Sectors

The worst of the drubbing in German automobile production is likely behind us, as new orders have recently gone vertical. Backlogs are also sky-high and suggest that a definitive turn looms in German motor vehicle output. The leading indicators of Japanese…

Highlights Chart 1Track The CRB/Gold Ratio

Track The CRB/Gold Ratio

Track The CRB/Gold Ratio

Earlier this year the Fed signaled a dovish policy shift in response to slowing global growth and tighter financial conditions. In large part due to the Fed’s move, financial conditions are now easing and the CRB Raw Industrials index – a timely proxy for global growth – is starting to perk up. But when will this improvement translate to higher Treasury yields? The CRB/gold ratio offers some clues. Gold moves higher when monetary policy eases. Then with a lag, that easier policy spurs stronger global growth and a rising CRB index. Eventually, that stronger growth puts rate hikes back on the table. A more hawkish Fed limits the upside in gold and sends Treasury yields higher. In fact, we find that the 10-year Treasury yield only starts to rise when the CRB index outpaces the gold price (Chart 1). The recent jump in the CRB index is a positive sign, but we shouldn’t expect Treasury yields to rise until the CRB/gold ratio heads higher. In the meantime, investors should maintain below-benchmark portfolio duration and initiate positive-carry yield curve trades (see page 10) to boost returns while we wait for the next upward adjustment in yields. Feature Investment Grade: Overweight Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 59 basis points in February, bringing year-to-date excess returns up to +243 bps. The Federal Reserve’s pause opens a window for corporate spreads to tighten during the next few months. We recommend overweight positions in corporate bonds for now, but will be quick to reduce exposure once spreads reach our near-term targets (Chart 2). Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

In last week’s report we published option-adjusted spread targets for each corporate credit tier.1 The targets are based on the median 12-month breakeven spreads during prior periods when the slope of the yield curve is quite flat but not yet inverted, what we call a Phase 2 environment.2 Currently, the Aa-rated spread of 59 bps is 3 bps above our target (panel 2). The A-rated spread of 91 bps is 6 bps above our target (panel 3). The Baa-rated spread of 156 bps is 28 bps above our target (panel 4). The Aaa-rated spread is already below our target. We advise investors to avoid the Aaa-rated credit tier. With profit growth poised to moderate during the next few quarters, it is unlikely that gross corporate leverage will continue to decline at its current pace (bottom panel). As such, we will be quick to reduce corporate bond exposure when spreads reach our targets. Renewed Fed hawkishness will be another headwind for corporate bonds in the second half of the year.

Chart

Chart

High-Yield: Overweight High-Yield outperformed the duration-equivalent Treasury index by 175 basis points in February, bringing year-to-date excess returns up to +590 bps. In last week’s report we published near-term spread targets for each high-yield credit tier.3 The targets are based on the median 12-month breakeven spreads seen during periods when the yield curve is quite flat but not yet inverted, what we call a Phase 2 environment.4 At present, the Ba-rated option-adjusted spread is 224 bps, 37 bps above our target. The B-rated spread is 376 bps, 81 bps above our target. The Caa-rated spread is 780 bps, 208 bps above our target. Our default-adjusted spread is an alternative measure of high-yield valuation. It represents the excess spread available in the High-Yield index after accounting for expected default losses. It is currently 243 bps, very close to the historical average of 250 bps (Chart 3). In other words, if corporate defaults match the Moody’s baseline forecast during the next 12 months, high-yield bonds will return 243 bps in excess of duration-matched Treasuries, assuming no change in spreads. Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

The Moody’s baseline forecast calls for a default rate of 2.4% during the next 12 months. This appears a touch too optimistic, as our own macro model is calling for a default rate closer to 3.5%.5 In either case, junk bonds currently offer adequate compensation for default risk. MBS: Neutral Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 6 basis points in February, bringing year-to-date excess returns up to +39 bps. The conventional 30-year zero-volatility spread tightened 2 bps on the month, driven by a 5 bps decline in the compensation for prepayment risk (option cost). The fall in option cost was partially offset by a 3 bps widening in the option-adjusted spread (OAS). The recent drop in the 30-year mortgage rate led to a jump in mortgage refinancings from historically low levels, putting some temporary upward pressure on MBS spreads (Chart 4). However, the relatively tepid pace of new issuance during the past few years means that the existing MBS stock is not very exposed to refinancing risk, even if mortgage rates fall further. All in all, we view agency MBS as one of the safest spread products in the current macro environment. Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

The problem with MBS is that valuation remains unattractive. The index option-adjusted spread for conventional 30-year MBS is well below its average pre-crisis level (panel 3) and the sector offers less compensation than normal compared to corporate bonds (panel 4). We continue to recommend a neutral allocation to agency MBS. An upgrade will only be appropriate when value in the corporate sector is no longer attractive relative to expected default risk. Government-Related: Underweight The Government-Related index outperformed the duration-equivalent Treasury index by 38 basis points in February, bringing year-to-date excess returns up to +92 bps. Sovereign debt outperformed duration-equivalent Treasuries by 97 bps on the month, bringing year-to-date excess returns up to +320 bps. Local Authorities outperformed the Treasury benchmark by 54 bps in February, bringing year-to-date excess returns up to +86 bps. Foreign Agencies outperformed by 44 bps in February, bringing year-to-date excess returns up to +109 bps, while Domestic Agencies outperformed by 12 bps on the month, bringing year-to-date excess returns up to +9 bps. Supranationals outperformed by 10 bps in February, bringing year-to-date excess returns up to +13 bps. The USD-denominated sovereign debt of most countries continues to look expensive relative to equivalently-rated U.S. corporate credit. However, in a recent report we highlighted that Mexican sovereign debt is an exception (Chart 5).6 Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

Not only is Mexican sovereign debt cheap relative to U.S. corporate credit, but our Emerging Markets Strategy service highlights that the Mexican peso is very cheap as measured by the real effective exchange rate based on unit labor costs.7 This is not surprising given that the peso has been relatively flat versus the dollar during the past two years, despite real interest rates being much higher in Mexico than in the U.S. Municipal Bonds: Overweight Municipal bonds outperformed the duration-equivalent Treasury index by 85 basis points in February, bringing year-to-date excess returns up to +92 bps (before adjusting for the tax advantage). The average Aaa-rated Municipal / Treasury yield ratio fell 5% in February, and currently sits at 81% (Chart 6). This is more than one standard deviation below its post-crisis mean and right at the average level that prevailed in the late stages of the previous cycle, between mid-2006 and mid-2007. Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

In other words, municipal bonds on average are no longer cheap. Rather, they appear fairly valued compared to similar prior macro environments. But a pure focus on the average yield ratio across the curve hides an important distinction. The yield ratio for short maturities (2-year and 5-year) is very low relative to history, while the yield ratio for long maturities (10-year, 20-year and 30-year) remains quite cheap (panel 2). Investors should continue to focus on long-maturity municipal debt to add yield to U.S. bond portfolios. In our research into the phases of the credit cycle, we often divide the cycle based on the slope of the yield curve. Since 1983, in the middle phase of the credit cycle when the 3/10 Treasury slope is between 0 bps and 50 bps (where it stands today), investment grade corporate bonds have delivered annualized excess returns of +3 bps. In contrast, municipal bonds have delivered annualized excess returns of +64 bps (before adjusting for the tax advantage).8 Given strong historical returns during the current phase of the cycle and the fact that our Municipal Health Monitor remains in “improving health” territory (bottom panel), we advocate an overweight allocation to municipal bonds. Treasury Curve: Favor 2/30 Barbell Over 7-Year Bullet Treasury yields rose in February, led by the long-end of the curve. The 2/10 Treasury slope steepened 3 bps on the month and currently sits at 21 bps. The 5/30 slope steepened 1 bp on the month and currently sits at 57 bps. Our 12-month fed funds discounter remains below zero, meaning that the market is priced for rate cuts during the next year (Chart 7). We continue to view rate hikes as more likely than cuts on this time horizon, and therefore recommend yield curve trades that will profit from a move higher in our discounter. In prior research we found that the 5-year and 7-year Treasury maturities are most sensitive to changes in our discounter, so any trade where you sell the 5-year or 7-year bullet and buy a duration-matched barbell consisting of the long and short ends of the curve will provide the appropriate exposure.9 Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

An added benefit of implementing a barbell over bullet strategy in the current environment is that barbells currently offer higher yields than bullets, meaning that you earn positive carry as you wait for the market to price rate hikes back into the curve (bottom 2 panels).10 Not surprisingly, barbell strategies also look attractively valued on our yield curve models, the output of which is found in Appendix B. TIPS: Overweight TIPS outperformed the duration-equivalent nominal Treasury index by 36 basis points in February, bringing year-to-date excess returns up to +120 bps. The 10-year TIPS breakeven inflation rate rose 11 bps on the month and currently sits at 1.96%. The 5-year/5-year forward TIPS breakeven inflation rate rose 7 bps on the month and currently sits at 2.07%. Both rates remain below the 2.3% - 2.5% range that has historically been consistent with inflation expectations that are well-anchored around the Fed’s target. After last month’s increase, the 10-year TIPS breakeven inflation rate is currently very close to the fair value reading from our Adaptive Expectations model (Chart 8).11 This model is based on a combination of backward-looking and forward-looking inflation measures and is premised on the idea that investors’ inflation expectations take time to adjust to changing macro environments. The current fair value reading from the model is 1.97%, but that fair value will trend steadily higher as long as core CPI inflation remains above 1.84%. The 1.84% threshold is the annualized trailing 10-year growth rate in core CPI, and it is the most important variable in the model. Chart 8Inflation Compensation

Inflation Compensation

Inflation Compensation

On that note, core CPI has increased at an annual rate of 2.58% during the past four months, well above the necessary threshold. And while some forward-looking inflation measures have moderated, notably the ISM Prices Paid index (panel 3), this is largely a reaction to the recent drop in energy prices. A drop that should reverse as global growth improves in the coming months. ABS: Neutral Cut To Underweight Asset-Backed Securities outperformed the duration-equivalent Treasury index by 22 basis points in February, bringing year-to-date excess returns up to +38 bps. The index option-adjusted spread for Aaa-rated ABS narrowed 8 bps on the month and currently sits at 31 bps, 3 bps below its pre-crisis low (Chart 9). Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Our excess return Bond Map, shown in Appendix C on page 18, shows that Aaa-rated ABS offer a relatively poor risk/reward trade-off compared to other U.S. bond sectors. Aaa-rated auto loan ABS in particular offer greater risk and lower potential return than the Aggregate Plus index (the Bloomberg Barclays Aggregate index plus high-yield). Tight spreads look even more unattractive when you consider that the delinquency rate for consumer credit is rising, and according to the uptrend in household interest expense, will continue to march higher in the coming quarters (panel 4). Lending standards are also tightening for both credit cards and auto loans, a dynamic that often coincides with a rising delinquency rate and wider ABS spreads (bottom panel). Given the recent spread tightening, we advise investors to reduce consumer ABS exposure in U.S. bond portfolios. Other sectors, such as Agency CMBS, offer a more attractive risk/reward trade-off within high-rated spread product. Non-Agency CMBS: Underweight Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 74 basis points in February, bringing year-to-date excess returns up to +142 bps. The index option-adjusted spread for non-agency Aaa-rated CMBS tightened 13 bps on the month and currently sits at 93 bps, below the average pre-crisis level but somewhat higher than the recent tights (Chart 10). Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

The Fed’s Senior Loan Officer Survey showed that banks tightened lending standards on commercial real estate (CRE) loans in Q4 and witnessed falling demand (bottom 2 panels). This, coupled with decelerating CRE prices paints a relatively negative picture for non-agency CMBS. Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Teasury index by 49 basis points in February, bringing year-to-date excess returns up to +77 bps. The index option-adjusted spread tightened 8 bps on the month and currently sits at 48 bps. The excess return Bond Map in Appendix C shows that Agency CMBS offer high potential return compared to other low-risk spread products. An overweight allocation to this defensive sector continues to make sense. Appendix A - The Golden Rule Of Bond Investing We follow a two-step process to formulate recommendations for bond portfolio duration. First, we determine the change in the federal funds rate that is priced into the yield curve for the next 12 months. Second, we decide – based on our assessments of the economy and Fed policy – whether the change in the fed funds rate will exceed or fall short of what is priced into the curve. Most of the time, a correct answer to this question leads to the appropriate duration call. We call this framework the Golden Rule Of Bond Investing, and we demonstrated its effectiveness in the U.S. Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018, available at usbs.bcaresearch.com. Chart 11 illustrates the Golden Rule’s track record by showing that the Bloomberg Barclays Treasury Master Index tends to outperform cash when rate hikes fall short of 12-month expectations, and vice-versa. At present, the market is priced for 2 basis points of rate cuts during the next 12 months. Given that we expect the Fed to deliver rate hikes in the second half of this year, we recommend that investors maintain below-benchmark portfolio duration. Chart 11The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

We can also use our Golden Rule framework to make 12-month total return forecasts for the Bloomberg Barclays Treasury index under different scenarios for the change in the fed funds rate. To forecast total returns we first calculate the 12-month fed funds rate surprise in each scenario by comparing the assumed change in the fed funds rate to the current value of our 12-month discounter. This rate hike surprise is then mapped to an expected change in the Treasury index yield using a regression based on the historical relationship between those two variables. Finally, we apply the expected change in index yield to the current characteristics (yield, duration and convexity) of the Treasury index to estimate total returns on a 12-month horizon. The below tables present those results, along with 95% confidence intervals.

Image

Image

Appendix B - Butterfly Strategy Valuation The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com U.S. Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of +55 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 55 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As of February 28, 2019)

The Sequence Of Reflation

The Sequence Of Reflation

Table 5Butterfly Strategy Valuation: Standardized Residuals (As of February 28, 2019)

The Sequence Of Reflation

The Sequence Of Reflation

Table 6Discounted Slope Change During Next 6 Months (BPs)

The Sequence Of Reflation

The Sequence Of Reflation

Appendix C - Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the U.S. fixed income market. The Map employs volatility-adjusted breakeven spread analysis to show how likely it is that a given sector will earn/lose money during the subsequent 12 months. The Map does not incorporate any macroeconomic view. The horizontal axis of the Map shows the number of days of average spread widening required for each sector to lose 100 bps versus a position in duration-matched Treasuries. Sectors plotting further to the left require more days of average spread widening and are therefore less likely to see losses. The vertical axis shows the number of days of average spread tightening required for each sector to earn 100 bps in excess of duration-matched Treasuries. Sectors plotting further toward the top require fewer days of spread tightening and are therefore more likely to earn 100 bps of excess return.

Chart 12

Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Jeremie Peloso, Research Analyst jeremiep@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com 2 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2018, available at usbs.bcaresearch.com 3 Please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com 4 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2019, available at usbs.bcaresearch.com 5 Please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 6 Please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 7 Please see Emerging Markets Strategy Weekly Report, “Dissecting China’s Stimulus”, dated January 17, 2019, available at ems.bcaresearch.com 8 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2018, available at usbs.bcaresearch.com 9 Please see U.S. Bond Strategy Weekly Report, “Don’t Position For Curve Inversion”, dated January 22, 2019, available at usbs.bcaresearch.com 10 Please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com 11 Please see U.S. Bond Strategy Weekly Report, “Adaptive Expectations In The TIPS Market”, dated November 20, 2018 available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

CHART 7

CHART 7

Neutral We have successfully ridden down the S&P 1500 components index on a structural basis over the past four years. But now, factors are falling into place for an end to this multi-year bloodbath. On Monday, we lifted exposure to neutral from underweight, locking in relative gains of 36% since inception. In the U.S., light vehicle sales have been stable over the past five years and the latest Conference Board consumer confidence release showed that consumers’ plans to purchase a car remain upbeat, and could serve as a catalyst to unlock excellent relative value (middle panel). With regard to President Trump’s hawkish tariff rhetoric and the ongoing U.S./China trade tussle, automobile components makers have taken a big hit. But, there are high odds of an end to the U.S./China trade dispute. Tack on a softening greenback courtesy of a more dovish Fed. U.S. auto components producers will likely grab a larger slice of the global auto parts revenue pie (top panel). Still a number of risks keep us from turning outright bullish on this consumer discretionary subsector, including auto loan delinquencies which are increasing rapidly, approaching last cycle’s peak (bottom panel). Bottom Line: The easy money has already been made by shying away from auto component manufacturers and we lifted the S&P 1500 auto components index to neutral; please see Monday’s Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S15AUTC – APTV, BWA, GNTX, GT, DAN, VC, FOXF, DORM, LCII, DJPH, AXL, ADNT, CTB, THRM, GTX, SMP, CPS, MPAA, SUP.

Highlights Portfolio Strategy While equities will likely be higher in the coming 9-12 months, we would refrain from committing fresh capital to the market at this juncture. A better entry point lies ahead. Tactically, this market needs a breather to digest the V-shaped formation since last December’s G20 meeting before it resumes its bull run. Firming leading indicators of global auto sales, upbeat auto components industry operating metrics, a softening U.S. dollar, the looming truce in the U.S./China trade spat and depressed relative technicals and valuations all suggest that it no longer pays to be bearish the S&P 1500 auto components index. Augment positions to neutral. The global economic soft patch that is exerting downward pressure on real interest rates, a soft U.S. dollar and rising global policy uncertainty, all signal that it still makes sense to hold a global gold mining equity portfolio hedge. Recent Changes Lift the S&P 1500 auto components index to neutral and cement gains of 36% today. From a portfolio management perspective, downgrade the S&P semi equipment index to neutral for a gain of 16% since the December 17, 2018 inception. Table 1

The Good, The Bad And The Ugly

The Good, The Bad And The Ugly

Feature The S&P 500 hit a trouble spot last week, despite positive news on the U.S./China trade tussle. Clearly, there is an element of “buy the rumor sell the news” in the market as equities have come a long way this year, reversing all of last December’s steep losses. But, the SPX now faces stiff resistance at the most important 2,800 level as we highlighted in recent research.1 Chart 1 shows “The Good”. From a sentiment/technical perspective, fresh all-time highs in the S&P 500 advance/decline line portend ongoing gains in this broad-based equity market advance. The junk bond market sends an equally encouraging signal: The Barclays total return high yield corporate bond index has vaulted to new highs, which bodes well for the SPX (middle panel, Chart 1). Finally, all three of the S&P risk parity total return indexes2 have slingshot into uncharted territory and suggest that the S&P 500 is headed there next. Chart 1The Good…

The Good…

The Good…

Nevertheless, there are some cracks appearing in the U.S. economy. News of an abysmal retail sales report was quickly discredited by pundits, with some blaming poor data collection due to the government shutdown. Chart 2 shows “The Bad”. Worrisomely, contracting intermodal rail carloads and a nosedive in the “First Data merchant services dollar spend” at retailers likely corroborate the Commerce Department’s weak retail sales data. Moreover, the recent plunge in the Goldman Sachs MAP (Macro-data Assessment Platform) Surprise Index, which is now probing a three year low, suggests that the U.S. economy is in a soft-patch. Chart 2…The Bad…

…The Bad…

…The Bad…

Charts 3 & 4 show “The Ugly”. Our Economic Impulse Indicator (EII) first introduced last October,3 has taken a turn for the worse. Six economic indicators encapsulating the U.S. economy comprise the EII, and there is clear deterioration in economic activity on a second derivative basis. The recent contraction in the overall business (manufacturing, wholesale and retail) sales-to-inventories (SI) ratio also warns of profit trouble in the coming quarters (Chart 4). Keep in mind that this data series only goes to November 2018 and once it gets updated to include December later this week, the SI ratio will likely fall deeper into the contraction zone. Chart 3…And The…

…And The…

…And The…

Chart 4…Ugly

…Ugly

…Ugly

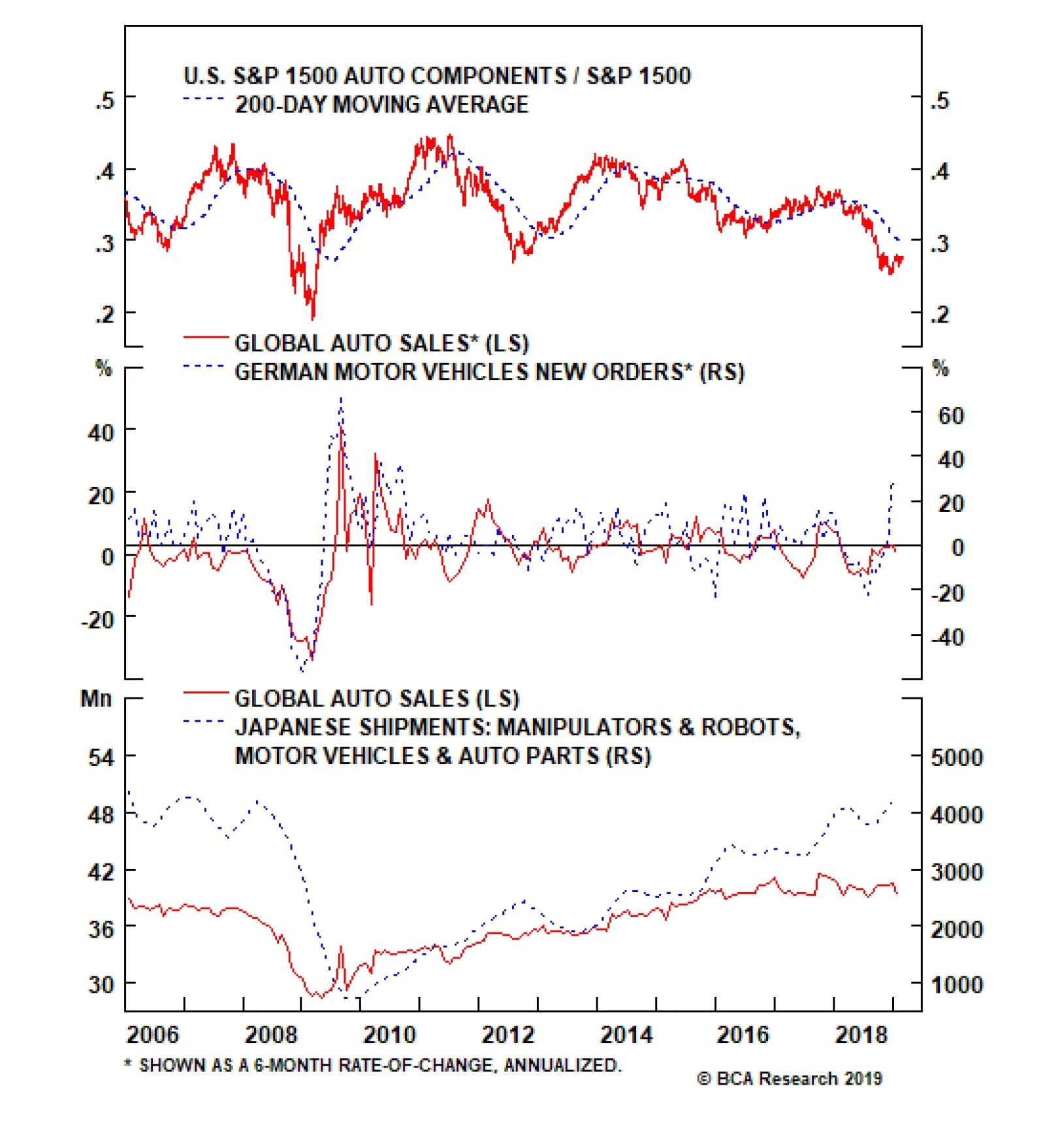

So should investors take some chips off the table given this macro backdrop? Prior to answering the question, as a reminder, BCA’s view remains that the business cycle is alive and well and there is no recession on a cyclical time horizon. Therefore, equities should be higher in the coming 9-12 months. Our end-2019 SPX target remains at 3,000 based on $181 EPS for calendar year 2020 assuming a 16.5 multiple.4 Nevertheless from a shorter-term perspective, we would refrain from committing fresh capital to this market, as we believe a better entry point lies ahead. Tactically, this market now needs a breather to digest the V-shaped formation since last December’s G20 meeting, before it resumes its bull run. In addition, we would book gains on any alpha generating tactical trades; today we crystalize 16% gains in the S&P semi equipment tactical overweight position since the December 17, 2018 inception and downgrade to neutral. This week, we book handsome profits on a long-held underweight in a consumer discretionary subindex that Trump’s hawkish tariff rhetoric and actions have badly wounded. We also update a materials subsector that benefits from the ongoing global reflationary impulse. Auto Components: Aiming For Pole Position? We have successfully ridden down the S&P 1500 components index on a structural basis over the past four years. But now, factors are falling into place for an end to this multi-year bloodbath. We are lifting exposure to neutral from underweight, locking in relative gains of 36% since inception. Global auto sales are the main driver of auto components profits, thus identifying where we stand in the global auto sales cycle is key. Bellwether German automakers have been caught in an emissions-related downdraft with “Dieselgate” weighing heavily on this sector when new emissions-test procedures were implemented last quarter. The top panel of Chart 5 shows that the worst is likely behind this drubbing in German automobile production as new orders have recently gone vertical. Backlogs are also sky-high and suggest that a definitive turn looms in German motor vehicle output. The upshot is that global auto sales may come out of their recent funk. Chart 5Global Auto Sales Are About To Turn

Global Auto Sales Are About To Turn

Global Auto Sales Are About To Turn

The Japanese car industry, the other global heavyweight, also suffered a minor setback last year, but leading indicators of Japanese auto production are also ticking higher. Japanese industrial robot shipments are at fresh cyclical highs and signal that global auto sales will hook up (bottom panel, Chart 5). In the U.S., light vehicle sales have been stable over the past five years, but auto industrial production growth has been roaring, rising 40 percentage points from the manufacturing recession trough (second panel, Chart 6). Chart 6Improving…

Improving…

Improving…

All of this paints a brightening backdrop for U.S. auto components manufacturers. Indeed, auto components new orders are at all-time highs (middle panel, Chart 7), at a time when inventories remain tame. In fact the new orders-to-inventories ratio sits squarely above one and continues to firm, with unfilled orders also at all-time highs (Chart 8). As a result, selling prices are accelerating at a healthy clip (third panel, Chart 6). The upshot is that industry profits will likely overwhelm. Chart 7…Operating…

…Operating…

…Operating…

Chart 8...Auto Component Metrics

...Auto Component Metrics

...Auto Component Metrics

On the domestic demand front, the latest Conference Board consumer confidence release showed that consumers’ plans to purchase a car remain upbeat, and could serve as a catalyst to unlock excellent relative value (bottom panel, Chart 7). With regard to President Trump’s hawkish tariff rhetoric and the ongoing U.S./China trade tussle, automobile components makers have taken a big hit. But, there are high odds of an end to the U.S./China trade dispute. Tack on a softening greenback courtesy of a more dovish Fed. U.S. auto components producers will likely grab a larger slice of the global auto parts revenue pie (top panel, Chart 7). Despite these tailwinds, investors have relentlessly avoided auto component stocks. Technicals remain washed out and industry valuations are a small fraction of the broad market and below the historical mean as per the relative price-to-sales ratio (Chart 9). Chart 9Cheap And Oversold…

Cheap And Oversold…

Cheap And Oversold…

Nevertheless, we refrain from turning outright bullish on this consumer discretionary subsector given the following risks: First, auto loan delinquencies are increasing rapidly, approaching last cycle’s peak. Second, car financing interest rates are still rising, which, at the margin, dents demand for new car sales. Third, auto credit growth is decelerating and demand for auto loans is also anemic according to the Fed’s latest Senior Loan Officer survey (Chart 10). This stands in marked contrast to the aforementioned Conference Board’s survey of consumers’ plans to buy a car. Finally, were President Trump to proceed with auto tariffs on European car manufacturers once he strikes a deal with China, U.S. auto parts producers will suffer a setback. Chart 10…But There Are Some Risks

…But There Are Some Risks

…But There Are Some Risks

Netting it all out, the easy money has already been made by shying away from auto component manufacturers. Firming leading indicators of global auto sales, upbeat auto components industry operating metrics, a softening U.S. dollar, the looming truce in the U.S./China trade spat and depressed relative technicals and valuations all suggest that it no longer pays to be bearish the S&P 1500 auto components index. Bottom Line: Lift the S&P 1500 auto components index to neutral and crystalize gains of 36% today. The ticker symbols for the stocks in this index are: BLBG: S15AUTC – APTV, BWA, GNTX, GT, DAN, VC, FOXF, DORM, LCII, DJPH, AXL, ADNT, CTB, THRM, GTX, SMP, CPS, MPAA, SUP. A Modest Gold Portfolio Hedge Still Makes Sense Within our broad-based U.S. equity sector and subsector coverage, we continue to recommend a modest gold-related hedge via being overweight the global gold mining index (given that the S&P gold index only comprises a single stock) versus the MSCI All-Country World Index, expressed through the long GDX:US/short ACWI:US exchange traded funds. There is compelling evidence that gold bullion is a reliable reflationary gauge. The shiny metal troughed in mid-August, leading even the JP Morgan EM FX index. Since then, it has been in an uninterrupted run rising over $180/oz. or 15% and sniffing out a reflationary impulse. Not only is there a tight inverse correlation with the trade-weighted U.S. dollar, but over the past three years the Chinese renminbi also moves in close lockstep with gold (Chart 11). Now that Chinese policymakers have opened the credit spigots (January credit data revealed the largest ever month-over-month loan increase in the history of the data, please refer to the second panel of Chart 2 in last week’s publication)5 reflating their economy, there are high odds that gold can break out of its past five year trading range in a bullish fashion. Chart 11Gold Is Sniffing Out A Reflationary Impulse

Gold Is Sniffing Out A Reflationary Impulse

Gold Is Sniffing Out A Reflationary Impulse

Commodity sentiment and positioning data suggest that gold’s run up will prove durable and continue to underpin the relative share price ratio (second & third panels, Chart 12). Chart 12Bullish Bullion Positioning Underpins Global Gold Miners

Bullish Bullion Positioning Underpins Global Gold Miners

Bullish Bullion Positioning Underpins Global Gold Miners

Importantly, the precious metals industry has not stood still. It has embarked on a massive consolidation phase and the recent spike in M&A activity in global gold miners signals that there is more upside for relative share prices (top panel, Chart 12). But the good news does not stop there. Globally there is a slowdown that has infected a number of economies and BCA’s calculated Global ZEW economic sentiment index has lit a fire under gold mining stocks (Global ZEW shown inverted, second panel, Chart 13). The longer the global soft-patch lasts the longer Central Banks will remain on the sidelines or even ease monetary policy in order to rekindle growth. This macro backdrop represents fertile ground for gold and gold related equities (bottom panel, Chart 14). Chart 13Rising Uncertainty, Global Growth Softpatch And…

Rising Uncertainty, Global Growth Softpatch And…

Rising Uncertainty, Global Growth Softpatch And…

Chart 14…Falling Real Rates Are Excellent Gold Mining Supports

…Falling Real Rates Are Excellent Gold Mining Supports

…Falling Real Rates Are Excellent Gold Mining Supports

Keep in mind that gold bullion yields zero and the gold mining equities’ dividend yield trails the broad market by 100bps; thus, there is an opportunity cost to holding gold and gold related equities, especially now that even U.S. cash yields 2.5%. This explains the inverse correlation with real interest rates and the recent 30bps fall in the U.S. 10-year TIPS yield reinforces gold bullion and the relative share price ratio (TIPS yield shown inverted, middle panel, Chart 14). Moreover, the global policy uncertainty index is perking up given the ongoing U.S./China trade tussle (top panel, Chart 13), recent news of a no deal between the U.S. and North Korea and looming Brexit deadline. All of this underpins global gold stocks (top panel, Chart 13). Tack on the recent fear that gripped markets, and skyrocketing equity risk premia, and the ingredients are in place for additional gains in the relative share price ratio (third panel, Chart 13). While some semblance of normality has returned to global bourses year-to-date, fixed income investors do not share the euphoria their equity peers are emitting. Such a dichotomy favors global gold mining stocks. Finally, with regard to relative valuations and technicals, global gold equities remain in undervalued territory, but have recently recovered smartly from deeply oversold conditions (Chart 15). Chart 15Valuations Ready To Shine

Valuations Ready To Shine

Valuations Ready To Shine

In sum, gold bullion is sniffing out a reflationary impulse that is bullish for global gold mining equities. The global economic soft patch that is exerting downward pressure on real interest rates, a soft U.S. dollar and rising global policy uncertainty, all signal that it still makes sense to hold a global gold mining equity portfolio hedge. Bottom Line: Stay overweight the global gold miners index (long GDX:US/short ACWI:US), and remove the downgrade alert. Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA U.S. Equity Strategy Weekly Report, “Trader’s Paradise” dated January 28, 2019,available at uses.bcaresearch.com. 2 https://us.spindices.com/documents/methodologies/methodology-sp-risk-parity-indices.pdf?force_download=true 3 Please see BCA U.S. Equity Strategy Report, “Icarus Moment” dated October 22, 2018, available at uses.bcaresearch.com. 4 Please see BCA U.S. Equity Strategy Report, “Catharsis” dated January 14, 2019, available at uses.bcaresearch.com. 5 Please see BCA U.S. Equity Strategy Report, “Reflationary Or Recessionary” dated February 25, 2019, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

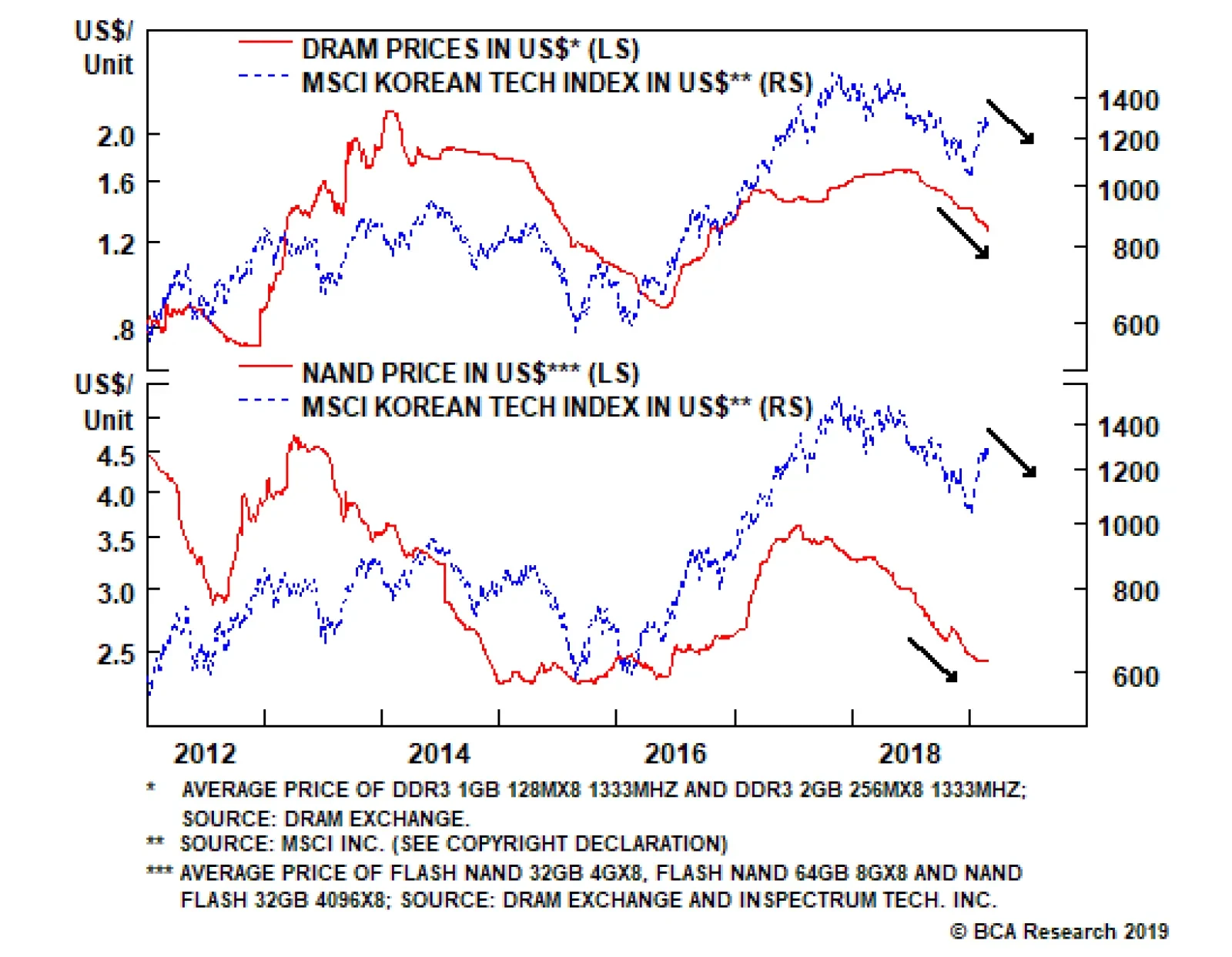

Korea’s dependence on the semiconductor sector has risen considerably in the past several years: Semiconductor exports have risen from under 10% to slightly above 20% of total goods exports. On the demand front, memory demand from the global smartphone…

Feature The GAA DM Equity Country Allocation model is updated as of February 28, 2019. The quant model increased allocations to Spain, Italy, Sweden and Germany at the expense of the U.S., the Netherlands and Switzerland. As such, now the model underweights the U.S., Japan, the U.K, France, Canada (downgraded from overweight) and Australia, while overweighting Germany, Spain, Italy, Switzerland and Sweden (upgraded from underweight), as shown in Table 1. Table 1Model Allocation Vs. Benchmark Weights

GAA Quant Model Updates

GAA Quant Model Updates

As shown in Table 2 and Charts 1, 2 and 3, the overall model outperformed the MSCI World benchmark by 18 bps in February, with a 54 bps of outperformance from the Level 2 model offset by a 9 bps of underperformance from Level 1. Since going live, the overall model has outperformed by 148 bps, with Level 2 outperforming by 267 bps and Level 1 outperforming by 29 bps. Table 2Performance (Total Returns In USD %)

GAA Quant Model Updates

GAA Quant Model Updates

Chart 1GAA DM Model Vs. MSCI World

GAA DM Model Vs. MSCI World

GAA DM Model Vs. MSCI World

Chart 2GAA U.S. Vs. Non U.S. Model (Level 1)

GAA U.S. Vs. Non U.S. Model (Level 1)

GAA U.S. Vs. Non U.S. Model (Level 1)

Chart 3GAA Non U.S. Model (Level 2)

GAA Non U.S. Model (Level 2)

GAA Non U.S. Model (Level 2)

Please see also the website http://gaa.bcaresearch.com/trades/allocation_performance. For more details on the models, please see Special Report, “Global Equity Allocation: Introducing The Developed Markets Country Allocation Model,” dated January 29, 2016, available at https://gaa.bcaresearch.com. Please note that the overall country and sector recommendations published in our Monthly Portfolio Update and Quarterly Portfolio Outlook use the results of these quantitative models as one input, but do not stick slavishly to them. We believe that models are a useful check, but structural changes and unquantifiable factors need to be considered too in making overall recommendations. GAA Equity Sector Selection Model We are happy to reintroduce the GAA Equity Sector Selection model after we suspended it as of October 2018 following the GICS adjustments to global sector composition. As noted in our September 2018 Special Alert and October 2018 Quarterly, the most notable changes occurred in the new Communication Services sector (previously known as Telecommunication Services) and the Information Technology sector, whereas the Consumer Discretionary sector had various yet insubstantial movements in and out of the sector. Having received historical performance of the revised data, we have retested and adjusted various inputs in the model to match the cyclicality of the revised sectors. We were able to backtest the model to only June 2008 as this was the starting point of the revised data. Given the nature of firms that are now included in the global Communication Services sector, we revised our classification of this sector from a defensive to a cyclical. Hence, it will be positively impacted by the model’s growth component. Furthermore, we have introduced Real Estate as its own sector (following its removal from Financials in August 2016). Additionally, we have neutralized the impact of the liquidity component on the Real Estate sector; in other terms, we found no evidence that the Fed cycle affects this sector in any of its four phases. We also revised the valuations component by shortening the confirming signal of our technical indicator from a 12-month to a 6-month moving average. To properly assess the model’s adjusted performance, we have reset the “since going live date” to begin in March 2019. However, the historical backtested performance of the model will still be shown in Chart 4. Additionally, we show the old model’s performance vs. its benchmark (Table 3). Chart 4Overall Model Performance

Overall Model Performance

Overall Model Performance

Given the above, and following our Monthly Update that was released yesterday, the model corroborates our slightly cyclical stance by overweighting Industrials and Materials (Table 4). Additionally, the model’s biggest underweight shift from last month was on Consumer Staples as the momentum indicator significantly deteriorated. The model is overweight Utilities due to positive inputs from its momentum and liquidity components. Table 3Old Model’s Performance

GAA Quant Model Updates

GAA Quant Model Updates

Table 4Current Model Allocations

GAA Quant Model Updates

GAA Quant Model Updates

For more details on the model, please see the Special Report “Introducing The GAA Equity Sector Selection Model,” dated July 27, 2016, available at https://gaa.bcaresearch.com. Xiaoli Tang, Associate Vice President xiaoliT@bcaresearch.com Amr Hanafy, Research Associate amrh@bcaresearch.com

The Chip Cycle Is Turning

The Chip Cycle Is Turning

Neutral There are high odds that the chip cycle will soon take a turn for the better. Global chip sales have been decelerating for 17 months and are now on the cusp of contraction (middle panel). Over the past two decades, steep contractions have been associated with recession. Given that BCA’s view does not call for recession this year, it is highly unlikely for global semi sales to suffer a major setback. While we do not rule out a brief and shallow dip below zero similar to the 2011/12 and 2015/16 parallels, leading indicators of global semi sales suggest that a trough is near. Namely, BCA’s Global Leading Economic Indicator (GLEI) diffusion index is in a V-shaped recovery signaling that global growth is close to a nadir (middle panel). Similarly the U.S. dollar is decelerating which is a boon to global growth and conducive to higher global chip sales (trade-weighted U.S. dollar shown inverted, bottom panel). Bottom Line: In Monday’s Weekly Report, we lifted the S&P semiconductors index to neutral and added it to our upgrade watch list; we are looking for an opportunity to boost to overweight on a pullback, stay tuned. Finally, from a risk management perspective we increased our trailing stop to 15% in our tactical overweight in the S&P semi equipment index, in order to protect gains. The ticker symbols for the stocks in the S&P semiconductors index are: BLBG: S5SECO – INTC, AVGO, TXN, NVDA, QCOM, MU, ADI, XLNX, AMD, MCHP, MXIM, SWKS, QRVO.

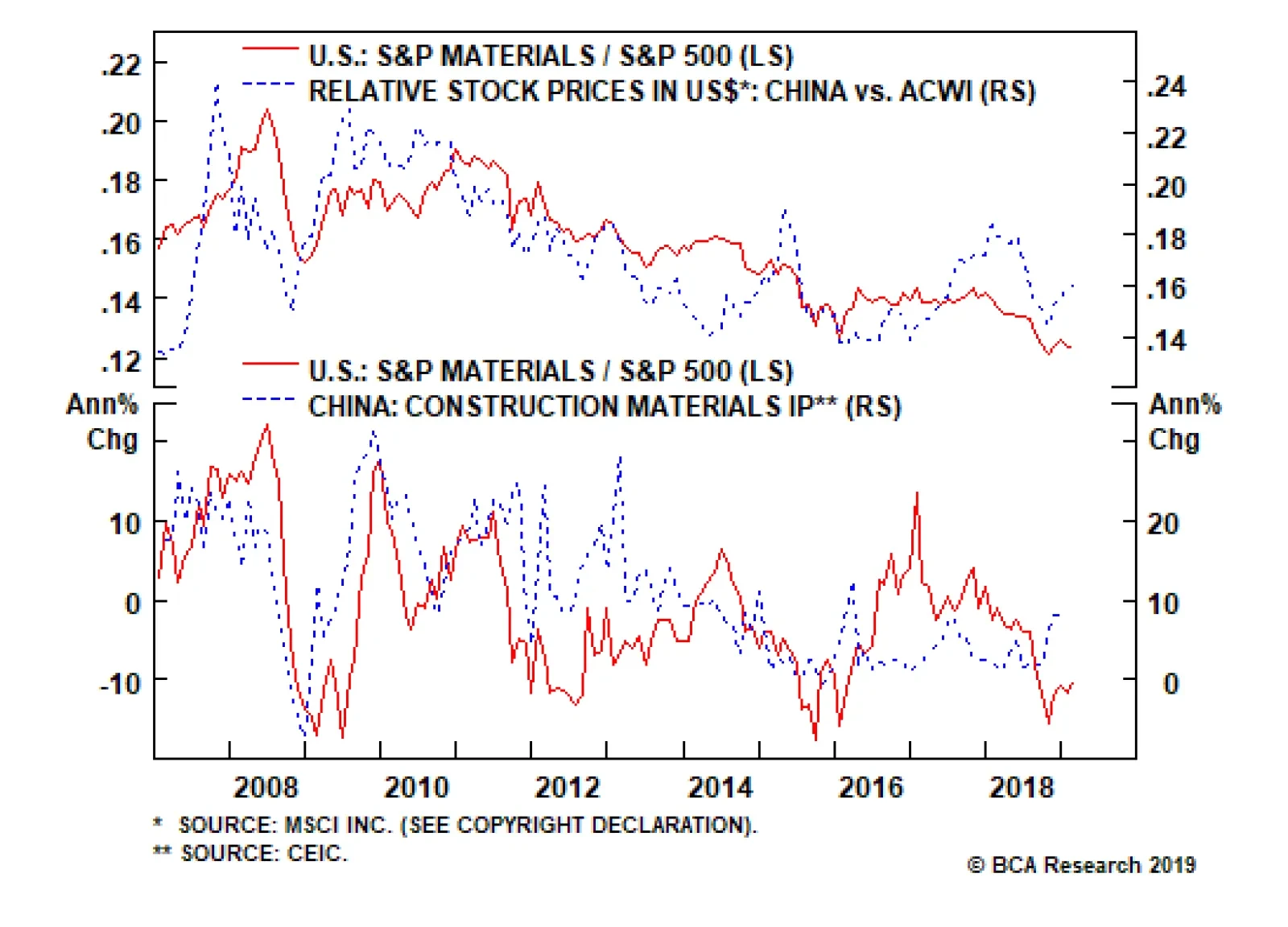

The U.S. Equity Strategy team recently upgraded the S&P materials index to overweight via boosting the steel index to an above benchmark allocation and subsequently they also put on a market-neutral trade: long materials / short utilities. They are…

Highlights The global shipping-fuels market will tighten as UN-mandated fuel standards kick in next year. This will keep ship fuels, known as bunkers, and other distillate prices – e.g., diesel and jet fuel – elevated relative to other refined products like gasoline. In turn, this will boost demand for lighter, sweeter crudes – particularly Brent and similar grades – that allow refiners to raise distillate yields, as they scramble to meet higher demand for low-sulfur ship-fuel next year. After pipeline expansions in the Permian Basin come on line later this year, WTI exports should provide the marginal light-sweet barrel refiners will need to raise distillate output next year. Light-sweet exports from the U.S. will find a ready home in the Atlantic Basin and Asia, as demand for shipping fuels – along with other distillates– rises. Still, the ramp in WTI exports from the U.S. will be hampered by a lack of deep-water ports that can accommodate very large crude carriers (VLCCs) used to ship crude oil globally. As a result, we expect the light-sweet crude market ex-U.S. to tighten. Given this expectation, we are extending our long July 2019 Brent vs. short July 2020 Brent recommendation – up 240.2% since inception January 3 – to long 2H19 Brent vs. short 2H20 Brent. Highlights Energy: Overweight. In line with our expectation, OPEC is showing no sign of agreeing to raise production less than two months after initiating output cuts to drain inventories. Separately, Muhammadu Buhari was re-elected for a second four-year term as Nigeria’s president. The main opposition party rejected the results, following record-low voter turnout, after elections were unexpectedly delayed by one week, according to the BBC. Base Metals/Bulks: Neutral. The prompt March copper contract on the CME’s COMEX is attempting to fill a gap just above $2.95/lb, which opened in July 2018 as U.S. – China trade tensions rose. Positive signals from Sino – U.S. trade talks are supporting prices. Precious Metals: Neutral. Palladium traded to a record high of $1,536.50/oz Monday, pushing it more than $200/oz over gold. Platinum prices also rallied, as South African miners were notified by labor unions of intended strikes next week. Russia’s leading producer, Norilsk Nickel, which accounts for 40% of global palladium production, expects an 800k-ounce physical deficit in 2019, according to Reuters. Ags/Softs: Underweight. U.S. President Donald Trump said he would delay increasing U.S. tariffs on Chinese imports. Trump also said he expects to meet China’s President Xi Jinping to conclude the trade deal they’ve been negotiating if both sides continue to make progress. Feature Maritime shipping represents ~ 80% of international trade, and is responsible for roughly 90% of the total sulfur emissions from the transportation sector. In 2008, the UN’s International Maritime Organization (IMO) adopted a new regulation to reduce the cap for sulfur content of ships’ fuel oil – known as bunker fuel – to 3.5% from 4.5% in 2012, and to 0.5% from 3.5% in 2020 (Chart 1).1 Chart of the WeekReducing Marine Sulfur Pollution Requires Higher-Priced Low-Sulfur Fuels

Reducing Marine Sulfur Pollution Requires Higher-Priced Low-Sulfur Fuels

Reducing Marine Sulfur Pollution Requires Higher-Priced Low-Sulfur Fuels

Around 50% of the cost of shipping is fuel costs. This amounts to more than 4mm b/d of bunker fuel (~ 3.5mm b/d of High-Sulfur Fuel Oil, or HSFO, and ~ 0.8mm b/d of marine gasoil, known as MGO). Hence, the IMO 2020 regs threaten demand of ~ 3.5mm b/d of HSFO. As the January 1, 2020, IMO deadline approaches, uncertainty surrounding the new regs remains elevated. On the demand side, shippers have the option to install abatement technology (i.e., scrubbers); burn IMO 2020-compliant fuels like MGO; use liquefied natural gas (LNG) as a fuel on ships; or do nothing, i.e., not comply with the regulation. Refiners on the supply side have to adjust via a combination of increasing MGO and Low-Sulfur Fuel Oil (LSFO) production; modifying their crude slates, which will favor lighter, sweeter crudes like Brent and WTI; building additional refining capacity; or running their units harder – i.e., increase refinery utilization rates – to produce more fuel. Demand for bunkers is the only part of the HSFO market that is growing. IMO 2020 removes the all-important shipping consumer of residual fuel oil, which will have a major impact on simple refineries, and will force a dramatic reconfiguration of the shipping and refining industries. To date, shippers and refiners have been slow to implement required changes as market participants have an incentive to move last.2 We agree with a recent McKinsey analysis, which notes the simplest solution for shippers is to switch to MGO.3 We also could see an uptick in demand for LSFO with sulfur content below the 0.5% limit for blending purposes. This would push demand for the lower-sulfur fuels and prices up. It also would pressure HSFO prices lower over the short term, to the point where this fuel can compete in the utility sector as a fuel, or in the refining sector as a charging stock for complex refiners. The IEA expects MGO consumption to rise from 0.8mm b/d to 1.7mm b/d in 2020.4 Complex Refiners, Light-Sweet Crude Producers Benefit Moving to LSFO and MGO shifts the burden of IMO 2020 to the refining market. According to the IEA, around 80% of the sulfur content in crude is removed from the final product. Once IMO 2020 is implemented, this will rise to 90%. In the lead-up to the IMO 2020 deadline, refiners are adjusting their crude slates to minimize residual fuel and maximize distillate output. As a result, demand for light-sweet crudes like Brent and WTI – the crude being produced in ever-rising quantities in the U.S. shales – will increase. At the same time, heavier crudes exported by Venezuela and GCC states will see demand fall, which means the spread between these crudes will favor the lighter, sweeter barrel, all else equal.5 Simple refineries incapable of cracking the complex heavy-sour crudes favored by U.S. Gulf Coast refiners will either have to upgrade, close, or use low-sulfur crude as a charging-stock input. According to McKinsey, the switch to marine gasoil will lead to an increase of 1.5mm b/d of distillate demand. This represents ~ 2.2 to 2.7mm b/d of increased demand for light-sweet oil. The IEA estimates diesel prices could rise by 20 – 30%, as a result.6 This increased demand for low-sulfur bunkers – MGO in particular –will keep prices for distillates generally well supported over the next year or so at the expense of HSFO. S&P Global Platts reported this week the first physical trade for U.S. Gulf Coast 0.5% MGO was done in its official trading window at $67.70/bbl, a $3.75/bbl premium to HSFO.7 IMO 2020 will keep distillates the star performers for refiners. Distillate crack spreads – most visible in the ultra-low-sulfur diesel (ULSD) cracks employing the CME’s NY Harbor ULSD futures vs. WTI and Brent – recently were trading $16/bbl over gasoline cracks using the Exchange’s RBOB futures (Charts 2A and 2B). We expect these cracks to remain wide, to incentivize more distillate-production capacity. Chart 2ABrent Diesel And Gasoline Cracks Likely Trade > $14/bbl Wide

Brent Diesel and Gasoline Cracks Likely Trade Greater Than $14/bbl Wide

Brent Diesel and Gasoline Cracks Likely Trade Greater Than $14/bbl Wide

Chart 2BBrent Diesel Cracks Will Remain Elevated Following IMO 2020

Brent Diesel Cracks Will Remain Elevated Following IMO 2020

Brent Diesel Cracks Will Remain Elevated Following IMO 2020

Prices for other distillates also will be supported by IMO 2020 – e.g., jet fuel – over the coming year, given the high correlation of products within this cut of the barrel. These distillate prices also are highly correlated with Brent and WTI prices, as can be seen in Chart 3, and in Tables 1 and 2. These high correlations likely will persist as IMO 2020 is implemented, and hedgers seek out liquid markets in which to shed their price risk.8 Chart 3Global Distillate Prices Will Be Supported by IMO 2020

Global Distillate Prices Will Be Supported by IMO 2020

Global Distillate Prices Will Be Supported by IMO 2020

Table 1Distillate Fuels’ Correlations Remain High Around The World

IMO 2020: The Greening Of The Ship-Fuel Market

IMO 2020: The Greening Of The Ship-Fuel Market

Table 2Percent Changes In Distillates Also Are Highly Correlated

IMO 2020: The Greening Of The Ship-Fuel Market

IMO 2020: The Greening Of The Ship-Fuel Market

Baker & O’Brien, an energy consultancy based in Dallas, Texas, expects a number of factors – ranging from non-compliance with IMO 2020; increased use of scrubbers to capture sulfur-oxide emissions; blending to make IMO 2020-compliant marine fuel; upgrades by refiners and changes in their crude slates – will lead to lower prices once the market adjusts to the new regs.9 We do not disagree, but the timing on this likely hinges on how quickly U.S. light-sweet crude oil exports ramp up. Investment Implications WTI exports – actually LTO exports from U.S. shales – will provide the marginal light-sweet barrel refiners will need to raise distillate output next year. As a result, LTO exports from the U.S. will find a ready home in the Atlantic Basin and Asia, as demand for low-sulfur shipping fuels increases. However, this will not happen overnight. At present WTI exports from the U.S. are hampered by a lack of deep-water ports that can accommodate the VLCCs used to ship crude oil. The 2mm b/d of expanded pipeline capacity out of the Permian by the end of this year will move the U.S. crude-oil bottleneck from the Permian to the U.S. Gulf.10 So, as refiners prepare this year for the IMO 2020 regs effective January 1, 2020, the light-sweet crude market ex-U.S. – particularly Brent– will tighten. This already is visible in the backwardation we were expecting at the beginning of this year, when we recommended getting long July 2019 Brent vs. short July 2020 Brent, which is up 240.2% since inception on January 3. Given our expectation for a tighter light-sweet crude market ex-U.S., we are liquidating our existing Brent 2019 long position vs. a short position in July 2020 at tonight’s close, and replacing it with a long 2H19 Brent vs. a short 2H20 Brent position.11 Bottom Line: The implementation of IMO 2020 will tighten marine fuels markets globally, as refiners increase their demand for light-sweet crude oil and shippers most likely increase their demand for MGO and lower-sulfur fuels generally. Robert P. Ryan, Senior Vice President Commodity & Energy Strategy rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Footnotes 1 The regulation is part of Annex VI to the International Convention for the Prevention of Pollution from Ships (MARPOL). Following the adoption of the regulation in 2008, a provision was kept in order to review the compliant fuel availability and possibly push the implementation to 2025. In October 2016, the IMO’s Marine Environment Protection Committee confirmed the final implementation date (January 1, 2020) following a positive assessment of the availability for shippers of compliant fuels. Any amendment to MARPOL needs to be circulated for a minimum of six months, and can only be implemented 16 months after adoption, therefore, no legal amendment to the current January 2020 date are possible. Please see https://www.iea.org/etp/tracking2017/internationalshipping/ 2 The slow response by refiners can be explained by: (1) the fact that a switch to LSFO or MGO prior to the actual deadline would lead to a financial loss due to the current high price of LSFO and MGO vs. HSFO; (2) abatement technology requires large upfront investments (i.e. capital cost of new processing units, storage tanks, loss of revenue from laying ships in dry dock while they are retrofitted, and a permanent loss of deck space and loading capacity to the new equipment); and (3) the unpredictability of fuel prices and the endogenous relationship between other shippers and the behavior of prices. In other words, trying to get out in front of the official implementation of IMO 2020 leads to unnecessary financial burdens and to competitive disadvantage. Please see Halff, Antoine, Lara Younes, Tim Boersma (2019), “The Likely Implications of the new IMO standards on the shipping industry.” Energy Policy, 126: 277 - 286. 3 Please see “IMO 2020 and the outlook for marine fuels,” published by McKinsey & Company, September 2018. S&P Global Platts reaches a similar conclusion in a report entitled “Turning tides, the future of fuel oil after IMO 2020,” which was released this month. Platts notes, “The IMO’s lower sulphur cap is set to take away the bulk of marine fuel oil demand from the start of next year. Most ship owners and operators will switch to burning new low-sulfur bunker blends, translating into an almost overnight shift of 3 million b/d of demand.” 4 The IEA expects 30% of the current HSFO bunker demand will switch to marine gasoil (MGO), 30% of the HSFO bunker demand will switch to the new ultra low 0.5% sulphur fuel (ULSFO), and 40% of HSFO bunker demand will remain.) In the IEA’s modeling, this could push prices up by as much as 30%. Please see “Oil 2018: Analysis and forecasts to 2023” published by the IEA. It is available at iea.org 5 Please see “IMO 2020 and the Brent – Dubai Spread,” published by The Oxford Institute For Energy Studies in September 2018. Of course, reducing the export of heavy-sour crudes, as has been done by the Gulf Arab members of OPEC will keep the Brent – Dubai spread tighter than pure economics would dictate. 6 Please see sources in footnotes 3 and 4. 7 This trade was done in the Platts Market on Close assessment. Please see “USGC Marine Fuel 0.5% has first physical trade in Platts MOC process,” published by S&P Global Platts February 26, 2019. 8 These are short-term correlations, which use daily data from 2017 to now. We present correlations in levels and in percent-changes, given these are cointegrated variables. Please see section 3.3 of “Correlation, regression, and cointegration of nonstationary economic time series,” by Soren Johansen, published November 6, 2007, by the Center for Research in Econometric Analysis of Time Series at the University of Aarhus. 9 Please see “The Thunder Rolls – IMO 2020 And The Need For Increased Global Oil Refinery Runs (Part 3)” published by Baker & O’Brien, December 11, 2018. 10 An additional 1mm b/d of new takeaway is scheduled for 1H21, following a final investment decision from an Exxon-led group that will move Permian Basin LTO to the U.S. Gulf. This came one day after Exxon FID’d a 250k b/d buildout of its Beaumont refinery in Houston, which will increase capacity by more than 65%, Natural Gas Intelligence reported January 30. 11 Please see EIA’s This Week in Petroleum report titled “Upcoming changes in marine fuel sulfur limits will affect crude oil and petroleum product markets,” published January 16, 2019. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in Summary of Closed Trades

Image

S&P Materials Update - Heed The Chinese Reflationary Message

S&P Materials Update - Heed The Chinese Reflationary Message

Overweight We recently upgraded the S&P materials index to overweight via boosting the steel index to an above benchmark allocation and subsequently we also put on a market-neutral trade: long materials / short utilities; we reiterate all three recent moves. The top panel of the chart shows that Chinese stocks are capturing the reflationary policy trifecta (credit, monetary and fiscal) that the Chinese authorities are instituting and deep cyclical materials stocks will likely be the primary beneficiaries of such efforts. Importantly, Chinese construction materials industrial production (IP) is expanding at an accelerating pace (bottom panel), and is the mirror image of still decelerating overall Chinese IP growth prints. Recovering Chinese demand for construction materials on the back of increasing infrastructure spending underpins the recent firming commodity price backdrop and suggests that S&P materials profits are on a solid footing. Bottom Line: Stay overweight the S&P materials index.