Sectors

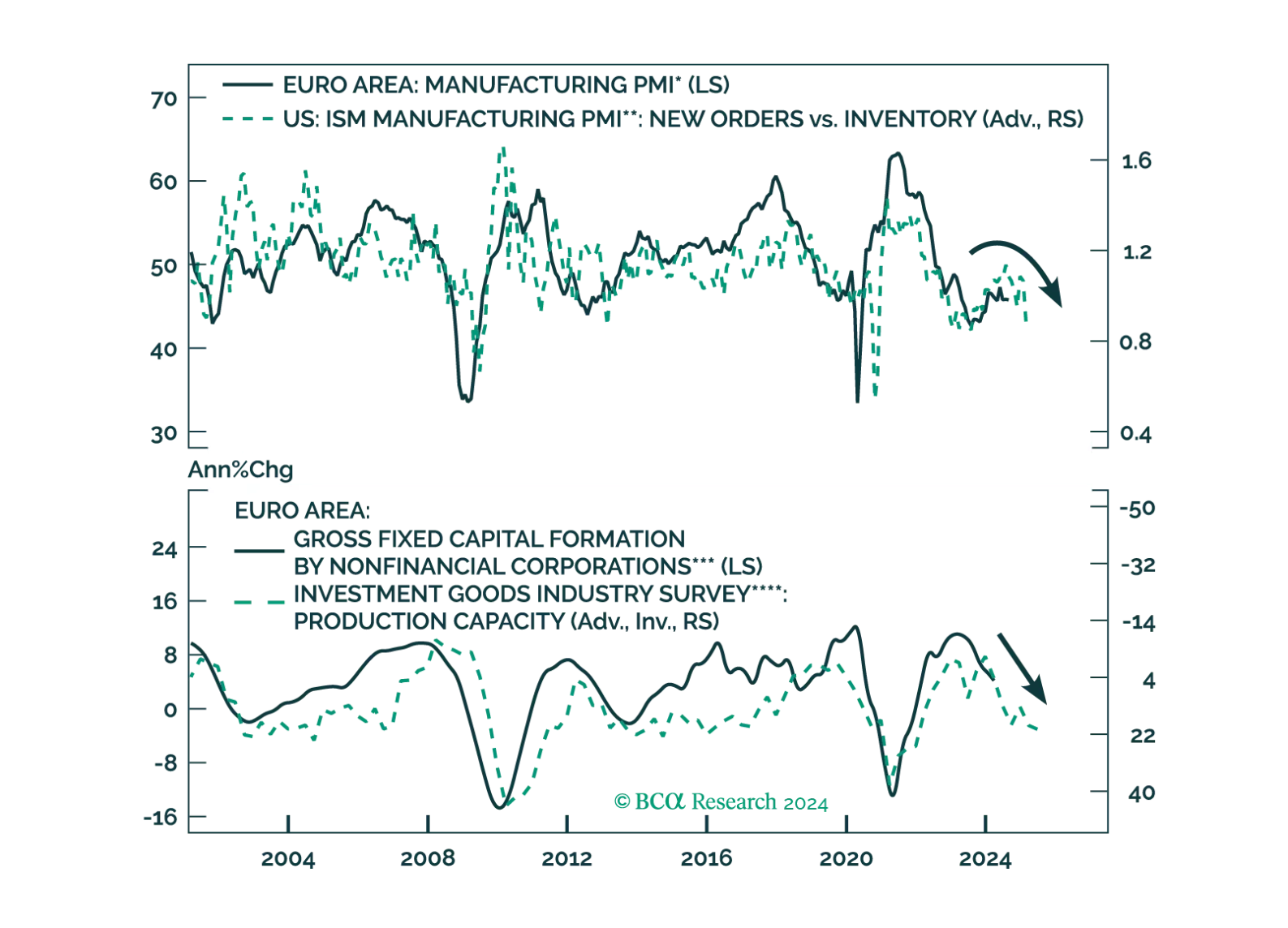

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?

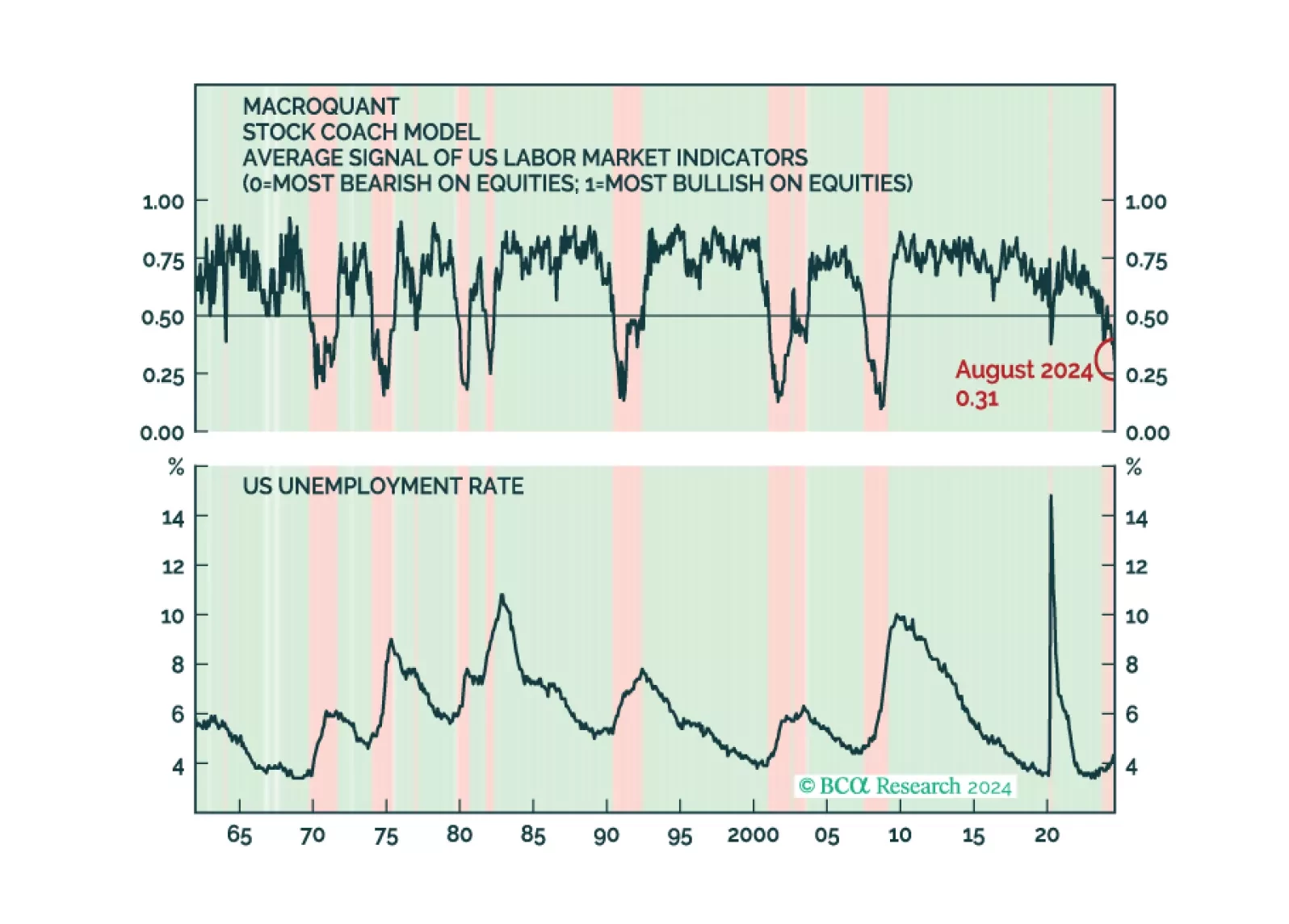

August nonfarm payrolls expanded by 142 thousand workers, from a downwardly revised 89 thousand and below expectations of 165 thousand. Payroll growth fell to a four-year-low of 116 thousand on a 3-month moving average basis. Notably, pro-cyclical…

The Fed’s Beige Book compiles qualitative input sourced from business and other organizational contacts in each of its 12 Districts. It precedes FOMC meetings by a couple of weeks and is meant to help participants trace the evolution of economic conditions. …

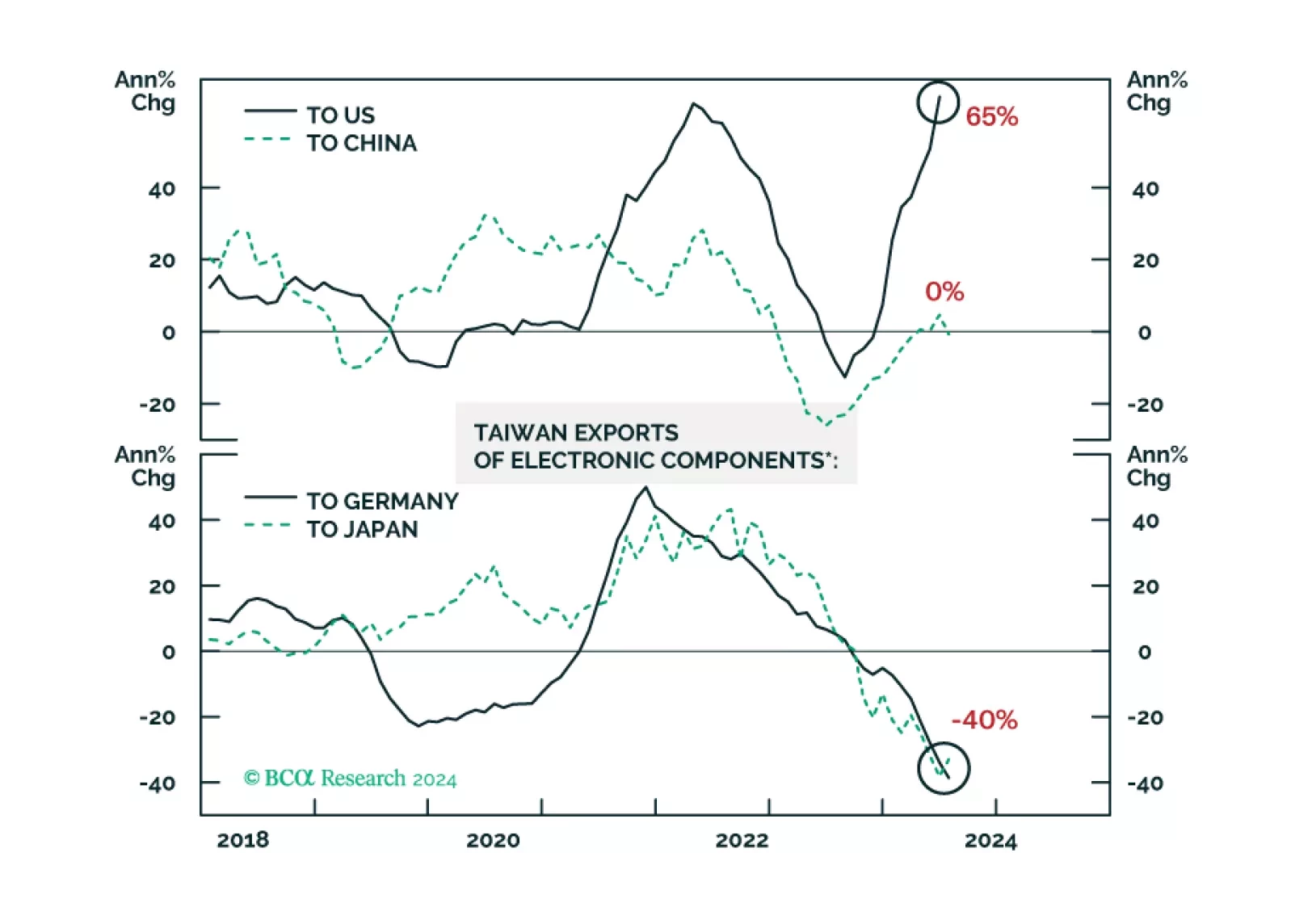

According to BCA Research’s Emerging Markets Strategy Service, China has been accumulating high-value memory semiconductors in anticipation of further US restrictions. Since October 2022, the US has been tightening rules that would limit China’s progress…

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

The Q2 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Nearly 80% (60%) of companies have topped earnings (sales) expectations in Q2, according to Factset. Excluding Materials and Real…

The risk-on soft-landing narrative dominated investors’ psyche last month and pro-cyclical assets topped the August return ranking. Asian currencies led the pack by a wide margin, while the dollar was the largest laggard. Markets pricing in an upcoming Fed…

According to BCA Research’s European Investment Strategy service, an increase in borrowing costs will further weaken vulnerable corporate balance sheets. As suggested by their Corporate Health Monitors (CHMs), the health of High-Yield corporate balance sheets…

MacroQuant continues to recommend underweighting equities and overweighting bonds. This is consistent with the Global Investment Strategy Team's decision to downgrade global equities to underweight in late June.

Chinese onshore and offshore bank stocks have outperformed their respective broad markets by 26% and 24% since October. Despite deteriorating return on assets, return on equity and net interest margins, investors have sought out their high dividend yields and…