Sectors

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and developed market rates cuts will likely be too modest and come too late to save the day. Nimble investors or those highly sensitive to tracking error should not be underweight stocks over the coming 3-6 months. Over a 6-12 month time horizon, we continue to recommend that investors remain underweight global equities versus US$-hedged long-maturity developed market government bonds. Section II is a guest report written by Martin Barnes, BCA’s former Chief Economist. Martin revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.

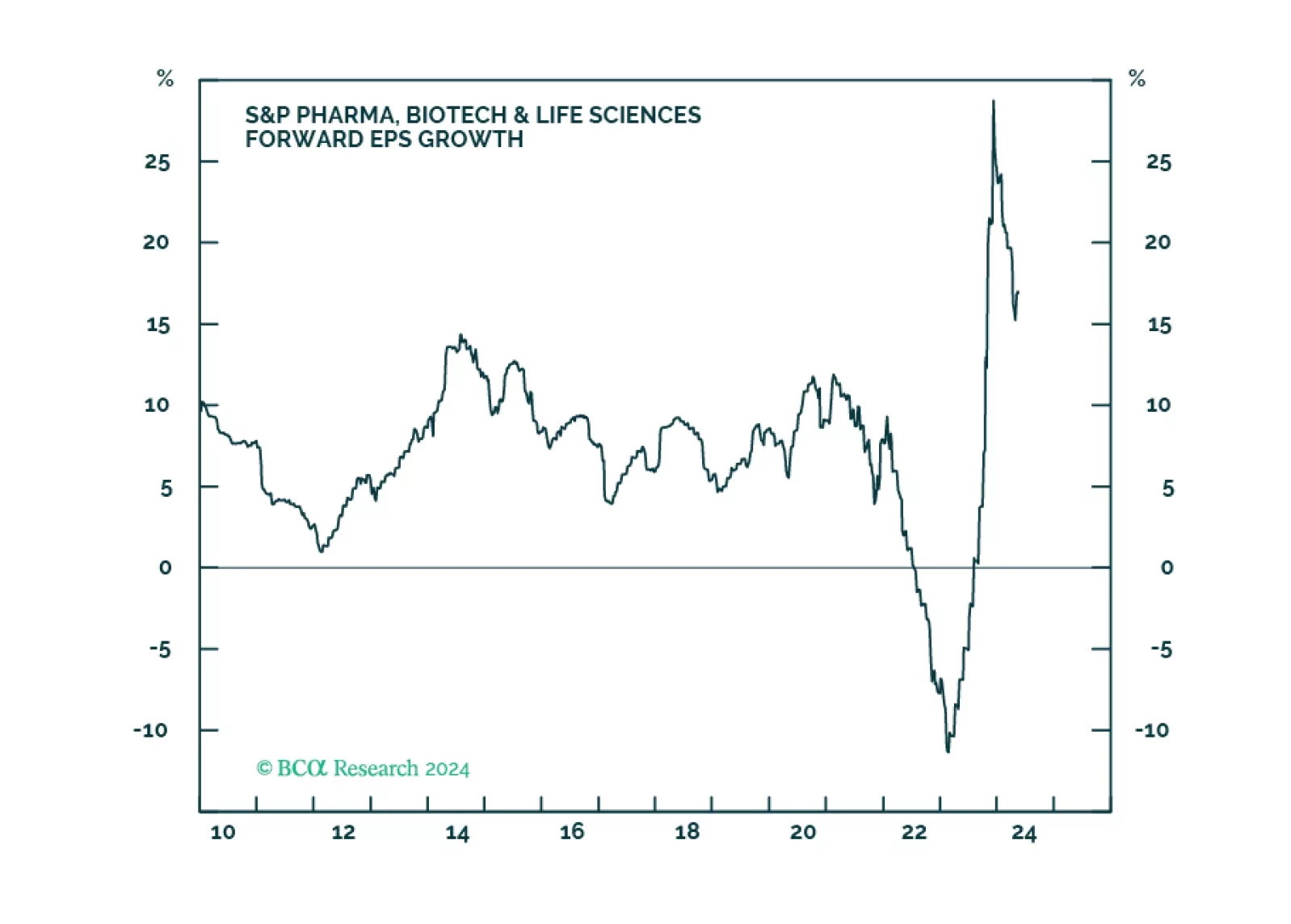

We recommend overweight in Pharma over a tactical and strategic investment horizon, as challenges, that have recently hampered the industry group’s performance, are dissipating. Likely election outcomes are positive for the industry, while major trends like generative AI applied to drug development and an aging population are long-term tailwinds.

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.

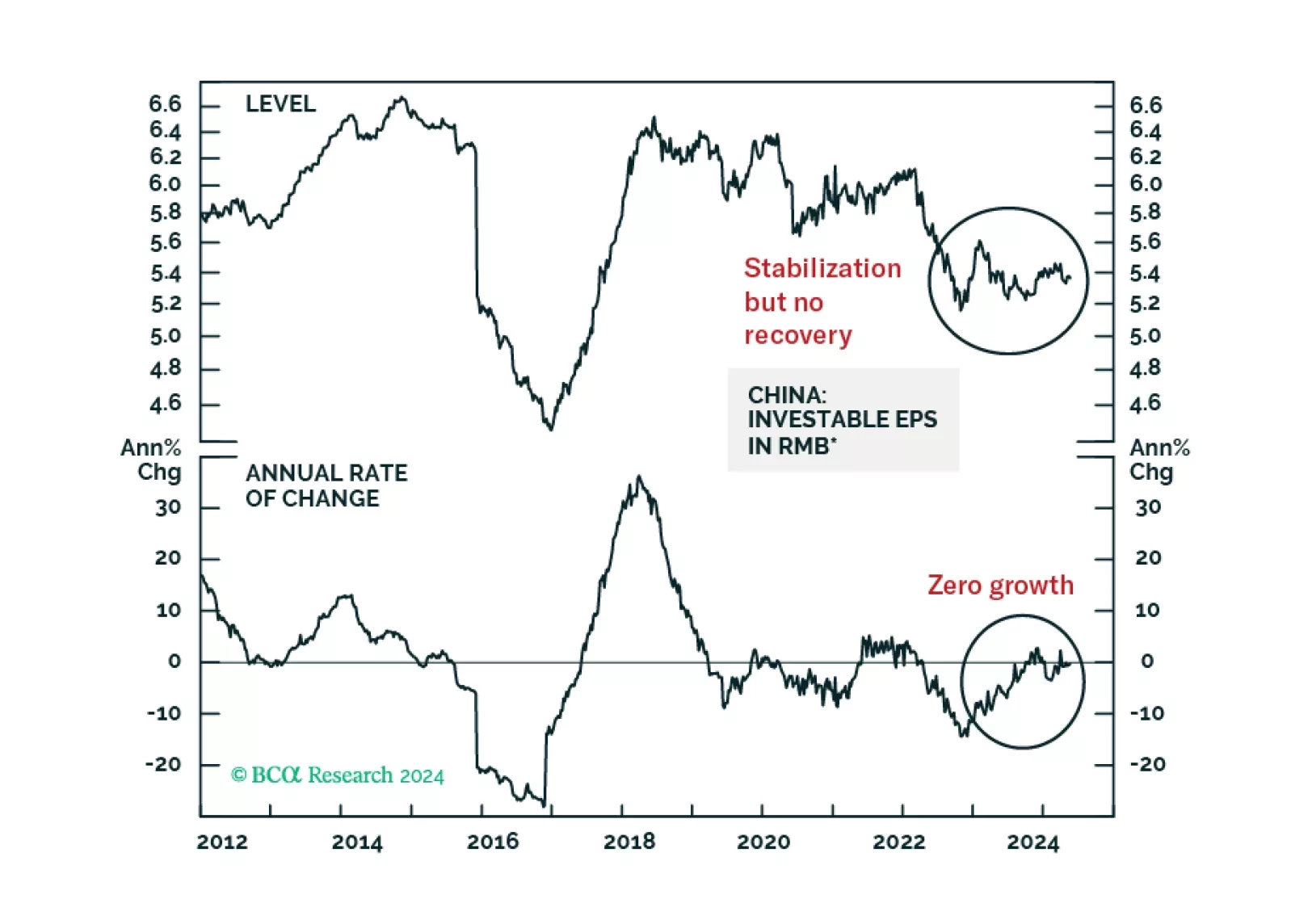

The RMB 500 billion program is small, as it is equivalent to only 4% of property developers' total funding from the past 12 months. This will preclude a recovery in property construction this year. Corporate profits will determine the path of China’s share prices on a cyclical time horizon. Deflation in China will persist for now, which will depress corporate profits even if volumes grow modestly.

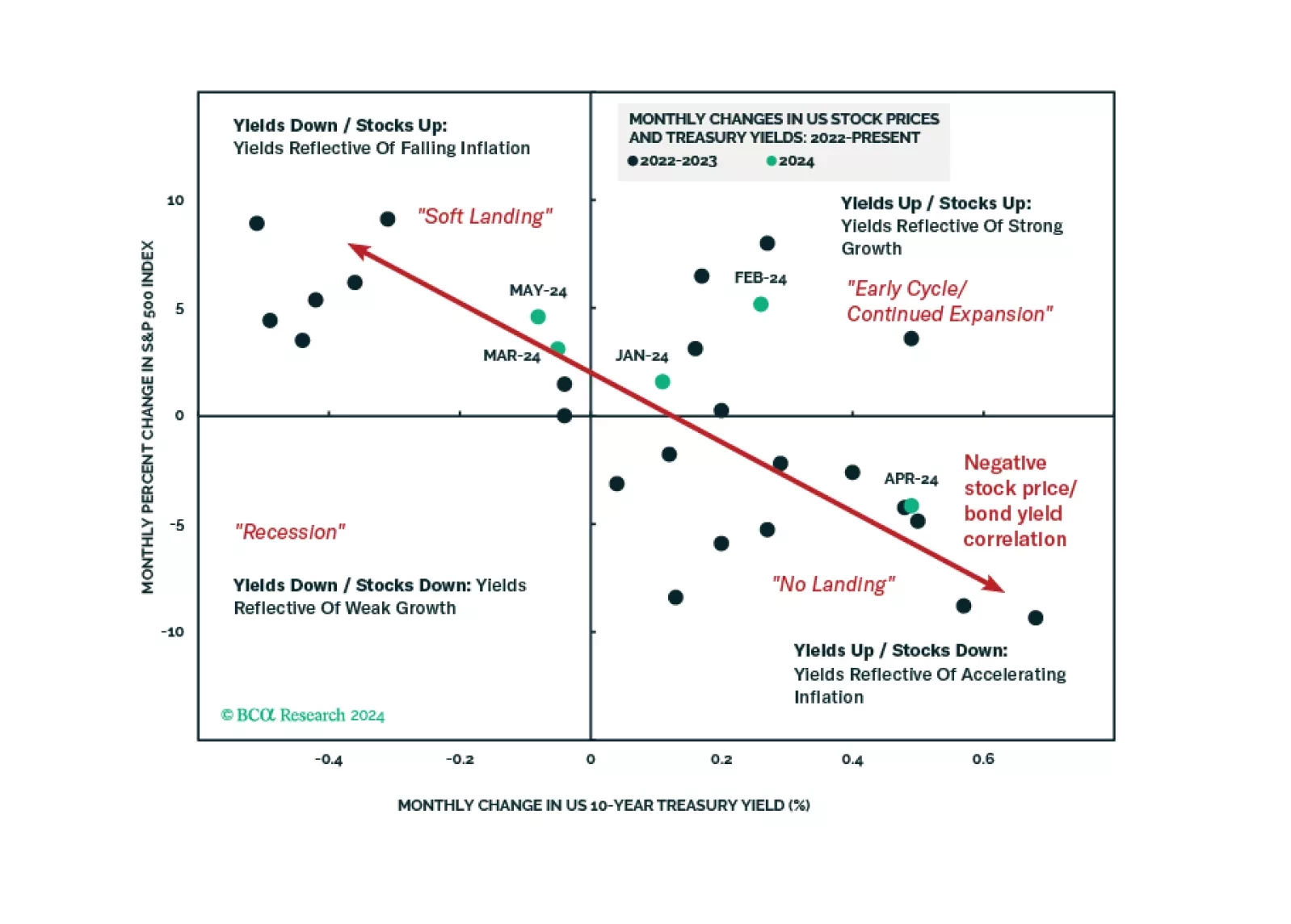

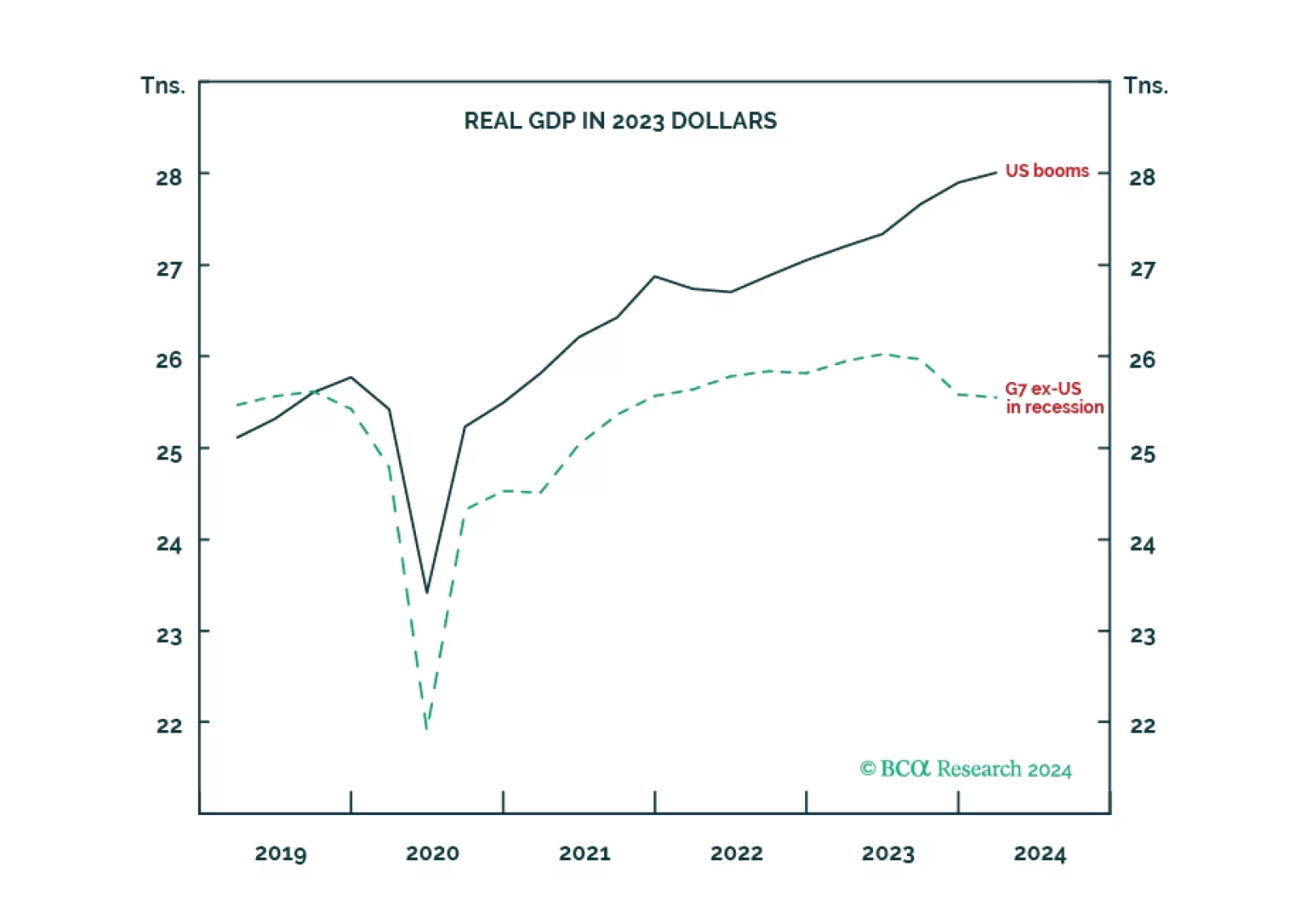

The economic schism in the world economy, between the non-US developed economy in recession and the US in strong growth, is unprecedented during our lifetimes. Now the schism will continue in reverse, as the non-US developed economy rebounds while the US fades. There are important implications for rates, the dollar, and sector and regional equity allocation which we discuss. Plus: base metals are a tactical short.

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

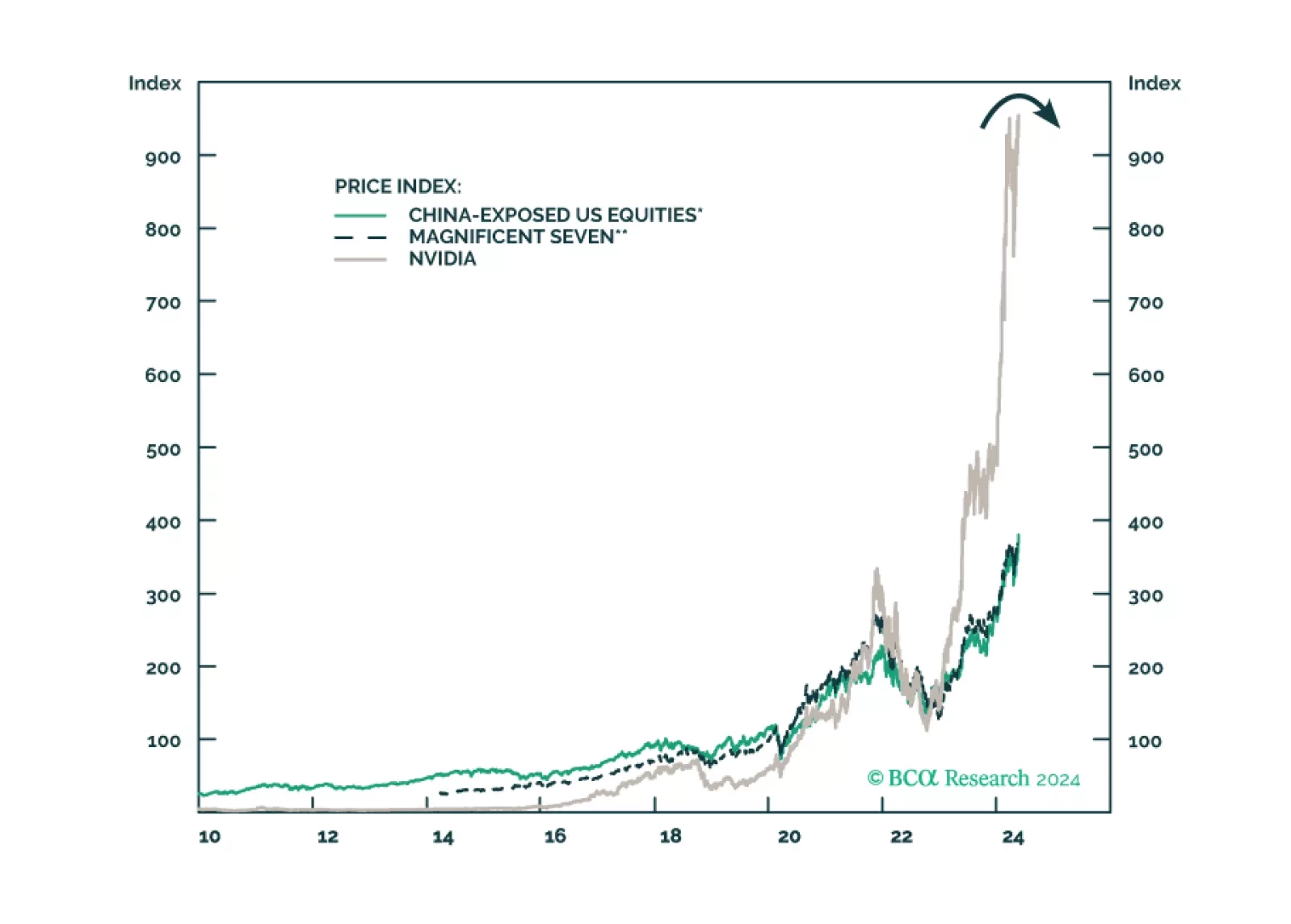

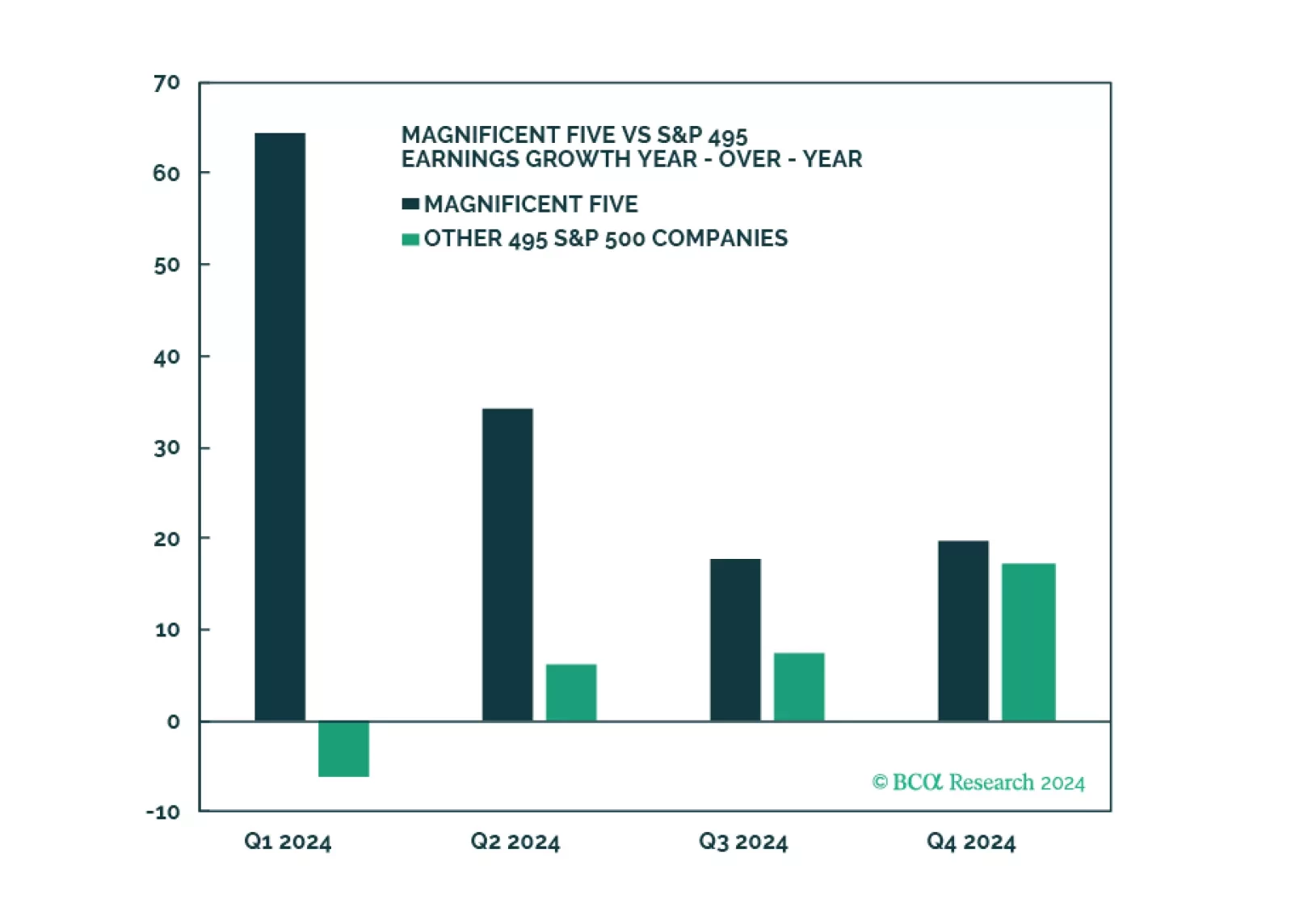

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is expected to broaden into yearend. Companies are optimistic about the economy. Development of AI applications is in full swing, but few companies are monetizing them yet. Consumer spending is strong but is slowing. We reiterate our underweight of consumer sectors, and overweight of Software and Services as the “don’t fight AI” adage holds.