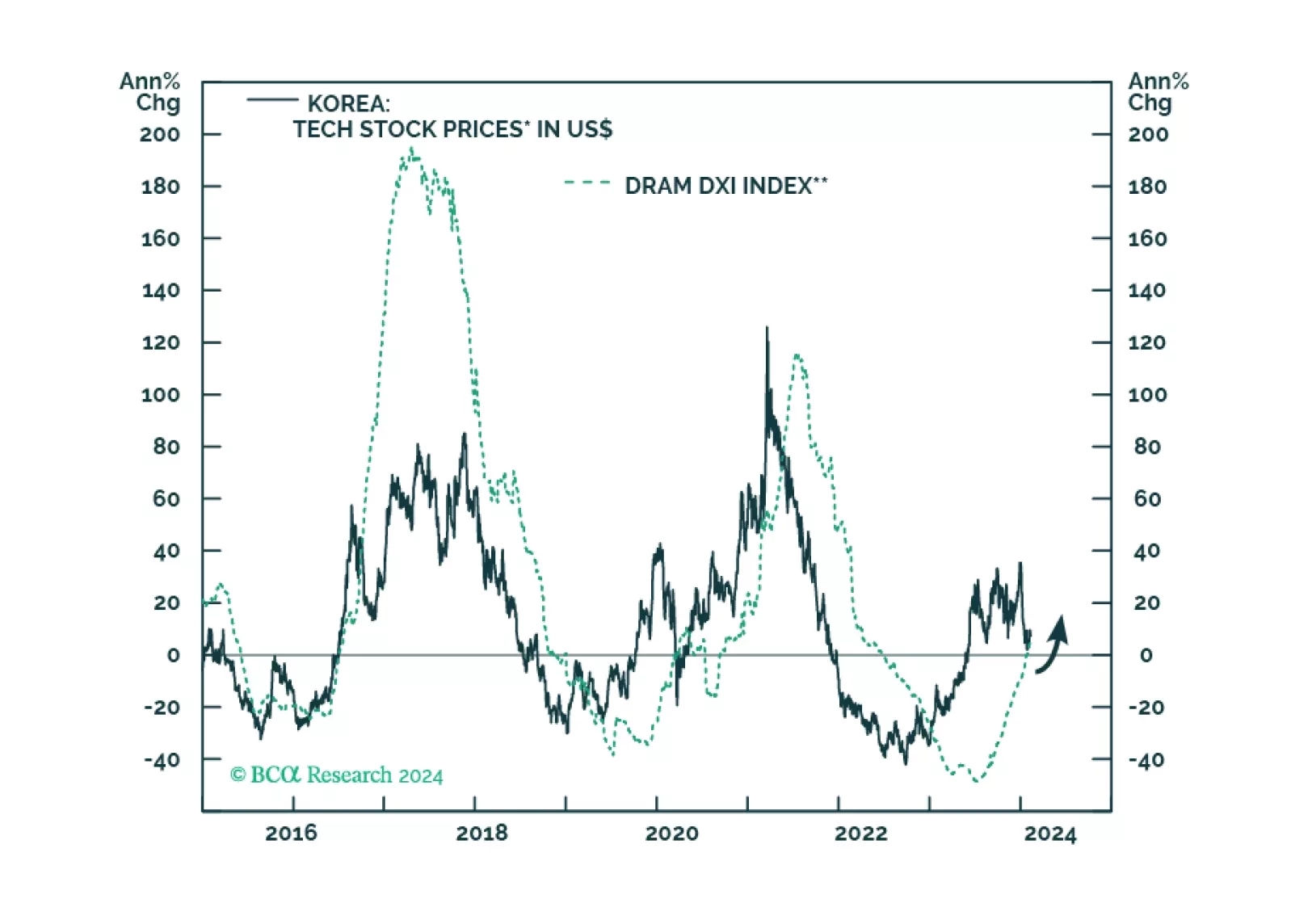

South Korea

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

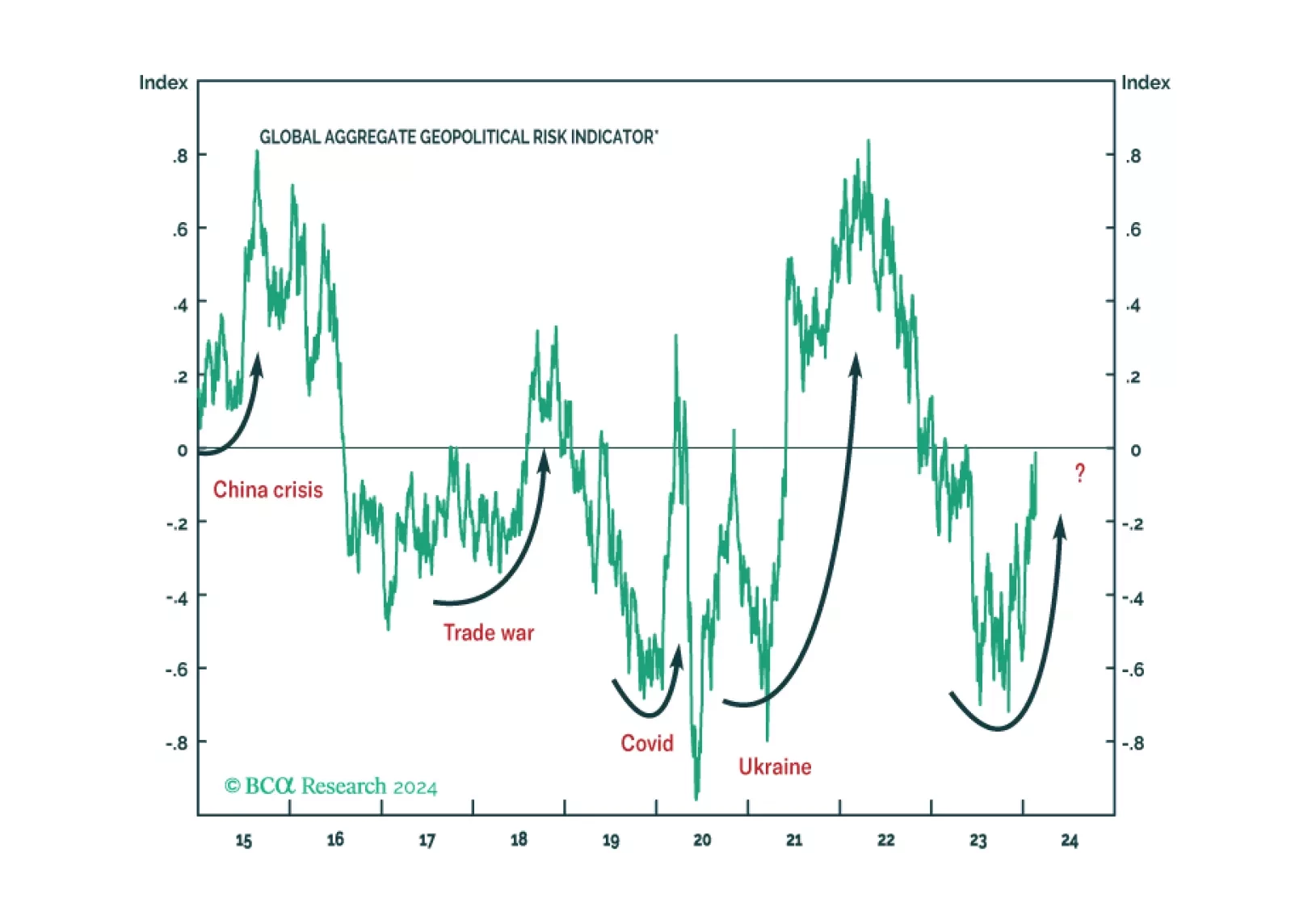

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

The global memory chip market will improve in 2024, characterized by a further rebound in memory chip prices and decent demand growth. Artificial intelligence (AI) memory and a replacement cycle of servers, smartphones, and PCs will propel memory chip shipment. We remain overweight South Korean equities within the EM equity benchmark. we also recommend a new relative trade of long Korean tech stocks and short the EM equity benchmark.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.