Sovereign Debt

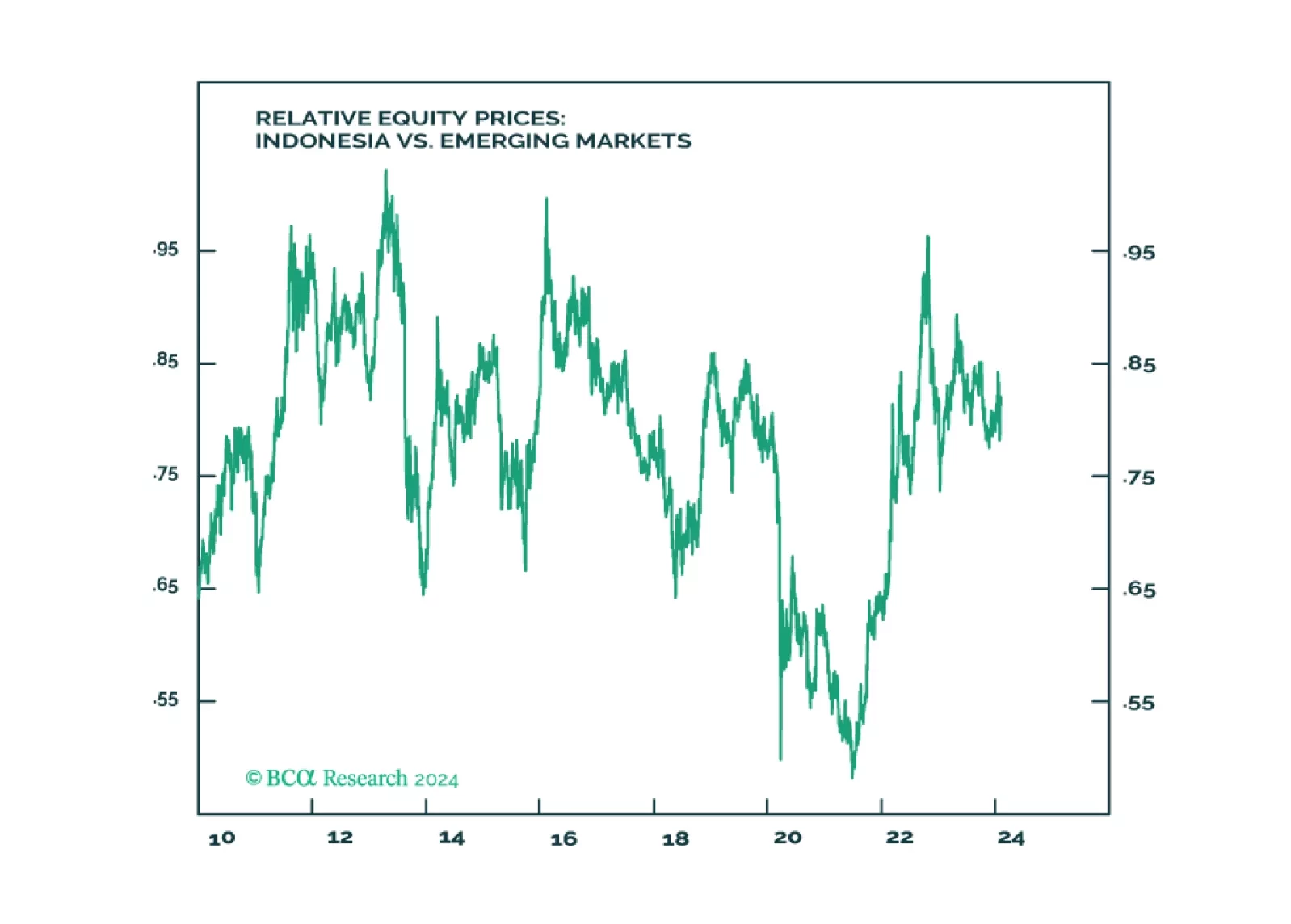

Indonesia will not revert to dictatorship. Yet the guardrails against authoritarianism are also constraining the actions of the next government in tackling near term domestic and regional challenges. For long-term positioning, use potential selloff from a “dictatorship scare” to build position as structural outlook for Indonesia is positive due to the China-West divorce and the global energy transition.

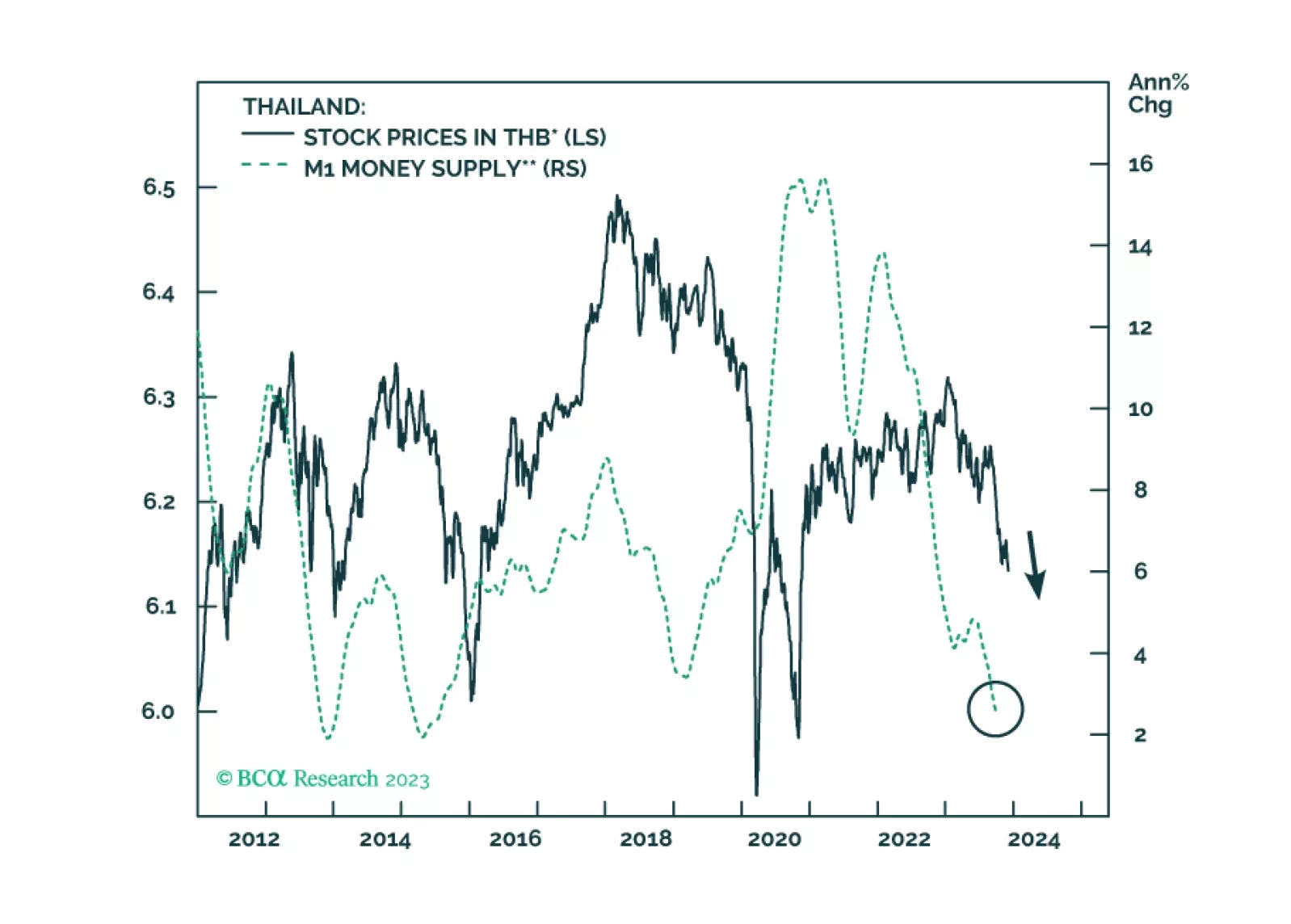

Meager credit growth and shrinking real wages will keep Thai inflation very low in the coming months. The currency will get support from an improving current account surplus. Fixed-income investors should upgrade Thailand from neutral to overweight within EM domestic bond portfolios.

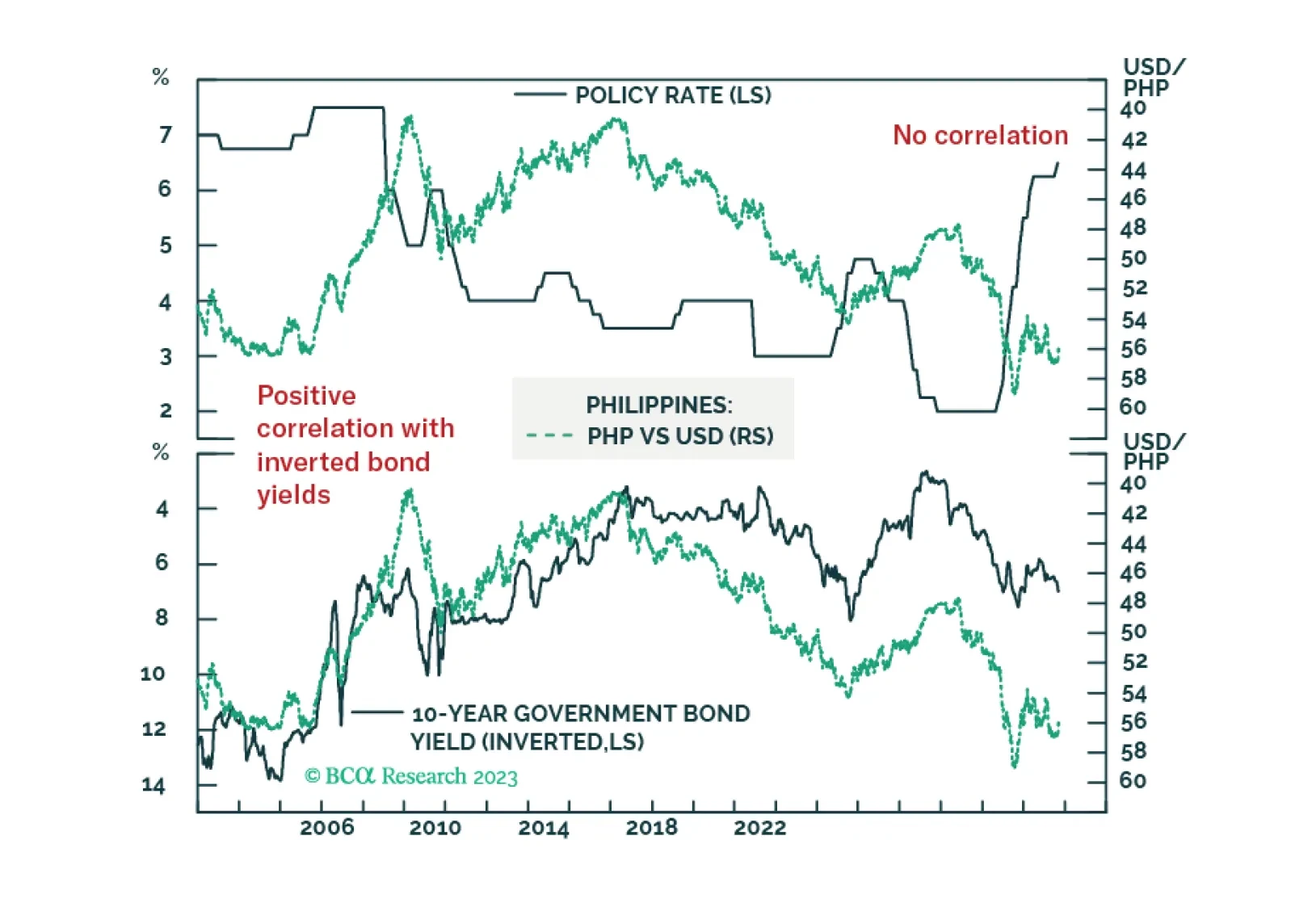

The recent rate hike by the Philippines central bank cannot control food inflation. Nor can it stem the currency slide.

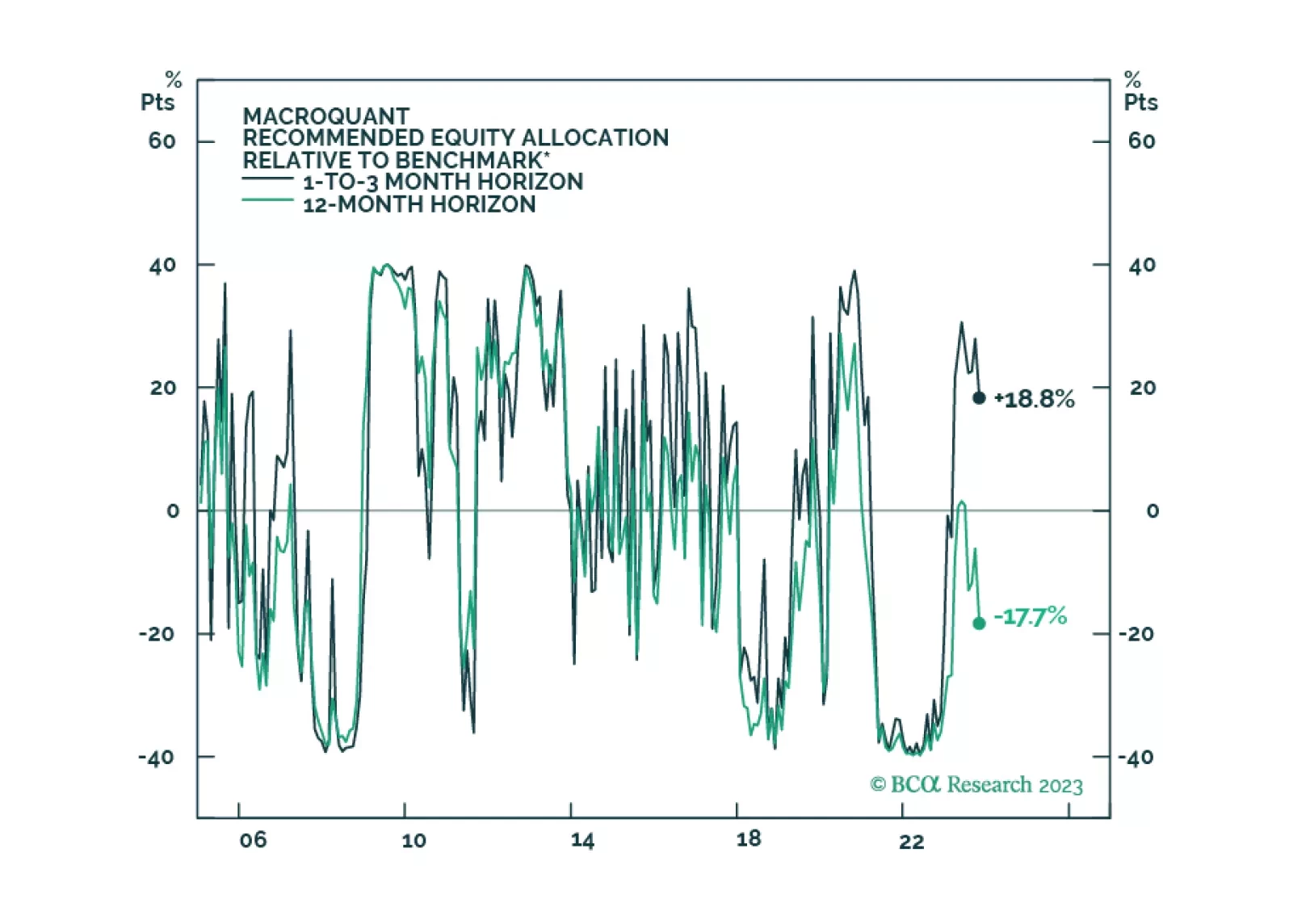

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

China’s extremely high savings rate is the real culprit behind its current economic woes. The authorities have been slow to stimulate the economy, and the risks of “Japanification” have increased. For now, the fact that China is exporting deflation is not such a bad thing. However, if global recession risks were to flare up again, a lethargic Chinese economy would be a cause for concern. Chinese stocks are quite cheap but lack a clear catalyst to move higher. Favor EM markets where earnings and sales estimates have been moving up lately.