Sectors

Despite a stellar Q3 earnings print, the S&P 500 had a terrible October as EPS continues to do the hard work in lifting the market (Chart 1). Chart 1EPS Doing The Heavy Lifting

EPS Doing The Heavy Lifting

EPS Doing The Heavy Lifting

We bought the dip,1 consistent with our view of deploying longer term oriented capital were a 10% pullback to occur, given our view of no recession for the next 9 to 12 months.2 Financials and industrials should lead the next leg up and we believe a rotation into these beaten up stocks is going to materialize in the coming months. On the flip side, as volatility is making a comeback and the fed is on a path to lift rates to 3% by June of next year, fixed income proxies and consumer discretionary stocks should be avoided and a preference for large caps over small caps should be maintained (Chart 2). Chart 2The Return Of Vol May Spoil The Party

The Return Of Vol May Spoil The Party

The Return Of Vol May Spoil The Party

Further, a valuation reset has taken hold, pushed by the surprising rise of the equity risk premium over the course of the past two years, representing a surge in negative sentiment from investors, despite the usually tight inverse correlation with the ISM, the core sentiment indicator of the manufacturing economy (Chart 3). Chart 3ERP And The Economy Are Inversely Correlated

ERP And The Economy Are Inversely Correlated

ERP And The Economy Are Inversely Correlated

Nevertheless, while everyone is focusing on the euphoric above trend growth of the U.S. economy, a risk lurking beneath the surface is a domestic economic soft patch.3 We have likely stolen demand from the future and brought consumption forward especially with the stock market related fiscal easing that is front loaded to 2018 and less so for next year. On that front our Economic Impulse Indicator is warning that the U.S. economy cannot grow at such a pace, unless a bipartisan divide can be crossed to deliver enough firepower to rekindle GDP growth (Chart 4). Chart 4Economic Impulse Yellow Flag

Economic Impulse Yellow Flag

Economic Impulse Yellow Flag

Further, at least part of the blame for higher volatility rests with increasing trade uncertainty as the Trump administration has pursued an aggressive trade policy. Still, the evidence so far indicates that any trade weakness has been borne disproportionately by the rest of the world, to the U.S.' benefit (Charts 5 & 6). Chart 5U.S. Is Winning The Trade War

U.S. Is Winning The Trade War

U.S. Is Winning The Trade War

Chart 6U.S. Has The Upper Hand

U.S. Has The Upper Hand

U.S. Has The Upper Hand

We remain cognizant of a few key risks to our sanguine U.S. equity view. Principal among these is the rising U.S. dollar and its eventual infiltration into S&P 500 earnings, which has thus far been muted (Chart 7). Chart 7Watch The U.S. Dollar

Watch The U.S. Dollar

Watch The U.S. Dollar

Further, a softening housing market bodes ill for U.S. economic growth. This is the first time since the GFC that residential investment's contribution to real GDP growth turned negative for three consecutive quarters (Chart 8). Chart 8Peak Housing

Peak Housing

Peak Housing

Chris Bowes, Associate Editor chrisb@bcaresearch.com 1 Please see BCA U.S. Equity Strategy Daily Insight, "Time To Bargain Hunt," dated October 26, 2018, available at uses.bcaresearch.com. 2 Please see BCA U.S. Equity Strategy Weekly Report, "The "FIT" Market," dated October 9, 2018, available at uses.bcaresearch.com. 3 Please see BCA U.S. Equity Strategy Weekly Report, "Critical Reset," dated October 29, 2018, available at uses.bcaresearch.com. S&P Financials (Overweight) Unchanged from its trajectory when we updated our cyclical indicators earlier this year, the S&P financials CMI has continued to accelerate. A historically low unemployment rate, combined with unusually resilient economic growth, underpin the surge in the CMI to its highest levels post-GFC. Further goosing the indicator, particularly with respect to the core banks sub-sector, is the recent rise in Treasury yields and a modest steepening in the yield curve both of which bode well for bank profits. However, financials have not responded to this exceptionally bullish data the way we expected, with worries over future loan growth fully offsetting the positive backdrop; financials have been falling throughout 2018. Still, inflation is threatening to rise (albeit gradually) and a selloff looms in the bond market. We highlighted earlier this fall that sectors who benefit from rising interest rates while serving as inflation hedges should outperform against this backdrop. Cue the return of S&P financials. As shown in Chart 10, the S&P financials index has shown a historically strong positive correlation with interest rates and inflation expectations and we expect the recent divergence to be closed via a catch-up in the former. As noted above, bearishness has reigned in 2018 and the result has been a steep fall in our valuation indicator (VI) to more than one standard deviation below normal while our technical indicator (TI) is deep in oversold territory. Chart 9S&P Financials (Overweight)

S&P Financials (Overweight)

S&P Financials (Overweight)

Chart 10Financials Are Trailing Rates

Financials Are Trailing Rates

Financials Are Trailing Rates

S&P Industrials (Overweight) S&P industrials, much like their cyclical brethren S&P financials, benefit from higher interest rates and also serve as hedges against rising inflation. As we have noted in recent research, industrials are levered to the commodity cycle and thus represent an indirect inflation hedge. This hedge only becomes problematic when industrials stocks are unable to pass these rising commodity costs through to the consumer. As shown in Chart 12, pricing power is not yet an issue for these deep cyclicals. Given the positive macro backdrop for S&P industrials, the CMI has risen to new cyclical highs. Despite the forgoing, fears over trade wars and tariff-driven higher input costs, combined with slowing global demand for capital goods, have weighed on the index. The result is that S&P industrials remain deeply oversold on a technical basis while hovering around the neutral line from a valuation perspective. We reiterate our overweight recommendation. Chart 11S&P Industrials (Overweight)

S&P Industrials (Overweight)

S&P Industrials (Overweight)

Cjart 12Resilient Industrials Pricing Power

Resilient Industrials Pricing Power

Resilient Industrials Pricing Power

S&P Energy (Overweight, High-Conviction) Our energy CMI has moved horizontally since our last update of the cyclical macro indicators. However, this followed a snap-back recovery from the extremely depressed levels of 2016 and 2017. Nevertheless, the S&P energy index has moved sideways in line with the CMI. Energy stocks have significantly trailed crude oil prices since the latter broke out roughly a year ago (Chart 14). Disbelief in the longevity of the increase in oil prices is the likely culprit weighing on the index, along with a bottleneck-induced steep shale oil price discount to WTI. There are high odds that a catch up phase looms, especially if BCA's Commodity & Energy Strategy service's view of a looming oil price spike materializes, and we reiterate our overweight recommendation. Our VI has been hovering at one standard deviation below fair value, while our TI trending into oversold territory. Chart 13S&P Energy (Overweight, High-Conviction)

S&P Energy (Overweight, High-Conviction)

S&P Energy (Overweight, High-Conviction)

Chart 14Crude Prices Are Still Leading The Way

Crude Prices Are Still Leading The Way

Crude Prices Are Still Leading The Way

S&P Consumer Staples (Overweight) Unchanged from our previous update, our consumer staples CMI has moved sideways, near a depressed level. However, share prices have finally been staging the recovery we have anticipated for several years on the back of firm consumer data, solid sector profitability and an overall cyclical rotation into staples. Despite the recent outperformance, both from an earnings and market perspective, consumer staples remain a deeply unloved sector. With respect to the former, earnings growth has outstripped the market's reaction by a wide margin. This is reflected on our VI which only recently rose from one standard deviation below fair value while our TI has only just begun a retreat from oversold territory. Staples' share of retail sales have arrested their steep declines from 2014-2016, which we view as a precursor to a rebound in weak industry sales (top panel, Chart 16). Exports of consumer staples have already been staging a comeback, despite the strengthening of the U.S. dollar which has historically presaged a relative earnings outperformance (middle panel, Chart 16). Considering the already-strong industry return on equity, any relative earnings gains should result in a valuation rerating (third panel, Chart 16). We reiterate our outperform rating on this cyclically defensive index. Chart 15S&P Consumer Staples (Overweight)

S&P Consumer Staples (Overweight)

S&P Consumer Staples (Overweight)

Chart 16Staples Are Making A Comback

Staples Are Making A Comback

Staples Are Making A Comback

S&P Health Care (Neutral) In a mid-summer report , we upgraded the S&P pharma and biotech indexes to neutral which, considering their ~50% weight of the S&P health care index, took our overall recommendation on S&P health care to neutral. In the report, we proffered five reasons why the S&P pharma and biotech indexes were set for a rebound following their precipitous decline from 2016 onwards. These were: firming operating metrics, late cycle dynamics, likelihood of pricing power regulatory relief, the rising U.S. dollar and investor and analyst capitulation. Our timing has proved prescient as the S&P pharma index has been dramatically outperforming since the upgrade (top panel, Chart 18). With respect to pharma's operating metrics, our pharma productivity proxy (industrial production / employment) has been soaring, implying that earnings should surge (second panel, Chart 18). This seems particularly likely as the pace of improvement in drug shipments exceeds inventory growth by a fairly wide margin (third and bottom panels, Chart 18). Despite the upbeat backdrop for pharma, our health care CMI has declined modestly, though remains at a neutral level relative to history. Further, the pharma recovery has taken our VI from undervalued to a neutral position, a reading which is echoed by our TI. Chart 17S&P Health Care (Neutral)

S&P Health Care (Neutral)

S&P Health Care (Neutral)

Chart 18Pharma Strength Is Lifting Health Care

Pharma Strength Is Lifting Health Care

Pharma Strength Is Lifting Health Care

S&P Technology (Neutral) The stratospheric rise of tech profits, particularly in the past two years, have done most of the heavy lifting in pulling the S&P 500's profit margin ever higher (second panel, Chart 20) as well as pushing the index itself to new all-time highs in September. The San Francisco Fed's tech pulse index - an index of coincident indicators of technology sector activity - suggests more profit growth is in the offing (third panel, Chart 20), an intimation repeated by our technology CMI. However, we remain cognizant of three material risks to bullishness in tech. First, the tech sector garners 60% of its revenues from abroad and thus the appreciating U.S. dollar is a significant profit headwind (bottom panel, Chart 20). Second, a rising U.S. inflation backdrop along with the related looming selloff in the bond market should knock the wind out of the tech sector's sails. Third, leading indicators of emerging Asian demand are souring rapidly and were the trade war to re-escalate, EM economic data would retrench further. Lastly, neither our VI nor our TI send particularly compelling messages, as both are on the expensive side of neutral, despite the recent tech selloff. We sustain a barbell portfolio within the sector by recommending an overweight position in the late-cyclical and capex-driven technology hardware, storage & peripherals and software indexes while recommending an underweight position in the early-cyclical semi and semi equipment indexes. Chart 19S&P Technology (Neutral)

S&P Technology (Neutral)

S&P Technology (Neutral)

Chart 20Tech Is King But Beware The U.S. Dollar

Tech Is King But Beware The U.S. Dollar

Tech Is King But Beware The U.S. Dollar

S&P Materials (Neutral) Our materials CMI has recently plumbed new lows, a result of tightening monetary policy and the accompanying selloff in the bond market. As a reminder, the heavyweight chemicals component of the materials index typically sees earnings (and hence stock prices) underperform as real interest rates are moving higher. Despite this negative backdrop, chemicals fundamentals have remained surprisingly resilient. Pricing power has stayed in its multi-year uptrend (second panel, Chart 22) while productivity gains have accelerated, coinciding with an erosion of sell-side bearishness (third panel, Chart 22). Still, chemical production has clearly rolled over (bottom panel, Chart 22) which could lead to a quick reversal of the gains in our productivity proxy and a faltering in rebounding EPS estimates. Combined with BCA's view of rising real interest rates for the next year, this is enough to keep us on the fence. Our VI too shows a neutral reading, though our TI has declined steeply into an oversold position. Chart 21S&P Materials (Neutral)

S&P Materials (Neutral)

S&P Materials (Neutral)

Chart 22Fundamentals In Chemicals Have Improved

Fundamentals In Chemicals Have Improved

Fundamentals In Chemicals Have Improved

S&P Utilities (Underweight) Our utilities CMI is at a 25-year low, driven down by the ongoing backup in interest rates. Such a move is predictable, given that utilities stocks are the closest to perfect fixed income proxies in the equity space. The S&P utilities sector has been enjoying a relative resurgence recently, driven by spiking natural gas prices and a supportive electricity demand backdrop from a roaring economy (ISM survey shown inverted, bottom panel, Chart 24) and, more than anything, a general market retreat into safe haven assets. We recently trimmed our exposure to the sector from neutral to underweight because the S&P utilities sector was yielding 3.5% and the competing risk free asset was near 3.2% and investors would prefer to shed, at the margin, riskier high-yielding equities and park the proceeds in U.S. Treasurys (top panel, Chart 24). Since the run up in S&P utilities without a corresponding decline in Treasury yields, that spread has narrowed. Neither our VI nor our TI send compelling messages as both are in neutral territory, though our bearish thesis on utilities has less to do with their valuation relative to themselves or other equities than to bonds. Chart 23S&P Utilities (Underweight)

S&P Utilities (Underweight)

S&P Utilities (Underweight)

Chart 24Utilities Should Still Be Avoided

Utilities Should Still Be Avoided

Utilities Should Still Be Avoided

S&P Real Estate (Underweight) Our real estate CMI has reversed a recent recovery to set a new decade low; the only time it has shown a lower reading was during the Great Financial Crisis. Excluding the inflating of the property bubble in advance of the GFC, REITs have had a very tight inverse correlation with UST yields; the resulting downward pressure on the S&P REITs index is thus very predictable (top panel, Chart 26). Much like the S&P utilities sector in the previous section, and in the context of BCA's higher interest rate view, we continue to avoid this sector. The rate-driven downward pressure could be overlooked if all was well on an operating basis but this is not the case. Non-residential construction continues to rise (albeit more slowly than last year) in the face of higher borrowing rates (second panel, Chart 26). Further, demand looks slack as occupancy rates clearly crested at the beginning of last year (bottom panel, Chart 26). As well, on the residential front, multi-family housing starts remain elevated which should prove deflationary to rents. Our VI suggests that REITs are fairly valued, which is somewhat surprising given the negative backdrop, while our TI echoes a neutral view. Chart 25S&P Real Estate (Underweight)

S&P Real Estate (Underweight)

S&P Real Estate (Underweight)

Chart 26A Bearish Backdrop For REITs

A Bearish Backdrop For REITs

A Bearish Backdrop For REITs

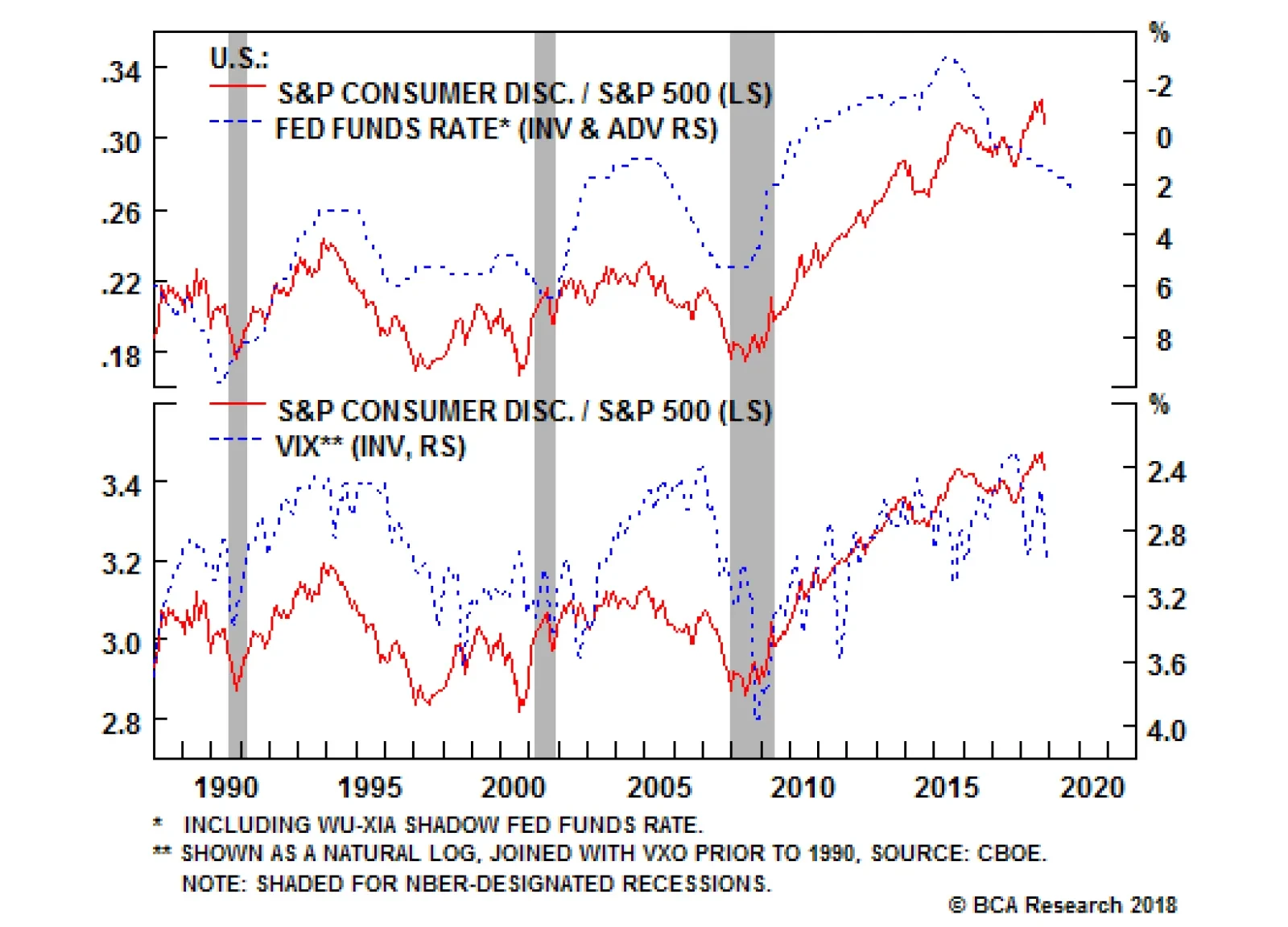

S&P Consumer Discretionary (Underweight) While we remain constructive on financials that benefit from higher rates, we continue to recommend investors avoid the consumer discretionary sector - the other early cyclical - that suffers when interest rates rise. The second panel of Chart 28 depicts this inverse correlation consumer discretionary equities have with interest rates, especially the fed funds rate. Most discretionary equites are levered off of floating rates and thus any increase in the fed funds rates gets reflected immediately in banks' prime lending rate. Also, most consumer debt is floating rate debt and thus tighter monetary conditions, at the margin, dampen consumer debt uptake and as a knock off on effect, weigh on discretionary consumer outlays. Not only are higher interest rates anchoring consumer discretionary stocks but rising energy prices are also dealing a blow to this sector. We show our Consumer Drag Indicator (CDI, comprising mortgage rates and energy prices) in the bottom panel of Chart 28. Historically, our CDI has been an excellent leading indicator of relative share price momentum. Currently, the message is clear: the sinking CDI signals that a bear market in consumer discretionary stocks has likely commenced. All of this is captured by our CMI which has been sinking since the beginning of the year. Meanwhile, our VI has broken out to nearly its highest level ever which we believe is largely a function of the decreasing diversification of the S&P consumer discretionary index as AMZN now represents more than 30% of its market value following the redistribution of the media indexed to the new S&P communication services index. Our TI has been falling from overbought territory recently and now sends a neutral message. Chart 27S&P Consumer Discretionary (Underweight)

S&P Consumer Discretionary (Underweight)

S&P Consumer Discretionary (Underweight)

Chart 28Higher Rates Spell Declines For Consumer Discretionary

Higher Rates Spell Declines For Consumer Discretionary

Higher Rates Spell Declines For Consumer Discretionary

S&P Communication Services (Underweight) As the newly-minted communication services has little more than a month of existence, we do not have adequate history to create a cyclical macro indicator. However, we have created Chart 29 below with a number of valuation indicators, though we caution that they too are less reliable than the other indicators presented in the preceding pages, owing to a dearth of history. Rather, we refer readers to our still-fresh initiation of coverage on the sector and look forward to being able to deliver something more substantive in the future. Chart 29S&P Communication Services (Underweight)

S&P Communication Services (Underweight)

S&P Communication Services (Underweight)

Size Indicator (Favor Large Vs. Small Caps) Our size CMI has been hovering near the boom/bust line, as it has for most of the last two years. Despite the neutral CMI reading, we downgraded small caps earlier this year , and moved to a large cap preference, based on the diverging (and unsustainable) debt levels of small caps vs. their large cap peers (top and second panels, Chart 31). We expect the divergence in leverage and stock price to be rationalized as it usually has: via a fall in the latter. Considering the dramatic valuation gap that has opened between large and small caps, particularly on a Shiller P/E (or cyclically adjusted P/E, CAPE) basis (bottom panel, Chart 31), no space remains for any small cap profit mishaps. Our VI is trending towards small caps being undervalued, though without conviction while our TI is hovering in the neutral zone. Chart 30Size Indicator (Favor Large Vs. Small Caps)

Size Indicator (Favor Large Vs. Small Caps)

Size Indicator (Favor Large Vs. Small Caps)

Chart 31Too Much Debt And High Valuations Should Hurt Small Caps

Too Much Debt And High Valuations Should Hurt Small Caps

Too Much Debt And High Valuations Should Hurt Small Caps

Overweight The S&P consumer finance index, much like their larger financials peers in the S&P banks index, have mostly not participated in the rise in Treasury yields, a relationship that has heretofore been relatively tight (top panel). This is despite credit card interest rate spreads that are pushing close to their post-GFC highs; such moves in the spread have typically heralded bullish sell-side sentiment changes and the current message is no different as earnings estimates have soared (second panel). While rate-driven revenues are climbing, the cost picture remains stable. The credit card delinquency rate has ticked up modestly but remains at severely depressed levels, driven by historically low unemployment (bottom panel). We continue to expect a sector rotation with financials and industrials leading the next phase of the market advance, a result of the bond market selloff gaining steam into year-end and beyond.1 Accordingly, we reiterate our overweight recommendation. The ticker symbols for the stocks in this index are: BLBG: S5CFINX - AXP, DFS, SYF, COF. 1 Please see BCA U.S. Equity Strategy Weekly Report, "The "FIT" Market," dated October 9, 2018, available at uses.bcaresearch.com.

Earnings Are Not The Problem For Consumer Finance

Earnings Are Not The Problem For Consumer Finance

Neutral As a wholly domestic industry, the S&P health care facilities index is well insulated from trade tremors that have been shaking the broad market this year. It is thus understandable that the index has been rallying in 2018. Still, as a particularly labor-intensive industry, rising wages pose a significant risk. On that front, investors have reason to be wary; the employment cost index for hospitals has jumped dramatically in its most recent reading, rising faster than at any point since the financial crisis, now keeping pace with overall payrolls (second panel). Further, job openings are soaring, having doubled in the last five years (third panel) which suggests hospital employment costs have much further to rise. Still, the picture is not all bad. Other input costs, such as the cost of medical equipment and supplies, have fallen steeply and now hover close to the deflation line (bottom panel). This could be enough to sustain margins, everything else being equal. Net, we reiterate our neutral stance on the S&P health care facilities index. The ticker symbols for the stocks in this index are: BLBG: S5HCFA - UHS, HCA.

A Mixed Cost Picture For Health Care Facilities

A Mixed Cost Picture For Health Care Facilities

Feature In the late 1980s, half of the global stock market capitalization resided in Japan Furthermore, almost a third of the Japanese stock market capitalization resided in banks. It followed that to have a view on the global stock market you had to have a view on Japanese banks. Indeed, in 1988, five of the ten largest companies in the world were Japanese banks. Less than ten years later, the weighting of Japanese banks in the global stock market had collapsed to less than one percent, rendering Japanese banks a largely irrelevant part of a global equity portfolio. In the new millennium, it was the turn of European banks to step into the limelight. By 2007, the proportion of the euro area's stock market capitalization in banks had ballooned to a quarter. And then, Europe followed in Japan's footsteps. Today, the weighting of banks in the Euro Stoxx has plunged to around a tenth. Could European banks now become a global investment irrelevance too (Feature Chart)? Feature ChartAre Europe's Banks Following In Japan's Footsteps?

Are Europe's Banks Following In Japan's Footsteps?

Are Europe's Banks Following In Japan's Footsteps?

European banks have performed very poorly. From their peak in 2007, a one dollar investment in euro area banks relative to the world index would now be worth just 15 cents. But Japanese banks have performed abysmally: from their peak in the late 1980s, a one dollar investment in Japanese banks relative to the world index would now be worth a pitiful 3 cents (Chart I-2 and Chart I-3).1 Chart 2Japan Dominated The Global Stock Market In The Late 1980s

Japan Dominated The Global Stock Market In The Late 1980s

Japan Dominated The Global Stock Market In The Late 1980s

Chart 3Banks Have Performed Abysmally

Banks Have Performed Abysmally

Banks Have Performed Abysmally

What turned Japanese bank shares from heroes to zeroes? Some people point to sky-high valuations: in the late 80s, Japanese bank dividend yields dropped below 0.5 percent (Chart I-4), and these high valuations clearly contributed to their subsequent poor investment performance. But this was not the main reason. Chart 4Japanese Banks Offered Miserly Dividend Yields

Japanese Banks Offered Miserly Dividend Yields

Japanese Banks Offered Miserly Dividend Yields

Banks' Lifeblood Is Credit Creation The main reason for the severe underperformance of Japanese banks was that they lost their lifeblood: credit creation. Put simply, if bank assets stop growing structurally, then it is impossible for bank revenues to grow structurally. But in Japan, it was worse: from the 1990s through the mid noughties, private sector indebtedness actually shrank from 220 percent to 160 percent of GDP, and this explains the bulk of the abysmal performance of bank equities (Chart I-5). Chart 5Banks' Lifeblood Is Credit Creation

Banks' Lifeblood Is Credit Creation

Banks' Lifeblood Is Credit Creation

The important lesson is that the structural outlook for bank equities depends first and foremost on the structural outlook for bank credit creation. This is especially true in Europe because the majority of credit intermediation occurs via the banking system rather than via the bond market. So how can we assess the structural outlook for bank credit creation? Basically by noting that there appears to be an upper limit at which all the good lending has been done. Additional bank credit then generates misallocation of capital and mal-investments. At which point, the economy and bank asset quality start to suffer, limiting any further increase in profitable lending. The precise point at which this happens is not set in stone, because high levels of public indebtedness, through 'crowding out', can pull down the limit of productive private indebtedness. And vice-versa. Nevertheless when private indebtedness, as a percentage of GDP, reaches the mid-200s, the evidence suggests that the scope for further growth becomes limited. On this basis, the outlook for bank asset growth in Europe is a mixed bag. In Switzerland, Sweden and Norway, private indebtedness already stands at 250 percent of GDP, implying that the stock of profitable bank assets is close to its upper limit (Chart I-6). Chart 6In Switzerland, Sweden And Norway, Private Indebtedness Is Very High

In Switzerland, Sweden And Norway, Private Indebtedness Is Very High

In Switzerland, Sweden And Norway, Private Indebtedness Is Very High

Meanwhile in the euro area, private indebtedness ratios in the Netherlands and Belgium are already well above 200 percent, and in France at 200 percent. On the other hand, the ratios in Germany and Italy - the largest and third largest euro area economies - are barely above 100 percent (Chart I-7). This bestows on them the honour of the lowest privately indebted major economies in the world (Chart I-8), with considerable theoretical capacity for bank asset growth. Admittedly, Italy has a high level of public indebtedness. Nevertheless, it is hard to deny that if the banking system in Italy could be unfrozen, there is great scope for economically productive lending. Chart 7In Germany And Italy, Private Indebtedness Is Very Low

In Germany And Italy, Private Indebtedness Is Very Low

In Germany And Italy, Private Indebtedness Is Very Low

Chart 8In Japan, Private Indebtedness Has Plunged

In Japan, Private Indebtedness Has Plunged

In Japan, Private Indebtedness Has Plunged

Having said all that, we now turn to something that bank investors everywhere in the world should fear: blockchain. Blockchain Is A Mortal Threat To Banks The internet's major innovation was to decentralize and democratize information. Before the internet, the creation, ownership and dissemination of information was a function centralized to privileged organizations: governments, media and entertainment companies. But after the internet, anybody and everybody could create, receive and share content - and this has proved to be a game changer for the governments, media and entertainment companies that previously owned and/or controlled the information. In the same way, blockchain's major innovation is to decentralize and democratize trust. The Economist even described blockchain as "the trust machine".2 It follows that blockchain will be a game changer for the privileged organizations whose raison d'être is to supply trust and integrity in transactions - essentially, those that act as a middleman. Clearly, one such privileged organization is the banking system, because the banking system is really nothing more than a middleman that provides trust and integrity in the transaction between the people with savings and the people who want to borrow those savings. Granted, banks also assess and price the credit risk of borrowers as well as provide a degree of insurance for savers. But with the prevalence of universal credit scoring systems and compensation schemes, there is a growing tendency to decentralize those functions too. Put simply, blockchain removes the need for a middleman. Until now, counterparties without an established trust relationship could only transact through a middleman who could add the trust and integrity overlay. But once each participant in the transaction trusts the blockchain itself, they no longer need to use a costly intermediary, like a bank. Therefore, just as the internet has revolutionized politics, media and entertainment, it is our very high conviction view that blockchain will revolutionize the way that money, assets and securities are held, transferred and accounted for. And the major casualty will be the banking system as we now know it. Investment Considerations The structural case for European banks is that Germany and Italy - the largest and third largest euro area economies - have considerable scope for bank credit expansion. The structural case against is that the other European economies have very limited scope for bank credit expansion. Furthermore, we confidently predict that within a decade blockchain will have decentralized and democratized financial intermediation, transforming it to something that is unrecognizable from today. Overall, this will not be a good thing for bank investors. With this in mind, German and Italian real estate and real estate equities are a much cleaner structural play on the potential for increased private indebtedness in those economies, whether intermediated by the banking system or not (Chart I-9 and Chart I-10). Chart 9The Evolution Of Private Indebtedness...

European Banks: The Case For And Against

European Banks: The Case For And Against

Chart 10...Drives The Real Estate Market

Drives The Real Estate Market

Drives The Real Estate Market

We end with another important lesson from Japan. Even in a three decade long bear market, the banks had the capacity for countertrend bursts of outperformance from oversold levels, sometimes by as much as 50 percent in a year. This is because even within a structural bear trend, there are cycles of excessive depression. European banks could be ripe for such a countertrend burst of outperformance. This year, European banks sank by 35 percent versus European healthcare. However, the sharp deceleration in global credit growth which dragged them down has now clearly reversed (Chart I-11). On this basis, the next six months could be a countertrend phase: a brief opportunity to own some European banks, at least relative to other equity sectors. Chart 11European Banks Are Ripe For A Burst Of Outperformance

European Banks Are Ripe For A Burst Of Outperformance

European Banks Are Ripe For A Burst Of Outperformance

Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com 1 Performances are calculated in common currency terms. 2 Please see 'the trust machine', The Economist, October 31, 2015.

Highlights China's old economy continues to slow in the leadup to the negative effect of U.S. import tariffs on Chinese export growth. Weaker trade data over the coming few months is likely to weigh further on investor sentiment. Our Li Keqiang leading indicator has risen off of its low, but not in a broad-based fashion. While the RMB depreciation has caused Chinese monetary conditions indexes to move sharply higher, money and credit growth remain weak. The recent breakdown in Chinese consumer staples stocks is an exception to the broad trend of low-beta sector outperformance. Fears have risen that the Chinese consumer is faltering, a concern that we will address in a Special Report next week. Feature Tables 1 and 2 highlight key developments in China's economy and its financial markets over the past month. On the growth front, the September update to Bloomberg's measure of the Li Keqiang index (LKI), and our newly created alternative LKI, makes it clear that China's economy continues to slow in the leadup to the negative shock from the external sector. The fact that both LKIs peaked early in 2017 highlights that the slowdown was precipitated by monetary tightening, which has only recently reversed. This easing in monetary conditions has likely improved the liquidity situation in China, but it remains to be seen whether it will prompt any meaningful acceleration in credit growth. Table 1The Trend In Domestic Demand, And The Outlook For Trade, Is Negative

Checking In On The Data

Checking In On The Data

Table 2Financial Market Performance Summary

Checking In On The Data

Checking In On The Data

From an investment strategy perspective, our recommendations remain unchanged. Despite deeply oversold conditions in China's stock markets, investors should avoid outright long positions for now due to the high odds of additional negative catalysts over the coming few months. We expect further weakness in the RMB, and expect USD-CNY to break through 7, suggesting that investors trading within the Chinese equity universe should only favor domestic stocks in currency-hedged terms for now. Finally, we continue to recommend an overweight stance towards low-beta sectors within the investable market, and believe that onshore corporate bonds are a buy despite pervasive default concerns. In reference to Tables 1 and 2, we provide several detailed observations concerning developments in China's macro and financial market data below: Bloomberg's measure of the Li Keqiang index (LKI) fell in September, confirming that activity in China's old economy is trending lower. A downtrend in industrial activity is even more apparent in our alternative LKI (Chart 1), which is constructed using total freight (instead of railway freight) and secondary industry electricity consumption (instead of overall electricity production). Chart 1China's Old Economy Is Slowing, Before The Trade Shock Hits

China's Old Economy Is Slowing, Before The Trade Shock Hits

China's Old Economy Is Slowing, Before The Trade Shock Hits

Our BCA Li Keqiang leading indicator has risen somewhat from its June low, driven by the two monetary conditions indexes (MCIs) included in the indicator. Both of these MCIs have, in turn, been driven by the substantial weakness in the RMB over the past four months. This sharp improvement has not been matched by the other components of the indicator: Chart 2 illustrates that the low end of the component range remains quite weak, in contrast to mid-2015 when both the high and low ends of the range were in a clear uptrend. Chart 2A Narrow Pickup In Our LKI Leading Indicator

A Narrow Pickup In Our LKI Leading Indicator

A Narrow Pickup In Our LKI Leading Indicator

Nearly all of the housing market indicators included in Table 1 are above their 12-month moving average, with the exception of pledged supplementary lending by the PBOC. Pledged supplementary lending itself sequentially increased quite meaningfully in October, underscoring that policymakers are keen to avoid the risk of overtightening the economy at a time when external demand is likely to weaken considerably. Still, smoothed residential sales volume growth has ticked down for two months in a row, suggesting that the extremely stretched pace of floor space started is likely to moderate over the coming months. Chinese export growth remains buoyant, despite several manufacturing and general business condition surveys showing a substantial deterioration over the past few months. As we go to press, China's October trade data has not yet been released, but we expect exports to weaken considerably in the coming few months. This could further weigh on investor sentiment if the slowdown exceeds the market's expectations. Within China's equity market universe, both domestic and investable stocks are deeply oversold in absolute terms, having declined 30% and 28% from their late-January peaks, respectively. Our technical indicators for both markets suggest that Chinese stocks have actually reached 1 standard deviation oversold, a level that has historically served as a platform for a rebound. Still, this speaks merely to the odds of a rebound, not when one will occur, and we can identify further negative catalysts for the equity over the coming 3 months. Avoid outright long positions for now. Despite having fallen significantly themselves, Taiwan and Hong Kong's equity markets have materially outperformed Chinese investable stocks since the beginning of the year (Chart 3). However, Taiwan's outperformance trend has recently moved in the opposite direction, as global investors begin to price in the fact that tensions between the U.S. and China are strategic and long-term in nature, not merely focused on trade.1 Taiwan is extremely exposed to this rivalry, warranting a higher equity risk premium. Chart 3Taiwan's Recent Outperformance Is Likely Reversing

Taiwan's Recent Outperformance Is Likely Reversing

Taiwan's Recent Outperformance Is Likely Reversing

Within Chinese investable stocks, low-beta equity sectors have in general continued to outperform over the past month. Our long MSC China low-beta sectors / short MSCI China trade is up 10% since initiation on June 27, and we expect further gains in the near-term. One exception to this trend is the relative performance of domestic and investable consumer staples stocks, which have recently underperformed their respective broad markets (Chart 4). The selloff has been sharp in the case of the domestic market, and has been in response to heightened fears that household consumption is weakening, a sector of the economy that heretofore had been reliably strong. In response to these developments, please note that BCA's China Investment Strategy service will be publishing a Special Report outlook detailing the outlook for the Chinese consumer next week. Chart 4Fears About Chinese Consumers Are Growing

Fears About Chinese Consumers Are Growing

Fears About Chinese Consumers Are Growing

The Chinese government bond yield curve has bull steepened considerably since the middle of the year, although it has oscillated without a trend over the past month. To the extent that traditional interpretations of the yield curve apply similarly to China, this suggests that domestic investors are pessimistic about the growth outlook, and expect monetary policy to remain easy. For now, this supports our recommendation to avoid outright long positions in Chinese stocks. Domestic Chinese and global investors remain deeply averse to Chinese corporate bonds, and we continue to disagree that aversion is warranted. Chart 5 highlights that the ChinaBond Corporate Bond total return index remains in a solid uptrend, even for bonds rated AA-. Incredibly, panel 2 of Chart 5 illustrates that global investors who have access to onshore corporate bonds have not lost money this year in unhedged terms, despite the material weakness in the RMB since the middle of the year. We continue to recommend onshore corporate bond positions over the coming 6-12 months.2 Chart 5Chinese Corporate Bonds: A Contrarian Long

Chinese Corporate Bonds: A Contrarian Long

Chinese Corporate Bonds: A Contrarian Long

CNY-USD rose materially last week, in response to speculation that the U.S. is readying a possible trade deal with China. Our geopolitical strategists recommend fading the odds of a near-term trade truce, implying that the odds of USD-CNY breeching 7 over the coming months are substantial. While economically meaningless in and of itself, the threshold is psychologically important and its failure to hold could spark meaningful renewed fears of uncontrolled capital outflow from China. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com 1 Please see Emerging Markets Strategy Weekly Report "EMs Are In A Bear Market," published October 18, 2018. Available at ems.bcaresearch.com. 2 Please see China Investment Strategy Weekly Report "Investing In The Middle Of A Trade War," published September 19, 2018. Available at cis.bcaresearch.com. Cyclical Investment Stance Equity Sector Recommendations

Underweight Marriott International, the hotel heavyweight of the S&P hotels, resorts and cruise lines index reported results on Monday and the company's outlook was grim, calling for revenue growth below analyst forecasts on the back of higher room growth. This is confirmed by our leading data which shows capacity growth accelerating, leading us to be concerned that a recent resurgence in pricing power is primed for a collapse (second panel). Meanwhile, labor costs, which are a relatively greater part of overall industry costs, have visibly shifted higher (third panel). A top line squeeze combined with ballooning costs does not bode well for profit growth. Thus while the valuation multiple has significantly contracted (bottom panel), we remain afraid of falling into a value trap. Stay underweight. The ticker symbols for the stocks in this index are: BLBG: S5HOTL - MAR, CCL, RCL, HLT, WYN, NCLH.

Still Checked Out Of Hotels

Still Checked Out Of Hotels

Underweight While we remain constructive on financials that benefit from higher rates, we continue to recommend investors avoid the consumer discretionary sector - the other early cyclical - that suffers when interest rates rise. The second panel of our chart depicts this inverse correlation consumer discretionary equities have with interest rates, especially the fed funds rate. Most discretionary equites are levered off of floating rates and thus any increase in the fed funds rate gets reflected immediately in banks' prime lending rate. Also, most consumer debt is floating rate debt and thus tighter monetary conditions, at the margin, dampen consumer debt uptake and, as a knock-on effect, weigh on discretionary consumer outlays. Not only are higher interest rates anchoring consumer discretionary stocks but rising energy prices are also dealing a blow to this sector. Our Consumer Drag Indicator (CDI, comprising mortgage rates and energy prices) has been an excellent leading indicator of relative share price momentum and currently, the message is clear: the sinking CDI signals that a bear market in consumer discretionary stocks has likely commenced (bottom panel). Bottom Line: The path of least resistance is lower for the S&P consumer discretionary index, stay underweight. Please see Monday's Weekly Report for more details.

Consumer Discretionary Stocks Are Still A Sell

Consumer Discretionary Stocks Are Still A Sell

The above chart depicts this inverse correlation consumer discretionary equities have with interest rates, especially the fed funds rate. Most discretionary equites are levered off of floating rates and thus any increase in the fed funds rates gets reflected…

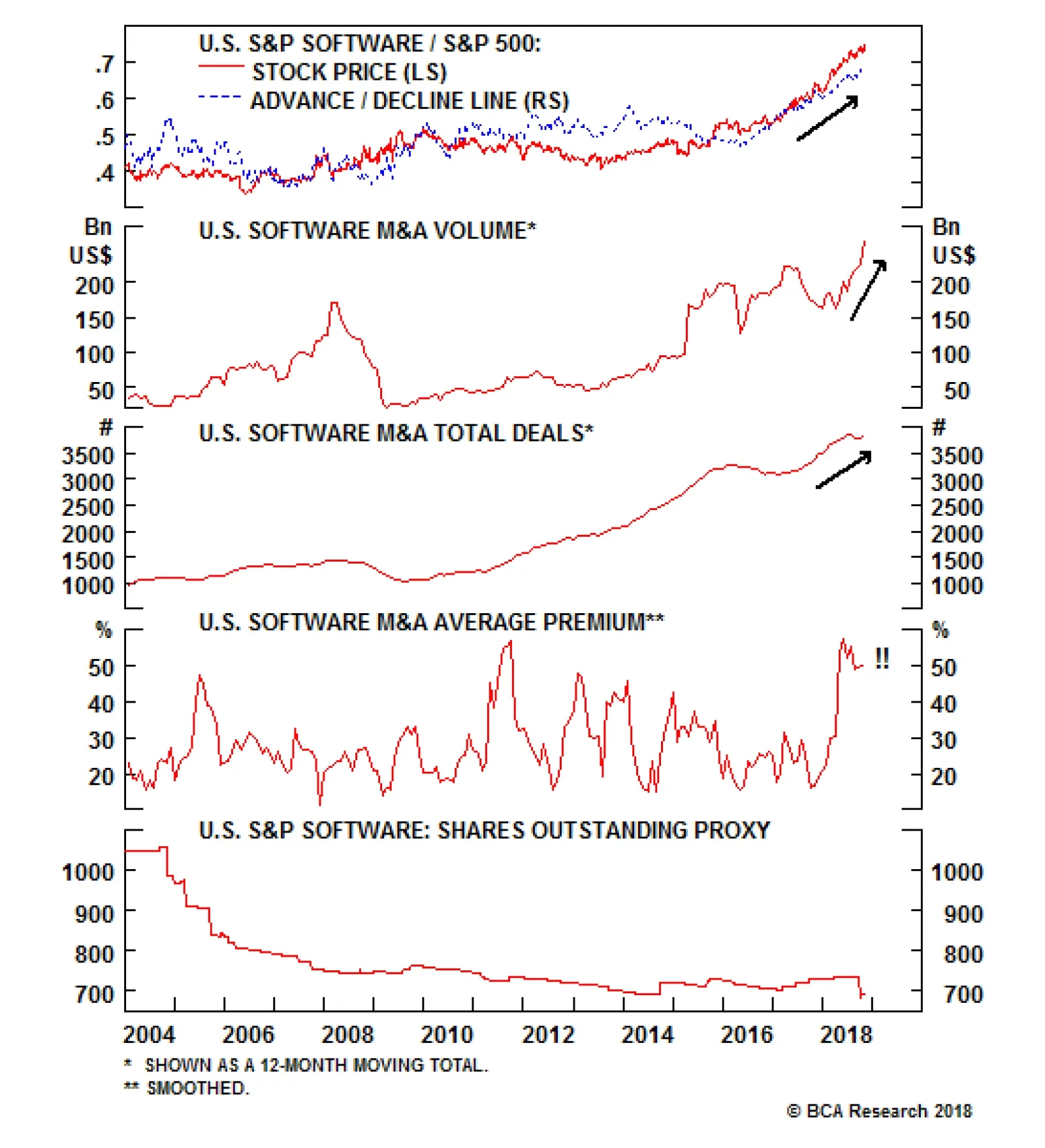

Inter-industry M&A activity is reaching fever pitch and this frenzy is bidding up premia to stratospheric levels. The push to the cloud, SaaS and even AI has boosted the appeal of software stocks and brought them to the forefront of potential takeout…

Overweight (High-conviction) Despite recent tech stock ills, software stocks continue to defy gravity and remain in a multi-year uptrend, still above the dotcom bubble relative performance highs (top panel). We reiterate our high-conviction overweight status and within tech we continue to prefer the S&P software and S&P tech hardware, storage & peripherals indexes to the early-cyclical tech S&P semis and S&P semi equipment subgroups. While rising M&A premia have been a core driver of software stock performance, industry operating metrics are on fire which supports the elevated industry valuation multiples. Top line growth is accelerating and running at a higher clip than the broad market. The recovery in the software price deflator (middle panel), a proxy for industry pricing power, corroborates this bright demand backdrop. Impressively, labor additions have been muted, implying that margins can expand further and possibly challenge cyclical highs (bottom panel). Overall, feverish software M&A activity, the ongoing capex upcycle, firming industry operating metrics and pristine balance sheets, suggest that software stocks are a must have for equity portfolios; please see Monday's Weekly Report for more details. Bottom Line: The S&P software index remains a high-conviction overweight. The ticker symbols for the stocks in this index are: BLBG: S5SOFT - MSFT, ORCL, ADBE, CRM, INTU, RHT, ADSK, CA, SNPS, CTXS, ANSS, CDNS, FTNT and SYMC.

Software Is In High Demand

Software Is In High Demand