Sectors

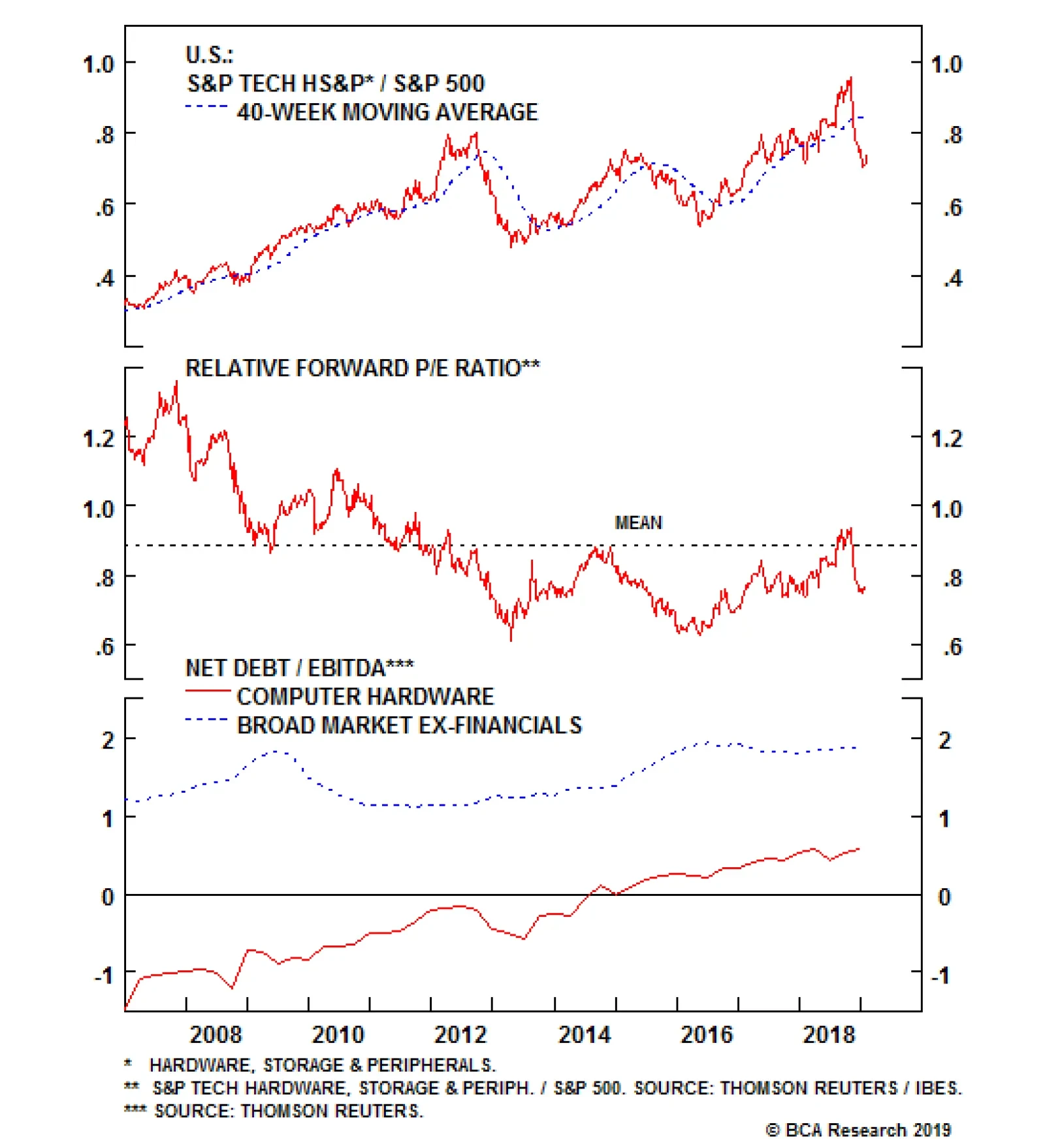

The S&P tech hardware, storage & peripherals (THSP) index bounced yesterday on the back of index heavyweight Apple’s results. While the relatively weak results had long been telegraphed to the market and the upcoming quarter’s guidance was…

Domestic long-term housing prospects remain compelling, especially given that the GFC wrung out all the residential real estate excesses. Currently, household formation is still running higher than housing starts and building permits. Similarly the…

Overweight The S&P tech hardware, storage & peripherals (THSP) index bounced yesterday on the back of index heavyweight Apple’s results. While the relatively weak results had long been telegraphed to the market and the upcoming quarter’s guidance was underwhelming, the company’s stock saw a relief rally based on the absence of a further deterioration in results. Importantly, the index’s valuation continues to trail the broad market by more than 20% (second panel), though dissecting this is significant. Apple’s net cash position is well known by the market which, as of the most recent quarter, stood at more than $27/share. While the overall S&P THSP index has moved to a net debt positive position, the spread versus the broad market ex-financials remains close to 1.5 turns of EBITDA (bottom panel). Adjusting for this would bias the P/E ratio even lower, creating in our view an unreasonable discount. Bottom Line: With the slowdown in China being a known known and resolution of the trade dispute a potential positive catalyst,1 the worst case appears to be priced in to Apple. We reiterate our overweight recommendation for the S&P THSP index and are removing our downgrade alert. The ticker symbols for the stocks in the S&P THSP index are: BLBG: S5CMPE - HPQ, WDC, STX, XRX, AAPL, HPE, NTAP.

Is This The Bottom For Apple

Is This The Bottom For Apple

1 Please see BCA U.S. Equity Strategy Weekly Report, “Trader’s Paradise” dated January 28, 2019, available at uses.bcaresearch.com.

After rising for thousands of years, human intelligence has begun to decline in developed economies. This can be seen in falling IQ scores and a decline in math and science test scores. Environmental factors appear to account for the bulk of this decline, but no one knows what these factors are. If left unchecked, falling intelligence will severely undermine productivity growth. This could lead to lower equity multiples, larger budget deficits, and ultimately, much higher government bond yields. Technological advances, particularly in the genetic realm, promise to radically raise IQs. In a complete abandonment of its one-child policy, China will combine these controversial technologies with pro-natal measures in order to boost sagging birth rates. The coming Eugenic Wars will be one of the most important economic and geopolitical developments of the 21st century. Part 1: What The Tame Fox Says In 1959, a Soviet scientist named Dmitry Belyaev embarked on an ambitious experiment: to domesticate the silver fox. A geneticist by training, Belyaev wanted to replicate the process by which animals such as cats and dogs came to live side-by-side with humans. It was a risky endeavor. The Soviets had essentially banned the study of Mendelian genetics in favor of the blank slate ideology that is popular in progressive circles today. Belyaev persevered. Working under the guise of studying vulpine physiology, he selected foxes based on only one trait – tamability. Less than 10% of foxes made it to the subsequent generation, with the other 90% being sent off to fur farms. By the fourth generation, the changes were undeniable. Rather than fleeing humans, the foxes sought out their attention with no prompting whatsoever. They even wagged their tails and whined and whimpered like dogs do. The tame foxes also displayed physical changes. Their ears flopped over. Their snouts became shorter and their tails stood upright. "By intense selective breeding, we have compressed into a few decades an ancient process that originally unfolded over thousands of years," wrote Lyudmila Trut, who began as Belyaev’s assistant and took over the project when her boss died in 1985. Genetically Capitalist? Evolution can broadly proceed in two ways. The first way is through random mutations. This form of evolution, which scientists sometimes refer to as genetic drift, can take thousands of years to yield any discernable changes. The second way is through natural selection, a process that exploits existing variations in genetic traits. As the Russian fox experiment illustrates, evolution driven by selective pressures (either natural or artificial) can occur fairly quickly. Did selective pressures manifest themselves in human evolution in the lead up to the Industrial Revolution? Did humans, in some sense, domesticate themselves? In his book, A Farewell To Alms, economic historian Gregory Clark argued in the affirmative. Clark documented that members of skilled professions in Medieval England had twice as many surviving children as unskilled workers (Chart II-1). Indeed, the fledgling middle class of the time had even more surviving children than the aristocracy, who were often out fighting wars. As a result, the wages of craftsmen declined by a third relative to laborers between 1200 and 1800, implying that the supply of skilled labor was growing more quickly than the demand for skilled workers over this period. Chart II-1Richer Men Had More Surviving Children In Medieval England

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

In subsequent work, Clark and Neil Cummins argued that the spread of bourgeois values across pre-industrial England was more consistent with a model of genetic transmission than a cultural one (see Box II-1 for details). Similar developments occurred in other parts of the world. For example, in China, the gateway into the bureaucracy for a thousand years was the highly competitive imperial exam. Xi Song, Cameron Campbell, and James Lee showed that high-status men had more surviving children during the eighteenth- and nineteenth-centuries (Chart II-2).1 Chart II-2High-Status Men In China Produced More Descendants In The 18th And 19th Centuries

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The 10,000 Year Explosion Stephen Jay Gould famously said that “There’s been no biological change in humans in 40,000 or 50,000 years. Everything we call culture and civilization we’ve built with the same body and brain.” Gould was wrong. Data from the International HapMap Project show that human evolution accelerated by 100-fold starting around 10,000 years ago (Chart II-3). Chart II-3Human Evolution Has Accelerated 100-Fold Over The Past 10,000 Years

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

In their book The 10,000 Year Explosion: How Civilization Accelerated Human Evolution, Gregory Cochran and the late Henry Harpending explained why evolution sped up so rapidly.2 The advent of agriculture led to a surge in population levels. This, in turn, increased the absolute number of potentially beneficial genetic mutations that could be subject to selection effects. Farming and the rise of city states also completely reshaped the environment in which people lived. Basic biology teaches us that environmental dislocations of this kind tend to generate selective pressures that cause evolution to accelerate. John Hawks, professor of anthropology and genetics at the University of Wisconsin-Madison, put it best: “We are more different genetically from people living 5,000 years ago than they were different from Neanderthals.” Many of the changes to our genomes relate to diet and diseases. The various genetic resistances that people have built up to malaria are all less than 10,000 years old. Mutations to the LCT gene, which confers lactose tolerance into adulthood, occurred independently in three different geographical locations: one in East Asia, one in the Middle East, and one in Africa. The Middle Eastern variant was probably responsible for the rapid enlargement of the Indo-European language group, which now stretches from India to Ireland. The African variant likely facilitated the Bantu expansion, which started near the present-day border of Nigeria and Cameroon, and then spread out across almost all of sub-Saharan Africa. Evolution Of The Human Brain About half of the genes in the human genome regulate some aspect of brain function. Given the rapid acceleration in evolution, it would be rather surprising if our own brains had not been affected. And indeed, there is plenty of evidence that they were. The frontal lobe of the brain has increased in size over the past 10,000 years. This is the part of the brain that regulates such things as language, memory, and long-term planning. Testosterone levels have also declined. That may explain the steady reduction in violent crime rates (Chart II-4). Chart II-4Long-Term Decline In Homicide Rates

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

We know that certain genes that are associated with higher intelligence have been under recent selective pressure. For example, the gene that leads to torsion dystonia – a debilitating movement disorder – appears to have increased in frequency. Why would a gene that causes a known disease become more widespread? The answer is that individuals who have this particular mutation tend to have IQs that are around 10-to 20-points above the population average. Why IQ Matters IQ has a long and contentious history. Yet, despite numerous efforts to jettison the concept, it has endured for one simple reason: It has more predictive power than virtually anything else in the psychological realm. A simple 30-minute IQ test can help predict future educational attainment, job performance, income, health, criminality, and fertility choices (Table II-1 and Chart II-5). IQ even predicts trader performance!3 Table II-1What IQ Predicts (Results From Meta-Analyses)

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Chart II-5IQ Tests Don’t Just Measure How Well You Can Do On An IQ Test

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Like most physiological traits, IQ is highly heritable.4 The genetic contribution to IQ increases from 20% in early childhood to as high as 80% by one’s late teens and remains at that level well into adulthood.5 This makes IQ almost as heritable as height (Chart II-6). Chart II-6The Inheritance You Cannot Renounce

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Although there is a great deal of variation among individuals, on average, more intelligent people earn higher incomes (Chart II-7). If the same relationship existed in the pre-industrial era, as seems likely, then human intelligence probably increased in a way that facilitated the economic explosion that we associate with the Industrial Revolution. The stunning implication is that the emergence of the modern era was a question of “when, not if.” Chart II-7IQ Tends To Be Positively Correlated With Income And Wealth

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Part 2: The Flynn Effect By the late-19th century, it had become clear that the rich were no longer having as many children as the poor. This realization, together with the growing popularity of Darwin’s theories, helped galvanize the eugenics movement. Contrary to popular belief, this movement was not a product of the far-right. In fact, the most vocal proponents of eugenics were among the progressive left. John Maynard Keynes, for example, served as the Director of the British Eugenics Society between 1937 and 1944. Yet, a funny thing happened on the road to idiocracy: The concerns of eugenicists did not come to pass. Rather than becoming dimmer, people became smarter. This phenomenon is now known as the Flynn Effect, named after James Flynn, a psychologist who was among the first to document it. Chart II-8 shows the evolution of IQ scores in a sample of countries between 1940 and 1990. The average country recorded IQ gains of three points per decade over this period, a remarkably large increase over such a relatively short period of time. Chart II-8The Flynn Effect: It Was Nice While It Lasted

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Explaining The Flynn Effect The Flynn Effect must have been entirely driven by environmental factors since genetic factors – namely the tendency of less-educated people to have more children, and to have them at an earlier age – would have reduced average IQs over the past two hundred years. But how could environmental factors have played the dominant role in light of the strong role of genes discussed above? The answer was proposed by geneticist Richard Lewontin in the 1970s. Lewontin suggested imagining a genetically-diverse sack of seed corn randomly distributed between two large identical fields. One field had fertilizer added to it while the other did not. Genetic variation would explain all of the differences in the height of corn stalks within each field, while environmental factors (the addition of fertilizer) would explain all of the difference in the average height of corn stalks between the two fields. This logic explains why genes can account for the bulk of the variation in IQs within any demographic group, while environmental effects may explain most of the variation across groups, as well as why average scores have changed over time. And what environmental effects are these? The truth is that no one really knows. Plenty of theories have been advanced, but so far there is still little consensus on the matter. Bigger, Healthier Brains It has long been known that learning increases the amount of grey matter in the brain. For example, a recent study showed that the hippocampi of London taxi drivers tend to be larger due to the need for drivers to memorize and navigate complex routes.6 The emergence of modern societies likely kicked off a virtuous circle where the need to solve increasingly complex tasks forced people to hone their learning skills, leading to higher IQs and further technological progress. The introduction of universal primary education amplified this virtuous circle. Better health undoubtedly helped as well. Early childhood diseases reduce IQ by diverting the body’s resources away from mental development towards fighting off infections. There is a strong correlation between measured IQ and disease burden across countries (Chart II-9). A number of studies have documented a strong relationship between the timing of malaria eradication in the U.S. and other parts of the world and subsequent observed gains in childhood IQs.7 Chart II-9IQ And Disease Burden

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Brain size and IQ are positively correlated. Forensic evidence from the U.S. suggests that the average volume of adult human skulls has increased by 7% since the late 1800s, or roughly the size of a tennis ball.8 Part 3: The End Of A 10,000 Year Trend The problem with environmental effects is that they eventually run into diminishing returns. This appears to have happened with the Flynn Effect. In fact, not only does the recent evidence suggest that the Flynn Effect has ended, but the data suggest that IQs are starting to decline. Chart II-10 shows that average math and science test scores fell in the OECD’s Program For International Scholastic Achievement (PISA) between 2009 and 2015, the latest year of the examination. The drop in math and science test scores has been mirrored in falling IQ scores. Flynn observed a decade ago that IQs of British teenagers were slipping.9 Similar results have been documented in France, the Netherlands, Germany, Denmark, and most recently, Norway. Chart II-10Math And Science Skills Are Slipping In The OECD

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Norwegian results, published last year, are particularly noteworthy.10 Bernt Bratsberg and Ole Rogeberg examined three-decades worth of data on IQ tests of Norwegian military conscripts. Military duty has been mandatory for almost all men in Norway since 1814, which means that the study’s authors were able to collect comprehensive data on most Norwegian men and their fathers. Their paper clearly shows that IQ peaked with the generation born in the mid-1970s and declined by about five points, or one-third of a standard deviation, for the one born in 1990 (Chart II-11). For the first time in recorded history, Norwegian kids today are not scoring as well as their parents. Chart II-11Norwegian IQs Have Been Falling For Those Born Since The Mid-1970s

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

A Mystery What caused the sudden reversal of the Flynn Effect in Norway and most other developed economies? Nobody knows. We can, however, offer three possible theories: New Technologies For much of human history, rising intelligence and technological innovation were complementary processes, meaning that the smartest people were the ones who could best exploit the new technologies that were coming their way. Moreover, as noted above, even those who were less gifted benefited from the mental stimulation that a technologically advanced society provided. It remains to be seen how future technological advances such as generalized AI will affect human intelligence, but recent technological advances seem to have had a dumbing down effect.11 For example, the GPS has obviated the need for people to navigate unfamiliar locations, thus blunting the development of their visuospatial skills. Modern word processors have made spelling skills less important. Having all the information in the world just a click away is a wonderful thing, but it has reduced the need for our brains to retain and codify what we learn. Meanwhile, the constant bombardment of information to which we are subject has made it difficult to concentrate on anything for long. How many youth today can read a report of this length without checking their Facebook feed multiple times? My guess is not many. Diminishing Returns To Education The ability to take young bright minds, who would have otherwise spent their lives doing menial labor, and provide them with an education was probably the greatest tailwind to growth that the 20th century enjoyed. There is undoubtedly still scope to continue this process, but the low-hanging fruits have been picked. Educational attainment has slowed dramatically in most of the world (Chart II-12). Economist James Heckman estimates that U.S. high-school graduation rates, properly measured, peaked over 40 years ago.12 Chart II-12The Contribution To Economic Growth From Rising Human Capital Is Falling

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Despite billions of dollars spent, efforts to improve school performance have generally fallen flat. A recent high-level report by the U.S. Department of Education concluded that “The panel did not find any empirical studies that reached the rigor necessary to determine that specific turnaround practices produce significantly better academic outcomes.”13 This gets to a point that most parents already know, which is that when people talk about “bad schools," they are really talking about “bad students.” Deteriorating Health Better health probably contributed to the Flynn Effect. But is it possible to have too much of a good thing? More calories are welcome when people are starving, but today’s calorie-rich, nutrient-poor diets have led to a surge in obesity rates. A clean environment reduces the spread of germs, but it also makes children hypersensitive to foreign substances. Following German reunification, researchers observed that allergies were much more common among West German children than their Eastern peers, presumably because of the West’s more salubrious environment.14 All sorts of weird and concerning physiological changes are occurring. Sperm counts have fallen by nearly 60% since the early 1970s.15 Testosterone levels in young men are dropping. Among girls, the age of first menarche has declined by two years over the past century.16 Are chemical agents in the environment responsible? If they are, what impact are they having on cognitive development? Nobody knows. Reported mental illness is also on the rise. The share of U.S. teenagers with a reported major depressive episode over the prior year surged by over 60% between 2010 and 2017 (Chart II-13). The fraction of young adults that made suicide plans nearly doubled.17 More than 20% of U.S. women over the age of 40 are on antidepressants.18 Five percent of U.S. children are receiving ADHD medication.19 Chart II-13A Disturbing Deterioration In Mental Health

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Implications For Economic Growth And Asset Markets So far, the reversal of the Flynn Effect has been largely confined to the developed economies. Test scores are still rising in the developing world, albeit from fairly low levels. For example, two recent studies have documented significant IQ gains in Kenya and Brazil.20 In the poorest countries, opportunities for improving health abound. Even small steps such as fortifying salt with iodine (which costs about five cents per person per year) have been shown to boost IQ by nearly one standard deviation.21 Measures to reduce inbreeding are also likely to boost IQ scores.22 Yet, we should not underestimate the importance of falling cognitive skills in developed economies. Chart II-14 shows that there is a clear positive correlation between student score on math and science and per capita incomes. Chart II-14Positive Correlation Between Student Scores On Math And Science And Per Capita Income

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Most technological innovation still takes place in developed economies. There is an extremely tight relationship between visuospatial IQ and the likelihood of becoming an inventor (Chart II-15). Since IQ is distributed along a bell curve, a 0.1 standard deviation drop in IQs across the entire distribution will result in an 8% decline in the share of people with IQs over 100, a 14% decline in those with IQs over 115, and a 21% decline in those with an IQ over 130 (by convention, each standard deviation on an IQ test is worth 15 points). Chart II-15Having A Compass In Your Head Makes You A Better Inventor

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Falling IQs could result in slower productivity growth, which could further strain fiscal balances. Lower IQs are also associated with decreased future orientation.23 People who live for the moment tend to save less. A decline in savings would push up real rates, leading to less capital accumulation. History suggests that a deceleration in productivity growth and higher real rates will put downward pressure on equity multiples (Chart II-16). Chart II-16Equity Multiples Tend To Fall When Real Rates Rise And Productivity Growth Declines

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Part 4: Generation E For 200 years, the environmentally-driven Flynn Effect disguised the underlying genetically-driven decline in IQs that began not long after the dawn of the Industrial Revolution. Flynn has acknowledged this himself, noting at the 2017 International Society For Intelligence Research Conference that “I have no doubt that there has been some deterioration of genetic quality for intelligence since the late Victorian times.”24 Now that the Flynn Effect has reversed, both genes and the environment are working together to reduce cognitive abilities in developed economies. This means that the most important trend in the world – a trend that allowed the human population to increase during the Malthusian era and later allowed output-per-worker to soar following the Industrial Revolution – has broken down. Yet, there may be another twist in the story – one that began just a few months ago: the first members of Generation E were born. E Is For Edited ... Or Eugenics Lulu and Nana will be like most other children, but with one key difference: They will be the first humans ever to have their genomes edited through a procedure know as CRISPR-Cas9. Rogue Chinese scientist He Jiankui deactivated their CCR5 gene, which the HIV virus uses as a gateway into the body. His actions were rightfully condemned around the world for endangering the twins’ health by using a procedure that has not yet been fully vetted in animal studies, let alone in human trials (Lulu and Nana’s father is HIV+ but it is debatable whether the children were at an elevated risk of infection). He Jiankui remains under house arrest at the university where he worked. But whatever his fate, the dam has been broken. For better or for worse, the era of personal eugenics has arrived. The Return Of The Silver Fox It is easier to delete a gene than to add one. It is even more difficult to swap out a large number of genes in a way that achieves a predictable outcome. Thus, the successful manipulation of highly polygenic traits such as intelligence — traits that are linked to hundreds of different genes – may still be decades away.25 Predicting a trait is much simpler than modifying it, however. The cost of sequencing a human genome has fallen by more than 99% since 2001 (Chart II-17). Start-up company Genomic Prediction has already developed a test for fertilized embryos for IVF users that predicts height within a few centimetres and IQ with a correlation of 0.3-to-0.4, roughly as accurate as standardized tests such as the SAT or ACT.26 Other companies are following suit.27 Chart II-17Sequencing Costs Have Plummeted

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Some will recoil in horror at the prospect of selecting prospective children in this manner. They will argue that such technologies, beyond being simply immoral, will widen social inequality between those who can afford them and those who cannot. Others will counter that screening embryos for certain traits is not that dissimilar to what people already do with prospective romantic partners. They will also point out that mass usage of these technologies will drive down prices to the point that even poor people will be able to access them, thus giving low IQ parents the chance to have high IQ kids. They might also note that such technologies may be the only way to reverse the ongoing accumulation of deleterious mutations within the human germline that has been the unintended by-product of the proliferation of life-saving medicines.28 We will not wade into this thorny debate, other than to note that there will be huge incentives for people to avail themselves of these technologies. The Coming Eugenic Wars And not just individuals either – governments too. While the initial impact of eugenic technologies will be small, the effects will compound over time. Carl Shulman and Nick Bostrom estimate that genetic screening could boost average IQs by up to 65 points in five generations (Table II-2). Table II-2A Poisoned Chalice? Genetic Screening Can Raise IQ

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

China has been investing heavily in genetic technologies. As Geoffrey Miller has argued, China’s infatuation with eugenics spans into the modern day.29 Like most other countries, fertility in China is negatively correlated with IQ. Mingrui Wang, John Fuerst, and Jianjun Ren estimate that China is currently losing nearly one-third of a point in generalized intelligence per decade, with the loss having accelerated rapidly between the 1960s and mid-1980s.30 The decline in the genetic component of Chinese IQs is coming at a time when the population itself is about to shrink. According to the UN’s baseline forecast, China will lose 450 million working-age people by the end of the century (Chart II-18). Meanwhile, the country is saddled with debt, the result of an economic model that has, for decades, recycled copious household savings into debt-financed fixed-investment spending in an effort to shore up domestic demand. Chart II-18China’s Labor Pool Is Shrinking

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The authorities may be tempted to tackle all three problems simultaneously by adopting generous pro-natal measures – call it the “at least one-child policy”– which increasingly harnesses emerging eugenic technologies. The resulting baby boom would strengthen domestic demand, thus making the economy less dependent on exports, while ensuring China’s long-term geopolitical viability. The Eugenic Wars are coming, and they will be unlike anything the world has seen before. BOX II-1 The Diffusion Of Bourgeois Values: Culture Or Genes? Higher-income people had more surviving children in the centuries leading up to the Industrial Revolution. Real per capita income was broadly stable during this period. This implies that there must have been downward social mobility, with sons, on average, being less wealthy than their fathers. This downward mobility, in turn, spread the characteristics of higher-income people across the broad swathe of society. What were these characteristics? Cultural values that emphasized thrift, diligence, and literacy were undoubtedly part of what was passed on to future generations. But surprisingly, it also appears that genetic transmission played an important, and perhaps pivotal, role. Models of genetic transmission make very concrete predictions about the correlations in economic status that one would expect to see among relatives. Biological brothers share 50% of their genes, as do fathers and sons. Likewise, first cousins share 25% of their genes, the same as grandfathers and sons. These facts yield two testable predictions: The first is that the correlation coefficient on status measures such as wealth, occupation, and education should be the same for relatives that share the same fraction of genes such as sibling pairs and father-son pairs. Box Chart II-1 shows that this is borne out by the data. The second prediction is that the correlation between status and genetic distance should follow a linear trend so that, for example, the correlation in wealth among brothers is twice that of first cousins and four times that of second cousins. Box Chart II-2 shows that this is also borne out by the data. BOX CHART II-1Comparative Father-Son And Brother Correlations By Status

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

BOX CHART II-2Wealth Correlations By Genetic Distance

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

Other evidence supports the importance of genes in the transmission of status across generations. The correlation in measures such as wealth, education, and occupation is much higher among identical twins than fraternal twins. Adopted children turn out to be more similar to their biological parents on these measures when they reach adulthood than their adopted parents, even when the children have never met their biological parents. The parent-child correlation also remains the same regardless of family size, suggesting that spreading the same resources over more children may not harm life outcomes to any discernible degree, at least on the measures listed above. Peter Berezin Chief Global Strategist Global Investment Strategy Footnotes 4 Xi Song, Cameron Campbell, and James Lee, "Descent Line Growth and Extinction From A Multigenerational Perspective, Extended Abstract," American Sociological Review 80:3, (April 21, 2015): 574-602. 5 Gregory Cochran and Henry Harpending, "The 10,000 Year Explosion: How Civilization Accelerated Human Evolution," Basic Books, (2009). 6 Mark Grinblatt, Matti Keloharju, and Juhani T. Linnainmaa, “IQ, Trading Behavior, and Performance,” Journal of Financial Economics, 104:2, (May 2012): 339-362. 7 Thomas Bouchard, "Genetic Influence On Human Psychological Traits - A Survey," Current Directions in Psychological Science 13:4, (August 2004): 148-151. 8 The tendency for the genetic contribution to IQ to increase until early adulthood and then to remain at high levels until old age is known as the Wilson Effect. There is no consensus on what causes it, but it probably reflects a number of factors: 1) It may take some children longer than normal to reach full intellectual maturity. Testing their IQs at a young age will result in scores that are lower than those expected based on their parents’ IQs. The opposite is true for children whose IQs increase relatively quickly in young age, but possibly top out earlier; 2) Environmental effects are probably more important in young age when a child’s brain is still quite malleable; 3) Self-reinforcing gene-environment interactions tend to increase with age. Children do not have much control over their environment, but as they get older, they will seek out activities that are more in keeping with their genetic predispositions. For example, a studious child may pursue a career that reinforces their love of learning. 9 "Cache Cab: Taxi Drivers' Brains Grow to Navigate London's Streets," Scientific American, (December 2011). 10 Atheendar Venkataramani, "Early Life Exposure to Malaria and Cognition in Adulthood: Evidence from Mexico," Journal of Health Economics 31:5, (July 2012): 767-780; Hoyt Bleakley, "Health, Human Capital and Development," Annual Review of Economics 2, (March 2010): 283-310; Hoyt Bleakley, "Malaria Eradication in the Americas: A Retrospective Analysis of Childhood Exposure," American Economic Journal: Applied Economics 2, (April 2010): 1-45. 11 "Anthropologists Find American Heads Are Getting Larger," ScienceDaily, (May 2012). 12 "British Teenagers Have Lower IQs Than Their Counterparts Did 30 Years Ago," The Telegraph, (February 2009). 13 Bernt Bratsberg and Ole Rogeberg, "Flynn Effect And Its Reversal Are Both Environmentally Caused," Proceedings of the National Academy of Sciences 115:26, (June 2018): 6674-6678. 14 On the face of it, artificial intelligence would appear to be a substitute for human intelligence. Many applications of AI would undoubtedly have this feature, especially those that allow computers to perform complex mental tasks that humans now must do. However, there are several ways that AI may eventually come to complement human intelligence. First, and most obviously, AI could be used to augment human capabilities either directly by hardwiring it into our brains, or indirectly through the development of drugs or genetic techniques which improve cognition. Second, looking further out, the benefits of highly intelligent AI systems would be limited if humans did not possess the requisite intelligence to understand certain concepts that are currently beyond our mental reach. No matter how well intentioned, trying to explain string theory to a mouse is not going to succeed. There are probably a multitude of ideas that AI could reveal that we simply cannot comprehend at current levels of human intelligence. 15 James Heckman and Paul La Fontaine, "The American High School Graduation Rate: Trends and Levels," The Review of Economics and Statistics 92:2, (May 2010): 244–262. 16 "Turning Around Chronically Low-Performing Schools," The Institute of Education Sciences (IES), (May 2008). 17 E. von Mutius, F.D. Martinez, C. Fritzsch, T. Nicolai, G. Roell, and H. H. Thiemann, "Prevalence Of Asthma And Atopy In Two Areas Of West Germany And East Germany," American Journal of Respiratory and Critical Care Medicine 149:2, (February 1994): 358-64. 18 "Sperm Counts In The West Plunge By 60% In 40 Years As ‘Modern Life’ Damages Men’s Health," Independent, (July 2017). 19 Kaspar Sørensen, Annette Mouritsen, Lise Aksglaede, Casper P. Hagen, Signe Sloth Mogensen, and Anders Juul, "Recent Secular Trends in Pubertal Timing: Implications for Evaluation and Diagnosis of Precocious Puberty," Hormone Research in Paediatrics 77:3, (May 2012): 137-145. 20 “Results from the 2017 National Survey On Drug Use And Health: Detailed Tables,” Substance Abuse and Mental Health Services Administration, Center for Behavioral Health Statistics and Quality, Rockville (Maryland), (September, 2018). 21 Laura A. Pratt, Debra J. Brody, and Qiuping Gu, "Antidepressant Use Among Persons Aged 12 and Over: United States, 2011–2014," NCHS Data Brief No. 283, Centers for Disease Control and Prevention, (August 2017). 22 Some, but not all, of the increase in reported rates of mental illness may be due to more aggressive diagnosis by health practitioners. For example, a recent study revealed that children born in August were 30% more likely to receive an ADHD diagnosis than those born in September, simply because they were less mature compared to other kids in the first few years of elementary school. See: Timothy J. Layton, Michael L. Barnett, Tanner R. Hicks, and Anupam B. Jena, "Attention Deficit-Hyperactivity Disorder and Month of School Enrollment," New England Journal of Medicine 379:22, (November 2018): 2122-2130. 23 Tamara C. Daley, Shannon E. Whaley, Marian D. Sigman, Michael P. Espinosa, and Charlotte Neumann, "IQ On The Rise: The Flynn Effect In Rural Kenyan Children," Psychological Science 14:3, (June 2003): 215-9; Jakob Pietschnig and Martin Voracek, "One Century of Global IQ Gains: A Formal Meta-Analysis of the Flynn Effect (1909-2013)," Perspectives on Psychological Science 10:3, (May 2015): 282-306. 24 N. Bleichrodt and M. P. Born, “Meta-Analysis of Research on Iodine and Its Relationship to Cognitive Development,” In: ed. J. B. Stanbury, "The Damaged Brain of Iodine Deficiency," Cognizant Communication Corporation, New York, (1994): 195-200; "Iodine status worldwide: WHO Global Database on Iodine Deficiency," World Health Organization, Geneva, (2004). 25 Mohd Fareed and Mohammad Afzal, "Estimating the Inbreeding Depression on Cognitive Behavior: A Population Based Study of Child Cohort," PLOS ONE 9:12, (October 2015): e109585. 26 H. de Wit, J. D. Flory, A. Acheson, M. McCloskey, and S. B. Manuck, "IQ And Nonplanning Impulsivity Are Independently Associated With Delay Discounting In Middle-Aged Adults," Personality and Individual Differences 42:1, (January 2007): 111-121; W. Mischel and R. Metzner, "Preference For Delayed Reward As A Function Of Age, Intelligence, And Length Of Delay Interval," Journal of Abnormal and Social Psychology 64:6, (July 1962): 425-31. 27 James Flynn, “IQ decline and Piaget: Does the rot start at the top?” Lifetime Achievement Award Address, 18th Annual meeting of ISIR, (July 2017). 28 For a good discussion of these issues, please see Richard J. Haier, “The Neuroscience of Intelligence,” Cambridge Fundamentals of Neuroscience in Psychology, (December 2016). 29 "The Future of In-Vitro Fertilization and Gene Editing," Psychology Today, (December 2018). 30 "DNA Tests For IQ Are Coming, But It Might Not Be Smart To Take One," MIT Technology Review, (April 2018). 31 Michael Lynch, "Rate, Molecular Spectrum, And Consequences Of Human Mutation," Proceedings of the National Academy of Sciences 107:3, (January 2010): 961-968. 32 Geoffrey Miller, "What *Should* We Be Worried About?" Edge, (2013). 33 Mingrui Wang, John Fuerst, and Jianjun Ren, "Evidence Of Dysgenic Fertility In China," Intelligence 57, (April 2016): 15-24.

Highlights Global equity markets have managed to recoup some of last year’s plunge since we upgraded stocks to overweight in late December. The equity rally has been tentative, however, and so far feels more like a technical bounce from oversold levels than a resumption of the bull market. One driving factor behind last year’s market swoon was that policy uncertainty spiked at a time when the last pillar of global growth, the U.S., was showing signs of cracking. Investors thus welcomed the Fed’s signal that it would pause in March. Nonetheless, shrinkage in the Fed’s balance sheet is proving to be troublesome. Quantitative tightening does not necessarily imply permanently higher risk premia, but it will be a source of volatility. There are hopeful but tentative signs that a U.S. slowdown is not the precursor to a recession. The hit to GDP from the U.S. government shutdown will be reversed next quarter. The FOMC has also signaled that policymakers are attuned to the economic risks associated with tightening financial conditions, and that the calm inflation backdrop provides room to maneuver. The FOMC will stand pat in March, but should restart rate hikes in June as the economic soft patch ends. We still see only a modest risk of a U.S. recession this year. In contrast, our outlook for growth outside the U.S. remains downbeat for at least the first half of the year. Among the advanced economies, Japan and Europe are being the most affected by the Chinese economic slowdown and global trade tensions. This means that monetary policy divergence will continue to be a tailwind for the dollar. China continues to stimulate at the margin, but efforts so far have been insufficient to put a floor under growth. The contraction in Chinese exports has just begun. It is still too early to upgrade EM assets or base metals. Despite the cloud still surrounding Brexit, sterling is beginning to look attractive as a long-term punt. Our decision to upgrade corporate bonds to overweight this month, similar to our reasoning for upgrading equities in December, is based on improved value and a sense that investor pessimism had become excessive. Just as the selloff in risk assets was overdone, so too was the rally in government bonds. It is highly unlikely that the Fed is done tightening, as is currently discounted in the money market curve. A resumption of Fed rate hikes around mid-year means that the 10-year Treasury yield will move back above 3% by year end. Feature Global equity markets have managed to recoup some of last year’s plunge since we upgraded the asset class back to overweight in the latter half of December. A decline in the VIX and high-yield bond spreads are also positive signs that global risk appetite is recovering, following an overdone investor ‘panic attack’ last quarter. The equity rally has been tentative, however, and so far feels more like a simple technical bounce from oversold levels than a resumption of the bull market. One problem is that policy uncertainty has spiked at a time when the last pillar of global growth, the U.S., is showing signs of cracking (Chart I-1). Investors are skittish while they await a clear de-escalation of U.S./China trade tensions, an end to the U.S. economic soft patch, an end to the U.S. government shutdown, and signs that global growth is bottoming (especially in China). There has only been some modestly positive news on a couple of these issues. Chart I-1Policy Uncertainty Has Spiked

Policy Uncertainty Has Spiked Watch Policy Uncertainty

Policy Uncertainty Has Spiked Watch Policy Uncertainty

Another factor that appeared to play a role in last quarter’s market swoon is the fear that the end of asset purchases by the European Central Bank and the normalization of the Fed’s balance sheet necessarily imply a structural de-rating for all risk assets. A related worry is that the de-rating might intensify the global economic slowdown, resulting in a self-reinforcing negative feedback loop. Does QT Imply Lower Multiples? The question of balance sheet normalization is a difficult one because there is widespread disagreement on how, or even whether, quantitative easing (QE) works. We have always maintained that QE was not about creating a wave of central bank liquidity that flowed into asset prices. Central banks did not “print money” – they created bank reserves. These reserves did not result in a major acceleration in broader measures of money growth, including M1 and M2, largely because there was little demand for loans and because banks tightened lending standards. In other words, the credit channel of monetary policy was broken. The implication is that investors should not worry that quantitative tightening (QT) implies a withdrawal of central bank liquidity that must mechanically come from the sale of risk assets. Rather, we believe that QE operates mostly through the portfolio balance effect. There are two ways to think about this channel. First, the central bank forced investors to move into riskier assets by purchasing large amounts of “safe” assets, such as government bonds. Investors had little choice but to redeploy the capital into other riskier areas, pushing up asset prices. The second perspective is that central bank purchases of government bonds depressed both the yield curve and bond volatility. Volatility fell because investors could forecast the policy rate with certainty – it would be glued to zero (or negative) for the foreseeable future in most of the advanced economies. This is akin to strong forward guidance that flattened the yield curve. Aggressive monetary stimulus, such as QE, also helped to reduce the perceived risk that the economy would succumb to secular stagnation or fall back into recession. Reduced bond volatility, lower bond yields, and less economic risk all increased the attractiveness of the riskier asset classes. These explanations represent two sides of the same coin. Either way, QE boosted a broad array of asset prices. If this is true, then unwinding QE must be bearish for risk assets, all else equal. In the case of the U.S., the fed funds rate is much more difficult to forecast than was the case when the Fed was buying bonds. Higher yields and bond volatility imply a lower equilibrium multiple in the equity market and wider equilibrium corporate bond spreads. Nonetheless, all else is not equal. If interest rates and bond volatility are rising in the context of healthy economic and profit growth, then it is likely that the perceived risk of secular stagnation is falling. It would be a sign that the economy has finally put the financial crisis firmly in the rear-view mirror. It could be the case that the upgrade in economic confidence overwhelms the negative impact of the reverse portfolio balance effect related to quantitative tightening, allowing risk assets to rise. No one can prove this thesis one way or the other and we are not making the case that unwinding the Fed’s balance sheet will necessarily go smoothly, especially since interest rates are rising at the same time. The problem is that both investors and the Fed are trying to figure out where the neutral fed funds rate lies. If the so-called level of R-star is still very low, then the Fed might have already made a policy mistake by raising rates too far. We discussed in last month’s Overview the market implications of four scenarios for the level of R-star and the Fed’s success in correctly guessing it. If the economy holds up and the economic soft patch ends in the coming months as we expect, then investors will revise their estimate of the neutral rate higher and risk assets will rally even as bond yields rise. The Doom Loop One risk to our base-case scenario is the so-called financial conditions “doom loop”. Irrespective of whether or not QT is playing a role, the doom loop scenario involves a shock to investor confidence that leads to a tightening in financial conditions and market liquidity as stock prices fall and credit spreads widen. More onerous financial conditions, in turn, undermine economic activity, which then feeds back into even tighter financial conditions. One could make the argument that risk assets are even more exposed to this type of negative feedback loop today than in past monetary tightening cycles because of program trading, the Fed’s balance sheet shrinkage and investors’ lingering shell shock from the Great Recession and financial crisis. Nonetheless, there are a few mitigating factors to consider. We believe that a doom loop is more likely to unfold when economic growth becomes very sensitive to changes in financial conditions. This normally happens when economic and financial imbalances are elevated. On a positive note, unlike in the lead-up to the last two recessions, the U.S. private sector is a net saver whose income outstrips spending by 2.1% of GDP (Chart I-2). The highly cyclical parts of the U.S. economy are not stretched to the upside as a share of GDP, reducing the risk that overspending in one part of the economy will required a deep contraction to correct the imbalance (Chart I-3). Chart I-2U.S. Private Sector: A New Saver

U.S. Private Sector: A New Saver The U.S. Private Sector Is A Net Saver

U.S. Private Sector: A New Saver The U.S. Private Sector Is A Net Saver

Chart I-3U.S. Cyclical Spending Not Extended

U.S. Cyclical Spending Not Extended

U.S. Cyclical Spending Not Extended

In terms of financial excesses, the good news is that the U.S. household sector is in its best shape in decades. Our main concern is debt accumulation in the corporate sector. We reviewed the related risks in a Special Report published in the November 2018 issue.1 We concluded that corporate leverage will not cause the next U.S. recession, because high levels of debt will only become a problem when profits begin to contract (i.e. when the economic downturn is already underway). Nonetheless, when a recession does occur, corporate spreads will widen by more than in the past for any given degree of economic contraction (see below). ‘Fed Put’ Still In Play Another factor that tempers the risk of a doom loop is that the so-called ‘Fed Put’ is still operating. The December FOMC Minutes and comments by various FOMC members communicated to investors that the Fed is attuned to the economic risks associated with tightening financial conditions, and that the calm inflation backdrop provides policymakers with room to maneuver. Chair Powell even said he was willing to adjust the Fed’s balance sheet run-off if necessary. One important reason for policymakers’ willingness to be flexible is that the fed funds rate is still not far from the zero-lower-bound, making it potentially more difficult for the FOMC to respond adequately in the event of a recession this year because the fed funds rate can only be cut by 250 basis points. Several U.S. data releases have been delayed due the government shutdown, but what has been released has been mixed. The downdraft in the January reading of the manufacturing ISM was eye-opening, highlighting that the global manufacturing slowdown has reached U.S. shores. The good news is that the non-manufacturing ISM and the small business survey, although off their peaks, remain consistent with solid underlying growth. The December U.S. payroll report revealed that wage growth continued to accelerate on the back of gangbusters job creation at the end of the year. There have also been some recent hints that the soft patch in capital spending and housing is ending (Chart I-4). Existing home sales fell sharply in December, but extremely low inventories suggest that it is more of a supply than a demand problem. The impressive bounce in home mortgage applications for purchases is a hopeful sign. U.S. commercial and industrial loan growth is also accelerating. Chart I-4Some Tentative Signs

Some Tentative Signs

Some Tentative Signs

These tentative signs that the economic soft patch is close to an end will not be enough to get the FOMC to tighten in March, after so many members have gone out of their way to signal a pause in recent weeks. Nonetheless, we believe the economy will remain strong enough for the Fed to resume hiking in June. The U.S. government shutdown will complicate interpreting incoming economic data. Ultimately, while its impact on Q1 real GDP growth will be non-trivial, it will be reversed the following quarter and we do not expect any permanent damage to be done. U.S. inflation should edge higher by mid-year, supporting our view that the Fed will resume tightening in June. The decline in oil prices will continue to feed into a lower headline inflation rate in the coming months, but that does not mean that the core rate will fall. Indeed, core CPI has increased by roughly 0.2% in each of the past three months, translating into an annualized rate of approximately 2.4%. Base effects will depress annual core inflation in February but, thereafter, this effect will begin to reverse. The acceleration in wage growth according to measures such as average hourly earnings and the Employment Cost Index highlights that underlying inflationary pressures continue to percolate (Chart I-5). The implication is that the Treasury bond market is overly complacent in discounting that the fed funds rate has peaked for the cycle. Chart I-5U.S. Wage Pressure Is Percolating

U.S. Wage Pressure Is Percolating

U.S. Wage Pressure Is Percolating

Looking further ahead, our base case remains that the next U.S. recession will not occur until 2020, and will be the result of tighter fiscal policy and further Fed tightening that takes short-term rates a step too far. No Bottom Yet For Global Growth Our outlook for growth outside the U.S. remains downbeat for at least the first half of the year. Our global economic indicators still show no sign of a turnaround, except for a bottoming in the diffusion index based on BCA’s Global Leading Economic Indicator (Chart I-6). The global ZEW economic sentiment index continued to fall in January, while business and consumer confidence readings in the advanced economies eroded heading into year end. Chart I-6Global Leading Indicators Still Deteriorating

Global Leading Indicators Still Deteriorating Global Growth Is Still Moderating...

Global Leading Indicators Still Deteriorating Global Growth Is Still Moderating...

A better global growth dynamic awaits more serious policy stimulus in China. Real GDP growth decelerated further to 6.4% year-over-year in the last quarter of 2018. This is no disaster, but the point is that there are still no signs of stabilization. The Chinese authorities continue to tweak the policy dials at the margin, most recently providing some tax cuts and a liquidity injection into the banking system. Nonetheless, the central government has so far abstained from stimulating the property market due to existing speculative excesses. This is very different from the previous two policy easing episodes, including 2015/16 (Chart I-7). Chart I-7China: No Property Market Stimulus...

China: No Property Market Stimulus...

China: No Property Market Stimulus...

The stimulus undertaken so far has been insufficient in terms of putting a floor under growth according to our 12-month Credit Impulse (Chart I-8). It is a hopeful sign that broad money growth is trying to bottom, but this does not guarantee that the credit impulse is about to turn. The latter is required to confirm that Chinese import demand will accelerate, providing a lift to EM exporters, EM asset prices and commodity prices. Without a positive credit impulse, China’s investment and construction activity will continue to moderate, leading to lower imports of machinery and raw materials. Chart I-8...And No Credit Impulse

...And No Credit Impulse

...And No Credit Impulse

The economic situation in China is likely to get worse before it gets better. Dismal trade figures in December confirmed that the trade war is beginning to bite. The period of export ‘front-running’ related to higher U.S. tariffs is over as total exports fell by 4.4% year-over-year. Last year’s collapse in export orders indicates that the woes are just beginning. In turn, moderating production related to the Chinese export sector will bleed into domestic consumption and imports, suggesting that it is too early to expect a durable rally in EM assets or commodity prices. Lackluster Chinese demand and growing trade concerns have weighted on global business confidence, contributing to the pullback in capital goods orders, manufacturing PMIs and industrial production in the advanced economies (Chart I-9). Even the average service sector PMI and consumer confidence index in the advanced economies have fallen in recent months, although both remain at a high level. Chart I-9The Fallout From Trade

The Fallout From Trade

The Fallout From Trade

Europe and Japan, in particular, are feeling the pinch. German GDP only grew 1.5% in 2018, implying that Q4 GDP growth was in the vicinity of just 0.2% QoQ. Meanwhile, European industrial production contracted by 3.3% year-over-year in December. The German Ifo and ZEW surveys do not point to any significant improvements in this trend. A few idiosyncratic factors explain some of this poor performance, including new emissions testing standards that have weighted on the German auto industry, a tightening in financial conditions in Italy, and the ‘gilets jaunes’ protests in France. Nonetheless, the euro area slowdown cannot be fully explained by one-off factors. The economy is highly sensitive to global trade fluctuations given that 18% of the euro area’s gross value added is generated in the manufacturing sector. Hence, China’s poor economic health has been painful for Europe, and the trend in Chinese credit does not bode well for the near term (Chart I-10). The European Central Bank (ECB) is likely to stay on the defensive as a result, especially as euro area core inflation, which has been stuck near 1% for three years, is unlikely to pick up if growth remains on the back foot. The ECB stuck with the view that the economic soft patch is temporary after the January policy meeting, but policymakers will consider providing more stimulus in March if the economy does not pick up (using forward guidance or a new TLTRO). This will weigh on the euro. Chart I-10China's Woes Are Infecting Europe

China's Woes Are Infecting Europe

China's Woes Are Infecting Europe

Japan is suffering from similar ills. Exports are no longer growing, and foreign machinery and factory orders are contracting at a 4.1% and 4.3% pace, respectively. This weakness is not mimicked in domestic growth, but the disproportionate contribution of the external sector to Japan’s overall economic health means that this country is also falling victim to the malaise witnessed in China and emerging markets, the destination of 19% and 45% of Japanese shipments, respectively (Chart I-11). Collapsing oil prices and a firming trade-weighted yen have amplified this deflationary backdrop. It is therefore far too early to bet that the Bank of Japan will tighten the monetary dials. Chart I-11Japan Hit By The Chinese Cold As Well

Japan Hit By The Chinese Cold As Well

Japan Hit By The Chinese Cold As Well

If we are correct that the U.S. economic soft patch will soon end, then the dollar will once again look to be the best of a bad lot. Interest rate expectations will move in favor of the dollar. We expect the dollar to rise by about 6% this year on a trade-weighted basis, appreciating most strongly against the AUD and SEK. As for sterling, it is beginning to look attractive as a long-term punt. Brexit Deadlock We are a month closer to the end-March deadline and a Brexit deal seems even farther out of reach. It could play out in one of three ways: (1) a “no deal” where the U.K. leaves the EU with no alternative in place; (2) a “soft Brexit” involving an agreement to form a permanent customs union or some sort of “Norway plus” arrangement; or (3) a decision to reverse the results of the original referendum and stay in the EU. There is no support for the “no deal” option in Parliament, which means that it won’t happen. We do not have a strong view on which of the latter two scenarios will occur. The odds of another referendum are rising and the polls are swinging away from any sort of Brexit, suggesting that the original referendum result may be over-turned via another referendum (Chart I-12). Nonetheless, for investors, it does not matter much whether it is scenario 2 or 3; either outcome would be welcomed by markets. Overweight sterling positions are attractive as a long-term play, although it could be some time before the final solution emerges. Chart I-12Brexit Result May Be Overturned

Brexit Result May Be Overturned

Brexit Result May Be Overturned

Upgrade Corporate Bonds To Overweight Given the recent global economic dynamics, it is perhaps surprising that U.S. corporate financial health actually improved in 2018 according to our Corporate Health Monitors (CHM). We highlighted in the aforementioned Special Report the risks facing U.S. corporate bonds when the economic expansion ends. High levels of corporate leverage mean that the interest coverage ratio for the median corporation in the Barclays-Bloomberg index will plunge to near or below all-time historic lows. The potential for a large wave of fallen angels implies that downgrade activity will be particularly painful for corporate bond investors. The surge in lower-quality issuance has led to a downward trend in the average credit rating and has significantly raised the size of the BBB-rated bonds relative to the IG index and relative to the broader universe of corporate bonds. Moreover, poor market liquidity and covenant erosion will intensify pressure for corporate spreads to widen when the bear market arrives. Rapid debt accumulation is reflected in our bottom-up Corporate Health Monitors (CHM) for the U.S. investment-grade and high-yield sectors (Chart I-13). The CHMs are constructed from six financial ratios that the rating agencies use when rating individual companies. The companies in our bottom-up sample were chosen so as to mimic the sector and quality distribution in the Bloomberg-Barclay’s corporate bond index. Chart I-13U.S. Corporate Health

U.S. Corporate Health

U.S. Corporate Health

The debt-to-book-value of equity ratio for both the U.S. IG and HY sample of companies has risen to nose-bleed levels, although the ratio appears to have flattened off for the latter. Despite rising leverage, the HY CHM has shifted into “improved health” territory and the IG CHM is on the verge of doing the same. Last year’s upturn in the profitability measures, such as the return on capital, overwhelmed the deteriorating leverage trend. In Europe, where we distinguish between domestic and foreign issuers, rising leverage has been concentrated among the latter until recently (Chart I-14). In any event, the CHM for both types of issuers is close to the neutral zone. Chart I-14Euro Area Corporate Health

Euro Area Corporate Health

Euro Area Corporate Health

Improving U.S. corporate health on its own would not justify increasing exposure to corporate bonds within balanced portfolios or moving down in quality. Profit growth is likely to moderate this year, especially in Europe, such that last year’s improvement in corporate health is likely to reverse. And, as previously discussed, the economic cycle is well advanced and this sector is particularly vulnerable to a recession. Nonetheless, value has improved enough to warrant a tactical upgrade to overweight within fixed-income portfolios, at a time when the FOMC has signaled a pause and the next recession is at least a year away. Implied volatility should continue to moderate and spreads should narrow, similar to dynamics in 2016, the last time that the Fed signaled patience following a period of market turmoil (Chart I-15). Chart I-15Fed Patience To Narrow Spreads

Fed Patience To Narrow Spreads

Fed Patience To Narrow Spreads

Spreads have already narrowed from the peak in late December, but 12-month breakeven spreads for most credit tiers are all still close to or above their historical means, except for AA-rated issues (Chart I-16). For example, the 12-month breakeven spread2 for the Baa credit tier is 46%. This means that the spread has been tighter than its current level 46% of the time since 1988 and wider than its current level 54% of the time. Historically, spreads tend to hover within the tight-end of their historical range during this phase of the credit cycle, and only cheapen significantly when the yield curve inverts and the default rate moves higher. Chart I-16Value Restored In IG Corporates...

Value Restored In IG Corporates...

Value Restored In IG Corporates...

For U.S. high yield, our estimate of the spread adjusted for expected defaults has risen to 237 bps (Chart I-17). This implies that investors are discounting a 2019 default rate of 3.2%, in line with Moody's forecast. Since we do not foresee recession this year, high-yield bonds are not expensive enough to be avoided within a portfolio. Chart I-17...And In HY Too

...And In HY Too

...And In HY Too

Value has also improved in the European corporate bond market, but our global fixed-income team still recommends favoring the U.S. market for global credit investors. Leverage is higher in the U.S., especially relative to domestic issuers in Europe, but the U.S. economic and profit outlook for 2019 is better. Conclusions Our decision to upgrade corporate bonds this month, similar to our reasoning for upgrading equities to overweight in December, is based on improved value and a sense that investor pessimism had become excessive. For the equity market, the S&P 12-month forward P/E is an attractive 15.4 as we go to press, and bottom-up estimates for 2019 EPS have been slashed to a very reasonable 8%. Just as the selloff in risk assets late last year was overdone, so too was the rally in government bonds. It is highly unlikely that the Fed is done tightening. A resumption of Fed rate hikes, probably in June, means that the 10-year Treasury yield will move back above 3% by year end. Across the major countries, market expectations for yields 5-10 years from now are close to current levels, which is extremely complacent (Chart I-18). Investors should keep duration short of benchmark. Chart I-18Forward Rates Far Too Low

Forward Rates Far Too Low

Forward Rates Far Too Low

Our shift to overweight in both equities and corporate bonds is tactical in nature. We fully expect to move back to neutral and then to underweight later this year or into 2020, as the peak in U.S. GDP draws nearer. Timing will be difficult as always, which means that investors should be prepared to trim risk exposure earlier than implied by our base-case economic timeline. The tactical upgrade does not imply that we have become more sanguine on the economic and geopolitical risks for 2019. We do not believe that quantitative tightening or U.S. corporate leverage will truncate the U.S. expansion prematurely. Nonetheless, there is a plethora of other risks to keep us up at night. These include a Fed policy mistake, a hard economic landing in China, a full-blown financial crisis in Italy and an escalation in U.S./China trade tensions. The last one has diminished marginally in probability. We have a sense that the recent equity market downdraft unnerved President Trump, such that he now has a diminished appetite for upsetting investors with talk of an escalating trade war ahead of next year’s election. Outside of these well-known risks, our geopolitical team has recently published its “Black Swans” report for 2019. These are deemed to be risks that are off of most investors’ radar screens, but that would have profound implications if they were to occur: It is premature to expect armed conflict over Taiwan, but an outbreak of serious tensions between China and Taiwan is possible as Sino-American strategic distrust continues to build. Russia and Ukraine may have a shared incentive to renew hostilities this year. Saudi Arabia has received a “blank cheque” from Donald Trump, and thus it may continue to be provocative. This could boost the geopolitical risk premium in oil prices. Tensions are building in the Balkans. A renewed conflict on Europe’s doorstep could be the next great geopolitical crisis. A “Lame Duck” Trump could stage a military intervention in Venezuela. We encourage interested readers to see our Special Report for details.3 As for emerging market assets and base metals, we continue to shy away until we receive confirmation that China is aggressively stimulating. We expect better news on this front by mid-year, but watch our China Credit Impulse indicator for timing. In contrast, investors should be overweight oil and related assets now because our commodity specialists still see the price of Brent rising above US$80/bbl sometime this year. Recent political turmoil in Venezuela buttresses our bullish oil view. Finally, this month’s fascinating Special Report, penned by BCA’s Chief Global Strategist, Peter Berezin, examines the long-term implications of the peaking in the average IQ in the advanced economies. Average intelligence is falling for both demographic and environment reasons. The impact will be far from benign, potentially leading to lower productivity growth, lower equity multiples, larger budget deficits and higher equilibrium bond yields. The report begins on page 20. Mark McClellan Senior Vice President The Bank Credit Analyst Mathieu Savary Vice President Foreign Exchange Strategy January 31, 2019 Next Report: February 28, 2019 II. The Most Important Trend In The World Has Reversed And Nobody Knows Why After rising for thousands of years, human intelligence has begun to decline in developed economies. This can be seen in falling IQ scores and a decline in math and science test scores. Environmental factors appear to account for the bulk of this decline, but no one knows what these factors are. If left unchecked, falling intelligence will severely undermine productivity growth. This could lead to lower equity multiples, larger budget deficits, and ultimately, much higher government bond yields. Technological advances, particularly in the genetic realm, promise to radically raise IQs. In a complete abandonment of its one-child policy, China will combine these controversial technologies with pro-natal measures in order to boost sagging birth rates. The coming Eugenic Wars will be one of the most important economic and geopolitical developments of the 21st century. Part 1: What The Tame Fox Says In 1959, a Soviet scientist named Dmitry Belyaev embarked on an ambitious experiment: to domesticate the silver fox. A geneticist by training, Belyaev wanted to replicate the process by which animals such as cats and dogs came to live side-by-side with humans. It was a risky endeavor. The Soviets had essentially banned the study of Mendelian genetics in favor of the blank slate ideology that is popular in progressive circles today. Belyaev persevered. Working under the guise of studying vulpine physiology, he selected foxes based on only one trait – tamability. Less than 10% of foxes made it to the subsequent generation, with the other 90% being sent off to fur farms. By the fourth generation, the changes were undeniable. Rather than fleeing humans, the foxes sought out their attention with no prompting whatsoever. They even wagged their tails and whined and whimpered like dogs do. The tame foxes also displayed physical changes. Their ears flopped over. Their snouts became shorter and their tails stood upright. "By intense selective breeding, we have compressed into a few decades an ancient process that originally unfolded over thousands of years," wrote Lyudmila Trut, who began as Belyaev’s assistant and took over the project when her boss died in 1985. Genetically Capitalist? Evolution can broadly proceed in two ways. The first way is through random mutations. This form of evolution, which scientists sometimes refer to as genetic drift, can take thousands of years to yield any discernable changes. The second way is through natural selection, a process that exploits existing variations in genetic traits. As the Russian fox experiment illustrates, evolution driven by selective pressures (either natural or artificial) can occur fairly quickly. Did selective pressures manifest themselves in human evolution in the lead up to the Industrial Revolution? Did humans, in some sense, domesticate themselves? In his book, A Farewell To Alms, economic historian Gregory Clark argued in the affirmative. Clark documented that members of skilled professions in Medieval England had twice as many surviving children as unskilled workers (Chart II-1). Indeed, the fledgling middle class of the time had even more surviving children than the aristocracy, who were often out fighting wars. As a result, the wages of craftsmen declined by a third relative to laborers between 1200 and 1800, implying that the supply of skilled labor was growing more quickly than the demand for skilled workers over this period.

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

In subsequent work, Clark and Neil Cummins argued that the spread of bourgeois values across pre-industrial England was more consistent with a model of genetic transmission than a cultural one (see Box II-1 for details). Similar developments occurred in other parts of the world. For example, in China, the gateway into the bureaucracy for a thousand years was the highly competitive imperial exam. Xi Song, Cameron Campbell, and James Lee showed that high-status men had more surviving children during the eighteenth- and nineteenth-centuries (Chart II-2).4

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The 10,000 Year Explosion Stephen Jay Gould famously said that “There’s been no biological change in humans in 40,000 or 50,000 years. Everything we call culture and civilization we’ve built with the same body and brain.” Gould was wrong. Data from the International HapMap Project show that human evolution accelerated by 100-fold starting around 10,000 years ago (Chart II-3).

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

In their book The 10,000 Year Explosion: How Civilization Accelerated Human Evolution, Gregory Cochran and the late Henry Harpending explained why evolution sped up so rapidly.5 The advent of agriculture led to a surge in population levels. This, in turn, increased the absolute number of potentially beneficial genetic mutations that could be subject to selection effects. Farming and the rise of city states also completely reshaped the environment in which people lived. Basic biology teaches us that environmental dislocations of this kind tend to generate selective pressures that cause evolution to accelerate. John Hawks, professor of anthropology and genetics at the University of Wisconsin-Madison, put it best: “We are more different genetically from people living 5,000 years ago than they were different from Neanderthals.” Many of the changes to our genomes relate to diet and diseases. The various genetic resistances that people have built up to malaria are all less than 10,000 years old. Mutations to the LCT gene, which confers lactose tolerance into adulthood, occurred independently in three different geographical locations: one in East Asia, one in the Middle East, and one in Africa. The Middle Eastern variant was probably responsible for the rapid enlargement of the Indo-European language group, which now stretches from India to Ireland. The African variant likely facilitated the Bantu expansion, which started near the present-day border of Nigeria and Cameroon, and then spread out across almost all of sub-Saharan Africa. Evolution Of The Human Brain About half of the genes in the human genome regulate some aspect of brain function. Given the rapid acceleration in evolution, it would be rather surprising if our own brains had not been affected. And indeed, there is plenty of evidence that they were. The frontal lobe of the brain has increased in size over the past 10,000 years. This is the part of the brain that regulates such things as language, memory, and long-term planning. Testosterone levels have also declined. That may explain the steady reduction in violent crime rates (Chart II-4).

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

We know that certain genes that are associated with higher intelligence have been under recent selective pressure. For example, the gene that leads to torsion dystonia – a debilitating movement disorder – appears to have increased in frequency. Why would a gene that causes a known disease become more widespread? The answer is that individuals who have this particular mutation tend to have IQs that are around 10-to 20-points above the population average. Why IQ Matters IQ has a long and contentious history. Yet, despite numerous efforts to jettison the concept, it has endured for one simple reason: It has more predictive power than virtually anything else in the psychological realm. A simple 30-minute IQ test can help predict future educational attainment, job performance, income, health, criminality, and fertility choices (Table II-1 and Chart II-5). IQ even predicts trader performance!6

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why

The Most Important Trend In The World Has Reversed And Nobody Knows Why