Sentiment

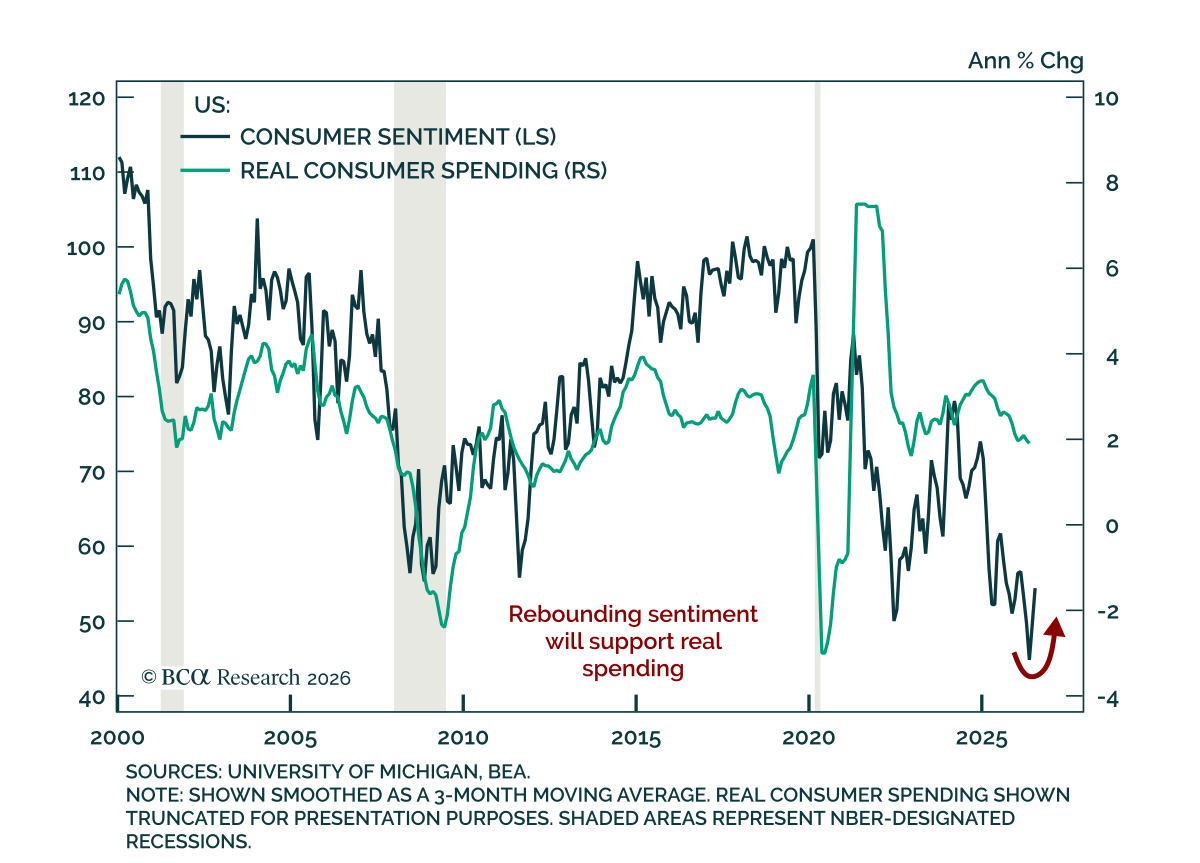

The preliminary July University of Michigan survey pointed to improving sentiment and anchored inflation expectations. The survey beat estimates, with the headline index rising to 54.4 from 49.5, driven by both consumers’ assessment of current conditions and…

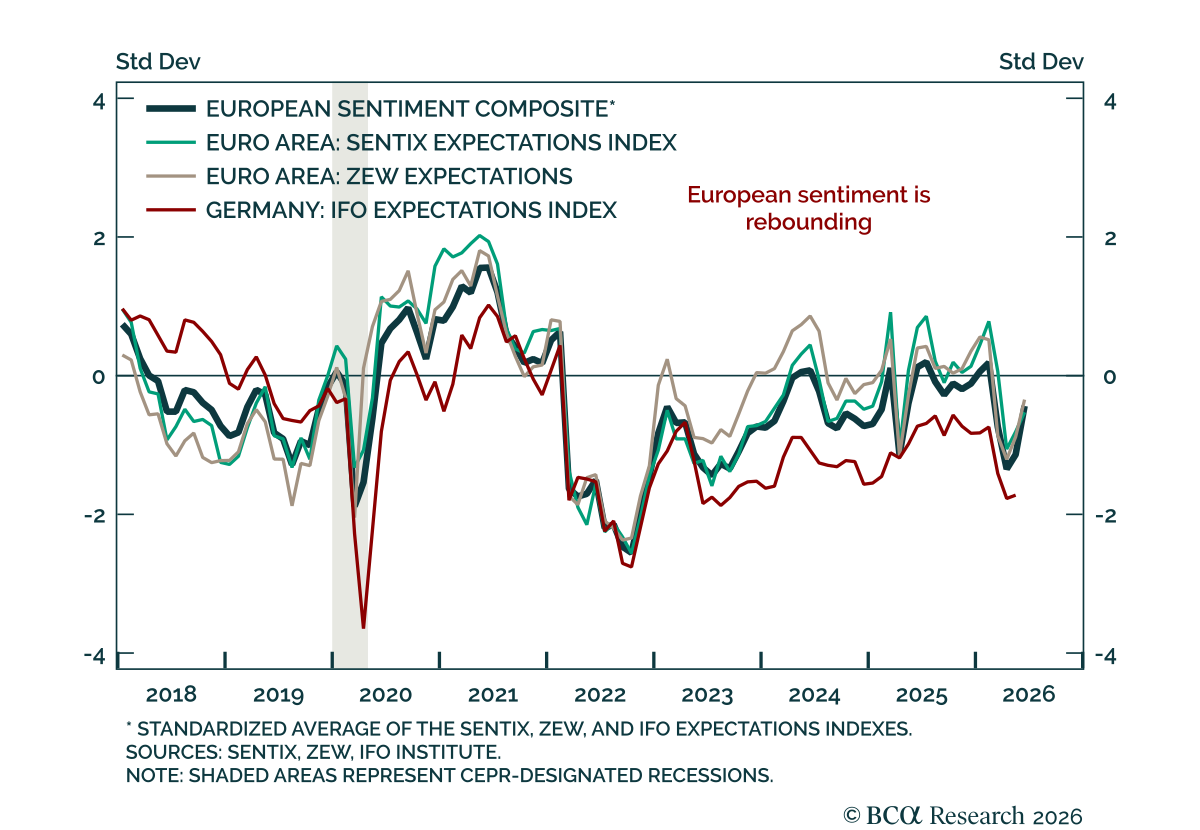

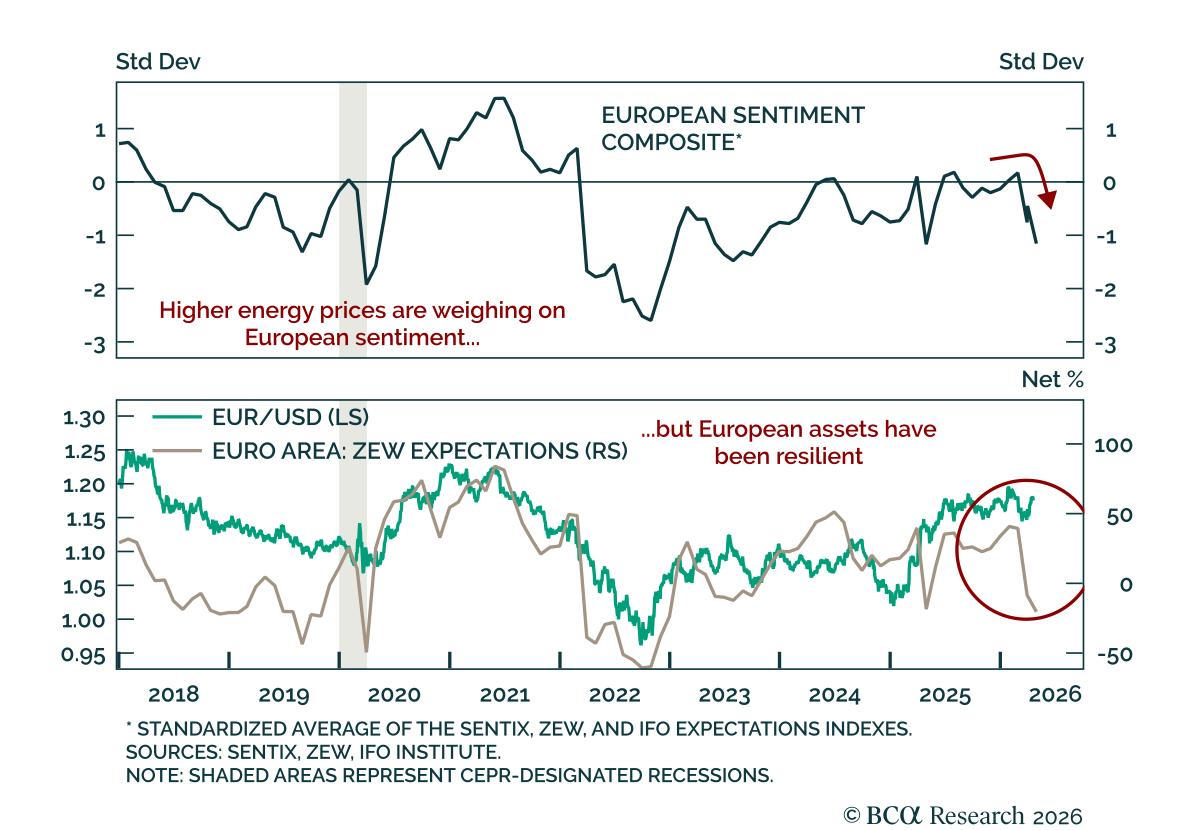

The June ZEW was mixed, with Germany’s expectations beating estimates while current-conditions measures worsened further. The survey period included Monday, June 15, when the US-Iran deal was announced. That split between European expectations and…

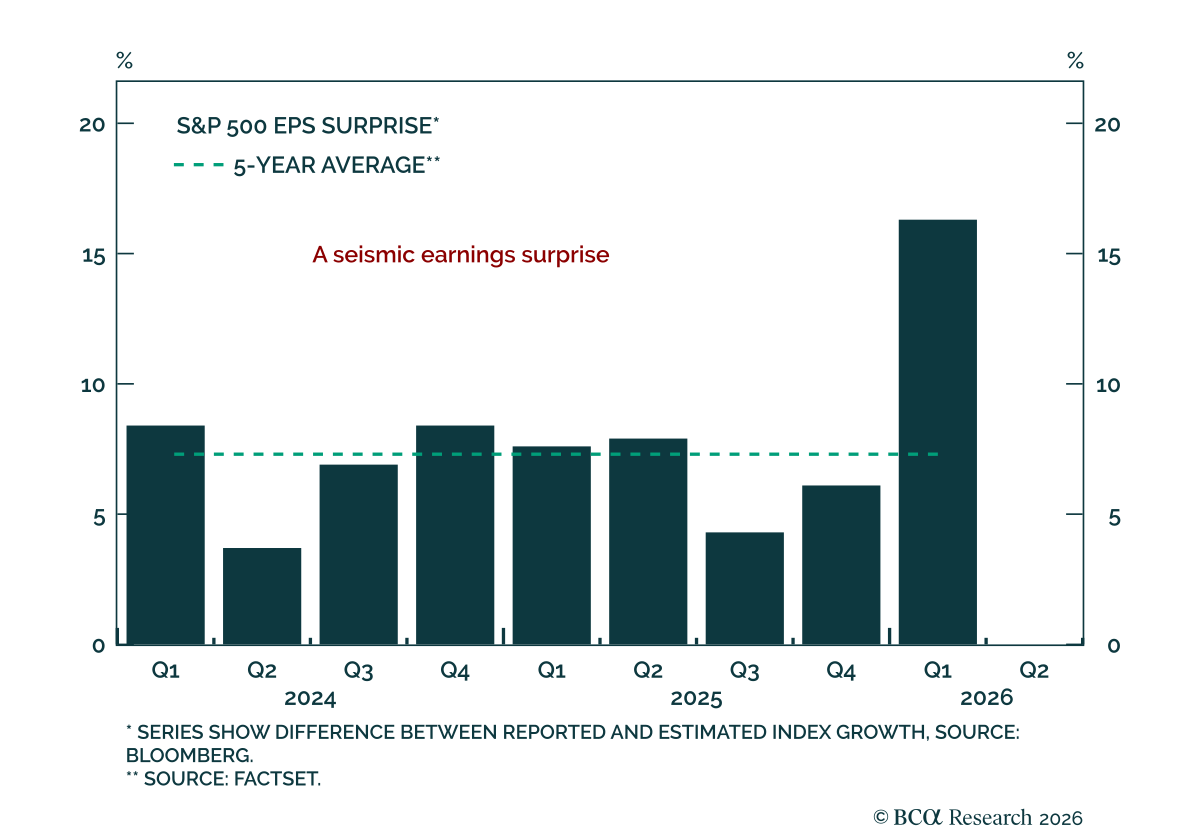

Our US Investment strategists remain constructive on the US economy as there is no evidence of overheating or looming stagflation. The S&P 500 has risen for eight straight weeks, supported by strong earnings. With 94% of constituents reporting, this…

Against the earnings-versus-everything-else market backdrop, stellar earnings are easily outweighing elevated oil prices, rising yields and the increased probability that the Fed may hike rates before the year is out. US allocators should remain invested in equities.

The April ZEW showed continued deterioration in European sentiment, with no sign yet of a rebound. Germany’s expectations component missed estimates and fell to -17.2 from -0.5, while the eurozone measure fell to -20.4 from -8.5. Current conditions in Germany…

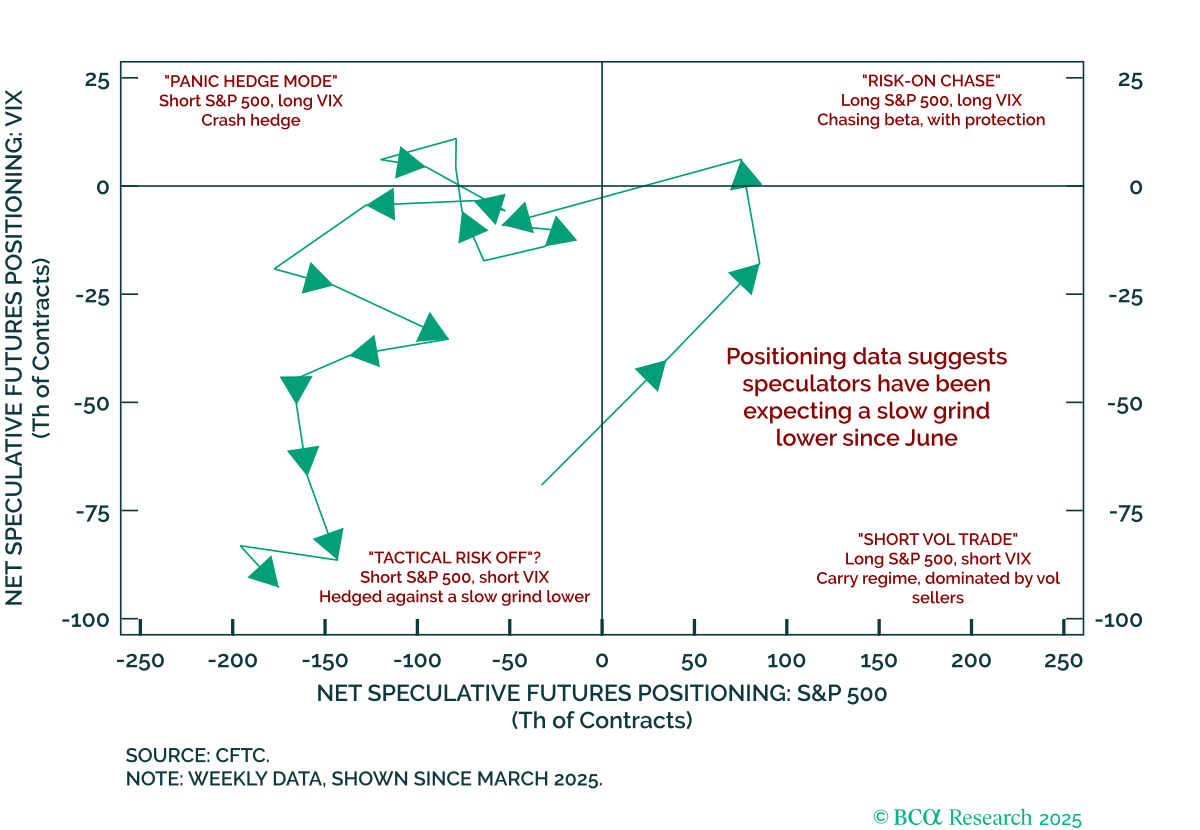

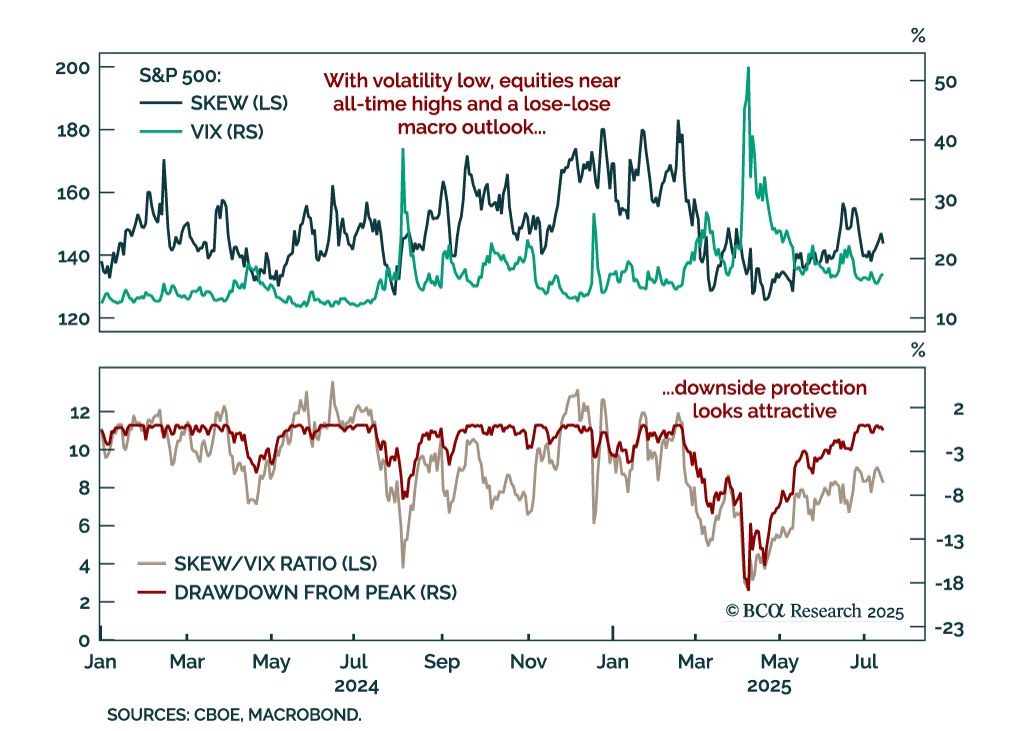

Volatility has fallen to 2025 lows even as positioning data show caution despite the S&P 500’s steady rebound. US equities have climbed back to all-time highs with minimal drawdown, steadily compressing realized volatility and pulling implied…

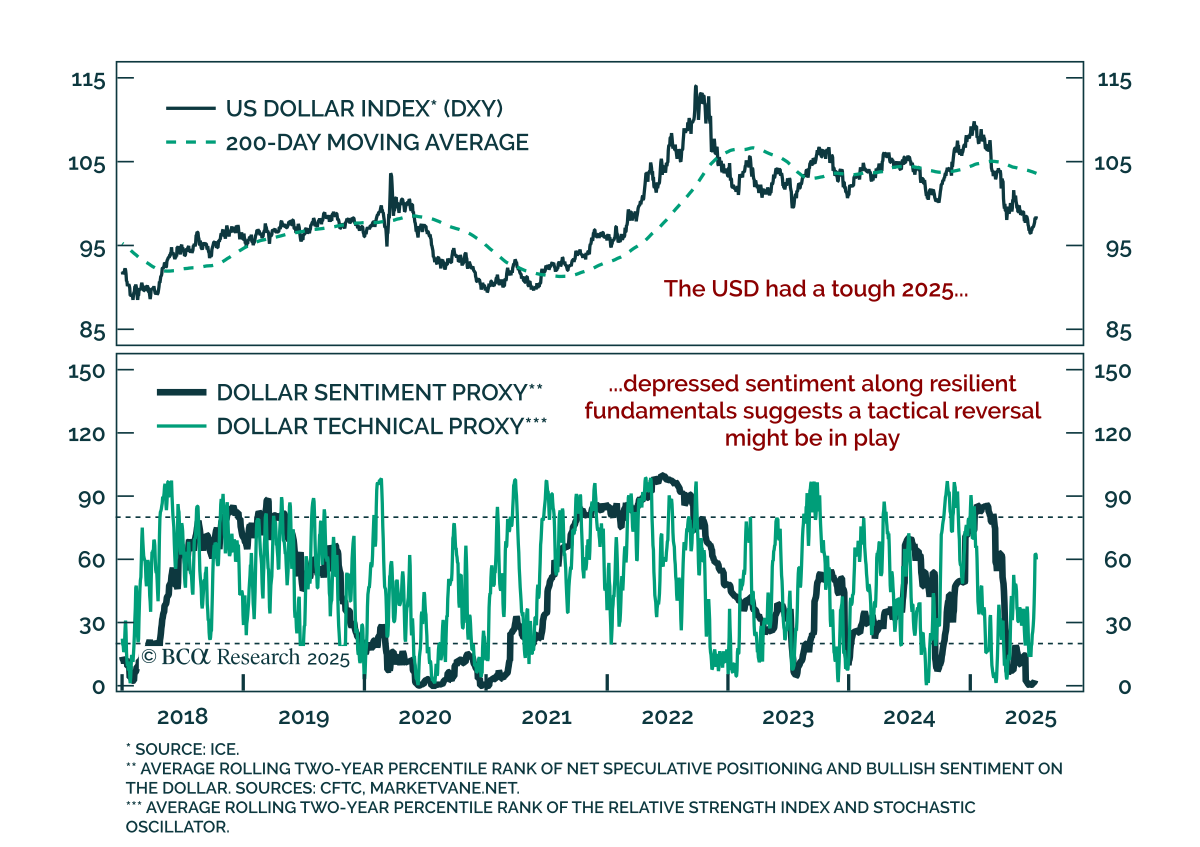

The USD remains structurally challenged, but near-term tactical conditions suggest a temporary bottom is in place. After a sustained selloff and rising concerns around its reserve status, the dollar has decoupled from rate differentials, a behavior more…

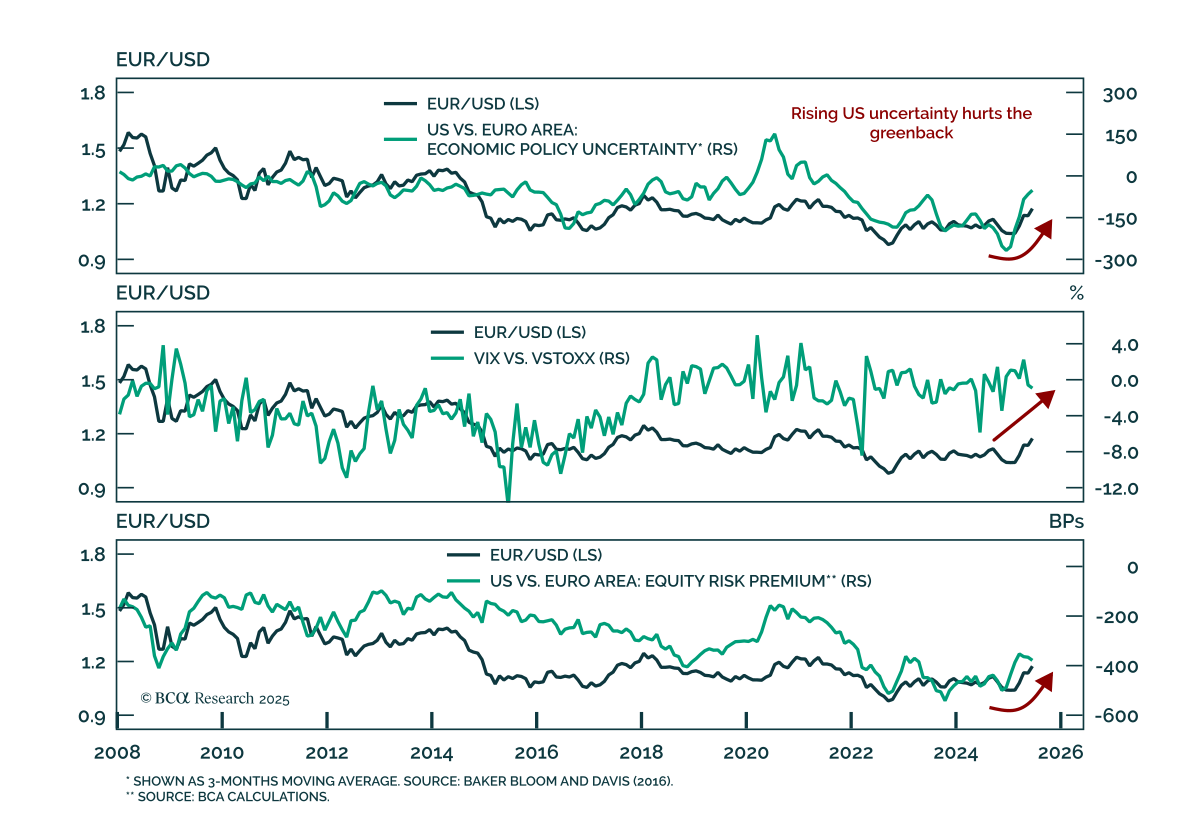

Rising US macro uncertainty and external imbalances are reinforcing euro strength and are supportive of a long-term bullish view on EUR/USD. Our Chart Of The Week comes from Mathieu Savary, Chief Strategist for Developed Markets ex US.Trump’s policy agenda is…

The S&P 500 sits near all-time highs, but sentiment and positioning suggest euphoria has not driven this rally. Prices are elevated, yet the SKEW/VIX ratio sits at 8.3, or its 67th percentile. While not at extreme levels associated with reversals, it…

Hard aggregate macro data series remain solid, but surveys of businesses and consumers continue to worsen and the list of consumer-facing companies lowering earnings estimates gets longer by the week. We believe surging equities are ignoring the adverse effects of tariffs and reiterate our defensive asset allocation recommendations.