Sectors

According to our Bank Credit Analyst service, an inflection point in the relative performance of US stocks is not likely to occur over the coming 6-12 months. A recession favors US equities in common currency terms barring substantially less global ex-US…

US housing market data have been mixed. In June, the FHFA House Price index unexpectedly declined 0.1% m/m and the NAHB housing market index unexpectedly eased to 39 from a 41 reading. In July, starts and permits both disappointed, contracting 6.8% and 4.0%…

The Conference Board’s Consumer Confidence measure surprised to the upside in August, rising from 100.3 to 103.3, above expectations of 100.7. Consumers’ assessment of present economic conditions climbed 0.8 points to 134.4, while their expectations about the…

Brazilian equities have largely underperformed their EM peers in USD terms since the beginning of the year. Rising public debt and inflation are the two main forces weighing on the Brazilian bourse. Our Emerging Market strategists expect public debt-to-GDP…

Preliminary estimates suggest that US durable goods orders growth rebounded sharply from a 6.9% m/m contraction to 9.9% growth in July, upending expectations of a more muted 5.0% monthly increase. However, a 34.8% m/m rise in transportation equipment orders…

European regulatory carbon credits (EUAs) are becoming increasingly investable as an asset class. In a Special Report published last September, our Global Investment strategists agreed to the strategic bull case for EUAs, but highlighted a bearish view on…

The equal-weighted S&P 500 index reached a new all-time high of 7,096.12 on Monday. Chair Powell’s comments at the Jackson Hole Symposium last week dispelled any remaining doubt about a September rate cut and sent smaller stocks higher. The Russell…

According to BCA Research’s US Political Strategy service, in the final months of an election cycle, equities underperform relative to non-election years. This extends further into Q1 of the following year due to uncertainty. Once the election results are…

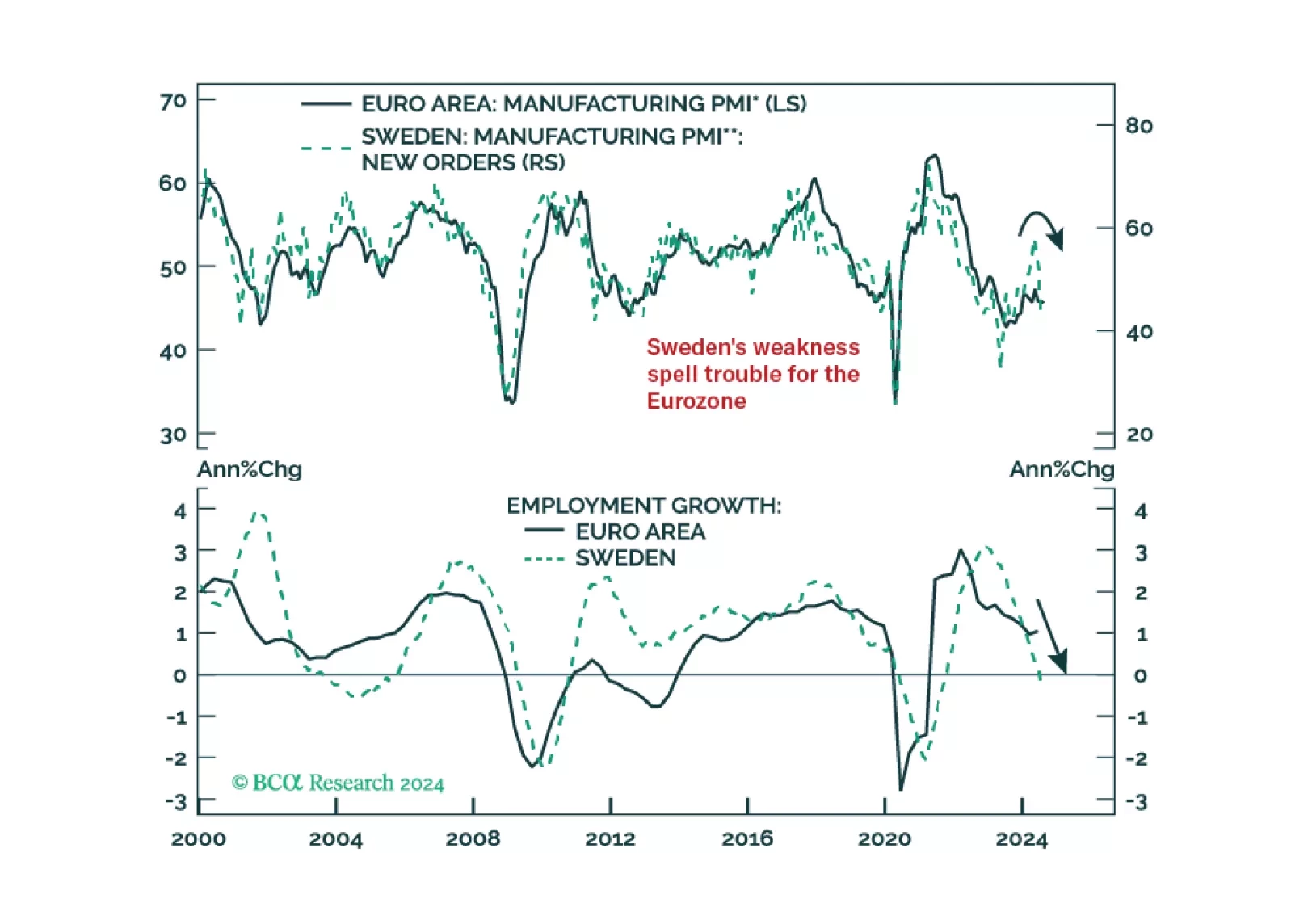

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

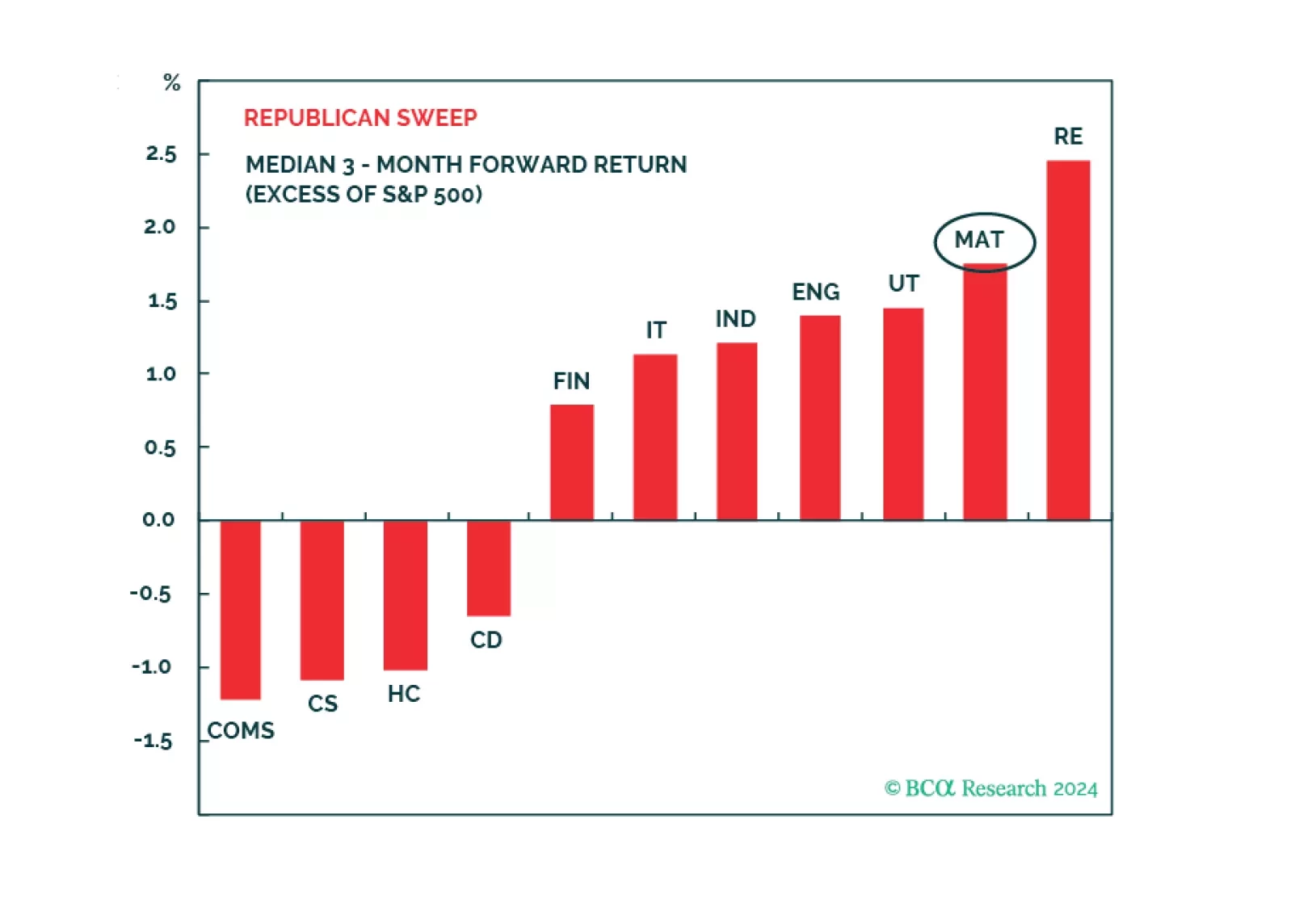

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.