Sectors

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

Banks have had an amazing run, and while such strong performance is unlikely to repeat, there is still oomph left in the trade thanks to a more favorable regulatory environment, stronger demand for loans, a steeper yield curve, and a strong pipeline of capital market activity. Key risks are further tightening of monetary policy and an increase in bad loans. We reiterate our overweight on Capital Markets, Diversified Banks, and Regional Banks.

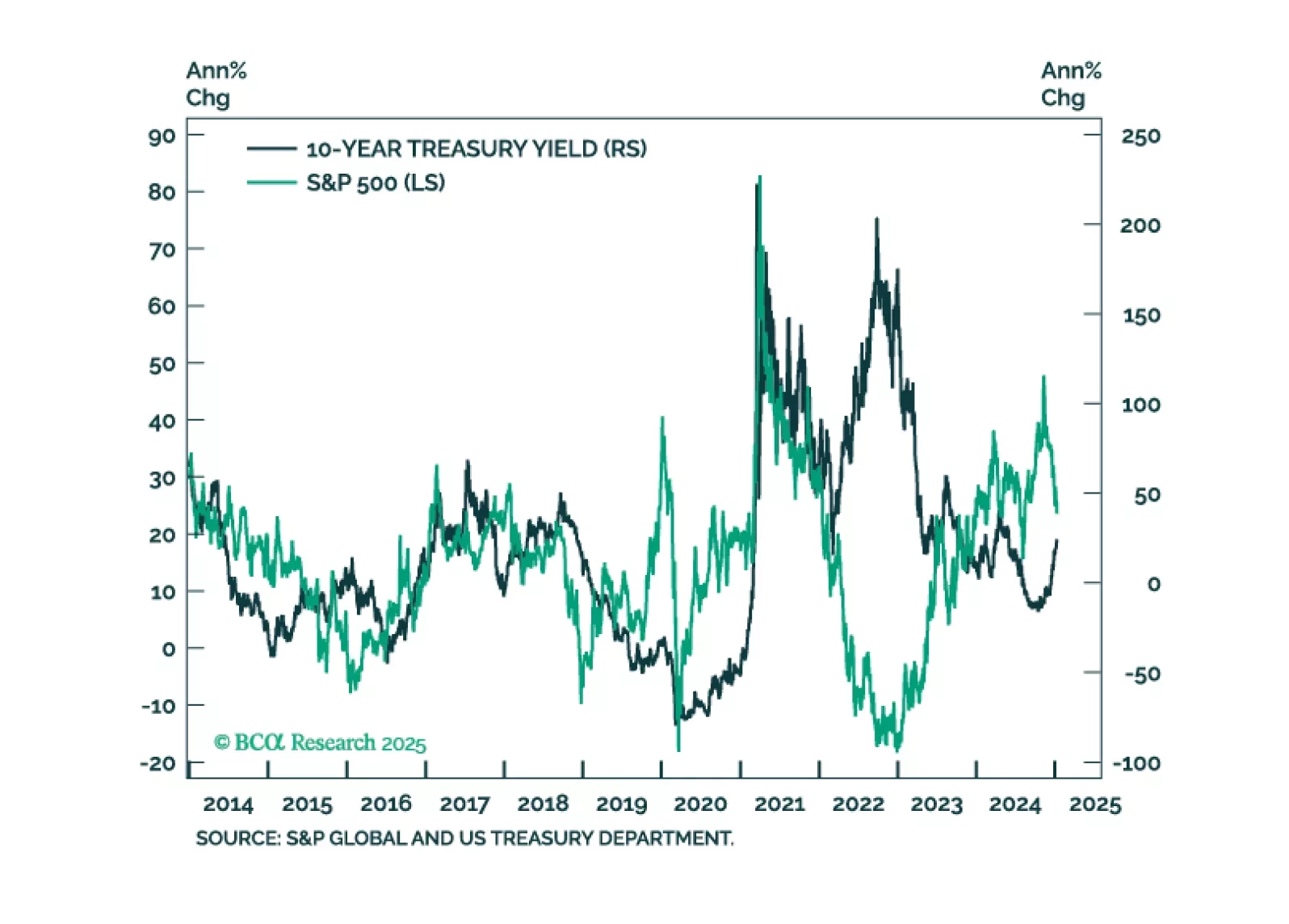

In this first presentation of 2025, we start with an overview of the 2025 outlook webcast polls, and a brief post-mortem of the 2024 market performance. Then, we shift gears and examine what is behind the recent surge in bond yields and its implications for equities. We also review market technicals and positioning and conclude with a list of trades to prepare our portfolio for continued moves in yields.

To kick start our new research agenda at Equity Analyzer, we welcome you to our weekly screener report. Each week we will deliver three screeners highlighting stocks exposed to various macro and investment views and themes, that have either been suggested by various BCA strategies, such as the Global Investment Strategy, or are based on research by the Equity Analyzer team. In our first installment, we take a look at US Tech stocks, equity sentiment, and quality "bubble" stocks.

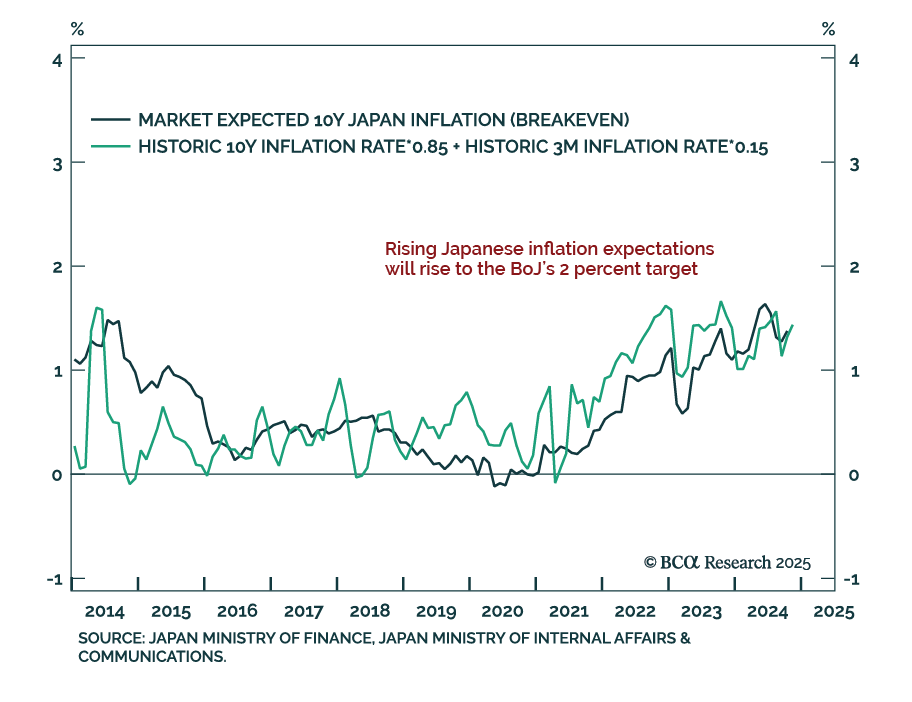

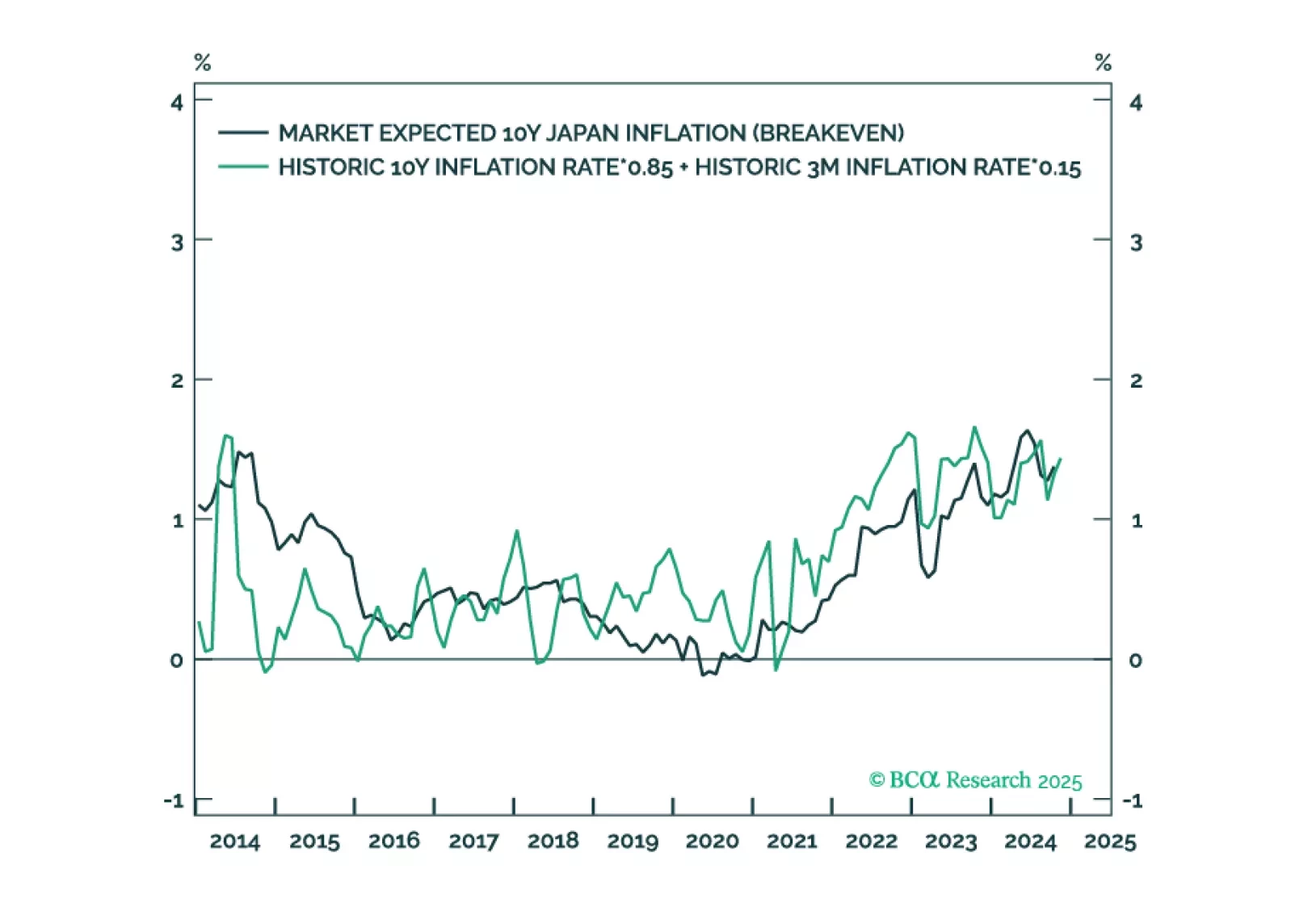

In most developed economies, rising inflation expectations will lift them further above the 2 percent target, limiting the scope for further interest rate cuts. But in Japan, rising inflation expectations will lift them up to the BoJ’s 2 percent target, removing the BoJ’s justification for its zero-interest rate policy. The normalisation of Japan’s monetary policy poses a big structural risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations. From a timing perspective though, wait until the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have collapsed. Plus: go tactically long copper.

Paradoxically, raging optimism on the US economy is making a reacceleration in growth less likely in 2025. The reaction of the bond market has made the Fed rethink its cutting campaign. Markets are also constraining Trump’s agenda. US manufacturing will not recover with a surging dollar. Fears of inflation and debt sustainability have made moderate House Republicans push back against the President Elect’s wishes. Given the sky-high optimism embedded in asset prices, we believe a defensive portfolio stance is warranted on a 12-month horizon. Overweight gold to hedge the risk of a fiscal crisis.