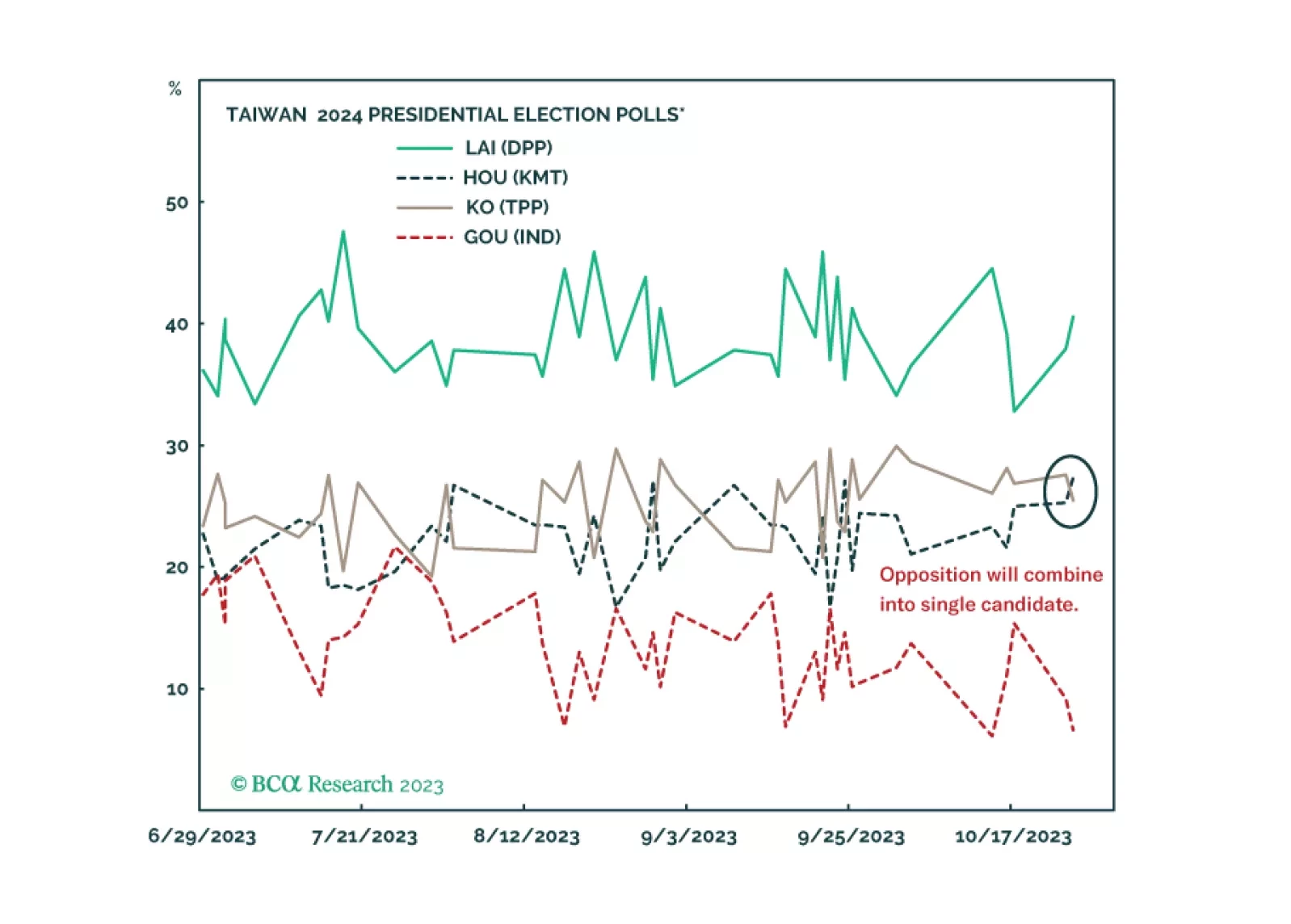

Taiwan

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.

China removed checks and balances in its political system to deal with a very dangerous economic transition. The transition is going badly, yet investors cannot rely on checks and balances to correct or prevent policy mistakes. The Taiwanese election is a looming bellwether.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.