ensure food security. As countries become increasingly aware of the risks to food supplies, some have already introduced protectionist measures, especially in the former Soviet Union: The Russian agriculture ministry proposed setting up a quota for Russian grain exports and has already announced that it is suspending exports of processed grains from March 20 for 10 days. Kazakhstan suspended exports of several agricultural goods including wheat flour and sugar until at least April 15. On March 27, Ukraine’s economy ministry announced that it was monitoring wheat export and would take measures necessary to ensure domestic supplies are adequate. Vietnam temporarily suspended rice contracts until March 28 as it checked if it had sufficient domestic supplies. The challenge is that, unlike China, inventories in the rest of the world are not any higher than during the previous food crisis and do not provide much of a buffer against supply shortfalls (Chart 19). Higher food prices would be especially painful to lower income countries where food makes up a larger share of household spending (Chart 20). In addition to using their strategic food stockpiles, governments will attempt to mitigate the impact of higher food prices by implementing a slew of policies:

Chart 20

Trade policies: Producing countries will want to protect domestic supplies by restricting exports – either through complete bans or export quotas. Importing countries will attempt to reduce the burden of higher prices on consumers by cutting tariffs on the affected goods. Consumer-oriented policies: Importing countries will provide direct support to consumers in the form of food subsidies, social safety nets, tax reductions, and price controls. Producer-oriented policies: Governments will provide support to farmers to encourage greater production using measures such as input subsidies, producer price support, or tax exemptions on goods used in production. While these policies will help alleviate the pressure on consumers, they also result in greater government expenditures and lower revenues. Thus, subsidizing the import bill of a food price shock can weigh on public finances, debt levels, and FX reserves. Currencies already facing pressure due to the recessionary environment, such as Turkey, South Africa and Chile will come under even greater downward pressure. Food inventories ex-China are insufficient to protect against supply shortages. Bottom Line: COVID-19’s logistical disruptions are challenging farm output. This is especially true when transporting goods and individuals across borders rather than within countries. This will be especially challenging for food importing countries, as some producers have already started erecting protectionist measures and this will result in an added burden on government budgets that are already extended in efforts to contain the economic repercussions of the pandemic. Investment Implications Chart 21Ag Prices Inversely Correlated With USD

Ag Prices Inversely Correlated With USD

Ag Prices Inversely Correlated With USD

China will continue trying to maximize its market share and move up the value chain in drug production. At the same time, the US is likely to diversify away from China and try to cap China’s market share. This will result in tense trade negotiations regardless of the outcome of the US election. The COVID-19 experience with medical shortages and newfound public awareness of potential medical supply chain vulnerabilities means that another round of the trade war is likely. Stay long USD-CNY. Regarding agriculture, demand for agricultural commodities is relatively inelastic. This inelasticity should prevent a complete collapse in prices even amid a weak demand environment. Thus given the risk on supplies, prices face upward pressure. However, not all crops are facing these same market dynamics. While wheat and rice prices have started to move in line with the dynamics described above, soybeans and to a greater extent corn prices have not reacted as such (Chart 21). In the case of soybeans, we expect demand to be relatively muted. China accounts for a third of the world’s soybean consumption. 80% of Chinese soybeans are crushed to produce meal to feed China’s massive pork industry. However, the 21% y/y decline in pork output in 2019 on the back of the African Swine Flu outbreak will weigh on demand and mute upward pressures on supplies. Demand for corn will also likely come in weak. The COVID-19 containment measures and the resulting halt in economic activity reduce demand for gasoline and, as a consequence, reduce demand for corn-based ethanol, which is blended with gasoline. In addition to the above fundamentals, ag prices have been weighed down by a strong USD which makes ex-US exporters relatively better off, incentivizing them to raise exports and increase global supplies. A weaker USD – which we do not see in the near term – would help support ag prices. It is worth noting that if there is broad enforcement of protectionist measures, then producers will not be able to benefit from a stronger dollar. In that case we may witness a breakdown in the relationship between ag prices and the dollar. In light of these supply/demand dynamics, we expect rice and wheat prices to be well supported going forward and to outperform corn and soybeans. Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See "Tackling COVID-19 Together: The Trade Policy Dimension," Global Trade Alert, University of St. Gallen, Switzerland, March 23, 2020. 2 See Rachel Abrams et al, "Governments and Companies Race to Make Masks Vital to Virus Fight," The New York Times, March 21, 2020. 3 The announcement also notes that there are other alternatives that can be used by patients. See "Coronavirus (COVID-19) Supply Chain Update," US FDA, February 27, 2020. 4 All regulated drugs include prescription (brand and generic), over the counter, and compounded drugs. 5 Please see Huang, Yanzhong, "The Coronavirus Outbreak Could Disrupt The US Drug Supply," Council on Foreign Relations, March 5, 2020. 6 The central government ordered local authorities to allow animal feed to pass through checkpoints amid the lockdowns. In addition, Beijing has relaxed import restrictions by lifting a ban on US poultry products and announcing that importers could apply for waivers on goods tariffed during the trade war such as pork and soybeans. The lifting of these restrictions also serves to help China meet its phase one trade deal commitments. Please see "Coronavirus hits China’s farms and food supply chain, with further spike in meat prices ahead," South China Morning Post, dated February 21, 2020.

Avoid REITs At All Costs

Avoid REITs At All Costs

We continue to recommend investors avoid the S&P real estate sector. For investors seeking defensive protection we would recommend hiding in the S&P health care sector instead, as we highlighted in our mid-March report.1 The chart on the right shows a disturbing breakdown in the inverse correlation between the relative share price ratio and the 10-year Treasury yield. While it makes intuitive sense that this fixed income proxy sector (i.e. high dividend yielding) should move in the opposite direction of the competing risk-free yielding asset, at times of tumult this correlation reverts to positive (top panel) as the sector looses its attractiveness thanks to the very illiquid assets that dominate REITs’ holdings. Commercial real estate prices also remain extended and vulnerable to a deflationary shock (bottom panel). Currently there is no real price discovery as no landlord would dare put any properties for sale in this market starved for liquidity. With the exception of distressed sales, we deem that the “mark to model” mantra will make a comeback, eerily reminiscent of the GFC. Bottom Line: Shy away from the S&P real estate sector. The ticker symbols for the stocks in this index are: BLBG: S5RLST – CCI, AMT, PLD, EQIX, DLR, PSA, SBAC, AVB, EQR, FRT, SPG, WELL, ARE, CBRE, O, BXP, ESS, EXR, DRE, PEAK, HST, MAA, UDR, VTR, WY, AIV, IRM, PEG, VNO, SLG. For more details please refer to this Monday’s Weekly Report. 1 Please see BCA US Equity Strategy Weekly Report, “Inflection Point” dated March 16, 2020, available at uses.bcaresearch.com

Making predictions about the economic and market outlook seems a futile exercise in the midst of such massive uncertainty. The deluge of articles about COVID-19 merely serves to highlight that nobody really knows how things will play out in the year ahead. Much depends on whether an effective vaccine or treatment becomes available within a reasonable timescale and that remains an open question. Social and economic disruption will continue to intensify until the spread of the virus starts to abate. One thing is certain. Economic activity around the world faces its biggest contraction in modern times. Declines in second quarter GDP will be mind-numbingly bad in a wide range of countries, especially those that have instituted lockdowns and the closure of non-essential businesses. According to the OECD, the median economy faces an initial output decline of around 25% as a result of shutdowns and restrictions.1 Chart 1A Meltdown In Economic Activity

A Meltdown In Economic Activity

A Meltdown In Economic Activity

Estimates for the drop in US real GDP in the second quarter range as high as 50% at an annual rate. To put this into perspective, the peak-to-trough decline in US real GDP in the 2007-09 recession was a mere 4% over six quarters, and that felt catastrophic at the time. The New York Fed’s weekly economic index2 has already fallen to the lows of 2008 and worse is still to come (Chart 1). Could things be as bad as the 1930s Great Depression when US real GDP contracted by 25% over a three-year period? That would require an extreme apocalyptic view about the progression of the virus and does not bear thinking about. I am not that gloomy. Policymakers are acting aggressively to limit the economic damage. Central banks are flooding the system with liquidity and the cost of money is negligible. Meanwhile, fiscal caution has been thrown to the wind with massive government stimulus in many countries. While this will not prevent a deep recession, it will minimize the downside risks and support the eventual rebound. Markets are understandably in a deep funk because it is hard to price unknown risks. If this is no more than a two-quarter economic downturn followed by a sharp recovery, then a good buying opportunity in risk assets is in place given that monetary policy will stay hyper accommodative for a considerable time. If the downturn lingers much longer than that, then equities remain at risk. While loath to make a prediction, I am uncharacteristically tending to the more optimistic side. Let’s make the heroic assumption that we are not in an end of days scenario and that this crisis will pass at some point in the next year- hopefully sooner than later. What are some of the longer-run implications? A few come to mind. The backlash against globalization will gather impetus. Public sector debt will rise to unimaginable peacetime levels. Meanwhile, the crisis puts the final nail in the coffin of the private sector Debt Supercycle. Monetary policy will err on the side of ease for a very long time. The way that companies and other institutions have been forced to adapt to the crisis could trigger lasting changes in how they operate. Globalization In Full Retreat Chart 2A Retreat From Globalization

A Retreat From Globalization

A Retreat From Globalization

The peak of globalization has been a central part of the BCA view for several years.3 Long before the current crisis, it was clear that anti-globalization forces were gathering strength, illustrated by increased trade barriers, a backlash against inward migration in many countries, and reduced flows of foreign direct investment (Chart 2). The Trump Administration’s imposition of tariffs and the Brexit vote were two of the more obvious examples of the change in attitudes. The supply-chain interruptions caused by factory shutdowns in China will reinforce the view that shifting production to cheaper-cost countries overseas went too far. At a minimum, it seems inevitable that many companies will seek to reduce their reliance on a single producer for critical components. On the medical front, one striking fact to emerge was that China supplies around 80% of US antibiotics. There will be massive pressure to develop greater homegrown supplies of medical supplies and other products deemed critical for economic and national security. The crisis also has led to a breakdown of the Schengen Area of open borders within the European Union (EU). Many member countries have reinstituted border controls and it is unclear when these might be removed. The free movement of people is a core principle of the EU. Meanwhile, the Maastricht Treaty rules on fiscal discipline, a key element of economic union, have been thrown out of the window. Even Germany has bowed to the pressure of relaxing fiscal constraints. Finally, a worsening situation for the already troubled Italian banking system will threaten EU financial stability. Overall, the crisis will leave a huge question mark over the long-term viability of the EU. Globalization was a major force behind disinflation as production shifted to low-cost producers. A reversal of this trend will thus be inflationary, at the margin. For many, this will be a price worth paying if it means increased job security and reduced vulnerability of supply chains. But the shift away from globalization will not be the only trend that threatens an eventual resurgence of inflation. The Explosion In Government Debt: Last Gasp Of The Debt Supercycle BCA introduced the concept of the Debt Supercycle more than 40 years ago to describe the actions of policymakers to pump up demand rather than allow financial imbalances to be fully unwound during economic downturns. This inevitably meant that each new cycle began with a higher level of financial imbalances. As indebtedness rose, the economic costs of a financial cleansing increased, requiring ever-more desperate policy measures to shore things up. Unfortunately, such actions merely created the conditions for greater excesses and imbalances down the road. For example, the Federal Reserve’s aggressive response to the bursting of the tech bubble in 2000 helped set the scene for the even bigger housing bubble later in the decade. In that sense, the Debt Supercycle was a self-reinforcing trap that was bound to end badly, and that occurred in 2007. Chart 3The US Household Love Affair With Debt Died A Decade Ago

The US Household Love Affair With Debt Died A Decade Ago

The US Household Love Affair With Debt Died A Decade Ago

Our discussion of the US Debt Supercycle was focused largely on the private sector because that is where rising imbalances posed the greatest threat to economic and financial stability. Rising public sector imbalances were less of a concern because governments do not finance themselves through the banking sector. Moreover, unlike the private sector, taxes can always be raised to boost revenues or, in extremis, the authorities can resort to the printing press. At the end of 2014, we wrote that the Debt Supercycle was dead. By that, we meant that easing policy would no longer be able to encourage a new cycle of leverage-financed private-sector spending. The downturn of 2007-09 was a turning point in attitudes toward debt, much in the way that those who lived through the Great Depression were financially conservative for the rest of their lives. Our view has been vindicated by the fact the ratio of household debt to income has decisively broken its pre-housing bubble uptrend and has failed to revive in the face of record-low interest rates (Chart 3). Corporate borrowing has been strong, but largely to finance stock buybacks and M&A activity. Capital spending has been disappointing this cycle, despite strong profits and margins. The current deep downturn will add a further nail in the coffin of the private sector Debt Supercycle. The shock of the recession and destruction of wealth will leave a legacy of increased financial caution with households wanting to build precautionary savings and companies striving to repair damaged balance sheets. It would not be a surprise to see the US personal saving rate head back to the double-digit levels of the early 1980s. While the private sector embraces greater financial conservatism, we are witnessing the start of an extraordinary surge in public sector deficits and debt from already high levels. Chart 4A Bad Starting Point For A Surge In The Federal Deficit

A Bad Starting Point For A Surge In The Federal Deficit

A Bad Starting Point For A Surge In The Federal Deficit

Budget deficits automatically rise during recessions because tax receipts drop and spending on unemployment and welfare programs goes up (Chart 4). In the past, the starting point for deficits generally was low before a recession took hold. This time, the federal deficit has breached 5% of GDP when the economy was doing fine. With the current recession set to be deeper than in 2007-09 and fiscal stimulus likely to end up much more than the initial $2 trillion package, the deficit will far exceed the previous post-WWII peak of almost 10% of GDP, reached in fiscal 2009. The ratio of federal debt to GDP will soar past 100% within the next few years, exceeding the peak reached in WWII. A speedy decline in WWII debt burdens was helped by a sharp rebound in economic activity, supported by a powerful combination of demographics (the post-WWII baby boom) and pent-up demand. Real GDP grew at an average annualized pace of 4.3% in both the 1950s and 1960s. Unfortunately, slower population growth means that growth in the next one and two decades will be less than half that pace. At the same time, the federal deficit will be under upward pressure because of the impact of an aging population on healthcare and social security. In other words, restoring order to fiscal finances through normal measures (growth and/or austerity) will be an impossible task. High levels of government debt are perfectly manageable when private sector savings are plentiful, interest rates are negligible, and investors seek the safety of low-risk bonds. Thus, $1 trillion US federal deficits have not prevented Treasury yields from falling to all-time lows. However, such conditions will not last indefinitely. The timing of when bloated budget deficits start to impact markets and thus the economy will partly depend on the actions of the Fed. Monetary Policy: Is There A Limit To What It Can Do? Gone are the days when monetary policy was a rather technical exercise: tweaking the level of interest rates to ensure that money and credit trends delivered the economic growth consistent with low and stable inflation. In the past decade, the old rule book has been discarded with policymakers forced to take ever-more extreme measures to prevent total collapse of the economic and financial system. The 2007-9 downturn was easier to deal with than the current crisis. The primary problem a decade ago was a financial rather than economic seizure. While policymakers had to be creative, the main task was to shore up systemically important financial institutions and inject enough liquidity into the system to restore normal market functioning. And it worked. This time, the issue is an economic not financial seizure and associated liquidity strains are a symptom, not the primary problem. The immediate role of central banks is again to ensure that the financial system continues to function by injecting whatever amounts of liquidity are necessary. But monetary policy cannot directly bail out all the businesses that face bankruptcy or help those that have lost their jobs. That is the role of fiscal policy. What central banks can do is print money to finance the rise in budget deficits. During WWII, the Fed had an agreement with the Treasury Department to peg the level of long-term yields below 2.5% and this arrangement persisted until 1951, long after the war ended. This ensured that a post-war rebound in private credit demand would not cause a spike in interest rates that might short-circuit the recovery. We could well see a similar arrangement in the coming years, though it might be an informal rather than publicized agreement. The key point is that the Fed will be massively biased toward easy policy for many years. The current generation of central bankers have experienced periodic threats of deflation rather than inflation during the past 20 years and that will shape how they perceive the balance of risks going forward. After the Great Depression of the 1930s, fears of deflation lingered well into the 1950s and policymakers’ resulting complacency toward inflation led to the inflation spike of the 1970s. We are at a similar point again. The Fed will remain a massive buyer of Treasury bonds, even as the economy recovers because it will not want to risk higher yields undermining growth. Even if inflation starts to rise, the Fed will justify a continued easy stance on the grounds that inflation has fallen far short of its 2% target for many years. Given the combination of a global blowout in central bank balance sheets and the retreat from globalization, the scene will be set for inflation to surprise on the upside. But this may not occur for several years because the recession will create a lot of spare capacity and deflation is a greater near-term threat than inflation. We have long argued that a sustained upturn in inflation would be preceded by a final bout of deflation. The revival of inflation may be gradual but its insidious nature ultimately will make it more dangerous. It seems inevitable that there will have to be monetization of public sector debt, not only in the US but in other major economies. Once investor confidence returns, the demand for government bonds will recede and yields will be under upward pressure. Financial repression may help contain the rise, but that cannot be a long-term solution. In the end, central banks will be the bond buyers of last resort and ultimately it will have to be written off via making the debt effectively non-maturing. If the economic picture continues to deteriorate could central banks use quantitative easing to start buying assets such as equities and real estate? Current legislation prevents such purchases in the case of the Fed and European Central Bank. Of course, legislation can always be changed but the Fed would be reluctant for Congress to change the Federal Reserve Act. That could open a can of worms including amendments such as requiring regular audits of policy decisions and altering how regional presidents are chosen. But it will not be the Fed’s decision and if things get bad enough then nothing should be ruled out. An Accelerated Move To Virtual Activity? The restrictions on travel and public meetings and the closure of many businesses have forced companies to embrace online ways of conducting operations. And the same applies to schools and universities. In many cases, companies may find that virtual meetings between far-flung offices work rather well. This could cause a major rethink about future spending on business travel. Replacing travel with virtual meetings not only saves on airfares but also frees up employee time and reduces stress. And the improvements in communication technology make virtual meetings almost as good as the real thing. Of course, this is not a great story for airlines. The same arguments can be made for education but are slightly less compelling because of the social dimension. Mixing with friends and peers is one of the big attractions for students and most would be loath to give this up. And for working parents, it is not feasible to have children stuck at home. Nonetheless, at the post-secondary level, there could be a move to more online teaching. Another consequence of the current crisis has been a forced shift to more online shopping. This trend was already well established but is now likely to accelerate. Those retailers who fail to adapt will fall by the wayside. Market Implications As noted at the outset, it is hard to make predictions without knowing how the virus will progress. But we know a few things. First, there is not much scope for bond yields to fall from current levels. Second, equity valuations have improved as a result of the collapse in prices. Third, monetary policy will remain supportive of markets for a long time. On this basis, it is easy to conclude that stocks should beat bonds handsomely over the medium and long term. The short-term picture is cloudier. If the recession is short-lived and economic activity rebounds strongly, then we currently have a good buying opportunity for stocks. But there is no way to make a prediction about this with any conviction. The case for a strong recovery is that policy is massively stimulative and there will be a lot of pent-up demand. The case for a slow and drawn-out recovery is that consumers and businesses will be left with greatly weakened balance sheets and the loss of small businesses and associated jobs could be a lasting problem. A final issue is that fears of another virus wave could weigh on consumer and business confidence. Initially, there will be some extremely strong quarters of growth but beyond that, the odds favor a drawn-out recovery rather than a vigorous one. Faced with such uncertainty, one strategy is to rely on technical indicators rather than economic forecasts as a judge of whether it is safe to rebuild positions in risk assets. This gives some reason for encouragement as measures of sentiment are at depressed extremes, typically seen only at major bottoms. And this is supported by momentum indicators at oversold extremes. However, a word of caution: these indicators make the case for a near-term bounce but say nothing about the durability of any rally. For some time, non-US markets have looked more appealing than Wall Street from a valuation perspective. That remains the case, but there is an important caveat. Thus far, the virus has been more of a problem for the developed countries than emerging ones (China and Iran excepted). It remains to be seen whether Africa, and Latin America and other countries in Asia and the Middle East can avoid a catastrophic spread of the virus. It could potentially be disastrous given the poor infrastructure and lack of government resources in those regions. Moreover, a shift away from globalization is not bullish for the emerging world. Some positions in gold are a good hedge given current uncertainties and the fact that inflation fears will rise long before actual inflation picks up. In normal circumstances, the extraordinary rise in the US budget deficit would be bearish for the US dollar. But other countries are following the same path so in relative terms, the US is no worse off. And there is still no serious competition to the dollar as the global reserve currency. Thus, while the dollar might weaken somewhat, it should not be a major source of risk to US assets. In closing, it is impossible to provide the certainty and high-conviction predictions that investors crave. That makes it rash to make aggressive bets on how things will play out in the economy and markets. At BCA, we favor equities over bonds but advise continued near-term caution. The bottoming process in equities could be volatile and drawn-out. Building positions gradually seems the most sensible strategy. Martin H. Barnes, Senior Vice President Chief Economist mbarnes@bcaresearch.com Footnotes 1 For an estimate of the virus impact on a range of economies, please see the recent OECD report “Evaluating the initial impact of COVID-19 containment measures on economic activity”. Available at: www.oecd.org 2 The report and underlying data are available at www.newyorkfed.org. 3 For example, the retreat from globalization was discussed in our 2015 Outlook report published at the end of 2014.

Dear Client, This week’s report is written by BCA’s chief economist, Martin Barnes. Martin explores the myriad ways the pandemic could influence long-term economic and financial trends. I trust you will find his report very insightful. Best regards, Peter Berezin, Chief Global Strategist Making predictions about the economic and market outlook seems a futile exercise in the midst of such massive uncertainty. The deluge of articles about COVID-19 merely serves to highlight that nobody really knows how things will play out in the year ahead. Much depends on whether an effective vaccine or treatment becomes available within a reasonable timescale and that remains an open question. Social and economic disruption will continue to intensify until the spread of the virus starts to abate. One thing is certain. Economic activity around the world faces its biggest contraction in modern times. Declines in second quarter GDP will be mind-numbingly bad in a wide range of countries, especially those that have instituted lockdowns and the closure of non-essential businesses. According to the OECD, the median economy faces an initial output decline of around 25% as a result of shutdowns and restrictions.1 Chart 1A Meltdown In Economic Activity

A Meltdown In Economic Activity

A Meltdown In Economic Activity

Estimates for the drop in US real GDP in the second quarter range as high as 50% at an annual rate. To put this into perspective, the peak-to-trough decline in US real GDP in the 2007-09 recession was a mere 4% over six quarters, and that felt catastrophic at the time. The New York Fed’s weekly economic index2 has already fallen to the lows of 2008 and worse is still to come (Chart 1). Could things be as bad as the 1930s Great Depression when US real GDP contracted by 25% over a three-year period? That would require an extreme apocalyptic view about the progression of the virus and does not bear thinking about. I am not that gloomy. Policymakers are acting aggressively to limit the economic damage. Central banks are flooding the system with liquidity and the cost of money is negligible. Meanwhile, fiscal caution has been thrown to the wind with massive government stimulus in many countries. While this will not prevent a deep recession, it will minimize the downside risks and support the eventual rebound. Markets are understandably in a deep funk because it is hard to price unknown risks. If this is no more than a two-quarter economic downturn followed by a sharp recovery, then a good buying opportunity in risk assets is in place given that monetary policy will stay hyper accommodative for a considerable time. If the downturn lingers much longer than that, then equities remain at risk. While loath to make a prediction, I am uncharacteristically tending to the more optimistic side. Let’s make the heroic assumption that we are not in an end of days scenario and that this crisis will pass at some point in the next year- hopefully sooner than later. What are some of the longer-run implications? A few come to mind. The backlash against globalization will gather impetus. Public sector debt will rise to unimaginable peacetime levels. Meanwhile, the crisis puts the final nail in the coffin of the private sector Debt Supercycle. Monetary policy will err on the side of ease for a very long time. The way that companies and other institutions have been forced to adapt to the crisis could trigger lasting changes in how they operate. Globalization In Full Retreat Chart 2A Retreat From Globalization

A Retreat From Globalization

A Retreat From Globalization

The peak of globalization has been a central part of the BCA view for several years.3 Long before the current crisis, it was clear that anti-globalization forces were gathering strength, illustrated by increased trade barriers, a backlash against inward migration in many countries, and reduced flows of foreign direct investment (Chart 2). The Trump Administration’s imposition of tariffs and the Brexit vote were two of the more obvious examples of the change in attitudes. The supply-chain interruptions caused by factory shutdowns in China will reinforce the view that shifting production to cheaper-cost countries overseas went too far. At a minimum, it seems inevitable that many companies will seek to reduce their reliance on a single producer for critical components. On the medical front, one striking fact to emerge was that China supplies around 80% of US antibiotics. There will be massive pressure to develop greater homegrown supplies of medical supplies and other products deemed critical for economic and national security. The crisis also has led to a breakdown of the Schengen Area of open borders within the European Union (EU). Many member countries have reinstituted border controls and it is unclear when these might be removed. The free movement of people is a core principle of the EU. Meanwhile, the Maastricht Treaty rules on fiscal discipline, a key element of economic union, have been thrown out of the window. Even Germany has bowed to the pressure of relaxing fiscal constraints. Finally, a worsening situation for the already troubled Italian banking system will threaten EU financial stability. Overall, the crisis will leave a huge question mark over the long-term viability of the EU. Globalization was a major force behind disinflation as production shifted to low-cost producers. A reversal of this trend will thus be inflationary, at the margin. For many, this will be a price worth paying if it means increased job security and reduced vulnerability of supply chains. But the shift away from globalization will not be the only trend that threatens an eventual resurgence of inflation. The Explosion In Government Debt: Last Gasp Of The Debt Supercycle BCA introduced the concept of the Debt Supercycle more than 40 years ago to describe the actions of policymakers to pump up demand rather than allow financial imbalances to be fully unwound during economic downturns. This inevitably meant that each new cycle began with a higher level of financial imbalances. As indebtedness rose, the economic costs of a financial cleansing increased, requiring ever-more desperate policy measures to shore things up. Unfortunately, such actions merely created the conditions for greater excesses and imbalances down the road. For example, the Federal Reserve’s aggressive response to the bursting of the tech bubble in 2000 helped set the scene for the even bigger housing bubble later in the decade. In that sense, the Debt Supercycle was a self-reinforcing trap that was bound to end badly, and that occurred in 2007. Chart 3The US Household Love Affair With Debt Died A Decade Ago

The US Household Love Affair With Debt Died A Decade Ago

The US Household Love Affair With Debt Died A Decade Ago

Our discussion of the US Debt Supercycle was focused largely on the private sector because that is where rising imbalances posed the greatest threat to economic and financial stability. Rising public sector imbalances were less of a concern because governments do not finance themselves through the banking sector. Moreover, unlike the private sector, taxes can always be raised to boost revenues or, in extremis, the authorities can resort to the printing press. At the end of 2014, we wrote that the Debt Supercycle was dead. By that, we meant that easing policy would no longer be able to encourage a new cycle of leverage-financed private-sector spending. The downturn of 2007-09 was a turning point in attitudes toward debt, much in the way that those who lived through the Great Depression were financially conservative for the rest of their lives. Our view has been vindicated by the fact the ratio of household debt to income has decisively broken its pre-housing bubble uptrend and has failed to revive in the face of record-low interest rates (Chart 3). Corporate borrowing has been strong, but largely to finance stock buybacks and M&A activity. Capital spending has been disappointing this cycle, despite strong profits and margins. The current deep downturn will add a further nail in the coffin of the private sector Debt Supercycle. The shock of the recession and destruction of wealth will leave a legacy of increased financial caution with households wanting to build precautionary savings and companies striving to repair damaged balance sheets. It would not be a surprise to see the US personal saving rate head back to the double-digit levels of the early 1980s. While the private sector embraces greater financial conservatism, we are witnessing the start of an extraordinary surge in public sector deficits and debt from already high levels. Chart 4A Bad Starting Point For A Surge In The Federal Deficit

A Bad Starting Point For A Surge In The Federal Deficit

A Bad Starting Point For A Surge In The Federal Deficit

Budget deficits automatically rise during recessions because tax receipts drop and spending on unemployment and welfare programs goes up (Chart 4). In the past, the starting point for deficits generally was low before a recession took hold. This time, the federal deficit has breached 5% of GDP when the economy was doing fine. With the current recession set to be deeper than in 2007-09 and fiscal stimulus likely to end up much more than the initial $2 trillion package, the deficit will far exceed the previous post-WWII peak of almost 10% of GDP, reached in fiscal 2009. The ratio of federal debt to GDP will soar past 100% within the next few years, exceeding the peak reached in WWII. A speedy decline in WWII debt burdens was helped by a sharp rebound in economic activity, supported by a powerful combination of demographics (the post-WWII baby boom) and pent-up demand. Real GDP grew at an average annualized pace of 4.3% in both the 1950s and 1960s. Unfortunately, slower population growth means that growth in the next one and two decades will be less than half that pace. At the same time, the federal deficit will be under upward pressure because of the impact of an aging population on healthcare and social security. In other words, restoring order to fiscal finances through normal measures (growth and/or austerity) will be an impossible task. High levels of government debt are perfectly manageable when private sector savings are plentiful, interest rates are negligible, and investors seek the safety of low-risk bonds. Thus, $1 trillion US federal deficits have not prevented Treasury yields from falling to all-time lows. However, such conditions will not last indefinitely. The timing of when bloated budget deficits start to impact markets and thus the economy will partly depend on the actions of the Fed. Monetary Policy: Is There A Limit To What It Can Do? Gone are the days when monetary policy was a rather technical exercise: tweaking the level of interest rates to ensure that money and credit trends delivered the economic growth consistent with low and stable inflation. In the past decade, the old rule book has been discarded with policymakers forced to take ever-more extreme measures to prevent total collapse of the economic and financial system. The 2007-9 downturn was easier to deal with than the current crisis. The primary problem a decade ago was a financial rather than economic seizure. While policymakers had to be creative, the main task was to shore up systemically important financial institutions and inject enough liquidity into the system to restore normal market functioning. And it worked. This time, the issue is an economic not financial seizure and associated liquidity strains are a symptom, not the primary problem. The immediate role of central banks is again to ensure that the financial system continues to function by injecting whatever amounts of liquidity are necessary. But monetary policy cannot directly bail out all the businesses that face bankruptcy or help those that have lost their jobs. That is the role of fiscal policy. What central banks can do is print money to finance the rise in budget deficits. During WWII, the Fed had an agreement with the Treasury Department to peg the level of long-term yields below 2.5% and this arrangement persisted until 1951, long after the war ended. This ensured that a post-war rebound in private credit demand would not cause a spike in interest rates that might short-circuit the recovery. We could well see a similar arrangement in the coming years, though it might be an informal rather than publicized agreement. The key point is that the Fed will be massively biased toward easy policy for many years. The current generation of central bankers have experienced periodic threats of deflation rather than inflation during the past 20 years and that will shape how they perceive the balance of risks going forward. After the Great Depression of the 1930s, fears of deflation lingered well into the 1950s and policymakers’ resulting complacency toward inflation led to the inflation spike of the 1970s. We are at a similar point again. The Fed will remain a massive buyer of Treasury bonds, even as the economy recovers because it will not want to risk higher yields undermining growth. Even if inflation starts to rise, the Fed will justify a continued easy stance on the grounds that inflation has fallen far short of its 2% target for many years. Given the combination of a global blowout in central bank balance sheets and the retreat from globalization, the scene will be set for inflation to surprise on the upside. But this may not occur for several years because the recession will create a lot of spare capacity and deflation is a greater near-term threat than inflation. We have long argued that a sustained upturn in inflation would be preceded by a final bout of deflation. The revival of inflation may be gradual but its insidious nature ultimately will make it more dangerous. It seems inevitable that there will have to be monetization of public sector debt, not only in the US but in other major economies. Once investor confidence returns, the demand for government bonds will recede and yields will be under upward pressure. Financial repression may help contain the rise, but that cannot be a long-term solution. In the end, central banks will be the bond buyers of last resort and ultimately it will have to be written off via making the debt effectively non-maturing. If the economic picture continues to deteriorate could central banks use quantitative easing to start buying assets such as equities and real estate? Current legislation prevents such purchases in the case of the Fed and European Central Bank. Of course, legislation can always be changed but the Fed would be reluctant for Congress to change the Federal Reserve Act. That could open a can of worms including amendments such as requiring regular audits of policy decisions and altering how regional presidents are chosen. But it will not be the Fed’s decision and if things get bad enough then nothing should be ruled out. An Accelerated Move To Virtual Activity? The restrictions on travel and public meetings and the closure of many businesses have forced companies to embrace online ways of conducting operations. And the same applies to schools and universities. In many cases, companies may find that virtual meetings between far-flung offices work rather well. This could cause a major rethink about future spending on business travel. Replacing travel with virtual meetings not only saves on airfares but also frees up employee time and reduces stress. And the improvements in communication technology make virtual meetings almost as good as the real thing. Of course, this is not a great story for airlines. The same arguments can be made for education but are slightly less compelling because of the social dimension. Mixing with friends and peers is one of the big attractions for students and most would be loath to give this up. And for working parents, it is not feasible to have children stuck at home. Nonetheless, at the post-secondary level, there could be a move to more online teaching. Another consequence of the current crisis has been a forced shift to more online shopping. This trend was already well established but is now likely to accelerate. Those retailers who fail to adapt will fall by the wayside. Market Implications As noted at the outset, it is hard to make predictions without knowing how the virus will progress. But we know a few things. First, there is not much scope for bond yields to fall from current levels. Second, equity valuations have improved as a result of the collapse in prices. Third, monetary policy will remain supportive of markets for a long time. On this basis, it is easy to conclude that stocks should beat bonds handsomely over the medium and long term. The short-term picture is cloudier. If the recession is short-lived and economic activity rebounds strongly, then we currently have a good buying opportunity for stocks. But there is no way to make a prediction about this with any conviction. The case for a strong recovery is that policy is massively stimulative and there will be a lot of pent-up demand. The case for a slow and drawn-out recovery is that consumers and businesses will be left with greatly weakened balance sheets and the loss of small businesses and associated jobs could be a lasting problem. A final issue is that fears of another virus wave could weigh on consumer and business confidence. Initially, there will be some extremely strong quarters of growth but beyond that, the odds favor a drawn-out recovery rather than a vigorous one. Faced with such uncertainty, one strategy is to rely on technical indicators rather than economic forecasts as a judge of whether it is safe to rebuild positions in risk assets. This gives some reason for encouragement as measures of sentiment are at depressed extremes, typically seen only at major bottoms. And this is supported by momentum indicators at oversold extremes. However, a word of caution: these indicators make the case for a near-term bounce but say nothing about the durability of any rally. For some time, non-US markets have looked more appealing than Wall Street from a valuation perspective. That remains the case, but there is an important caveat. Thus far, the virus has been more of a problem for the developed countries than emerging ones (China and Iran excepted). It remains to be seen whether Africa, and Latin America and other countries in Asia and the Middle East can avoid a catastrophic spread of the virus. It could potentially be disastrous given the poor infrastructure and lack of government resources in those regions. Moreover, a shift away from globalization is not bullish for the emerging world. Some positions in gold are a good hedge given current uncertainties and the fact that inflation fears will rise long before actual inflation picks up. In normal circumstances, the extraordinary rise in the US budget deficit would be bearish for the US dollar. But other countries are following the same path so in relative terms, the US is no worse off. And there is still no serious competition to the dollar as the global reserve currency. Thus, while the dollar might weaken somewhat, it should not be a major source of risk to US assets. In closing, it is impossible to provide the certainty and high-conviction predictions that investors crave. That makes it rash to make aggressive bets on how things will play out in the economy and markets. At BCA, we favor equities over bonds but advise continued near-term caution. The bottoming process in equities could be volatile and drawn-out. Building positions gradually seems the most sensible strategy. Martin H. Barnes, Senior Vice President Chief Economist mbarnes@bcaresearch.com Footnotes 1 For an estimate of the virus impact on a range of economies, please see the recent OECD report “Evaluating the initial impact of COVID-19 containment measures on economic activity”. Available at: www.oecd.org 2 The report and underlying data are available at www.newyorkfed.org. 3 For example, the retreat from globalization was discussed in our 2015 Outlook report published at the end of 2014.

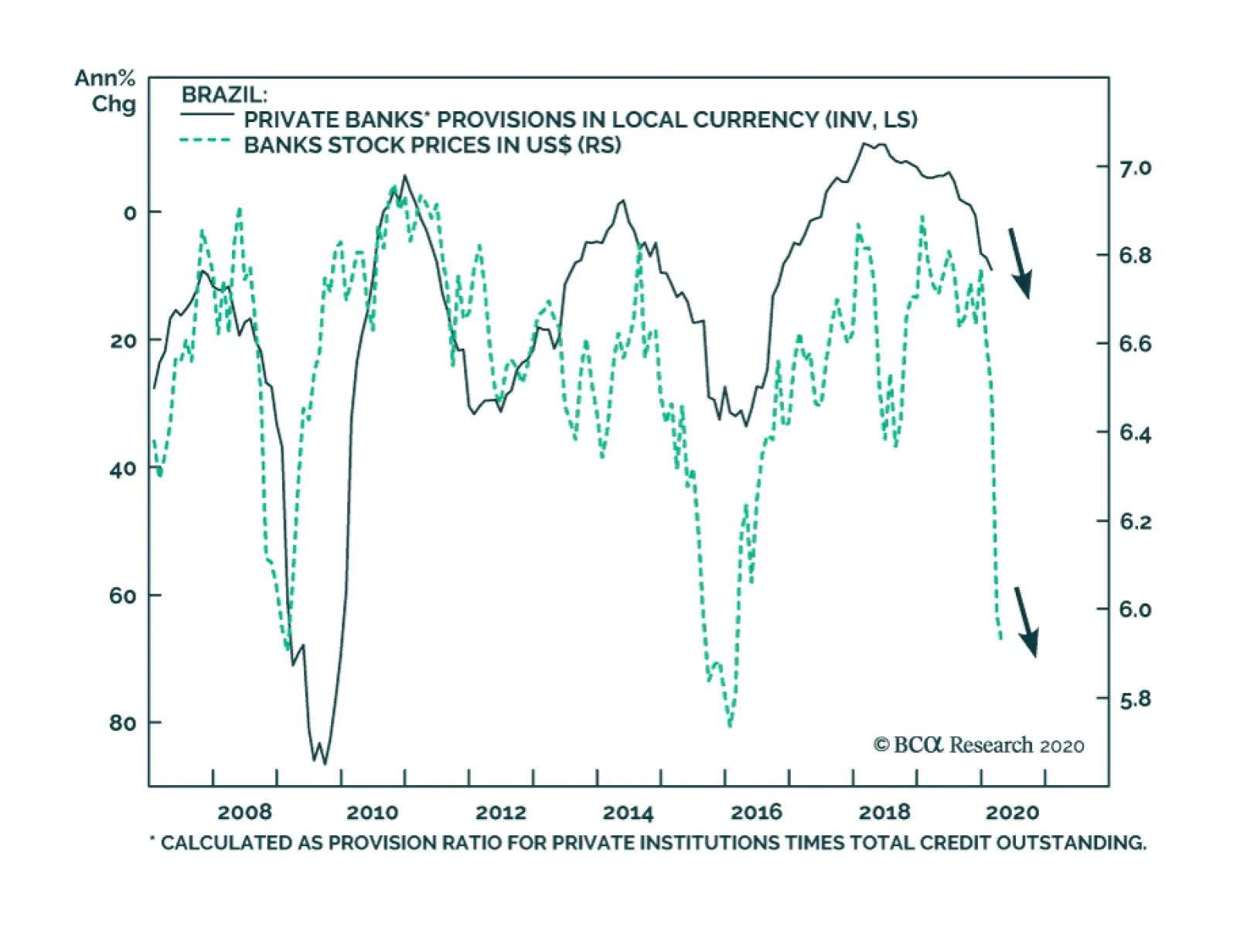

On Tuesday, BCA Research's Emerging Markets Strategy service concluded that the cyclical outlook for Brazilian bank stocks has worsened further due to the COVID-19 pandemic, despite the fact that valuations have improved. Brazilian banks have plunged 55% in…

Favor Defensive Tech

Favor Defensive Tech

In our latest Weekly Report we boosted the S&P data processing index to overweight from previously underweight. Data processing stocks are a services-based defensive tech index that typically thrive in deflationary and recessionary environments, according to empirical evidence (see chart). We are currently in recession, thus a deflationary impulse will grip the economy and investors will flock to defensive tech stocks when growth is scarce. Tack on the spike in the greenback, and the disinflationary backdrop further boosts the allure of these tech services stocks (third panel). Beyond the recessionary related tailwinds, data processing stocks should also enjoy firming relative demand. While the two bellwether stocks, V and MA, will suffer from the decrease in consumption that requires physical visits and from select services outlays that are severely affected by the coronavirus, online spending by households and corporations should at least serve as a partial offset. Bottom Line: We recently lifted the S&P data processing index to overweight from previously underweight. The ticker symbols for the stocks in this index are: BLBG: S5DPOS – ADP, V, MA, PYPL, FIS, FISV, GPN, PAYX, FLT, BR, JKHY, WU, ADS.

Highlights Recommended Allocation

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality

The outlook for markets over the next few months is highly uncertain. On the optimistic side, new COVID-19 cases are probably close to peaking (for now), and so equities could continue to rally. But there are many risks too. Growth numbers will be horrendous for some months. Second-round effects (corporate defaults, problems in EM and with euro zone banks, for example) will emerge. We recommend a balanced portfolio, robust both for risk-on rallies and a further sell-off. We stay overweight equities versus bonds. Government bonds will not provide significantly positive returns even in a severe recession. Thus, over the next 12-months, equities are likely to outperform them. But we leaven the equity overweight with a “minimum volatility” strategy, overweight the low-beta US market, and more stable sectors such as Healthcare and Technology. Within bonds, we stay underweight government bonds, and raise Investment Grade credit to overweight, given the Fed’s backstop. Even in a risk-on rally, government yields will not rise quickly so we recommend a neutral stance on duration. The massive stimulus will eventually be inflationary, so we recommend TIPS, which are very cheaply valued. We are overweight cash and gold as hedges against further market turbulence. Among alternatives, macro hedge funds and farmland look attractively defensive now. We would start to look for opportunities in private debt (especially distressed debt) as the recession advances. Commodity futures are attractive as an inflation hedge. Overview Playing The Optionality From the start of the crisis, we argued that markets would bottom around the time when new cases of COVID-19 peaked. At the end of March, there were clear signs that this would happen in April, with Italy and Spain having probably already peaked and the US, if it follows the same trajectory, being only two or three weeks away (Chart 1). Chart 1Close To A Peak In New Cases?

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality

But what happens next? A relief rally is likely, as often happens in bear markets – and indeed one probably started with the three-day 18% rise in US equities in the last week of March. Note, for example, the strong rallies in spring 2008 and summer 2000 before the second leg down in those bear markets (Chart 2). Chart 2Mid Bear Market Rallies Are Common

Mid Bear Market Rallies Are Common

Mid Bear Market Rallies Are Common

However, there is still a lot of potential bad news for markets to digest. Global growth has collapsed, as a result of people in many countries being forced to stay at home. US GDP growth in Q2 could fall by as much as 10% quarter-on-quarter (unannualized). Horrendously bad data will come as a shock to investors over the coming months. Despite the unprecedented stimulus measures from central banks and governments worldwide (Chart 3), nasty second-round effects are inevitable. Given the high level of corporate debt in the US, defaults will rise, to perhaps above the level of 2008-9 (Chart 4). EM borrowers have almost $4 trillion of foreign-currency debt outstanding, and will struggle to service this after the rise in the dollar and wider credit spreads. Euro area banks are poorly capitalized and have high non-performing debt levels left over from the last recession; they will be hit by a new wave of bankruptcies. Undoubtedly, there are some banks and hedge funds sitting on big trading losses after the drastic sell-off and stomach-churning volatility. Mid-East sovereign wealth funds will unload more assets to fill fiscal holes left by the collapsed oil price. Chart 3Massive Stimulus Everywhere

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality

Chart 4Possible Second-Round Effects

Possible Second-Round Effects

Possible Second-Round Effects

There is also the question of when the pandemic will end. We are not epidemiologists, so find this hard to judge (but please refer to the answers from an authority in our recent Special Report1). The coronavirus will disappear only when either enough people in a community have had the disease to produce “herd immunity,” or there is a vaccine – which is probably 18 months away. Some epidemiologists argue that in the UK and Italy 40%-60% of the population may have already had COVID-19 and are therefore immune.2 But an influential paper from researchers at Imperial College suggested that repeated periods of lockdown will be necessary each time a new wave of cases emerges3 (Chart 5). Chart 5More Waves Of The Pandemic To Come?

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality

At the end of March, global equities were only 23% off their mid-February record high – and were down only 34% even at their low point. That doesn’t seem like enough to fully discount all the potential pitfalls over coming months. This sort of highly uncertain environment is where portfolio construction comes in. We recommend that clients position their portfolios with optionality to remain robust in any likely outcome. There are likely to be rallies in risk assets over coming months, particularly when the coronavirus shows signs of petering out. There is significant asymmetric career risk for portfolio managers here. No portfolio manager will be fired for missing the pandemic and underperforming year-to-date (though some may because their firms go out of business or retrench). But a PM who misses a V-shaped rebound in risk assets over the rest of the year could lose their job. This will provide a strong incentive to try to pick the bottom. Chart 6Bond Yields Can't Go Much Lower

Bond Yields Can't Go Much Lower

Bond Yields Can't Go Much Lower

Government bond yields are close to their theoretical lows. The 10-year US Treasury yield is 0.6% and it unlikely to fall below 0% even in a severe recession (since the Fed has stated that it will not cut short-term rates below 0%). In other countries, the low for yields has turned out to be around -0.3% to -0.9% (Chart 6). The total return from risk-free bonds, therefore, will be close to zero even in a dire economic environment (Table 1). This means that the call between bonds and equities comes down to whether equity prices will be higher or lower in 12-months. Quite likely, they will be higher. Given this, and the optionality of participating in rebounds, we maintain our overweight on equities versus bonds. We would, however, be inclined to lower our equity weighting in the event of a big rally in stocks over the next few months. Table 1Not Much Room For Upside From Bonds

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality

Table 2Bear Markets Are Often Much Worse

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality

But there are also many downside risks. In the past two recessions, global equities fell by 50%-60% (Table 2). Despite the much worse economic environment this time, the peak-to-trough decline is so far much more limited. Moreover, valuations are not particularly compelling yet (Chart 7). To leaven our overall overweight on equities, we recommend a “minimum volatility” strategy, with tilts towards the low-beta US market, and some more defensive sectors such as Healthcare and Technology. China and China-related stocks also look somewhat attractive, since that country got over the coronavirus first, and is responding with a big increase in infrastructure spending (Chart 8). To hedge against downside risk, we also leave in place our overweights in cash and gold. Chart 7Equities Are Not Yet Super Cheap

Equities Are Not Yet Super Cheap

Equities Are Not Yet Super Cheap

Chart 8China Infra Spending To Rise

China Infra Spending To Rise

China Infra Spending To Rise

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking – About The Coronavirus Have We Seen The Bottom In Equity Markets? Chart 9Watch Closely COVID-19

Quarterly Portfolio Outlook: Playing The Optionality

Quarterly Portfolio Outlook: Playing The Optionality