Sectors

Highlights Portfolio Strategy Despite the Fed’s supra natural powers, the deep rooted global growth slowdown will likely win the tug of war versus flush liquidity, especially if the trade war spat stays unresolved and the U.S. dollar remains well bid, both of which undermine U.S. corporate sector profitability. Recent Changes There are no changes to the portfolio this week. Table 1

The Fed Apotheosis

The Fed Apotheosis

Feature Equities hit all-time highs last week, eagerly anticipating this Wednesday’s Fed decision to commence an easing interest rate cycle and save the day. The looming global liquidity injection is the sole reason that stocks are holding near their all-time highs. While markets are treating the Fed as a deity, empirical evidence suggests that risks are actually lurking beneath the surface. Over the past two decades the correlation between stocks and the fed funds rate has been tight and positive. Given the bond market’s view of four fed cuts in the coming year, equity gains are likely running on fumes (Chart 1). Chart 1Mind The Positive Correlation

Mind The Positive Correlation

Mind The Positive Correlation

As we highlighted recently, we remain perplexed that stocks are diverging from earnings.1 Anticipating a flush global liquidity backdrop (i.e. global central banks increasing their reflationary efforts) likely explains this dynamic as the former should ultimately rekindle economic growth, which in turn should boost profit growth. However, the disinflationary fallout from the ongoing manufacturing recession and the petering out in the global credit impulse signal that the liquidity pipes remain clogged. We recently read and re-read the Bank For International Settlements (BIS) Hyun Song Shin’s “What is behind the recent slowdown” speech where he eloquently argues that the global trade deceleration predates last spring’s U.S./China trade dispute.2 Shin has a compelling argument blaming the growth deceleration on the drop in manufactured goods global value chains (GVC) and he depicts this as global trade trailing global GDP (top panel, Chart 2). Interestingly, despite the V-shaped recovery following the Great Recession, global trade never really regained its footing, failing to surpass the 2007 peak. Shin then links this slowdown in global supply chains to financial conditions and the role that banking plays in global trade financing. The middle panel of Chart 2 shows that the GVC move with the ebbs and flows of global banks. In other words, healthy banks tend to boost global trade and vice versa. Finally, given that most trade financing is conducted in U.S. dollars, the greenback’s recent appreciation also explains trade blues. Simply put, decreased availability of U.S. dollar denominated bank credit as a result of a rising greenback is another culprit (U.S. dollar shown inverted, bottom panel, Chart 2). Ergo, there is no miracle cure for the sputtering world economy, especially given the recent re-escalation in global trade tensions and the stubbornly high U.S. dollar, and the gap between buoyant share prices and poor profit performance is likely to narrow via a fall in the former. Two weeks ago we highlighted that foreign sourced profits for U.S. multinationals are under attack as BCA’s global ex-U.S. ZEW survey ticked down anew (top panel, Chart 3). Tack on the global race to ZIRP (and in some cases further into NIRP) and it is crystal clear that the profit recession has yet to run its course. Chart 2Grim Trade Backdrop...

Grim Trade Backdrop...

Grim Trade Backdrop...

Chart 3...Will Continue To Weigh On Foreign Sourced Profits

...Will Continue To Weigh On Foreign Sourced Profits

...Will Continue To Weigh On Foreign Sourced Profits

Meanwhile, China is likely exporting its deflation to the rest of the world and until its business sector regains pricing power, U.S. profits will continue to suffer (bottom panel, Chart 3). Turning over to U.S. shores and domestic corporate pricing power, the news is equally grim. Our pricing power proxy is outright contracting and warns that revenue growth is also under duress for U.S. corporates. Similarly, the ISM manufacturing prices paid subcomponent fell below the 50 boom/bust line and steeply contracting raw industrials commodities are signaling that 6%/annum top line growth for the SPX is unsustainable (Chart 4). On a cyclical 3-12 month time horizon we remain cautious on the broad equity market. Chart 4Sales Pressures...

Sales Pressures...

Sales Pressures...

Chart 5...Are Building Rapidly

...Are Building Rapidly

...Are Building Rapidly

Melting inflation expectations and the NY Fed’s softening Underlying Inflation Gauge (UIG) best encapsulate this softening revenue backdrop and warn that any further letdown in inflation risks sinking S&P 500 sales growth below the zero line (Chart 5). Netting it all out, despite the Fed’s supra natural powers, the deep rooted global growth slowdown will likely win the tug of war versus flush liquidity, especially if the trade war spat stays unresolved and the U.S. dollar remains well bid, both of which undermine U.S. corporate sector profitability. On a cyclical 3-12 month time horizon we remain cautious on the broad equity market. This is U.S. Equity Strategy’s view, which stands in contrast to the more sanguine equity BCA House View. What follows is a recap of recent (mostly) defensive moves in the health care, consumer staples, materials, tech, consumer discretionary and communication services sectors. Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com S&P Health Care (Overweight) Upgraded from Neutral S&P Health Care Equipment (Overweight) Upgraded from Neutral Fear-based sell-off created a buying opportunity in the U.S. health care equipment index as fundamentals remain upbeat. Rising U.S. medical equipment exports are a tailwind for this health care subgroup as 60% of its revenues are generated outside the United States (second panel). The EM demographic shift (not shown) represents yet another boost to the sector as U.S. companies are the technology leaders and often the only source for equipping hospitals/clinics around the globe. Our move to upgrade the S&P health care equipment index also pushed the entire health care sector from neutral to overweight (bottom panel). S&P Health Care

S&P Health Care

S&P Health Care

S&P Managed Health Care (Overweight) Upgraded from Neutral The Bernie Sanders “Medicare For All” bill reintroduction created a buying opportunity in the S&P managed health care index and we were swift to act on it in mid-April. Contained industry cost factors including wages staying at the 2% mark help preserve industry margins (bottom panel). Melting medical cost inflation signals that HMO profit margins will likely expand (third panel). Overall healthy labor market conditions with unemployment insurance claims probing 60-year lows should underpin managed health care enrollment (top & second panels). S&P Managed Health Care

S&P Managed Health Care

S&P Managed Health Care

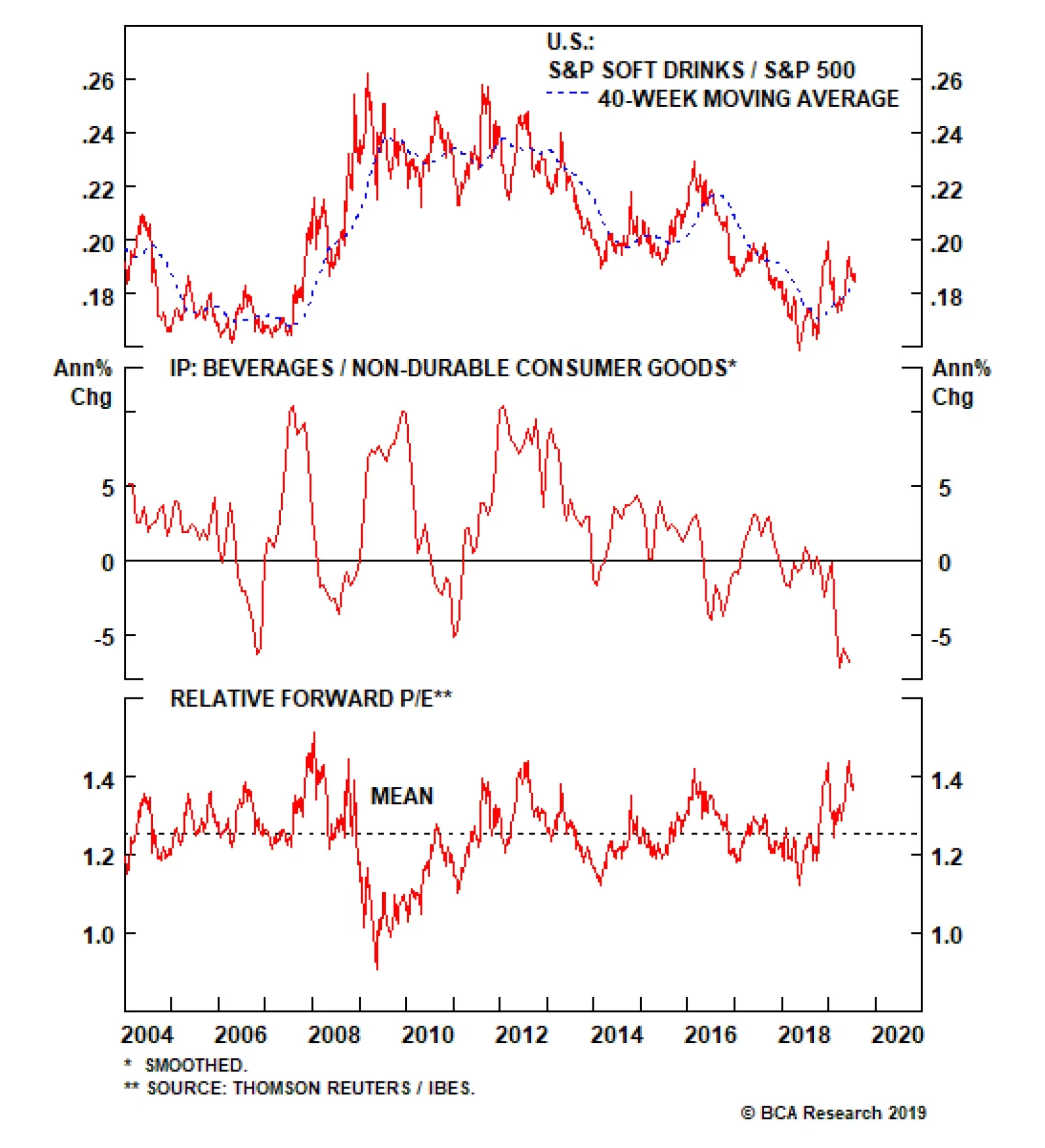

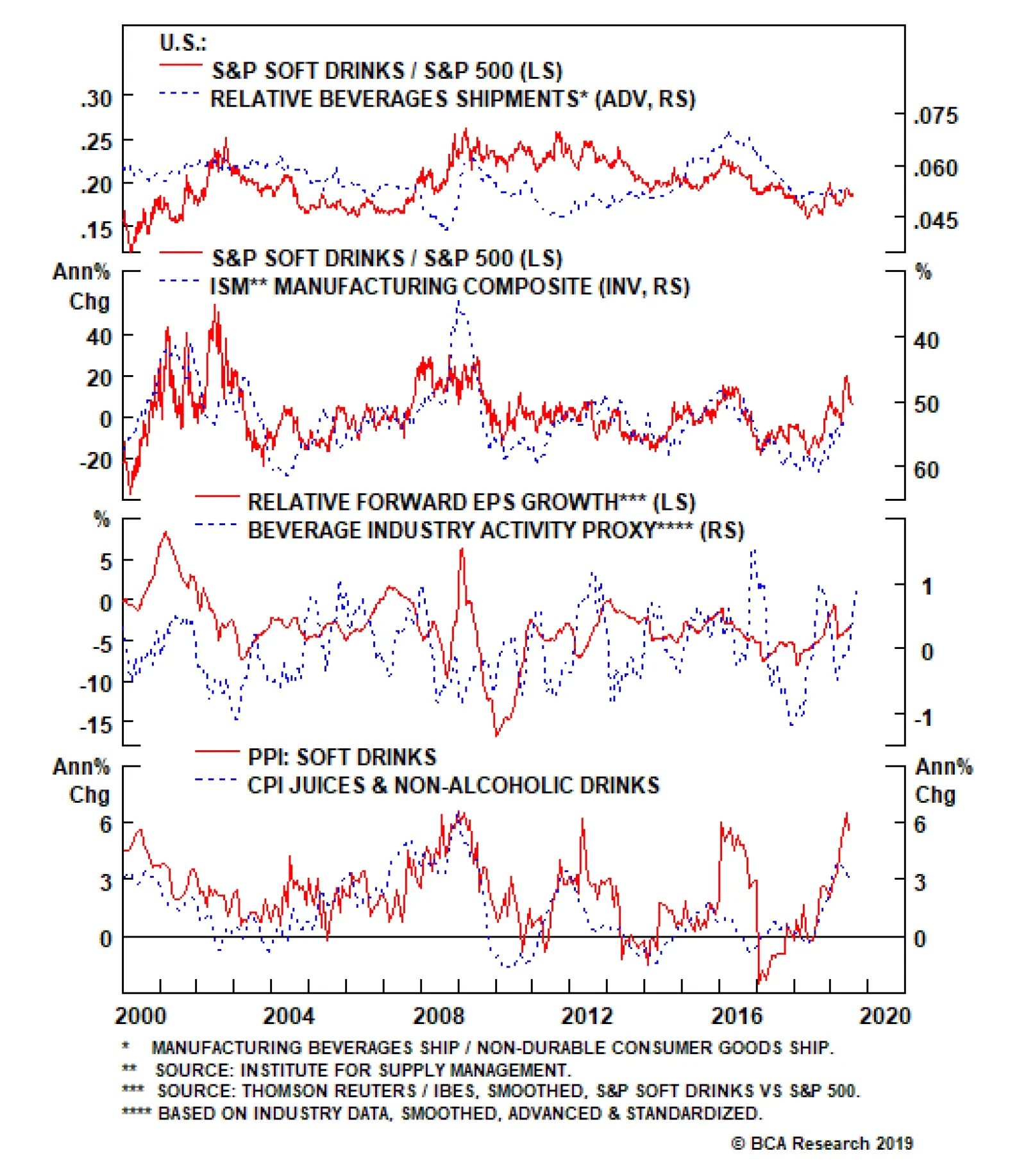

S&P Hypermarkets (Overweight) Upgraded from Neutral S&P Soft Drinks (Neutral) Upgraded from Underweight A deteriorating macro landscape reflected in the steep fall in U.S. economic data surprises, the drubbing of the 10-year U.S. Treasury yield and melting inflation make a compelling case for an overweight stance in the S&P Hypermarkets index (top & second panels). Similarly, safe haven soft drinks stocks shine when economic conditions are deteriorating (third panel). This defensive pure-play consumer goods sub-sector is also enjoying a rebound in operating metrics, and thus it no longer pays to stay bearish. We lifted exposure to neutral last week, locking in gains of 5.5% since inception. S&P Hypermarkets

S&P Hypermarkets

S&P Hypermarkets

S&P Materials (Neutral) Downgraded from Overweight S&P Chemicals (Underweight) Downgraded from Neutral Global macro headwinds continue to weigh on this deep cyclical sub-index as the risks of a full-blown trade war will likely take a bite out of final demand (third panel). Chemical producers garner 60% of their revenues from abroad and falling U.S. chemical exports are troublesome for this index (top & second panels). Given that chemicals have a 74% market cap weight in the S&P materials index, our move to underweight on the sub-index level also pushed the entire S&P materials index to neutral from overweight. S&P Materials

S&P Materials

S&P Materials

S&P Technology (Neutral) Downgrade Alert S&P Software (Overweight) Lifted trailing stops As a part of our portfolio de-risking measures, we put a 27% profit-taking stop loss on our overweight S&P software index call on June 10. Once triggered, a downgrade to neutral in the S&P software index would also push our S&P tech sector weight to a below benchmark allocation. Meanwhile, our EPS model for the overall tech sector is on the verge of contraction on the back of sinking capex and a firming U.S. dollar (middle panel). The San Francisco Fed’s Tech Pulse Index is also closing in on the expansion/contraction line warning that tech stocks are in for a rough ride (bottom panel). S&P Technology

S&P Technology

S&P Technology

S&P Technology Hardware, Storage & Peripherals (Neutral) Downgraded from Overweight As nearly 60% of the revenues for the S&P technology hardware, storage & peripherals (THS&P) index are sourced from abroad, deflating EM currencies sap foreign consumer purchasing power and weigh on the industry’s exports (third panel). Global export volumes have sunk into contractionary territory, to a level last seen during the Great Recession (not shown) and underscore that industry exports will remain under pressure. The IFO World Economic Survey confirms this challenging export backdrop as it is still pointing toward sustained global export ails (second panel). As a result, all of this has shaken our confidence in an overweight stance in the S&P THS&P and we were compelled to move to the sidelines in early June for a modest relative loss since inception. S&P Technology Hardware, Storage & Peripherals

S&P Technology Hardware, Storage & Peripherals

S&P Technology Hardware, Storage & Peripherals

S&P Consumer Discretionary (Underweight) Upgrade Alert S&P Home Improvement Retail (Neutral) Upgraded from underweight In the July 8 Weekly Report, we put the S&P consumer discretionary sector on an upgrade alert as this early-cyclical sector benefits the most from lower interest rates (bottom panel). The way we will execute this upgrade will be by triggering the upgrade alert on the S&P internet retail index. Melting interest rates and rebounding lumber prices are a boon for home improvement retailers (HIR, second & third panels). Tack on profit-augmenting industry productivity gains and it no longer pays to be bearish HIR. S&P Consumer Discretionary

S&P Consumer Discretionary

S&P Consumer Discretionary

S&P Homebuilders (Neutral) Downgraded from overweight Long S&P Homebuilders / Short S&P Home Improvement Retail Booked Profits Lumber represents an input cost to homebuilders (we booked profits of 10% in our overweight recommendation on May 22 and downgraded to neutral) whereas it is an important selling item in Big Box building & supply retailers that make a set margin on it (third panel). On June 18, as part of our de-risking strategy, we locked in 10% gains in the long S&P homebuilders/short S&P home improvement retail trade that hit our stop loss and we moved to the sidelines. S&P Homebuilders

S&P Homebuilders

S&P Homebuilders

S&P Telecommunication Services (Neutral) Upgraded from Underweight The recent escalation of the trade spat has pushed July’s Markit’s flash U.S. manufacturing PMI reading to 50 - the lowest level since the history of the data. Historically, relative S&P telecom services share price momentum has moved inversely with the manufacturing PMI and the current message is to expect a sustained rebound in the former (bottom panel). Rock bottom profit expectations and firming industry operating metrics signal that most of the grim news is priced in bombed out telecom services valuations (middle panel), and it no longer pays to be underweight. In late-May, we lifted exposure to neutral for 6% relative gains since inception. S&P Telecommunication Services

S&P Telecommunication Services

S&P Telecommunication Services

S&P Movies & Entertainment (Overweight) Upgraded from Neutral Structural shifts in the streaming services industry marked a start of a pricing war with incumbents and new entrants fighting for market share, as evidenced by DIS’s pricing of their upcoming Disney+ service. Consumer confidence remains glued to multi-decade highs and there are high odds that the big gulf that has opened up between confidence and relative S&P movies & entertainment share prices will narrow via a rise in the latter (top panel). Moreover, more dollars spent on recreation is synonymous with a margin expansion in the S&P movies & entertainment index (bottom panel). This consumer spending backdrop is also conducive to a rise in relative profitability, the opposite of what the sell-side currently expects. S&P Movies & Entertainment

S&P Movies & Entertainment

S&P Movies & Entertainment

Arseniy Urazov, Research Associate ArseniyU@bcaresearch.com Footnotes 1 Please see BCA U.S. Equity Strategy Weekly Report, “Beware Profit Recession” dated July 8, 2019, available at uses.bcaresearch.com. 2 https://www.bis.org/speeches/sp190514.pdf Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

In the previous Insight we highlighted a number of firming beverage industry operating metrics, however, soft drinks industrial production itself is still waving a yellow flag. In fact, relative output is contracting at the steepest pace in two decades. …

As our U.S. Equity Strategy team continues to shift its portfolio away from cyclical and toward defensive exposure, it is upgrading the S&P soft drinks index from underweight to neutral. This defensive pure-play consumer goods sub-sector sparkles during…

BCA takes pride in its independence. Strategists publish what they really believe, informed by their framework and analysis. Occasionally, this independence results in strongly diverging views and we currently are in one of those times. Within BCA, two views on the cyclical (six to 12-months) outlook for assets have emerged. One camp expects global growth to rebound in the second half of the year. Along with accelerating growth, they anticipate stock prices and risk assets to remain firm, cyclical equities to outperform defensive ones, safe-haven yields to move up, and the dollar to weaken. Meanwhile, another group foresees a further deterioration in activity or a delayed recovery, additional downside in stocks and risk assets, outperformance of defensives relative to cyclicals, low safe-haven yields, and a generally stronger dollar. For the sake of transparency, we have asked representatives of each camp to make their case in a round-table discussion, allowing our clients to decide for themselves which view is more appealing to them. Global Investment Strategy’s Peter Berezin, U.S. Investment Strategy’s Doug Peta, and Global Fixed Income Strategy’s Rob Robis take the mantle for the bullish camp. U.S. Equity Strategy’s Anastasios Avgeriou, Emerging Market Strategy’s Arthur Budaghyan, and European Investment Strategy’s Dhaval Joshi represent the bearish group.1 The round-table discussion below focuses on the cyclical outlook. For longer investment horizons, most strategists agree that a recession is highly likely by 2022. Moreover, on a long-term basis, valuations in both risk assets and safe-haven bonds are very demanding. In this context, a significant back up in yields could hammer risk assets. The BCA Round Table Mathieu Savary: Yield curve inversions have often been harbingers of recessions. Anastasios, you are amongst those investors troubled by this inversion. Do you not worry that this episode might prove similar to 1998, when the curve only inverted temporarily and did not foreshadow a recession? Moreover, how do you account for the highly variable time lags between the inversion of the yield curve and the occurrence of a recession? Chart II-1 (ANASTASIOS)The 1998 Episode Revisited

The 1998 Episode Revisited

The 1998 Episode Revisited

Anastasios Avgeriou: The yield curve inverts at or near the peak of the business cycle and it eventually forewarns of upcoming recessions. This past December, parts of the yield curve inverted and now, BCA’s U.S. Equity Strategy service is heeding the signal from this simple indicator, especially given that the SPX has subsequently made all-time highs as our research predicted.2 The yield curve inversion forecasts a Fed rate cut, and it has never been wrong on that front. It served well investors that heeded the message in June of 1998 as the market soon thereafter fell 20% in a heartbeat. If investors got out at the 1998 peak near 1200 and forwent about 350 points of gains until the March 2000 SPX cycle peak, they still benefited if they held tight as the market ultimately troughed near 777 in October 2002 (Chart II-1). With regard to timing the previous seven recessions using the yield curve, if we accept that mid-1998 is the starting point of the inversion, it took 33 months before the recession commenced. Last cycle, the recession began 24 months after the inversion. Consequently, December 2020 is the earliest possible onset of recession and September 2021, the latest. Our forecast calls for SPX EPS to fall 20% in 2021 to $140 with the multiple dropping between 13.5x and 16.5x for an SPX end-2020 target range of 1,890-2,310.3 In other words we are not willing to play a 100-200 point advance for a potential 1,000 point drawdown. The risk/reward tradeoff is to the downside, and we choose to sit this one out. Mathieu: Rob, you take a much more sanguine view of the current curve inversion. Why? Rob Robis: While the four most dangerous words in investing are “this time is different,” this time really does appear to be different. Never before have negative term premia on longer-term Treasury yields and a curve inversion coexisted (Chart II-2). Longer-term Treasury yields have therefore been pushed down to extremely low levels by factors beyond just expectations of a lower fed funds rate. The negative Treasury term premium is distorting the economic message of the U.S. yield curve inversion. Chart II-2 (ROB)Negative Term Premium Distorting The Economic Message Of An Inverted Yield Curve

Negative Term Premium Distorting The Economic Message Of An Inverted Yield Curve

Negative Term Premium Distorting The Economic Message Of An Inverted Yield Curve

Term premia are depressed everywhere, as seen in German, Japanese and other yields, reflecting the intense demand for safe assets like government bonds during a period of heightened uncertainty. Global bond markets may also be discounting a higher probability of the ECB restarting its Asset Purchase Program, as term premia typically fall sharply when central banks embark on quantitative easing. This has global spillovers. Prior to previous recessions, U.S. Treasury curve inversions occurred when the Fed was running an unequivocally tight monetary policy. That is not the case today. The real fed funds rate still is not above the Fed’s estimate of the neutral real rate, a.k.a. “r-star,” which was the necessary ingredient for all previous Treasury curve inversions since 1960 (Chart II-3). Chart II-3 (ROB)Fed Policy Is Not Tight Enough For Sustained Curve Inversion

Fed Policy Is Not Tight Enough For Sustained Curve Inversion

Fed Policy Is Not Tight Enough For Sustained Curve Inversion

Mathieu: The level of policy accommodation will most likely determine whether Anastasios or Rob is proven right. Peter, you have been steadfastly arguing that policy, in the U.S. at least, remains easy. Can you elaborate why? Peter Berezin: Remember that the neutral rate of interest is the rate that equalizes the level of aggregate demand with the economy’s supply-side potential. Loose fiscal policy and fading deleveraging headwinds are boosting demand in the United States. So is rising wage growth, especially at the bottom of the income distribution. Given that the U.S. does not currently suffer from any major imbalances, I believe that the economy can tolerate higher rates without significant ill-effects. In other words, monetary policy is currently quite easy. Of course, we cannot observe the neutral rate directly. Like a black hole, one can only detect it based on the effect that it has on its surroundings. Housing is by far the most interest rate-sensitive sector of the economy. If history is any guide, the recent decline in mortgage rates will boost housing activity in the remainder of the year (Chart II-4). If that relationship breaks down, as it did during the Great Recession, it would suggest that the neutral rate is quite low. Chart II-4 (PETER)Declining Mortgage Rates Bode Well For Housing

Declining Mortgage Rates Bode Well For Housing

Declining Mortgage Rates Bode Well For Housing

Given that mortgage underwriting standards have been quite strong and the homeowner vacancy is presently very low, our guess is that housing will hold up well. We should know better in the next few months. Mathieu: Dhaval, you do not agree. Why do you think global rates are not accommodative?

Chart II-5

Dhaval Joshi: Actually, I think that global rates are accommodative, but that the global bond yield can rise by just 70 bps before conditions become perilously un-accommodative. Here’s where I disagree with Peter: for me, the danger doesn’t come from economics, it comes from the mathematics of ultra-low bond yields. The unprecedented and experimental panacea of our era has been ‘universal QE’ – which has led to ultra-low bond yields everywhere. But what is not understood is that when bond yields reach and remain close to their lower bound, weird things happen to the financial markets. I refer you to other reports for the details, but in a nutshell, the proximity of the lower bound to yields increases the risk of owning supposedly ‘safe’ bonds to the risk of owning so-called ‘risk-assets’. The result is that the valuation of risk-assets rises exponentially (Chart II-5). Because when the riskiness of the asset-classes converges, investors price risk-assets to deliver the same ultra-low nominal return as bonds.4 Comparisons with previous economic cycles miss the current danger. The post-2000 policy easing distorted the global economy by engineering a credit boom – so the subsequent danger emanated from the most credit-sensitive sectors in the economy such as mortgage lending. In contrast, the post-2008 ‘universal QE’ has severely distorted the valuation relationship between bonds and global risk-assets – so this is where the current danger lies. Higher bond yields can suddenly undermine the valuation support of global risk-assets whose $400 trillion worth dwarfs the global economy by five to one. Where is this tipping point? It is when the global 10-year yield – defined as the average of the U.S., euro area,5 and China – approaches 2.5%. Through the past five years, the inability of this yield to remain above 2.5% confirms the hyper-sensitivity of financial conditions to this tipping point (Chart II-6). Right now, I agree that bond yields are accommodative. But the scope for yields to move higher is quite limited. Chart II-6 (DHAVAL)Since 2015, the Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Since 2015, the Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Since 2015, the Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Mathieu: Monetary policy is important to the outlook, but so is the global manufacturing cycle. The global growth slowdown has been concentrated in the manufacturing sector, tradeable goods in particular. Across advanced economies, the service and consumer sectors have been surprisingly resilient, but this will not last if the industrial sector decelerates further. Arthur, you still do not anticipate any major improvement in global trade and industrial production. Can you elaborate why? Chart II-7 (ARTHUR)Global Trade Is Down Due To China Not U.S.

Global Trade Is Down Due To China Not U.S.

Global Trade Is Down Due To China Not U.S.

Arthur Budaghyan: To properly assess the economic outlook, one needs to understand what has caused the ongoing global trade/manufacturing downturn. One thing we know for certain: It originated in China, not the U.S. Chart II-7 illustrates that Korean, Japanese, Taiwanese and Singaporean exports to China have been shrinking at an annual rate of 10%, while their shipments to the U.S. have been growing. China’s aggregate imports have also been contracting. This entails that from the perspective of the rest of the world, China has been and remains in recession. Chart II-8 (ARTHUR)Stimulus Versus Marginal Propensity To Spend

Stimulus Versus Marginal Propensity To Spend

Stimulus Versus Marginal Propensity To Spend

U.S. manufacturing is the least exposed to China, which is the main reason why it has been the last shoe to drop. Hence, the U.S. has lagged in this downturn, and one should not be looking to the U.S. for clues about a potential global recovery. We need to gauge what will turn Chinese demand around. In this regard, the rising credit and fiscal spending impulse is positive, but it has so far failed to kick start a recovery (Chart II-8). The key reason has been a declining marginal propensity to spend among households and companies. Notably, the marginal propensity to spend of mainland companies leads industrial metals prices by a few months, and it currently continues to point south (Chart II-8, bottom panel). The lack of willingness among Chinese consumers and enterprises to spend is due to several factors: (1) the U.S.-China confrontation; (2) high levels of indebtedness among both enterprises and households (Chart II-9); (3) ongoing regulatory scrutiny over banks and shadow banking as well as local government debt; and (4) a lack of outright government subsidies for purchases of autos and housing. Chart II-9 (ARTHUR)Chinese Households Are Leveraged Than U.S. Ones

Chinese Households Are Leveraged Than U.S. Ones

Chinese Households Are Leveraged Than U.S. Ones

On the whole, the falling marginal propensity to spend will all but ensure that any recovery in mainland household and corporate spending is delayed. Mathieu: Meanwhile, Peter, you have a much more optimistic stance. Why do you differ so profoundly with Arthur’s view? Peter: China’s deleveraging campaign began more than a year before global manufacturing peaked. I have no doubt that slower Chinese credit growth weighed on global capex, but we should not lose sight of the fact there are natural ebbs and flows at work. Most manufactured goods retain some value for a while after they are purchased. If spending on, say, consumer durable goods or business equipment rises to a high level for an extended period, a glut will form, requiring a period of lower production. These demand cycles typically last about three years; roughly 18 months on the way up, 18 months on the way down (Chart II-10). The last downleg in the global manufacturing cycle began in early 2018, so if history is any guide, we are nearing a trough. The fact that U.S. manufacturing output rose in both May and June, followed by this week’s sharp rebound in the July Philly Fed Manufacturing survey, supports this view. Chart II-10 (PETER)The Global Manufacturing Cycle Has Likely Reached A Bottom

The Global Manufacturing Cycle Has Likely Reached A Bottom

The Global Manufacturing Cycle Has Likely Reached A Bottom

Of course, extraneous forces could complicate matters. If trade tensions ratchet higher, this would weaken my bullish thesis. Nevertheless, with China stimulating its economy again, it would probably take a severe trade war to push the global economy into recession. Mathieu: Dhaval, you are not as negative as Arthur, but nonetheless expect a slowdown in the second half of the year. What is your rationale? Dhaval: To be clear, I am not forecasting a recession or major downturn – unless, as per my previous answer, the global 10-year bond yield approaches 2.5% and triggers a severe dislocation in global risk-assets. In fact, many people get the relationship between recession and financial market dislocation back-to-front: they think that the recession causes the financial market dislocation when, in most cases, the financial market dislocation causes the recession! Nevertheless, I do believe that European and global growth is entering a regular down-oscillation based on the following compelling evidence: 1. From a low last summer, quarter-on-quarter GDP growth rates in the developed economies have already rebounded to the upper end of multi-year ranges. 2. Short-term credit impulses in Europe, the U.S., and China are entering down-oscillations (Chart II-11). Chart II-11 (DHAVAL)Short-Term Impulses Rebounded... But Are Now Rolling Over

Short-Term Impulses Rebounded... But Are Now Rolling Over

Short-Term Impulses Rebounded... But Are Now Rolling Over

3. The best current activity indicators, specifically the ZEW economic sentiment indicators, have rolled over. 4. The outperformance of industrials – the equity sector most exposed to global growth – has also rolled over. Why expect a down-oscillation? Because it is the rate of decline in the bond yield that drove the rebound in growth after its low last summer. Furthermore, it is impossible for the rate of decline in the bond yield to keep increasing, or even stay where it is. Counterintuitively, if bond yields decline, but at a reduced pace, the effect is to slow economic growth. Mathieu: A positive and a negative view of the world logically result in bifurcated outlooks for interest rates and the dollar. Rob, how do you see U.S., German, and Japanese yields evolving over the coming 12 months? Rob: If global growth rebounds, U.S. Treasury yields will have far more upside than Bund or JGB yields. Inflation expectations should recover faster in the U.S., with the Fed taking inflationary risks by cutting rates with a 3.7% unemployment rate and core CPI inflation at 2.1%. The Fed is also likely to disappoint by delivering fewer rate cuts than are currently discounted by markets (90bps over the next 12 months). Treasury yields can therefore increase more than German and Japanese yields, with the ECB and BoJ more likely to deliver the modest rate cuts currently discounted in their yield curves (Chart II-12). Chart II-12 (ROB)U.S. Treasuries Will Underperform Bunds & JGBs

U.S. Treasuries Will Underperform Bunds & JGBs

U.S. Treasuries Will Underperform Bunds & JGBs

Japanese yields will remain mired at or below zero over the next 6-12 months, as wage growth and core inflation remain too anemic for the BoJ to alter its 0% target on 10-year JGB yields. German yields have a bit more potential to rise if European growth begins to recover, but will lag any move higher in Treasury yields. That means that the Treasury-Bund and Treasury-JGB spreads will move higher over the next year. Negative German and Japanese yields may look completely unappetizing compared to +2% U.S. Treasury yields, but this handicap vanishes when all three yields are expressed in U.S. dollar terms. Hedging a 10-year German Bund or JGB into higher-yielding U.S. dollars creates yields that are 50-60bps higher than a 10-year U.S. Treasury. It is abundantly clear that German and Japanese bonds will outperform Treasuries over the next year if global growth recovers. Mathieu: Peter, your positive view on global growth means that the Fed will cut rates less than what is currently priced into the OIS curve. So why do you expect the dollar to weaken in the second half of 2019? Peter: What the Fed does affects interest rate differentials, but just as important is what other central banks do. The ECB is not going to raise rates over the next 12 months. However, if euro area growth surprises on the upside later this year, investors will begin to question the need for the ECB to keep policy rates in negative territory until mid-2024. The market’s expectation of where policy rates will be five years out tends to correlate well with today’s exchange rate. By that measure, there is scope for interest rate differentials to narrow against the U.S. dollar (Chart II-13). Chart II-13A (PETER)Interest Rate Expectations Against The U.S. Should Narrow (II)

Interest Rate Expectations Against The U.S. Should Narrow (I)

Interest Rate Expectations Against The U.S. Should Narrow (I)

Chart II-13B (PETER)Interest Rate Expectations Against The U.S. Should Narrow (I)

Interest Rate Expectations Against The U.S. Should Narrow (II)

Interest Rate Expectations Against The U.S. Should Narrow (II)

Chart II-14 (PETER)The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Keep in mind that the U.S. dollar is a countercyclical currency, meaning that it moves in the opposite direction of global growth (Chart II-14). This countercyclicality stems from the fact that the U.S. economy is more geared towards services than manufacturing compared with the rest of the world. As such, when global growth accelerates, capital tends to flow from the U.S. to the rest of the world, translating into more demand for foreign currency and less demand for dollars. If global growth picks up in the remainder of the year, as I expect, the dollar will weaken. Mathieu: Arthur, as you are significantly more negative on growth than either Rob or Peter, how do you see the dollar and global yields evolving over the coming six to 12 months? Arthur: I am positive on the trade-weighted U.S. dollar for the following reasons: The U.S. dollar is a countercyclical currency – it exhibits a negative correlation with the global business cycle. Persistent weakness in the global economy emanating from China/EM is positive for the dollar because the U.S. economy is the major economic block least exposed to a China/EM slowdown. Meanwhile, the greenback is only loosely correlated with U.S. interest rates. Thereby, the argument that lower U.S. rates will drive the value of the U.S. currency much lower is overemphasized. The Federal Reserve will cut rates by more than what is currently priced into the market only in a scenario of a complete collapse in global growth. Yet this scenario would be dollar bullish. In this case, the dollar’s strong inverse relationship with global growth will outweigh its weak positive relationship with interest rates. Contrary to consensus views, the U.S. dollar is not very expensive. According to unit labor costs based on the real effective exchange rate – the best currency valuation measure – the greenback is only one standard deviation above its fair value. Often, financial markets tend to overshoot to 1.5 or 2 standard deviations below or above their historical mean before reversing their trend. One of the oft-cited headwinds facing the dollar is positioning, yet there is a major discrepancy between positioning in DM and EM currencies versus the U.S. dollar. In aggregate, investors – asset managers and leveraged funds – have neutral exposure to DM currencies, but they are very long liquid EM exchange rates such as the BRL, MXN, ZAR and RUB versus the greenback. The dollar strength will occur mostly versus EM and commodities currencies. In other words, the euro, other European currencies and the yen will outperform EM exchange rates. I have less conviction on global bond yields. While global growth will disappoint, yields have already fallen a lot and the U.S. economy is currently not weak enough to justify around 90 basis points of rate cuts over the next 12 months. Mathieu: Before we move on to investment recommendations, Anastasios, you have done a lot of interesting work on the outlook for U.S. profits. What is the message of your analysis? Chart II-15 (ANASTASIOS)Gravitational Pull

Gravitational Pull

Gravitational Pull

Anastasios: While markets cheered the trade truce following the recent G-20 meeting, no tariff rollback was agreed. Since the tariff rate on $200bn of Chinese imports went up from 10% to 25% on May 10, odds are high that manufacturing will remain in the doldrums. This will likely continue to weigh on profits for the remainder of the year. Profit growth should weaken further in the coming six months. Periods of falling manufacturing PMIs result in larger negative earnings growth surprises as market forecasters rarely anticipate the full breadth and depth of slowdowns. Absent profit growth, equity markets lack the necessary ‘oxygen’ for a durable high-quality rally. Until global growth momentum turns, investors should fade rallies. Our four-factor SPX EPS growth model is flirting with the contraction zone. In addition, our corporate pricing power proxy and Goldman Sachs’ Current Activity Indicator both send a distress signal for SPX profits (Chart II-15). Already, more than half of the S&P 500 GICS1 sectors’ profits are estimated to have contracted in Q2, and three sectors could see declining revenues on a year-over-year basis, according to I/B/E/S data. Q3 depicts an equally grim profit picture that will also spill over to Q4. Adding it all up, profits will underwhelm into year-end. Mathieu: Doug, you do not share Anastasios’s anxiety. What offsets do you foresee? Moreover, you are not concerned by the U.S. corporate balance sheets. Can you share why? Doug Peta: As it relates to earnings, we foresee offsets from a revival in the rest of the world. Increasingly accommodative global monetary policy and reviving Chinese growth will give global ex-U.S. economies a boost. That inflection may go largely unnoticed in U.S. GDP, but it will help the S&P 500, as U.S.-based multinationals’ earnings benefit from increased overseas demand and a weaker dollar. When it comes to corporate balance sheets, shifting some of the funding burden to debt from equity when interest rates are at generational lows is a no-brainer. Even so, non-financial corporates have not added all that much leverage (Chart II-16). Low interest rates, wide profit margins and conservative capex have left them with ample free cash flow to service their obligations (Chart II-17). Chart II-16 (DOUG)Corporations Have Not Added Much Leverage ...

Corporations Have Not Added Much Leverage ...

Corporations Have Not Added Much Leverage ...

Chart II-17 (DOUG)...Though They Have Ample Cash Flow To Service It

...Though They Have Ample Cash Flow To Service It

...Though They Have Ample Cash Flow To Service It

Every single viable corporate entity with an effective federal tax rate above 21% became a better credit when the top marginal rate was cut from 35% to 21%. Every such corporation now has more net income with which to service debt, and will have that income unless the tax code is revised. You can’t see it in EBITDA multiples, but it will show up in reduced defaults. Mathieu: The last, and most important question. What are each of your main investment recommendations to capitalize on the economic trends you anticipate over the coming 6-12 months? Let’s start with the pessimists: Arthur: First, the rally in global cyclicals and China plays since December has been premature and is at risk of unwinding as global growth and cyclical profits disappoint. Historical evidence suggests that global share prices have not led but have actually been coincident with the global manufacturing PMI (Chart II-18). The recent divergence is unprecedented. Chart II-18 (ARTHUR)Global Stocks Historically Did Not Lead PMIs

Global Stocks Historically Did Not Lead PMIs

Global Stocks Historically Did Not Lead PMIs

Chart II-19 (ARTHUR)China And EM Profits Are Contracting

China And EM Profits Are Contracting

China And EM Profits Are Contracting

Second, EM risk assets and currencies remain vulnerable. EM and Chinese earnings per share are shrinking. The leading indicators signal that the rate of contraction will deepen, at least the end of this year (Chart II-19). Asset allocators should continue underweighting EM versus DM equities. Finally, my strongest-conviction, market-neutral trade is to short EM or Chinese banks and go long U.S. banks. The latter are much healthier than EM/Chinese ones, as we discussed in our recent report.6 Anastasios: The U.S. Equity Strategy team is shifting away from a cyclical and toward a more defensive portfolio bent. Our highest conviction view is to overweight mega caps versus small caps. Small caps are saddled with debt and are suffering a margin squeeze. Moreover, approximately 600 constituents of the Russell 2000 have no forward profits. Only one S&P 500 company has negative forward EPS. Given that both the S&P and the Russell omit these figures from the forward P/E calculation, this is masking the small cap expensiveness. When adjusted for this discrepancy, small caps are trading at a hefty premium versus large caps (Chart II-20). We have also upgraded the S&P managed health care and the S&P hypermarkets groups. If the economic slowdown persists into early 2020, both of these defensive subgroups will fare well. In mid-April, we lifted the S&P managed health care group to an above benchmark allocation and posited that the selloff in this group was overdone as the odds of “Medicare For All” becoming law were slim. Moreover, a tight labor market along with melting medical cost inflation would boost the industry’s margins and profits (Chart II-21). Chart II-20 (ANASTASIOS)Continue To Avoid Small Caps

Continue To Avoid Small Caps

Continue To Avoid Small Caps

Chart II-21 (ANASTASIOS)Buy Hypermarkets

Buy Hypermarkets

Buy Hypermarkets

Chart II-22 (ANASTASIOS)Stick With Managed Health Care

Stick With Managed Health Care

Stick With Managed Health Care

This week, we upgraded the defensive S&P hypermarkets index to overweight arguing that the souring macro landscape coupled with a firming industry demand outlook will support relative share prices (Chart II-22). Dhaval: To be fair, I am not a pessimist. Provided the global bond yield stays well below 2.5 percent, the support to risk-asset valuations will prevent a major dislocation. But in a growth down-oscillation, the big game in town will be sector rotation into pro-defensive investment plays, especially into those defensives that have underperformed (Chart II-23). On this basis: Overweight Healthcare versus Industrials. Overweight the Eurostoxx 50 versus the Shanghai Composite and the Nikkei 225. Overweight U.S. T-bonds versus German bunds. Overweight the JPY in a portfolio of G10 currencies. Chart II-23 (DHAVAL)Switch Out Of Growth-Sensitives Into Healthcare

Switch Out Of Growth-Sensitives Into Healthcare

Switch Out Of Growth-Sensitives Into Healthcare

Mathieu: And now, the optimists: Doug: So What? is the overriding question that guides all of BCA’s research: What is the practical investment application of this macro observation? But Why Now? is a critical corollary for anyone allocating investment capital: Why is the imbalance you’ve observed about to become a problem? As Herbert Stein said, “If something cannot go on forever, it will stop.” Imbalances matter, but Dornbusch’s Law counsels patience in repositioning portfolios on their account: “Crises take longer to arrive than you can possibly imagine, but when they do come, they happen faster than you can possibly imagine.” Look at Chart II-24, which shows a vast white sky (bull markets) with intermittent clusters of gray (recessions) and light red (bear markets) clouds. Market inflections are severe, but uncommon. When the default condition of an economy is to grow, and equity prices to rise, it is not enough for an investor to identify an imbalance, s/he also has to identify why it’s on the cusp of reversing. Right now, as it relates to the U.S., there aren’t meaningful imbalances in either markets or the real economy. Chart II-24 (DOUG)Recessions And Bear Markets Travel Together

Recessions And Bear Markets Travel Together

Recessions And Bear Markets Travel Together

Even if we had perfect knowledge that a recession would arrive in 18 months, now would be way too early to sell. The S&P 500 has historically peaked an average of six months before the onset of a recession, and it has delivered juicy returns in the year preceding that peak (Table II-1). Bull markets tend to sprint to the finish line (Chart II-25). If this one is like its predecessors, an investor risks significant relative underperformance if s/he fails to participate in its go-go latter stages.

Chart II-

Chart II-25

We are bullish on the outlook for the next six to twelve months, and recommend overweighting equities and spread product in balanced U.S. portfolios while significantly underweighting Treasuries. Peter: I agree with Doug. Equity bear markets seldom occur outside of recessions and recessions rarely occur when monetary policy is accommodative. Policy is currently easy, and will get even more stimulative if the Fed and several other central banks cut rates. Global equities are not super cheap, but they are not particularly expensive either. They currently trade at about 15-times forward earnings. Given the ultra-low level of global bond yields, this generates an equity risk premium (ERP) that is well above its historical average (Chart II-26). One should favor stocks over bonds when the ERP is high. Chart II-26A (PETER)Equity Risk Premia Remain Elevated (I)

Equity Risk Premia Remain Elevated (I)

Equity Risk Premia Remain Elevated (I)

Chart II-26B (PETER)Equity Risk Premia Remain Elevated (II)

Equity Risk Premia Remain Elevated (II)

Equity Risk Premia Remain Elevated (II)

The ERP is especially elevated outside the United States. This is partly because non-U.S. stocks trade at a meager 13-times forward earnings, but it also reflects the fact that bond yields are lower overseas. As global growth accelerates, the dollar will weaken. Equity sectors and regions with a more cyclical bent will benefit (Chart II-27). We expect to upgrade EM and European stocks later this summer. A softer dollar will also benefit gold. Bullion will get a further boost early next decade when inflation begins to accelerate. We went long gold on April 17, 2019 and continue to believe in this trade. Rob: For fixed income investors, the most obvious way to play a combination of monetary easing and recovering global growth is to overweight corporate debt versus government bonds (Chart II-28). Chart II-27 (PETER)EM And Euro Area Equities Outperform When Global Growth Improves

EM And Euro Area Equities Outperform When Global Growth Improves

EM And Euro Area Equities Outperform When Global Growth Improves

Chart II-28 (ROB)Best Bond Bets: Overweight Global Corporates & Inflation-Linked Bonds

Best Bond Bets: Overweight Global Corporates & Inflation-Linked Bonds

Best Bond Bets: Overweight Global Corporates & Inflation-Linked Bonds

Within the U.S., corporate bond valuations look more attractive in high-yield over investment grade. Assuming a benign outlook for default risk in a reaccelerating U.S. economy, with the Fed easing, going for the carry in high-yield looks interesting. Emerging market credit should also do well if we see a bit of U.S. dollar weakness and additional stimulus measures in China. European corporates, however, may end up being the big winner if the ECB chooses to restart its Asset Purchase Program and ramps up its buying of European company debt. There are fewer restrictions for the ECB to buy corporates compared to the self-imposed limits on government bond purchases. The ECB would be entering a political minefield if it chose to buy more Italian debt and less German debt, but nobody would mind if the ECB helped finance European companies by buying their bonds. If one expects reflation to be successful, a below-benchmark stance on portfolio duration also makes sense given the current depressed level of government bond yields worldwide. Yields are more likely to grind upward than spike higher, and will be led first by increasing inflation expectations. Inflation-linked bonds should feature prominently in fixed income portfolios, especially in the U.S. where TIPS will outperform nominal yielding Treasuries. Mathieu: Thank you very much to all of you. Below is a comparative summary of the main arguments and investment recommendations of each camp. Anastasios Avgeriou U.S. Equity Strategist Peter Berezin Chief Global Strategist Arthur Budaghyan Chief Emerging Markets Strategist Dhaval Joshi Chief European Investment Strategist Doug Peta Chief U.S. Investment Strategist Robert Robis Chief Fixed Income Strategist Mathieu Savary The Bank Credit Analyst Summary Of Views And Recommendations The Bulls…

Image

…And The Bears

Image

Footnotes 1 To be fair to each individual involved, this is simplifying their views. Even within each camp, the negativity or positivity ranges on a spectrum, as you will be able to tell from the debate itself. 2 Please see BCA U.S. Equity Strategy Weekly Report, “Signal Vs. Noise,” dated December 17, 2018, available at uses.bcaresearch.com. 3 Please see BCA U.S. Equity Strategy Weekly Report, “A Recession Thought Experiment,” dated June 10, 2019, available at uses.bcaresearch.com. 4 Please see the European Investment Strategy Weekly Report “Risk: The Great Misunderstanding Of Finance,” October 25, 2018 available at eis.bcaresearch.com. 5 France is a good proxy for the euro area. 6 Please see Emerging Markets Strategy Weekly Report, “On Chinese Banks And Brazil,” available at ems.bcaresearch.com.

(Part II) Bubbling Up

(Part II) Bubbling Up

Neutral While in the previous Insight we highlighted a number of firming beverage industry operating metrics, soft drinks industrial production is still waving a yellow flag. In fact, relative output is contracting at the steepest pace in two decades (middle panel). A quick inventory check explains part of this softness. Beverage inventories continue to expand and this supply overhang will continue to weigh on output until inventory clears all channels (not shown). Finally, soft drinks stocks are trading at a 37% premium to the broad market and near the top end of the historical range. While this frothy valuation backdrop is worrisome, should earnings continue to surprise to the upside as we expect in the coming quarters then soft drink equities will grow into their pricey valuations. Bottom Line: Upgrade the S&P soft drinks index from underweight to neutral and lock profits of 5.5% since inception. The ticker symbols for the stocks in this index are: BLBG: S5SOFD - PEP, KO, MNST.

(Part I) Bubbling Up

(Part I) Bubbling Up

Neutral As we continue shifting our portfolio away from cyclical and toward defensive exposure, we are upgrading the S&P soft drinks index from underweight to neutral, locking in a relative gain of 5.5% since inception. This defensive pure-play consumer goods sub-sector sparkles during economic slumps and heightened policy uncertainty (ISM shown inverted, second panel). Despite the broad-based slowing inflation data, both the soft drinks industry’s CPI and PPI measures continue growing at a healthy pace (bottom panel). PEP and KO results reflected this rising pricing power backdrop, as both companies had success in passing these price hikes down the supply chain. Moreover, relative beverage shipments have likely troughed, and similar to overall non-discretionary sales outshining discretionary retail sales (not shown), signal that a brighter demand backdrop looms. Importantly, our beverage industry activity proxy corroborates this message pointing to a recovery in relative profit growth (third panel). However, there are a couple of thorny issues that are still keeping us at bay and preventing us from lifting exposure all the way to overweight (please see the next Insight).

Stick With Airlines For Now

Stick With Airlines For Now

Overweight-Downgrade Alert Airline stocks bounced off a critical support level on the back of encouraging profit results (top panel). Lower kerosene prices especially for the non-hedged carriers are flowing straight to the bottom line and a busy travel season signals additional gains in the coming months (jet fuel shown inverted, second panel). Not only domestic, but also international airfares are rebounding smartly and signal more revenue growth for airline stocks despite the grounding of the 737 MAX jet likely into 2020 (third panel). Sell side analysts have taken notice and the industry’s net EPS revisions ratio is on a slingshot recovery. While we continue to avoid rails (see the recent Insight) and remain neutral on airfreight & logistics, airlines are a positive exception within transports. Bottom Line: Stick with an above benchmark allocation in the S&P airlines index, but stay tuned. The ticker symbols for the stocks in this index are: BLBG: S5AIRL - DAL, LUV, UAL, AAL and ALK.

Housekeeping

Housekeeping

Last Thursday we were stopped out from our tactical S&P semi equipment underweight position as it hit our -7% stop loss (bottom panel). We are obeying the stop loss and are returning this index to a neutral weighting as better than expected profits from both ASML and TSMC lifted all chip-related equities. In marked contrast, our long global gold miners/short S&P oil & gas exploration & production trade initiated just last week has gone parabolic, spiking to 17% (top panel). While our thesis has not changed in this high beta tactical pair trade, from a risk management perspective, we are moving our stop loss from -10% to +12% in order to protect profits. Bottom Line: Stick with the counter-cyclical long global gold miners/short S&P oil & gas exploration & production trade via the long GDX:US/short XOP:US exchange traded funds. For additional details on the rationale behind this trade, please refer to last Monday’s Weekly Report.

Last week we participated in BCA’s inaugural roundtable discussion where three bullish strategists sat across three bearish ones and debated global growth, the yield curve’s message, the profit outlook, to name a few, and concluded with a number of investment recommendations. What follows is a snippet of our conversation. “Mathieu: Before we move on to investment recommendations, Anastasios, you have done a lot of interesting work on the outlook for U.S. profits. What is the message of your analysis? Anastasios: While markets cheered the trade truce following the recent G-20 meeting, no tariff rollback was agreed. Since the tariff rate on $200bn of Chinese imports went up from 10% to 25% on May 10, odds are high that manufacturing will remain in the doldrums. This will likely continue to weigh on profits for the remainder of the year. Profit growth should weaken further in the coming six months (see Chart 1). Periods of falling manufacturing PMI result in larger negative earnings growth surprises as market forecasters rarely anticipate the full breadth and depth of slowdowns. Absent profit growth, equity markets lack the necessary ‘oxygen’ for a durable high-quality rally. Until global growth momentum turns, investors should fade rallies. Our four-factor SPX EPS growth model is flirting with the contraction zone. In addition, our corporate pricing power proxy and Goldman Sachs’ Current Activity Indicator both send a distress signal for SPX profits (see Charts 1 and 2). Chart 1

The BCA Roundtable

The BCA Roundtable

Chart 2

The BCA Roundtable

The BCA Roundtable

Already, more than half of the S&P 500 GICS1 sectors’ profits are forecast to contract in Q2, and three sectors could see declining revenues versus a year ago comps, according to I/B/E/S data. Q3 depicts an equally grim profit picture that will also spill over to Q4. Adding it all up, profits will underwhelm into yearend.” Please refer to last Friday’s Special Report for additional details.

Avoid Getting Railroaded

Avoid Getting Railroaded

Underweight Our underweight S&P railroads call has moved into the black as CSX rattled the industry and chopped 2019 revenue growth from positive 1-2% to negative 2%. While UNP’s numbers were better than expected and partially offset CSX’s weakness, transport data does not lie and warns that a sizable slowdown is already underway in rail freight (second panel). In fact, our rail shipments diffusion indicator is sinking like a stone to levels last hit at the depths of the GFC (third panel). Such broad-based weakness in nearly every rail carload category is worrisome and warns that overly optimistic relative profit expectations (not shown) will suffer a setback. Softening demand for rail freight services will likely remain under intense downward pressure as there is little progress made on the U.S./China trade spat front. As a result, industry pricing power will continue to wane and ignite a de-rating phase in rail valuations (bottom panel). Bottom Line: Stay underweight the S&P railroads index. The ticker symbols for the stocks in this index are: BLBG: S5RAIL - UNP, CSX, NSC, KSU.