Sectors

Highlights Portfolio Strategy The firming long-term housing demand backdrop, lumber price cost relief, steady new home prices and favorable new home sales expectations, all signal that it is time to buy homebuilders. On the flip side, we do not want to overstay our welcome in the S&P home improvement retail index as a number of leading industry profit indicators have started to wave a yellow flag. Recent Changes Boost the S&P Homebuilding index to overweight today. Trim the S&P Home Improvement Retail index to neutral and lock in gains of 13.3% today. Table 1

Indurated

Indurated

Feature Another week, another SPX all-time high. Investors have refocused their attention on the important macro drivers: solid profits, easing fiscal policy, and still-benign monetary policy with the real fed funds rate barely probing 0%. Trade-related rhetoric has taken the back seat as it has now become obvious that the rest of the world will bear the brunt of President Trump's trade escalation. Our EPS growth models are sniffing this out, with the SPX ticking higher, while our global profit model sinking close to nil (Chart 1). Chart 1Ex-U.S. EPS Will Bear The Brunt Of Trade Wars

Ex-U.S. EPS Will Bear The Brunt Of Trade Wars

Ex-U.S. EPS Will Bear The Brunt Of Trade Wars

Importantly, we are impressed by how thick-skinned the market has become to negative trade-related news. Putting the looming Chinese tariffs into proper perspective is instructive. Assuming a 25% tariff rate on $250bn worth of Chinese manufactured goods and no relief from the renminbi's steep depreciation since April, results in a "tax" of $63bn. The net new "tax" is actually $53bn as an average 3.8%1 import tariff rate already exists on manufactured goods. The consumer and corporations will bear the brunt of this "tax", so it is worth examining the data on household net worth, consumer incomes, and corporate sales. Federal Reserve data show that household net worth increased by $8.1tn in the past year. BEA data reveal that total wage & salary disbursements increased by $400bn, and BCA's projections call for $600bn increase in SPX sales for 2019 (using IBES data for calendar 2019, Chart 2). In other words, it becomes clear that $53bn in a new tariff "tax" will barely eat into net worth, consumer incomes or corporate revenue flows. In addition, according to the IMF, fiscal easing in 2019 will surpass even this year's fiscal expansion in the U.S. The upshot is that over 1% of GDP in fiscal thrust in 2019 thwarts the specter of tariffs, before the fiscal impulse turns negative starting in 2020 (bottom panel, Chart 2). Meanwhile, following up from last week's report when we posited that the current macro backdrop resembles more the mid-2000s than the late-1990s, we are challenging ourselves and asking what if we are wrong in our assessment. Could we actually be replaying a late-1990s episode instead? Revisiting the late-1990s in more detail is in order, refreshing our memory on the sequence of events that led to the climactic LTCM bailout, and highlighting potential signposts that can be helpful in navigating today's macro and equity market maps. In March 1997 the Fed raised rates and pushed the fed funds rate to 5.5%. In hindsight that was a mistake as the Fed then paused the tightening cycle and watched as the Thai baht began to tumble in late-June 1997, eventually gripping all of the emerging world. True, the U.S. stock market modestly pulled back in October 1997 and the VIX spiked to 38. Then, as equities recovered in Q1/1998 and jumped to fresh all-time highs, suddenly the yield curve inverted in May 1998. Undeterred, the S&P 500 hit another peak in July of 1998 before falling roughly 20% in the subsequent month. Finally, once Russia defaulted and the Fed had to bail out the banks due to the LTCM fiasco, the FOMC, late in the game in September 1998, started to ease monetary policy, and engineered a steepening of the yield curve (Chart 3). Chart 2Trade "Tax" A Drop In The Bucket

Trade “Tax” A Drop In The Bucket

Trade “Tax” A Drop In The Bucket

Chart 3Sequence Of Macro Events Matters

Sequence Of Macro Events Matters

Sequence Of Macro Events Matters

The most important signpost from this trip down memory lane is the yield curve. In other words, heed the signal from the bond market: the yield curve inversion correctly predicted a reversal of Fed policy and naturally led the temporary peak in the stock market. Importantly, despite the peak-to-trough near-20% decline in the SPX between July and late-August 1998, if someone had bought the index on Jan 2, 1998 and held through the cathartic LTCM bailout, they remained in the black (bottom panel, Chart 3), and a buy the dip strategy was a winning one. As a last reminder, the SPX jumped another 65% from the August 1998 trough until the March 2000 peak that was preceded, once again, by another yield curve inversion. At the current juncture, were the yield curve to invert we would become overly cautious on the broad equity market as we highlighted in late-June2, and would begin to transition the portfolio away from cyclicals and toward defensives. But, we are not there yet. Thus, we sustain our sanguine broad equity market outlook on a 9-12 month horizon and our SPX target remains 10% higher with EPS doing all the heavy lifting as the multiple moves sideways (for more details, please refer to our April 30th, 2018 Weekly Report titled "Lifting SPX Target"). This week we are taking a deeper dive in housing and housing-related equities and making a subsurface portfolio shift. Look Through The Housing Soft Patch, And... While housing-related data releases have been slightly weaker than anticipated lately, we deem that this softness is transitory as housing market fundamentals rest on solid foundations. On the demand side, first-time home buyers still make only a third of total home sales and the homeownership rate is near generational lows, underscoring that pent up housing demand exists. In fact, the percentage of 18-34 year-olds that live with their parents remains close to 32% a multi-decade high and also represents another source of housing demand that has been dormant because of the Great Recession (Chart 4). Importantly, household formation is still running at a higher clip than housing starts and permits, signaling that the risk of a significant supply/demand imbalance is rising. Historically, this gets resolved via higher prices. Further on the supply side, inventories of existing and new homes for sale remain low and point toward a tight residential housing market (Chart 5). The 98.5% homeowner occupancy rate corroborates the apparent residential real estate market tightness. Chart 4Homeownership Still Well Within Reach

Homeownership Still Well Within Reach

Homeownership Still Well Within Reach

Chart 5Positive Housing Demand/Supply Dynamics

Positive Housing Demand/Supply Dynamics

Positive Housing Demand/Supply Dynamics

True, affordability has taken a hit both as a result of rising home price inflation and mortgage rates. But, putting affordability in historical context reveals that homeownership is still well within reach. Were we to exclude that aberration of the post 2007 surge in affordability owing to the collapse in house prices and all-time lows in mortgage rates, affordability is higher than the 1992-2007 range and only lower than the early 1970s. The reason is largely because of still generationally-low interest rates (Chart 5). While a rising interest rate backdrop and sustained house price inflation will continue to dent affordability, as long as job certainty remains intact and wage growth picks up steam as we expect (please see Chart 4 from last week's publication), we doubt that the U.S. housing market will suffer a relapse. ...Boost Homebuilders To Overweight, But... In that light, we recommend augmenting exposure to overweight in the S&P homebuilding index. With the labor market at full employment and unemployment insurance claims on the verge of breaking below the 200K mark, housing starts should regain their footing (Chart 6) and propel homebuilding profits. In addition, the latest Fed Senior Loan Officer survey showed that demand for residential real estate loans ticked higher, while simultaneously bankers remain willing extenders of mortgage credit. The implication is that new home sales will likely reaccelerate in the coming months (third & bottom panels, Chart 7). Chart 6Homebuilders Rest On Solid Foundations

Homebuilders Rest On Solid Foundations

Homebuilders Rest On Solid Foundations

Chart 7Lumber Input Cost Relief

Lumber Input Cost Relief

Lumber Input Cost Relief

While galloping lumber prices were previously a key reason for putting the S&P homebuilding index on our high-conviction underweight list, the recent liquidation, down $300/thousand board feet since the mid-May peak, in lumber prices represents a massive input cost relief for homebuilders (second panel, Chart 7). With regard to the relative pricing power front, previous price concessions (new home prices compared with existing home prices) are paying off as new home sales are steadily gaining a larger slice of the overall home sales pie (second & third panels, Chart 8). As input cost relief is slated to kick in during the next few months, especially on the framing lumber front, at a time when new home prices have stabilized, homebuilding sales and profits will likely overwhelm (bottom panel, Chart 8). While the latest NAHB/Wells Fargo National Home Market survey showed some softness on the overall housing market index (HMI), keep in mind that both the HMI and the sales expectations subcomponents of the survey are squarely above the 50 boom/bust line and only slightly below the recent cyclical highs (top and second panels, Chart 9). This healthy housing backdrop is also evident in plentiful construction job openings and expanding national house prices (third & bottom panels, Chart 9). Nevertheless, there are two risks to our upbeat S&P homebuilding view. First, interest rates. At the margin, rising mortgage rates can be a source of deficient housing demand especially for first-time home buyers. However, as mentioned earlier, interest rates are generationally low (middle panel, Chart 10) and the job market remains vibrant which should continue to entice first-time home buyers to make one of the largest purchase decisions of their lifetime. Chart 8Price Hikes Should Stick

Price Hikes Should Stick

Price Hikes Should Stick

Chart 9Big Gaps Set To Narrow

Big Gaps Set To Narrow

Big Gaps Set To Narrow

Chart 10Two Risks: Interest Rates & Wages

Two Risks: Interest Rates & Wages

Two Risks: Interest Rates & Wages

Second, industry wage inflation. Construction sector wages are climbing rapidly, as much as 150bps faster than overall average hourly earnings (bottom panel, Chart 10). This is another key input cost for homebuilders that could eat into profit margins, especially if new home price inflation does not stick. In sum, a firming long-term housing demand backdrop, lumber price cost relief, steady new home prices and favorable leading indicators of new home sales will more than offset rising interest rates and industry wage inflation. Bottom Line: A playable opportunity has surfaced to ride the S&P homebuilding index higher. Lift exposure to overweight. The ticker symbols for the stocks in this index are: BLBG: S5HOME - DHI, LEN, PHM. ...Don't Over Stay Your Welcome In Home Improvement Retailers Nevertheless, we do not want to overstay our welcome on the other residential real estate-levered consumer discretionary subgroup, the S&P home improvement retail (HIR) index. We recommend a downgrade to a benchmark allocation for a relative gain of 13.3% since the July 5, 2016 inception. Such a move does not reflect a worsening overall housing view; as we made clear in our analysis above, we remain housing market bulls. Instead, we are concerned that too much euphoria is already priced in HIR equities. Chart 11 shows that fixed residential investment as a percentage of GDP is up 50% from trough to the recent peak (similar to the advance in existing home sales), whereas relative HIR performance is up 170% in the same time frame. Our worry is that optimistic sell side analysts' relative profit forecasts will be hard to attain, let alone surpass (bottom panel, Chart 11). Three main reasons are behind our softening EPS backdrop for home improvement retailers. First, our HIR model has plunged on the back of the wholesale liquidation in lumber prices and rising interest rates (Chart 12). Lumber deflation in particular will prove a profit headwind as building supply Big Box retailers make a set margin on wood products. Chart 11Too Much Euphoria

Too Much Euphoria

Too Much Euphoria

Chart 12Timberrrr!

Timberrrr!

Timberrrr!

Second, household appliance and furniture & durable selling prices have tentatively crested, and represent another source of profit headaches for HIR (bottom panel, Chart 13). Finally, select industry operating metrics suggest that the easy profits are behind HIR. Not only is our productivity growth proxy (sales per employee) on the verge of deflating, but also an inventory surge has sunk the HIR sales-to-inventories ratio into the contraction zone (second & third panels, Chart 13). But there are still some pockets of strength in the home improvement retailing industry that prevent us from turning outright bearish on the S&P HIR index. Despite the aforementioned easing in appliance and furniture wholesale prices, our HIR implicit price deflator has spiked on a short-term rate of change basis, likely owing to firm demand for remodeling activity. Indeed, the latest NAHB remodeling survey remains perched near record highs. The implication is that the recent lull in industry sales growth may reverse (middle and bottom panels, Chart 14). Importantly, a large driver of the previous cycle's remodeling activity was the availability of HELOCs and the stratospheric rise in Mortgage Equity Withdrawal (popularized by Fed economist Dr. James Kennedy). Now that home equity has nearly doubled to near 60% from the depths of the GFC, there are rising odds that homeowners may begin to tap their rebuilt equity and embark upon more renovations (top & middle panels, Chart 15). Tack on rising disposable incomes (bottom panel, Chart 15) and a buoyant labor market and the outlook for remodeling activity brightens further. Chart 13Operational Trouble Brewing...

Operational Trouble Brewing…

Operational Trouble Brewing…

Chart 14...But Offsets...

…But Offsets…

…But Offsets…

Chart 15...Exist

…Exist

…Exist

Netting it out, is it prudent to lock in gains in the S&P HIR index as profit drivers have downshifted at the margin. Bottom Line: Crystalize gains of 13.3% in the S&P HIR index since inception, and downgrade exposure to neutral. The ticker symbols for the stocks in this index are: BLBG: S5HOMI - HD, LOW. Anastasios Avgeriou, Vice President U.S. Equity Strategy anastasios@bcaresearch.com 1 Source: The World Bank, https://data.worldbank.org/indicator/TM.TAX.MANF.SM.FN.ZS?locations=US&name_desc=true 2 Please see BCA U.S. Equity Strategy Weekly Report, "Has The Reward/Risk Tradeoff Changed?" dated June 25, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

Highlights We review last year's "Three Tantalizing Trades" and offer four additional ones: Trade #1: Long June 2019 Fed funds futures contract/short Dec 2020 Fed funds futures contract Trade #2: Long USD/CNY Trade #3: Short AUD/CAD Trade #4: Long EM stocks with near-term downside put protection Feature A Review Of Last Year's "Three Tantalizing Trades" I had the pleasure of speaking at BCA's last Annual Investment Conference on September 25th, 2017, where I presented the following three trade ideas (Chart 1): 1. Short December 2018 Fed funds futures We closed this trade for a profit of 70 basis points. Had we held on, it would be up 92 basis points as of the time of this writing. 2. Long global industrial equities/short utilities We closed this trade on February 1st for a gain of 12%, as downside risks to global growth began to mount. This proved to be a timely decision, as the trade would be up only 6.1% had we kept it on. We would not re-enter this trade at present. 3. Short 20-year JGBs/long 5-year JGBs This trade struggled for much of 2018 but sprung back to life in August. It is up 0.6% since we initiated it. We still like the trade over the long haul. Investors are grossly underestimating the risk that Japanese inflation will move materially higher as an aging population creates a shortage of workers and a concomitant decline in the national savings rate. We also think the government will try to egg on any acceleration in consumer prices in order to inflate away its debt burden. In the near term, however, the trade could struggle if a combination of weaker EM growth and an increase in the value of the trade-weighted yen cause inflation expectations to decline. Four Additional Trades Trade #1: Long June 2019 Fed funds futures contract/short December 2020 Fed funds futures contract Investors expect U.S. short-term rates to rise to 2.38% by the end of 2018 and 2.85% by the end of 2019. The 47 basis points in tightening priced in for next year is less than the 75 basis points in hikes implied by the Fed dots. Investors appear to have bought into Larry Summers' secular stagnation thesis. They are convinced that short rates will not be able to rise above 3% without triggering a recession (Chart 2). Chart 1Revisiting Last Year's Three Tantalizing Trades

Revisiting Last Year's Three Tantalizing Trades

Revisiting Last Year's Three Tantalizing Trades

Chart 2Markets Expect No Fed Hikes Beyond Next Year

Four Tantalizing Trades

Four Tantalizing Trades

Regardless of what one thinks of Summers' thesis, it must be acknowledged that it is a theory about the long-term drivers of the neutral rate of interest. Over a shorter-term cyclical horizon, many factors can influence the neutral rate. Critically, most of these factors are pushing it higher: Fiscal policy is extremely stimulative. The IMF estimates that the U.S. cyclically-adjusted budget deficit will reach 6.8% of GDP in 2019 compared to 3.6% of GDP in 2015. In contrast, the euro area is projected to run a deficit of only 0.8% of GDP next year, little changed from a deficit of 0.9% it ran in 2015 (Chart 3). The relatively more expansionary nature of U.S. fiscal policy is one key reason why the Fed can raise rates while the ECB cannot. Credit growth has picked up. After a prolonged deleveraging cycle, private-sector nonfinancial debt is rising faster than GDP (Chart 4). The recent easing in The Conference Board's Leading Credit Index suggests that this trend will continue (Chart 5). Wage growth is accelerating. Average hourly earnings surprised on the upside in August, with the year-over-year change rising to a cycle high of 2.9%. This followed a stronger reading in the Employment Cost Index in the second quarter. A simple correlation with the quits rate suggests that there is plenty of upside for wage growth (Chart 6). Faster wage growth will put more money into workers pockets who will then spend it. The savings rate has scope to fall. The personal savings rate currently stands at 6.7%, more than two percentage points higher than what one would expect based on the current ratio of household net worth-to-disposable income (Chart 7). If the savings rate were to fall by two points over the next two years, it would add 1.5% of GDP to aggregate demand. Chart 3U.S. Fiscal Policy Is More Expansionary Than The Euro Area

U.S. Fiscal Policy Is More Expansionary Than The Euro Area

U.S. Fiscal Policy Is More Expansionary Than The Euro Area

Chart 4U.S. Private-Sector Nonfinancial Debt Is Rising At Close To Its Historic Trend

U.S. Private-Sector Nonfinancial Debt Is Rising At Close To Its Historic Trend

U.S. Private-Sector Nonfinancial Debt Is Rising At Close To Its Historic Trend

Chart 5U.S. Credit Growth Will Remain Strong

U.S. Credit Growth Will Remain Strong

U.S. Credit Growth Will Remain Strong

Chart 6Quits Rate Is Signaling That There Is Upside For Wage Growth

Quits Rate Is Signaling That There Is Upside For Wage Growth

Quits Rate Is Signaling That There Is Upside For Wage Growth

Chart 7The Personal Savings Rate Has Room To Fall

Four Tantalizing Trades

Four Tantalizing Trades

A back-of-the-envelope calculation suggests that these cyclical factors will permit the Fed to raise rates to 5% by 2020, almost double what the market is discounting.1 A more hawkish-than-expected Fed will bid up the value of the greenback. A stronger dollar, in turn, will undermine emerging markets, which have seen foreign-currency debts balloon over the past six years (Chart 8). The deflationary effects of a stronger dollar and falling commodity prices could temporarily cause investors to price out some hikes over the next few quarters. With that in mind, we recommend shorting the December 2020 Fed funds futures contract, while going long the June 2019 contract. The first leg of the trade captures our expectation that the market will revise up its estimate the terminal rate, while the second leg captures near-term risks to global growth. The gap between the two contracts has widened over the past few days as we have prepared this report, but at 21 basis points, it has plenty of room to increase further (Chart 9). Chart 8EM Dollar Debt Is High

EM Dollar Debt Is High

EM Dollar Debt Is High

Chart 9U.S. Rate Expectations Are Too Low Beyond Mid-2019

U.S. Rate Expectations Are Too Low Beyond Mid-2019

U.S. Rate Expectations Are Too Low Beyond Mid-2019

Trade #2: Long USD/CNY China's economy is slowing, which has prompted the government to inject liquidity into the financial system. The spread in 1-year swap rates between the U.S. and China has fallen from about 3% earlier this year to 0.6% at present, taking the yuan down with it (Chart 10). It is doubtful that China will be willing to match - let alone exceed - U.S. rate hikes. This suggests that USD/CNY will appreciate. China's real trade-weighted exchange rate has weakened during the past four months, but is up 25% over the past decade (Chart 11). U.S. tariffs on $250 billion (and counting) of Chinese imports threaten to erode export competitiveness, making a further devaluation necessary. Chart 10USD/CNY Has Tracked China-U.S. Interest Rate Differentials

USD/CNY Has Tracked China-U.S. Interest Rate Differentials

USD/CNY Has Tracked China-U.S. Interest Rate Differentials

Chart 11The RMB Is Still Quite Strong

The RMB Is Still Quite Strong

The RMB Is Still Quite Strong

President Trump will oppose a weaker yuan. However, just as China's actions earlier this year to strengthen its currency did not prevent the U.S. from imposing tariffs, it is doubtful that efforts by the Chinese authorities to talk up the yuan would appease Trump. Besides, China needs a weaker currency. The Chinese economy produces too much and spends too little. The result is excess savings, epitomized most clearly in a national savings rate of 46%. As a matter of arithmetic, national savings need to be transformed either into domestic investment or exported abroad via a current account surplus. China has concentrated on the former strategy over the past decade. The problem is that this approach has run into diminishing returns. Chart 12 shows that the capital stock has risen dramatically as a share of GDP. As my colleague Jonathan LaBerge has documented, the rate of return on assets among Chinese state-owned companies, which have been the main driver of rising corporate leverage, has fallen below their borrowing costs (Chart 13).2 Chart 12China's Capital Stock Has Grown Alongside Rising Debt Levels

China's Capital Stock Has Grown Alongside Rising Debt Levels

China's Capital Stock Has Grown Alongside Rising Debt Levels

Chart 13China: Rate Of Return On Assets Below Borrowing Costs For State-Owned Companies

China: Rate Of Return On Assets Below Borrowing Costs For State-Owned Companies

China: Rate Of Return On Assets Below Borrowing Costs For State-Owned Companies

Now that the economy is awash in excess capacity, the authorities will need to steer more excess production abroad. This will require a larger current account surplus which, in turn, will necessitate a relatively cheap currency. The dollar is currently working off overbought technical conditions, a risk we flagged in our August 31st report.3 That process should be complete over the next few weeks. Meanwhile, hopes of a massive Chinese stimulus focused on fiscal/credit easing will fade. The combination of these two forces will push up USD/CNY above the psychologically-critical 7 handle by the end of the year. Trade #3: Short AUD/CAD A weaker yuan will raise raw material costs to Chinese firms. This will hurt commodity prices. Industrial metals are much more vulnerable to slower Chinese growth than oil. Chart 14 shows that China consumes close to half of all the copper, nickel, aluminum, zinc, and iron ore produced in the world, compared to only 15% of oil output. Our expectation that developed economy growth will hold up better than EM growth over the next few quarters implies that oil will outperform industrial metals. Oil is also supported by a tighter supply backdrop, particularly given the downside risks to Iranian and Venezuelan crude exports. A bet on oil over metals is a bet on DM over EM growth in general, and the Canadian dollar over the Australian dollar specifically (Chart 15). Canada exports more oil than metals, while Australian exports are dominated by ores and metals. In terms of valuations, the Canadian dollar is still somewhat cheap relative to the Aussie dollar based on our FX team's long-term valuation model (Chart 16). Chart 14China Is A More Dominant Consumer Of Metals Than Oil

China Is A More Dominant Consumer Of Metals Than Oil

China Is A More Dominant Consumer Of Metals Than Oil

Chart 15Oil Over Metals = CAD Over AUD

Oil Over Metals = CAD Over AUD

Oil Over Metals = CAD Over AUD

Chart 16Canadian Dollar Still Somewhat Cheap Versus The Aussie Dollar

Canadian Dollar Still Somewhat Cheap Versus The Aussie Dollar

Canadian Dollar Still Somewhat Cheap Versus The Aussie Dollar

The loonie has been weighed down by ongoing fears that Canada will be left out of a renegotiated NAFTA. However, our geopolitical strategists believe that the Trump administration is trying to focus more on China, against whom the case for unfair trade practices is far easier to make. The U.S. has already negotiated a trade deal with Mexico and an agreement with Canada is more likely than not. If a new deal is struck, the Canadian dollar will rally. We recommended going short AUD/CAD on June 28. The trade is up 3.4%, carry-adjusted, since then. Stick with it. Trade #4: Long EM stocks with near-term downside put protection It is too early to call a bottom in EM assets. Valuations have not yet reached washed-out levels (Chart 17). Bottom fishers still abound, as evidenced by the fact that the number of shares outstanding in the MSCI iShares Turkish ETF has almost tripled since early April (Chart 18). However, at some point - probably in the first half of next year - investors will liquidate their remaining bullish EM bets. During the 1990s, this capitulation point occurred shortly after the collapse of Long-Term Capital Management in September 1998. EM equities fell by 26% between April 21, 1998 and June 15, 1998. After a half-hearted attempt at a rally, EM stocks tumbled again in July, falling by 35% between July 17 and September 10. The second leg of the EM selloff brought down the S&P 500 by 22%. Thanks to a series of well-telegraphed Fed rate cuts, global markets stabilized on October 8th (Chart 19). The S&P 500 surged by 68% over the next 18 months. The MSCI EM index more than doubled in dollar terms over this period. EM stocks outperformed U.S. equities by a whopping 71% between February 1999 and February 2000. Europe also outperformed the U.S. starting in mid-1999. Value stocks, which had lagged growth stocks over the prior six years, also finally gained the upper hand. Chart 17EM Assets: Valuations Not Yet At Washed Out Levels

EM Assets: Valuations Not Yet At Washed Out Levels

EM Assets: Valuations Not Yet At Washed Out Levels

Chart 18EM Bottom Fishers Still Abound

EM Bottom Fishers Still Abound

EM Bottom Fishers Still Abound

Chart 19The ''Great Equity Rotation'' Is Coming: A Roadmap From The 1990s

The ''Great Equity Rotation'' Is Coming: A Roadmap From The 1990s

The ''Great Equity Rotation'' Is Coming: A Roadmap From The 1990s

The "Great Equity Rotation" is coming. All the trades that have suffered lately - overweight EM, long Europe/short U.S., long cyclicals/short defensives, long value/short growth - will get their day in the sun. Investors can prepare for this inflection point by scaling into EM equities today, but guarding against near-term downside risk by buying puts. With that in mind, we are going long the iShares MSCI Emerging Market ETF (EEM), while purchasing March 15, 2019 out-of-the-money puts with a strike price of $41. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com 1 Depending on which specification of the Taylor rule one uses, a one percent of GDP increase in aggregate demand will increase the neutral rate of interest by half a point (John Taylor's original specification) or by a full point (Janet Yellen's preferred specification). Fiscal policy is currently about 3% of GDP too simulative compared to a baseline where government debt-to-GDP is stable over time. Assuming a fiscal multiplier of 0.5, fiscal policy is thus boosting aggregate demand by 1.5% of GDP. Nonfinancial private credit has increased by an average of 1.5 percentage points of GDP per year since 2016. Assuming that every additional one dollar of credit increases aggregate demand by 50 cents, the revival in credit growth is raising aggregate demand by 0.75% of GDP, compared to a baseline where credit-to-GDP is flat. The labor share of income has increased by 1.25% of GDP from its lows in 2015. Assuming that every one dollar shift in income from capital to labor boosts overall spending on net by 20 cents, this would have raised aggregate demand by 0.25% of GDP. Lastly, if the savings rate falls by two points over the next two years, this would raise aggregate demand by 1.5% of GDP. Taken together, these factors are boosting the neutral rate by anywhere from 2% (Taylor's specification) to 4% (Yellen's specification). This is obviously a lot, and easily overwhelms other factors such as a stronger dollar that may be weighing on the neutral rate. 2 Please see China Investment Strategy Special Report, "Chinese Policymakers: Facing A Trade-Off Between Growth And Leveraging," dated August 29, 2018. 3 Please see Global Investment Strategy Weekly Report, "The Dollar And Global Growth: Are The Tables About To Turn?" dated August 31, 2018. Strategy & Market Trends Tactical Trades Strategic Recommendations Closed Trades

The opposing sides of our market- and industry-neutral trade going long the S&P homebuilding index/short the S&P REITs index1 have both been on the receiving end of negative data in the last month. With respect to homebuilders, housing permits, a leading indicator of future starts, fell well short of expectations this week and took the S&P homebuilding index down with it. Meanwhile rising UST yields have been weighing heavily on REIT stocks. The end result is that our trade has given up its early gains. The macro environment tells us that it is too early to throw in the towel on this trade. We continue to believe prices in the residential real estate sector have the upper hand over their commercial real estate (CRE) peers. Existing home inventories have tightened and remain at historically low levels, which should support pricing. On the flip side, our CRE occupancy rate composite is still contracting, warning that already-slowing pricing has further to fall. The divergence in pricing should support homebuilders' returns at the expense of REITs. Bottom Line: We reiterate our long S&P homebuilding/short S&P REITs pair trade. The ticker symbols for the stocks in the S&P homebuilding and S&P REITs indexes are: BLBG: S5HOME - LEN, PHM, DHI and BLBG: S5REITS - IRM, MAA, AMT, BXP, PLD, ESS, CCI, PSA, O, VTR, VNO, WY, EQIX, DLR, EXR, DRE, FRT, WELL, SBAC, HCP, GGP, KIM, EQR, UDR, REG, MAC, HST, SPG, AVB, AIV, SLG, ARE, respectively. 1 Please see BCA U.S. Equity Strategy Special Report, "UnReal Estate Opportunity," dated July 9, 2018, available at uses.bcaresearch.com.

Stick With Homebuilders Over REITs

Stick With Homebuilders Over REITs

Overweight Rail stocks in general, and Union Pacific (UNP) in particular, got a major lift yesterday when UNP announced a plan to implement the principles of Precision Scheduled Railroading (PSR) in its push to improve customer deliveries and profitability. Recall that PSR was developed by Hunter Harrison first at CN Rail, then CP Rail and finally at CSX where its implementation took industry profit laggards to profit leadership. Though his recent passing was untimely, the 9% year-over-year improvement in CSX’s Q2/18 operating ratio is a testament to the success of Mr. Harrison’s strategy. The timing for a renewed approach at UNP could scarcely be better. Both demand and pricing are soaring (second and third panels) and the resulting congestion is threatening profitability. We expect the ongoing supportive macro backdrop, combined with operating improvements such as these, to sustain the operating margin improvement trend of the past two years (bottom panel). Stay overweight, despite the 20% in relative return since inception. The ticker symbols for the stocks in this index are: BLBG: S5RAIL - UNP, CSX, NSC, KSU.

A Plan That Works

A Plan That Works

Highlights The latest round of tariffs on U.S. imports from China confirms that the Trump administration's confrontation with China goes beyond the mid-term elections. Desynchronization between the U.S. and China/EM growth foreshadows dollar appreciation. The latter is the right medicine for the global economy for now. A stronger dollar is required to redistribute growth and inflation away from the U.S. and towards the rest of the world. China needs a weaker currency to offset deflationary pressures stemming from domestic deleveraging and trade tariffs. For EM ex-China, the dollar rally is painful, but it is the right medicine in the long run. It will bring about the unraveling of excesses within their economies. Feature The global economy presently finds itself between two strong and opposing crosscurrents: robust growth and mounting inflationary pressures in the U.S. on the one hand, and weakening Chinese growth on the other. Desynchronization between China/EM and the U.S. has been our theme since April 2017.1 Although this theme has become evident and to a certain degree priced into the markets, we believe it is not yet time to abandon it. Before exploring this analysis in greater depth, we will address the issue of whether strong U.S. demand will reverse the slowdown in the global trade cycle, and update our thoughts on the trade wars. Global Trade And Trade Wars Our leading indicators for global trade do not herald a reversal in the global exports slowdown. Chart I-1 demonstrates that the ratio of risk-on versus safe-haven currencies2 leads global export volumes by several months, and it does not yet flag any improvement. Chart I-1Risk-On / Safe-Haven Currency Ratio As An Indicator Of Global Trade

Risk-On / Safe-Haven Currency Ratio As An Indicator Of Global Trade

Risk-On / Safe-Haven Currency Ratio As An Indicator Of Global Trade

In addition, Taiwanese exports of electronic products lead the global trade cycles by a couple of months, and they are currently pointing to further deceleration in world exports (Chart I-2). It seems extremely robust U.S. domestic demand growth has not prevented a slowdown in global trade in general and EM exports in particular. The reason for this is that many developing countries' shipments to China are larger than their exports to the U.S., as illustrated in Table I-1. Chart I-2Taiwanese Electronics Exports##br## Slightly Lead Global Exports

Taiwanese Electronics Exports Slightly Lead Global Exports

Taiwanese Electronics Exports Slightly Lead Global Exports

Table I-1Many Emerging Economies##br## Sell More To China Than To The U.S.

Desynchronization Compels Currency Adjustments

Desynchronization Compels Currency Adjustments

The latest decision by the U.S. administration to impose a 10% tariff on $200 billion of imports from China and increase this rate to 25% starting January 1, 2019 confirms that the Trump administration's confrontation with China goes beyond the mid-term elections. The true intention of the U.S. is to contain China's geopolitical rise to preserve its global hegemony. These episodes of import tariffs will likely mark the beginning of a much longer and drawn-out geopolitical confrontation. Our colleagues at BCA's Geopolitical Strategy service have been noting for several years that a U.S.-China confrontation is unavoidable.3 In this vein, it is not clear to us why global growth-sensitive and China-leveraged plays in financial markets have rallied in recent days on the new tariff announcement. We can think of two reasons: (1) markets expect China to stimulate domestic demand aggressively to counter tariffs; and (2) gradually rising U.S. import tariffs will boost global trade in the near term, as companies front load their production and shipments before the 25% tariff rate takes hold. On the first point, there has so far been no major new fiscal stimulus announced in China. We detailed fiscal numbers in our August 23 report,4 and there have been no changes since. As to liquidity easing - which has been material - our assessment is that it is likely to be overwhelmed by ongoing regulatory tightening on banks and shadow banking. In short, lingering credit excesses and regulatory tightening will hamper the monetary transmission mechanism from lower interest rates to faster credit growth. So far, money growth in China remains very weak (Chart I-3). Chart I-3China's Narrow Money And EM Stocks

China's Narrow Money And EM Stocks

China's Narrow Money And EM Stocks

On the second point, we cannot rule out a moderate and temporary improvement in global trade due to various technical factors. Yet, any rally rooted in this will prove to be short-lived and fleeting. Bottom Line: Escalating tariffs on U.S. imports from China will reinforce the tectonic macro shifts that have been in place since early this year: it will lift U.S. inflation slightly and weigh on Chinese growth. Rising U.S. Inflation U.S. core inflation is accelerating and moving above the Federal Reserve's soft target of 2%. This will substantially narrow the Fed's maneuvering room to respond to the turmoil in EM and weakening growth outside the U.S. Chart I-4 demonstrates that an equally weighted average of various core consumer inflation measures for the U.S. has been markedly accelerating. The components of this core inflation aggregate are presented in Chart I-5 and include: trimmed mean CPI, trimmed mean PCE, market-based core PCE and median CPI. Besides, the U.S. labor market is super tight, and employee compensation growth will continue to rise. This will put downward pressure on corporate profit margins and will push businesses to consider passing on their rising costs to consumers. Provided wage growth will continue accelerating and the job market and confidence both remain strong, odds are that companies will be able to raise their selling prices. Chart I-4U.S. Inflation Is Rising...

U.S. Inflation Is Rising...

U.S. Inflation Is Rising...

Chart I-5...Based On Various Core Measures

...Based On Various Core Measures

...Based On Various Core Measures

Weakening Chinese Growth Growth continues to weaken in China. In particular: The aggregate freight index (transport by railway, highway, waterway, and aviation) is sluggish and the measure of Air China's freight continues to downshift (Chart I-6). The strength in China's residential property market since 2015 has partially been due to the central bank providing very cheap financing directly to housing via its Pledged Supplementary Lending (PSL) scheme. We have argued in the past that this represents nothing less than monetization of excess housing inventories directly by the People's Bank of China.5 This has boosted property prices and sales, supporting the economy over the past two years. Having met the objective of reducing housing inventories, the PBoC has lately reduced the amount of PSL. Provided changes in PSL flows have led both housing prices and sales volumes, it is reasonable to expect a relapse in new sales in the next six months or so (Chart I-7). Chart I-6China: A Slowdown In Freight Indicators

China: A Slowdown In Freight Indicators

China: A Slowdown In Freight Indicators

Chart I-7China: Housing Sales To Roll Over Soon

China: Housing Sales To Roll Over Soon

China: Housing Sales To Roll Over Soon

Our main theme in China has been and remains shrinking construction activity - both infrastructure and property building. This is the primary rationale for our negative view on commodities prices as well as weakness in mainland aggregate imports. Chart I-8 illustrates property construction activity is already contracting. Headline fixed asset investment in real estate has been held up by booming land purchases, yet equipment purchases as well as construction and installation have been shrinking (Chart I-8). Capital expenditures for all industries, including construction and installation, purchase of equipment and instruments - but excluding land values - are also very weak (Chart I-9). Chart I-8China: Property Investment##br## Excluding Land Is Contracting

China: Property Investment Excluding Land Is Contracting

China: Property Investment Excluding Land Is Contracting

Chart I-9China: Overall Capex##br## Is Very Weak

China: Overall Capex Is Very Weak

China: Overall Capex Is Very Weak

Interestingly, our proxy for marginal propensity to spend6 by Chinese companies leads global industrial metals prices, and continues pointing to more downside (Chart I-10). With respect to oil, Chinese oil import growth has downshifted considerably (Chart I-11) implying that global oil prices have been mostly propped up by supply concerns. Chart I-10Chinese Companies' Propensity##br## To Spend And Metal Prices

Chinese Companies' Propensity To Spend And Metal Prices

Chinese Companies' Propensity To Spend And Metal Prices

Chart I-11China: A Slowdown##br## In Oil Imports

China: A Slowdown In Oil Imports

China: A Slowdown In Oil Imports

Currency Markets As A Rebalancing Mechanism Pressures from growth desynchronization between the U.S. and China and trade wars continue to build. Left unchecked, these imbalances will enlarge and culminate into a bust. A release valve is needed to diffuse these accumulating pressures. Currency and bond markets often act as such - they move to rebalance the global economy and amend economic excesses. Odds are that exchange rates will continue to act as a rebalancing conduit. A stronger dollar is the right medicine for the global economy at the moment. A stronger dollar is required to redistribute growth away from the U.S. and towards the rest of the world. In particular, dollar appreciation is needed to cap budding U.S. inflationary pressures. China needs a weaker currency to offset deflationary pressures stemming from domestic deleveraging and trade tariffs. In turn, a stronger greenback will cause capital outflows from EM and compel the unraveling of excesses within the developing economies. While the result will be painful growth retrenchment for EM in the medium term, cheapened currencies and deleveraging (an unwinding of credit excesses) will ultimately create a foundation for stronger and healthier growth in the years ahead. As to the question of why the dollar would rally in the face of widening twin deficits, we have the following remarks. In a world where growth and inflation are scarce (i.e., in a deflationary milieu), a wider current account deficit and higher inflation - signs of robust domestic demand - will attract capital, ultimately lifting a country's currency. By contrast, in a world of strong growth and intensifying inflationary pressures, twin deficits and higher inflation will cause a country's currency to depreciate. Our assessment is that the global economic backdrop is still more deflationary than inflationary, despite intensifying inflationary pressures in the U.S. Therefore, twin deficits and inflation in the U.S. will be at a premium. That and the fact that the Federal Reserve is willing to continue tightening are conducive for dollar appreciation. As we have argued in previous reports, the U.S. dollar is not cheap,7 but it is not particularly expensive either. In fact, odds are it will get much more expensive before topping out. Bottom Line: Beyond any possible short-term countertrend moves, the path of least resistance for the U.S. dollar is up, and for the RMB and EM currencies, down. As these adjustments within the currency markets endure, EM risk assets will stay under selling pressure and underperform their developed market counterparts. Indonesia: At The Whims Of Foreign Portfolio Flows 20 September 2018 The Indonesian currency has reached a two- decade low, and equities and bonds have sold off considerably. Is it time to turn positive on the nation's financial markets? Our bias remains that this selloff is not over and stocks, bonds as well as the currency have more downside. The basis is that Indonesia's balance of payments (BoP) will continue to deteriorate. Indonesia has been very reliant on volatile foreign portfolio flows to fund its current account deficit (Chart II-1). Not surprisingly, a reversal in foreign portfolio inflows to emerging markets (EM) has hurt this country's financial markets. We expect international capital flows to EM to be lackluster, which will continue to weigh on Indonesia's capital account. In the meantime, Indonesia's current account deficit is likely to widen in the months ahead. First, export revenues will begin rolling over on the back of lower copper and palm oil prices. Together, these commodities account for 13% of Indonesian exports. Second, the ongoing slowdown in China may eventually weigh on thermal coal prices. This commodity makes up another 12% of exports. Third, Indonesian imports remain very robust. Overall, a widening current account/trade deficit is typically negative for both share prices and the rupiah (Chart II-2). Chart II-1Indonesia: Foreign ##br##Portfolio Flows Are Key

Indonesia: Foreign Portfolio Flows Are Key

Indonesia: Foreign Portfolio Flows Are Key

Chart II-2Deteriorating Trade Balance ##br##Is Bearish For Equities

Deteriorating Trade Balance Is Bearish For Equities

Deteriorating Trade Balance Is Bearish For Equities

To prevent further currency depreciation, the government announced it will curb certain imports by raising tariffs.While this policy may succeed in limiting imports, it will also raise inflation by pushing prices of imported goods higher. This will allow inefficient domestic producers to stay in business. Higher inflation is fundamentally negative for the currency and local bonds. The above dynamics are making Indonesia's macro outlook increasingly toxic because Bank Indonesia (BI) will probably need to tighten monetary policy further in order to stabilize the rupiah and restrain inflation. Crucially, the BI's objective is to maintain rupiah stability in order to keep inflation tame. Further, Perry Warjiyo, the current governor of BI, has highlighted his preference for setting decisive and preemptive policies. Indonesia's central bank has already raised interest rates, and more hikes are likely if the currency continues depreciating - as we expect. On top of rate hikes, the BI will continue to deplete its foreign exchange reserves to defend the rupiah. Chart II-3 shows that foreign exchange reserve selling by the BI is shrinking local banking system liquidity (commercial bank reserves at the central bank) and lifting domestic interbank rates. In turn, higher local rates will cause bank loan growth to slow, hurting domestic demand. The latter will be very negative for profit growth and share prices because the Indonesian stock market is heavily dominated by banks and other domestic plays. The outlook for Indonesian banks is crucial for the performance of the Indonesian bourse, given they account for 42% of total MSCI market cap. Unfortunately, banks still rest on shaky foundations: Chart II-3Selling FX Reserves = Higher Interbank Rates

Selling FX Reserves = Higher Interbank Rates

Selling FX Reserves = Higher Interbank Rates

Chart II-4Net Interest Margins Will Keep Compressing

Net Interest Margins Will Keep Compressing

Net Interest Margins Will Keep Compressing

Not only will demand for loans slump as borrowing costs rise, but banks' net interest margins will also continue to compress (Chart II-4). Weaker growth and higher interest rates will also lead to a considerable rise in non-performing loans (NPLs), and cause banks' provisioning levels to spike. Higher provisions will hurt their earnings (Chart II-5). Notably, banks have boosted their profits substantially in the past two years by reducing their provisions. This process is set to reverse very soon. Finally, a word on overall equity valuations is warranted. Despite the correction that has taken place, this bourse is not yet trading at compelling valuation levels neither in absolute nor in relative terms (Chart II-6). Chart II-5Downside Ahead For Banks' Shares

Downside Ahead For Banks' Shares

Downside Ahead For Banks' Shares

Chart II-6Indonesian Bourse Isn't Cheap

Indonesian Bourse Isn't Cheap

Indonesian Bourse Isn't Cheap

Bottom Line: The rupiah will remain under selling pressure. This in turn will create a toxic macro mix of higher inflation, rising borrowing costs and weaker domestic demand. We recommend investors keep an underweight position in Indonesian stocks as well as local and sovereign bonds within their respective EM dedicated portfolios. We are also maintaining our short positions in the rupiah versus the U.S. dollar and on 5-year local currency bonds. Arthur Budaghyan, Senior Vice President Emerging Markets Strategy arthurb@bcaresearch.com Ayman Kawtharani, Associate Editor ayman@bcaresearch.com Footnotes 1 Please see Emerging Markets Strategy Weekly Report, "Toward A Desynchonized World?" dated April 26, 2017, the link is available at ems.bcaresearch.com. 2 Relative total return (carry included) of four equally weighted EM (ZAR, RUB, BRL and CLP) and three DM (AUD, NZD and CAD) commodities currencies versus an equally weighted average of two safe-haven currencies - the Japanese yen and Swiss franc. 3 Please see Geopolitical Strategy Weekly Report, "We Are All Geopolitical Strategists Now," dated March 28, 2018, the link is available at gps.bcaresearch.com. 4 Please see Emerging Markets Strategy Weekly Report, "EM: Do Not Catch A Falling Knife," dated August 23, 2018, the link is available at ems.bcaresearch.com. 5 Please see Emerging Markets Strategy Special Report, "China Real Estate: A Never-Bursting Bubble?" dated April 6, 2018, the link is available at ems.bcaresearch.com. 6 Calculated as a ratio of corporate demand deposits to time deposits. Rising demand deposits relative to time (savings) deposits entail that companies are gearing up to spend /invest money and vice versa. 7 Please see Emerging Markets Strategy Special Report, "The Dollar: Will The U.S. Invoke A "Nuclear" Option?" dated August 30, 2018, the link is available at ems.bcaresearch.com. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Highlights Prediction 1: A major financial downturn will trigger the next major economic downturn, and not the other way round. Prediction 2: The straw that will break the back of a fragile financial system will be the global long bond yield rising by 60 bps within a short space of time. But for those who can fine tune, the global long bond yield must rise a further 30-50 bps before reaching the tipping point for the global risk-asset edifice. Take short-term profits in the overweight position in 30-year government bonds. Take short-term profits in the underweight position in basic materials. Take short-term profits in the underweight positions in Italy (MIB) and Spain (IBEX) and overweight position in Denmark (OMX). Feature The twenty-first century has witnessed three major downturns: the first started in 2000; the second started in 2007 culminating in the Lehman crisis a year later; and the third started in 2011 (Chart of the Week). Today, we are going to stick our necks out and make two predictions about the century's fourth major downturn. Chart of the WeekThree Episodes When Equities Underperformed Bonds By 20 Percent Or More

Three Episodes When Equities Underperformed Bonds By 20 Percent Or More

Three Episodes When Equities Underperformed Bonds By 20 Percent Or More

A major financial downturn will trigger the fourth major economic downturn. The straw that will break the back of a fragile financial system will be the global long bond yield rising by 60 bps within a short space of time. Where The Consensus Is Very Wrong As investment strategists, our primary focus should be the financial markets rather than the economy. On this basis, we define a major downturn in terms of the markets: an episode in which equities underperform bonds by more than 20 percent over a period of more than six months.1 All the same, our market based definition of a major downturn perfectly captures the three occasions that the European economy went into recession or stagnation (Chart I-2). Does this mean that the economic downturns triggered the financial market downturns? No, quite the reverse. The onset of the three major financial downturns clearly preceded the onset of the three major economic downturns. Chart I-2Three Episodes When The Euro Area Economy ##br##Contracted Or Stagnated

Three Episodes When The Euro Area Economy Contracted Or Stagnated

Three Episodes When The Euro Area Economy Contracted Or Stagnated

On reflection, this is hardly surprising. The twenty-first century's major economic downturns have all resulted from financial market distortions and fragilities: the bubble valuations of the technology, media and telecom sectors in 2000 (Chart I-3); the mispricing of U.S. mortgages and credit in 2007 (Chart I-4); and the mispricing of euro area sovereign credit risk in 2011 (Chart I-5). Therefore, it makes perfect sense that the downturns in financial markets should precede the downturns in the economy, even when both are measured in real time. Chart I-3The Major Downturns Stemmed From##br## Financial Market Distortions: The Dot Com ##br##Bubble In 1999/2000...

The Major Downturns Stemmed From Financial Market Distortions: The Dot Com Bubble In 1999/2000...

The Major Downturns Stemmed From Financial Market Distortions: The Dot Com Bubble In 1999/2000...

Chart I-4...The Mispricing Of U.S. ##br##Mortgages And Credit##br## In 2007/2008...

...The Mispricing Of U.S. Mortgages And Credit In 2007/2008...

...The Mispricing Of U.S. Mortgages And Credit In 2007/2008...

Chart I-5...And The Mispricing Of Euro Area ##br##Sovereign Credit Risk##br## In 2010/2011

...And The Mispricing Of Euro Area Sovereign Credit Risk In 2010/2011

...And The Mispricing Of Euro Area Sovereign Credit Risk In 2010/2011

Today, the consensus overwhelmingly believes that an economic downturn will cause the next major downturn in financial markets. But history has taught us time and time again that the causality is much more likely to run the other way. Why not learn the lesson? So here's our first prediction: a major financial downturn will trigger the fourth major economic downturn, and not the other way round. This prediction raises some obvious questions: what could be the major fragility in financial markets, and what could fracture it? A Sharp Rise In Bond Yields Triggered The Last Three Major Downturns Look carefully at the financial market downturns that started in 2000, 2007 and 2011, and you will see another striking similarity. In each episode, the global long bond yield rose by 60 bps or more in the months that preceded the onset of the financial market downturn: April 1999 through January 2000 (Chart I-6); March through July 2007 (Chart I-7); and October 2010 through April 2011 (Chart I-8). This strongly suggests that the spike in the bond yield was the trigger for the subsequent major downturn in financial markets. Chart I-6A Sharply Rising Bond Yield Triggered ##br##The Major Downturn Of 2000

A Sharply Rising Bond Yield Triggered The Major Downturn Of 2000

A Sharply Rising Bond Yield Triggered The Major Downturn Of 2000

Chart I-7A Sharply Rising Bond Yield Triggered##br## The Major Downturn Of 2007 And 2008

A Sharply Rising Bond Yield Triggered The Major Downturn Of 2007 And 2008

A Sharply Rising Bond Yield Triggered The Major Downturn Of 2007 And 2008

Chart I-8A Sharply Rising Bond Yield Triggered ##br##The Major Downturn Of 2011

A Sharply Rising Bond Yield Triggered The Major Downturn Of 2011

A Sharply Rising Bond Yield Triggered The Major Downturn Of 2011

A sharp rise in bond yields is usually the straw that breaks the back of financial market fragilities, in (at least) one of three ways: it flushes out those actors that are reliant on cheap liquidity; it pressures interest rate sensitive sectors in the economy; and it weighs on the valuations of other assets such as equities, especially if those valuations are already extremely elevated. Which segues us neatly to the current fragility in the global financial system. As we wrote last week, the post-2008 global experiment with quantitative easing, and zero and negative interest rate policy has boosted the valuations of all risk-assets across all geographies across all asset-classes. And the total value of those global risk-assets is $400 trillion, equal to about five times the size of the global economy.2 We have also consistently highlighted that not only do the rich valuations of $400 trillion of risk-assets depend (inversely) on bond yields, but that this relationship is an exponential function.3 So here's our second prediction: the straw that will break the back of a fragile financial system will be the global long bond yield rising by 60 bps within a short space of time - just as it did in 2000, 2007 and 2011. But Bond Yields Haven't Gone Up Far Enough... Yet Now comes some bullish news, at least for those who can play shorter-term moves in the market. The global long bond yield has been trapped within a tight channel and is only 20 bps up from its recent low in April (Chart I-9). Therefore, it has the scope to rise a further 30-50 bps before reaching the tipping point for the global risk-asset edifice and unleashing a 'risk-off' phase. Chart I-9In 2018, The Bond Yield Has Not Risen Sharply...Yet

In 2018, The Bond Yield Has Not Risen Sharply...Yet

In 2018, The Bond Yield Has Not Risen Sharply...Yet

For those who want to fine tune their investment strategy, the journey up to that turning point would define a phase when many of this year's cyclical sector underperformances would end or even switch to a phase of modest outperformances. Bear in mind that the cyclical sector underperformances this year have been substantial: European banks have underperformed healthcare by 35 percent; global basic materials have underperformed the market by 10 percent; emerging market equities have underperformed developed market equities by 15 percent. So it is prudent to take some short-term profits, especially as these trends are likely to end, at least in the near term. Hence, three weeks ago we closed our underweight banks versus healthcare position, booking a tidy profit of 23 percent. Today, we are closing our underweight position in basic materials versus the market, booking a profit of 6 percent. In a similar vein, we are taking the modest profits in our overweight position in 30-year government bonds. Sector allocation has unavoidable implications for stock market allocation - because the mainstream stock market indexes all have dominant sector skews which determine their relative performances (Chart I-10). Chart I-10Italy Vs. Denmark = Banks Vs. Healthcare

Italy Vs. Denmark = Banks Vs. Healthcare

Italy Vs. Denmark = Banks Vs. Healthcare

On this basis, closing our underweight banks versus healthcare removes the justification for being underweight bank-dominant Italy (MIB) and Spain (IBEX) and the justification for being overweight healthcare-dominant Denmark (OMX). These three positions now move to neutral. While we consider our next shift, our European stock market allocation is temporarily reduced to just five positions. Overweight: France, Ireland, Switzerland. Underweight: Sweden, Norway. Finally, just to say that there will be no report next week as I will be attending our annual Investment Conference which is in Toronto this year. I look forward to seeing some of you there. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com 1 Based on the relative performance of the MSCI All Country World Index versus the JP Morgan Global Government Bond Index, both in local currency terms. 2 Please see the European Investment Strategy Weekly Report 'Trapped: Have Equities Trapped Bonds?' September 13 2018 available at eis.bcaresearch.com. 3 Please see the European Investment Strategy Weekly Report 'The Rule Of 4 For Equities And Bonds' August 2 2018 available at eis.bcaresearch.com. Fractal Trading Model* This week, we note that the very strong recent outperformance of U.S. telecoms versus U.S. autos is technically extended, reaching a fractal dimension that has previously signalled the start of a countertrend move. Hence, the recommended trade is short U.S. telecoms, long U.S. autos. Set a profit target of 9% with a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment's fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-11

U.S. Telecom VS. Autos

U.S. Telecom VS. Autos

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report "Fractals, Liquidity & A Trading Model," dated December 11, 2014, available at eis.bcaresearch.com Fractal Trading Model Recommendations Equities Bond & Interest Rates Currency & Other Positions Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Underweight In yesterday's Daily Insight, we highlighted our neutral barbell portfolio in tech, staying overweight secular growth defensive tech sub-sectors (namely S&P software and S&P tech hardware, storage & peripherals, both of which are high-conviction overweights) and underweight the hyper-cyclical chip and chip equipment stocks. With respect to the latter, we think the macro environment has deteriorated. Three factors underpin our negative view on semi equipment's growth prospects and there is no light at the end of the tunnel yet. Bitcoin's (and other cryptocurrencies) collapse is dealing a blow, at the margin, to demand for semi equipment (second panel). Taiwan's financials statement-reported data on IT capex and national data on overall Taiwanese capital outlays corroborates this downbeat demand backdrop (third panel). Finally, the drubbing in EM currencies is sapping purchasing power from the consumer and also warns that things will get worse for U.S. semi equipment stocks before they get better (bottom panel). Bottom Line: Continue to avoid the S&P semis and S&P semi equipment indexes; see Monday's Weekly Report for more details. The ticker symbols for the stocks in these indexes are: BLBG: S5SECO - INTC, NVDA, QCOM, TXN, AVGO, MU, ADI, AMD, MCHP, XLNX, SWKS, QRVO, and BLBG: S5SEEQ - AMAT, LRCX, KLAC, respectively.

Avoid Chip Stocks At All Costs

Avoid Chip Stocks At All Costs

Stay Neutral S&P Tech

Stay…

Neutral The stratospheric rise of tech profits, particularly in the past two years, have done most of the heavy lifting in pulling the S&P 500's profit margin ever higher, pushing the index itself to new all-time highs last month. The implication is that in order for the broad market to suffer a severe blow, tech has to take a hit, and vice versa. On the EPS front, our profit growth model has recently ticked higher from an already extended level, signaling that the profit outlook remains bright (second panel). The news on the operating front is equally encouraging. The San Francisco Fed's tech pulse index - an index of coincident indicators of technology sector activity - is reaccelerating (third panel). Such positivity is offset by the acknowledgment of three material risks. First, the tech sector garners 60% of its revenues from abroad and thus the appreciating U.S. dollar is a significant profit headwind (bottom panel). Second, a rising U.S. inflation backdrop along with the related looming selloff in the bond market should knock the wind out of the tech sector's sails. Third, leading indicators of emerging Asian demand are souring rapidly and were the trade war to re-escalate, EM economic data would retrench further. Bottom Line: We prefer to remain on the sidelines in the S&P information technology sector and sustain a barbell portfolio within the sector. Please see this week's Weekly Report for more details.

Tech On Steroids

Tech On Steroids

Highlights Portfolio Strategy Stick with a neutral weighting in the tech sector as rising interest rates, higher inflation and a firming greenback offset improving industry operating metrics on the back of the virtuous capex upcycle. Chip and chip equipment stocks will remain under pressure as global semi sales are under attack and leading indicators of semi demand suggest that more pain lies ahead at a time when chip selling prices are steeply decelerating. Recent Changes There are no changes to our portfolio this week. Table 1

Party Like It's 2004!

Party Like It's 2004!

Feature Equities regained their footing last week and remain perched near all-time highs. Investors are largely ignoring the trade-related uncertainty and are instead focusing on the upbeat economic backdrop. Both soft and hard data continue to send an unambiguously healthy signal for the U.S. economy, a potent tonic for corporate profitability. Chart 1EPS Will Do All The Heavy Lifting

EPS Will Do All The Heavy Lifting

EPS Will Do All The Heavy Lifting

While a lot of parallels have been drawn between today and the late-1990s, our sense is that the current financial market and economic outlooks resemble more the mid-2000s. Chart 1 shows that, between 2004 and the stock market peak in late-October 2007, forward profit growth estimates peaked at over 20%/annum and the forward multiple drifted steadily lower. Nevertheless, stocks remained well bid and rose alongside forward EPS (top and third panels, Chart 1). In other words, despite decelerating forward profit growth estimates and a contracting forward multiple, expanding forward EPS did the heavy lifting, explaining all of the advance in the SPX. The similarities to today are eerie: while profit growth peaked in Q1/2018, 10% EPS growth is elevated for the tenth year of an expansion, and the forward multiple is coming in (Chart 1). On the policy front, the Bush tax cuts hit in the mid-2000s with the elimination of the double taxation of dividends and a drop in personal income tax rates, along with a one-time cash repatriation of corporate profits stashed abroad. With regard to the economic backdrop, capex was roaring and nominal GDP was firing on all cylinders as a housing bubble was getting inflated. The GDP deflator also hit a high mark. The ISM manufacturing survey eclipsed 61 in 2004 and non-farm payrolls were expanding smartly (Chart 2). But despite all that apparent overheating especially in the housing market, the real fed funds rate was near zero in 2004 (top panel, Chart 3). Finally, a number of financial market metrics were also similar to today. Oil prices were on their way to triple digits, high yield spreads were below 400bps and the VIX probed, at the time, all-time lows (Chart 3). However, one key difference between the mid-2000s and today is the strengthening U.S. dollar. The firming greenback remains a key risk to our positive equity market view (bottom panel, Chart 3), as it will eventually infiltrate EPS. Netting it all out, if history at least rhymes, an earnings-led advance in the SPX is the most likely outcome. Our sanguine cyclical (9-12 month) equity market view remains predicated on a 10%/annum increase in EPS and a sideways-to-lower move in the forward multiple. Meanwhile, wage inflation is slowly starting to rear its ugly head. In fact, we are surprised by the fits and starts in average hourly earnings growth. At this stage of the cycle, wage growth should start galloping higher as executives aggressively bid up the price of labor in order to fill job openings and bring expansion plans to fruition. A simple wage growth indicator comprising resource utilization and the unemployment gap suggests that wage inflation will really kick into higher gear in the coming 12 months (shown as a Z-score, Chart 4). Chart 2Eerie...

Eerie…

Eerie…

Chart 3...Parallels With 2004

...Parallels With 2004

...Parallels With 2004

Chart 4Mind The Return Of Inflation

Mind The Return Of Inflation

Mind The Return Of Inflation

Two weeks ago we highlighted that the S&P 500's profit margins are benefiting from lower corporate taxes and muted wage growth, a goldilocks backdrop. Despite evidence of a pending inflationary impulse, as long as businesses are successful in passing rising input costs down the supply chain and onto the consumer, then margins and EPS will continue to expand. Nevertheless, deconstructing the SPX's all-time high profit margins is in order. Chart 5 & Chart 6 show the 11 GICS1 sector profit margin time series using Standard & Poor's data, and Chart 7 is a snapshot of Q2/2018 profit margins for the 11 sectors and the broad market. Chart 5Sectorial Profit ...

Sectorial Profit …

Sectorial Profit …

Chart 6...Margin Breakdown

...Margin Breakdown

...Margin Breakdown

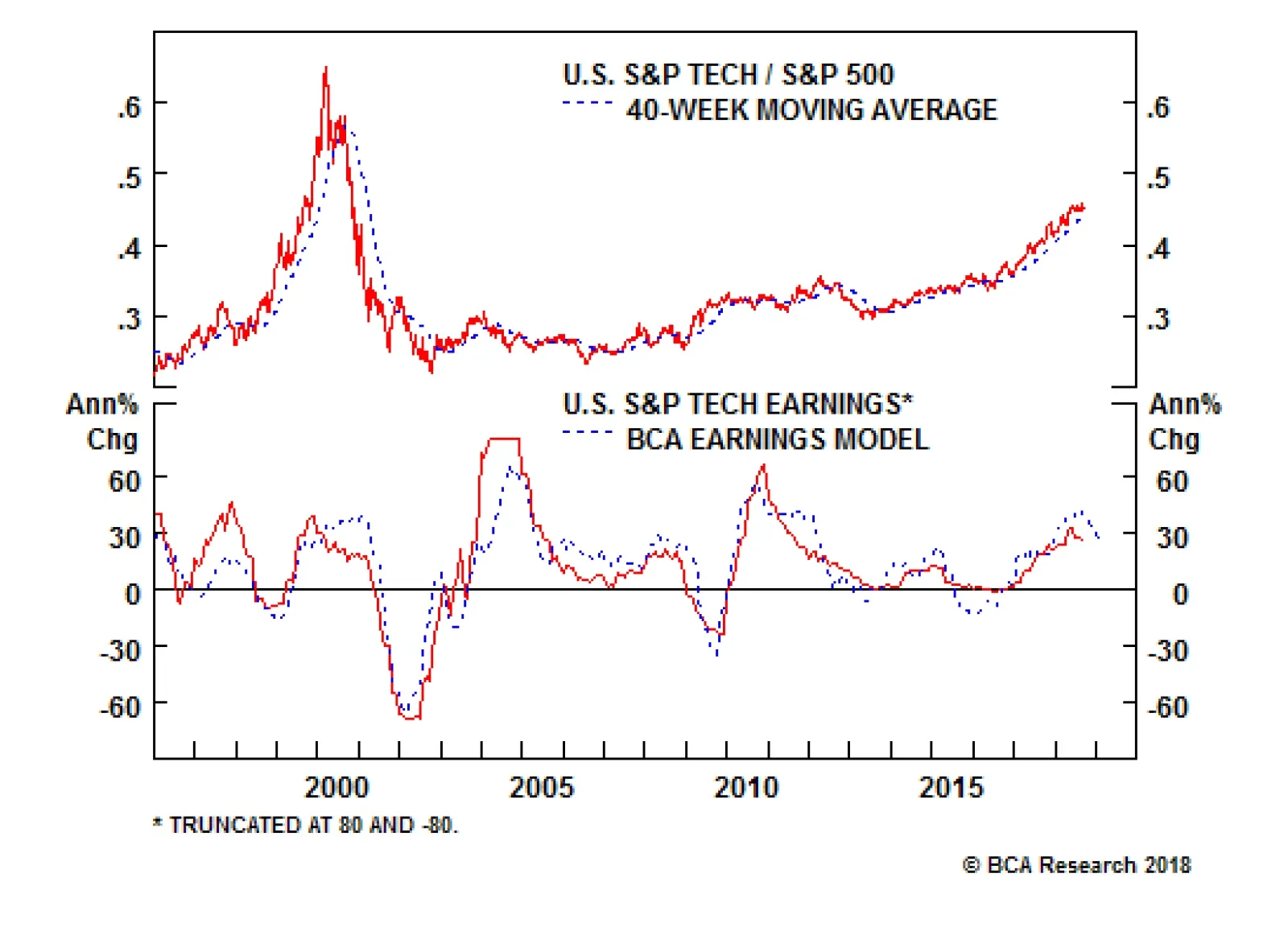

Chart 7Tech Is A Clear Outlier

Party Like It's 2004!

Party Like It's 2004!

Five sectors (tech, industrials, materials, consumer discretionary and utilities) are enjoying record-high profit margins, and four (financials, consumer staples, telecom services and real estate) are on the verge of joining that club. This leaves two sectors with declining margin profiles: health care and energy. While most sectors are +/- five percentage points away from the S&P 500, the tech sector sports profit margins at twice the level of the SPX or eleven percentage points higher and is the clear outlier (Chart 7). The implication is that the broad market's EPS fortunes are closely tied to the high-flying tech sector that commands a 26% market cap weight. Thus, this week we are compelled to highlight the deep cyclical tech sector, and two of its hyper-sensitive and foreign exposed subcomponents. Tech On Steroids In late-August we published a chart on tech margins (which we are reprinting today) showing the upward force they have exerted on the broad equity market for the better part of the past decade (top panel, Chart 8). Naturally, stratospheric profits must underpin these parabolic margins. The middle panel of Chart 8 highlights that since 2006 tech EPS have almost quadrupled, pulling SPX profits higher. As a reminder, the S&P tech sector commands a 24% profit weight in the S&P 500, the highest since the history of this data series and almost double the weight during the previous cycle's peak (bottom panel, Chart 8). The implication is that in order for the broad market to suffer a severe blow, tech has to take a hit, and vice versa. Chart 8Secular Tech EPS Growth Has Boosted Margins

Secular Tech EPS Growth Has Boosted Margins

Secular Tech EPS Growth Has Boosted Margins

Chart 9EPS Growth Model Flashing Green

EPS Growth Model Flashing Green

EPS Growth Model Flashing Green

On the EPS front, our profit growth model has recently ticked higher from an already extended level, signaling that the profit outlook remains bright (Chart 9). The virtuous capex upcycle - BCA's key theme for the year - remains the key driver behind our EPS model. Chart 10 shows that the tech sector continues to make inroads in the overall capex pie, according to financial statement-reported data, and has now doubled its share since the GFC trough to roughly 12%. National accounts corroborate this data and underscore that pent up demand is getting unleashed, following a near 15-year hibernation period (bottom panel, Chart 10). The news on the operating front is equally encouraging. The San Francisco Fed's tech pulse index - an index of coincident indicators of technology sector activity1 - is reaccelerating. Tech new orders-to-inventories are also picking up steam and suggest that sell side analysts have set the relative EPS bar too low (Chart 11). Finally, the latest PCE report revealed that consumer outlays on tech goods are also gaining momentum, even relative to overall consumer spending. While this upbeat backdrop would point to an above benchmark tech allocation, three risks keep us at bay. First, the tech sector garners 60% of its revenues from abroad and thus the appreciating U.S. dollar is a significant profit headwind, especially for 2019 when the delayed negative FX translation effects will most likely emerge (third panel, Chart 12). Chart 10Capex On The Upswing...

Capex On The Upswing…

Capex On The Upswing…

Chart 11...Underpinning Tech Operating Metrics...

...Underpinning Tech Operating Metrics…

...Underpinning Tech Operating Metrics…

Chart 12...But Three Risks Keep Us At Bay

...But Three Risks Keep Us At Bay

...But Three Risks Keep Us At Bay

Second, a rising U.S. inflation backdrop along with the related looming selloff in the bond market should knock the wind out of the tech sector's sails. Tech business models are built to withstand deflation and thrive in a disinflationary environment. Thus, when inflation re-emerges, tech stocks suffer (CPI and 10-year UST yield shown inverted, top two panels, Chart 12). Third, leading indicators of emerging Asian demand are souring rapidly and were the trade war to re-escalate, EM in general and tech-laden Korean and Taiwanese economic data in particular would retrench further (bottom panel, Chart 12). Bottom Line: We prefer to remain on the sidelines in the S&P information technology sector and sustain a barbell portfolio within the sector. As a reminder we continue to express our bullishness via two high-conviction overweight defensive tech sub-sectors, S&P software and S&P tech hardware, storage & peripherals (THSP), and our bearishness via avoiding their early cyclical peers, S&P semis and S&P semi equipment. Avoid Chip Stocks At All Costs While we are neutral the broad tech sector and prefer secular growth defensive tech sub-sectors, we continue to recommend shying away from chip and chip equipment stocks. Chart 13 shows the extreme sensitivity to changes in final demand of chip related stocks versus their defensive tech peers. In more detail, software and THSP indexes are in a secular advance with regard to EPS outperformance, whereas semis and semi equipment profits are hyper-cyclical with mean-reverting relative profit profiles. Granted, the commoditization of semiconductors explains this close correlation with the business cycle. But, as we highlighted last November when we put the semi equipment index on the high-conviction underweight list, extrapolating EPS growth euphoria far into the future was fraught with danger.2 In fact, late-November 2017 marked the peak in semi equipment performance versus the overall IT sector, confirming the early cyclical nature of chip stocks (Chart 14). Chart 13Bifurcated EPS

Bifurcated EPS

Bifurcated EPS