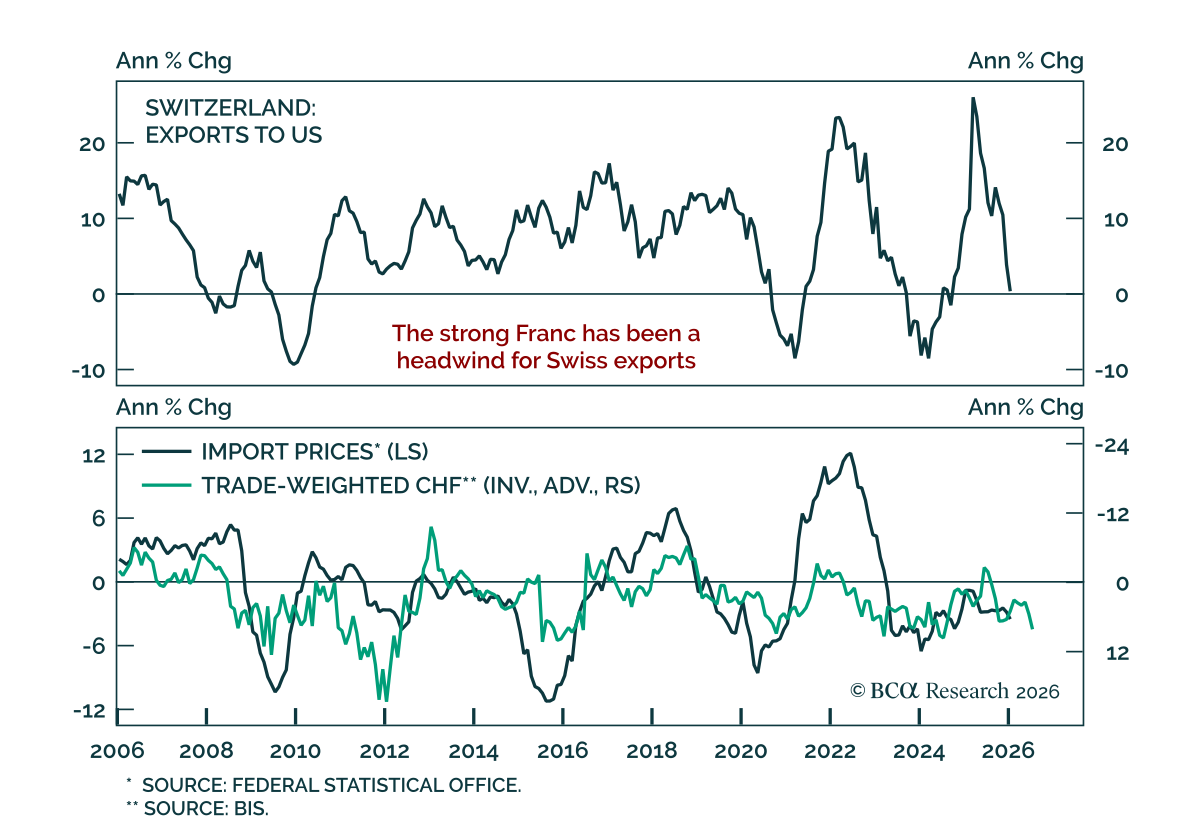

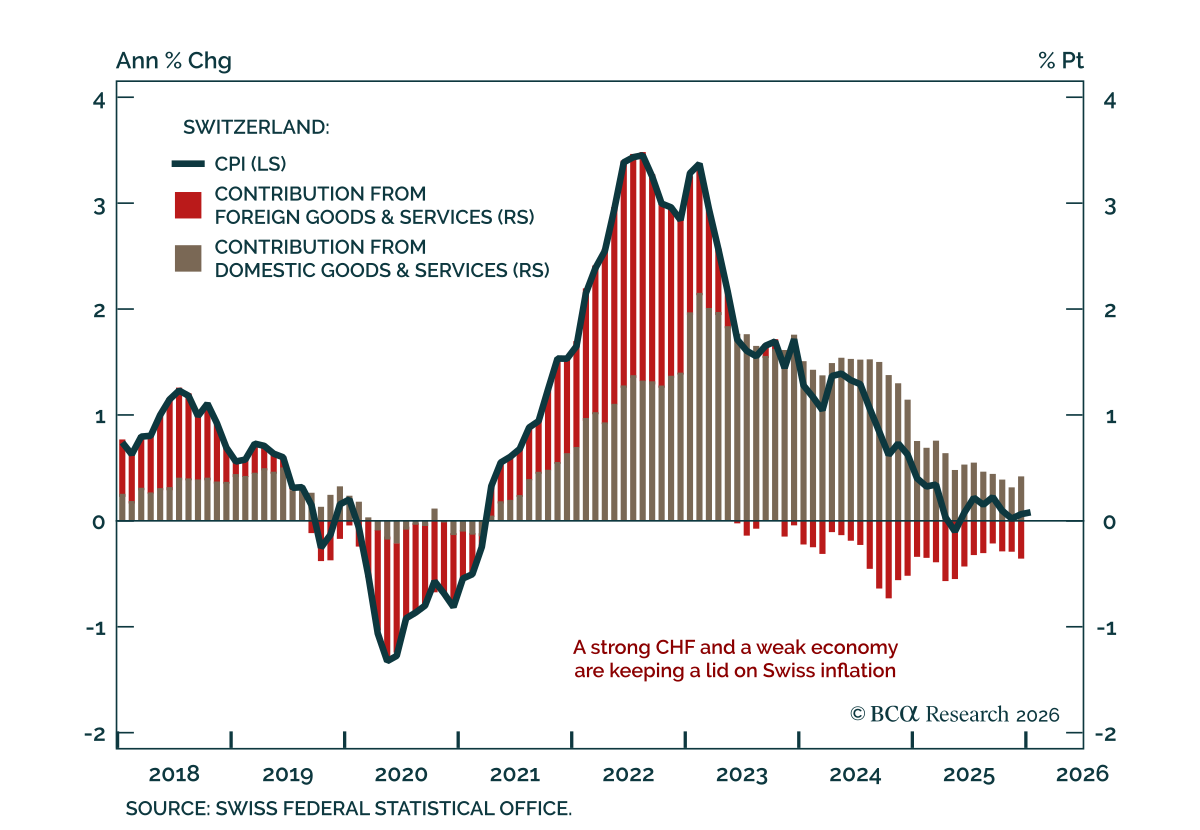

Switzerland

The Section 122 tariffs under the US Trade Act of 1974 are more favorable to Europe; the trade-weighted tariff rate falls to 10.45%, from 11.74% pre-ruling. This positive development does not change our overall views on Europe, as we expected lower tariffs ahead of the US midterms.

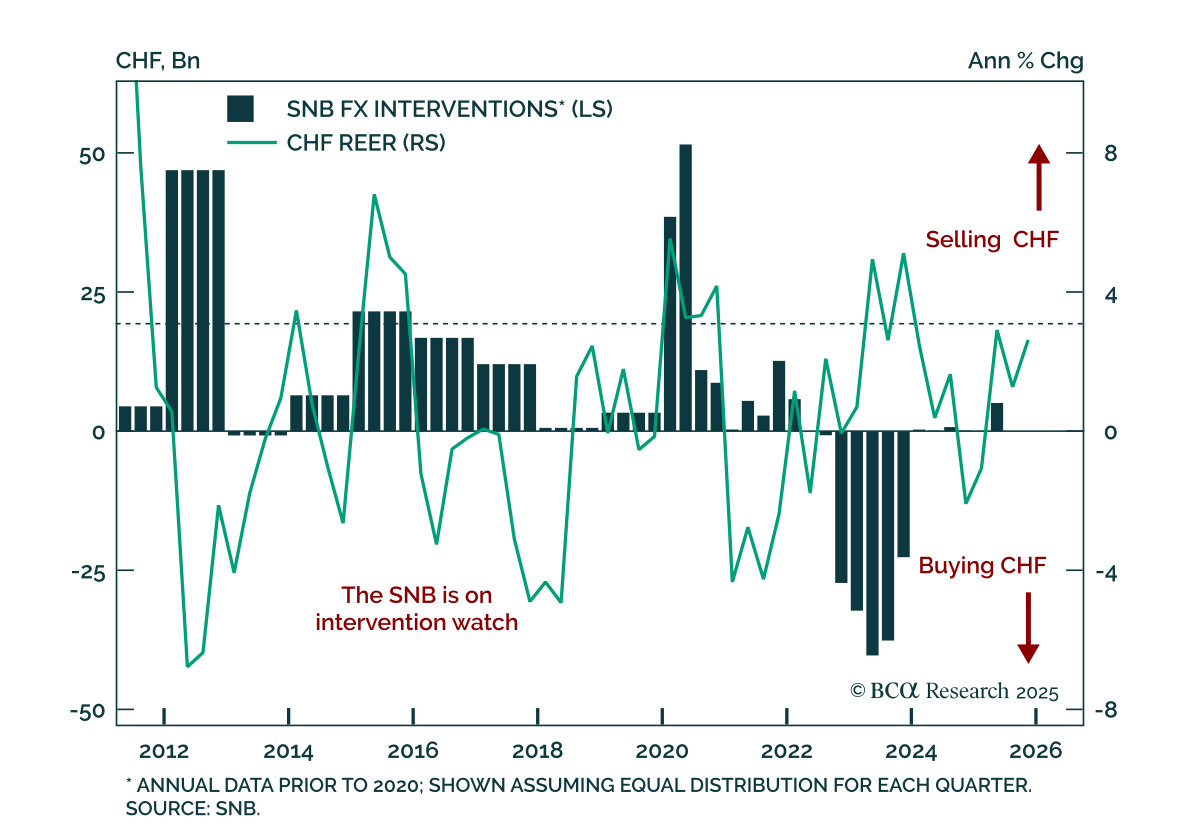

We spent last week meeting investors in Switzerland. This Strategy Insight revisits the most prominent topics we discussed, including repatriation fears, SNB intervention, and Dutch pension reform.

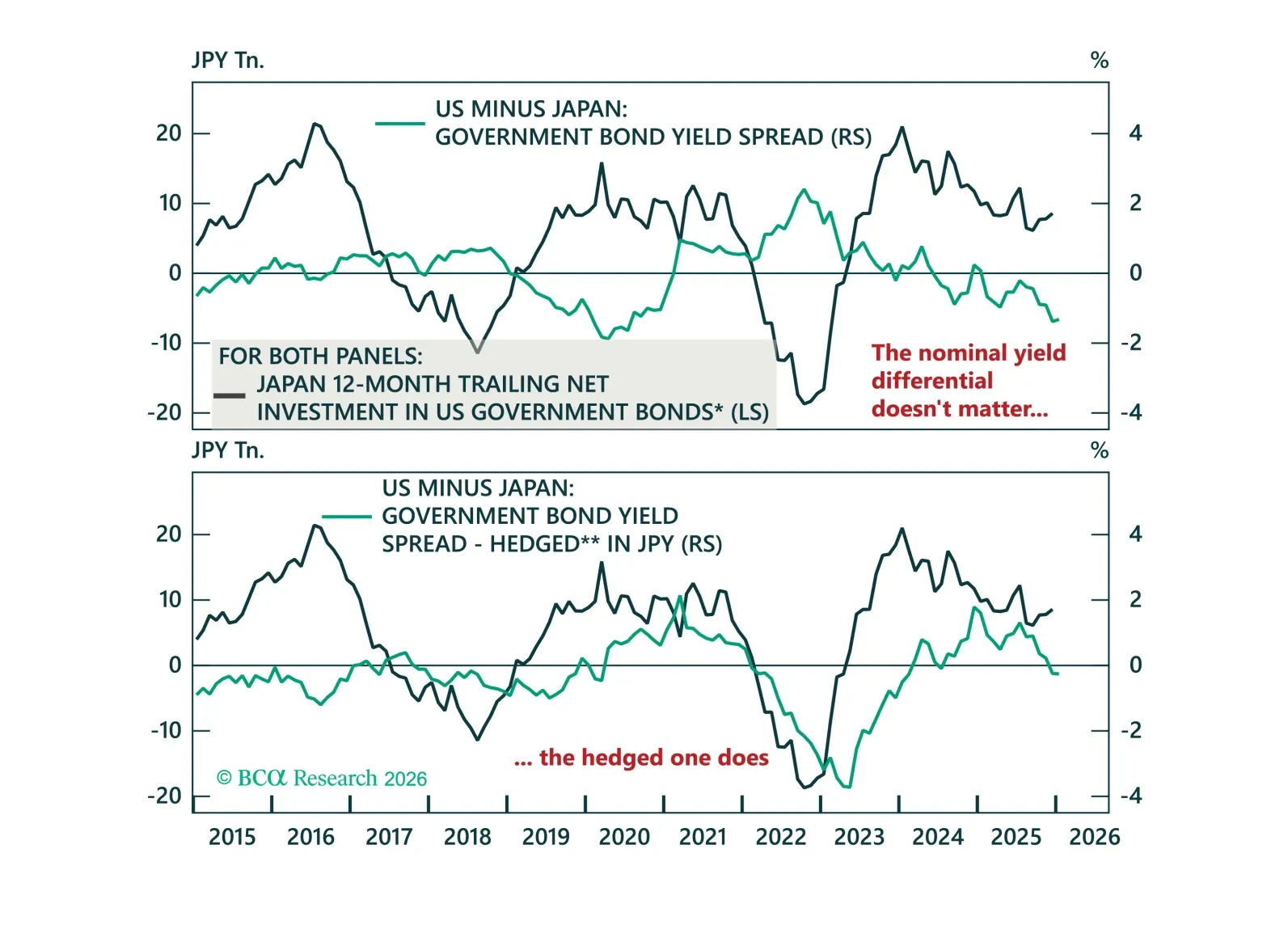

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

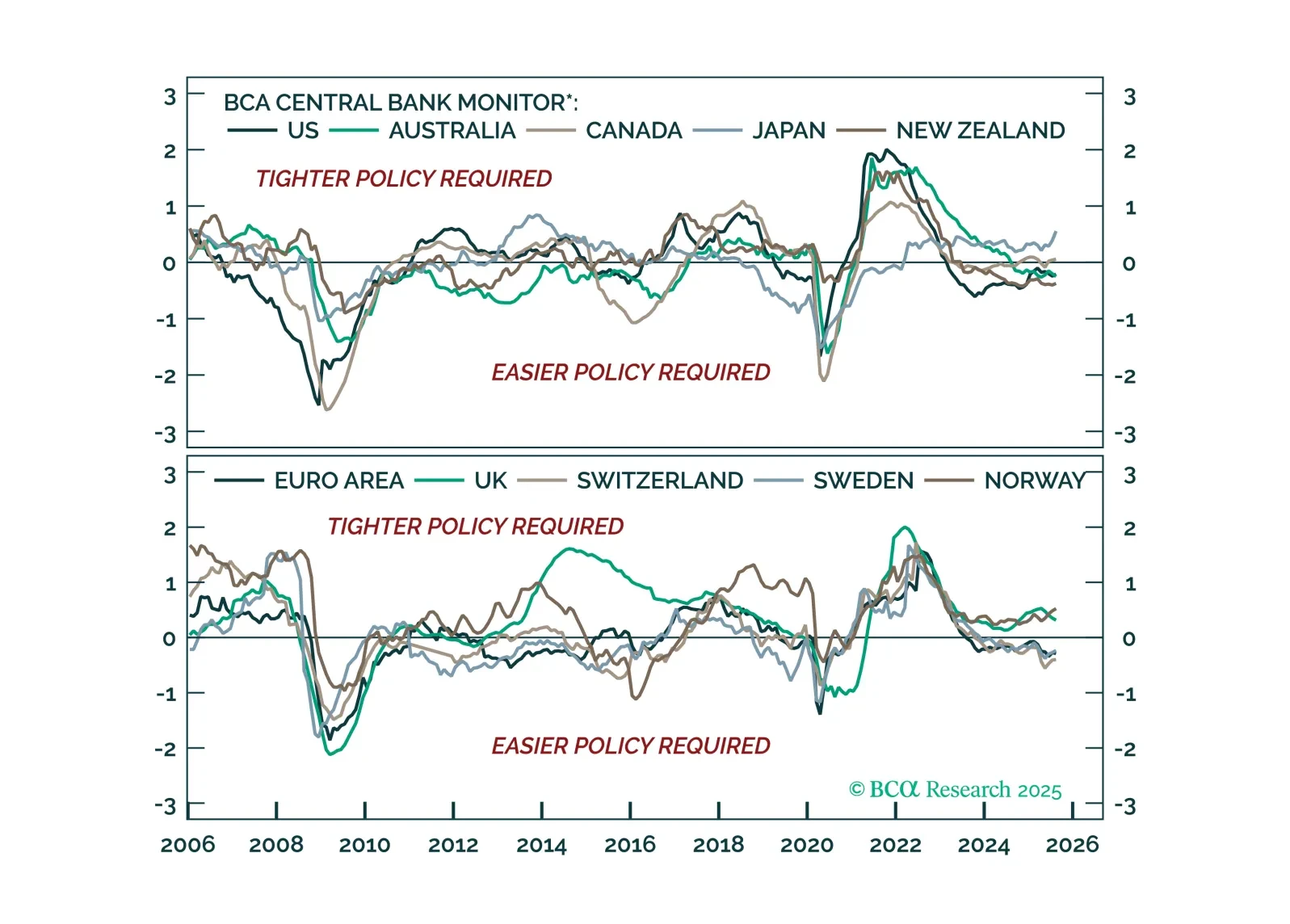

Monetary policy divergences are re-emerging. We rely on BCA’s Central Bank Monitor to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.