Services

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

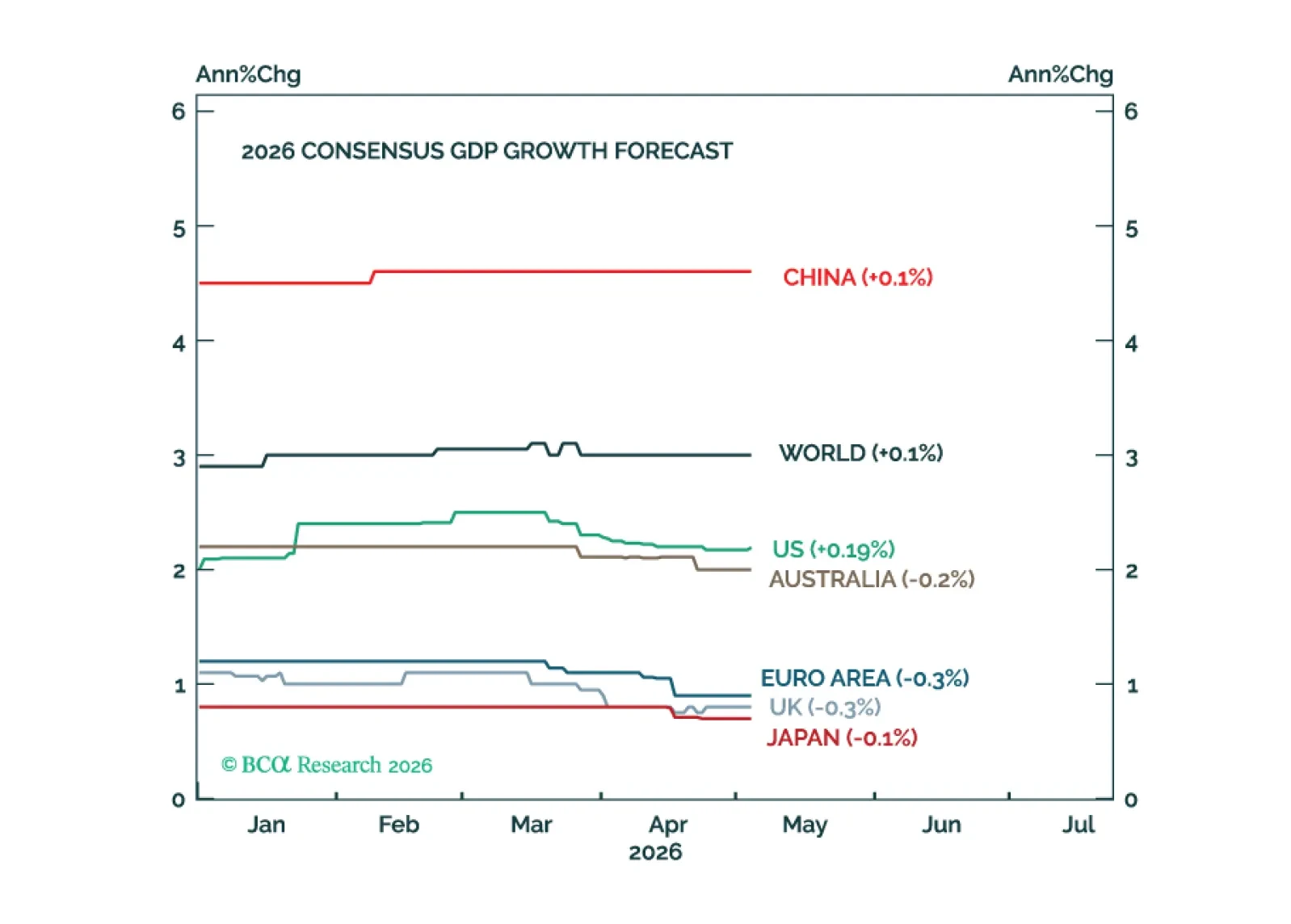

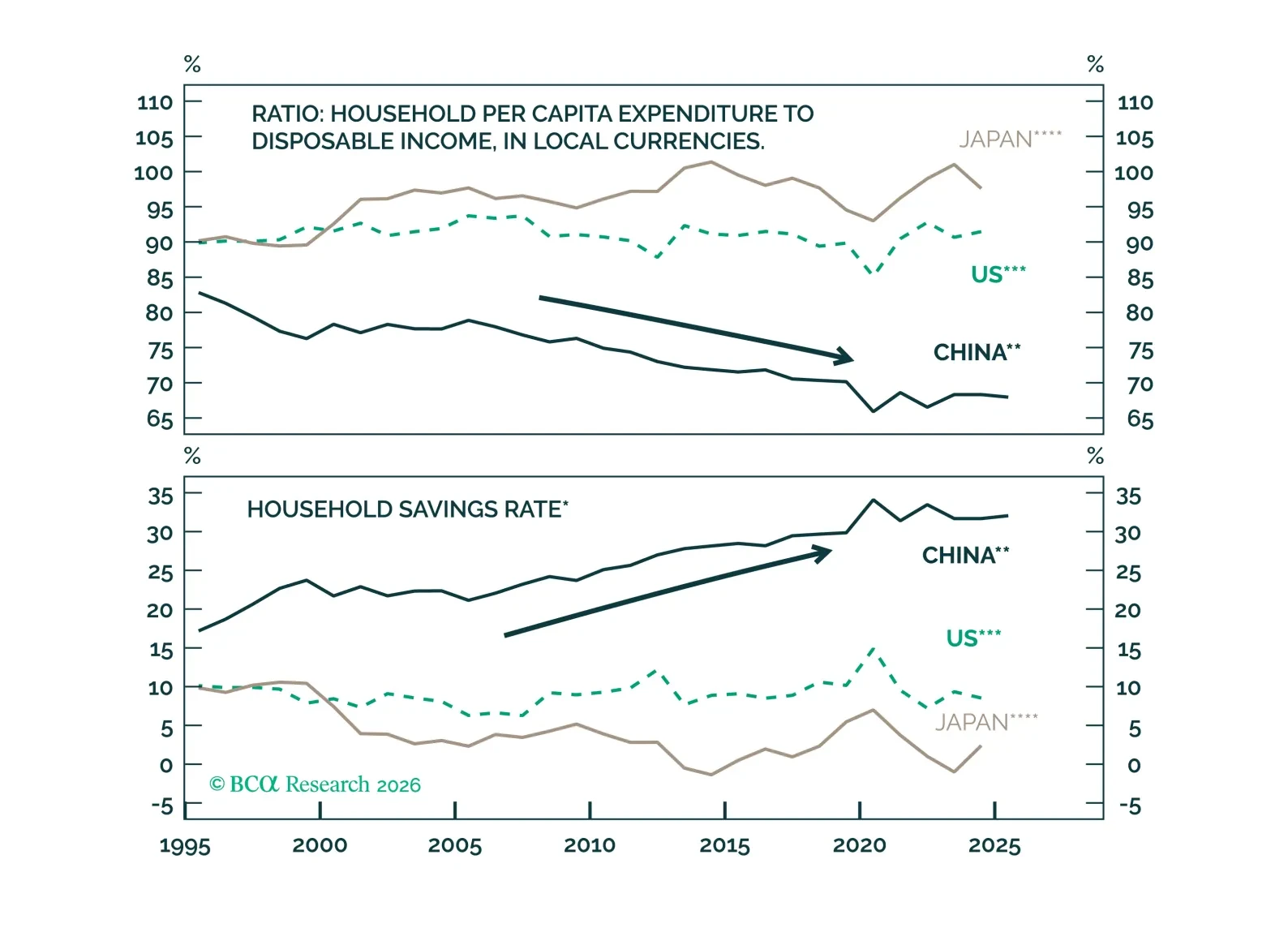

This report analyzes the structural and cyclical factors driving service spending in Chinese households and highlights sectors with promising investment opportunities for the next 6 to 12 months.

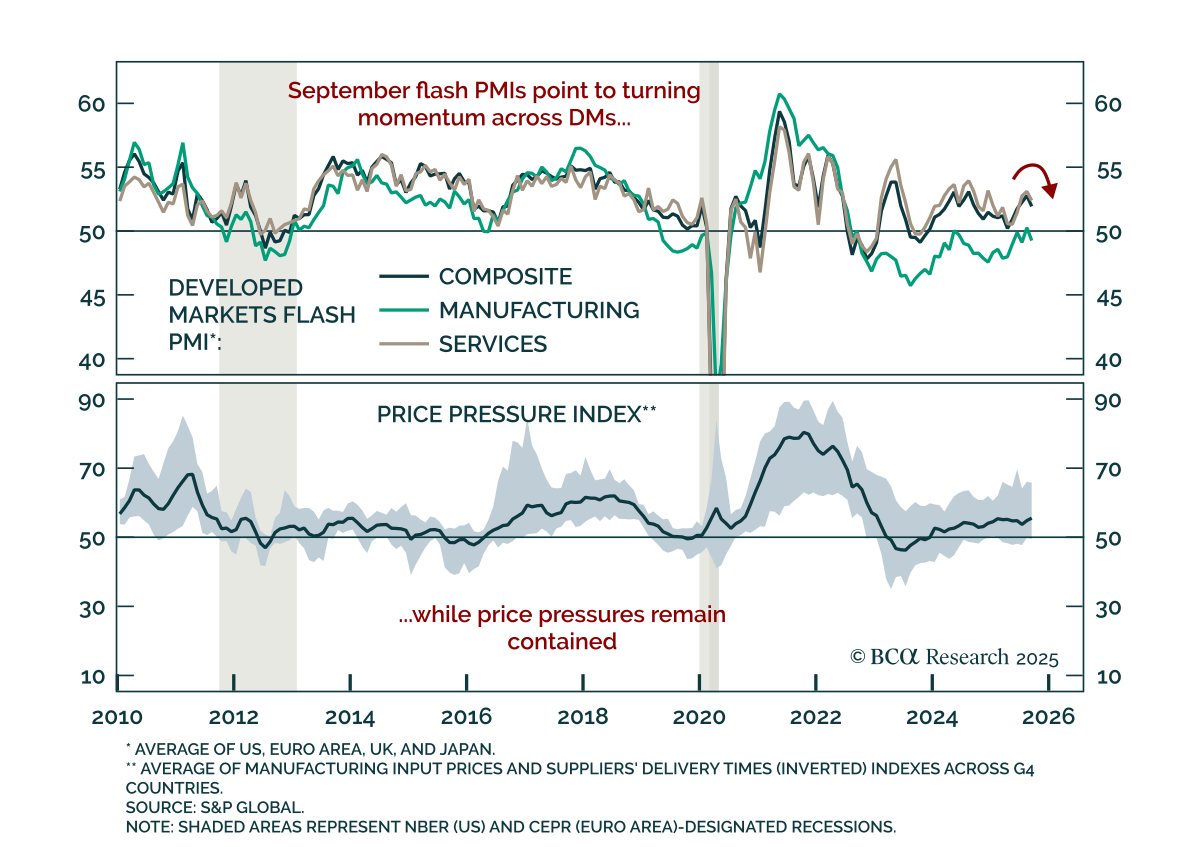

September flash PMIs show slowing global momentum, reinforcing US equity outperformance and underweights in industrial metals. The US composite slipped to 53.6 from 54.6, led by weaker manufacturing. Europe was mixed: Services strengthened modestly but…

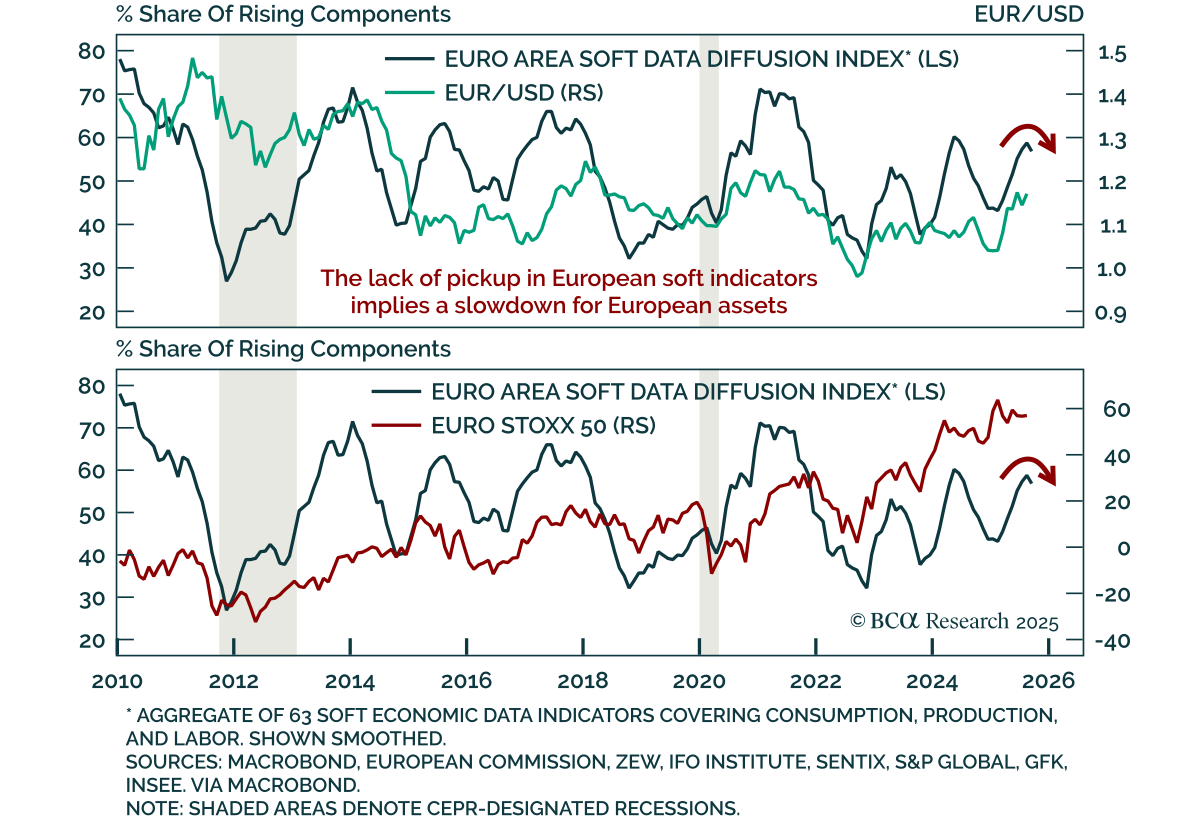

European sentiment indicators weakened again in August and September, reinforcing tactical US outperformance. While the September flash consumer confidence print beat expectations, it is still sluggish. Surveys such as Sentix and ZEW, both leading indicators…

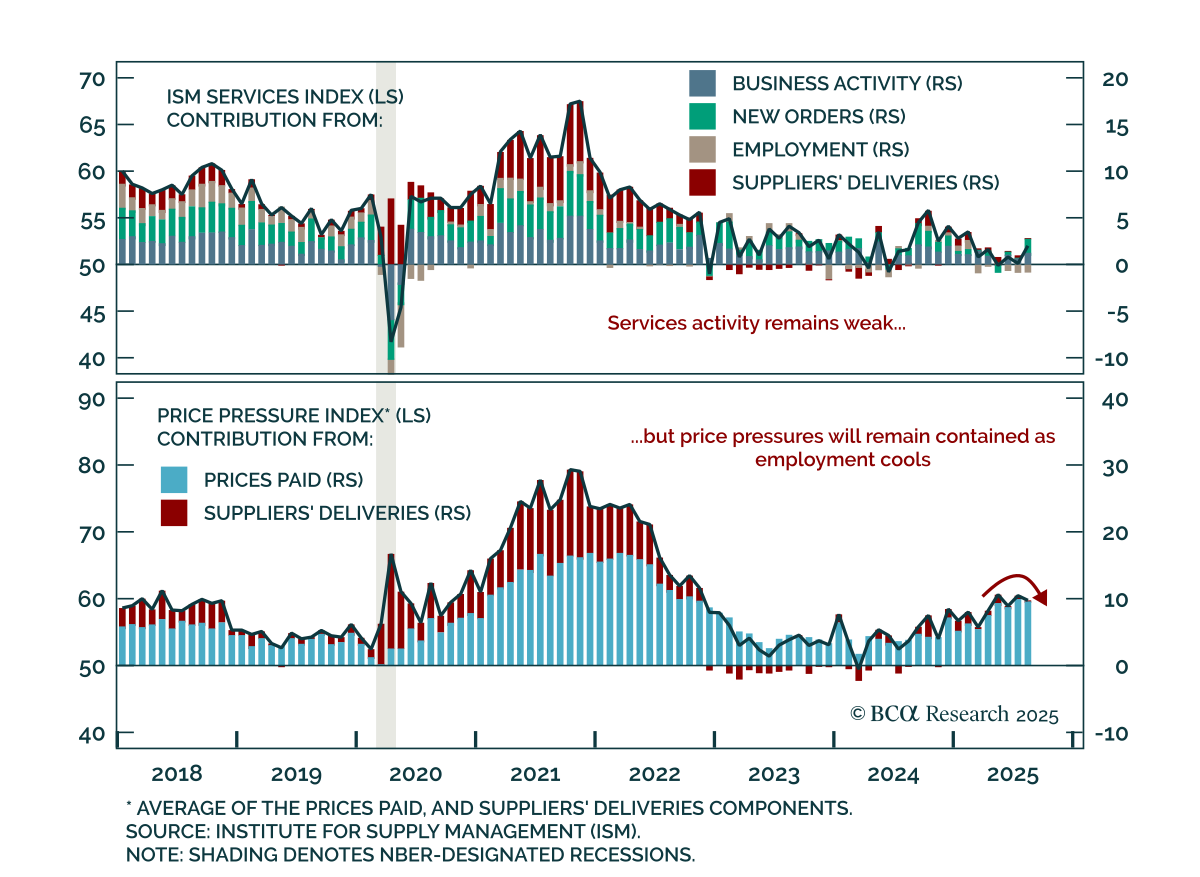

August ISM Services beat expectations, but employment weakness highlights fragile momentum. The index rose to 52.0 from 50.1, driven by business activity and new orders. However, the employment component stayed in contraction at 46.5. Inflation signals…

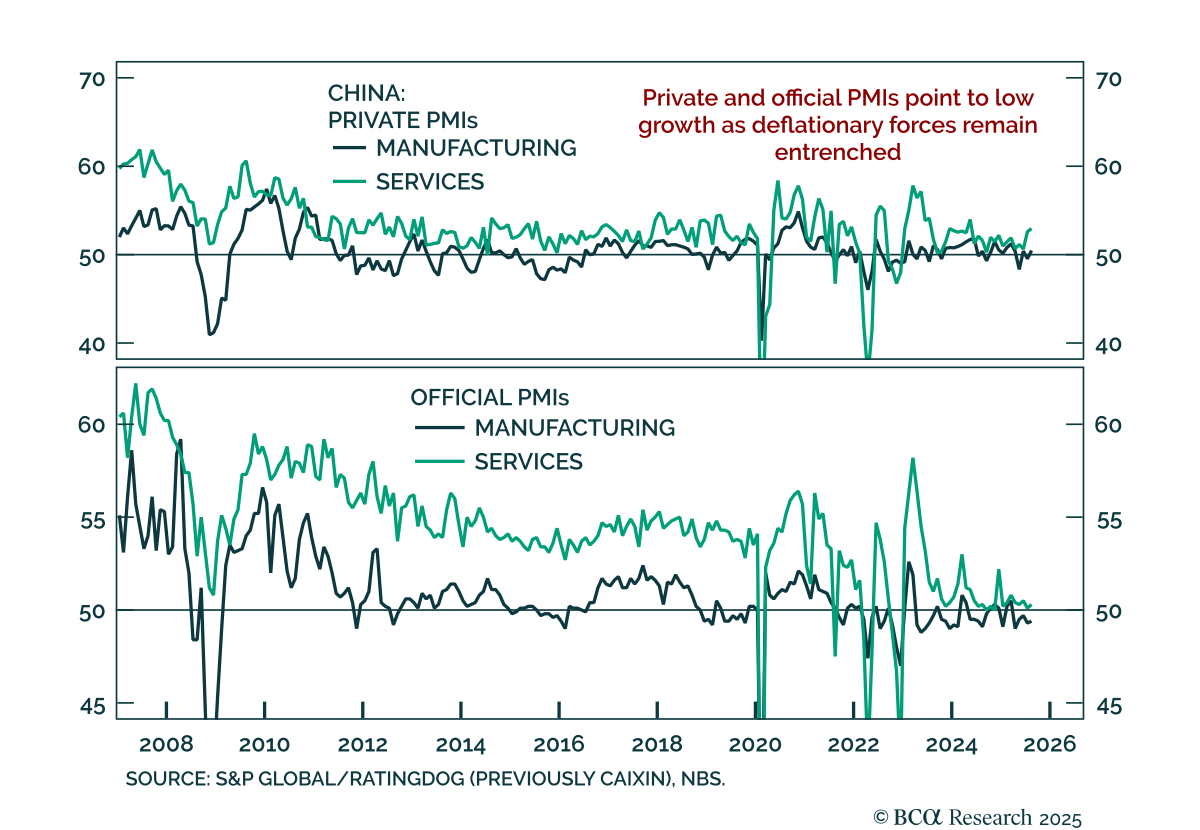

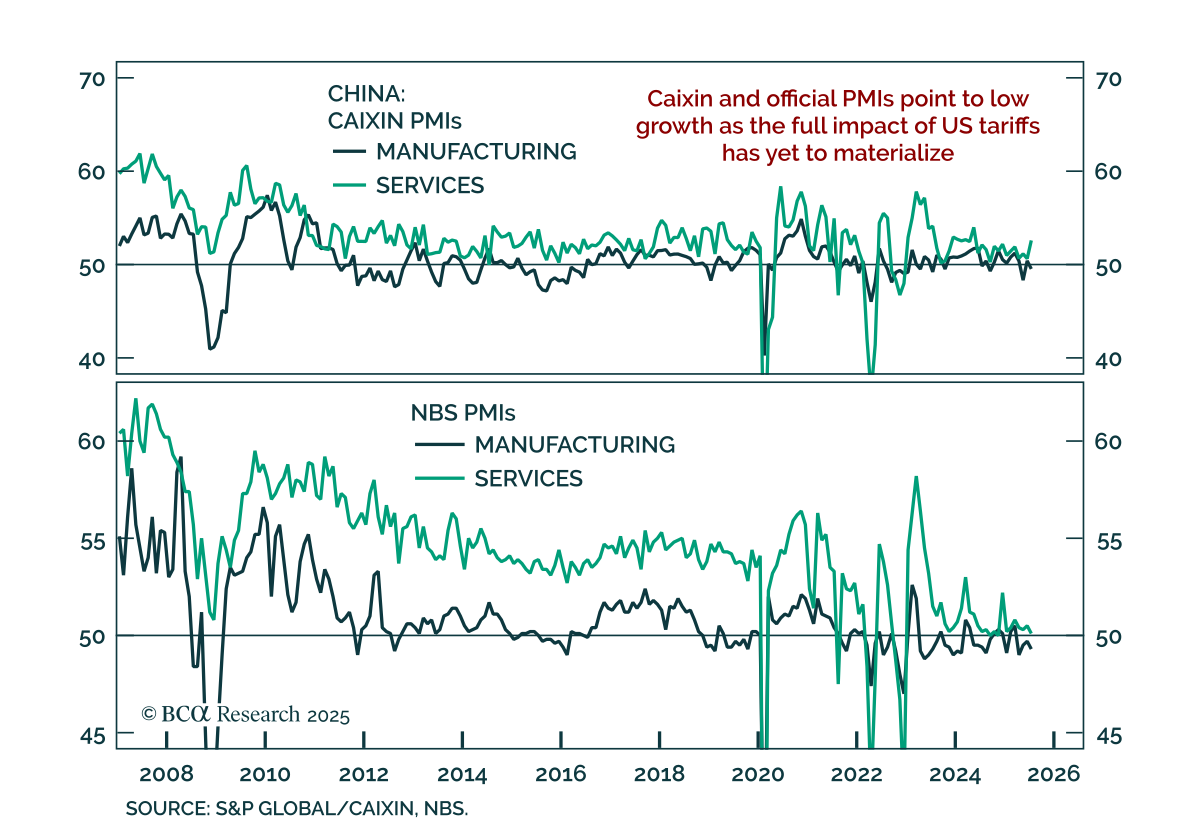

China’s August PMIs improved, but underlying data point to persistent weakness and limited momentum. The official NBS composite rose to 50.5 from 50.2, with manufacturing still in contraction at 49.4 and services edging higher to 50.3. Private PMIs showed…

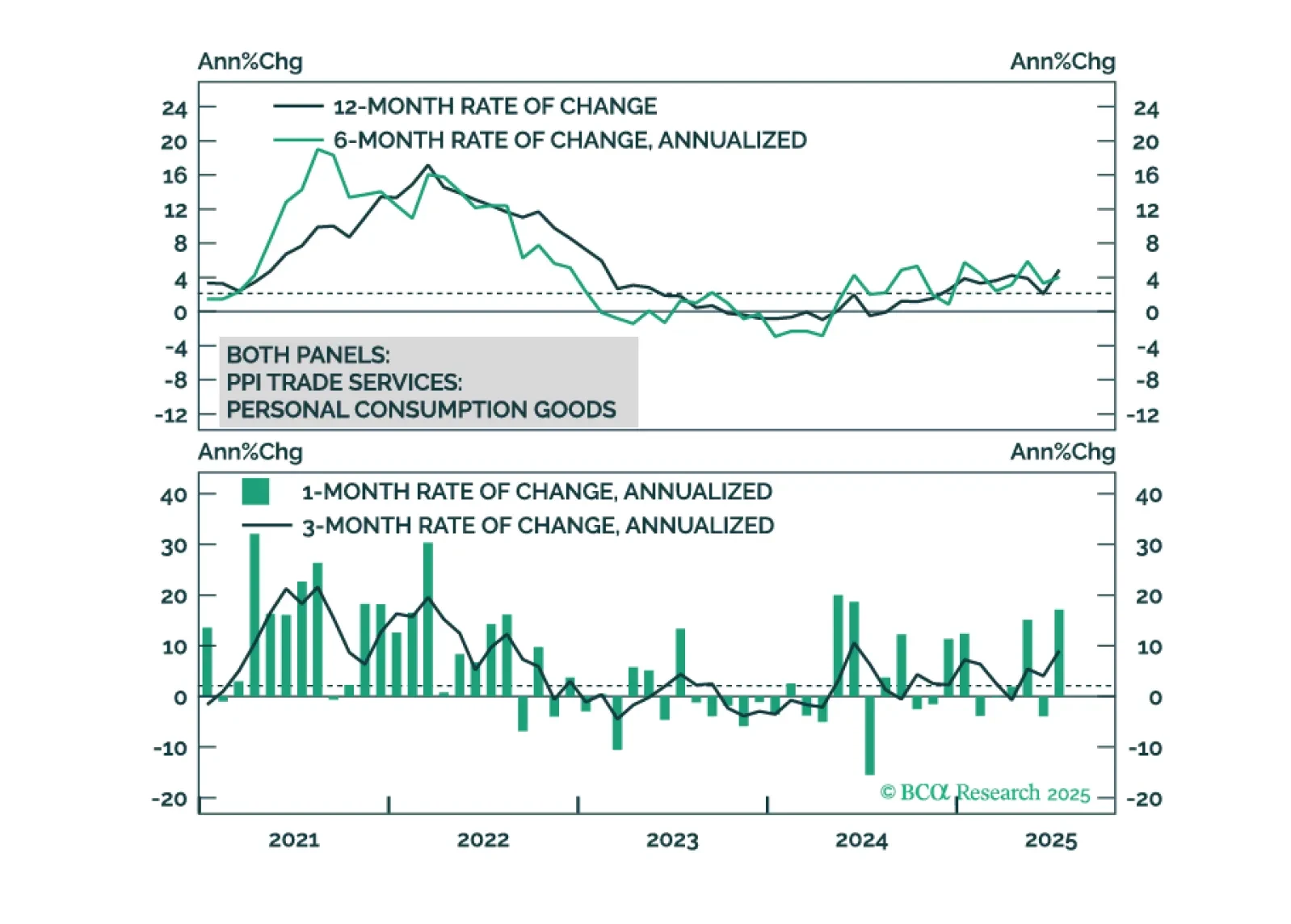

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

The July PMIs and inflation data confirm that China faces a persistent low-growth, deflationary backdrop, with weak demand and tariff risk warranting defensive equity positioning. The Caixin manufacturing PMI fell to 49.5, while services ticked up at 52.6.…

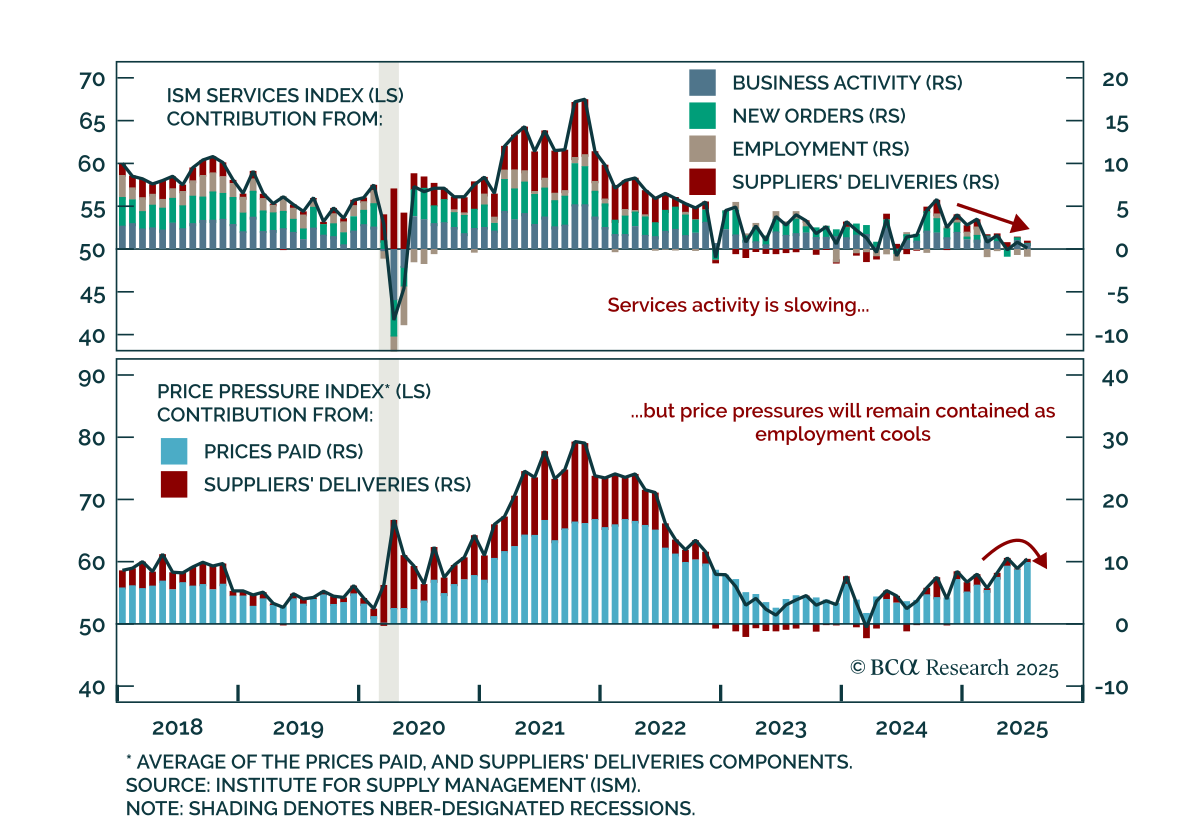

The July ISM Services report showed a stagflationary impulse, but soft labor momentum reinforces the view that price pressures remain contained. The headline index fell to 50.1 from 50.8, missing expectations. New orders softened to 50.3, while employment…

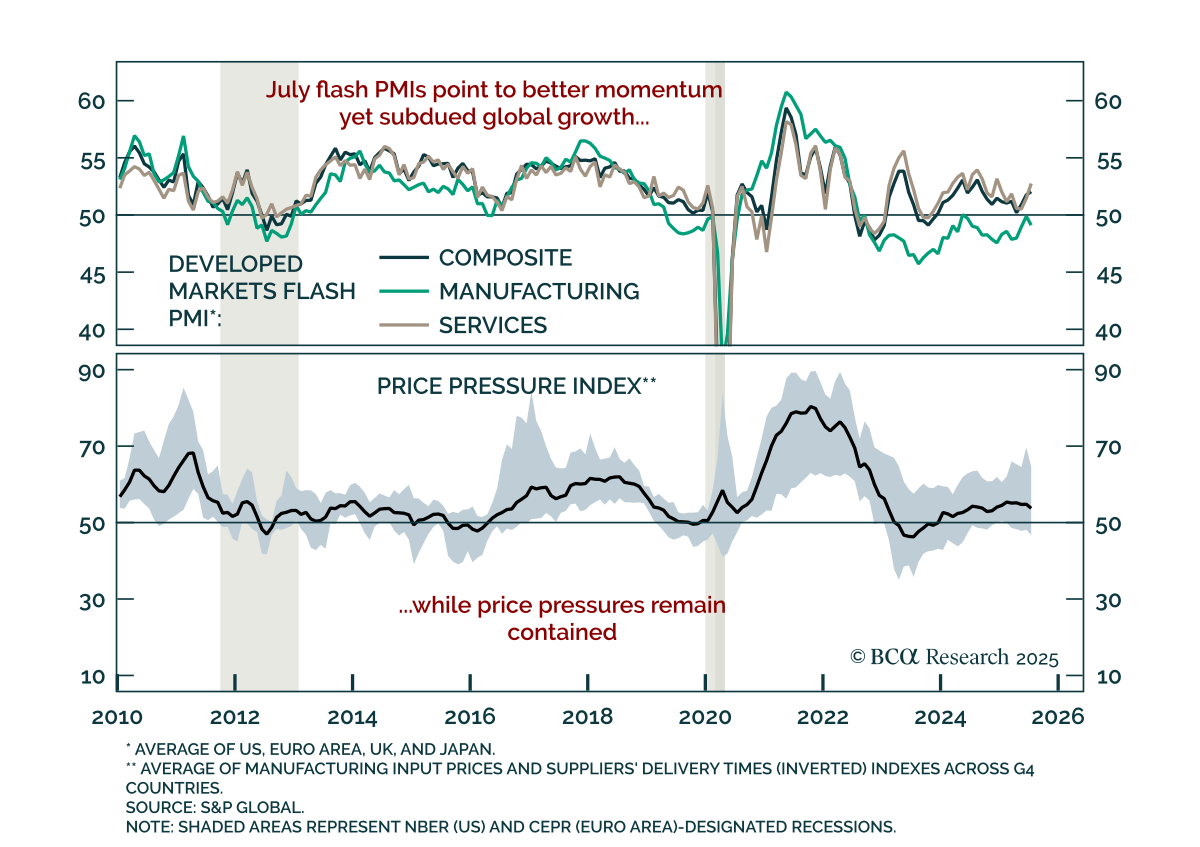

July DM flash PMIs point to improving global growth momentum led by services, but manufacturing remains weak and upside is limited, reinforcing our defensive stance. Services PMIs improved in the US, Europe, and Japan, but slowed in the UK. Manufacturing…