Sectors

Dear Client, We will be working on our 2022 Outlook for China, which will be published on December 8. Next week we will be sending you BCA Research’s Annual Outlook, featuring long-time BCA client Mr. X, who visits towards the end of each year to discuss the economic and financial market outlook for the year ahead. Best regards, Jing Sima China Strategist Feature In meetings with our North American clients this past week, we expressed the view that China’s economic growth is on a downward trend and easing measures have been gradual and modest in scope. Most clients agreed that China’s economy faces tremendous headwinds, however, some investors were more optimistic about the outlook for Chinese stocks in the next 6 to 12 months. Valuations in both China’s onshore and offshore equity markets have dropped to multi-year lows and macro policies have started to ease. Cheaply valued Chinese stocks should have more upside in the wake of policy support. Policy tone recently pivoted to a more growth supporting bias, but the existing easing measures will not offset the deceleration in both credit growth and domestic demand. China’s economic activity may worsen before it stabilizes in mid-2022. Moreover, China’s financial markets do not seem to have priced in the economic weakness. Therefore, in the next one to two quarters, risks to Chinese stocks are tilted toward the downside. Chart 1Chinese Stocks Will Truly Bottom When The Economy Troughs

Chinese Stocks Will Truly Bottom When The Economy Troughs

Chinese Stocks Will Truly Bottom When The Economy Troughs

Below are some of the main questions from our meetings and our answers. Q: Policies have started to be more pro-growth. Why do you still underweight Chinese stocks? A: There are two reasons that we maintain a cautious view on Chinese stocks for at least the next six months, in both absolute terms and relative to global equities. First, we do not think that the magnitude of existing easing measures is sufficient to offset the economy’s downward momentum. Secondly, China’s business cycle lags credit growth by about six to nine months. The timing of a turnaround in the economy and stock prices may be later than investors have priced in. In short, we need to see more reflationary measures and a rebound in credit growth to have a legitimate macro fundamental basis to overweight Chinese stocks (Chart 1). Credit growth on a year-on-year basis stopped falling in October. The underlying data in credit creation, however, points to a weakening in demand for corporate loans (Chart 2). Loans to the housing sector are well below a year ago (Chart 3). Chart 2Weakening Loan Demand

Weakening Loan Demand

Weakening Loan Demand

Chart 3Bank Loans To The Housing Sector Have Not Turned Around

Bank Loans To The Housing Sector Have Not Turned Around

Bank Loans To The Housing Sector Have Not Turned Around

Chart 4It Will Take Time For Policy Easing To Restore Confidence In The Corporate Sector

It Will Take Time For Policy Easing To Restore Confidence In The Corporate Sector

It Will Take Time For Policy Easing To Restore Confidence In The Corporate Sector

Despite an acceleration in local government bond issuance in October and RMB300 billion in additional bank loans to support small and medium enterprises, growth in medium- to long-term corporate loans peaked (Chart 4). In previous cycles, a rollover in corporate demand for longer-term bank lending on average lasted more than nine months, suggesting that any policy adjustments will take a while to restore confidence in the corporate sector. Without a decisive pickup in credit growth, corporate earnings growth will be at risk of deteriorating. Moreover, policy tightening since earlier this year is still working its way through the economy and major economic indicators in China continue to decline (Chart 5). We think that China’s economy is set to decelerate even more in the next several months, suggesting that earnings uncertainty will likely rise. This, combined with reactive policymakers, already slowing earnings momentum, and a downward adjustment in 12-month forward earnings, suggests that investors have not yet reached the maximum bearishness for Chinese stock prices (Chart 6). Chart 5No Signs Of Improvement In The Economy

No Signs Of Improvement In The Economy

No Signs Of Improvement In The Economy

Chart 6The Earnings Adjustement Process Is Only Beginning

The Earnings Adjustement Process Is Only Beginning

The Earnings Adjustement Process Is Only Beginning

Q: What is the impact of China’s property market slowdown on the economy? Will recent policy easing stop deterioration in the real estate sector? A: Policy has been recalibrated by relaxing restrictions on mortgage lending and rules for land sales.1 However, the negative financing loop among developers, households and local governments may take longer to improve. Meanwhile, the market may underestimate the downside risks in housing-related activity in the next 6 to 12 months. Chart 7Households' Home Buying Intentions Have Plummeted

Households' Home Buying Intentions Have Plummeted

Households' Home Buying Intentions Have Plummeted

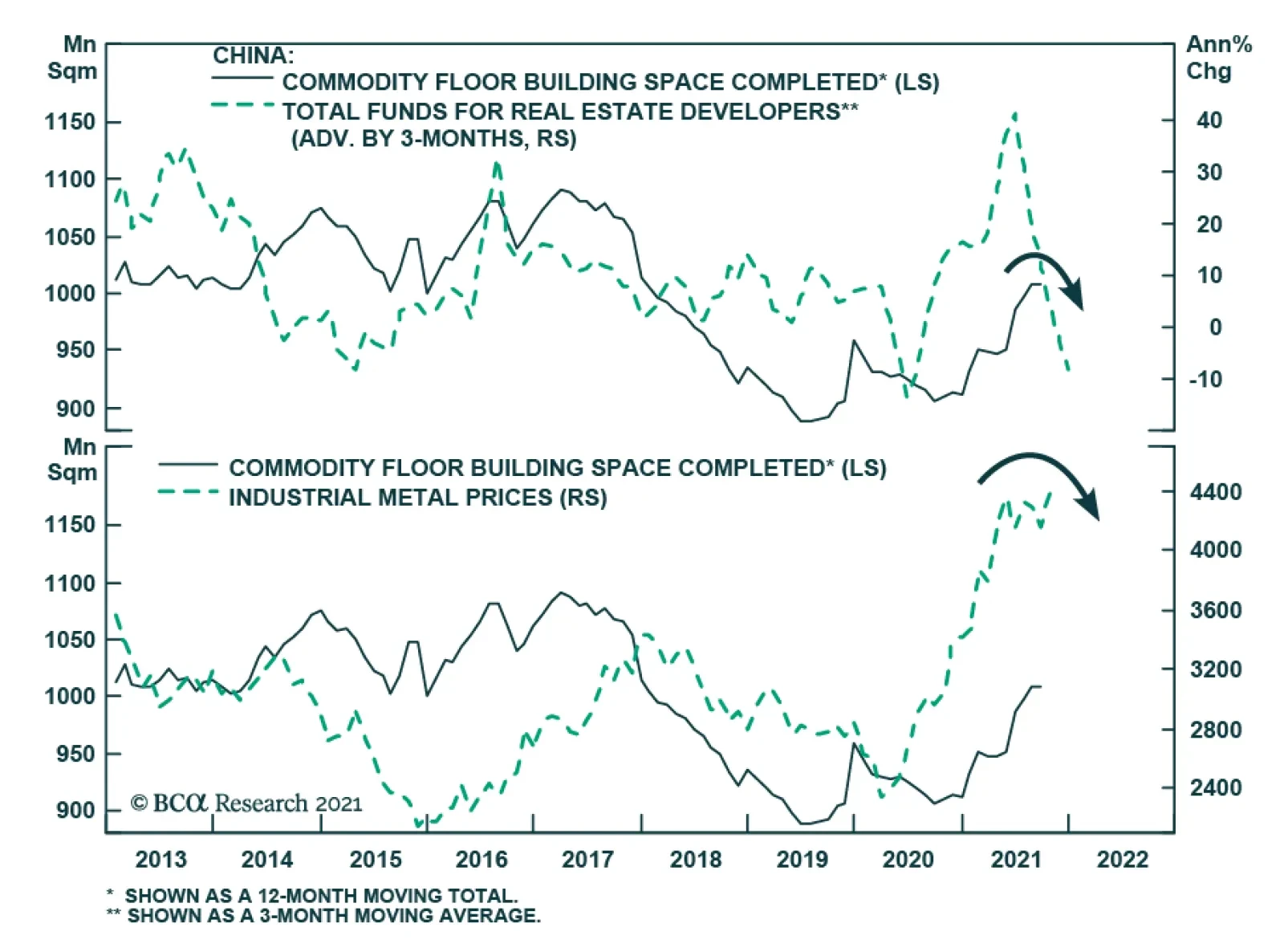

Our view is based on the following: Home sales will likely remain in contraction in the next two quarters. Aggressive crackdowns on property market speculation in the past 12 months have fundamentally shifted consumers’ expectations for future home prices. The impending pilot property tax reform2 (details yet to be disclosed) will only encourage the wait-and-see sentiment of potential buyers. Home sales contracted by 24% in October from a year ago. In previous cycles, contractions in home sales normally lasted for more than 12 months. Moreover, the proportion of households planning to buy a house dropped to only 7.7% in Q3 2021 from 11.6% in Q4 2020 (Chart 7). Real estate developers have slashed new projects and land purchases to preserve liquidity for debt servicing (Chart 8, first and second panels). Policymakers may succeed in prompting banks to resume lending to developers in order to alleviate the escalating risk of widespread defaults. However, so far the marginal easing has failed to reverse the downward trend in bank credit to developers along with home sales (Chart 8, third and bottom panels). Funding constraints for real estate developers will probably be sustained for another six months, despite the recent easing measures. Construction activity, housing starts, and real estate investment will likely remain in doldrum at least through 1H22 (Chart 9). Chart 8Housing Activities Are Still Falling

Housing Activities Are Still Falling

Housing Activities Are Still Falling

Chart 9Less Funding = Less Investment And Completions

Less Funding = Less Investment And Completions

Less Funding = Less Investment And Completions

The marked reduction in land sales will impede local governments’ revenues and weigh on infrastructure investment (Chart 10). Real estate and infrastructure financing contributed 50% of the increase in total Chart 10Local Government Revenues Largely Depend On The Housing Sector

Local Government Revenues Largely Depend On The Housing Sector

Local Government Revenues Largely Depend On The Housing Sector

social financing in 2020. Given that local governments face funding constraints from a slump in land sale incomes, policies on leverage from local government financing vehicles (LGFVs) will have to meaningfully loosen up to allow a rise in bank lending to support infrastructure investment. As discussed in previous reports, an acceleration in local government special-purpose bond issuance can only partially offset weak credit growth. Furthermore, shadow banking activity, which comprises LGFV borrowing and is highly correlated with China’s infrastructure investment growth, remains in contraction and indicates that growth in infrastructure investment is unlikely to rebound strongly (Chart 11). The sharp weakening of real estate construction activities will drag down the demand for building materials, machinery, home appliances and automobiles. Real estate accounts for about 60% of Chinese households’ wealth, thus any substantial drop in home prices will further weaken households’ propensity to consume (Chart 12). Chart 11More Easing Needed For A Meaningful Pickup In Infrastructure Investment

More Easing Needed For A Meaningful Pickup In Infrastructure Investment

More Easing Needed For A Meaningful Pickup In Infrastructure Investment

Chart 12Falling Demand For Commodities And Consumer Goods

Falling Demand For Commodities And Consumer Goods

Falling Demand For Commodities And Consumer Goods

Chart 13AOn The Surface Housing Inventories Are Lower Than Six Years Ago...

On The Surface Housing Inventories Are Lower Than Six Years Ago...

On The Surface Housing Inventories Are Lower Than Six Years Ago...

There are nontrivial risks that the real estate slowdown will evolve into a downturn similar to that of 2014-15. Although the existing housing inventory is more modest than the start of the 2014/15 property downturn, developers have accumulated more debt and unfinished projects in this cycle than in the past (Charts 13A & 13B). Policymakers will have to relax property sector policies much more forcefully to prevent the downturn from intensifying. In the interim, we will likely witness more deterioration in the sector. Chart 13B...But Developers Have Built Up Massive Leverages And Hidden Inventories In The Past Three Years

...But Developers Have Built Up Massive Leverages And Hidden Inventories In the Past Three Years

...But Developers Have Built Up Massive Leverages And Hidden Inventories In the Past Three Years

Q: If the property market accounts for such a big portion of local governments’ revenues, why hasn’t the waning housing market forced policymakers to loosen restrictions? A: We think regulators have been slow to backtrack property market reforms because this year China’s fiscal deficit has narrowed from last year due to lower government spending and improved income from corporate taxes. In previous property market downturns, such as 2011/12, 2015/16 and 2019, property policy restrictions were lightened following major declines in government revenues (Chart 14). However, in 2021 China’s fiscal balance sheet has been stronger than in previous cycles; central and local governments have collected much more taxes, particularly corporate taxes, than in 2020 (Chart 15). Meanwhile, government expenditures so far this year have been lower, resulting in a large improvement in the country’s fiscal deficit (Chart 16). Chart 14Falling Gov Revenues Forced Policymakers To Backtrack Reforms In The Past...

Falling Gov Revenues Forced Policymakers To Backtrack Reforms In The Past...

Falling Gov Revenues Forced Policymakers To Backtrack Reforms In The Past...

Chart 15...But This Year Gov Tax Revenues Have Been Strong

...But This Year Gov Tax Revenues Have Been Strong

...But This Year Gov Tax Revenues Have Been Strong

Chart 16Fiscal Deficit Improved This Year Despite Falling evenues From Land Sales

Fiscal Deficit Improved This Year Despite Falling evenues From Land Sales

Fiscal Deficit Improved This Year Despite Falling evenues From Land Sales

As discussed above, slightly loosened restrictions on land purchases by some regional governments will not restore developers’ confidence and boost the demand for land. The sharp increase in government's corporate tax collection will also start to ebb as economic growth slows and corporate profits decline. As such, even if government expenditures remain the same next year, the fiscal deficit will grow because revenues will be under substantial downward pressure. We expect that Chinese policymakers will have to take more actions to stabilize fiscal conditions. Forecasting exactly when this will occur is difficult, but a benign government balance sheet in much of this year is delaying policymakers’ response to the flagging housing market. Meantime, both policymakers and investors may be complacent about the state of the economy until the full scale of the property sector spillover risk becomes clear. Q: Rates are low and industrial profit growth has been strong this year. Why has capex been so sluggish? A: Investment growth in the manufacturing sector has been lackluster because their profit margins have been squeezed by rising input costs. On the other hand, investment in the mining industry has been constrained by policy restrictions. An acceleration in China’s de-carbonization efforts this year has likely constrained investment in the mining sector. Even though industrial profit growth has been concentrated among the upstream industries such as mining which profits grew by a stunning 100% this year, investment in the sector was mostly flat from a year ago (Chart 17). During the first half of the year, mid- to downstream firms were caught between rising input prices and a weak recovery in domestic consumption. Manufacturing investment grew faster than the mining sector, but manufacturing profit growth only increased by about 30% year to date (Chart 18). However, we think manufacturing investment growth may improve slightly into 2022 as the sector continues to gain pricing power. Chart 17Mining Sector's Profit Growth Way Outpaced Investment

Mining Sector's Profit Growth Way Outpaced Investment

Mining Sector's Profit Growth Way Outpaced Investment

Chart 18Manufacturing Sector Profit Growth Has Been Much More Muted Than Upstream Industries

Manufacturing Sector Profit Growth Has Been Much More Muted Than Upstream Industries

Manufacturing Sector Profit Growth Has Been Much More Muted Than Upstream Industries

Q: The RMB has been strong against the dollar, despite China’s maturing business cycle. What is your outlook for the RMB next year? A: The RMB exchange rate has been boosted by China’s record current account surplus, wide interest rate differentials and speculation that tension between the US and China will abate. However, all three favorable conditions supporting the RMB are in danger of reversing next year. Chart 19The RMB Has Been Appreciating Despite A Strong USD

The RMB Has Been Appreciating Despite A Strong USD

The RMB Has Been Appreciating Despite A Strong USD

Chart 20The RMB's Appreciation Deviates From Economic Fundamentals

The RMB's Appreciation Deviates From Economic Fundamentals

The RMB's Appreciation Deviates From Economic Fundamentals

Despite broad-based dollar strength, the CNY/USD has appreciated by 4.5% year to date (Chart 19). The RMB’s appreciation deviates from China’s economic fundamentals (Chart 20). Strong global demand for goods has boosted Chinese exports while travel restrictions curbed foreign exchange outflows by domestic households (Chart 21). China-US real interest rate differentials have been in favor of the CNY versus USD, bringing net foreign inflows to China’s onshore bond market (Chart 22). Additionally, the recent meeting between President Joe Biden and President Xi Jinping has prompted speculation that the US will lessen tariffs on Chinese imports. Chart 21Large Current Account Surplus

Large Current Account Surplus

Large Current Account Surplus

Chart 22Favorable Interest Rate Differentials And Strong Fund Inflows

Favorable Interest Rate Differentials And Strong Fund Inflows

Favorable Interest Rate Differentials And Strong Fund Inflows

Chart 23China's Extremely Robust Export Growth Unlikely To Sustain In 2022

China's Extremely Robust Export Growth Unlikely To Sustain In 2022

China's Extremely Robust Export Growth Unlikely To Sustain In 2022

Chart 24A Strong RMB Does Not Bode Well For Chinese Exporters' Profits

A Strong RMB Does Not Bode Well For Chinese Exporters' Profits

A Strong RMB Does Not Bode Well For Chinese Exporters' Profits

These factors will likely turn against the CNY next year. First, export growth will moderate as the composition of US consumption rotates from goods to services (Chart 23). Secondly, it would not be in the PBoC’s best interests to let the RMB strengthen too rapidly because an appreciating currency would be a deflationary force on China’s export and manufacturing sectors (Chart 24). While we expect policymakers to maintain their preference for a gradual approach to stimulus, we assign a high probability to a reserve requirement ratio (RRR) cut in early 2022. In this environment, Chinese bond yields will decline, which would narrow the China-US interest rate differential. Finally, while there may be some changes to US tariffs on China, it is doubtful that there would be a broad-based removal of tariffs. Chart 25The CNY/USD Will Likely Fall And Converge To Chinese Stocks' (Under)performance

The CNY/USD Will Likely Fall And Converge To Chinese Stocks' (Under)performance

The CNY/USD Will Likely Fall And Converge To Chinese Stocks' (Under)performance

The CNY’s outperformance stands out as it marks a break from its correlation with China’s relative equity performance vis-à-vis the US (Chart 25). The signal from the currency suggests that either global equity investors are overly pessimistic about economic and regulatory risks in China, or overly optimistic about the value of China’s currency. The latter option is more likely at the moment, and the CNY/USD exchange rate is at the risk of converging to the underperformance of Chinese investable stocks next year. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 China Cities Ease Land Bidding Rules as Property Stress Spreads - Bloomberg 2 China’s Pilot Property Tax Reforms Benefit Markets Despite Short-Term Pain, Analysts Say - Caixin Global Market/Sector Recommendations Cyclical Investment Stance

Highlights Last month we published a report on the US corporate margins, titled “Marginally Worse.” In the report, we concluded that margins are likely to contract next year, hobbled by a slowdown in top-line growth, falling productivity, a decline in corporate pricing power, and soaring costs of labor and materials. Q3-2021 – another stellar earnings season: Companies achieved superior earnings growth and expanded margins. However, many companies guided down for Q4-2021 and 2022 citing mounting challenges, such as higher costs of labor, shipping, and raw materials. As such, deciphering which sectors are best positioned to maintain profitability is of paramount importance. Framework for Sector Margin Scorecard: We introduce a framework to rank the S&P 500 sector based on the expected resilience of their margins. It is based on four factors that provide a uniform basis for comparison across all sectors, despite their inherent differences in cost structure, effects of input costs, and ability to manage prices. The four factors driving changes in operating margins are: Sell-side operating margins forecasts as a concise summary of bottom-up company trends Pent-up demand for the sector’s products proxied by the difference between annualized sales growth in 2020 and 2021 and long-term annualized sales growth Pricing power or ability to pass on costs to customers Degree of operating leverage or ability to spread costs when sales volume increases Sectors with most resilient margins: According to this scorecard, Financials, Healthcare, Energy, and Utilities are in the best position to preserve operating margins (Table 1). Table 1Sector Margins Scorecard

Sector Margins Scorecard

Sector Margins Scorecard

Energy Sector - Upgrade to Overweight The medium-term supply/demand backdrop is highly supportive of the current crude oil prices, with a Brent price target of $81 and upside price risk due to inadequate capex. Margins are still below the pre-pandemic peak and the street expects them to increase by 7.74 percentage points over the next 12 months. High operating leverage converts growing demand from the global economic recovery into profitability. Financials – Overweight: O/W Banks, EW Insurance While sell-side analysts anticipate Financials margins will decline, we believe that margins may surprise on the upside: The sector has high operating leverage, is somewhat insulated from supply chain disruptions, sees green shoots in loan growth, and its pricing power is improving. Further, the BCA house view expects the 10-year Treasury yield will rise to 2.0% - 2.25% by the end of 2022, supporting net interest margins. Healthcare - Overweight: O/W Medical Equipment and Services, EW Pharma In July we published a report on the Healthcare sector, titled “Checking The Pulse: Deep Dive Into The Health Care Sector” and upgraded it to Overweight. The Healthcare sector is one of the most resilient sectors profitability-wise as, being defensive in nature, its sales are unaffected by changes in economic demand. The street expects margins to expand by over 2% over the next 12 months. Further, there is still significant pent-up demand for the health care services, and specifically for the elective procedures – the most lucrative segment of the Healthcare Sector. Pricing power has recently picked up. Feature Last month we published a report on US corporate profit margins, titled “Marginally Worse.” In that report, we took a close look at corporate margins by analyzing their key drivers. We have concluded that margins are likely to contract next year, driven by a slowdown in top-line growth, falling productivity, and a decline in corporate pricing power. The sales side of the margin equation will fail to offset upward cost pressures imposed by the tight labor market, soaring input prices and transportation costs, rising depreciation expense, and a potential increase in tax rates. We also developed a simple model that encapsulates all the moving parts (Chart 1). Our forecast, based on the model, reiterates that the path of least resistance for US corporate margins is lower.

Chart 1

In this report, we will take a close look at the S&P 500 sectors to gauge their ability to grow earnings and preserve margins. We aim to rank them by their ability to maintain profitability. Q3-2021 Earnings Season: Stellar Results Operating sector margins are a focal point for investors in the current environment of soaring shipping costs, PPI readings unseen for the last forty years, and a wage-price spiral that may lead to prolonged periods of elevated inflation. While rising costs have been a concern for a while now, the Q3-2021 earnings season has surprised on the upside, with 81% of companies exceeding analyst earnings expectations. Earnings increased by 42% year-over-year and sales 17%. The two-year annualized growth rate (CAGR) for S&P 500 earnings is 14.6% and 5.7% for sales. The pandemic trough has been all but forgotten, and earnings are back to their trend (Chart 2).

Chart 2

Chart 3

All sectors, except for Industrials and Consumer Discretionary, have earnings and sales that exceed pre-pandemic levels (Chart 3). Energy, Materials, and Tech enjoyed annualized eps growth over the past two years in excess of 20%. And of course, because of such robust earnings growth, most sectors have reached 2010 -2021 peak margins (Chart 4). And these are unprecedented high peaks: Most sectors’ margins are more than two standard deviations away from their five-year averages. From a statistical standpoint, Z-scores in this “zip code” indicate that the probability of even higher margins is minuscule (Chart 5).

Chart 4

Chart 5

How were companies able to achieve such stellar earnings growth and peak margins despite all the cost and supply chain disruption headwinds? The answer is strong sales growth, efficiency in managing suppliers, ability to pass on costs to customers by raising prices, and finally, high operating leverage. Here is what happened in the words of the companies: Home Depot: “Professional home improvement contractors have had huge backlogs of work to do, and impatient customers have in many cases been willing to pay up in order to get the goods needed despite supply chain problems.” Microsoft: "We do have good understanding of lead times required to meet the capacity and signals that we’re seeing. I think we do a good job managing that. It’s not to say we’re not impacted. Multiple suppliers are important to be able to manage through that, and I feel the team has done a very good job.” Union Pacific Corporation: "The Union Pacific team successfully navigated global supply chain disruptions, a major bridge outage, and additional weather events to produce strong quarterly revenue growth and financial results." Honeywell: "Our disciplined approach to productivity and pricing helped deliver a strong third quarter despite an uncertain global environment marked by supply chain constraints, increasing raw material inflation, and labor market challenges.” Coca-Cola: Our results through the first nine months of 2021," CEO Frank Harrison said, "reflect a strong balance of volume growth, price realization, and prudent expense management." However, there are also multiple cracks in the foundation, with companies such as Target and Amazon guiding lower both for Q4-2021 and 2022 citing higher costs of labor, shipping, and raw materials. As such, deciphering which sectors can maintain profitability is of paramount importance. Building A Sector Margin Scorecard So which sectors have the best ability to preserve or even expand margins over the next year? Forecasting profitability by sector is tricky, as every sector is different, and has disparate drivers of sales and costs, making cross-sectional comparisons challenging. However, we have an advantage – we are not aiming to predict a point estimate for each sector margin a year from now, but rather rank all sectors from best to worst in terms of their ability to maintain profitability. To do so, we have created a scorecard based on four factors that provide a uniform basis for comparison across all sectors, despite their inherent differences in cost structure, effects of input costs, and ability to manage prices. These factors also implicitly incorporate a potential mean reversion, i.e., high readings are unlikely to move even higher. Four factors capturing future changes in the profit margins are: Sell-side forecasts of operating margins over the next 12 months as a concise summary of bottom-up company trends Pent-up demand for the sector’s products proxied by the difference between 2019-2021 sales CAGR and long-term annualized sales growth Pricing power or ability to pass on costs to customers Degree of operating leverage or ability to spread costs when sales volume increases Factor 1: Expected Change In Operating Margins Over The Next 12 Months Top-down sector margin expectations for the next 12 months are an aggregation of the bottom-up company forecasts. Since the stock market is a market of stocks, this is an important summary of companies' trends which we incorporate into our ranking framework. In line with our view, sell-side analysts expect S&P 500 margins to contract by 1.2% over the next 12 months. Margin contraction is expected across the board with two notable exceptions: Energy and Healthcare. In the scorecard, we rank sectors based on the expected magnitude of the margin change, such that sectors with the least compression, or outright growth, are scoring better (Chart 6).

Chart 6

Factor 2: Pent-up Demand For The Sector’s Products Most sectors have enjoyed a fantastic sales and earnings recovery this year (Chart 7), with sales exceeding pre-pandemic levels thanks to strong consumer demand.

Chart 7

However, to gauge the level of pent-up demand for each sector, we compare 2020-2021 CAGR of sales growth with a long-term sales growth rate. We call this factor “sales growth differential.” Our thinking is that if recent sales growth is below a pre-pandemic normal, there is still demand left on the table. For example, the Consumer Discretionary sector is not yet back to the pre-pandemic “normal” pace of growth. Therefore, there is still strong demand for its products and services. This aligns well with what we were observing for months now. Fears of Covid-19 have resulted in a shift of spending from services to goods. As a result, demand for goods has overshot pre-pandemic levels, while demand for services is below its pre-pandemic trend and is enjoying a rebound (Chart 8). Chart 8There Is Still Pent-up Demand For Services

There Is Still Pent-up Demand For Services

There Is Still Pent-up Demand For Services

In the scorecard, we assign a higher score to the sectors like Industrials and Consumer Discretionary expecting a more significant pickup in sales growth, and a lower score to the sectors with sales growth that exceeds the historical average on the concern that mean reversion may be in store: A strong bounce back in sales has already materialized, and demand has been pulled forward. Factor 3: Pricing Power Pricing Power is a proprietary BCA indicator based on the PPI and CPI indices for the 60 different industries. Industries are rolled up into sector indices and the market index.1 Sectors with higher pricing power can pass on their costs to their customers. However, at some point, they may no longer be able to raise prices as that will dampen demand for their products. As a result, after a series of price increases, companies’ pricing power wanes. Today, pricing power of companies in most sectors is already two-to-three standard deviations above the five-year average, suggesting that the probability of further gains is extremely low, i.e., one percent or less (Chart 9). The only exceptions are the Healthcare and Financial sectors whose pricing power has barely budged.

Chart 9

What sectors do we prefer? Ones with a very high pricing power that is about to roll over or the ones whose pricing power is handicapped by outside political pressures and competitive headwinds? Since we believe that markets are driven by the second derivative, waning pricing power may have a detrimental effect on sector performance, while low and stable pricing power is already priced into expectations. To reflect this thinking, we penalize sectors whose pricing power is high relative to five years of history, expecting mean reversion. Factor 4: Degree Of Operating Leverage The degree of operating leverage (DOL), which gauges the company’s ability to spread its costs over sales, is largely determined by the cost of each marginal unit sold. This is a metric that assesses the cost structure of the sector in terms of fixed costs vs. variable costs. Sectors with higher fixed costs have higher operating leverage: It costs next to nothing to produce a marginal unit of sales, which leads to higher profitability as volume grows. We calculate DOL as the following: DOL= % Change in Operating Income/ % Change in Sales Percentage of change in operating income and sales is a five-year change to smooth out volatility and assess the longer-term relationship. Further, to obtain a comprehensive picture of the longer-term DOL, we calculate a median reading for each sector from 2010 to 2021. Median ignores extreme values and is better at capturing the “normal”. We also exclude negative and zero readings from our calculations to gauge DOL only when the companies are profitable (Chart 10).

Chart 10

Bringing It All Together: Operating Margins Sector Scorecard We have ranked all 11 sectors along the four dimensions described above. As a result, we expect Financials, Healthcare, Energy, and Utilities to be in the best position to preserve operating margins (Table 1). Table 1Sector Margins Scorecard

Sector Margins Scorecard

Sector Margins Scorecard

Energy Sector - Upgrade To An Overweight Energy profit margins are linked to underlying commodity prices. BCA Commodity and Energy strategists’ view is that the medium-term supply/demand backdrop is highly supportive of the current energy pricing dynamics and that the oil price is expected to stay high, at around its current level, for the next two years. They also note that upside price risk is increasing going forward, due to inadequate capex. Current operating margins remain well below the previous cyclical peak (Chart 11) and are expected to increase by 7.74 percentage points over the next 12 months. Although the price of oil has risen above the breakeven levels, energy companies are reluctant to invest in capex due to pressure from shareholder activists and newly found financial discipline. As a result, prices are likely to remain high until “high prices cure high prices”. In the meantime, energy producers are returning cash to shareholders – a unique bonus in the current world starved for yield. Chart 11The Street Expects the Energy Sector Margins To Expand. We concur...

The Street Expects the Energy Sector Margins To Expand. We concur...

The Street Expects the Energy Sector Margins To Expand. We concur...

Oil demand is expected to stay robust on the back of the global economic recovery, especially with an increase in consumption by airlines that are resuming international travel. Case in point: ExxonMobil (XOM) “anticipates demand improvement in its downstream segment with a continued economic recovery.” Upgrade Energy from an Equal Weight to an Overweight Financials – Overweight: O/W Banks, EW Insurance 2021 was a blockbuster year for banks on the back of the booming M&A and IPO activity. However, to achieve sustainable profitability, they need to jumpstart the loan growth process. There are early signs that lending is likely to pick up next year (Chart 12). According to JPM: "The customers who typically contribute to credit card loan growth are starting to spend the savings built up from the pandemic at a faster clip, suggesting they could be getting closer to taking on debt again" Regional banks already see the green shoots. According to Key Bank:"We are pleased with the trajectory of our loan growth." Chart 12Early Signs Of Lending Picking Up

Early Signs Of Lending Picking Up

Early Signs Of Lending Picking Up

Insurance companies are faring worse than Banks. Higher costs of labor and materials result in higher replacement costs, and higher customer payouts. However, insurers succeed in incorporating these higher expenses into pricing. While sell-side analysts anticipate margins will decline, (Chart 13) we believe that they may surprise on the upside: High operating leverage, improving pricing power (Chart 14) and growing demand for loans will contribute to strong profitability. Further, BCA expects the 10-year Treasury yield will rise to 2.0% - 2.25% by the end of 2022, supporting wider net interest margins. Chart 13While The Street Has Doubts About The Financial Sector Margins, We Are Constructive...

While The Street Has Doubts About The Financial Sector Margins, We Are Constructive...

While The Street Has Doubts About The Financial Sector Margins, We Are Constructive...

Chart 14Pricing Power Is Improving

Pricing Power Is Improving

Pricing Power Is Improving

Healthcare - Overweight: O/W Medical Equipment and Services, EW Pharma In July we published a report on the Healthcare sector, titled “Checking The Pulse: Deep Dive Into The Health Care Sector.” In this report, we upgraded the Healthcare sector to an overweight. Today, we reiterate the call. First, in a slowdown stage of the business cycle, Healthcare tends to outperform. Second, the Healthcare sector is one of the most resilient sectors profitability-wise as, being defensive by nature, its sales are unaffected by changes in economic demand. The street expects margins to expand by over 2% over the next 12 months (Chart 15). Further, there is still significant pent-up demand for health care services, and specifically for elective procedures – the most lucrative segment of the Healthcare market. Pricing power has recently picked up (Chart 16). Companies concur that life is getting better: According to JNJ:” many of the hospitals and other providers have to pay more for their input, and that's going to be reflected in the economics as we go forward. And of course, all that is reflected in how we price going forward”. Chart 15The Healthcare Margins Are Posed To Widen

The Healthcare Margins Are Posed To Widen

The Healthcare Margins Are Posed To Widen

Chart 16After A Prolonged Decline, Healthcare Pricing Power Is Finally On The Rise

After A Prolonged Decline, Healthcare Pricing Power Is Finally On The Rise

After A Prolonged Decline, Healthcare Pricing Power Is Finally On The Rise

Consumer Staples - Underweight Our sector margins scorecard has identified Consumer Staples as a sector most susceptible to a margin squeeze. Sell-side expects margins to contract by 2% (Chart 17). This is a sector that has low operating leverage which indicates that the marginal cost of producing each additional unit is high, and is particularly vulnerable to rising input costs. At the same time pricing power of the sector is likely to wane: companies were able to raise prices throughout 2021, and now pricing power is over four standard deviations above the five-year average (Chart 18). Raising prices in the environment when fiscal stimulus is in the rearview mirror, against a backdrop of negative real wage growth, will be challenging. Walmart surely knows its customers: It decided to “absorb higher costs and keep prices low for customers all across the business.” Operating Margins of Consumer Staples are likely to contract in 2022. Chart 17Consumer Staples Margins Are Expected To Plunge

Consumer Staples Margins Are Expected To Plunge

Consumer Staples Margins Are Expected To Plunge

Chart 18Pricing Power Is Not Sustainable

Pricing Power Is Not Sustainable

Pricing Power Is Not Sustainable

Investment Implications Our analysis indicates that companies in most sectors have reached their peak margins in Q3-2021. Looking ahead, there will be distinct profitability tracks, with some sectors expanding margins while others will experience margin compression. Sectors that have higher operating leverage, pent-up demand left over from the pandemic slowdown, and whose pricing power may still increase will fare best. Our scorecard screened all the 11 sectors based on these conditions, and Financials, Energy, Healthcare, and Utilities have the best shot at maintaining and even expanding their margins. We have been overweight Financials and Healthcare in our portfolios for a while now, and the expectation of resilient profitability only reinforces our conviction. We are upgrading Energy from neutral to an overweight on the back of the expected margin expansion and high oil price target. We are still underweight Utilities which we consider as a bond proxy, unlikely to outperform in a rising rates environment. Bottom Line In this report, we introduce a framework to rank the S&P 500 sectors based on the expected resilience of their margins. Factors we consider are operating leverage, pricing power, pent-up demand, and sell-side margin expectations. As a result of the analysis, we believe that Financials, Energy, Healthcare, and Utilities are posed for strong profitability in 2022. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Appendix: Chart 19

CHART 19

CHART 19

Chart 20

CHART 20

CHART 20

Chart 21

CHART 21

CHART 21

Chart 22

CHART 22

CHART 22

Chart 23

CHART 23

CHART 23

Chart 24

CHART 24

CHART 24

Chart 25

CHART 25

CHART 25

Chart 26

CHART 26

CHART 26

Chart 27

CHART 27

CHART 27

Chart 28

CHART 28

CHART 28

Chart 29

CHART 29

CHART 29

Chart 30

CHART 30

CHART 30

Footnotes 1 Pricing power is calculated by finding the difference between how much the industry has been able to increase prices and the change in the cost of the raw materials due to inflation. For example, for airlines, pricing power would be measured as the difference in the airfare CPI and jet fuel inflation. The exact calculation is industry specific. Industries are rolled up into sector indices and the market index. Recommended Allocation

Dear Client, There will be no report next week as we will be working on our Quarterly Strategy Outlook, which will be published the following week. In the meantime, please keep an eye out for BCA Research’s Annual Outlook, featuring long-time BCA client Mr. X, who visits towards the end of each year to discuss the economic and financial market outlook for the year ahead. Best regards, Peter Berezin Chief Global Strategist Highlights Inflation in the US, and to a lesser extent, in other major economies, will follow a “two steps up, one step down” trajectory of higher highs and higher lows. While inflation will fall in the first half of next year as goods prices stabilize, an overheated labor market will cause inflation to re-accelerate into 2023. The Fed will be slow to respond to high inflation, implying that monetary policy will remain accommodative next year. This should help propel stocks to new highs. Chinese stimulus will offset much of the drag from a weaker domestic property market. The dollar is a high momentum currency, so we wouldn’t bet against the greenback in the near term. Nevertheless, with “long dollar” now a consensus trade, we would position for a weaker dollar over a 12-month horizon. A depreciating dollar next year should help non-US equities, especially beleaguered emerging market stocks. The dollar will strengthen anew in 2023, as the Fed is forced to turn more hawkish, and global equities begin to buckle. From Ice To Fire In past reports, we have contended that inflation in the US, and to a lesser extent, in other major economies, would follow a “two steps up, one step down” trajectory of higher highs and higher lows. We are currently near the top of those two steps. The pandemic ushered in a major re-allocation of spending from services to goods (Chart 1). US inflation should dip over the next 6-to-9 months as the demand for goods decelerates and supply-chain disruptions abate. Chart 1The Pandemic Caused A Major Shift In Spending From Services To Goods

The Pandemic Caused A Major Shift In Spending From Services To Goods

The Pandemic Caused A Major Shift In Spending From Services To Goods

CHart 2Those With Low Paid Jobs Are Enjoying Stronger Wage Gains

Those With Low Paid Jobs Are Enjoying Stronger Wage Gains

Those With Low Paid Jobs Are Enjoying Stronger Wage Gains

The respite from inflation will not last long, however. The labor market is heating up. So far, most of the wage growth has been at the bottom end of the income distribution (Chart 2). Wage growth will broaden over the course of 2022, setting the scene for a price-wage spiral in 2023. We doubt that either fiscal or monetary policy will tighten fast enough to prevent such a spiral from emerging. As a result, US inflation will surprise meaningfully on the upside. Our view has no shortage of detractors. In this week’s report, we address the main counterarguments in a Q&A format: Q: What makes you think that service spending will rebound fast enough to offset the drag from weaker goods consumption? Chart 3Inventory Restocking Could Be A Source Of Growth Next Year

Inventory Restocking Could Be A Source Of Growth Next Year

Inventory Restocking Could Be A Source Of Growth Next Year

A: There is still a lot of pent-up demand for goods. Try calling any auto dealership. You will hear the same thing: “We have nothing in stock now, but if you put in an order today, you might get a vehicle in 3-to-6 months.” Thus, durable goods sales are unlikely to weaken quickly. And with inventories near record low levels, firms will need to produce more than they sell (Chart 3). Inventory restocking will support GDP growth. As for services, real spending in the US grew by 7.9% in the third quarter, an impressive feat considering that this coincided with the Delta-variant wave. Service growth will stay strong in the fourth quarter. The ISM non-manufacturing index jumped to a record high of 66.7 in October, up from 61.9 in September. The Atlanta Fed’s GDPNow model is tracking real PCE growth of 9.2% in Q4. Goldman’s Current Activity Indicator has hooked up (Chart 4).

Chart 4

Q: Aren’t you worried that spending on services might stall next year? A: Not really. Chart 5 shows the percentage change in real spending for various types of services from January 2020 to September 2021, the last month of available data.

Chart 5

Chart 6

The greatest decline in spending occurred in those sectors that were most directly affected by the pandemic. Notably, spending on movie theaters, amusement parks, and live entertainment in September was still down 46% on a seasonally-adjusted basis compared to last January. Hotel spending was down 22%. Spending on public transport was down 26%. Only spending on restaurants was back to normal. The number of Covid cases has once again started to trend higher in the US, so that path to normalization will take time (Chart 6). Nevertheless, with vaccination rates still edging up and new antiviral drugs set to hit the market, it is reasonable to assume that many of the hardest-hit service categories will recover next year. Q: What about medical services? Some have speculated that the shift to telemedicine will require much lower spending down the road. A: It is true that spending on outpatient services in September was $43 billon below pre-pandemic levels. However, over two-fifths of that shortfall was in dental services, which are not amenable to telemedicine. Spending on dental services was down 16% from its January 2020 levels, compared to 6% for physician services. A more plausible theory is that many people are still worried about venturing to the doctor’s or dentist’s office. In addition, a lot of elective procedures were canceled or postponed due to the pandemic. Clearing that backlog will lift medical spending next year. Chart 7The Flow Of Savings Has Fallen Back To Pre-Pandemic Levels But The Stock Of Accumulated Savings Remains High

The Flow Of Savings Has Fallen Back To Pre-Pandemic Levels But The Stock Of Accumulated Savings Remains High

The Flow Of Savings Has Fallen Back To Pre-Pandemic Levels But The Stock Of Accumulated Savings Remains High

In any case, the cost of a telemedicine appointment is typically no different from an in-person one. And, to the extent that telemedicine does become more widespread, this could encourage more people to seek medical assistance. Lastly, even if spending on certain services does not fully recover after the pandemic, this will probably simply result in a permanent increase in spending on goods. The only way that overall consumer spending will falter is if the savings rate rises, which seems unlikely to us. Q: Why do you say that? The savings rate has been very high throughout the pandemic. A: The savings rate did spike during the pandemic, but that was mainly because fewer services were available, and because households were getting transfer payments from the government. Now that these payments have ended, the savings rate has dropped to 7.5%, roughly where it was prior to the pandemic. There is good reason to think the savings rate will keep falling next year. Households are sitting on $2.3 trillion in excess savings, most of which reside in bank deposits (Chart 7). As they run down those savings, consumption will rise in relation to income. The household deleveraging cycle is over. After initially plunging during the pandemic, credit card balances are rising (Chart 8). Banks are eager to make consumer loans (Chart 9). Household net worth has risen by over 100% of GDP since the start of the pandemic (Chart 10). As we discussed three weeks ago, the wealth effect alone could boost annual consumer spending by up to 4% of GDP. Chart 8APost-GFC Deleveraging Has Ended And People Are Swiping Credit Cards Again Following The Pandemic Scare

Post-GFC Deleveraging Has Ended And People Are Swiping Credit Cards Again Following The Pandemic Scare

Post-GFC Deleveraging Has Ended And People Are Swiping Credit Cards Again Following The Pandemic Scare

Chart 8BPost-GFC Deleveraging Has Ended And People Are Swiping Credit Cards Again Following The Pandemic Scare

Post-GFC Deleveraging Has Ended And People Are Swiping Credit Cards Again Following The Pandemic Scare

Post-GFC Deleveraging Has Ended And People Are Swiping Credit Cards Again Following The Pandemic Scare

Chart 9Banks Are Easing Credit Standards For Consumer Loans

Banks Are Easing Credit Standards For Consumer Loans

Banks Are Easing Credit Standards For Consumer Loans

Chart 10A Record Rise In Household Net Worth

A Record Rise In Household Net Worth

A Record Rise In Household Net Worth

Q: Household wealth could fall as the Fed starts tapering and eventually raising rates. Wouldn’t that cool the economy? A: The taper is a fait accompli, and markets are already pricing in rate hikes starting in the second half of next year. If the Fed were to signal its intention to raise rates more quickly than what has been priced in, then home prices and stocks could certainly weaken. We do not think the Fed will pivot in a more hawkish direction before the end of next year, however. The Fed’s estimate of the neutral rate is only 2.5%, a big step down from its estimate of 4.25% in 2012. The market’s view is broadly in line with the Fed’s (Chart 11). Despite the upward move in realized inflation, long-term inflation expectations remain in check – expected inflation 5-to-10 years out in the University of Michigan survey has increased from 2.3% in late 2019 to 2.9%, bringing it back to where it was between 2010 and 2015. The 5-year/ 5-year forward TIPS breakeven inflation rate is near the bottom end of the Fed’s comfort zone (Chart 12). Chart 11The Fed And Investors Still Believe In Secular Stagnation

The Fed And Investors Still Believe In Secular Stagnation

The Fed And Investors Still Believe In Secular Stagnation

Chart 12Long-Term Inflation Expectations Are Not Yet A Concern For The Fed

Long-Term Inflation Expectations Are Not Yet A Concern For The Fed

Long-Term Inflation Expectations Are Not Yet A Concern For The Fed

Q: What about fiscal policy? Isn’t it set to tighten sharply next year? A: The US budget deficit will decline next year. However, this will happen against the backdrop of strong private demand growth. Moreover, budget deficits are likely to remain elevated in the post-pandemic period. This week, President Biden signed a $1.2 trillion infrastructure bill into law, containing $550 billion in new spending. BCA’s geopolitical strategists expect Congress to pass a $1.5-to-$2 trillion social spending bill using the reconciliation process. All in all, the IMF foresees the US cyclically-adjusted primary budget deficit averaging 4.9% of GDP between 2022 and 2026, compared to 2.0% of GDP between 2014 and 2019 (Chart 13).

Chart 13

Chart 14While Overall Consumption Has Recovered, Business Spending and Direct Government Expenditures Remain Below Trend

While Overall Consumption Has Recovered, Business Spending and Direct Government Expenditures Remain Below Trend

While Overall Consumption Has Recovered, Business Spending and Direct Government Expenditures Remain Below Trend

It should also be noted that government spending on goods and services has been quite weak over the past two years (Chart 14). The budget deficit surged because transfer payments exploded. Unlike direct government spending, which is set to accelerate over the next few years, households saved a large share of transfer payments. Thus, the fiscal multiplier will increase next year, even as the budget deficit shrinks. Q: We have focused a lot on demand, but what about supply? There are over 4 million fewer Americans employed today than before the pandemic and yet the job openings rate is near a record high. Chart 15Despite A Notable Decline, There Are Still A Lot Of People Avoiding Work Because Of Worries About Contracting Or Transmitting Covid

Despite A Notable Decline, There Are Still A Lot Of People Avoiding Work Because Of Worries About Contracting Or Transmitting Covid

Despite A Notable Decline, There Are Still A Lot Of People Avoiding Work Because Of Worries About Contracting Or Transmitting Covid

A: Some people who left the workforce will regain employment. According to the Census Bureau’s Household Pulse Survey, there are still 2.5 million people not working because they are afraid of catching or transmitting the virus (Chart 15). That said, some workers may remain sidelined for a while longer. The very same survey also revealed that about 8 million of the 100 million workers currently subject to vaccine mandates say that “they will definitely not get the vaccine.” In addition, about 3.6 million workers have retired since the start of the pandemic, about 1.2 million more than one would have expected based on pre-existing demographic trends. Most of these retirees will not work again. Lifestyle choices may keep others from seeking employment. Female labor participation has declined much more during the pandemic and than it did during the Great Recession (Chart 16). While many mothers will re-enter the labor force now that schools have reopened, some may simply choose to stay at home.

Chart 16

The bottom line is that the pandemic has reduced labor supply at a time when labor demand remains very strong. This is likely to exacerbate the labor shortage. Q: Any chance that higher productivity will offset some of the damage to the supply side of the economy from decreased labor participation? A: US labor productivity did increase sharply during the initial stages of the pandemic. However, that appears to have been largely driven by composition effects in which low-skilled, poorly-paid service workers lost their jobs. As these low-skilled workers have returned to the labor force, productivity growth has dropped. The absolute level of productivity declined by 5.0% at an annualized rate in the third quarter, leading to an 8.3% increase in labor costs. It is telling that productivity growth has been extremely weak outside the US (Chart 17). This gives weight to the view that the pandemic-induced changes in business practices have not contributed to higher productivity, at least so far. It is also noteworthy that a recent study of 10,000 skilled professionals at a major IT company revealed that work-from-home policies decreased productivity by 8%-to-19%, mainly because people ended up working longer. Increased investment spending should eventually boost productivity. Core capital goods orders, which lead corporate capex, are up 18% since the start of the pandemic (Chart 18). However, the near-term impact of increased investment spending will be to boost aggregate demand, stoking inflation in the process.

Chart 17

Chart 18US Capex Should Pick Up

US Capex Should Pick Up

US Capex Should Pick Up

Q: We have spoken a lot about the US, but the world’s second biggest economy, China, is facing a massive deflationary shock from the implosion of its real estate market. Could that deflationary impulse potentially cancel out the inflationary impulse from an overheated US economy? A: You are quite correct that inflation has risen the most in the US. While inflation has picked up in Europe, this mainly reflects base effects (Chart 19). Inflation in China has fallen since the start of the pandemic despite booming exports. There are striking demographic parallels between China today and Japan in the early 1990s. The bursting of Japan’s property bubble corresponded with a peak in the country’s working-age population (Chart 20). China’s working-age population has also peaked and is set to decline by more than 40% over the remainder of the century. Chart 19The US Stands Out As The Inflation Leader

The US Stands Out As The Inflation Leader

The US Stands Out As The Inflation Leader

Chart 20Demographic Parallels Between China And Japan

Demographic Parallels Between China And Japan

Demographic Parallels Between China And Japan

That said, there are important differences between the two nations. In 1990, Japan was a rich economy; output-per-hour was nearly 70% of US levels. China is still a middle-income economy; output-per-hour is only 20% of US levels (Chart 21). China has the ability to outgrow some of its problems in a way that Japan did not. In addition, Chinese policymakers have learned from some of Japan’s mistakes. They have been trying to curb the economy’s dependence on property development; real estate development investment has fallen from 12% of GDP in 2014 to less than 10% of GDP (Chart 22). China is still building too many new homes, but unlike Japan in the 1990s, the government is likely to pursue stimulus measures to compensate for a shrinking property sector. This should keep the economy from entering a deflationary slump.

Chart 21

Chart 22Real Estate Investment Has Peaked In China

Real Estate Investment Has Peaked In China

Real Estate Investment Has Peaked In China

Q: Let’s bring this back to markets. What is the main investment takeaway from your view? A: The main takeaway is that investors should remain bullish on stocks and other risk assets for the next 12 months but be prepared to turn more cautious in 2023. The neutral rate of interest in the US is higher than generally assumed. This means that monetary policy is currently more accommodative than widely believed, which is good for stocks. Unfortunately, it also means that a policy error is likely: The Fed will keep rates too low for too long, causing the economy to overheat. Chart 23Bank Stocks Tend To Outperform When Yields Rise

Bank Stocks Tend To Outperform When Yields Rise

Bank Stocks Tend To Outperform When Yields Rise

This overheating will not be evident over the next six months. As we noted at the outset of this report, the US economy is currently at the top of the proverbial two steps in our projected “two steps up, one step down” trajectory for inflation. The cresting in durable goods inflation will provide a temporary respite from inflationary worries, even as the underlying long-term driver of higher inflation – an increasingly tight labor market – gains traction. Strong consumer demand and persistent labor shortages will incentivize companies to invest in new capacity and automate production. This will benefit industrial stocks and select tech names. Rising bond yields will also boost bank shares (Chart 23). A country’s current account balance is simply the difference between what it saves and what it invests. With savings on the downswing and investment on the upswing, the US will find it increasingly difficult to finance its burgeoning trade deficit. The US dollar is a high momentum currency, so we wouldn’t necessarily bet against the greenback in the near term (Chart 24). Nevertheless, with “long dollar” now a consensus trade, we would position for a weaker dollar over a 12-month horizon (Chart 25).

Chart 24

Chart 25Long Dollar Is A Crowded Trade

Long Dollar Is A Crowded Trade

Long Dollar Is A Crowded Trade

Chart 26A Depreciating Dollar Next Year Should Help Non-US Equities

A Depreciating Dollar Next Year Should Help Non-US Equities

A Depreciating Dollar Next Year Should Help Non-US Equities

A depreciating dollar next year should help non-US equities, especially beleaguered emerging markets (Chart 26). The dollar will strengthen anew in 2023, as the Fed is forced to turn more hawkish, and global equities begin to buckle. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

Image

Special Trade Recommendations

Image

Current MacroQuant Model Scores

Image

Over the past few weeks, we have received numerous questions on the interplay between the S&P 500 earnings and the forward P/E multiple. The clients are asking how much earnings need to grow for the S&P 500 forward multiple to come down from the hefty 21.5x towards a historical average of 18x. To answer this question, we have created a matrix that summarizes permutations of changes in the index price and earnings growth and their effects on the resulting forward multiple. If we assume that the price of the S&P 500 does not budge, and investors get a 0% return over the next 12 months, earnings will have to grow by about 30% over the next 12 months for the multiple to come down to 18x – hardly a realistic scenario. If the S&P 500 returns 5%, then 30% earnings growth will result in the 19.6x multiple. The sell-side analysts currently expect a 10% earnings growth over the next twelve months: With no change in the price of the index, the resulting multiple will be 21.5x. If the S&P 500 returns 5%, the multiple will move to 23.2x. Bottom Line: Strong earnings growth does not justify elevated valuations, and re-rating is hardly in the cards.

Image

October new home prices fell for the second consecutive month in China (see The Numbers). Given how highly leveraged the Chinese property sector is, a continued decline in home prices would be an unwelcome development for Chinese policymakers. It raises the…

Highlights Why have Value stocks underperformed so much during the past decade? The rise in intangible assets is likely the most important reason since traditional valuation metrics are no longer an accurate measure of intrinsic value. Value stocks today have a larger negative tilt to Quality than they did in the past. This has hurt Value due to Quality's outperformance. Value's underperformance is not just the result of the relative performance of a few sectors or industries, although this has played a role. Falling interest rates have not been the main driver of Value’s underperformance as they can only account for a small portion of returns. “Migration”, or mean-reversion in and out of value buckets, has declined since the Great Financial Crisis, possibly because of an increase in monopoly power. But even this cannot fully account for the underperformance since 2012. We propose that investors who wish to invest in Value screen for Quality. They should also express their Value tilts in sectors with few intangibles, such as Energy or Materials. More sophisticated stock pickers can adjust earnings and book values for intangibles. Asset allocators who invest only in indices should stay away from a structural allocation to Value. Feature Chart 1No Premium From Value Stocks Over The Last Four Decades

No Premium From Value Stocks Over The Last Four Decades

No Premium From Value Stocks Over The Last Four Decades

Betting on cheap stocks has been a cornerstone of equity investing for decades. The rationale is simple: Stocks which are undervalued, according to some measure of intrinsic value, will eventually converge up to their fair value, on average, while stocks that are overvalued will converge down, on average. Historically, this bet on mean-reversion has proven successful – low price-to-book stocks have outperformed high price-to-book stocks by more than 3% per annum since 1927. However, the recent decades have put Value investing to the test. The Value factor, as defined by Fama and French, has not provided a structural premium in the US large cap space since the late 1970s (Chart 1, panel 1). Commercial Value indices haven’t been any more successful: Value aggregates by MSCI, Russell, and S&P have either underperformed or performed in line with the market benchmark over the same time frame (Chart 1, panel 2). The current situation presents a difficult dilemma. On the one hand, buying Value could be a tremendous opportunity. By several measures, Value stocks are the most undervalued they have been since the end of the tech bubble, right before they went on a historic run (Chart 2). Academic work has argued that these deep value spreads tend to be positively correlated with long-term outperformance of Value stocks.1 In a world of sky-high valuations and with equities and bonds projected to deliver very low returns over the next decade, a cheap return stream would be a fantastic addition to most portfolios. Chart 2Value Stocks Are Really Cheap

Value Stocks Are Really Cheap

Value Stocks Are Really Cheap

Chart 3

And yet, Value has become so popular, that many investors are now worried that the Value premium may no longer exist. This worry is not without merit. Several studies have shown that factors lose a sizable portion of their premium once they appear in academic literature2 (Chart 3). Other issues, such as the inability of valuation metrics to properly account for intrinsic value in the modern economy, have also led some investors to seriously question whether buying Value indices will deliver excess returns in the future. So what is the right answer? Why has Value underperformed so much? Is the beaten down Value factor a generational buying opportunity? Or will it continue its decline going forward? In this report we try to answer these questions. Using a company-level dataset from our BCA Research Equity Analyzer (EA), as well as drawing on the latest academic research, we assess the evidence behind Five Theories On Value’s Underperformance. Once we determine which explanations have merit and which do not, we conclude by providing some guidelines on how investors should consider the Value factor going forward in our Investment Implications section. A word of caution: We have constructed our sample of companies to roughly resemble the sample used by MSCI World. Thus, the conclusions from our analysis based on the EA dataset should be relevant to Value indices in general. However, be advised that the methodology that EA uses is different from other commercial Value indices. Specifically, the EA methodology is more aggressive in its positioning and uses a wider array of metrics. For clarity, Table 1 shows the metrics used by EA compared to other Value indices. If you wish to know more on how the methodology works, please refer to the Appendix. Table 1Value Factor Methodologies

Mythbusting The Value Factor

Mythbusting The Value Factor

Also, please note that our report will not deal with the cyclical outlook for Value. While it is entirely possible that a period of cyclical growth could help Value stocks outperform, the question we are trying to answer is whether buying cheap versus expensive stocks still provides a structural premium over the long term. While the Global Asset Allocation service does not use the Value versus Growth framework for equity allocation, our colleagues from our Global Investment Strategy service have written extensively on why they believe investors should pivot to Value on a cyclical basis.3 Five Theories On Value’s Underperformance Chart 4More To The Underperformance Of Value Than Sector Tilts

More To The Underperformance Of Value Than Sector Tilts

More To The Underperformance Of Value Than Sector Tilts

Theory #1: The underperformance of Value indices is purely a result of their sector composition Some investors suggest that Value stocks’ large underweight of mega-cap tech, as well as their overweight in Financials and Energy, have been responsible for Value’s woes over the past decade. However, our research suggests that this theory is not entirely correct. A Value index with the same sector and industry weightings as the Developed Markets (DM) benchmark has still underperformed by more than 15% since 2010 (Chart 4, panel 1). Sector and industry composition have been responsible for about a third of the underperformance of the DM Value index. What about excluding the FAANGM stocks? Again, the story is similar. Even when omitting these stocks from our investment universe, Value stocks have still underperformed by almost the same amount as a regular Value composite (Chart 4, panel 2). Finally, we can also look at the performance of cheap versus expensive stocks within each industry. Chart 5A shows that cheap stocks have underperformed expensive stocks in 18 and 17 out the 24 GICS Level 2 industries in DM and in the US, respectively, since 2012 (roughly corresponding to the peak in relative performance in the EA Value index). Even on an equally-weighted basis, which eliminates the effects of large companies, cheap stocks have underperformed expensive stocks in both the average and median industry (Chart 5B).

Chart 5

Chart 5

Verdict: Myth. The underperformance of cheap versus expensive stocks has been broad. While sector and industry dynamics have certainly been an important factor, Value's underperformance is not just the result of a few companies, sectors, or industries. Chart 6Value Likes Rising Yields...

Value Likes Rising Yields...

Value Likes Rising Yields...

Theory #2: The decline in interest rates is to blame for the underperformance of Value Another reason used to explain the underperformance of Value is the secular decline in interest rates. The reasoning goes as follows: Cash flows from growth stocks are set to be received further into the future, while cash flows from Value stocks are closer to the present. Using a Discounted Cash Flow model, one can show that all else being equal, a decline in the discount rate should result in a relatively higher increase in the present value for Growth stocks versus Value stocks. There is some evidence in support of this theory. While prior to 2010, Value and interest rates had an inconsistent relationship, the beta of cheap stocks to the monthly change in the 10-year US Treasury yield has increased markedly over the past 10 years (Chart 6, panel 1). On the other hand, the beta of expensive stocks to yields has become increasingly more negative. A similar situation occurs when we use the yield curve. Cheap stocks tend to exhibit higher excess returns whenever it steepens, while expensive stocks do so when it flattens (Chart 6, panel 2). Importantly, these relationships are not purely a result of Value’s exposure to banks. Value stocks excluding financials also show a strong positive relationship to both the 10-year yield and yield curve slope versus their growth counterparts (Chart 7). But while this relationship is statistically significant, it fails to be economically significant. Our analysis shows that the betas to either interest rates or the slope of the yield curve only explain a small fraction of the performance of cheap or expensive stocks (Chart 8). This result is in line with the research from Maloney and Moskowitz, which showed that the vast majority of the decline in Value in recent years could not be explained by interest rates.4 Chart 7...Even When Excluding Financials...

...Even When Excluding Financials...

...Even When Excluding Financials...

Chart 8...But Yields Don't Explain Much

...But Yields Don't Explain Much

...But Yields Don't Explain Much

Verdict: Myth. Cheap stocks have an increasingly positive beta to both the 10-year yield and the slope of the yield curve, whereas expensive stocks have an increasingly negative beta. However, while these betas are statistically significant, they can only account for a small portion of Value's underperformance. Theory #3: A decline in market mean-reversion is responsible for the underperformance of Value In a seminal paper, Fama and French describe the process of migration.5 Migration is when stocks move across different value buckets: For example, when stocks in the cheap bucket migrate to the neutral and expensive buckets, and when stocks in the expensive bucket migrate to the neutral or cheap buckets. Historically, this process of mean-reversion has provided a significant share of the Value premium. However, migration has declined significantly over the past decade (Chart 9, panel 1). The amount of market cap migrating each month as a percentage of total market cap has declined from over 12% before the GFC to less than 8% currently. Importantly, this decline in migration has been broad-based. Neither cheap, neutral, nor expensive stocks are moving to other valuation cohorts at the same rates that prevailed in the past (Chart 9, panel 2). The market has become much more ossified: Value stocks remain Value stocks, Neutral stocks remain Neutral stocks, and Growth stocks remain Growth stocks.5 Chart 9What Happens In Value Now Stays In Value

What Happens In Value Now Stays In Value

What Happens In Value Now Stays In Value

Chart 10Market Concentration Could Be The Reason Why Migration Has Declined

Market Concentration Could Be The Reason Why Migration Has Declined

Market Concentration Could Be The Reason Why Migration Has Declined

Why has migration declined? One theory is that industries have increasingly become more monopolistic, which means that it has become harder for new entrants to gain market share (Chart 10). Meanwhile market leaders are able to grow at an above-average pace thanks to their large network effects.6 What has been the role of this decreased migration in the performance of Value? A paper written by Arnott, Harvey, Kalesnik, and Linainmaa showed that while the returns attributable to migration have decreased over the past 15 years, this change is still not strong enough to explain the deep underperformance in Value.7 Our own research assigns it a relatively larger weight, with migration accounting for a little less than half of the underperformance of Value since 20128 (Table 2). Table 2Return Attribution Of Cheap And Expensive Stocks

Mythbusting The Value Factor

Mythbusting The Value Factor

Verdict: Somewhat True. Migration has declined since the GFC, possibly because of an increase in monopoly power. While this decline has certainly played a role in the underperformance of Value, it explains, at most, less than half of the drawdown since 2012. Theory #4: Value has underperformed because it is increasingly a play on junk stocks

Chart 11

It is a well-known empirical fact that cheap stocks tend to have lower Quality than expensive stocks. Conceptually this makes sense: Companies with higher profitability, more stability, and less leverage should trade at a valuation premium, whereas low income, high-debt companies should trade at a discount. However, this gap in Quality between cheap and expensive stocks is not always the same. Consider the composition of cheap and expensive stocks in 2000 – the eve of the tech bubble crash. About a third of expensive stocks were also junk (low quality), whereas 36% were quality stocks (Chart 11). Today, this composition is much different: Only about a fifth of the market capitalization of expensive stocks is junk, whereas quality stocks now make up 44% of the overall expensive cohort. On the other hand, the Quality of cheap stocks has deteriorated: Cheap junk stocks are now 37% of the cheap cohort versus 29% in 2000. Importantly, the difference in Quality between cheap and expensive stocks tends to be a good predictor for value returns (Chart 12). A big gap in the Quality factor often implies lower returns of cheap versus expensive stocks, whereas a small gap implies higher returns. These results are in line with similar research which has shown that Quality, or Quality proxies like profitability, can be used to enhance the Value factor.9 Chart 12Value Does Well When The Quality Gap Is Small

Value Does Well When The Quality Gap Is Small

Value Does Well When The Quality Gap Is Small

Why is this the case? As we have discussed in the past, Quality has been one of the best performing factors over the past 30 years - likely driven by powerful behavioral biases as well as by the incentives in the money management industry.10 As a result, taking an overly negative position on this factor over a long enough period eventually eats away at the Value premium. Verdict: True. Value stocks today have a larger negative tilt to Quality than they did in the past. This negative tilt has hurt Value as excess returns of cheap stocks tend to be dependent on their Quality gap to expensive stocks. Theory #5: Value has underperformed because traditional valuation metrics are no longer a reliable indicator of intrinsic value How exactly to measure whether a company is cheap or expensive has been a matter of debate since the very beginnings of Value investing. Benjamin Graham famously cautioned against using book value as a measure of intrinsic value, preferring a more holistic approach. Today most index providers use a combination of traditional valuation metrics like price-to-book and price-to-earnings to build Value indices. It is fair to ask if these measures are still relevant for today’s companies. Intangible investment has become a much larger part of the economy, having surpassed tangible investment in the US in the late 1990s (Chart 13). However, both US GAAP and IFRS are very restrictive on the capitalization of R&D activities, which are known to originate valuable intangible assets.11 Other types of intangible capital such as unique production processes or customer lists are normally also expensed within SG&A expenses and are never capitalized unless there is an acquisition. This means that both the book value and earnings of intangible-heavy companies could be inadequate estimates of their true intrinsic value.

Chart 13

Is there any evidence that this is the case? Using our EA dataset, we confirm that expensive companies generally have higher R&D expenditures as a percent of sales than cheap companies (Chart 14). Importantly, we see that the performance of Value within low R&D stocks is much better than the performance within high R&D stocks (Chart 15). This is line with the work of Dugar and Pozharny, who found that the value relevance for both earnings and book values has declined for high intangible companies, while it has stayed stable for low-intangible companies.12 This suggests that traditional valuation measures are losing their relevance as intangible-heavy companies become a larger part of the economy.13 Chart 14Growth Stocks Spend More On Intangibles

Growth Stocks Spend More On Intangibles

Growth Stocks Spend More On Intangibles

Chart 15Are Traditional Metrics Underestimating Intrinsic Value In High-Intangible Companies?

Are Traditional Metrics Underestimating Intrinsic Value In High-Intangible Companies?

Are Traditional Metrics Underestimating Intrinsic Value In High-Intangible Companies?