Sectors

Restaurants - Dine And Dash

Restaurants - Dine And Dash

Underweight The S&P restaurants index has had an exceptional month, following surprisingly healthy results from both McDonalds and Starbucks, which collectively represent approximately 80% of the index. We think the move is short-sighted and we would be sellers into the strength. The positive results at these restauranteurs would typically be reflected in outsized forward earnings growth estimates. However, this is not the case; as shown in the second panel, estimates for the S&P restaurants index are falling behind the broad market. Given the index’s rise without a corresponding earnings lift, the valuation multiple has soared and is now at a level 50% higher than the market (third panel). Meanwhile, the index has been dining out on an unhealthy diet of debt and balance sheets are stretched to extreme levels (bottom panel). In the absence of an unlikely surge of cash flow, particularly given the headwinds an appreciating U.S. dollar represents, a painful cycle of belt-tightening lies ahead. Bottom Line: Tepid earnings growth, high valuations and bulging leverage are a recipe for stock price declines in the S&P restaurants index; stay underweight. The ticker symbols for the stocks in this index are: BLBG: S5REST - MCD, SBUX, YUM, DRI, CMG.

Highlights On a 6-month horizon, go long a combination of banks and high quality 10-year bonds. The recommended combination is 25 cents in the banks and 75 cents in the bonds. The preferred banks are European or euro area and the preferred bonds are U.S. T-bonds. Stay short oil and gas versus financials. During December, use any sharp sell-offs in sterling to buy the pound… …and to downgrade the FTSE100 to underweight. Feature Chart of the WeekBanks And Bond Yields Were Connected At The Hip... Until This Year

Banks And Bond Yields Were Connected At The Hip... Until This Year

Banks And Bond Yields Were Connected At The Hip... Until This Year

Back in June, in Oddities In The 1st Half, Opportunities In The 2nd Half we pointed out two striking oddities in financial market behaviour. One oddity was the sharp decoupling of crude oil from industrial commodity prices (Chart I-2). It is highly unusual for crude oil to outperform copper by 50 percent in the space of just six months. We argued that such an extreme deviation would have to correct one way or another. Which of course it did… Chart I-2Crude Oil Abruptly Decoupled From Industrial Commodities... Then Abruptly Recoupled

Crude Oil Abruptly Decoupled From Industrial Commodities... Then Abruptly Recoupled

Crude Oil Abruptly Decoupled From Industrial Commodities... Then Abruptly Recoupled

The other oddity was the abrupt decoupling of bank equity performance from bond yields (Chart I-3 and Chart of the Week). Bank equity prices and bond yields are usually connected at the hip. The tight connection exists because higher bond yields tend to signal stronger economic growth, either real or nominal. Stronger growth should be good for banks as it is associated with both accelerating credit growth and lower provisions for non-performing loans. Chart I-3Banks Decoupled From Bond Yields... But Will Recouple

Banks Decoupled From Bond Yields... But Will Recouple

Banks Decoupled From Bond Yields... But Will Recouple

On the back of these two striking oddities, we recommended a compelling trade: short oil and gas versus financials. This trade is now in profit and has further to run, but today we want to introduce a new trade: go long a combination of banks and bonds. Explaining The Oddities Of 2018 The underperformance of banks from February through September was entirely consistent with similar underperformances in the other classically growth-sensitive sectors – industrials, and basic materials as well as the decline in industrial commodity prices (Chart I-4). Furthermore, these underperformances started well before any inkling of a trade war. This suggests that the cyclical sector underperformances were correctly reflecting a common or garden down-oscillation in global growth. Chart I-4Oil And Gas Was The Odd Man Out

Oil And Gas Was The Odd Man Out

Oil And Gas Was The Odd Man Out

Oil was a striking oddity because its supply dynamics, rather than its demand dynamics, were dominating its price action, at one point lifting its year-on-year inflation rate to 70 percent for Brent and 80 percent for WTI. Part of this surge in year-on-year inflation was also to do with the ‘base effect’, the dip in the oil price to $45 in the summer of 2017. The base effect shouldn’t really bother markets. After all, most people do not consciously compare a price today with the price precisely a year ago. The problem is that central banks do compare a price today with the price precisely a year ago in their inflation targets. Clearly, when oil price inflation was running at 80 percent, it was underpinning headline CPI inflation, central bank reaction functions, and thereby bond yields. Hence, the two striking oddities – oil abruptly decoupling from industrial commodities (Chart I-5) and bond yields abruptly decoupling from banks – are two sides of the same coin. From February through September, bond yields were taking their cue, at least partly, from the rising price of oil, given its major impact on headline inflation and on central bank reaction functions. Whereas banks, industrials, and industrial commodity prices were taking their cue from fading global growth and industrial activity. Chart I-5It Is Highly Unusual For Oil To Outperform Copper By 50% In Six Months

It Is Highly Unusual For Oil To Outperform Copper By 50% In Six Months

It Is Highly Unusual For Oil To Outperform Copper By 50% In Six Months

A Banks Plus Bonds Combination Could Be A Win-Win The oddities of 2018 are now correcting. With the oil price sharply lower, its year-on-year inflation rate has plunged to -10 percent (Chart I-6). Furthermore, as we have pointed out in recent reports, the sharp deceleration in global credit growth from February through September has clearly arrested and even reversed. The upshot is that banks and bond yields will recouple, one way or the other. Chart I-6Oil Inflation Down from 70% To -10%

Oil Inflation Down from 70% To -10%

Oil Inflation Down from 70% To -10%

Most likely, global growth will rebound somewhat and the beaten-down bank equity prices have considerable scope for recovery (Chart I-7), while the restraint on headline CPI inflation will keep bond yields in check. Indeed, as President Trump recently tweeted: Chart I-7Global Growth Will Rebound, So Will Banks

Global Growth Will Rebound, So Will Banks

Global Growth Will Rebound, So Will Banks

“Inflation down, are you listening Fed!” But if we are wrong and growth disappoints, bank equities are already beaten-down while a further downdraft in inflation will pull down bond yields. Either way, on a six month horizon a combination of banks and high quality 10-year bonds should be a win-win strategy. Given the different betas of the two investments, the recommended combination is 25 cents in the banks and 75 cents in the bonds. The preferred banks are European or euro area and the preferred bonds are U.S. T-bonds. Focus On Sectors And Currencies The remainder of this report is a reminder that successful macro investing requires the application of the Pareto Principle, also known as 80:20 rule. In macro investing, the vast majority of performance outcomes, ‘the 80’, are explained by a very small number of drivers, ‘the 20’. We find that the vast majority of a region’s or a country’s stock market relative performance is explained just by its distinguishing sector fingerprint combined with its currency (Chart I-8 - Chart I-12). Chart I-8Euro Stoxx 600 Vs. MSCI Emerging Markets = Global Healthcare In Euros Vs. Global Technology In Dollars

Euro Stoxx 600 Vs. MSCI Emerging Markets = Global Healthcare In Euros Vs. Global Technology In Dollars

Euro Stoxx 600 Vs. MSCI Emerging Markets = Global Healthcare In Euros Vs. Global Technology In Dollars

Chart I-9Euro Stoxx 50 Vs. S&P 500 = Global Banks In Euros Vs. Global Technology In Dollars

Euro Stoxx 50 Vs. S&P 500 = Global Banks In Euros Vs. Global Technology In Dollars

Euro Stoxx 50 Vs. S&P 500 = Global Banks In Euros Vs. Global Technology In Dollars

Chart I-10FTSE 100 Vs. S&P 500 = Global Oil And Gas In Pounds Vs. Global Technology In Dollars

FTSE 100 Vs. S&P 500 = Global Oil And Gas In Pounds Vs. Global Technology In Dollars

FTSE 100 Vs. S&P 500 = Global Oil And Gas In Pounds Vs. Global Technology In Dollars

Chart I-11FTSE 100 Vs. Nikkei 225 = Global Oil And Gas In Pounds Vs. Global Industrials In Yen

FTSE 100 Vs. Nikkei 225 = Global Oil And Gas In Pounds Vs. Global Industrials In Yen

FTSE 100 Vs. Nikkei 225 = Global Oil And Gas In Pounds Vs. Global Industrials In Yen

Chart I-12FTSE 100 Vs. Euro Stoxx 50 = Global Oil And Gas In Pounds Vs. Global Banks In Euros

FTSE 100 Vs. Euro Stoxx 50 = Global Oil And Gas In Pounds Vs. Global Banks In Euros

FTSE 100 Vs. Euro Stoxx 50 = Global Oil And Gas In Pounds Vs. Global Banks In Euros

Major stock markets comprise of multinational companies whose sales and profits are internationally diversified. But each major stock market has a distinguishing ‘long’ sector in which it contains up to a quarter of its total market capitalisation, as well as a distinguishing ‘short’ sector in which it has a significant under-representation. The combination of this long sector and short sector gives each equity index its distinguishing fingerprint (Table I-1): FTSE100 = long energy, short technology. Eurostoxx50 = long banks, short technology. Nikkei225 = long industrials, short banks and energy. S&P500 = long technology, short materials. MSCI Emerging Markets = long technology, short healthcare. Table I-1Each Major Stock Market Has A Distinguishing Fingerprint

Oil, Banks, And Bonds: The Oddities Of 2018

Oil, Banks, And Bonds: The Oddities Of 2018

The other important factor is the currency. The FTSE100 oil and gas stock, BP, receives its revenue and incurs its costs in multiple major currencies, such as euros and dollars. In other words, BP’s global business is currency neutral. But BP’s stock price is quoted in London in pounds. Hence, if the pound strengthens, the company’s multi-currency profits will decline relative to the stock price and weigh it down. Conversely, if the pound weakens, it will lift the BP stock price. This means that the domestic economy can impact its stock market through the currency channel. Albeit it is a counterintuitive relationship: a strong economy via a strong currency hinders the stock market; a weak economy via a weak currency helps the stock market. What does all of this mean for our European country allocation right now? From a sector perspective, a stance that is short oil and gas versus financials penalises the FTSE100 versus the Eurostoxx50, given the FTSE100’s oil and gas fingerprint and the Eurostoxx50’s banks fingerprint. Against this, a weakening pound would support the FTSE100. Given that Theresa May’s Brexit agreement will meet stiff resistance when it comes to Parliament in the second week of December, the point of maximum risk for the pound is still ahead of us. But as we argued last week, we ultimately expect relief for the pound as: either the Article 50 process is extended, or the U.K. moves into a transition period within a negotiated Brexit.1 Hence, during December, use any sharp sell-offs in sterling to buy the pound, and to downgrade the FTSE100 to underweight. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading Model* This week we note that this year’s sell-off in Italian equities is technically very stretched. Therefore, in a continued de-escalation of the budget spat between Italy and the EU, Italian equities would be ripe for a strong countertrend burst of outperformance. On this basis, our recommended trade is long MIB versus the Eurostoxx with a profit target of 5% and a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-13

Long MIB Vs. Euro Stoxx

Long MIB Vs. Euro Stoxx

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com Footnote 1 Please see the European Investment Strategy Weekly Report “DM Versus EM, And Two European Psychodramas”, November 22, 2018 available at eis.bcaresearch.com. Fractal Trading Model Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Turkish commercial banks have been ramping up purchases of local currency government bonds. Given that commercial banks create new money “out of thin air” when they buy assets from non-bank entities, should investors interpret this phenomenon positively or negatively? Under the backdrop of a severe recession, we view this phenomenon as a stabilizing factor that can provide moderate relief - a painkiller rather than a poison. Meanwhile, record-wide net interest rate spreads as well as rising purchases of government bonds yielding around 20% are positive for banks’ earnings amid an otherwise dismal economic outlook. To express a selective positive bias toward this depressed and still fundamentally challenged market versus other EMs, we recommend a relative equity trade: long Turkish banks / short EM banks, currency unhedged. Feature On August 15, 2018, we upgraded our stance on Turkish markets from underweight to neutral and closed our shorts in the currency and bank stocks after having been bearish/underweight for several years.1 Our rationale was that Turkish equity and currency valuations had become cheap, and its financial markets oversold. Yet we stated that the adjustment in interest rates and ensuing economic slowdown were still pending – preventing us from going overweight. Are Turkish interest rates now sufficiently high to put a floor under the currency? In other words, is monetary demagoguery – relentless bank lending promoted by the authorities amid high inflation – a thing of the past?2 At first glimpse, the answer appears to be no. Turkish banks have been aggressively buying local currency government bonds – at a time when foreigners have been selling their holdings (Chart I-1). Chart I-1Turkish Banks Have Been Buying Local Government Bonds

Turkish Banks Have Been Buying Local Government Bonds

Turkish Banks Have Been Buying Local Government Bonds

As we demonstrate in Box I-1 on page 9, commercial banks in all countries create new money when they purchase any asset, including any security, from non-bank entities. One can argue that the Turkish banks’ creation of money “out of thin air” holds the potential to trigger renewed currency depreciation. Furthermore, banks’ financing of the government depresses government bond yields, bringing down market-determined local currency interest rates. On the other hand, there is also evidence that banks have drastically curtailed financing to the real economy, which is causing a severe collapse in domestic demand. This has already squeezed imports and has started to narrow the current account deficit - a necessary condition for macro and exchange rate stabilization (Chart I-2). As such, it seems Turkey’s necessary macro adjustment is already under way. Chart I-2Turkey: Current Account Deficit Is Narrowing

Turkey: Current Account Deficit Is Narrowing

Turkey: Current Account Deficit Is Narrowing

These two dynamics – (1) banks financing the government by creating money “out of thin air” and (2) banks inhibiting financing to households and companies – are conflicting. While many economists refer to this phenomenon as a crowding out of the private sector by the government, we disagree with this analytical framework. Please refer to Box I-1 on page 9 for a more detailed discussion. Our assessment of these dynamics is as follows: In the current context of rapidly shrinking domestic demand, banks’ financing of the government is a mitigating factor in the ongoing macro adjustment. Commercial banks’ financing of the public sector via bond purchases caps market-determined interest rates and allows the government to spend, therefore diminishing the blow to the real economy. Consequently, the expansion of Turkish banks’ purchases of government bonds is a silver lining in an otherwise harsh macro adjustment. So long as this phenomenon is not prolonged indefinitely and does not cause the currency to plunge anew, it is an acceptable strategy for both banks and the government. In fact, it could form a fertile ground for Turkish banks’ stock prices to start rising from the ashes, at least relative to other emerging markets. Fiscal Deficit Financing By Banks: Poison Or Painkiller? Diagnosing a patient in critical condition and prescribing the right medicine is a complex task. Assessing monetary conditions in a financial crisis-stricken economy and determining the correct policy mix is no different. While monetary tightening may be the right medicine for some parts of the economy, monetary easing can be appropriate for others parts. In fact, this is what is currently happening in Turkey. There is a dichotomy occurring between monetary easing for the government (in the local currency bond market) and monetary tightening for companies and households. Chart 3 demonstrates that local currency broad money growth now slightly exceeds bank loan growth. One of the reasons for this is that banks are literally creating money by purchasing government securities. With a low likelihood of default and a yield of 20%, government securities are currently attractive for Turkish banks. On the surface, government deficit financing via money creation by banks might seem like a recipe for higher inflation. Yet, we have to put this phenomenon in the context of current cyclical economic conditions in Turkey. The economy is on the precipice of a major recession which will likely produce a major deflationary shockwave. Money and credit growth in real terms is negative (Chart I-3, bottom panel). In addition, government expenditures in real terms are now contracting, suggesting that fiscal policy is tight (Chart I-4). Furthermore, government debt levels are low – total public debt stands at 31% of GDP. This means that fiscal expansion is a lever that authorities can and should be using. Chart I-3Turkey: Money And Loan Growth Are Negative In Real Terms

Turkey: Money And Loan Growth Are Negative In Real Terms

Turkey: Money And Loan Growth Are Negative In Real Terms

Chart I-4Turkey: Fiscal Policy Is Tight

Turkey: Fiscal Policy Is Tight

Turkey: Fiscal Policy Is Tight

Hence, we infer that banks’ financing of government expenditures are not excessive from a macro perspective; particularly when considering the currently heightened recessionary crosscurrents. Bottom Line: The expansion of Turkish banks’ purchases of government bonds are capping local bond yields and, on the margin, allowing the government to support the economy. Given the backdrop of a severe recession, we view this as a stabilizing factor – a painkiller rather than a poison. Monetary Tightening In The Real Economy Commercial banks have substantially tightened financing to companies and households. Interest rates on bank loans to businesses and consumers have risen much more than the central bank’s policy rate. The former are now 850 basis points higher than the latter (Chart I-5, top panel). Chart I-5Turkey: Tight Monetary Conditions In The Real Economy

Turkey: Tight Monetary Conditions In The Real Economy

Turkey: Tight Monetary Conditions In The Real Economy

In real terms (deflated by core CPI), commercial bank loan interest rates are now 8% (Chart I-5, bottom panel). High real bank loan rates charged to households and companies will cause domestic demand to collapse – despite a real policy rate at zero. Provided economic activity is already shrinking, it will be difficult for debtors to achieve a hurdle real rate of 8%. This is already producing a collapse in loan demand and a material retrenchment in consumer and business spending. A statistical regression of economic activity variables on the change in borrowing costs demonstrates that the Turkish economy is in for a severe recession across all sectors, with capital expenditures being the hardest hit (Chart I-6). Chart I-6Turkey: The Recession Will Be Severe

Turkey: The Recession Will Be Severe

Turkey: The Recession Will Be Severe

A cheapened currency and high borrowing costs are the correct medicine for the nation’s deep economic imbalances – i.e. its large and persistent current account deficits. In fact, the real economy has already been adjusting: the current account excluding oil is starting to narrow (refer to Chart I-2 on page 2). This together with cheap valuations may help put a floor under the lira (Chart I-7). Chart I-7The Turkish Lira Is Cheap

The Turkish Lira Is Cheap

The Turkish Lira Is Cheap

Bottom Line: Interest rates on bank loans have increased much more than the central bank policy rate and are sufficiently high in real terms, foreshadowing a severe, but necessary, domestic demand contraction. Go Long Turkish Banks / Short EM Banks There appears to be a relative tactical opportunity to go long Turkish banks while shorting EM banks. Relative share prices in dollar terms between Turkish and EM banks are at an all-time low (Chart I-8). Odds are that Turkish banks will outperform for the time being. Chart I-8Long Turkish Banks / Short EM Banks

Long Turkish Banks / Short EM Banks

Long Turkish Banks / Short EM Banks

Not only are Turkish banks charging a large spread on loans relative to the policy rate, they are also enjoying a wide net interest rate spread – lending rates minus deposit rates. In fact, Turkish banks’ net interest rate spread is presently the highest in recorded history (Chart I-9, top panel). This is very positive for banks’ net interest margins (NIM) – net interest income as percent of loans - and earnings (Chart I-9, bottom panel). Chart I-9Turkish Banks' Margins Are Widening

Turkish Banks' Margins Are Widening

Turkish Banks' Margins Are Widening

In addition, banks’ purchases of government bonds allows them to expand their balance sheets and earn a yield that is around 20%. Given the government’s low credit risk, this is also positive for banks’ profits. On the negative side, non-performing loans (NPLs) are set to surge. Therefore, any investment consideration should take into account banks’ equity erosion due to surging NPLs. Turkish banks are presently extremely under-provisioned, as illustrated in Chart I-10. Yet their share prices have already plunged substantially, discounting a higher level of NPLs than banks have acknowledged and provisioned for. Chart I-10Turkey: NPLs Are Set To Surge

Turkey: NPLs Are Set To Surge

Turkey: NPLs Are Set To Surge

We have performed a credit stress test for the Turkish banking system. The scenario analysis shown in Table I-1 illustrates that banks’ share prices are already pricing in a significant amount of bad news regarding the NPL cycle. For example, in a scenario where the non-performing credit assets (NPCA) ratio rises to 20% from its current 3.5% level, bank stocks would be fairly valued at current levels. Table I-1Credit Stress Test For Turkish Banks

Turkish Monetary Demagoguery: A Thing Of The Past?

Turkish Monetary Demagoguery: A Thing Of The Past?

Considering that the NPL-to-total-loan ratio reached 18% after the 2001 currency crisis, we believe 20% is a reasonable estimate. The key difference between now and the 2001 crisis is that woes in 2001 were related to unsustainable government debt, while Turkey’s present problems stem from excessive private debt. This valuation part of the stress test assumes that the fair value for the price-to-book value (PBV) ratio adjusted for all credit losses is 1.3 - the average PBV ratio for EM banks since 2011. In short, banks’ stock prices are currently trading close to their fair value assuming 20% NPCA (Table I-1). In all scenarios, we assume a recovery rate of 40%. In terms of structural valuations, using our model for the cyclically-adjusted P/E (CAPE) ratio, Turkish banks are currently trading at two standard deviations below their fair value in absolute terms, and two-and-half standard deviations relative to the other EM banks (Chart I-11). Chart I-11Turkish Bank Stocks Are Cheap

Turkish Bank Stocks Are Cheap

Turkish Bank Stocks Are Cheap

Given that we expect an additional selloff in EM risk assets, Turkish bank stocks will likely relapse in absolute terms. This is why we recommend a market-neutral bet. In short, we expect more downside in the share price of EM banks than in Turkish ones for now. Investment Conclusions Given our overarching negative view on emerging markets as a whole, we are reluctant to be bullish on Turkish risk assets in absolute terms. The basis behind why we are not upgrading our stance on Turkey’s overall stock index is as follows: Non-financials companies are about to experience severe profit shrinkage as the recession deepens. Conversely, contraction in banks’ earnings will be mitigated by a very wide NIM and an increased financing of the government at yields above 20%. In addition, we expect EM currencies and high-yielding local bonds to resume their selloff, and corporate and sovereign credit spreads to widen. Given Turkey has historically been a high-beta market, it is difficult to bet on its financial markets outperforming EM peers in a bear market. Finally, the recent rebound in Turkish markets was from quite oversold levels and is currently facing its first technical resistance (Chart I-12). Chart I-12The Lira And Local Government Bonds Are Facing Their First Technical Resistance

The Lira And Local Government Bonds Are Facing Their First Technical Resistance

The Lira And Local Government Bonds Are Facing Their First Technical Resistance

Overall, we continue to recommend a neutral allocation to Turkey for EM dedicated equity investors, as well as local currency bond and credit portfolios. Nevertheless, to express a selective positive bias toward this depressed market versus other EMs, we recommend a relative equity trade: Long Turkish banks / short EM banks, currency unhedged. Stephan Gabillard, Senior Analyst stephang@bcaresearch.com Box 1 How Banks Create Money By Purchasing Assets From A Non-Bank Entity We demonstrate, in a stylized example, how a commercial bank (Bank 1) creates a new deposit in the banking system – which consists of two banks (Bank 1 and Bank 2) - when it purchases a bond from an investor (Investor A) that is a non-bank. For simplicity, we presume that this is the only transaction in the banking system on that day. All numbers we cite here are local currency values and all transactions take place in local currency. We assume at the beginning of Day 1 that both Bank 1 and Bank 2 each have excess reserves (ERs) of 1000 and existing deposits of 1000 (Figure I-1). Hence, the overall banking system ERs amount to 2000 and total deposits are equal to 2000. Figure I-1Begining Of Day 1 Balance Sheet & Transactions

Turkish Monetary Demagoguery: A Thing Of The Past?

Turkish Monetary Demagoguery: A Thing Of The Past?

As Bank 1 purchases a bond at the price of 300 from Investor A, the following balance sheet accounting entries take place (these entries are shown in red in Figure I-1): Bank 1 acquires a bond and its assets now include a bond valued at 300. Investor A has an account at Bank 2, so to pay for this purchase Bank 1 transfers 300 from its ERs to Bank 2’s ERs account at the central bank. Bank 1 ERs decline by 300. Hence, its assets and liabilities have not changed – it has just swapped 300 in ERs with 300 in bond (Figure I-1). Bank 2 credits Investor A’s deposit account by 300. Hence, Investor A received a deposit valued at 300 that it previously did not have. This is a new deposit for the whole banking system that was created “out of thin air”. Bank 2’s ERs and hence its total assets have risen by 300. This rise in Bank 2’s assets is balanced by the increase of its deposit by 300 (Figure I-2). In brief, this deposit is nothing more than an accounting entry to balance Bank 2’s assets and liabilities. Yet, deposits represent money and give their holders purchasing power. Figure I-2End Of Day 1 Balance Sheet

Turkish Monetary Demagoguery: A Thing Of The Past?

Turkish Monetary Demagoguery: A Thing Of The Past?

Assuming that during the day there was no other transaction in this banking system, the latter’s ERs have remained unchanged at 2000 yet its total deposits have risen from 2000 to 2300. A new deposit worth 300 was created without the central bank providing any funding (new ERs) to the banking system. Money supply is the sum of all deposits in the banking system and commercial banks create deposits “out of thin air” when they lend to non-banks or purchase assets from non-banks. As such, banks do not need to reduce private sector lending to fund the government. In other words, no “crowding out” of the private sector needs to take place for banks to buy government bonds. Footnotes 1 Please see Emerging Markets Strategy Special Alert "Turkey: Booking Profits On Shorts," dated August 15, 2018, the link available on page 14. 2 Please see Emerging Markets Strategy Special Report "Turkey's Monetary Demagoguery," dated June 1, 2016, available at ems.bcaresearch.com Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Air Freight & Logistics: We Have Liftoff

…

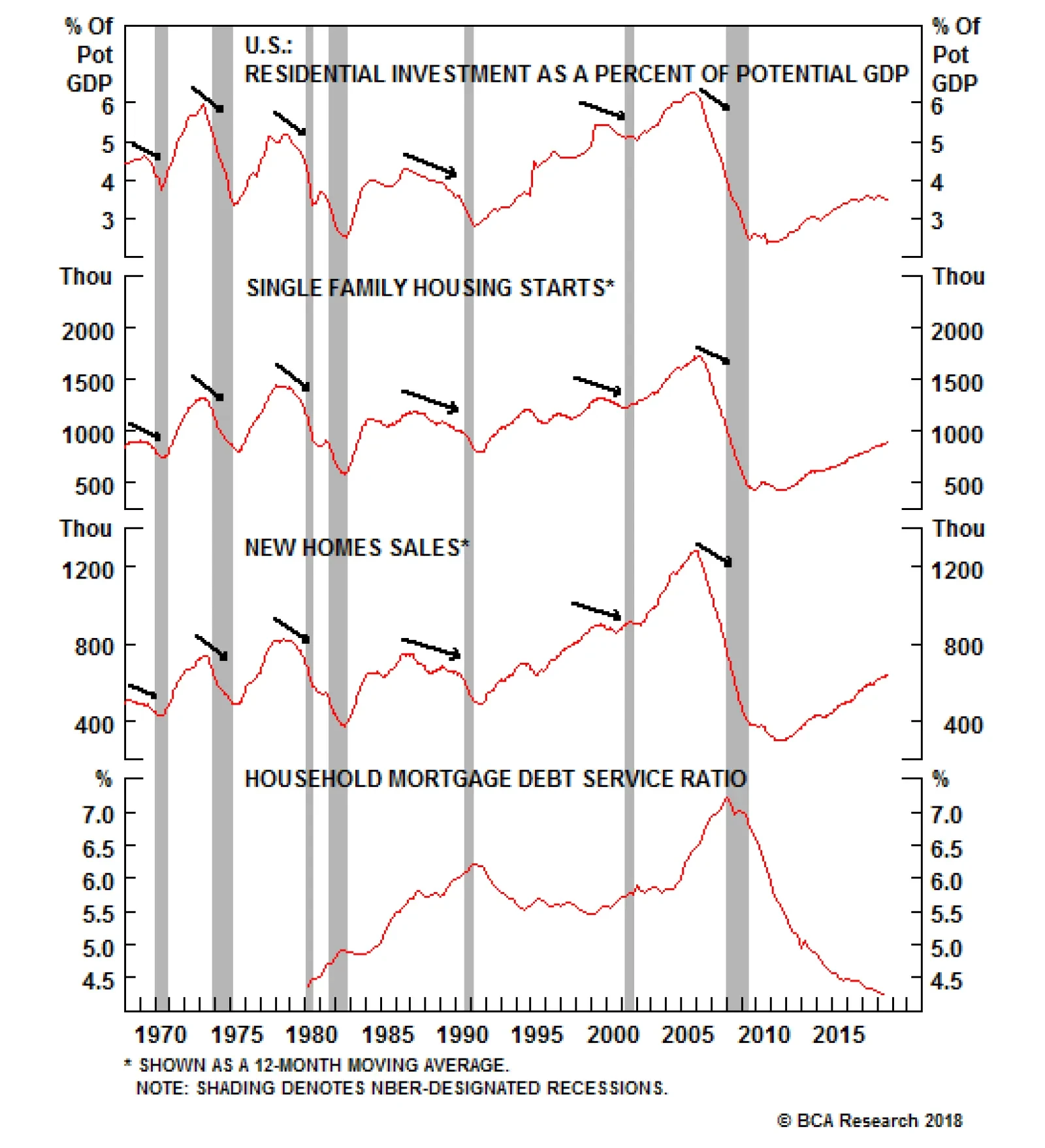

The above chart shows the three most important indicators of the housing market in our view. Residential investment as a share of potential GDP, the 12-month moving average of single family housing starts and the 12-month moving average of new home sales. At…

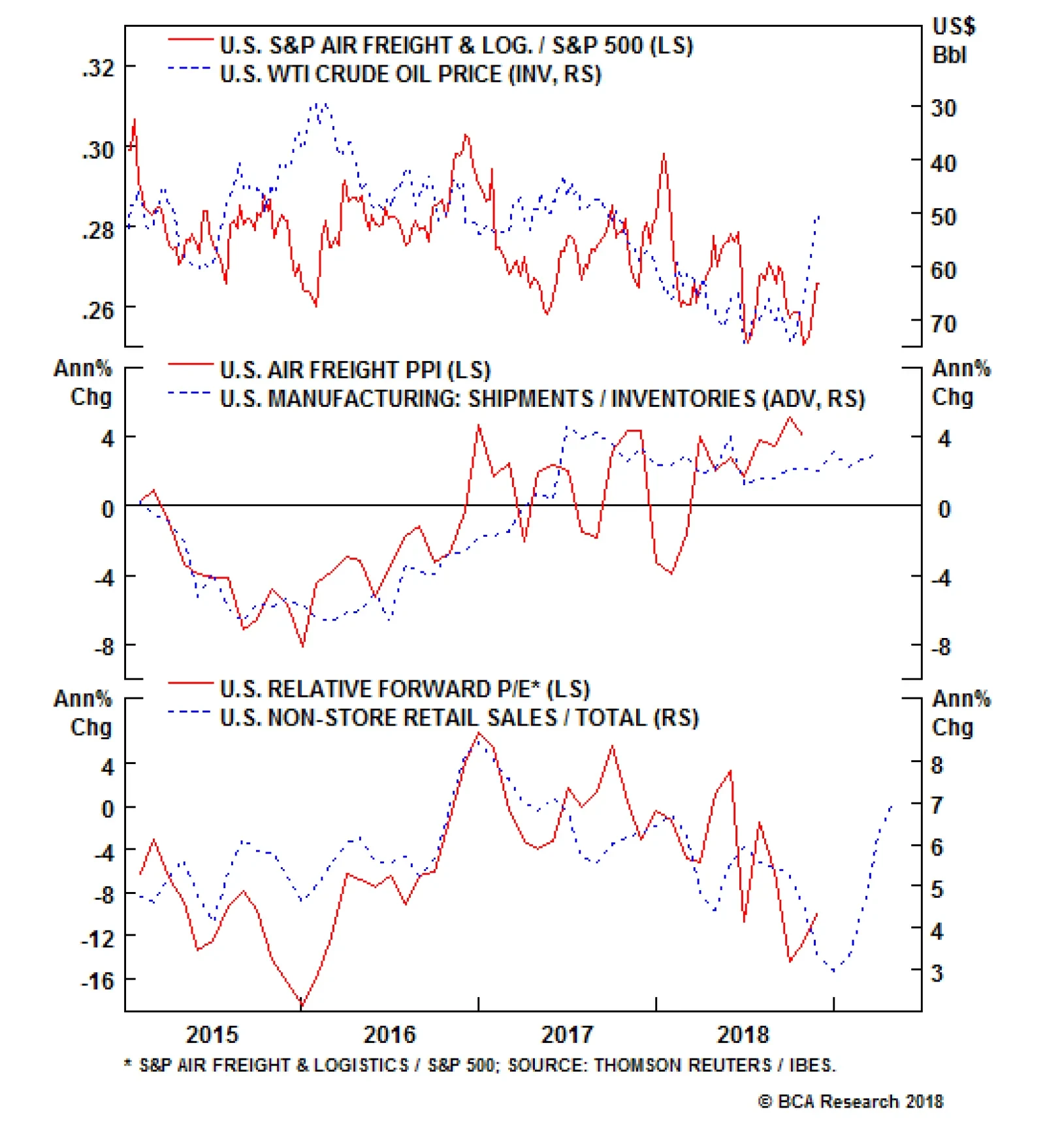

Overweight (High-conviction) Air freight & logistics stocks have been bouncing along the bottom for the better part of the past year and have formed a base that should serve as a launch board higher in the coming months. Energy costs comprise a large chunk of freight services input costs and the recent drubbing in oil markets will boost margins especially on the eve of the busiest season for courier delivery services (top panel). On that front, there are high odds that this holiday sales season will be another record setting one, especially given that corporations have paid out bonuses and shared part of the lowering in corporate taxes and also wage inflation is underpinning discretionary incomes. Keep in mind that the accelerating domestic manufacturing shipments-to-inventories ratio confirms that demand for hauling services is upbeat. The implication is that rising demand for freight services will buoy industry profits and lift stock prices out of their recent funk (middle panel). While the U.S./China trade tussle and the greenback are clear risks to our sanguine S&P air freight & logistics transportation subindex and have been intense headwinds for the sector, they are already reflected in depressed valuations (bottom panel). Bottom Line: We reiterate our high-conviction overweight status in the S&P air freight & logistics index; please see last week’s Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S5AIRF - FDX, UPS, EXPD and CHRW.

We Have Liftoff

We Have Liftoff

Mr. X and his daughter, Ms. X, are long-time BCA clients who visit our office toward the end of each year to discuss the economic and financial market outlook. This report is an edited transcript of our recent conversation. Mr. X: I have been eagerly looking forward to this meeting given the recent turbulence in financial markets. Our investments have done poorly in the past year and, with hindsight, I wish I had followed my instincts to significantly cut our equity exposure at the end of 2017, although we did follow your advice to move to a neutral stance in mid-2018. I remain greatly troubled by economic and political developments in many countries. I have long believed in open and free markets and healthy political discourse, and this all seems under challenge. As always, there is much to talk about. Ms. X: Let me add that I also am pleased to have this opportunity to talk through the key issues that will influence our investment strategy over the coming year. As I am sure you remember, I was more optimistic than my father about the outlook when we met a year ago but things have not worked out as well as I had hoped. In retrospect, I should have paid more attention to your view that markets and policy were on a collision course as that turned out to be a very accurate prediction. When I joined the family firm in early 2017, I persuaded my father that we should have a relatively high equity exposure and that was the correct stance. However, this success led us to maintain too much equity exposure in 2018, and my father has done well to resist the temptation to say “I told you so.” So, we are left with a debate similar to last year: Should we move now to an underweight in risk assets or hold off on the hope that prices will reach new highs in the coming year? I am still not convinced that we have seen the peak in risk asset prices as there is no recession on the horizon and equity valuations are much improved, following recent price declines. I will be very interested to hear your views. BCA: Our central theme for 2018 that markets and policy would collide did turn out to be appropriate and, importantly, the story has yet to fully play out. The monetary policy tightening cycle is still at a relatively early stage in the U.S. and has not even begun in many other regions. Yet, although it was a tough year for most equity markets, the conditions for a major bear market are not yet in place. One important change to our view, compared to a year ago, is that we have pushed back the timing of the next U.S. recession. This leaves a window for risk assets to show renewed strength. It remains to be seen whether prices will reach new peaks, but we believe it would be premature to shift to an underweight stance on equities. For the moment, we are sticking with our neutral weighting for risk assets, but may well recommend boosting exposure if prices suffer further near-term weakness. We will need more clarity about the timing of a recession before we consider aggressively cutting exposure. Mr. X: I can see we will have a lively discussion because I do not share your optimism. My list of concerns is long and I hope we have time to get through them all. But first, let’s briefly review your predictions from last year. BCA: That is always interesting to do, although sometimes rather humbling. A year ago, our key conclusions were that: The environment of easy money, low inflation and healthy profit growth that has been so bullish for risk assets will start to change during the coming year. Financial conditions, especially in the U.S., will gradually tighten as decent growth leads to building inflationary pressures, encouraging central banks to withdraw stimulus. With U.S. equities at an overvalued extreme and investor sentiment overly optimistic, this will set the scene for an eventual collision between policy and the markets. The conditions underpinning the bull market will erode only slowly which means that risk asset prices should continue to rise for at least the next six months. However, long-run investors should start shifting to a neutral exposure. Given our economic and policy views, there is a good chance that we will move to an underweight position in risk assets during the second half of 2018. The U.S. economy is already operating above potential and thus does not need any boost from easier fiscal policy. Any major tax cuts risk overheating the economy, encouraging the Federal Reserve to hike interest rates and boosting the probability of a recession in 2019. This is at odds with the popular view that tax cuts will be good for the equity market. A U.S. move to scrap NAFTA would add to downside risks. For the second year in a row, the IMF forecasts of economic growth for the coming year are likely to prove too pessimistic. The end of fiscal austerity has allowed the Euro Area economy to gather steam and this should be sustained in 2018. However, the slow progress in negotiating a Brexit deal with the EU poses a threat to the U.K. economy. China’s economy is saddled with excessive debt and excess capacity in a number of areas. Any other economy would have collapsed by now, but the government has enough control over banking and other sectors to prevent a crisis. Growth should hold above 6% in the next year or two, although much will depend on how aggressively President Xi pursues painful reforms. The market is too optimistic in assuming that the Fed will not raise interest rates by as much as indicated in their “dots” projections. There is a good chance that the U.S. yield curve will become flat or inverted by late 2018. Bonds are not an attractive investment at current yields. Only Greece and Portugal have real 10-year government bond yields above their historical average. Corporate bonds should outperform governments, but a tightening in financial conditions will put these at risk in the second half of 2018. The Euro Area and Japanese equity markets should outperform the U.S. over the next year reflecting their better valuations and more favorable financial conditions. Developed markets should outperform the emerging market index. Historically, the U.S. equity market has led recessions by between 3 and 12 months. If, as we fear, a U.S. recession starts in the second half of 2019, then the stock market would be at risk from the middle of 2018. The improving trend in capital spending should favor industrial stocks. Our other two overweight sectors are energy and financials. The oil price will be well supported by strong demand and output restraint by OPEC and Russia. The Brent price should average $65 a barrel over the coming year, with risks to the upside. We expect base metals prices to trade broadly sideways but will remain highly dependent on developments in China. Modest positions in gold are warranted. Relative economic and policy trends will favor a firm dollar in 2018. Unlike at the start of 2017, investors are significantly short the dollar which is bullish from a contrary perspective. Sterling is quite cheap but Brexit poses downside risks. The key market-relevant geopolitical events to monitor will be fiscal policy and mid-term elections in the U.S., and reform policies in China. With the former, the Democrats have a good chance of winning back control of the House of Representatives, creating a scenario of complete policy gridlock. A balanced portfolio is likely to generate average returns of only 3.3% a year in nominal terms over the next decade. This compares to average returns of around 10% a year between 1982 and 2017. As already noted, the broad theme that policy tightening – especially in the U.S. – would become a problem for asset markets during the year was supported by events. However, the exact timing was hard to predict. The indexes for non-U.S. developed equity markets and emerging markets peaked in late-January 2018, and have since dropped by around 18% and 24%, respectively (Chart 1). On the other hand, the U.S. market, after an early 2018 sell-off, hit a new peak in September, before falling anew in the past couple of months. The MSCI All-Country World index currently is about 6% below end-2017 levels in local-currency terms. Chart 1Our 'Collision Course' Theme For 2018 Played Out

Our 'Collision Course' Theme For 2018 Played Out

Our 'Collision Course' Theme For 2018 Played Out

We started the year recommending an overweight in developed equity markets but, as you noted, shifted that to a neutral position mid-year. A year ago, we thought we might move to an underweight stance in the second half of 2018 but decided against this because U.S. fiscal stimulus boosted corporate earnings and extended the economic cycle. Our call that emerging markets would underperform was on target. Although it was U.S. financial conditions that tightened the most, Wall Street was supported by the large cut in the corporate tax rate while the combination of higher bond yields and dollar strength was a major problem for many indebted emerging markets. Overall, it was not a good year for financial markets (Table 1). Table 1Market Performance

OUTLOOK 2019: Late-Cycle Turbulence

OUTLOOK 2019: Late-Cycle Turbulence

As far as the overall macro environment was concerned, we were correct in predicting that the IMF was too pessimistic on economic growth. A year ago, the IMF forecast that the advanced economies would expand by 2% in 2018 and that has since been revised up to 2.4% (Table 2). This offset a slight downgrading to the performance of emerging economies. The U.S., Europe and Japan all grew faster than previously expected. Not surprisingly, inflation also was higher than forecast, although in the G7, it has remained close to the 2% level targeted by most central banks. Table 2IMF Economic Forecasts

OUTLOOK 2019: Late-Cycle Turbulence

OUTLOOK 2019: Late-Cycle Turbulence

Despite widespread fears to the contrary, the data have supported our view that Chinese growth would hold above a 6% pace in 2018. Nevertheless, a slowdown currently is underway and downside risks remain very much in place in terms of excessive credit and trade pressures. Another difficult year lies ahead for the Chinese authorities and we will no doubt return to this topic later. As far as our other key forecasts are concerned, we were correct in our views that oil prices and the U.S. dollar would rise and that the market would be forced to revise up its predictions of Fed rate hikes. Of course, oil has recently given back its earlier gains, but we assume that is a temporary setback. On the sector front, our macro views led us to favor industrials, financials and energy, but that did not work out well as concerns about trade took a toll on cyclical sectors. Overall, there were no major macro surprises in 2018, and it seems clear that we have yet to resolve the key questions and issues that we discussed a year ago. At that time, we were concerned about the development of late-cycle pressures that ultimately would undermine asset prices. That story has yet to fully play out. It is hard to put precise timing on when the U.S. economy will peak and, thus, when asset prices will be at maximum risk. Nevertheless, our base case is that there likely will be a renewed and probably final run-up in asset prices before the next recession. Late-Cycle Challenges Mr. X: This seems like déjà-vu all over again. Since we last met, the cycle is one year older and, as you just said, the underlying challenges facing economies and markets have not really changed. If anything, things are even worse: Global debt levels are higher, inflation pressures more evident, Fed policy is moving closer to restrictive territory and protectionist policies have ratcheted up. If it was right to be cautious six months ago, then surely we should be even more cautious now. Ms. X: Oh dear, it does seem like a repeat of last year’s discussion because, once again, I am more optimistic than my father. Obviously, there are structural problems in a number of countries and, at some point, the global economy will suffer another recession. But timing is everything, and I attach very low odds to a downturn in the coming year. Meanwhile, I see many pockets of value in the equity market. Rather than cut equity positions, I am inclined to look for buying opportunities. BCA: We sympathize with your different perspectives because the outlook is complex and we also have lively debates about the view. The global equity index currently is a little below where it was when we met last year, but there has been tremendous intra-period volatility. That pattern seems likely to be repeated in 2019. In other words, it will be important to be flexible about your investment strategy. You both make good points. It is true that there are several worrying problems regarding the economic outlook, including excessive debt, protectionism and building inflation risks. At the same time, the classic conditions for an equity bear market are not yet in place, and may not be for some time. This leaves us in the rather uncomfortable position of sitting on the fence with regard to risk asset exposure. We are very open to raising exposure should markets weaken further in the months ahead, but also are keeping careful watch for signs that the economic cycle is close to peaking. In other words, it would be a mistake to lock in a 12-month strategy right now. Mr. X: I would like to challenge the consensus view, shared by my daughter, that the next recession will not occur before 2020, and might even be much later. The main rationale seems to be that the policy environment remains accommodative and there are none of the usual imbalances that occur ahead of recessions. Of course, U.S. fiscal policy has given a big boost to growth in the past year, but I assume the effects will wear off sharply in 2019. More importantly, there is huge uncertainty about the level of interest rates that will trigger economic problems. It certainly has not taken much in the way of Fed rate hikes to rattle financial markets. Thus, monetary policy may become restrictive much sooner than generally believed. I also strongly dispute the idea that there are no major financial imbalances. If running U.S. federal deficits of $1 trillion in the midst of an economic boom is not an imbalance, then I don’t know what is! At the same time, the U.S. corporate sector has issued large amounts of low-quality debt, and high-risk products such as junk-bond collateralized debt obligations have made an unwelcome reappearance. It seems that the memories of 2007-09 have faded. It is totally normal for long periods of extremely easy money to be accompanied by growing leverage and increasingly speculative financial activities, and I don’t see why this period should be any different. And often, the objects of speculation are not discovered until financial conditions become restrictive. Finally, there are huge risks associated with rising protectionism, the Chinese economy appears to be struggling, Italy’s banks are a mess, and the Brexit fiasco poses a threat to the U.K. economy. Starting with the U.S., please go ahead and convince me why a recession is more than a year away. BCA: It is natural for you to worry that a recession is right around the corner. The current U.S. economic expansion will become the longest on record if it makes it to July 2019, at which point it will surpass the 1990s expansion. Economists have a long and sad history of failing to forecast recessions. Therefore, a great deal of humility is warranted when it comes to predicting the evolution of the business cycle. The Great Recession was one of the deepest downturns on record and the recovery has been fairly sluggish by historic standards. Thus, it has taken much longer than usual for the U.S. economy to return to full employment. Looking out, there are many possible risks that could trip up the U.S. economy but, for the moment, we see no signs of recession on the horizon (Chart 2). For example, the leading economic indicator is still in an uptrend, the yield curve has not inverted and our monetary indicators are not contracting. Our proprietary recession indicator also suggests that the risk is currently low, although recent stock market weakness implies some deterioration. Chart 2Few U.S Recession 'Red Flags'

Few U.S Recession 'Red Flags'

Few U.S Recession 'Red Flags'

The buildup in corporate debt is a cause for concern and we are not buyers of corporate bonds at current yields. However, the impact of rising yields on the economy is likely to be manageable. The interest coverage ratio for the economy as a whole – defined as the profits corporations generate for every dollar of interest paid – is still above its historic average (Chart 3). Corporate bonds are also generally held by non-leveraged investors such as pension funds, insurance companies, and ETFs. The impact of defaults on the economy tends to be more severe when leveraged institutions are the ones that suffer the greatest losses. Chart 3Interest Costs Not Yet A Headwind

Interest Costs Not Yet A Headwind

Interest Costs Not Yet A Headwind

We share your worries about the long-term fiscal outlook. However, large budget deficits do not currently imperil the economy. The U.S. private sector is running a financial surplus, meaning that it earns more than it spends (Chart 4). Not only does this make the economy more resilient, it also provides the government with additional savings with which to finance its budget deficit. If anything, the highly accommodative stance of fiscal policy has pushed up the neutral rate of interest, giving the Fed greater scope to raise rates before monetary policy enters restrictive territory. The impetus of fiscal policy on the economy will be smaller in 2019 than it was in 2018, but it will still be positive (Chart 5). Chart 4The U.S. Private Sector Is Helping To Finance The Fiscal Deficit

The U.S. Private Sector Is Helping To Finance The Fiscal Deficit

The U.S. Private Sector Is Helping To Finance The Fiscal Deficit

Chart 5U.S. Fiscal Policy Still Stimulative In 2019

U.S. Fiscal Policy Still Stimulative In 2019

U.S. Fiscal Policy Still Stimulative In 2019

The risks to growth are more daunting outside the U.S. As you point out, Italy is struggling to contain borrowing costs, a dark cloud hangs over the Brexit negotiations, and China and most other emerging markets have seen growth slow meaningfully. The U.S., however, is a relatively closed economy – it is not as dependent on trade as most other countries. Its financial system is reasonably resilient thanks to the capital its banks have raised over the past decade. In addition, Dodd-Frank and other legislation have made it more difficult for financial institutions to engage in reckless risk-taking. Mr. X: I would never take a benign view of the ability and willingness of financial institutions to engage in reckless behavior, but maybe I am too cynical. Even if you are right that debt does not pose an immediate threat to the market, surely it will become a huge problem in the next downturn. If the U.S. federal deficit is $1 trillion when the economy is strong, it is bound to reach unimaginable levels in a recession. And, to make matters worse, the Federal Reserve may not have much scope to lower interest rates if they peak at a historically low level in the next year or so. What options will policymakers have to respond to the next cyclical downturn? Is there a limit to how much quantitative easing central banks can do? BCA: The Fed is aware of the challenges it faces if the next recession begins when interest rates are still quite low. Raising rates rapidly in order to have more “ammunition” for counteracting the downturn would hardly be the best course of action as this would only bring forward the onset of the recession. A better strategy is to let the economy overheat a bit so that inflation rises. This would allow the Fed to push real rates further into negative territory if the recession turns out to be severe. There is no real limit on how much quantitative easing the Fed can undertake. The FOMC will undoubtedly turn to asset purchases and forward guidance again during the next economic downturn. Now that the Fed has crossed the Rubicon into unorthodox monetary policy without generating high inflation, policymakers are likely to try even more exotic policies, such as price-level targeting. The private sector tends to try to save more during recessions. Thus, even though the fiscal deficit would widen during the next downturn, there should be plenty of buyers for government debt. However, once the next recovery begins, the Fed may feel increasing political pressure to keep rates low in order to allow the government to maintain its desired level of spending and taxes. The Fed guards its independence fiercely, but in a world of increasingly political populism, that independence may begin to erode. This will not happen quickly, but to the extent that it does occur, higher inflation is likely to be the outcome. Ms. X: I would like to explore the U.S.-China dynamic a bit more because I see that as one of the main challenges to my more optimistic view. I worry that President Trump will continue to take a hard line on China trade because it plays well with his base and has broad support in Congress. And I equally worry that President Xi will not want to be seen giving in to U.S. bullying. How do you see this playing out? BCA: Investors hoping that U.S. President Donald Trump and his Chinese counterpart Xi Jinping will reach a deal to end the trade war on the sidelines of the forthcoming G20 leaders' summit in Buenos Aires are likely to be disappointed. President Trump's fiscal policy is completely inconsistent with his trade agenda. Fiscal stimulus in a full-employment economy will suck in imports. It also forces the Fed to raise rates more aggressively than it otherwise would, leading to a stronger dollar. The result will be a larger U.S. trade deficit. Trump will not be able to blame Canada or Mexico for a deteriorating trade position because he just signed a trade agreement with them. The new USMCA agreement is remarkably similar to NAFTA, with the notable exception that it contains a clause barring Canada and Mexico from negotiating bilateral trade deals with China. This means Trump needs a patsy who will take the blame for America's burgeoning trade deficit and China will fill that role. For his part, President Xi knows full well that he will still be China’s leader when Trump is long gone. Giving in to Trump’s demands would hurt him politically. All this means that the trade war will persist. Mr. X: I see a trade war as a major threat to the economy, but it is not the only thing that could derail the economic expansion. Let’s explore that issue in more detail. The Economic Outlook Mr. X: You have shown in previous research that housing is often a very good leading indicator of the U.S. economy, largely because it is very sensitive to changes in the monetary environment. Are you not concerned about the marked deterioration in recent U.S. housing data? BCA: Recent trends in housing have indeed been disappointing, with residential investment acting as a drag on growth for three consecutive quarters. The weakness has been broad-based with sales, the rate of price appreciation of home prices, and builder confidence all declining (Chart 6). Even though the level of housing affordability is decent by historical standards, there has been a fall in the percentage of those who believe that it is a good time to buy a home. Chart 6Recent Softness In U.S. Housing

Recent Softness In U.S. Housing

Recent Softness In U.S. Housing

There are a few possible explanations for the weakness. First, the 2007-09 housing implosion likely had a profound and lasting impact on the perceived attractiveness of home ownership. The homeownership rate for people under 45 has remained extremely low by historical standards. Secondly, increased oversight and tighter regulations have curbed mortgage supply. Finally, the interest rate sensitivity of the sector may have increased with the result that even modest increases in the mortgage rate have outsized effects. That, in turn, could be partly explained by recent tax changes that capped the deduction on state and local property taxes, while lowering the limit on the tax deductibility of mortgage interest. The trend in housing is definitely a concern, but the odds of a further major contraction seem low. Unlike in 2006, the home vacancy rate stands near record levels and the same is true for the inventory of homes. The pace of housebuilding is below the level implied by demographic trends and consumer fundamentals are reasonably healthy. The key to the U.S. economy lies with business investment and consumer spending and these areas are well supported for the moment. Consumers are benefiting from continued strong growth in employment and a long overdue pickup in wages. Meanwhile, the ratio of net worth-to-income has surpased the previous peak and the ratio of debt servicing-to-income is low (Chart 7). Last year, we expressed some concern that the depressed saving rate might dampen spending, but the rate has since been revised substantially higher. Based on its historical relationship with U.S. household net worth, there is room for the saving rate to fall, fueling more spending. Real consumer spending has grown by 3% over the past year and there is a good chance of maintaining that pace during most of 2019. Chart 7U.S. Consumer Fundamentals Are Healthy

U.S. Consumer Fundamentals Are Healthy

U.S. Consumer Fundamentals Are Healthy

Turning to capital spending, the cut in corporate taxes was obviously good for cash flow, and surveys show a high level of business confidence. Moreover, many years of business caution toward spending has pushed up the average age of the nonresidential capital stock to the highest level since 1963 (Chart 8). Higher wages should also incentivize firms to invest in more machinery. Absent some new shock to confidence, business investment should stay firm during the next year. Chart 8An Aging Capital Stock

An Aging Capital Stock

An Aging Capital Stock

Overall, we expect the pace of U.S. economic growth to slow from its recent strong level, but it should hold above trend, currently estimated to be around 2%. As discussed earlier, that means capacity pressures will intensify, causing inflation to move higher. Ms. X: I share the view that the U.S. economy will continue to grow at a healthy pace, but I am less sure about the rest of the world. BCA: You are right to be concerned. We expected U.S. and global growth to diverge in 2018, but not by as much as occurred. Several factors have weighed on CEO confidence outside of the U.S., including trade wars, a strong dollar, higher oil prices, emerging market turbulence, the return of Italian debt woes, and a slowdown in the Chinese economy. The stress has shown up in the global manufacturing PMI, although the latter is still at a reasonably high level (Chart 9). Global export growth is moderating and the weakness appears to be concentrated in capex. Capital goods imports for the major economies, business investment, and the production of investment-related goods have all decelerated this year. Chart 9Global Manufacturing Slowdown

Global Manufacturing Slowdown

Global Manufacturing Slowdown

Our favorite global leading indicators are also flashing yellow (Chart 10). BCA’s global leading economic indicator has broken below the boom/bust line and its diffusion index suggests further downside. The global ZEW composite and the BCA boom/bust indicator are both holding below zero. Chart 10Global Growth Leading Indicators

Global Growth Leading Indicators

Global Growth Leading Indicators

Current trends in the leading indicators shown in Chart 11 imply that the growth divergence between the U.S. and the rest of the world will remain a key theme well into 2019. Among the advanced economies, Europe and Japan are quite vulnerable to the global soft patch in trade and capital spending. Chart 11Global Economic Divergence Will Continue

Global Economic Divergence Will Continue

Global Economic Divergence Will Continue

The loss of momentum in the Euro Area economy, while expected, has been quite pronounced. Part of this is due to the dissipation of the 2016/17 economic boost related to improved health in parts of the European banking system that sparked a temporary surge in credit growth. The tightening in Italian financial conditions following the government’s budget standoff with the EU has weighed on overall Euro Area growth. Softer Chinese demand for European exports, uncertainties related to U.S. trade policy and the torturous Brexit negotiations, have not helped the situation. Real GDP growth decelerated to close to a trend pace by the third quarter of 2018. The manufacturing PMI has fallen from a peak of 60.6 in December 2017 to 51.5, mirroring a 1% decline in the OECD’s leading economic indicator for the region. Not all the economic news has been bleak. Both consumer and industrial confidence remain at elevated levels according to the European Commission (EC) surveys, consistent with a resumption of above-trend growth. Even though exports have weakened substantially from the booming pace in 2017, the EC survey on firms’ export order books remains at robust levels (Chart 12). Importantly for the Euro Area, the bank credit impulse has moved higher.The German economy should also benefit from a rebound in vehicle production which plunged earlier this year following the introduction of new emission standards. Chart 12Europe: Slowing, But No Disaster

Europe: Slowing, But No Disaster

Europe: Slowing, But No Disaster

We interpret the 2018 Euro Area slowdown as a reversion-to-the-mean rather than the start of an extended period of sub-trend growth. Real GDP growth should fluctuate slightly above trend pace through 2019. Given that the Euro Area’s output gap is almost closed, the ECB will not deviate from its plan to end its asset purchase program by year end. Gradual rate hikes should begin late in 2019, assuming that inflation is closer to target by then. In contrast, the Bank of Japan (BoJ) is unlikely to change policy anytime soon. The good news is that wages have finally begun to grow at about a 2% pace, although it required extreme labor shortages. Yet, core inflation is barely positive and long-term inflation expectations are a long way from the 2% target. The inflation situation will have to improve significantly before the BoJ can consider adjusting or removing the Yield Curve Control policy. This is especially the case since the economy has hit a bit of an air pocket and the government intends to raise the VAT in 2019. Japan’s industrial production has stalled and we expect the export picture to get worse before it gets better. We do not anticipate any significant economic slack to develop, but even a sustained growth slowdown could partially reverse the gains that have been made on the inflation front. Ms. X: We can’t talk about the global economy without discussing China. You have noted in the past how the authorities are walking a tightrope between trying to unwind the credit bubble and restructure the economy on the one hand, and prevent a destabilizing economic and financial crisis on the other. Thus far, they have not fallen off the tightrope, but there has been limited progress in resolving the country’s imbalances. And now the authorities appear to be stimulating growth again, risking an even bigger buildup of credit. Can it all hold together for another year? BCA: That’s a very good question. Thus far, there is not much evidence that stimulus efforts are working. Credit growth is still weak and leading economic indicators have not turned around (Chart 13). There is thus a case for more aggressive reflation, but the authorities also remain keen to wean the economy off its addiction to debt. Chart 13China: No Sign Of Reacceleration

China: Credit Impulse Remains Weak

China: Credit Impulse Remains Weak

Waves of stimulus have caused total debt to soar from 140% of GDP in 2008 to about 260% of GDP at present (Chart 14). As is usually the case, rapid increases in leverage have been associated with a misallocation of capital. Since most of the new credit has been used to finance fixed-asset investment, the result has been overcapacity in a number of areas. For example, the fact that 15%-to-20% of apartments are sitting vacant is a reflection of overbuilding. Meanwhile, the rate of return on assets in the state-owned corporate sector has fallen below borrowing costs. Chart 14China: Debt Still Rising

China: Debt Still Rising

China: Debt Still Rising

Chinese exports are holding up well so far, but this might only represent front-running ahead of the implementation of higher tariffs. Judging from the steep drop in the export component of both the official and private-sector Chinese manufacturing PMI, exports are likely to come under increasing pressure over the next few quarters as the headwinds from higher tariffs fully manifest themselves (Chart 15). Chart 15Chinese Exports About To Suffer

Chinese Exports About To Suffer

Chinese Exports About To Suffer

The most likely outcome is that the authorities will adjust the policy dials just enough to stabilize growth sometime in the first half of 2019. The bottoming in China’s broad money impulse offers a ray of hope (Chart 16). Still, it is a tentative signal at best and it will take some time before this recent easing in monetary policy shows up in our credit impulse measure and, later, economic growth. A modest firming in Chinese growth in the second half of 2019 would provide a somewhat stronger demand backdrop for commodities and emerging economies that sell goods to China. Chart 16A Ray Of Hope From Broad Money

bca.bca_mp_2018_12_01_c16

bca.bca_mp_2018_12_01_c16

Ms. X: If you are correct about a stabilization in the Chinese economy next year, this presumably would be good news for emerging economies, especially if the Fed goes on hold. EM assets have been terribly beaten down and I am looking for an opportunity to buy. BCA: Fed rate hikes might have been the catalyst for the past year’s pain in EM assets, but it is not the underlying problem. As we highlighted at last year’s meeting, the troubles for emerging markets run much deeper. Our long-held caution on emerging economies and markets is rooted in concern about deteriorating fundamentals. Excessive debt is a ticking time bomb for many of these countries; EM dollar-denominated debt is now as high as it was in the late 1990s as a share of both GDP and exports (Chart 17). Moreover, the declining long-term growth potential for emerging economies as a group makes it more difficult for them to service the debt. The structural downtrend in EM labor force and productivity growth underscores that trend GDP growth has collapsed over the past three decades (Chart 17, bottom panel). Chart 17EM Debt A Problem Given Slowing Supply-Side...

EM Debt A Problem Given Slowing Supply-Side...

EM Debt A Problem Given Slowing Supply-Side...

Decelerating global growth has exposed these poor fundamentals. EM sovereign spreads have moved wider in conjunction with falling PMIs and slowing industrial production and export growth. And it certainly does not help that the Fed is tightening dollar-based liquidity conditions. EM equities usually fall when U.S. financial conditions tighten (Chart 18). Chart 18...And Tightening Financial Conditions

...And Tightening Financial Conditions

...And Tightening Financial Conditions

Chart 19 highlights the most vulnerable economies in terms of foreign currency funding requirements, and foreign debt-servicing obligations relative to total exports. Turkey stands out as the most vulnerable, along with Argentina, Brazil, Indonesia, Chile, and Colombia. In contrast, Emerging Asia appears to be in better shape relative to the crisis period of the late 1990s. Chart 19Spot The Outliers

OUTLOOK 2019: Late-Cycle Turbulence

OUTLOOK 2019: Late-Cycle Turbulence

The backdrop for EM assets is likely to get worse in the near term, given our view that the Fed will continue to tighten and China will be cautious about stimulating more aggressively. Our base case outlook sees some relief in the second half of 2019, but it is more of a “muddle-through” scenario than a V-shaped economic recovery. Mr. X: Perhaps EM assets could enjoy a bounce next year if the Chinese economy stabilizes, but the poor macro fundamentals you mentioned suggest that it would be a trade rather than a buy-and-hold proposition. I am inclined to avoid the whole asset class in 2019. Bond Market Prospects Ms. X: Let’s turn to fixed income now. I was bearish on bonds in 2018, but yields have risen quite a bit, at least in the United States. The Fed has lifted the fed funds rate by 100 basis points over the past year and I don’t see a lot of upside for inflation. So perhaps yields have peaked and will move sideways in 2019, which would be good for stocks in my view. BCA: Higher yields have indeed improved bond value recently. Nonetheless, they are not cheap enough to buy at this point (Chart 20). The real 10-year Treasury yield, at close to 1%, is still depressed by pre-Lehman standards. Long-term real yields in Germany and Japan remain in negative territory at close to the lowest levels ever recorded. Chart 20Real Yields Still Very Depressed

Real Yields Still Very Depressed

Real Yields Still Very Depressed

We called the bottom in global nominal bond yields in 2016. Our research at the time showed that the cyclical and structural factors that had depressed yields were at an inflection point, and were shifting in a less bond-bullish direction. Perhaps most important among the structural factors, population aging and a downward trend in underlying productivity growth resulted in lower equilibrium bond yields over the past couple of decades. Looking ahead, productivity growth could stage a mild rebound in line with the upturn in the growth rate of the capital stock (Chart 21). As for demographics, the age structure of the world population is transitioning from a period in which aging added to the global pool of savings to one in which aging is beginning to drain that pool as people retire and begin to consume their nest eggs (Chart 22). The household saving rates in the major advanced economies should trend lower in the coming years, placing upward pressure on equilibrium global bond yields. Chart 21Productivity Still Has Some Upside

Productivity Still Has Some Upside

Productivity Still Has Some Upside

Chart 22Demographics Past The Inflection Point

Demographics Past The Inflection Point

Demographics Past The Inflection Point

Cyclical factors are also turning against bonds. U.S. inflation has returned to target and the Fed is normalizing short-term interest rates. The market currently is priced for only one more rate hike after December 2018 in this cycle, but we see rates rising more than that. Treasury yields will follow as market expectations adjust. Long-term inflation expectations are still too low in the U.S. and most of the other major economies to be consistent with central banks’ meeting their inflation targets over the medium term. As actual inflation edges higher, long-term expectations built into bond yields will move up. The term premium portion of long-term bond yields is also too low. This is the premium that investors demand to hold longer-term bonds. Our estimates suggest that the term premium is still negative in the advanced economies outside of the U.S., which is not sustainable over the medium term (Chart 23). Chart 23Term Premia Are Too Low

Term Premia Are Too Low

Term Premia Are Too Low

We expect term premia to rise for two main reasons. First, investors have viewed government bonds as a good hedge for their equity holdings because bond prices have tended to rise when stock prices fell. Investors have been willing to pay a premium to hold long-term bonds to benefit from this hedging effect. But the correlation is now beginning to change as inflation and inflation expectations gradually adjust higher and output gaps close. As the hedging benefit wanes, the term premium should rise back into positive territory. Second, central bank bond purchases and forward guidance have depressed yields as well as interest-rate volatility. The latter helped to depress term premia in the bond market. This effect, too, is beginning to unwind. The Fed is letting its balance sheet shrink by about $50 billion per month. The Bank of England has kept its holdings of gilts and corporate bonds constant for over a year, while the ECB is about to end asset purchases. The Bank of Japan continues to buy assets, but at a much reduced pace. All this means that the private sector is being forced to absorb a net increase in government bonds for the first time since 2014 (Chart 24). Chart 25 shows that bond yields in the major countries will continue to trend higher as the rapid expansion of central bank balance sheets becomes a thing of the past. Chart 24Private Sector To Absorb More Bonds

OUTLOOK 2019: Late-Cycle Turbulence

OUTLOOK 2019: Late-Cycle Turbulence

Chart 25QE Unwind Will Weigh On Bond Prices

QE Unwind Will Weigh On Bond Prices

QE Unwind Will Weigh On Bond Prices

Ms. X: I’m not a fan of bonds at these levels, but that sounds overly bearish to me, especially given the recent plunge in oil prices. BCA: Lower oil prices will indeed help to hold down core inflation to the extent that energy prices leak into non-energy prices in the near term. Nonetheless, in the U.S., this effect will be overwhelmed by an overheated economy. From a long-term perspective, we believe that investors still have an overly benign view of the outlook for yields. The market expects that the 10-year Treasury yield in ten years will only be slightly above today’s spot yield, which itself is still very depressed by historical standards (Chart 26). And that also is the case in the other major bond markets. Chart 26Forward Yields Are Too Low

Forward Yields Are Too Low

Forward Yields Are Too Low

Of course, it will not be a straight line up for yields – there will be plenty of volatility. We expect the 10-year Treasury yield to peak sometime in 2019 or early 2020 in the 3.5%-to-4% range, before the next recession sends yields temporarily lower. Duration should be kept short at least until the middle of 2019, with an emphasis on TIPS relative to conventional Treasury bonds. We will likely downgrade TIPS versus conventionals once long-term inflation expectations move into our target range, which should occur sometime during 2019. The ECB and Japan will not be in a position to raise interest rates for some time, but the bear phase in U.S. Treasurys will drag up European and Japanese bond yields (at the very long end of the curve for the latter). Total returns are likely to be negative in all of the major bond markets in 2019. Real 10-year yields in all of the advanced economies are still well below their long-term average, except for Greece, Italy and Portugal (Chart 27). Chart 27Valuation Ranking Of Developed Bond Markets

OUTLOOK 2019: Late-Cycle Turbulence

OUTLOOK 2019: Late-Cycle Turbulence

Within global bond portfolios, we recommend being underweight bond markets where central banks are in a position to raise short-term interest rates (the U.S. and Canada), and overweight those that are not (Japan and Australia). The first ECB rate hike is unlikely before the end of 2019. However, the imminent end of the asset purchase program argues for no more than a benchmark allocation to core European bond markets within global fixed-income portfolios, especially since real 10-year yields in parts of continental Europe are the furthest below their long-term average. We are overweight gilts at the moment, but foresee shifting to underweight in 2019, depending on how Brexit plays out. Ms. X: What about corporate bonds? I know that total returns for corporates will be poor if government bond yields are rising. But you recommended overweighting corporate bonds relative to Treasurys last year. Given your view that the next U.S. recession is more than a year away, it seems reasonable to assume they will outperform government bonds. BCA: We were overweight corporates in the first half of 2018, but took profits in June and shifted to neutral at the same time that we downgraded our equity allocation. Spreads had tightened to levels that did not compensate investors for the risks. Recent spread widening has returned some value to U.S. corporates. The 12-month breakeven spreads for A-rated and Baa-rated corporate bonds are almost back up to their 50th percentile relative to history (Chart 28). Still, these levels are not attractive enough to justify buying based on valuation alone. As for high-yield, any rise in the default rate would quickly overwhelm the yield pickup in this space. Chart 28Corporate Bond Yields Still Have Upside

Corporate Bond Yields Still Have Upside