Sovereign Debt

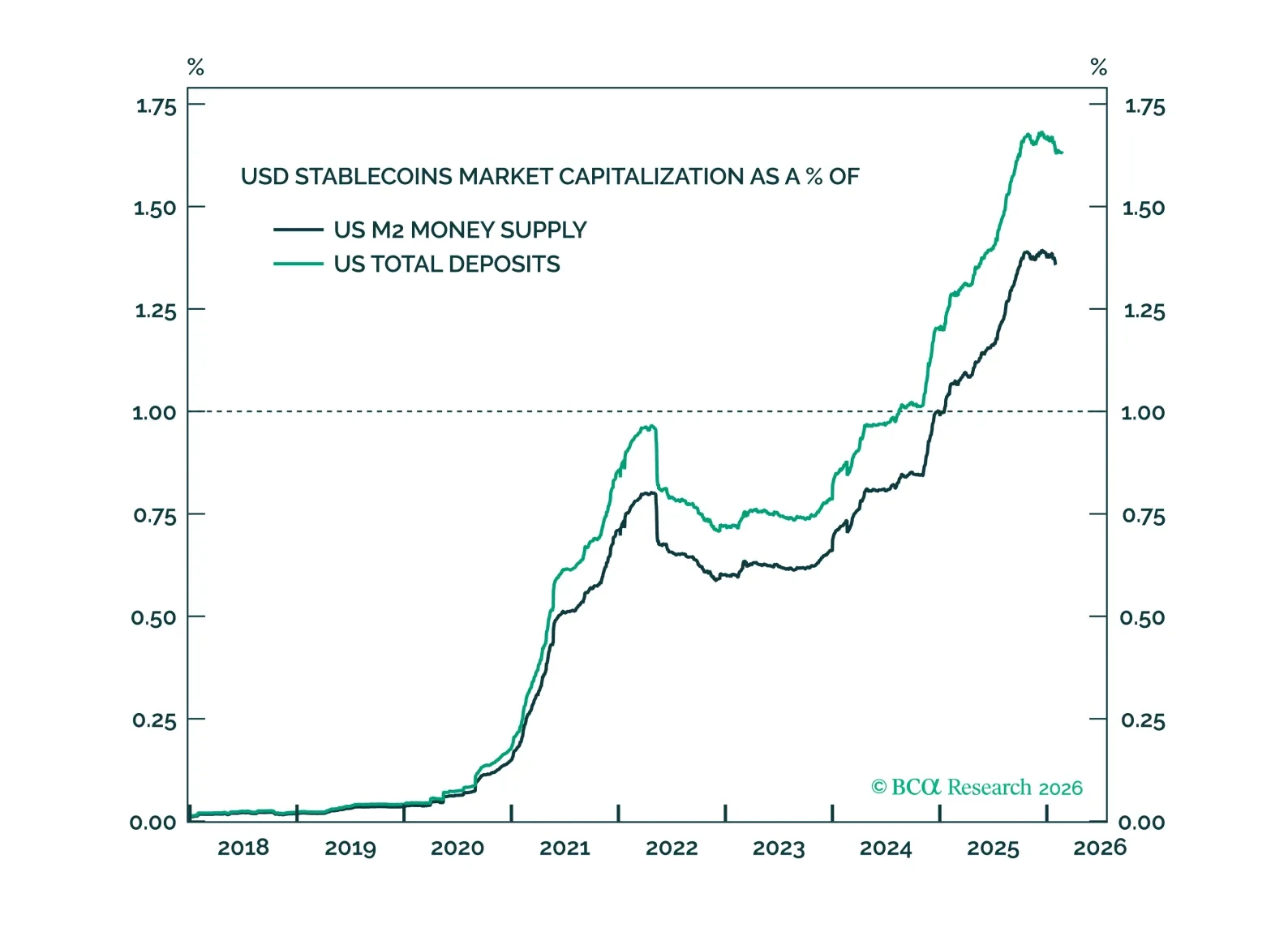

Stablecoins are evolving from a niche crypto instrument into a macro-relevant financial layer. This Special Report maps the transmission channels and consequences for the Treasury market, bank funding dynamics, and the dollar’s global footprint.

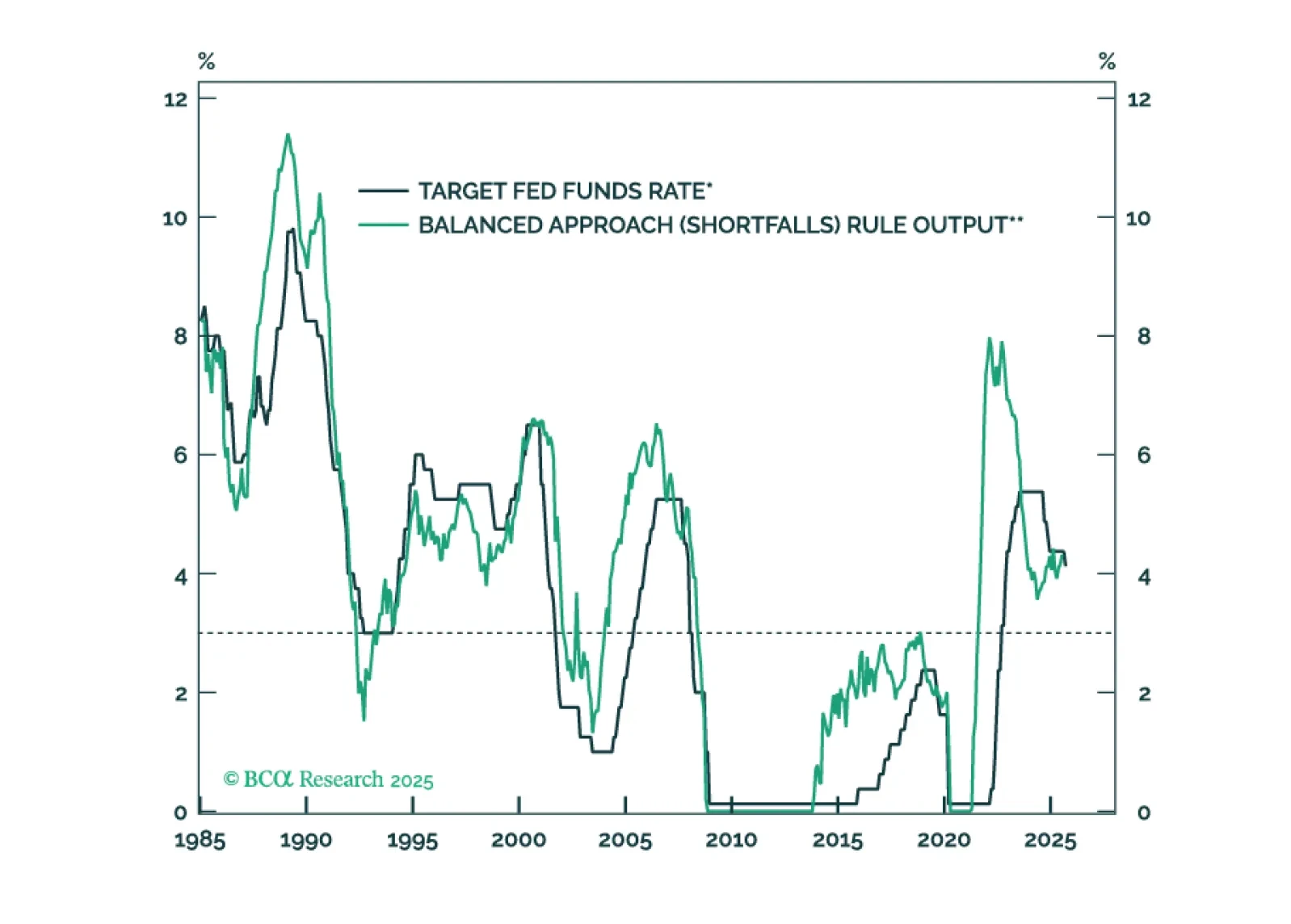

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

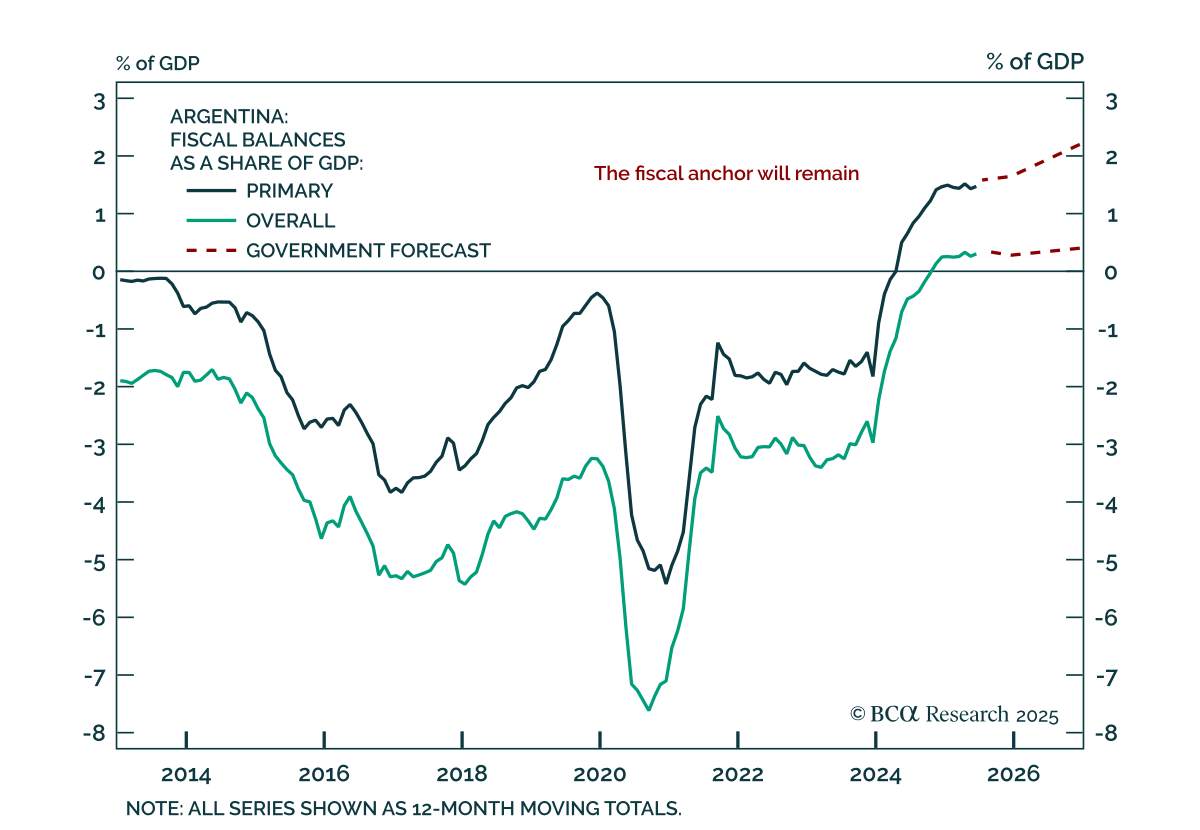

Despite the post-election selloff, investors should continue buying Argentine assets on weakness. Argentine markets sold off sharply after President Milei’s party suffered a crushing defeat in Sunday’s Buenos Aires election. Investors did not expect the…

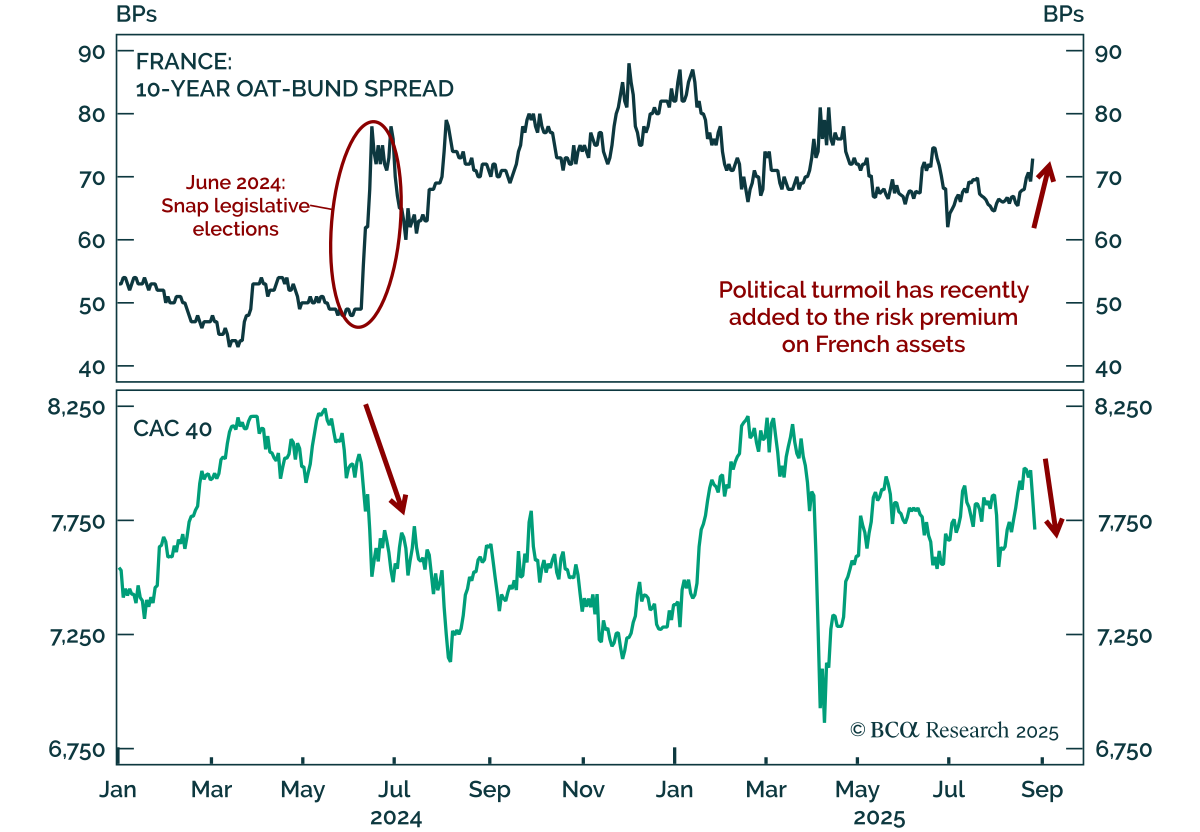

France’s renewed political turmoil highlights fiscal risks for OATs, but creates opportunities to buy French equities on dips. PM Bayrou has called a September 8 confidence vote over his deficit-cutting budget proposals, triggering a selloff in the…

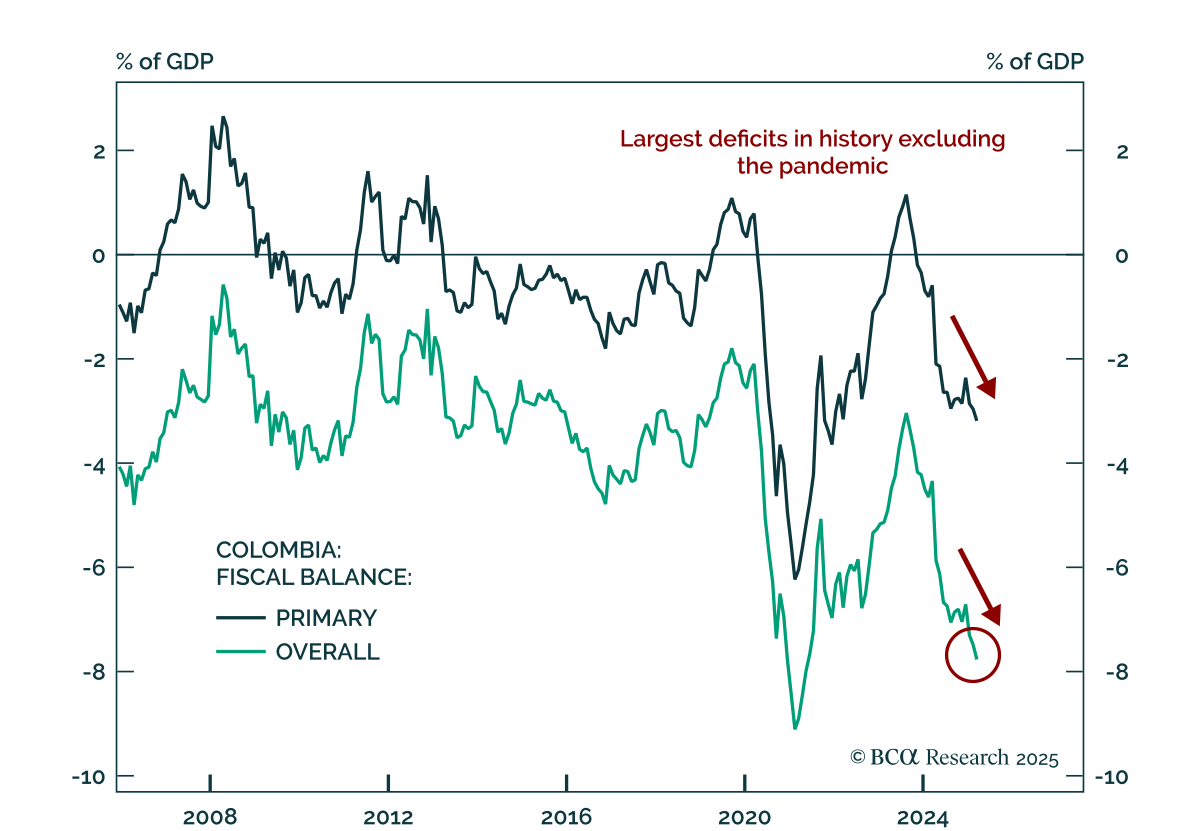

Our Emerging Markets strategists have upgraded Colombian equities, local bonds, and sovereign credit from underweight to neutral relative to EM benchmarks. Markets are caught between optimism about a potential rightward policy shift in 2026 and a…

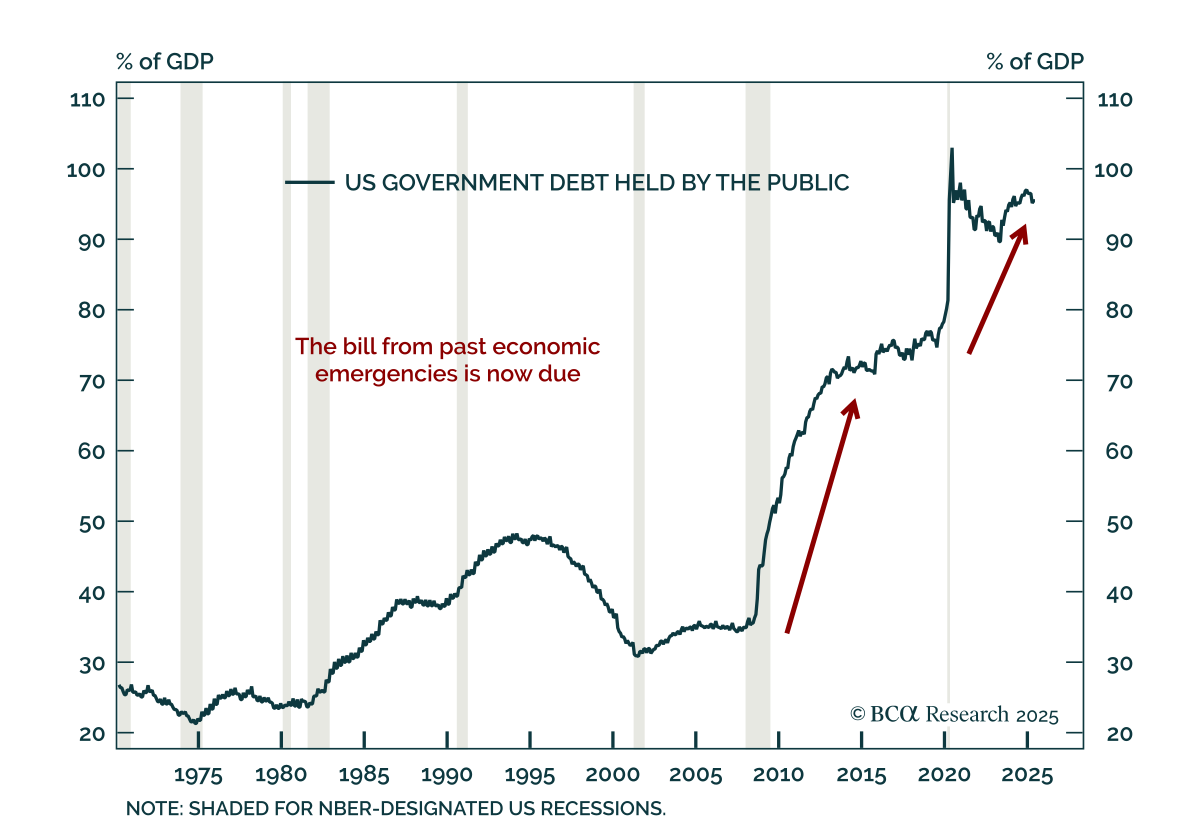

Our Bank Credit Analyst strategists argue that a US fiscal crisis should be treated as a base case over the next decade, not a tail risk. The ballooning US budget deficit reflects higher interest rates, demographic pressures, and the lingering effects of past…

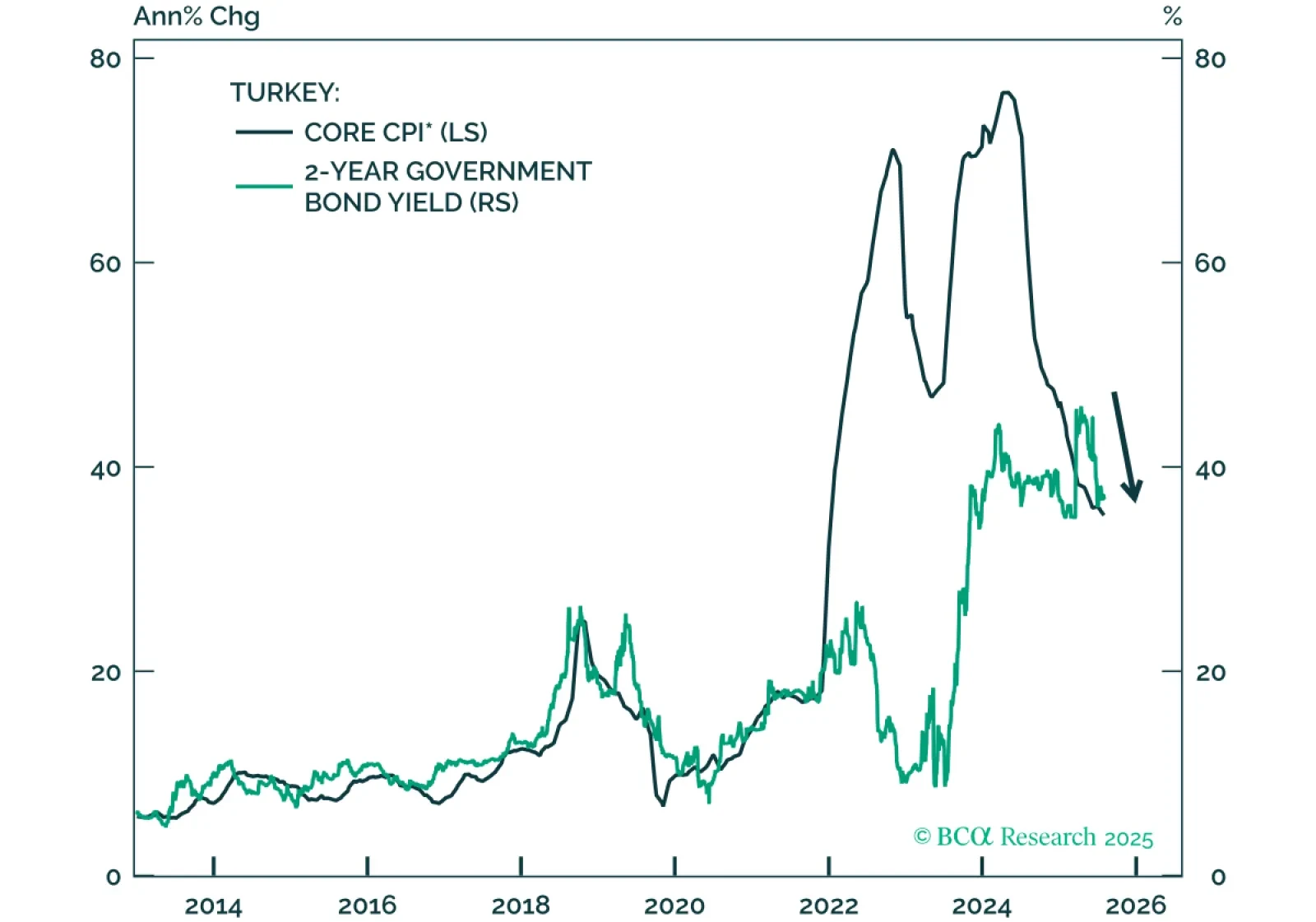

Turkey’s financial policymakers have pursued a disciplined and restrictive policy mix so far, delivering high real interest rates and curbing fiscal expansion even as the economy slows. This commitment to inflation control has paved the way for a pronounced decline in price pressures, prompting BCA’s Emerging Markets Strategy team to upgrade Turkish domestic bonds to overweight in its EM domestic bond portfolio. Similarly, Moody’s has recently upgraded Turkey’s credit rating and outlook. The lagged effects of the restrictive stance are now increasingly evident: real bank lending rates hover near 30%, real domestic demand growth is decelerating, and fiscal expenditure increases are barely keeping pace with inflation. Collectively, these conditions point to further disinflation and declining bond yields in the coming quarters (Chart 1).From an FX strategy perspective, the Turkish lira (TRY) presents a less precarious profile than many fear and what the forward markets currently imply.First, the current account deficit has narrowed considerably in recent years. As tight policy weighs on domestic demand, it will further curb goods imports and keep the current account deficit in check (Chart 2). This improvement should offset much of the expected export contraction due to slowing demand from the European manufacturing sector, reducing pressures on the lira from external balances. Second, the combination of receding inflation and very high nominal yields creates a compelling environment to attract sizable foreign portfolio flows into local currency debt. With foreign ownership of Turkish domestic government bonds currently low by historical standards, there’s significant room for new inflows (Chart 3). As such, the TRY depreciation over the next year will likely fall well short of the 26% pace currently implied by forward markets vis-à-vis the USD. Historically, periods of falling inflation have coincided with slower lira depreciation (Chart 4). A weaker trade-weighted US dollar could reinforce this trend, further curbing pressure on the currency. In this context, short-end local currency bonds are becoming increasingly attractive to global investors.Bottom Line: Falling inflation and a narrow current account deficit in Turkey have historically gone hand-in-hand with a less vulnerable currency. This time should be no different: the pace of the lira’s depreciation against the US dollar will likely ease in the coming months.

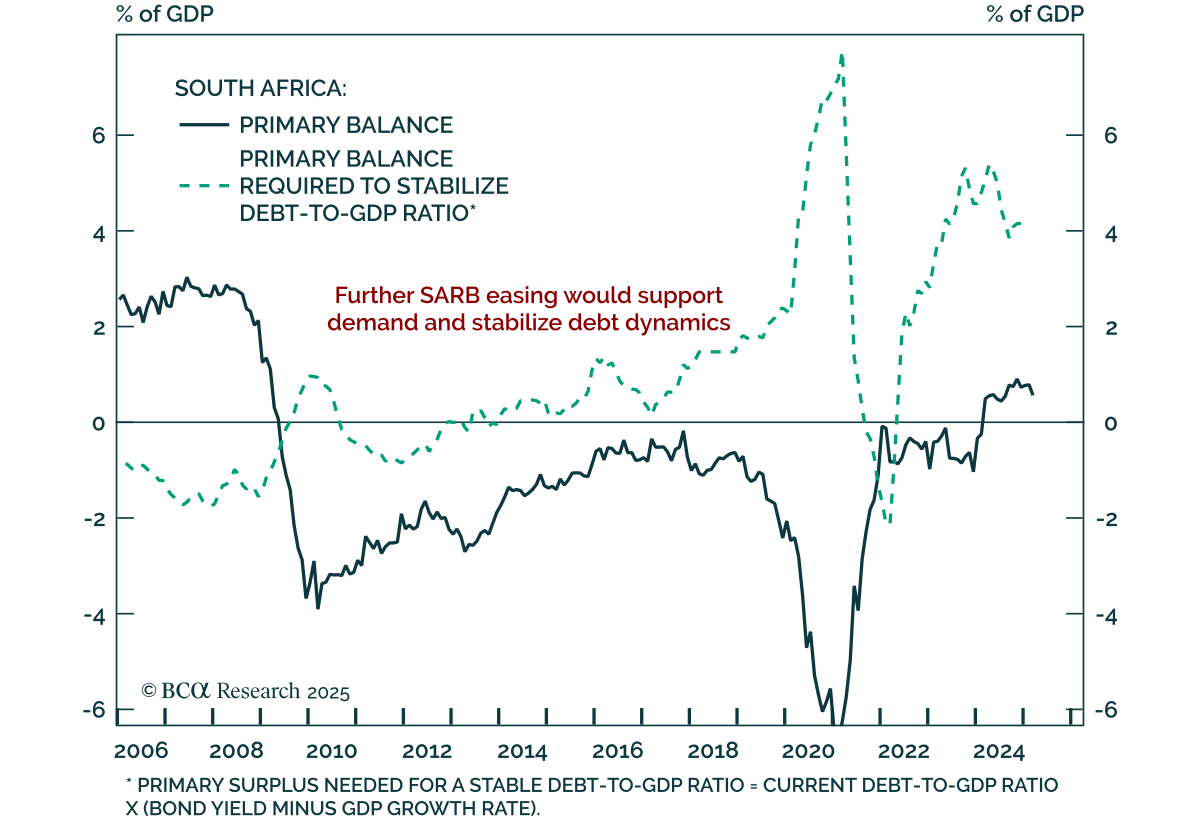

The SARB cut rates by 25 bps to 7.00%; our EM strategists expect further easing and recommends short ZAR exposure. Real interest rates remain elevated, and high borrowing costs are intensifying debt sustainability concerns, with 10-year yields far above…

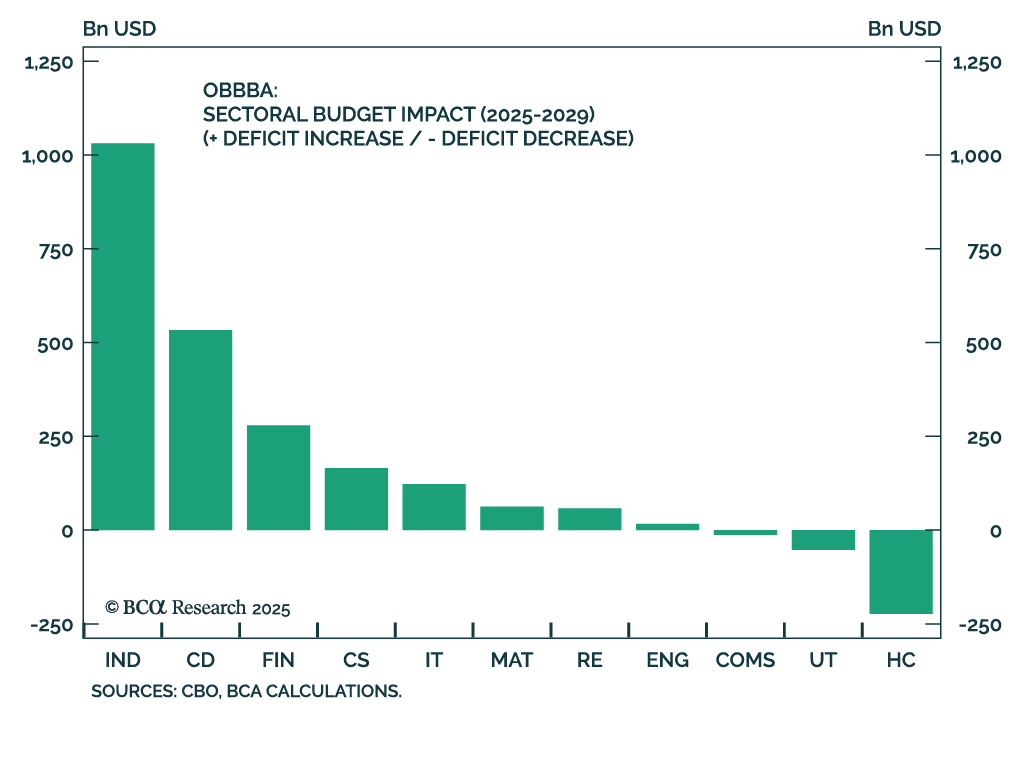

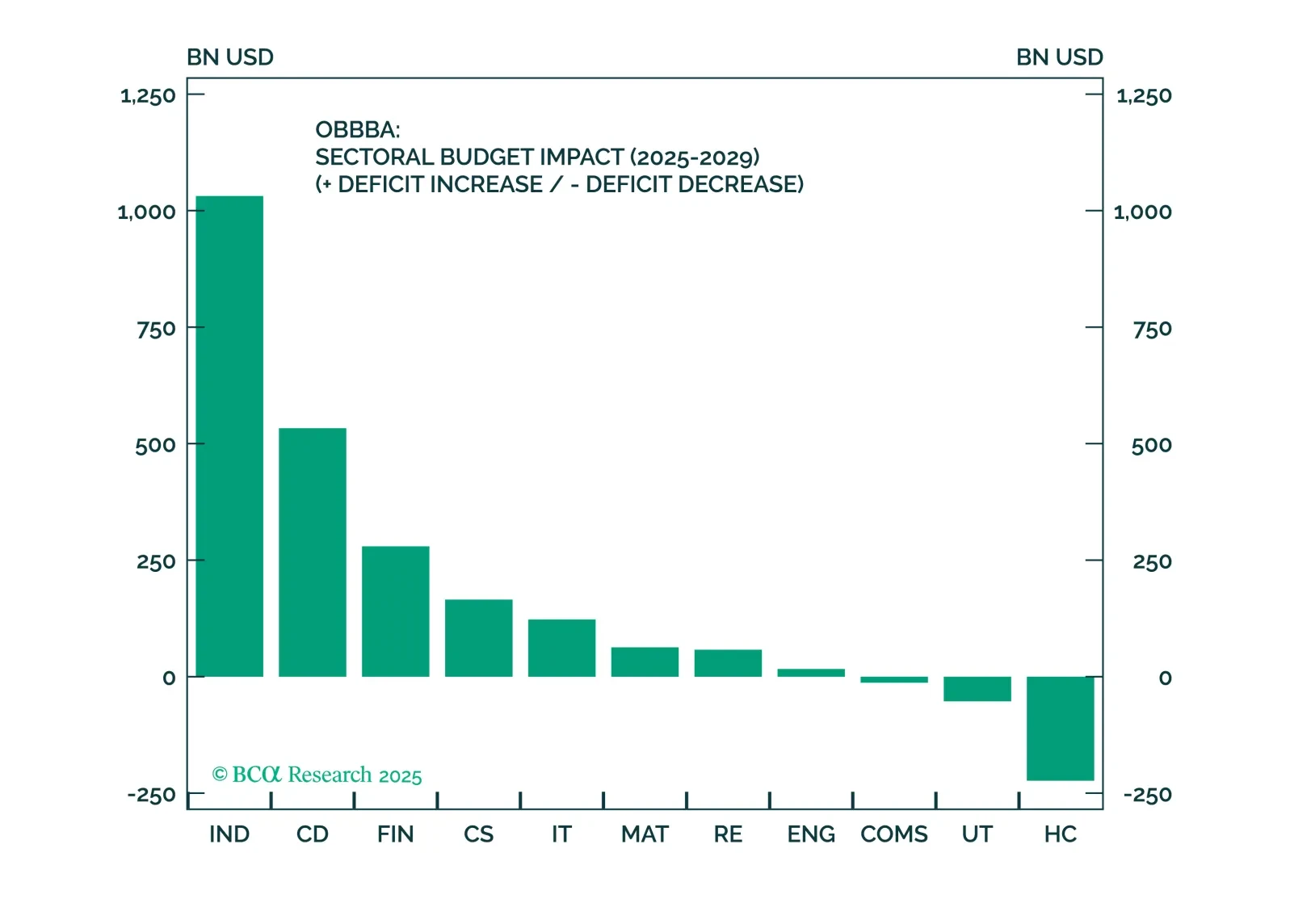

Our Geopolitical and Equity Analyzer teams recommend a Value and Quality-focused equity basket in Industrials, Financials, and Consumer Discretionary to capture OBBBA-driven upside. These sectors are the primary beneficiaries of the newly passed stimulus…

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.