Sectors

Feature We spent the past two weeks visiting and exchanging views with our clients in Asia. We presented our view that the ongoing stimulus measures are beginning to bear fruit in terms of stabilizing China’s economic activity, and that we expect the economic slowdown to bottom early next year. In addition, Chinese policymakers are signaling their willingness to accelerate stimulus on both monetary and fiscal fronts, which should mitigate the downside risks and help the economy regain traction in 2020. Interestingly, our view sparked divergent responses: clients outside of China were more upbeat about the state of the Chinese economy than clients from mainland China. While few investors we spoke to showed concerns over an imminent “hard landing” in China’s economy or systemic risk from China’s financial system, our mainland Chinese clients remain skeptical that the ongoing stimulus will be sufficient to revive the economy. They were also worried that financial regulations may be too restrictive to generate the amount of money growth needed for the economy. Another interesting observation was that while being pessimistic about the economy, our mainland Chinese investors share our assessment that Chinese domestic stocks still have some upside in the coming year. On the other hand, global investors, who are more sanguine about China’s economic recovery, prefer to wait on the sidelines before favoring Chinese investable stocks (Chart 1). Chart 1AA Tale Of Two Markets: Onshore Outperforms Global Markets...

A Tale Of Two Markets: Onshore Outperforms Global Markets

A Tale Of Two Markets: Onshore Outperforms Global Markets

Chart 1B...While Offshore Underperforms

...While Offshore Underperforms

...While Offshore Underperforms

Below we present some of the top questions that were posed by investors during our trip, along with our answers. We recap the conclusions of our view, and draw out the investment implications of the differences between the sentiments towards China’s equity markets, in the last question of the report. Q: Recent economic data suggests a weakening Chinese economy. Why do you think the economy will reach a bottom in 2020? Historically, China’s credit formation has consistently led economic activity by about three quarters (Chart 2). Even though credit growth this year has not been as strong as in previous expansionary cycles, a turning point in the credit impulse occurred at the start of 2019. This suggests that economic activity should turn around within the next two quarters. Chart 2Expecting A Turn In Q1 2020

Expecting A Turn In Q1 2020

Expecting A Turn In Q1 2020

Chart 3Emerging Green Shoots

Emerging Green Shoots

Emerging Green Shoots

Furthermore, despite weakening headline economic data, some underlying components indicate promising improvements (Chart 3): Growth in infrastructure investment has ticked up modestly in the past couple months, and is set to improve further. The State Council mandated local governments to allocate the proceeds from special-purpose bond sales to infrastructure projects by the end of October. This, combined with a frontloading of next year’s local government bonds, should lend support to infrastructure spending in the coming months. After fluctuating in and out of contraction for a year, growth in auto manufacturing production picked up in August and remained positive through October. This improvement is due to less contraction in auto sales and a faster reduction in auto inventories. Moreover, electricity output surged in October, which also indicates that growth may be gaining momentum. Chart 4Trade Should Improve Into 2020

Trade Should Improve Into 2020

Trade Should Improve Into 2020

Lastly, global financial conditions have eased significantly and credit growth has picked up worldwide, which should help support global demand. Even though Sino-US trade negotiations are ongoing, our baseline view is that a “Phase One” trade deal will be inked in the next couple months. Eased trade tensions and even some rollbacks in the existing tariffs on Chinese export goods, coupled with improved global demand, should provide some tailwinds to China’s external sector (Chart 4). Q: What is your outlook on China’s economic policy for 2020? The Chinese economic growth model remains reliant on credit formation and capital investment. Therefore, the sustainability of an economic recovery depends on whether Chinese policymakers are willing to keep the stimulus wheel turning. Chart 5A Sign Of A Policy Shift

A Sign Of A Policy Shift

A Sign Of A Policy Shift

For investors favoring China-related assets, the good news is that there has been an increasing urgency in policymakers’ tone to support economic growth since September. Capex growth from state-owned enterprises (SOEs) has increasingly outpaced the private sector, which is significant: A sustained rotation in the pace of SOE vis-à-vis private sector capex marked a turning point in the 2015-2016 cycle, when Chinese policymakers’ imperative to supporting growth outweighed their desire to continue with structural reforms (Chart 5). We do not expect a 2016-style drastic rise in SOE capex growth next year, because the current economic slowdown is not as severe or prolonged as in 2015. Nonetheless, the rotation in capex growth is an important signal that Chinese policymakers may be more willing to stimulate the economy by again allowing the state sector to upstage the private sector. In the meantime, we expect that some pro-growth “policy adjustments” will be deployed in 2020: Chart 6Infrastructure Investment Likely To Rise

Infrastructure Investment Likely To Rise

Infrastructure Investment Likely To Rise

Monetary policy will incrementally ease, with one to two 10-15bps loan prime rate (LPR) cuts in the next 3-6 months. At the same time, China’s central bank (PBoC) will keep bank liquidity ample and commercial banks’ funding costs relatively low, by continuing frequent liquidity injections to stabilize the interbank rate. A further cut in the reserve requirement ratio (RRR) is also highly likely. Keeping banks well capitalized will partially mitigate the pressure commercial banks face from falling profit margins and rising credit defaults. Accommodative monetary conditions will also support more stimulus on the fiscal front. We expect that the National People’s Congress in March 2020 will approve higher quotas on the issuing of local government bonds. Chinese state-owned commercial banks will continue to be the main buyers for local government bonds. A portion of 2020 local government special-purpose bond issuance will be frontloaded to the remainder of 2019 and into the first months of next year. Relaxed capital requirements will likely boost local governments’ infrastructure project funding and expenditures. Our model suggests infrastructure spending should pick up from the current 3.3% year-on-year, to close to 7.5% in the second and third quarters next year (Chart 6). There are subtle signs that the government is starting to relax restrictions on the real estate sector. Land sales by local governments have increased since mid-2019, and the trend will continue into 2020 (Chart 7). Income from land sales accounts for 70% of local government revenues, thus allowing more land sales should help fund a larger local government spending budget next year. Declining government subsidies to shantytown renovation (namely the Pledged Supplementary Lending, or PSL) have recently abated and will likely continue to improve (Chart 8). Chart 7Some Improvement To Come In The Real Estate Sector

Some Improvement To Come In The Real Estate Sector

Some Improvement To Come In The Real Estate Sector

Chart 8Government Subsidies Will Continue

Government Subsidies Will Continue

Government Subsidies Will Continue

December’s Central Economic Work Conference (CEWC) will set policy priorities for the following year. We think Chinese policymakers will make economic growth a top priority for 2020. Credit growth swelled in the first quarter of 2019 following the December 2018 CEWC, and we expect a surge in early 2020 as well.Due to the unusually high credit growth in January this year and the seasonal factor next year (Chinese New Year will fall in January 2020), the surge in credit growth, on a year-over-year basis, will more likely be muted until towards the end of the first quarter and into the second quarter. Investors should overweight Chinese investable stocks in the next 6-12 months, but need to watch for more positive signs to upgrade tactical stance. Beyond the second quarter, however, the outlook gets cloudier as tension from the US election heats up and President Trump may change his trade negotiation strategies with China.1 This may have implications on China’s domestic policies. But for now, our baseline view is that Chinese policymakers will incrementally accelerate the pace of economic stimulus throughout next year. Q: Monetary policy has been accommodative for more than a year, but capex this year has fallen below market expectations compared with past cycles. How will further stimulus help to revive investment and economic growth next year? In short, our answer is this: interest rate cuts alone will not be enough to boost economic growth in China. Capex, and growth more generally, will only revive through synchronized policy support from the Chinese authorities. In a previous report2 we discussed that the lack of response to monetary easing has been due to a less effective monetary policy transmission mechanism, a reactive and reluctant central bank, and a debt-loaded corporate sector. More importantly, the “half-measured” stimulus has been preferred by Chinese authorities in this cycle, as they prioritized financial de-risking over growth and have significantly tightened financial regulations since 2016. Given the expected policy pivot to a more pro-growth stance in the coming year, the following underlines our conviction that capex should pick up in 2020. Modern Money Theory (MMT), with Chinese characteristics:3 local governments will ramp up debt again, and this quasi-fiscal stimulus will be a key support to the economy in 2020. During the 2015-2016 cycle, aggressive interest cuts did not result in a significant uptick in credit growth. Bank lending was not the core driver for economic recovery in 2016. The economy only bottomed following an unprecedented issuance of local government bonds after mid-2015 (Chart 9). Chinese authorities will keep a “back door” open: even though overall tight financial regulations will remain intact, we expect the PBoC to allow a more moderate contraction in shadow banking (Chart 10). This will provide smaller banks and enterprises access to tap into bank credit. Importantly, this means the government will acquiesce to local governments in providing extra funding through shadow banking. We already see local government financing vehicles (LGFV) making a comeback in recent months. Chart 9A Chinese Version Of MMT

A Chinese Version Of MMT

A Chinese Version Of MMT

Chart 10The "Back Door" May Open Wider

The "Back Door" May Open Wider

The "Back Door" May Open Wider

Small- and medium-sized enterprises (SMEs) will benefit from lowered financing costs through the new LPR system. As we pointed out in our previous report,4 the new LPR regime is not intended as much to expand bank credit as to help struggling SMEs survive economic hardships. This, along with tax cuts, should provide SMEs some relief from capital constraints. Q. CPI has been rising sharply and is above the government’s inflation target of 3%. Will inflation prevent the PBoC from maintaining an easy monetary policy? Chart 11PBoC Likely To Capitulate To Producer Deflation

PBoC Likely To Capitulate To Producer Deflation

PBoC Likely To Capitulate To Producer Deflation

No. We think deflationary pressure in the industrial sector (measured by producer prices) poses a bigger threat to the economy, and that PBoC is more likely to loosen monetary policy than to tighten (Chart 11). Chart 12 shows that the recent surge in headline consumer prices has almost been entirely driven by soaring pork prices. There is compelling evidence from historical data that, unless core consumer price inflation also rises, climbing food prices alone will have a limited impact on PBoC policy (Chart 13). We think this approach is justified, as the necessity of “core feedthrough” is also what most central banks in the developed world look for when confronted with a detrimental supply shock. Chart 12Rising Pork Prices Have Driven Up Headline Inflation...

Rising Pork Prices Have Driven Up Headline Inflation...

Rising Pork Prices Have Driven Up Headline Inflation...

Chart 13...But Won't Be Driving Up Interest Rates

...But Won't Be Driving Up Interest Rates

...But Won't Be Driving Up Interest Rates

Chart 14A Wild Year For The RMB

A Wild Year For The RMB

A Wild Year For The RMB

Core CPI has been trending downwards since February 2018, and there is no evidence to suggest that food prices will drive up core CPI inflation (Chart 13, bottom panel). This, in combination with deflating producer prices, means that the probability of tighter monetary policy over the coming 6-9 months is extremely low. In fact, we expect, with high conviction, that the PBOC will guide the LPR lower in the coming months. Q: What is your view on the RMB for 2020? The RMB depreciated by 5% against the US dollar from its peak in February this year, mostly driven by market expectations of US tariffs imposed on Chinese export goods. Interest rate differentials, short-term capital flows, and economic fundamentals all have played much smaller roles in the RMB’s value changes (Chart 14). The depreciation in the CNY/USD this year has pushed the RMB close to two sigma below its long-term trend (Chart 15). As we expect a “Phase One” trade deal to be signed and trade tensions abating at least in the near term, the RMB will face upward pressure through the first half of 2020. The appreciation will also be supported by, although to a lesser extent, China’s improved domestic economy, rising demand for RMB-denominated assets, and a weakening US dollar (Chart 16). According to our model, the USD/CNY exchange rate can return to a 6.8-7.0 range, if a significant portion of the existing tariffs is rolled back (Chart 17). This range seems to be within the “fair value” of the RMB, justifiable by the current China-US interest rate differential (Chart 14, bottom panel). Chart 15Has The RMB Gone Too Far?

Has The RMB Gone Too Far?

Has The RMB Gone Too Far?

Chart 16Demand For RMB Assets On The Rise, Despite The Trade War

Demand For RMB Assets On The Rise, Despite The Trade War

Demand For RMB Assets On The Rise, Despite The Trade War

However, it would not be in the PBoC’s best interests to let the RMB appreciate too rapidly, because an appreciating Chinese currency would act as a deflationary force on China’s export and manufacturing sectors. The large differential in the China-US interest rates would allow PBoC to cut interest and/or RRR rates, to ease upward pressure on the RMB. Chart 17Tariff Rollbacks Will Push Up RMB

Tariff Rollbacks Will Push Up RMB

Tariff Rollbacks Will Push Up RMB

Q: How should equity investors position themselves towards China over the coming year? We are bullish on Chinese investable stocks in the next 6 to 12 months, based on our view that the Chinese economy will bottom in the first quarter next year, policy will be incrementally more supportive, and a “Phase One” trade deal will be signed soon. In the very near term, however, we think downside risks to Chinese equities are not trivial. We remain a neutral tactical stance, but will continue to watch for the following signs before upgrading our tactical call from neutral to overweight.5 Chart 18A (top panel) shows that cyclical stocks remain very depressed relative to defensives, underscoring investors’ lack of confidence in the Chinese economy and trade negotiations. A breakout in cyclicals versus defensives would signify a major improvement in investor sentiment towards Chinese economic growth. An uptick in the relative performance of industrials and consumer staples (Chart 18A, bottom panel). The negative sensitivity of industrials and positive sensitivity of consumer staples to monetary policy suggests that the relative performance between the two sectors may be a reflationary barometer for China’s economy. The relative performance trend remains off its recent low, which suggests that China’s existing policy stance has not yet turned more reflationary. A technical breakdown in the relative performance of healthcare and utility stocks (Chart 18B) would also be a bullish sign. Investable health care and utilities stocks have historically led China’s economic activity, core inflation and stock prices by 1-3 months. A technical breakdown in the relative performance of these sectors would signify that market participants anticipate a bottom in China’s economy. As we mentioned at the outset, we observed an interesting divergence in sentiment among our domestic versus global investors. This divergence is reflected in both the onshore and offshore stock markets; year to date, onshore A shares have outperformed global benchmarks by 5.6% (Chart 1, on page 1 of the report). Chart 18AWaiting For A Telltale Sign...

Waiting For A Telltale Sign...

Waiting For A Telltale Sign...

Chart 18B...Before A Tactical Upgrade

...Before A Tactical Upgrade

...Before A Tactical Upgrade

However, all of the outperformance in A shares occurred before end April, when the trade talks broke down and domestic credit expansion significantly slowed from the first quarter. Since May, the relative performance of A shares in US dollar terms has been mostly flat, reflecting the fact the markets were not expecting a significant stimulus forthcoming. Chinese investable stocks, on the other hand, have been trading heavily on the day-to-day news surrounding the trade negotiations and have significantly underperformed both domestic A shares and global benchmarks. Therefore, our base case view of a trade truce coupled with an improved Chinese economy and more supportive policy near year, warrant a cyclical overweight stance favoring Chinese investable stocks over their domestic peers. Earnings from both onshore and offshore markets will benefit from a modest improvement in economic activity, but we think the investable market will benefit more from the trade truce and more upside growth potential. Stay tuned. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1Please see Geopolitical Strategy Special Report, "Is China Afraid Of The Big Bad Warren?" dated October 25, 2019, available at gps.bcaresearch.com 2Please see China Investment Strategy Weekly Report, " Threading A Stimulus Needle (Part 1): A Reluctant PBoC," dated July 10 2019, available at cis.bcaresearch.com 3We call it a “MMT” because China’s state-owned commercial banks own approximately 80% of local government bonds. The commercial banks are essentially backed by China’s central bank, which has a fiat currency system and can make independent monetary policy decisions. 4Please see China Investment Strategy Weekly Report, "Mild Deflation Means Timid Easing," dated October 9, 2019, available at cis.bcaresearch.com 5Please see China Investment Strategy Special Report, "A Guide To Chinese Investable Equity Sector Performance," dated October 30, 2019, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

REIT's Demand Ails

REIT's Demand Ails

Underweight Similar to utilities, REITs have come to the forefront lately as they have populated the top return sector ranks. Importantly, today several key factors signal that investors should shed public market real estate exposure. Namely, weakening supply/demand dynamics, pricing pressures, macro headwinds and still pricey valuations (primarily rock bottom cap rates) are all firing warning shots. On the demand front, not only our proprietary real estate demand indicator has sunk recently, but also the latest Fed Senior Loan Officer survey revealed that demand for CRE loans remains feeble (third & bottom panels). Simultaneously, fewer bankers are willing to extend CRE credit according to the same quarterly Fed survey (second panel). This tightening backdrop coupled with decelerating credit growth, will continue to weigh on CRE prices and S&P REITs. Bottom Line: We reiterate our underweight rating in the S&P real estate sector. For more details, please refer to the most recent Weekly Report. The ticker symbols for the stocks in this index are: BLBG – S5RLST – AMT, PLD, CCI, SPG, EQIX, WELL, PSA, EQR, AVB, SBAC, O, DLR, WY, VTR, ESS, BXP, CBRE, ARE, PEAK, MAA, UDR, EXR, DRE, HST, REG, VNO, IRM, FRT, KIM, AIV, SLG, MAC.

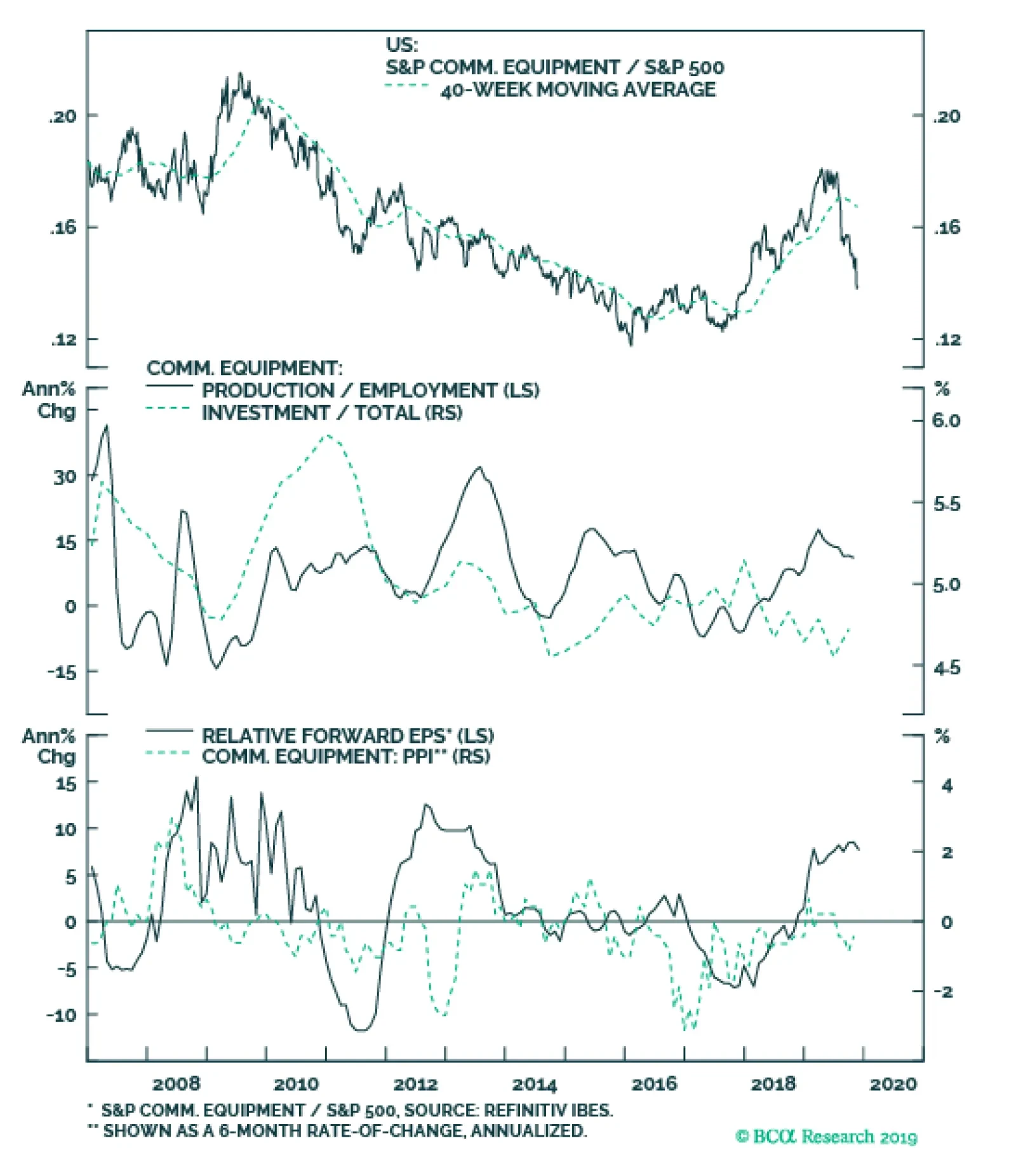

The communications equipment rally stalled early in the summer and has since morphed into a bear market. The darkening profit outlook for this niche tech sub-group warrants remaining underweight. Bellwether CSCO’s latest guidance was weak and confirmed…

The large weight of the tech sector in the US stock market explains much of the superior performance of US stocks over the past decade. EPS in the I.T. sector has grown a lot more quickly than in other sectors. Looking out, there are four reasons why US…

Dear Client, Instead of our regular weekly report next Monday, this Friday November 22, you will receive our flagship publication “The Bank Credit Analyst” with our annual investment outlook. Our regular publication service will resume on December 2 with our high-conviction calls for 2020. Kind regards, Anastasios Avgeriou Highlights Portfolio Strategy Weakening supply/demand dynamics, pricing pressures, macro headwinds and pricey valuations are all warning that REITs are headed south. Global capex blues and the ongoing manufacturing recession, the resilient US dollar and weak operating metrics all confirm that an underweight stance is still warranted in the S&P communications equipment index. Recent Changes There are no changes to our portfolio this week. Table 1

Gasping For Air

Gasping For Air

Feature The S&P 500 made fresh all-time highs again last week, as investors focused on hopes of a US/China trade deal and continued to ignore negative data/news at their own peril. Domestically, unemployment insurance claims jumped to the highest level since June, and none of the major market and industry groups showed a gain in output on a month-over-month basis in October according to the latest Fed industrial production release. Internationally, Korean exports remain in the doldrums, Chinese data releases were weak across the board, and the mighty US dollar is making multi-decade highs versus a slew of EM currencies. Chart 1Disquieting Gap

Disquieting Gap

Disquieting Gap

All of this begs the question is global growth going to recover and aid the equity market grow into its lofty valuation? Our indicators suggest that a definitive earnings trough is now pushed out to Q2/2020. Thus, equity market caution is still warranted. Given all the recent equity market euphoria, we feel more and more like “the lone calf standing on the desolate, dangerous, wolf-patrolled prairie of contrary opinion” as – arguably the greatest trader of all time – Jesse Livermore mused roughly a century ago. Share buybacks have been a key pillar underpinning stocks since the GFC averaging roughly $500bn/annum since 2010. But, last year equity retirement jumped to nearly $1tn/annum. That is clearly unsustainable, warning that there is a disconnect between the S&P 500 and already steeply decelerating share buybacks. Our equity retirement estimate for next year is a return to the 10-year average, signaling that the market may hit a significant air pocket (top panel, Chart 1). Another perplexing recent phenomenon has been the lack of buying on margin that typically confirms SPX breakouts. While this episode may be similar to the 2015/16 episode, if margin debt does not recover soon it will exert downward pull on the broad market (bottom panel, Chart 1). Turning over to earnings, revenues, margins and the forward multiple is instructive. Turning over to earnings, revenues, margins and the forward multiple is instructive. Chart 2 highlights the S&P 500 earnings growth surprise factor. In more detail, this IBES/Refinitiv data show how accurate the sell side analysts’ 12-month forward EPS forecasts have been over time: a reading above zero implies the analyst community was too timid, while a fall below zero signals analysts were too optimistic. Chart 2Unhinged From The EPS Accuracy Signal

Unhinged From The EPS Accuracy Signal

Unhinged From The EPS Accuracy Signal

Equity market momentum moves with the ebb and flow of this factor and given the still downbeat message both from our SPX profit model (please refer to our recent webcast slides) and our simple liquidity indicator (please see Chart 4 from last week’s publication), we doubt 10% profit growth is even plausible for 2020. On the margin front, all four key profit margin drivers are on the brink of turning from tailwinds to headwinds as we recently highlighted in our “Peak Margins?” Special Report. Revenue growth is also at risk of a standstill. Domestic producer prices are deflating, and the ISM prices paid index has been clobbered. German, Japanese, Korean and Chinese wholesale prices are contracting and the OECD’s composite PPI measure is also sinking, suggesting that final demand is anemic at best. Under such a dire global pricing backdrop, it will be challenging for SPX sales to sustain their positive momentum, especially if the greenback remains well bid (Chart 3). Chart 3Top Line Growth Troubles

Top Line Growth Troubles

Top Line Growth Troubles

Forward multiples have slingshot higher despite a near 40bps increase in the 10-year yield since Labor Day. When the discount rate rises the multiple should come in and vice versa. Thus, we would lean against the recent spike in the S&P 500 forward P/E (10-year yield shown inverted, Chart 4). This week we are updating our negative views on a niche high-yielding sector and a tech subgroup. Finally, while sifting through market internals, we recently stumbled upon the GICS2 S&P consumer services index. Digging deeper into services was revealing. This relative share price ratio has gapped down of late. One of the reasons is that the services component of the personal consumption expenditure (PCE) data is decelerating (PCE services shown advanced, middle panel, Chart 5). The ISM non-manufacturing survey is also an excellent leading indicator of the S&P consumer services index, and warns that things will likely get worse before they get better (bottom panel, Chart 5). Chart 4Lofty Valuations

Lofty Valuations

Lofty Valuations

Chart 5Market Internals Signal: Sit This One Out

Market Internals Signal: Sit This One Out

Market Internals Signal: Sit This One Out

This week we are updating our negative views on a niche high-yielding sector and a tech subgroup. Getting Real With Real Estate We would refrain from chasing high yielding real estate stocks higher, and would rather avoid them altogether at the current juncture. Similar to utilities, REITs have come to the forefront lately as they have populated the top return sector ranks. However, real estate stocks, which have split out of the financials sector, are a niche GICS1 sector with a mere 3% market capitalization weight in the SPX, and have not driven the S&P 500 to all-time highs. Instead, tech stocks have, owing to their 23% market capitalization weight, as we have shown in recent research.1 Importantly, several key factors continue to signal that investors should shed public market real estate exposure. Namely, weakening supply/demand dynamics, pricing pressures, macro headwinds and still pricey valuations (primarily rock bottom cap rates) are all firing warning shots. The commercial real estate (CRE) sector is a bubble candidate that exemplifies this cycle’s excesses. As we have highlighted in the past, CRE prices sit at roughly two standard deviations above both the historical time trend and the previous cycle’s peak (not shown).2 Worryingly, CRE demand is waning. Not only our proprietary real estate demand indicator has sunk recently, but also the latest Fed Senior Loan Officer survey revealed that demand for CRE loans remains feeble (third & bottom panels, Chart 6). Simultaneously, fewer bankers are willing to extend CRE credit according to the same quarterly Fed survey (Chart 7). This tightening backdrop is weighing on CRE credit growth and CRE prices (second panel, Chart 6). In fact, absent credit growth providing the necessary fuel to sustain the CRE price inflation frenzy, there are rising odds that investors pull the plug on REITs (top panel, Chart 7). Chart 6Demand Ails

Demand Ails

Demand Ails

Chart 7Time To...

Time To...

Time To...

Already, occupancy rates have crested and there are increasing anecdotes of credit quality deterioration. As a result, CRE rents are also failing to keep up with inflation which eats into relative cash flow growth prospects (Chart 8). The supply side build up tilts this delicate balance further into deficit. Non-residential construction shows no signs of abating, with multi-family housing starts still running at an historically high rate of roughly 400K/annum (Chart 9). Such relentless overbuilding sows the seeds of the eventual felling in CRE prices and rents, which should also dent the S&P real estate sector. Chart 8...Lighten Up On Real Estate

...Lighten Up On Real Estate

...Lighten Up On Real Estate

Chart 9Supply Build Up Is Deflationary

Supply Build Up Is Deflationary

Supply Build Up Is Deflationary

Meanwhile, interest rate related headwinds will also weigh on this high-yielding sector in coming quarters, especially if the selloff in the bond market gains steam as BCA’s fixed income strategists continue to expect. While in the 2000s REITs were positively correlated with the 10-year Treasury yield, since 2010 this relationship has flipped and is now a tight inverse correlation (Chart 10). Chart 10Rising Yields = Sell REITs

Rising Yields = Sell REITs

Rising Yields = Sell REITs

Finally, our proprietary Valuation Indicator (VI) has enjoyed an impressive run since the 2017 trough and despite the recent relative selloff remains in overvalued territory. Our Technical Indicator (TI) hit a wall of late near one standard deviation above the historical mean and has only partially unwound the overbought reading since the early 2018 bottom. If our thesis pans out, we expect heightened selling pressure to weigh further on our VI and TI (Chart 11). Chart 11Still Too Pricey

Still Too Pricey

Still Too Pricey

Bottom Line: We reiterate our underweight rating in the S&P real estate sector. The ticker symbols for the stocks in this index are: BLBG – S5RLST – AMT, PLD, CCI, SPG, EQIX, WELL, PSA, EQR, AVB, SBAC, O, DLR, WY, VTR, ESS, BXP, CBRE, ARE, PEAK, MAA, UDR, EXR, DRE, HST, REG, VNO, IRM, FRT, KIM, AIV, SLG, MAC . Lost Signal The communications equipment rally stalled early in the summer and has since morphed into a bear market. We are sticking with our underweight recommendation, especially given a darkening profit outlook for this niche tech sub-group. Bellwether CSCO’s latest guidance was weak and confirmed that this capex-laden tech sub-index is in for a rough ride. Worryingly, CSCO’s key enterprise segment has no pulse. Historically, this data series has been positively correlated with telecom carrier capital outlays and the current message is grim (second panel, Chart 12). Tack on the ongoing manufacturing recession with CEOs canceling/postponing capital spending plans and the outlook dims further for the revenue prospects of communications equipment vendors (third & bottom panels, Chart 12). Chart 12Heed The CSCO Warning

Heed The CSCO Warning

Heed The CSCO Warning

Adding insult to injury, the US/China trade war is further complicating the picture. The ongoing tariffs have exacerbated the global growth slowdown and global capex plans have come under intense scrutiny. The IFO’s World Economic Outlook capex intentions survey has plunged, warning that global exports of telecom gear have ample downside (Chart 13). Chart 13Global Capex Blues

Global Capex Blues

Global Capex Blues

Chart 14US Dollar The Deflator

US Dollar The Deflator

US Dollar The Deflator

The greenback’s resilience is also sapping business purchasing power, especially in the emerging markets, denting final-demand. Therefore, the US dollar’s appreciation robs communications equipment manufacturers’ pricing power, makes their goods more expensive in the global market place, and as a consequence forces market share losses on them (Chart 14). The greenback’s resilience is also sapping business purchasing power, especially in the emerging markets, denting final-demand. The implication of weakening pricing power is that profits will likely underwhelm. Currently, the sell-side is penciling in roughly 10% EPS growth for the S&P communications equipment index over and above the SPX in the next twelve months. This is a tall order and we would lean against such extreme analyst optimism (bottom panel, Chart 15). Operating metrics are quickly losing steam, another harbinger of profit ails for this tech sub-group. In more detail, our productivity proxy has taken a steep turn for the worse and industry executives have also put investment projects on hold (middle panel, Chart 15). Moreover, the communication equipment new orders-to-inventories ratio is contracting and industry resource utilization is probing multi-year lows, according to the Fed’s latest industrial production release. Under such a backdrop, relative top line growth is on track to level off and likely flirt with the contraction zone (Chart 16). Chart 15Operating Metric...

Operating Metric...

Operating Metric...

Chart 16...Dysphoria

...Dysphoria

...Dysphoria

Netting it all out, global capex blues, the resilient US dollar and weak operating metrics all confirm that an underweight stance is still warranted in the S&P communications equipment index. Bottom Line: Continue to avoid the S&P communications equipment index. The ticker symbols for the stocks in this index are: BLBG – S5COMM – CSCO, JNPR, MSI, ANET, FFIV. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA US Equity Strategy Insight Report, “Deciphering Sector Returns” dated August 30, 2019, available at uses.bcaresearch.com. 2 Please see BCA US Equity Strategy Special Report, “10 Most FAQs From The Road” dated April 8, 2019, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Stay neutral cyclicals over defensives (downgrade alert) Favor value over growth Favor large over small caps (Stop 10%)

Dear Client, I will be visiting clients in Paris, Amsterdam, and London next week. In lieu of our regular report, we will be sending you a Special Report from Matt Gertken, BCA’s Chief Geopolitical Strategist. Matt argues that US politics and the 2020 election represent the greatest source of geopolitical risk over the coming year, and possibly beyond. Best regards, Peter Berezin Highlights Having underperformed for more than ten years, non-US stocks are set to gain the upper hand over their US peers. A reacceleration in global growth, a weaker US dollar, and favorable valuations should all support non-US stocks next year. Meanwhile, one of the greater drivers of US equity outperformance – the stellar returns of tech stocks – is likely to dissipate. Investors should remain overweight global equities relative to bonds, but start increasing allocations to non-US stocks at the expense of US stocks. US Stocks: From Leaders To Laggards? US equities have handily outperformed their global peers since 2008. About half of that outperformance was due to faster sales-per-share growth in the US, a third was due to faster growth in US margins, and the rest was due to relative P/E expansion in favor of the US (Chart 1). Looking ahead, non-US stocks are set to gain the upper hand over their US peers thanks to an improving global growth backdrop, a weaker US dollar, and an increasingly irresistible valuation tailwind. Chart 1Faster Sales Growth, Rising Margins, And Relative PE Expansion Helped Drive US Outperformance Over The Past Decade

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

Improving Global Growth Outlook Global growth should benefit next year from the dovish pivot by most central banks. The share of central banks cutting/raising rates leads global growth by about 6-to-9 months (Chart 2). Chart 2Lower Rates Should Help Spur Growth

Lower Rates Should Help Spur Growth

Lower Rates Should Help Spur Growth

Chart 3The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The global manufacturing downturn is also coming to end as inventories continue to be run down. The auto sector, which has been at the forefront of the manufacturing slowdown, is finally showing signs of life. US banks stopped tightening lending standards for auto loans in the third quarter. They are also reporting stronger demand for vehicle financing (Chart 3). In Europe, the new orders-to-inventory ratio of the Markit Europe Automobile PMI has moved back to parity for the first time since the autumn of 2018. In China, vehicle production and sales are rebounding on a rate-of-change basis (Chart 4). Both automobile ownership and vehicle sales in China are still a fraction of what they are in most other economies (Chart 5). Chart 4Chinese Auto Sector Is Bottoming Out

Chinese Auto Sector Is Bottoming Out

Chinese Auto Sector Is Bottoming Out

Chart 5China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

The trade war is a clear and present danger to our bullish outlook on global growth. The good news is that President Trump has a strong incentive to make a deal. A resurgence in the trade war would hurt the economy, which is Trump’s best selling point (Chart 6). As a self-described master negotiator, Trump has to produce a “tremendous” deal for the American people. Had he negotiated an agreement a year or two ago, he would currently be on the hook for showing that it resulted in a smaller trade deficit with China. But with the presidential election only a year away, he can semi-credibly claim that the trade balance will improve only after he is re-elected. Assuming a “Phase 1” agreement is concluded, global business sentiment should improve. Chart 6Trump Gets Reasonably High Marks On His Handling Of The Economy, But Not Much Else

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

A détente in the trade war is unlikely to cause China to restart its deleveraging campaign. Credit growth is currently only a few points above trend nominal GDP growth, implying that the ratio of credit-to-GDP is barely increasing (Chart 7). The combined Chinese credit and fiscal impulse is still rising; it reliably leads global growth by about nine months (Chart 8). Chart 7China: The Deleveraging Campaign Has Been Put On The Backburner

China: The Deleveraging Campaign Has Been Put On The Backburner

China: The Deleveraging Campaign Has Been Put On The Backburner

Chart 8Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Faster Global Growth Should Disproportionately Benefit Non-US stocks The sector composition of international stocks is more skewed towards cyclicals than defensives compared to US stocks (Table 1). As a result, non-US stocks generally outperform their US peers when global growth accelerates (Chart 9). Table 1Cyclicals Are More Heavily Weighted Outside The US Stock Market

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

We would include financials in our definition of cyclical sectors. As global growth improves, long-term bond yields will increase at the margin (Chart 10). Since central banks are in no hurry to raise rates, yield curves will steepen. This will boost bank net interest margins, flattering profits and share prices (Chart 11). Chart 9Non-US Equities Usually Outperform When Global Growth Improves

Non-US Equities Usually Outperform When Global Growth Improves

Non-US Equities Usually Outperform When Global Growth Improves

Chart 10Stronger Economic Growth Will Put Upward Pressure On Government Bond Yields

Stronger Economic Growth Will Put Upward Pressure On Government Bond Yields

Stronger Economic Growth Will Put Upward Pressure On Government Bond Yields

The US Dollar Should Weaken Compared to most other economies, the United States has a large service sector and a small manufacturing base. This makes the US a “low beta” play on global growth. As a result, capital tends to flow from the US to the rest of the world when global growth picks up, putting downward pressure on the US dollar in the process (Chart 12). Chart 11Steeper Yield Curves Will Benefit Financials

Steeper Yield Curves Will Benefit Financials

Steeper Yield Curves Will Benefit Financials

Chart 12The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Interest-rate differentials have been moving against the dollar for most of this year (Chart 13). This makes the greenback more vulnerable to a correction. Chart 13The Dollar Has Been Diverging From Rate Differentials This Year

The Dollar Has Been Diverging From Rate Differentials This Year

The Dollar Has Been Diverging From Rate Differentials This Year

Chart 14Long Dollar Is A Crowded Trade

Long Dollar Is A Crowded Trade

Long Dollar Is A Crowded Trade

Bullish sentiment towards the dollar also remains somewhat stretched. Net long speculative positions are near the top of their historic range (Chart 14). Our tactical MacroQuant model, which has an excellent track record of predicting short-to-medium term moves in the dollar, has dropped its bullish bias towards the currency (Chart 15). Chart 15MacroQuant Has Soured On The US Dollar

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

A weaker dollar will help boost commodity prices, which is usually good news for cyclical stocks (Chart 16). A softer dollar will also raise the USD value of overseas shares, thus making international stocks more attractive in common-currency terms. Valuations Favor Non-US Stocks There is an old investment adage which says that valuations are useless as a short-term timing tool. That is only partially true. While valuations by themselves offer little guidance as to where the stock market is going in the short run, combined with a catalyst, valuations can make a big difference. When stocks are cheap, a bullish catalyst can cause prices to surge; whereas when stocks are expensive, a bearish catalyst can cause them to plunge. Looking ahead, non-US stocks are set to gain the upper hand over their US peers thanks to an improving global growth backdrop, a weaker US dollar, and an increasingly irresistible valuation tailwind. Non-US stocks are currently trading at 13.8-times forward earnings. This represents a significant discount to US stocks, which trade at a forward PE ratio of 17.7. The valuation discount is even greater if one looks at other measures such as the cyclically-adjusted PE, price-to-book, price-to-sales, and the dividend yield (Chart 17). Chart 16A Weaker Dollar Tends To Support Commodity Prices

A Weaker Dollar Tends To Support Commodity Prices

A Weaker Dollar Tends To Support Commodity Prices

Chart 17US Stocks Are More Expensive...

US Stocks Are More Expensive...

US Stocks Are More Expensive...

Differences in sector weights account for about a quarter of the valuation gap between the US and the rest of the world (Chart 18). The rest of the gap is due to cheaper valuations within sectors. Financials, utilities, and consumer discretionary stocks, in particular, are quite a bit more expensive in the US than elsewhere (Chart 19). Chart 18…Even When Adjusting For Sector Weights

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

Chart 19AEquity Sector Valuations: US Versus The Rest Of The World (I)

Equity Sector Valuations: US Versus The Rest Of The World (I)

Equity Sector Valuations: US Versus The Rest Of The World (I)

Chart 19BEquity Sector Valuations: US Versus The Rest Of The World (II)

Equity Sector Valuations: US Versus The Rest Of The World (II)

Equity Sector Valuations: US Versus The Rest Of The World (II)

The valuation gap between the US and the rest of the world is even starker if we compare earnings yields with bond yields. Since bond yields are lower outside the US, the implied equity risk premium is markedly higher for non-US stocks (Chart 20). An examination of the relative performance of US vs non-US companies over the past 50 years reveals two major tops, and one potential top. Some commentators have argued that the loftier valuations enjoyed by US stocks are warranted due to their superior growth prospects. While there may be some truth to that, it is worth noting that the IMF projects GDP growth (based on MSCI country weights) will be faster outside the US over the next five years (Chart 21). Chart 20Equity Risk Premia Remain Quite High

Equity Risk Premia Remain Quite High

Equity Risk Premia Remain Quite High

Chart 21Growth Prospects Brighter Outside The US

Growth Prospects Brighter Outside The US

Growth Prospects Brighter Outside The US

One should also keep in mind that relatively fast US earnings growth is a fairly recent phenomenon. Between 1970 and 2008, European EPS actually grew slightly faster than US EPS (Chart 22). Earnings in emerging markets also increased more rapidly than in the US during the two decades leading up to the Global Financial Crisis. Chart 22US Earnings Have Not Always Outperformed

US Earnings Have Not Always Outperformed

US Earnings Have Not Always Outperformed

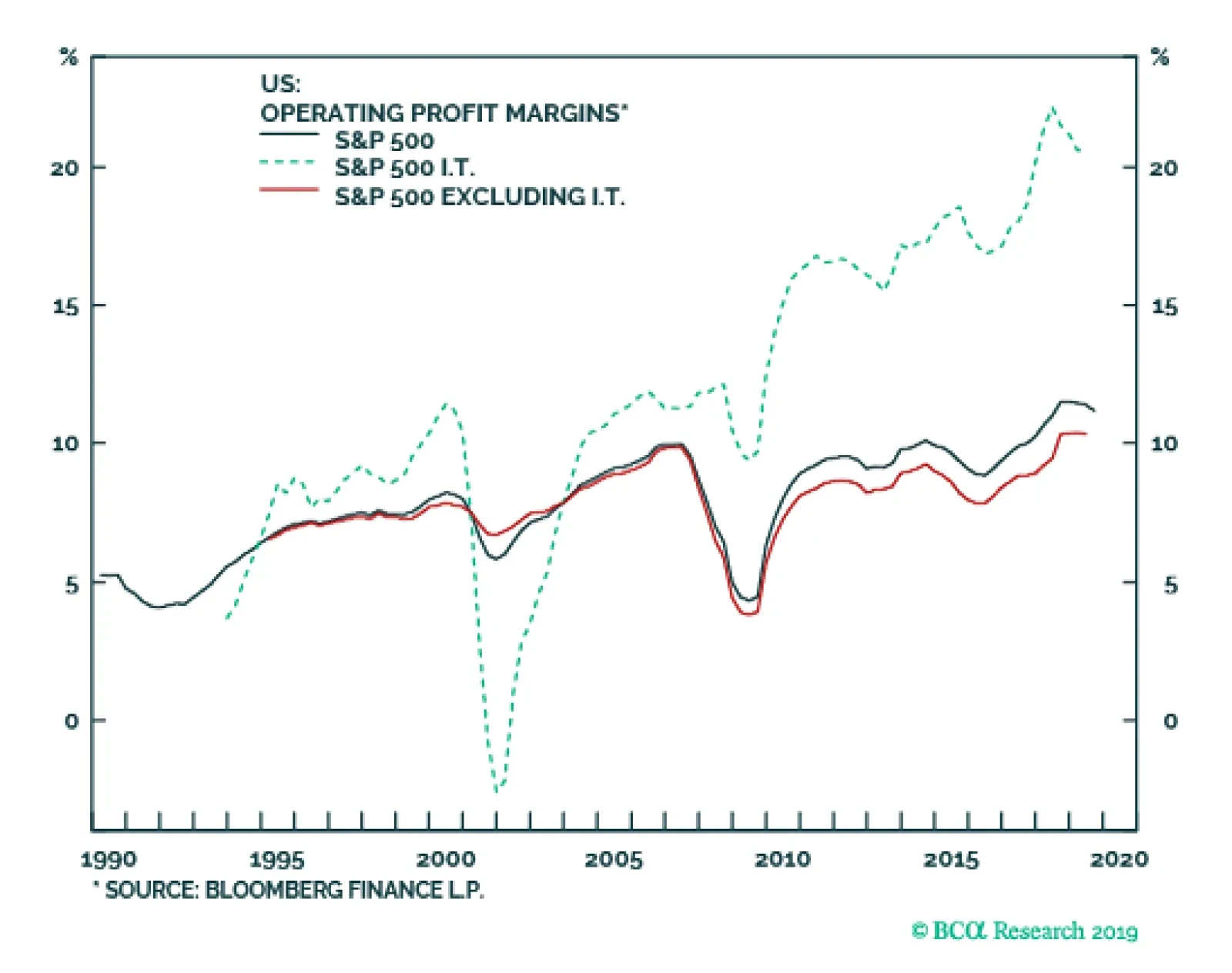

The Role Of US Tech The large weight of the tech sector in the US stock market explains much of the superior performance of US stocks over the past decade. As Chart 23 illustrates, EPS in the I.T. sector has grown a lot more quickly than in other sectors. Chart 23US Earnings: Who Has Been Doing The Heaving Lifting?

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

Chart 24S&P 500: Much Of The Increase In Margins Has Occurred In The I.T. Sector

S&P 500: Much Of The Increase In Margins Has Occurred In The I.T. Sector

S&P 500: Much Of The Increase In Margins Has Occurred In The I.T. Sector

Looking out, there are four reasons why US tech stocks may be due for a breather. First, tech valuations have gotten stretched relative to the broader market. Second, tech margins have risen to unprecedented high levels. We estimate that about half of the increase in S&P 500 profit margins since 2007 has been due to I.T. (Chart 24). Even that understates the role of tech in the expansion of profit margins because Standard & Poor’s no longer classifies some large-cap behemoths such as Google and Facebook as I.T. companies. Third, tech companies may face increased regulatory scrutiny in the years ahead stemming from alleged privacy violations, perceived monopolistic behavior, and worries about the censorship of online speech. This could weigh on sales and earnings growth. Fourth, the growth in private equity funds is likely to limit the number of tech companies that go public at a very early stage. Stock market investors were very lucky that companies such as Microsoft, Cisco, Nvidia, Qualcomm, Oracle, Amazon, and Netflix issued shares to the public at a young stage in their development (Table 2). All seven had market caps below $1 billion when they went public. Such hidden gems are becoming less common: The number of publicly listed companies in the US has fallen by more than half over the past two decades (Chart 25). The median age of tech companies at the time of IPO has risen from around 7 in the 1990s to 12 years today (Chart 26). Table 2Big Gains From Once Small Companies

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

Chart 25The Number Of Publicly Listed Companies Fell

The Number Of Publicly Listed Companies Fell

The Number Of Publicly Listed Companies Fell

Chart 26Tech Companies Entering The Public Arena Are Now More Mature

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

Had Uber gone public as a small, upstart company not long after it was founded in 2009, it probably would have also made public shareholders a lot of money. Instead, it ended up going public this year with a market cap of $75 billion, only to see it shrink to as low as $40 billion in the ensuing six months. We won’t even mention what would have happened if WeWork had gone public. Investment Conclusions An examination of the relative performance of US vs non-US companies over the past 50 years reveals two major tops, and one potential top: The first during the “Nifty 50” era of the late 1960s, the second during the 1990s dotcom boom, and the third during the recent FAANG craze (Chart 27). It is too early to say whether FAANG stocks have peaked, but it is worth noting that the group has underperformed the S&P 500 since May (Chart 28). Chart 27Putting The Recent FAANG Craze Into Context

Putting The Recent FAANG Craze Into Context

Putting The Recent FAANG Craze Into Context

Chart 28FAANG Stocks And The Market

FAANG Stocks And The Market

FAANG Stocks And The Market

Chart 29Has The Underperformance Of Value Run Its Course?

Has The Underperformance Of Value Run Its Course?

Has The Underperformance Of Value Run Its Course?

Regardless of whether the secular outperformance of US equities is ending, the cyclical backdrop that we foresee over the next 12-to-18 months – characterized by faster global growth, a weakening dollar, and higher commodity prices – is likely to favor non-US stocks. As such, investors should remain overweight global equities relative to bonds, but start increasing allocations to non-US stocks at the expense of US stocks. Consistent with this, we are initiating a new recommendation to go long the MSCI ACWI ex USA index versus the MSCI USA index in dollar terms. Looking across the various stock markets outside the US, we are particularly fond of Europe. Net profit margins among companies in the STOXX Europe 600 index are about three percentage points below the S&P 500. This gives European companies greater scope to boost earnings. European banks are especially attractive, sporting a forward PE of 8.3, a price-to-book ratio of 0.6, and a dividend yield of 6.1%. Lastly, on the question of style investing, we would note that the relative performance of the MSCI value and growth indices closely tracks the performance of global financials versus I.T. (Chart 29). Given our preference for the former over the latter, we suspect that value will outperform growth next year. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes Strategy & Market Trends MacroQuant Model And Current Subjective Scores

A Window Of Opportunity For International Stocks

A Window Of Opportunity For International Stocks

Tactical Trades Strategic Recommendations Closed Trades

Out Of Power Warning

Out Of Power Warning

Underweight Utilities stocks have been all the rave this year, but given their small weighting in the SPX they only explain a very small part of the broad market’s run (in contrast, the heavyweight tech sector explains most of the S&P 500’s rise as we highlighted in recent research). We reiterate our underweight stance in this small defensive sector that has run way ahead of soft profit fundamentals. Worrisomely, utilities trade with a 20 forward P/E handle and command a 20% premium to the broad market, but their forecast EPS growth rate at 5% trails the SPX by 350bps (not shown). The sector’s operating metrics reveal that investors piling into utilities is unwarranted. Natural gas prices are contracting at the steepest pace of the past four years (middle panel) and signal that the path of least resistance is lower for relative share price momentum. Meanwhile, electricity capacity utilization is in a multi decade downtrend, warning that the relative profitability will remain under pressure in the coming quarters (bottom panel). Bottom Line: Shy away from the expensive S&P utilities sector. Please refer to this Monday’s Weekly Report for additional details. The ticker symbols for the stocks in this index are: BLBG – S5UTIL– PPL, PNW, ATO, PEG, FE, EIX, AEE, SO, SRE, AEP, XEL, DTE, EVRG, WEC, AES, CMS, LNT, ED, NRG, D, AWK, DUK, ETR, EXC, NEE, CNP, NI, ES.

New Pair Trade Idea

New Pair Trade Idea

In this Monday’s Weekly Report, we initiated a market-neutral long S&P energy/short S&P utilities pair trade. The middle panel shows that energy stocks have come full circle and are trading at levels last seen two decades ago when WTI oil was fetching less than half of today’s $55/bbl price. Encouragingly, there seems to be long-term support for relative share prices at the current overly depressed level. While utilities have been making headlines all year long given their outperformance, when put in proper perspective this niche defensive sector with a mere 3% weight in the SPX looks like a shipwreck (bottom panel). Taken together, this battle between two diminishing sectors presents a tradable opportunity by favoring energy stocks at the expense of utilities. In fact, this ratio trades at more than two standard deviations below the historical uptrend, and thus offers a lucrative risk/reward profile (top panel). Bottom Line: Initiate long S&P energy/short S&P utilities pair trade. For fundamental reasons behind the trade, please refer to the most recent Weekly Report.

Highlights The attractiveness of European stocks is relative to European bonds rather than relative to non-European stocks. Despite vastly different stock market valuations in Germany, Japan, and the US, the implied prospective 10-year annualised returns are almost identical – at around 5 percent per annum. Overweight the DAX versus German long-dated bunds. Equities would lose their attractiveness if the global 10-year bond yield were to rise through 2.5 percent, because the required excess return from equities would viciously normalise. Tactically overweight EM versus DM. Fractal trade: short GBP/NOK, as the recent rally in the pound appears technically extended. Feature Chart of the WeekOverweight Europe Vs. World = Overweight Consumer Staples Vs. Technology

Overweight Europe Vs. World = Overweight Consumer Staples Vs. Technology

Overweight Europe Vs. World = Overweight Consumer Staples Vs. Technology

Stock markets recently broke to new highs, begging the perennial question: how attractive are equities at current valuations? To answer, we need to assess the prospective return that is now ‘baked in the equity valuation cake’. But which valuation metric gives the most credible assessment of prospective returns? Equity valuations based on assets are problematic – because nowadays, assets comprise intellectual capital or intangibles or ‘virtual’ assets, which are extremely difficult to value. Equity valuations based on earnings are problematic. Equity valuations based on earnings (profits) are also problematic – because they take no account of structurally high profit margins (Chart I-2). The problem is that earnings will face a headwind when profit margins normalise, depressing prospective returns. Some people suggest adjusting the earnings to derive a cyclically adjusted price to earnings multiple (CAPE), but by definition this does not correct for the structural rise in profit margins. Chart I-2Structurally High Profit Margins Flatter Earnings

Structurally High Profit Margins Flatter Equity Earnings Structurally High Profit Margins Flatter Earnings

Structurally High Profit Margins Flatter Equity Earnings Structurally High Profit Margins Flatter Earnings

Hence, the most credible assessment comes from price to sales – because sales are quantifiable, unambiguous, and undistorted by profit margins. Significantly, while price to earnings missed the high valuation of world equities in 1990 (Japanese bubble) and 2007 (credit bubble), price to sales did not (Chart I-3 and Chart I-4). Chart I-3Price To Earnings Missed The Japanese Bubble And The Credit Bubble...

Price To Earnings Missed The Japanese Bubble And The Credit Bubble...

Price To Earnings Missed The Japanese Bubble And The Credit Bubble...

Chart I-4...But Price To Sales ##br##Didn't

...But Price To Sales Didn't

...But Price To Sales Didn't

Are Stocks Attractive? Based on the credible assessment from price to sales, today’s prospective 10-year annualised return from world equities is around 5 percent (Chart I-5). This is not that different to the 4 percent prospective return at the peak of the credit bubble in 2007.1 Which raises an obvious question. Back in 2007, a secular growth boom provided the excuse for the rich absolute valuation, but today, if anything, investors fear a ‘secular stagnation’. What can excuse today’s rich absolute valuation? Chart I-5The Prospective Return From World Equities Is 5 Percent

The Prospective Return From World Equities Is 5 Percent

The Prospective Return From World Equities Is 5 Percent

The answer is ultra-low bond yields. In 2007, the global 10-year bond yield stood at 5 percent; today, it stands well below 2 percent (Chart I-6). A lower prospective return on bonds means a lower prospective return on competing long-duration assets, like equities. Chart I-6The Global 10-Year Bond Yield Has Plunged To Below 2 Percent

The Global 10-Year Bond Yield Has Plunged To Below 2 Percent

The Global 10-Year Bond Yield Has Plunged To Below 2 Percent

Moreover, as bond yields approach their lower bound, the riskiness of bonds rises because they take on an unattractive ‘lose-lose’ characteristic. As holders of Swiss government bonds discovered this year, prices do not rise much in a rally, but they do plunge in a sell-off. This higher riskiness of bonds justifies an abnormally low (or zero) ‘risk premium’ on competing long-duration assets, like equities. The 5 percent prospective return makes equities look attractive relative to bonds. The upshot is that the 5 percent prospective return from equities is low in absolute terms. But in a world of ultra-low numbers – for both bond yields and equity risk premiums – the 5 percent prospective return makes equities look attractive relative to bonds. At the peak of the credit bubble in 2007, equities were offering a lower prospective return than the 5 percent available from bonds. But today’s equity risk premium over bonds is generous. The caveat is that this would change if the global 10-year bond yield were to rise through 2.5 percent because the required risk premium on equities would viciously normalise. Are European Stocks Attractive? Turning to the relative attractiveness of major stock markets, it is tempting to think that the markets trading on the best head-to-head valuation comparisons are the most attractive. For example, Germany and Japan, both trading on a price to sales multiple of 0.9, appear compelling buys compared to the US, trading on a multiple of 2.1 (Chart I-7). But such a knee-jerk conclusion is wrong, for two reasons. Chart I-7Germany And Japan Trade On Much Lower Multiples Than The US

Germany And Japan Trade On Much Lower Multiples Than The US

Germany And Japan Trade On Much Lower Multiples Than The US

First, stock markets have very different sector compositions. Two sectors with vastly different structural growth prospects – say, technology and banks – must necessarily trade on vastly different valuations. So the sector with the lower valuation is not necessarily the better-valued sector. By extension, the stock market with the lower valuation because of its ‘sector fingerprint’ is not necessarily the better-valued stock market. Second, major stock markets are dominated by multinational companies with mixed currency sales and profits, while the stock price is quoted in the domestic currency. Hence, if the market expects the mixed currency profits to depreciate in domestic currency terms, the stock will trade at a discount. Put another way, if the domestic currency is cheap the stock market will appear cheap. The best way to see this is to look at the two valuations of dual-listed multinationals like the UK/US cruise operator Carnival. In London, the stock trades on a price to forward earnings at 9.7; in New York it trades at 10.3. But it would be absurd to suggest that Carnival is cheaper in London than in New York! The discrepancy is simply because the market expects the pound to appreciate versus the dollar. A head-to-head comparison of stock market valuations is misleading. Allowing for the distortions from sector skews and currency adjustments, the best way to assess an equity region’s attractiveness is to quantify the prospective return implied by its valuation versus its own history. The method is to regress historic starting price to sales with the (historic) prospective 10-year returns that followed. Then apply this relationship to the current price to sales to predict the (current) prospective 10-year return. The results are amazing. Despite the vastly different price to sales multiple of 0.9 in Germany and Japan, and 2.1 in the US, the implied prospective 10-year annualised returns are almost identical – at around 5 percent from each of the three stock markets (Chart I-8-Chart I-10). Chart I-8Expect Near-Identical Returns From The US...

Expect Near-Identical Returns From The US...

Expect Near-Identical Returns From The US...

Chart I-9…Germany…

...Germany...

...Germany...

Chart I-10...And Japan

...And Japan

...And Japan

Still, there is one significant difference: the 10-year bond yield is much lower in Germany and Japan than in the US, equating to a much more attractive equity risk premium of over 5 percent in Germany and Japan. So to answer this week’s title, yes, European stocks are attractive. But the attractiveness is not relative to non-European stocks, the attractiveness of European stocks is relative to European bonds. Bottom Line: maintain a structural overweight to the DAX versus German long-dated bunds. Europe’s ‘Sector Fingerprint’ Is No Longer Pro-Cyclical Over the short term, stock market relative performance is just the result of global sector relative performance combined with the unique sector fingerprint of each stock market. It follows that regional and country equity allocation must always start with a sector view combined with an awareness of the sector fingerprint of the major bourses (Table 1-1). Table I-1EM, DM, And Europe Have Unique ‘Sector Fingerprints’

Are European Stocks Attractive?

Are European Stocks Attractive?

In this regard, there is an important change. Market action plus index composition changes are making the European index less cyclical. Specifically, the European index is no longer over-weighted to Financials relative to the world index. Instead, the European sector fingerprint is now: ‘Overweight Consumer Staples, Underweight Technology’ (Chart of the Week). With the overweight skew being to defensive staples and the underweight skew to partly-cyclical tech, the cyclicality of the European index has become ambiguous. By contrast, emerging market (EM) equities remain ultra-cyclical with a sector fingerprint that is: ‘Overweight Banks, Underweight Healthcare’ (Chart I-11). Suffice to say, this is ultra-cyclical because the 10 percent overweight is to an unambiguously cyclical sector, while the symmetrical 10 percent underweight is to an unambiguously defensive sector. Chart I-11Overweight EM Vs. DM = Overweight Banks Vs. Healthcare

Overweight EM Vs. DM = Overweight Banks Vs. Healthcare

Overweight EM Vs. DM = Overweight Banks Vs. Healthcare

The upshot is that a pro-cyclical sector tilt no longer implies an overweight to European equities versus other regions, but it does strongly imply an overweight to EM equities. This is our recommended stance, albeit only on a tactical horizon until our leading indicators show that the current growth rebound can be sustained well into 2020. Stay tuned. Fractal Trading System* The broken 65-day fractal structure of GBP/NOK suggests that its recent rally is susceptible to a countertrend sell-off, albeit UK election campaign developments are likely to be the near-term sentiment drivers. Go short GBP/NOK, setting a profit target at 2.5 percent with a symmetrical stop-loss. In other trades, short Italian 10-year BTP achieved its 3 percent profit target and is now closed, while long gold / short nickel is very close to its 11 percent profit target. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes.

NOK/GBP

NOK/GBP

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 Total (capital plus income) nominal annualised returns Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades

Are European Stocks Attractive?

Are European Stocks Attractive?

Are European Stocks Attractive?

Are European Stocks Attractive?

Are European Stocks Attractive?

Are European Stocks Attractive?

Are European Stocks Attractive?

Are European Stocks Attractive?

Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

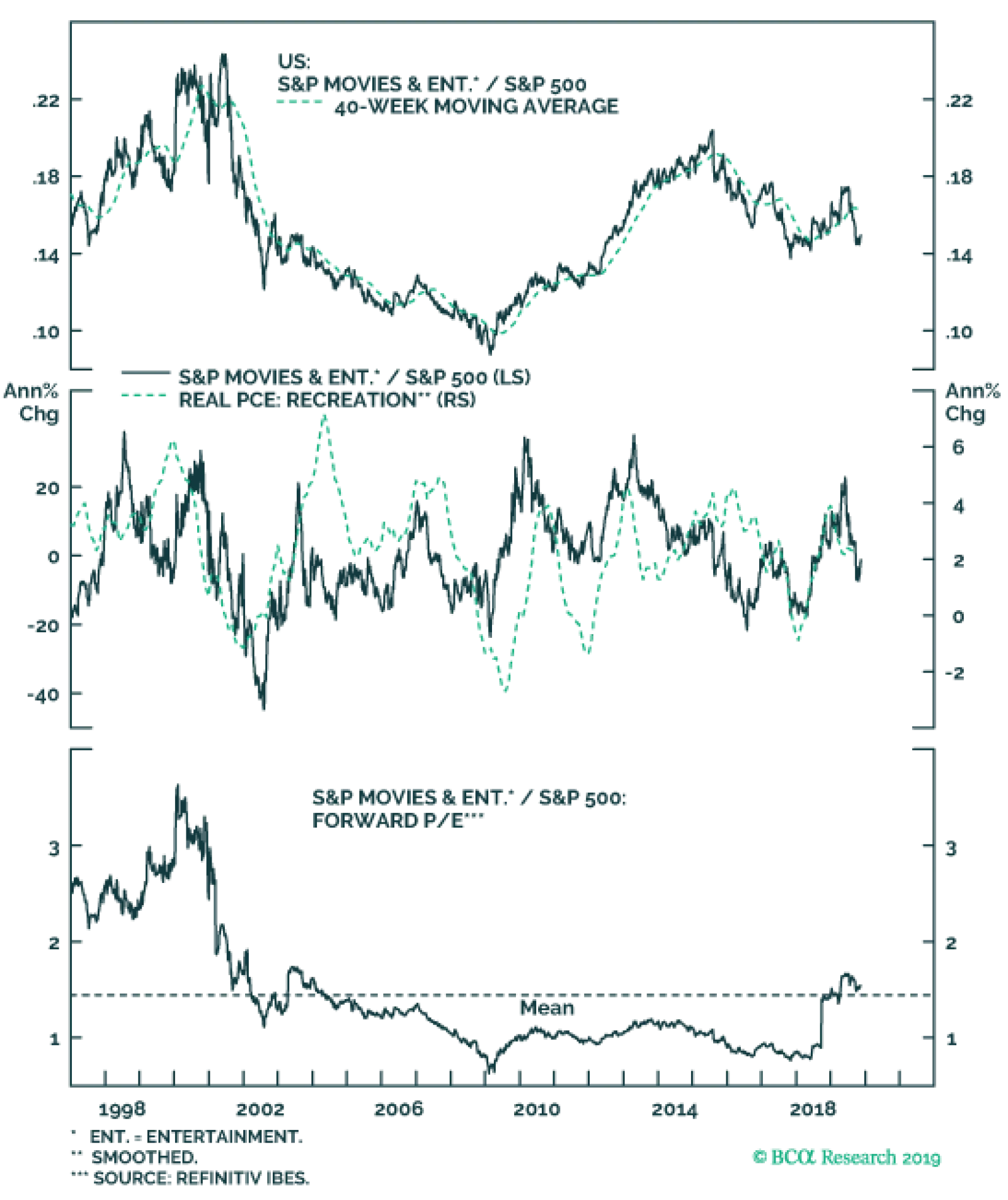

According to the University of Michigan, consumer confidence is softening; meanwhile, the ISM and NFIB surveys are all firing warning shots. However, we are still compelled to stick with our overweight S&P movies & entertainment call for three…