Sectors

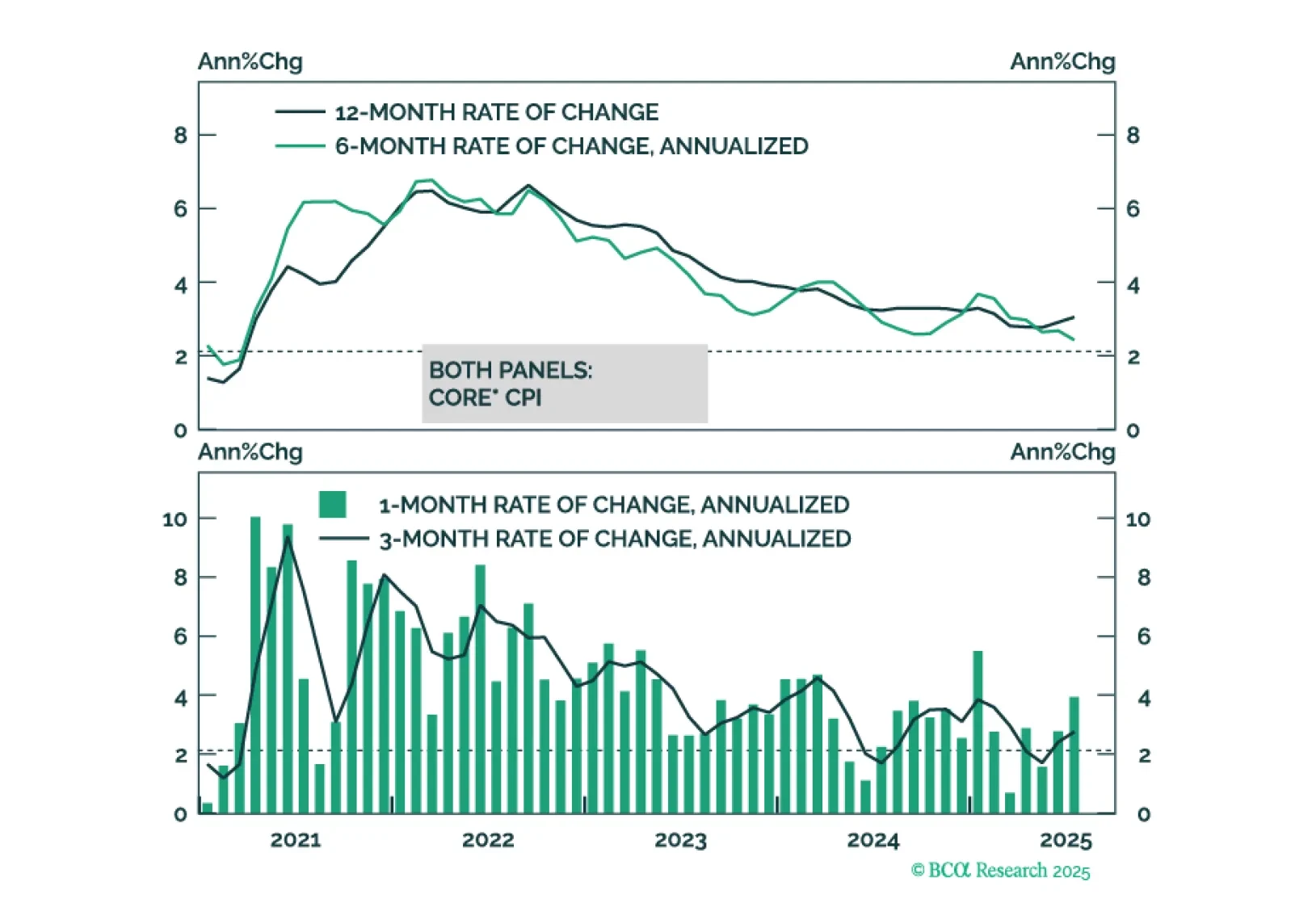

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

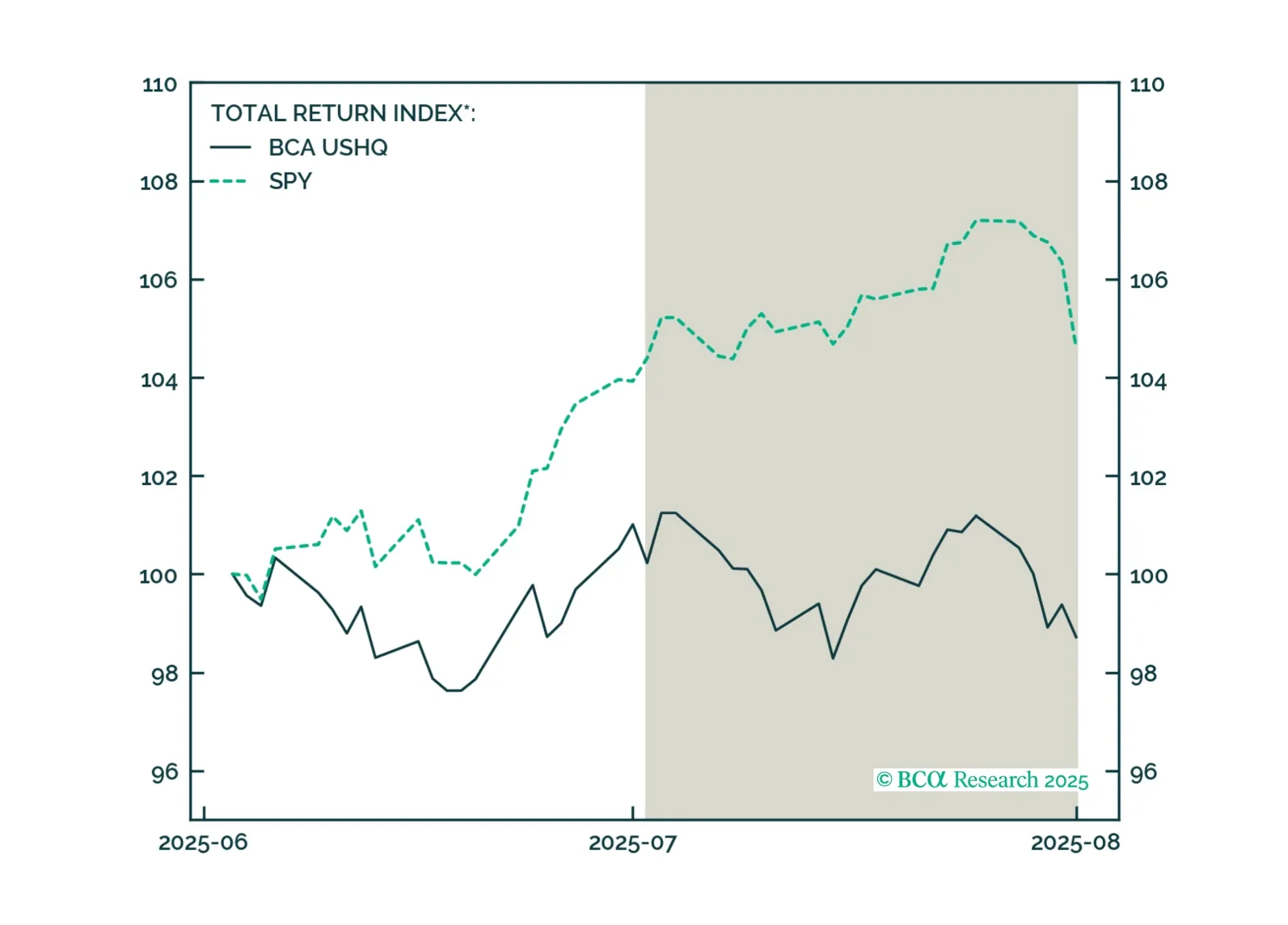

The US High Quality (USHQ) portfolio underperformed its benchmark through July, returning -1.5%, whilst its SPY benchmark returned 0.2%. On a trailing three-month basis, performance was notably weak vs. benchmark, with USHQ underperforming by approx. 750bps.

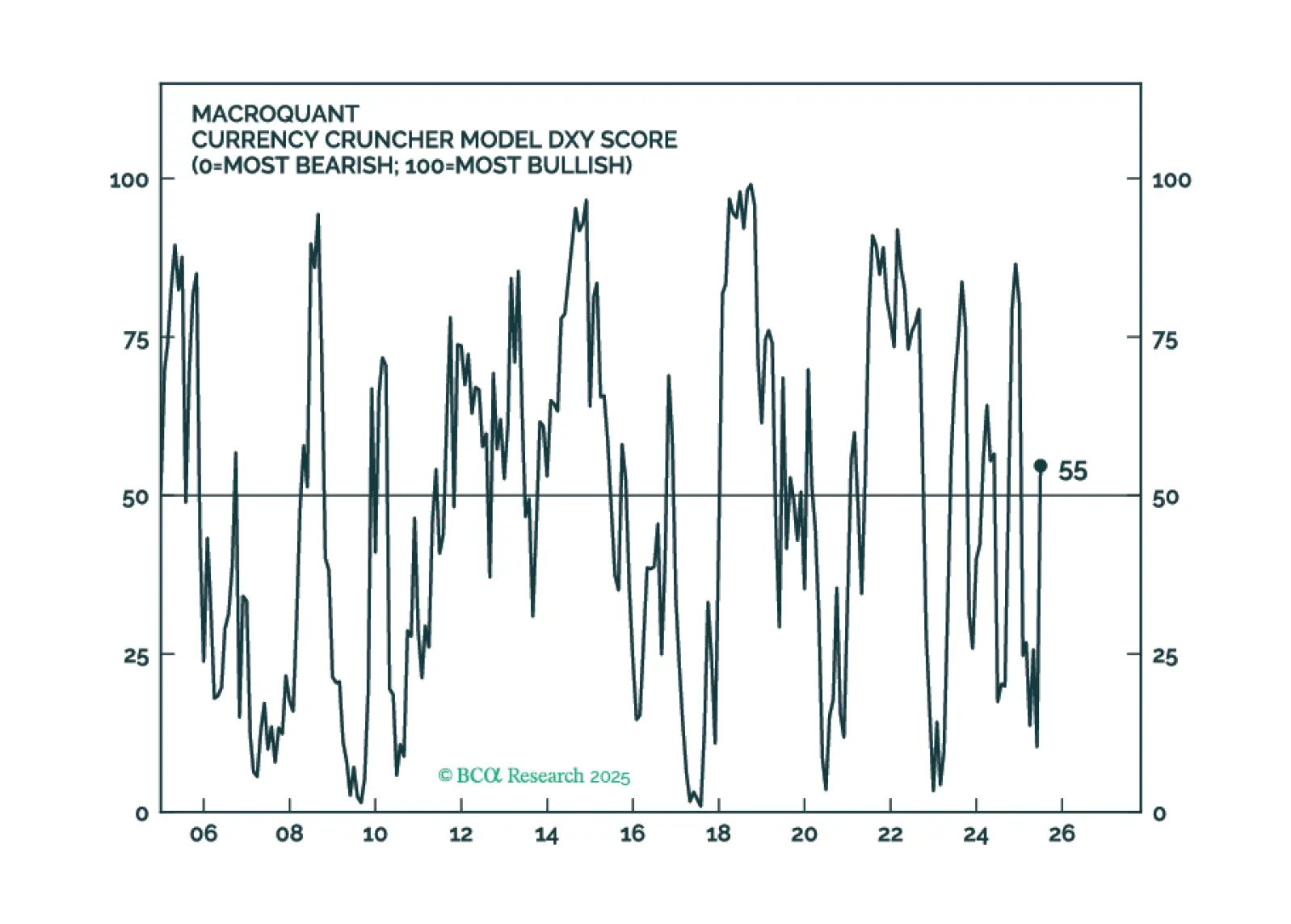

MacroQuant is recommending that equity investors keep their finger near the eject button but avoid pressing it for now. The model is warming up to the dollar again and sees scope for oil prices to rise.

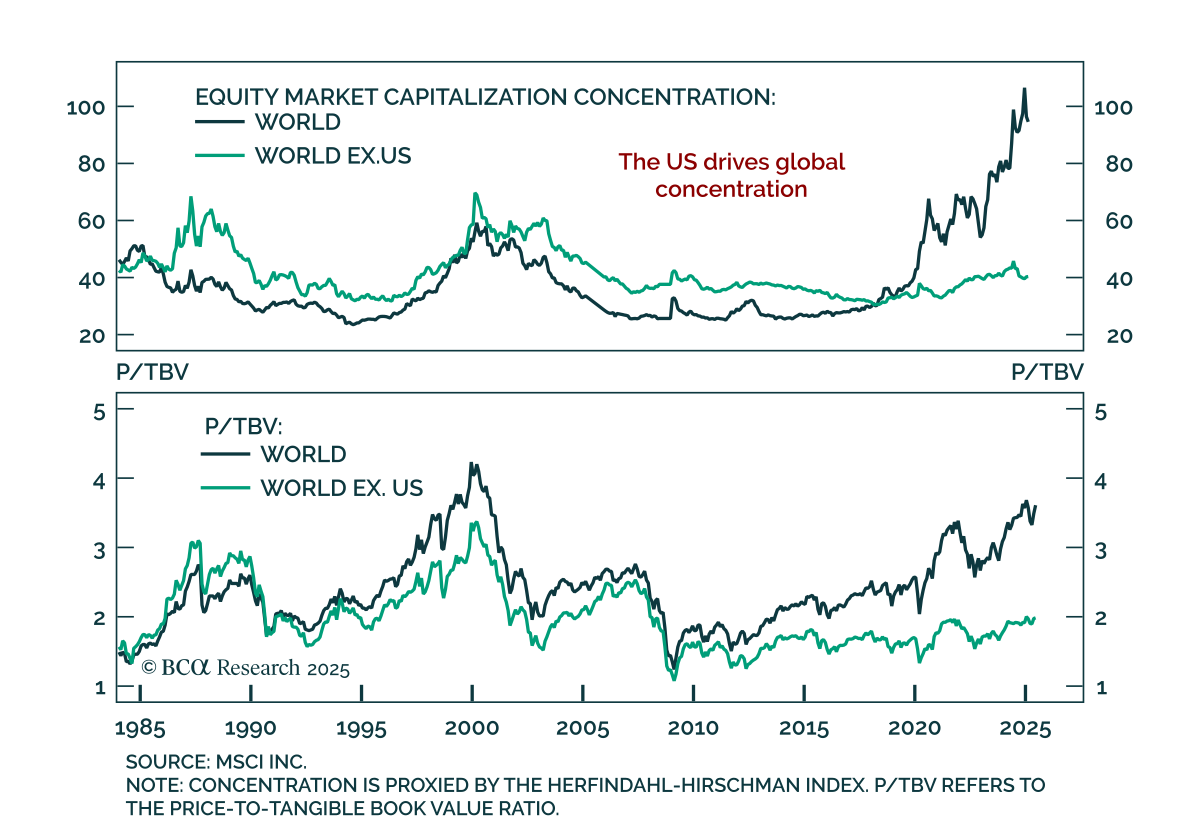

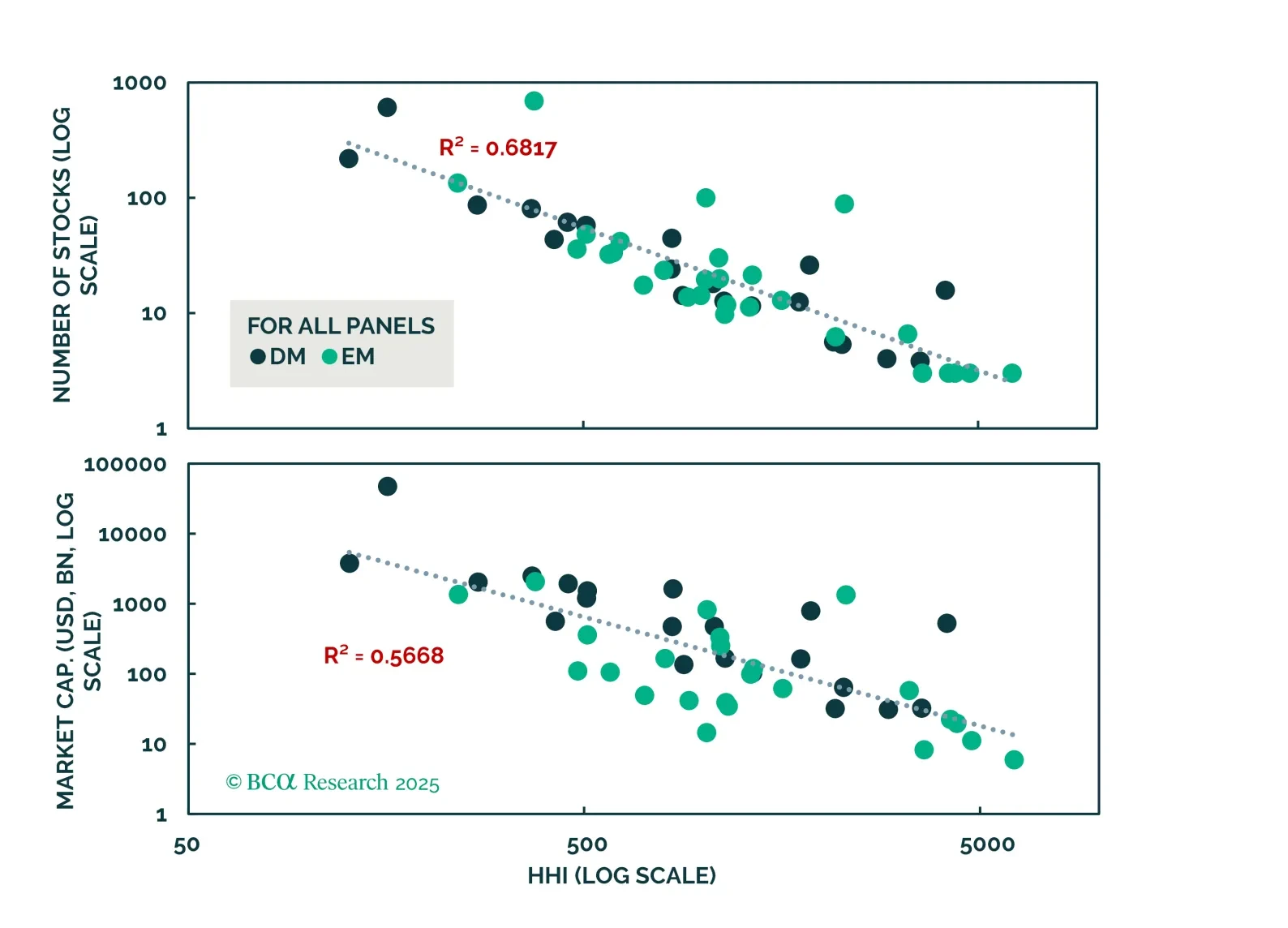

Using stock-level data for MSCI ACWI country indices going back to 1984 for Developed markets and 1988 for Emerging markets, we find that market concentration adds little predictive power for long term forward returns. Whatever predictive power it has disappears once we include traditional metrics like value and size. The same is true for idiosyncratic index risk. Index concentration is just not very important for determining risk and return in equity markets.

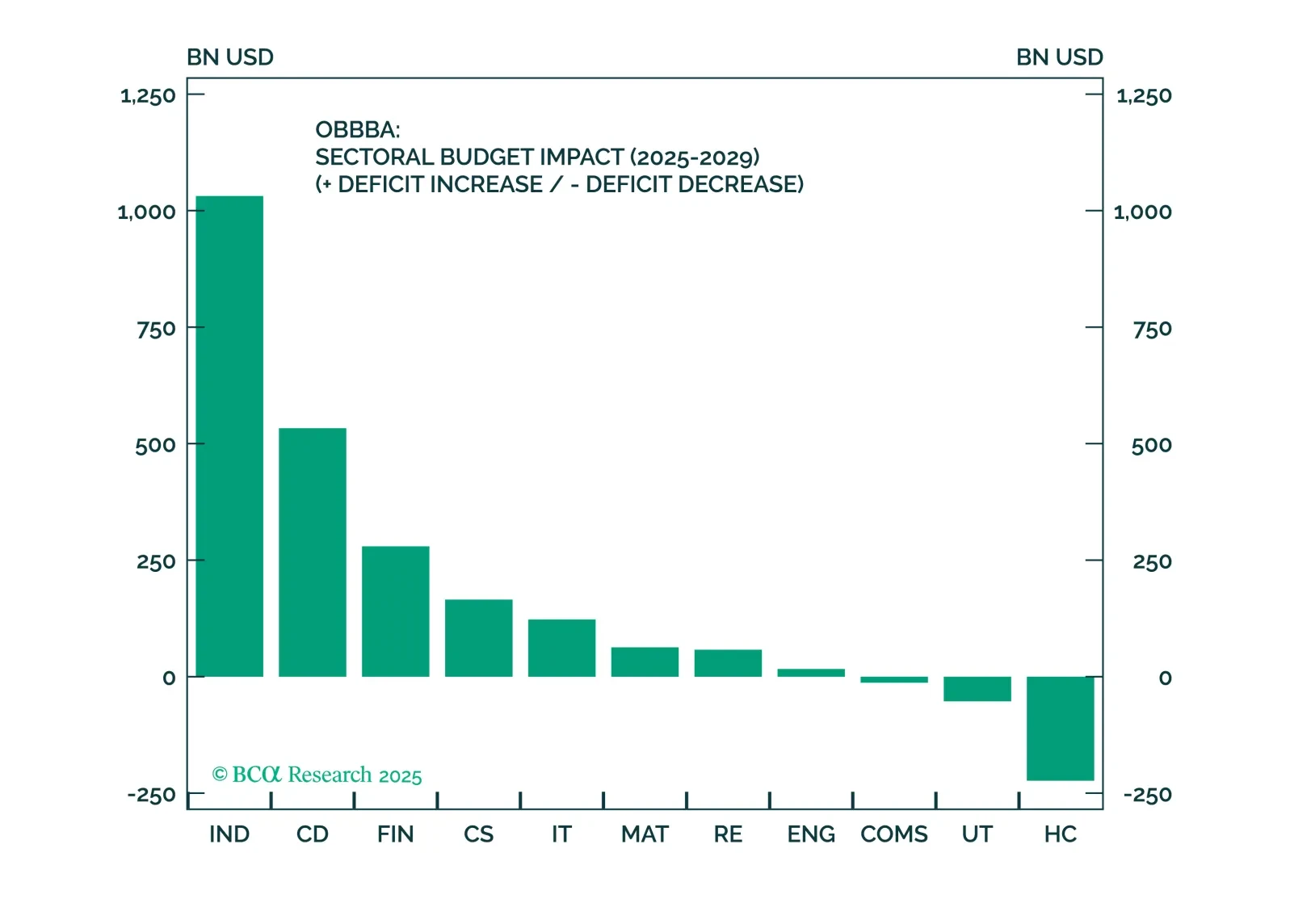

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

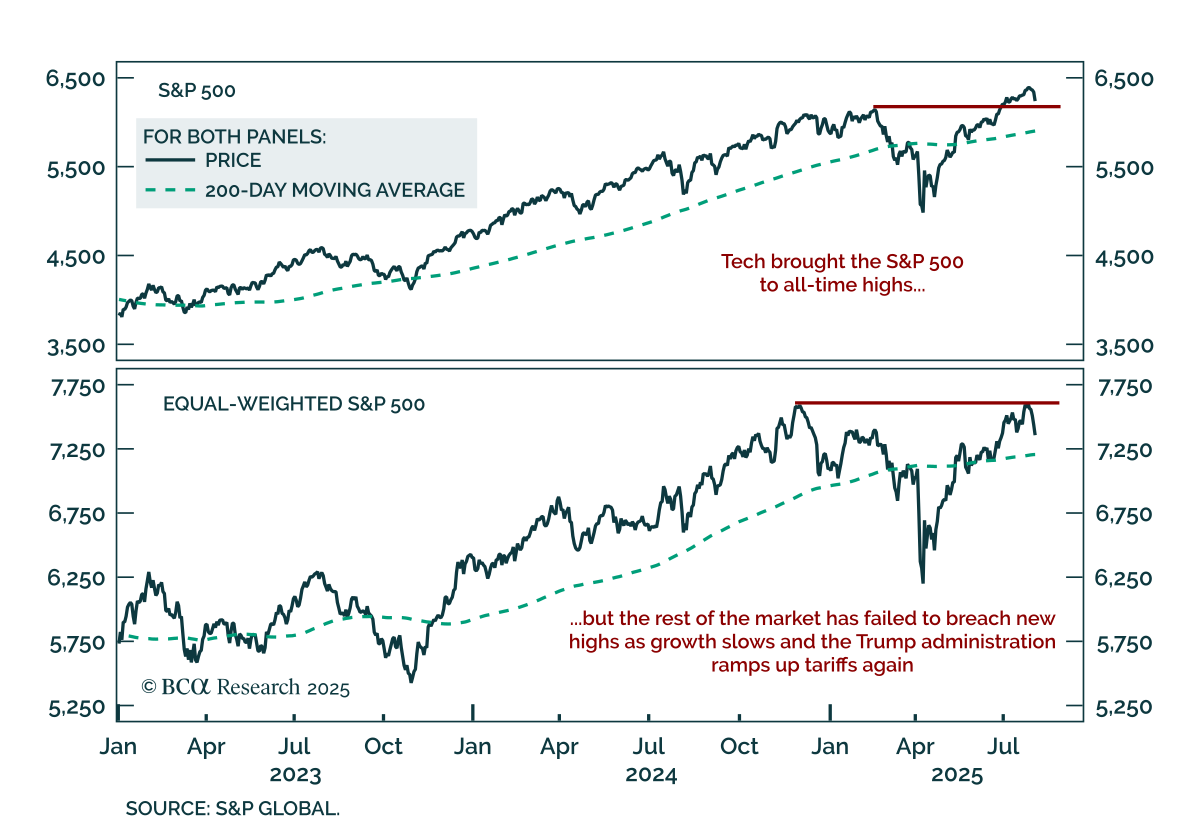

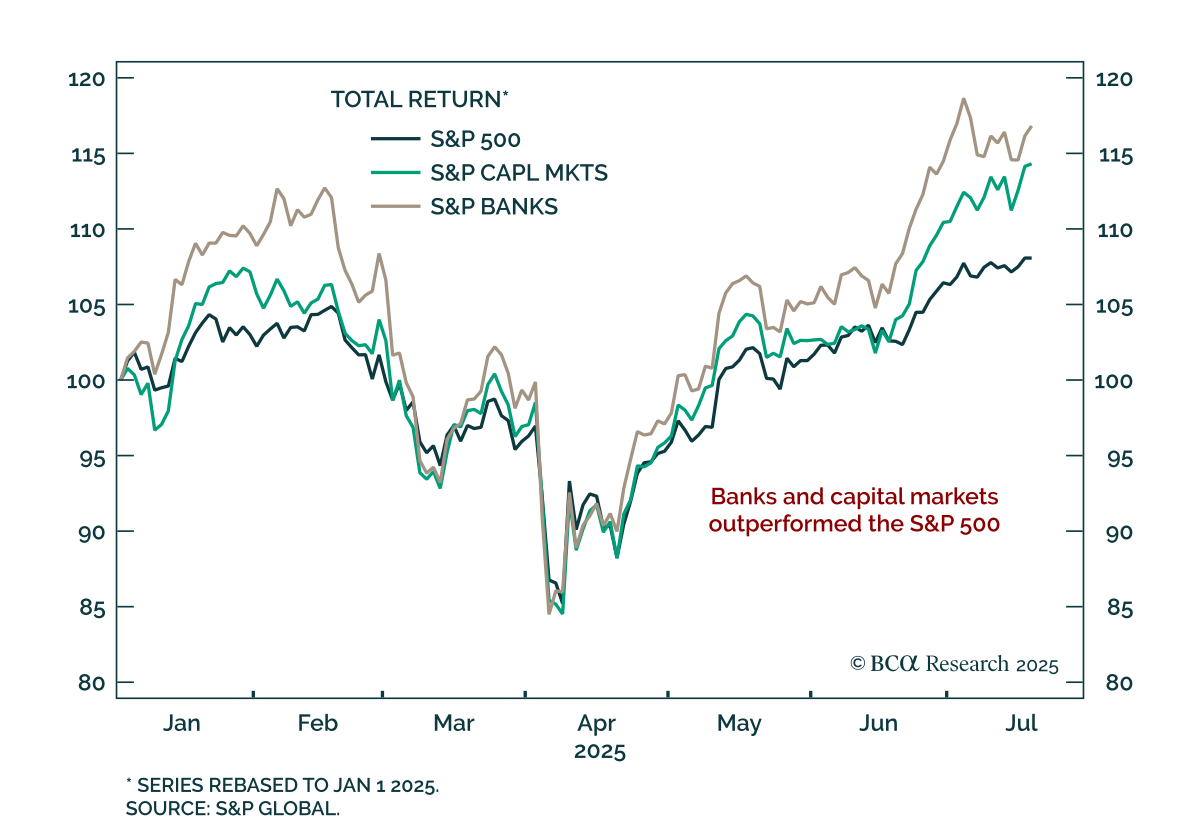

Earnings growth should continue to support equity performance this year. However, after blockbuster gains, some profit-taking is likely. We recommend booking profits and increasing exposure to Defensives.