Technology

Highlights Contrary to popular belief, the correlation between changes in interest rates and equity returns is not fixed: Stock prices have generally risen as yields have fallen over the last four decades, but there is no rule that states equity returns and bond yields will be inversely related. Tech stocks’ tight recent inverse correlation with interest rates is a new phenomenon and we expect it will be temporary: Relative differences in earnings have driven relative returns since the global financial crisis and their mirror image correlation with interest rates was a pandemic anomaly that has already withered. Rising interest rates are not a good reason for equity investors to reduce their Tech exposures: The conventional wisdom is not always wrong, but it almost never generates alpha. In this case, we believe the crowd has fallen for a fleeting illusion that will not persist. Feature Table 1Lapping The Field

Tech Stocks And Interest Rates: Less Than Meets The Eye

Tech Stocks And Interest Rates: Less Than Meets The Eye

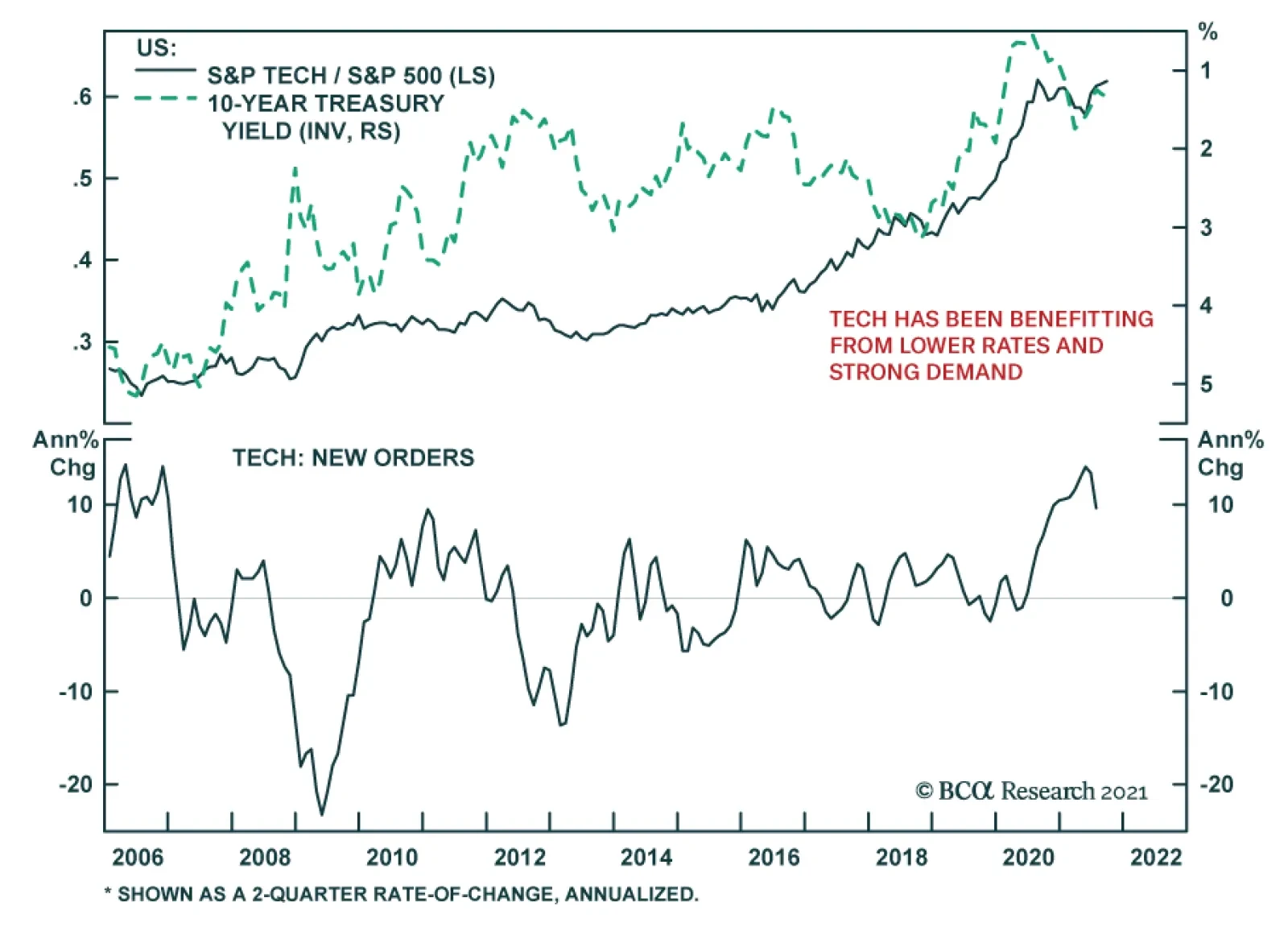

Perhaps nothing has lately generated more consensus agreement among equity strategists and other top-down observers than the claim that Tech stocks are particularly vulnerable to rising interest rates. Thanks to the Tech sector’s track record of generating outsized growth (Table 1), its future earnings streams are expected to be larger for longer than other sectors’, making them somewhat akin to long-maturity bonds from a duration perspective. Go-go growth stocks and Treasuries make for strange bedfellows, no matter how logical the earnings-stream reasoning may appear to be at first glance, and we view the application of duration concepts to equities as a stretch in any event. In this Special Report, we make the case that the recently observed tight inverse correlation between relative Tech sector performance and the 10-year Treasury yield is anomalous and should not be expected to persist. Right Church, Wrong Pew Duration is the weighted-average term to maturity of a bond’s cash flows and describes its price sensitivity to changes in interest rates. It is an essential feature of fixed income markets but attempts to extend the concept to equities necessarily fall flat. Bondholders receive interest and principal payments subject to a contractually fixed schedule that makes valuing a bond, especially one with negligible credit risk, a simple exercise in arithmetic. The present value of any bond (PV) is equal to the sum of its discounted series of cash flows, as in the equation

Chart

, where x = one of a series of n semi-annual payments, r = the discount rate and t = the time in years when the next payment will be received.

Chart 1

Assuming that all the interest payments and the principal payment will be received on time, the only variable term in the bond present value equation is the discount rate, r. As r appears solely in the denominator, a bond’s present value is inversely related to its moves. The cash streams accruing to stockholders are inherently unpredictable, however, and the present value of an equity interest is subject to fluctuations in the realized and estimated future values of x as well as changes in discount rate r. Forces that move r may or may not also move x and it is uncertain whether the numerator or denominator will exert a greater impact if they move together, as they might be expected to do in the case of the high-growth Tech sector. The explanatory power of changes in interest rates weakens as cash flow uncertainty increases. Month-over-month changes in the 10-year Treasury note yield1 explain virtually all the variation in one-month Bloomberg Barclays Treasury Index total returns (Chart 1, top panel). As cash flows become more uncertain with the introduction of modest credit risk, the correlation slips to -40% (Chart 1, middle panel). It weakens even further and flips its sign with equities, which have done better since the financial crisis when the 10-year yield rises than when it falls (Chart 1, bottom panel). Bottom Line: Duration is a metric for measuring bonds’ price sensitivity to changes in interest rates. Because of the uncertain nature of a company’s future cash flows and the multitude of independent variables that influence them, duration is an ill fit with equities. The Post-Crisis Experience The empirical record poses several challenges to the conventional wisdom about Tech stocks and interest rates, beginning with their desultory relationship in the first ten years following the financial crisis. From 2009 through 2018, changes in the 10-year yield are unable to explain any of the variability in relative Tech returns, though they exhibit a tight correlation beginning in 2019 (Chart 2). Tech stocks were utterly indifferent to the yield spikes of 2009 and 2010-11, as well as the sharp intervening decline in 2010, and only began to separate themselves from the field following the Brexit vote, outperforming the overall S&P 500 by 30 percentage points in just two years while the 10-year yield rose from 1.5% to 3%. They then proceeded to blow away the index as yields fell from 2.75% at the end of 2018 to 0.5% at the mid-2020 COVID bottom and have since fought the index to a draw despite a 100-basis point backup above 1.6%. Chart 2Nothing More Than A Lockdown Fling

Nothing More Than A Lockdown Fling

Nothing More Than A Lockdown Fling

In contrast to their all-over-the-map relationship with the level of interest rates, Tech stocks have exhibited a consistently tight fit with relative trailing earnings. A quantitatively inclined visitor from outer space viewing Chart 3 might reasonably conclude that relative Tech stock performance is fully explained by earnings, and all other variables are noise. The series have moved nearly in lockstep with each other and show that Tech’s relative trailing P/E multiple has been quite stable since the crisis. Until relative prices and relative earnings began heading in separate ways as the latter began to slip this Spring, Tech’s relative post-crisis outperformance had entirely been earned, not given. Chart 3Case Closed?

Case Closed?

Case Closed?

Multiples provide an opportunity for interest rate changes to re-enter the discussion. In a direct sense, Tech earnings are comparatively immune to moves in interest rates (the sector’s biggest constituents have immaterial amounts of debt and do not sell big-ticket items that have to be financed), though one might expect the price investors are willing to pay to claim a share of their comparatively backloaded future cash flows may well fluctuate with them. Chart 4, however, shows that the Tech sector’s relative forward multiple has not exhibited a consistent relationship with rates – the correlation between multiples and rates was positive and fairly strong from 2009 through 2018 but weakened and turned negative beginning in 2019. From 1995, when the forward multiple series began, through 2008 (not shown in the chart) the relationship was very weak and negative, generating an r-squared of just 1.4%. Chart 4Defying The Duration Intuition

Defying The Duration Intuition

Defying The Duration Intuition

The relationship between relative four-quarter forward earnings expectations and the 10-year yield sheds some light on how so many observers have been hoodwinked into mistaking correlation for causation. Excepting stretches at the beginning and the end of the 2009-2018 period, when relative forward estimates paid no heed to swings in interest rates, they exhibited a modest negative correlation with the 10-year yield (Chart 5). They moved together with one mind across all of 2020, but that solidarity appears anomalous when viewed against the entire post-crisis record generally and the years that bracket it specifically. In 2018-19, the two years preceding peak pandemic conditions, and 2021, the year following them, Tech’s relative forward earnings expectations have been flatly indifferent to the rate backdrop. Chart 5One-Off

One-Off

One-Off

We submit that the recently observed tight correlation between the 10-year yield and relative forward earnings expectations is an isolated pandemic phenomenon. As bond yields plunged in 2020 due to extraordinary monetary accommodation and fears of a worst-case economic outcome, Tech’s heavy concentration of pandemic winners shot the lights out in terms of actual and projected earnings. Away from the narrow 2020 sample, however, the other twelve years of post-crisis data suggest that there’s no relationship between forward earnings expectations and interest rates. Tech outearned the broader market at a steady rate for the ten years preceding the pandemic without regard for the rates market’s gyrations. Investment Implications Interest rates are a red herring for explaining variations in relative Tech stock performance. The ubiquity of the view that Tech stocks’ relative performance will be heavily influenced by changes in interest rates turns out to be another instance in which something everybody knows turns out not to be true. This finding does not make us Tech bulls; we think the big-picture backdrop is sufficiently mixed to justify our US Equity Strategy and Global Asset Allocation services’ neutral recommendations. We simply wanted to call out the flaws in a popular notion before it becomes even more entrenched. Changes in interest rates do not solely effect equity prices via a denominator effect. They impact the numerator as well. The numerator impacts are multifaceted and vary based on which factor comes to the fore in a given instance. They are much harder to anticipate and therefore hold much more promise for investors who can suss them out in advance. The denominator effect is immediately apparent to any undergraduate who has been introduced to the time value of money and therefore isn’t likely to generate alpha. What’s more, as Tech stocks’ relative performance history illustrates, the relationship between equities and rates is not fixed. The rise of globalization and the Fed’s post-Volcker inflation vigilance ushered in a multi-decade disinflationary trend that ultimately culminated in rampant deflation fears following the global financial crisis. Now that concerns about stagflation have shunted aside concerns about secular stagnation, investors are much less likely to cheer rate backups while wringing their hands over rate declines. As Arthur Budaghyan, BCA’s Chief Emerging Markets strategist, has written, the about-face in market perceptions of interest rates could flip the correlations between equity prices and interest rates from positive (stocks advance as rising interest rates are perceived as evidence of economic improvement) to negative (stocks fall when rates rise and rise when rates fall). Our colleague Jonathan LaBerge, managing editor of the Bank Credit Analyst, has noted that extended valuations increase growth stocks’ vulnerability to rising interest rates. We do not disagree, but they do not have all that much to fear if the backup in Treasury yields is in line with our US Bond Strategy service’s year-end 2021 and 2022 targets of 1.75% and 2-2.25%, respectively. Tech’s outperformance may well have run its course – relative performance is extended, the law of large numbers makes it increasingly difficult to sustain historic growth rates, the legal and regulatory outlook is darkening and a shift from pandemic winners to pandemic losers may be in train – but rising rates alone are not a good basis for trimming Tech exposures. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Duration measures a bond’s sensitivity to a parallel shift in the yield curve, but we use the 10-year Treasury yield as a proxy for the entire curve in our simple regressions of asset class returns against price changes.

Who Likes A Flattening Yield Curve?

Who Likes A Flattening Yield Curve?

In a recent daily report, we analyzed relative performance of the S&P 500 sectors and styles under different US 10-year Treasury yield (UST10Y) regimes. Today we expand our analysis and map relative performance of the S&P 500 sectors and styles under the distinct US Treasury yield curve regimes, defined as a three-months change between 10-year and 2-year yields. To analyze sector and style performance by regime, we calculate contemporaneous three-months relative returns of sectors and styles. To summarize the results, we calculate median relative return of each sector/style in each regime. We subtract total period median to remove the sector and style biases in the long-term performance. In a flattening yield curve environment, Defensives, Quality, and Growth tend to outperform, as it indicates scarcity of growth. Accordingly, Real Estate, Technology, Utilities, and Communications Services also outperform. Yield curve steepening is usually associated with growth acceleration. This regime gives boost to more economically sensitive and capex intensive sectors and styles: Value, Small caps, and Cyclicals. Bottom Line: The shape of the US Treasury yield curve will be an important variable to monitor going forward, as it has a substantial effect on relative sector and style performance.

Foreword Today we are publishing a charts-only report focused on the S&P 500, and GICS 1 sectors. Many of the charts are self-explanatory; to some, we have added a short commentary. The charts cover macro, valuations, fundamentals, technicals, and the uses of cash. Our goal is to equip you with all the data you need to make investment decisions along these sector dimensions. We also include performance, valuations and earnings growth expectation tables for all styles, sectors, industry groups, and industries (GICS 1, 2 and 3). We hope you will find this publication useful. We alternate between Styles and Sector chart pack updates on a bi-monthly basis. Changes In Positioning Downgrade Growth to an equal weight and upgrade Value to an equal weight. Upgrade Small to an overweight and downgrade Large to an underweight. Downgrade Technology to equal weight by reducing overweight in Software and Services. We remain overweight Semiconductors and Equipment. We are on board with the ongoing market rotation: We were waiting for a decisive shift in rates and a dissipation of the Covid-19 scare as a signal to initiate this repositioning (Chart 1). Chart 1Performance Of S&P 500 Sectors And Styles

US Equity Chart Pack

US Equity Chart Pack

Overarching Investment Themes: Rotation Has Begun! Taper Tantrum 2.0: With tapering imminent and monetary tightening around the corner, both real yields and nominal yields are up sharply over the past couple of weeks (Chart 2A). Chart 2ARates Are Up Sharply

Rates Are Up Sharply

Rates Are Up Sharply

Chart 2BProbability Of Two Rate Hikes In 2022 Has Been Climbing

Probability Of Two Rate Hikes In 2022 Has Been Climbing

Probability Of Two Rate Hikes In 2022 Has Been Climbing

Market expects two rate hikes by the end of 2022: Although Chairman Powell has explicitly separated the decision to taper from the timing of the first rate hike, which he conditioned on full employment and which is “a long way off,” the market is still spooked by the timing and the speed of rate hikes. Currently, the probability of two rate hikes in 2022 stands at around 40%, rising sharply over the past two weeks (Chart 2B). The BCA house view is that the Fed will start hiking in December of 2022. Market rotation is on: Rising yields and a recent decline in Delta variant infections have triggered a fast and furious style and sector rotation. Higher rates put pressure on rate-sensitive sectors and styles, such as Growth, Technology, Communication Services, and Real Estate. While the “taper tantrum” pullback affects the entire US equity market, areas most geared to rising rates, such as Cyclicals, Financials, and Small Caps fare the best (Chart 3). An easing of the Delta scare has led to the “reopening” trade outperforming the ”work-from-home” trade. Chart 3Rotation Away From Rate-sensitive Sectors And Styles

US Equity Chart Pack

US Equity Chart Pack

Macro Economic slowdown is finally priced in: At long last, deteriorating economic data is fully digested by investors. The Citigroup Economic Surprise index is still in negative territory (Chart 4A) but has turned decisively. The markets move on the second derivative and a “less bad” economic surprise is a major positive for the markets. Chart 4ADeterioration Of Economic Data Is Finally Priced In

Deterioration Of Economic Data Is Finally Priced In

Deterioration Of Economic Data Is Finally Priced In

Chart 4BSupply Bottleneck Are Not Easing

Supply Bottleneck Are Not Easing

Supply Bottleneck Are Not Easing

Supply-chain disruptions are not abating: Shipping costs continue their ascent. The average delay of cargo ships traveling between the Far East and North America is 12 days – compare that to 1 day in January 2020.1 The ISM PMI Supplier Performance index increased from 69.5 in August to 73.4 indicating that supply bottlenecks are not easing (Chart 4B). There are also significant backlogs of goods (Chart 5A), and plenty of new orders. It will take time for supply chains to normalize, with most industry participants expecting the situation to improve only in 2022. Chart 5AManufacturers Are Overwhelmed

Manufacturers Are Overwhelmed

Manufacturers Are Overwhelmed

Chart 5BA Whiff Of Stagflation?

A Whiff Of Stagflation?

A Whiff Of Stagflation?

Labor shortages: Companies are still struggling to fill job openings. According to the US Census Survey, “pandemic layoff” or “caring for children” were the top reasons for not working. The number of people not working because of Covid-19 infections or fear of Covid spiked at the end of August.2 This explains the August jobs report. The ugly “S” word: With the ubiquitous shortage of input materials and labor, along with transportation delays, suppliers are simply unable to meet demand for goods, pushing prices higher. Stagflation may be rearing its ugly head: The Dallas Fed manufacturing index is showing a divergence, with prices moving higher while business activity is shifting lower. This is not the case with the ISM PMI index components, but investors need to be vigilant (Chart 5B). Americans are in a worse mood: Consumer confidence survey readings continue on a downward path. The combination of higher prices for everyday goods, the loss of purchasing power, the discontinuation of supplementary unemployment benefits, and paychecks not adjusted for inflation weigh on consumer sentiment. On the positive side, jobs are still plentiful. Valuation And Profitability Despite recent turbulence and rotations across sectors and styles, consensus is still expecting 15% YoY earnings growth over the next 12 months. However, QoQ growth rates look very different as we remove the base effect: Growth is expected to dip this coming quarter (Q3, 2021), and stay modest for most of 2022. This is a low bar that should be easy for companies to clear, although supply disruptions may dent corporate earnings. In the meantime, valuations remain elevated at 20.7 forward earnings (Chart 6). Chart 6Earnings Growth Expectations Are Modest

US Equity Chart Pack

US Equity Chart Pack

Sentiment There are still inflows into US equities, but they are easing. This can be explained by FOMO (fear of missing out), and lots of cash sitting on the sidelines that many retail investors aim to park in US equities. (Chart 7A). However, this is changing as rising rates render the TINA (“there is no alternative”) trade much less attractive. Chart 7AInflows Into US Equities Are Easing

Inflows Into US Equities Are Easing

Inflows Into US Equities Are Easing

Chart 7BCapex Is On The Rise

Capex Is On The Rise

Capex Is On The Rise

Uses Of Cash Capex: Capital goods orders are soaring, pointing to robust capex. The latest S&P estimates suggest that capex will rise 13% this year.3 This points to economic normalization, and attests to corporate confidence in economic growth. It is also a likely byproduct of shortages that plague the US supply chain – companies are expanding their capacity. (Chart 7B). Investment Implications Low for longer is over: The Fed has committed to tapering within the next 2-3 months. Unless this intention is derailed by another Covid scare or a significant deterioration in economic growth, we are now convinced that rates will move up to hit the BCA house view of 1.7%-1.9% by year-end. S&P 500: There is plenty of rotation under the hood; yet we expect US equities to hold their own into the balance of the year as, for now, monetary and fiscal policy remain easy, and earnings growth is likely to surprise on the upside. Severe and prolonged supply disruptions are a key risk to this view, as they chip away from economic growth, and cut into companies sales growth and profitability. Growth vs. Value: With rates rising into year-end, interest-rate sensitive stocks, such as Growth and the Technology sector, are under pressure. Since we opened overweight Growth and underweight Value position on June 14, Growth has outperformed S&P 500 by 4.1%, and Value underperformed by 4.5%. We do not want to overstay our welcome, and are neutralizing both sides of the trade, bringing positioning to an equal weight. Technology has beaten the S&P 500 by 2.2%, and we are shifting to an equal weight positioning by reducing overweight of the Software Industry Group. We remain overweight Semiconductors and Equipment. We are closing our overweight to Growth and underweight to Value allocation. We reduce overweight to Technology. Chart 7C

US Equity Chart Pack

US Equity Chart Pack

Cyclicals vs. Defensives: The onset of the Delta variant is dissipating, and we expect consumer cyclicals to rebound as more people are willing to travel and eat out. We also believe that the parts of the Industrials sector most exposed to restocking of inventories, infrastructure, and construction will perform strongly. Small vs. Large: We are upgrading Small from neutral to an overweight, and downgrade Large to an underweight. Small is highly geared to rising rates. It is also cheaper than Large, and most of the earnings downgrades are already in the price. We are now constructive on this asset class. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com S&P 500 Chart 8Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 9Profitability

Profitability

Profitability

Chart 10Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 11Uses Of Cash

Uses Of Cash

Uses Of Cash

Communication Services Chart 12Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 13Profitability

Profitability

Profitability

Chart 14Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 15Uses Of Cash

Uses Of Cash

Uses Of Cash

Consumer Discretionary Chart 16Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 17Profitability

Profitability

Profitability

Chart 18Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 19Uses Of Cash

Uses Of Cash

Uses Of Cash

Consumer Staples Chart 20Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 21Profitability

Profitability

Profitability

Chart 22Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 23Uses Of Cash

Uses Of Cash

Uses Of Cash

Energy Chart 24Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 25Profitability

Profitability

Profitability

Chart 26Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 27Uses Of Cash

Uses Of Cash

Uses Of Cash

Financials Chart 28Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 29Profitability

Profitability

Profitability

Chart 30Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 31Uses Of Cash

Uses Of Cash

Uses Of Cash

Health Care Chart 32Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 33Profitability

Profitability

Profitability

Chart 34Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 35Uses Of Cash

Uses Of Cash

Uses Of Cash

Industrials Chart 36Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 37Profitability

Profitability

Profitability

Chart 38Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 39Uses Of Cash

Uses Of Cash

Uses Of Cash

Information Technology Chart 40Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 41Profitability

Profitability

Profitability

Chart 42Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 43Uses Of Cash

Uses Of Cash

Uses Of Cash

Materials Chart 44Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 45Profitability

Profitability

Profitability

Chart 46Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 47Uses Of Cash

Uses Of Cash

Uses Of Cash

Real Estate Chart 48Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 49Profitability

Profitability

Profitability

Chart 50Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 51Uses Of Cash

Uses Of Cash

Uses Of Cash

Utilities Chart 52Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 53Profitability

Profitability

Profitability

Chart 54Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 55Uses Of Cash

Uses Of Cash

Uses Of Cash

Footnotes 1 Source: eeSea 2 US Census Household Pulse Survey, Employment Table 3. 3 S&P Global Market Intelligence, S&P Global Ratings; Universe is Global Capex 2000 Recommended Allocation

Chart 1Cyclicals Styels and Sectors Outperform In The Rising Rates Environment

Treasury Rates Vs. Sector And Style Performance

Treasury Rates Vs. Sector And Style Performance

In a recent daily report, we analyzed performance of the S&P 500 sectors before and after the 2013 tapering announcement. Today we expand our analysis and map relative performance of the S&P 500 sectors and styles under the different US 10-year Treasury yields (UST10Y) regimes, i.e., rates rising vs rates falling.1 As expected, deep cyclicals, such as Energy, Financials, and Industrials fare best in a rising rates environment, while Communication Services and Health Care outperform when rates head south (Chart 1, top panel). Styles’ performance across regimes is broadly consistent with the sector performance. Specifically, Small Caps, thanks to their high exposure to deep cyclicals, post the best performance when UST10Y is rising. Meanwhile, defensives are a mirror image of Small Caps and outperform once global growth starts softening (Chart 1, bottom panel). Finally, we bring one more dimension to our analysis and calculate the performance of the long-duration Technology and Health Care sectors, under different rates and yield curve regimes (Chart 2). To do so, we overlap rates and yield curve regimes and calculate median performance of each cell. Both Technology and Health Care underperform when rates are rising, and the yield curve is steepening: Long end of the curve is most important for discounting cash flows. Chart 2Performance of Technology and Health Care Sectors Is Also A Function Of Changes Of The Yield Curve

Treasury Rates Vs. Sector And Style Performance

Treasury Rates Vs. Sector And Style Performance

The current environment of rising rates and flattening yield curve is empirically a goldilocks scenario for these sectors as a flattening yield curve signifies that the long-term rate, which is more important for discounting future cash flows, is falling and the P/E contraction phase will be limited. It will also be offset by the growth in earnings as rising long rates indicate higher growth. Falling rates are also good for Tech stocks regardless of the direction of change in the yield curve. The Health Care sector behaves somewhat differently: It tends to underperform when rates are falling but the yield curve is steepening as such scenario is not dire enough for Defensives to outperform. Bottom Line: Cyclical sectors and high beta styles tend to outperform in a rising rates environment. At the same time, the performance of Technology and Health Care stocks is more nuanced: rising Treasury rates are not necessarily bad for these sectors if the yield curve is flattening. Footnotes 1 Methodology: We calculate three months change in UST10Y and calculate median of three months contemporaneous relative returns for each sector at each regime. To remove historical performance biases, we subtract sector median relative return for the whole period.

HighlightsSince 2008, US equity outperformance versus global ex-US stocks has not been driven by stronger top-line growth. Instead, it has been caused by a narrowly-based increase in profit margins, the accretive impact of share buybacks on the EPS of US growth stocks, and an outsized expansion in equity multiples. To a lesser extent, the dollar has also boosted common currency relative performance.There are significant secular risks to these sources of US equity outperformance over the past 14 years. Elevated tech sector profit margins are likely to lead to increased competition and higher odds of regulatory action, leveraging has reduced the ability of US companies to continue to accrete EPS through changes to capital structure, relative multiples are not justified by relative ROE, and the US dollar is expensive and is likely to fall over a multi-year horizon.In absolute terms, we forecast that US stocks will earn annualized nominal total returns of between 1.8 - 4.7% over the coming decade, assuming 4-5% annual revenue growth, flat profit margins, a constant 2% dividend yield, and a constant equity risk premium. Long-maturity bond yields are below their equilibrium levels and are likely to rise in real terms over time, which will weigh on elevated equity multiples.Over the coming 6-12 months, our view that US 10-Year Treasury yields are likely to rise argues for an underweight stance toward growth versus value stocks. In turn, this implies that US stocks will underperform global stocks, especially versus developed markets ex-US.The risks that we have highlighted to the sources of US outperformance suggest that US stocks may be flat versus their global peers over the long-term, arguing for a neutral strategic allocation. It also suggests that investors should be prepared to accept more volatility in order to reduce the gap between expected and desired returns, and should look towards riskier investments and asset classes (such as real estate and alternative investments) as potential portfolio return enhancements.Feature Chart II-1The US Has Massively Outperformed Other Equity Markets Since The Global Financial Crisis

The US Has Massively Outperformed Other Equity Markets Since The Global Financial Crisis

The US Has Massively Outperformed Other Equity Markets Since The Global Financial Crisis

The US equity market has vastly outperformed its peers since the 2008/2009 global financial crisis. Chart II-1 highlights that an investment in US stocks at the end of 2007 is now worth over 4 times the invested amount, versus approximately 1.6 times for global ex-US stocks (when measured in US dollar terms). The chart also shows that USD-denominated total returns have been roughly the same for developed markets ex-US as they have been for emerging markets, highlighting the exceptional nature of US equities.In this report we provide a deep examination of the sources of US equity performance, their likely sustainability, and what this implies for long-term investor return expectations. US stocks have not outperformed because of stronger top-line (i.e. revenue) growth, and instead have benefitted from a narrowly-based increase in profit margins, active changes to capital structure that have benefitted stockholders, an outsized expansion in equity multiples relative to global stocks, and a structural appreciation in the US dollar.We conclude that there are significant risks to all of these sources of outperformance, and that a neutral strategic allocation to US equities is now likely warranted. We also highlight that, while a strategic overweight stance is still warranted toward stocks versus bonds, investors should no longer count on US stocks to deliver returns that are in line with or above commonly-cited absolute return expectations. This argues for a greater tolerance of volatility, and the pursuit of riskier investments and asset classes (such as real estate and alternative investments) as potential portfolio return enhancements.A Deep Examination Of US Outperformance Since 2008Breaking down historical total return performance is the first step in judging whether US equities are likely to outperform their global ex-US peers on a structural basis. Below we deconstruct US and global total return performance over the past 14 years into six different components, and analyze the impact of some of these components on a sector-by-sector basis. The six components presented are:Total revenue growth for each equity market, in local currency termsThe change in profit marginsThe impact of changes in capital structure and index compositionThe change in the trailing P/E ratioThe income return from dividendsThe impact of changes in foreign exchangeThe sum of the first three factors explains the total growth in earnings per share over the period, and the addition of the fourth factor explains each market’s local currency price return. Income returns are added to explain total return over the period, with the sixth factor then explaining common currency total return performance. The FX effect for US stocks is zero by construction, given that we measure common currency performance in US$ terms. Chart II-2Strong US Returns Have Not Been Due To Strong Top Line Growth

October 2021

October 2021

Chart II-2 presents the annualized absolute impact of these factors for the MSCI US index since 2008. The chart highlights that U.S. stock prices have earned roughly 11% per year in total return terms over the past 14 years, with significant contributions from revenue growth, multiple expansion, margins, and the return from dividends.Interestingly, however, Chart II-3 highlights that US equities have not significantly outperformed on the basis of the first factor, total local currency revenue growth, at least relative to overall global ex-US stocks (see Box II-1 for more details). DM ex-US stocks have experienced very weak revenue growth since 2008, but this has been compensated for by outsized EM revenue growth. It is also notable that US revenue growth has actually underperformed US GDP growth over the period, dispelling the notion that US equity outperformance has been due to strong top-line effects.Chart II-3The US Has Outperformed Due To Margins, Capital Structure, Multiples, And The Dollar

October 2021

October 2021

Box II-1Proxying The Impact Of Changes In Shares OutstandingWe proxy the impact of changes in shares outstanding (and thus the impact of equity dilution / accretion) by dividing each index’s market capitalization by its stock price. This measure is not a perfect proxy, as changes in index composition (such as the addition/deletion of index constituents) will change the index’s market capitalization but not its stock price. We also calculate total revenue for each market by multiplying local currency sales per share by the market cap / stock price ratio, meaning that the total revenue growth figures shown in Chart II-3 should best be viewed as estimates that in some cases reflect index composition effects.However, Chart II-B1 highlights that adjusting the market cap / stock price ratio for the number of firms in the index does not meaningfully change our overall conclusions. This approach would imply a larger dilution effect for DM ex-US than suggested in Chart II-3, and a smaller effect for emerging markets (due to a significant rise in the number of EM index constituents since 2008). In addition, global ex-US revenue growth is modestly lower than US revenue growth when using this approach. But this gap would account for a fraction of US equity outperformance over the period, underscoring that the US has massively outperformed global ex-US stocks due to margin, capital structure, and multiple expansion effects. Chart II-B1The US Has Not Meaningfully Outperformed Due To Revenue Growth, No Matter How You Slice It

October 2021

October 2021

Chart II-3 also highlights that global ex-US stocks have modestly outperformed the US in terms of the fifth factor, the income return from dividends. This has almost offset the negative FX return (the sixth factor) from a net rise in the US dollar over the period.What is clear from the chart is that the second, third, and fourth factors explain almost all of the difference in total return between US and global ex-US stocks since 2008. The US experienced a significant increase in profit margins versus a modest contraction for global ex-US, a modest fillip from changes in capital structure and index composition versus a substantial drag for ex-US stocks, and a sizable rise in equity multiples that has outpaced what has occurred around the globe in response to structurally lower interest rates. Chart II-4US Margin Outperformance Has Been Narrowly-Based

October 2021

October 2021

The significant rise in aggregate US profit margins over the past 14 years has often been attributed to the strong competitiveness of US companies, but Chart II-4 highlights that the aggregate change mostly reflects a narrow sector composition effect. The chart shows the change in US and global ex-US profit margins by level 1 GICS sector since 2008, and underscores that overall profit margins outside of the US have fallen mostly due to lower oil prices. Conversely, in the US, profit margins have substantially risen in only three out of ten sectors: health care, information technology, and communication services.Chart II-5 highlights that global ex-US equity multiples have risen in a majority of sectors since 2008, but not by the same magnitude as what has occurred in the US. De-rating in the resource sector partially explains the gap, but stronger US multiple expansion in the heavily-weighted consumer discretionary, information technology, and communication services sectors appears to explain most of the gap in multiple expansion.Chart II-5Multiples Have Risen Globally, But More So For Broadly-Defined US Tech Stocks

October 2021

October 2021

Finally, Charts II-6 & II-7 highlights that there has been a strong growth versus value dimension to the impact of changes in capital structure and index composition on regional equity performance. The charts show that equity dilution and other changes to index composition have caused a similar drag on the returns from value stocks in the US and outside the US. However, the charts also highlight that the more important effect has been the accretive impact of share buybacks on the EPS of US growth stocks, which has not been matched by growth stocks outside of the US. As noted in Box II-1, part of this gap may be explained by an increase in the number of companies included in the MSCI Emerging Markets index, but Chart II-8 highlights that the global ex-US ratio of market capitalization to stock price has still risen significantly over the past 14 years, in contrast to that of the US even after controlling for the number of index components. Chart II-6There Has Been A Strong Style Dimension…

There Has Been A Strong Style Dimension...

There Has Been A Strong Style Dimension...

Chart II-7…To The Impact Of Changes In Capital Structure And Index Composition

...To The Impact Of Changes In Capital Structure And Index Composition

...To The Impact Of Changes In Capital Structure And Index Composition

Chart II-8The Accretive Impact Of US Growth Stock Buybacks Has Not Been Matched Globally

The Accretive Impact Of US Growth Stock Buybacks Has Not Been Matched Globally

The Accretive Impact Of US Growth Stock Buybacks Has Not Been Matched Globally

The bottom line for investors is that there have been multiple factors contributing to US equity outperformance since 2008, but aggregate top-line growth has not been one of them. Broadly-defined technology companies (including media & entertainment and internet retail firms) have been responsible for nearly all of the relative rise in profit margins and most of the relative expansion in multiples over the past 14 years, and US growth stocks have benefitted from the accretive impact of share buybacks to a larger degree than what has occurred globally.The Relative Secular Return Outlook For US StocksWe present below several structural risks to the continued outperformance of US equities for the factors that have been most responsible for this performance over the past 14 years. In some cases, these risks speak to the potential for US outperformance to end, not necessarily that the US will underperform. But even the cessation of US outperformance along one or more of these factors would be significant, as it would imply a potential inflection point in the most consequential trend in regional equity performance since the 2008/2009 global financial crisis.Profit MarginsChart II-9 presents the 12-month trailing combined profit margin for the US consumer discretionary, information technology, and communication services sector versus that of the remaining sectors. The chart underscores the points made by Chart II-4 in time series form, namely that the net increase in overall US profit margins since 2008 has been narrowly based. Chart II-9The US Profit Margin Expansion Has Been Driven By Broadly-Defined Tech Stocks

The US Profit Margin Expansion Has Been Driven By Broadly-Defined Tech Stocks

The US Profit Margin Expansion Has Been Driven By Broadly-Defined Tech Stocks

Over a 6-12 month time horizon, the clear risk to US profit margins is an end to the COVID-19 pandemic. The profitability of broadly-defined tech stocks has surged during the pandemic, in response to a significant shift toward online goods purchases and elevated spending on tech equipment. A durable end to the pandemic is likely to reverse some of these spending patterns, which will likely weigh on margins for broadly-defined tech stocks. Chart II-10The Regulatory Risks Facing Big Tech Are Real

October 2021

October 2021

Over the longer term, the risk is that extremely elevated profit margins are likely to increase the odds of regulatory action from Washington and invite competition. On the former point, our US Political Strategy service has highlighted that a bipartisan consensus in public opinion holds that Big Tech needs tougher regulation (Chart II-10), and this consensus grew substantially over the controversial 2020 political cycle.1 This regulatory pressure is currently best described as a “slow boil,” as not all surveys show strong majorities in favor of regulation, and Republicans and Democrats disagree on the aims of regulation.But the bottom line is that Big Tech is likely to remain in the hot seat after the various controversies of the pandemic and 2016-2020 elections, just as big banks faced tougher regulation in the wake of the subprime mortgage crisis. This underscores that a “slow boil” may turn into a faster one at some point over the secular horizon, which would very likely weigh on profit margins. Elevated tech sector profit margins makes regulatory action more likely because policymakers will perceive a stronger ability for these firms to weather a “regulatory shock.”On the latter point about competition, it is true that broadly-defined tech stocks follow a “platform” business model that will be difficult to supplant. These companies benefit from powerful network effects that have taken years to accrue, suggesting that they will not be rapidly replaced by competitors.Still, the experience of Microsoft in the years following its meteoric rise in the second half of the 1990s provides a cautionary tale for broadly-defined tech stocks today. In the late-1990s, it was difficult for investors to envision how Microsoft’s near-total product dominance of the PC ecosystem could ever be displaced, but it eventually lost market share due to the rise of mobile devices and their competing operating systems.In addition, Microsoft’s fundamental performance suffered even before the rise of the modern-day smartphone & mobile device market. Chart II-11 highlights the annualized components of Microsoft’s price return from 1999-2007 versus the late-1990s period, which underscores that changes in margins, changes in multiples, and stock price returns may be persistently negative in a scenario in which revenue growth slows (even if revenue growth itself remains positive).Chart II-11Microsoft Offers A Cautionary Tale For Dominant Business Models

October 2021

October 2021

Some of the reversal of Microsoft’s fortunes during this period were self-inflicted, and the firm also suffered from an economy-wide slowdown in tech equipment spending as a result of the 2001 recession that persisted into the early years of the subsequent recovery. But the key point for investors is that company and sector dominance may wane, and the fact that broadly-defined tech sector profit margins are extremely elevated raises the risk that further increases may not materialize.Capital Structure And Index CompositionAs noted above, the beneficial impact from changes in capital structure and index composition for US equities has occurred due to the accretive impact of share buybacks on the EPS of US growth stocks, which has not been matched by growth stocks outside of the US.In our view, this accretive impact has occurred for two reasons. First, US growth stocks have taken advantage of historically low interest rates and leverage to shift their capital structure to be more debt-focused over the past 14 years. Second, this shift has been aided by the fact that US growth stocks have experienced stronger cash flows than their global peers, which have been used to service higher debt payments.However, Charts II-12 and II-13 suggest that this process may be in its late innings. Chart II-12 highlights that the US nonfinancial corporate sector debt service ratio (DSR) did indeed fall below that of the euro area following the global financial crisis, but that this reversed in 2016. At the onset of the pandemic, the US nonfinancial corporate sector DSR was rising sharply, and was approaching its early-2000 highs. During the pandemic, the corporate sector DSR has continued to rise in both regions, but this almost exclusively reflects a (temporary) decline in operating income, not a surge in corporate sector debt or a rise in interest rates.Not all of the pre-pandemic rise in the US corporate sector DSR was concentrated in broadly-defined tech stocks, but some of it likely was. The key point for investors is that the US nonfinancial corporate sector had a lower capacity to leverage itself relative to companies in the euro area at the onset of the pandemic, which implies a less accretive impact on relative earnings per share in the future. Chart II-13 reinforces this point by highlighting that the uptrend in relative cash flow for US growth stocks, versus global ex-US, appears to have ended in 2015. The uptrend has continued in per share terms, but this appears to be flattered by the impact of buybacks itself. Chart II-12Can The US Continue To Accrete EPS Through Stock Buybacks?

Can The US Continue To Accrete EPS Through Stock Buybacks?

Can The US Continue To Accrete EPS Through Stock Buybacks?

Chart II-13US Growth Companies Are No Longer Generating More Cash Than Their Global Peers

US Growth Companies Are No Longer Generating More Cash Than Their Global Peers

US Growth Companies Are No Longer Generating More Cash Than Their Global Peers

Admittedly, we see no basis to conclude that the persistent earnings dilution that has occurred in emerging markets over the past 14 years will end, or even slow, over the secular horizon. This underscores that emerging markets will need to generate stronger revenue growth to prevent the dilution effect from acting as a continued drag on EM vs. US equity performance, and it is an open question as to whether this will occur. Thus, for now, we have more conviction in the view that capital structure and index composition changes may contribute less to US equity outperformance versus developed markets ex-US over the coming several years.Equity MultiplesThere are three arguments against the idea that US equity multiples will continue to expand relative to those of global ex-US stocks. First, Chart II-14 highlights a point that we have made in previous Bank Credit Analyst reports, which is that aggressive multiple expansion in the US has now rendered US stocks to be the most dependent on low long-maturity bond yields than at any point since the global financial crisis. Chart II-14US Stocks Are The Most Dependent On Low Bond Yields In Over A Decade

US Stocks Are The Most Dependent On Low Bond Yields In Over A Decade

US Stocks Are The Most Dependent On Low Bond Yields In Over A Decade

Over the coming 6- to 12-months, we strongly doubt that US 10-year Treasury yields will rise outside of the range that would be consistent with the US equity risk premium from 2002 to 2007 (discussed in further detail in the next section). But the chart also shows that this range is now clearly below trend nominal GDP growth, suggesting that higher interest rates on a structural basis may cause outright multiple contraction for US stocks. This is particularly true for growth stocks, which have been responsible for a significant portion of US equity outperformance, given their comparatively long earnings duration. Chart II-15US Multiples Are Not Justified By Higher Return On Equity

US Multiples Are Not Justified By Higher Return On Equity

US Multiples Are Not Justified By Higher Return On Equity

Second, it has been often argued by some investors that a premium is warranted for US stocks given their comparatively high return on equity, but Chart II-15 highlights that this is not the case. The chart shows the relative price-to-book ratio for the US versus global and developed markets ex-US compared with regression-based predicted values based on relative return on equity. The chart clearly highlights that the US price-to-book ratio is meaningfully higher than it should be relative to global stocks, especially when compared to other developed markets. Versus DM ex-US, the only comparable period that saw a relative P/B – relative ROE deviation of this magnitude occurred in the late-1980s, when US stocks were meaningfully less expensive than relative ROE would have suggested. This relationship completely normalized in the years that followed, which would imply a substantial relative multiple contraction for US stocks over the coming several years were the gap shown in Chart II-15 to close.Third, Chart II-16 presents the share of US stock market capitalization accounted for by the largest 10% of stocks by size. The chart highlights that the concentration of US market capitalization has risen to an extreme level that has only been reached in two other cases over the past century. Historically, prior stock market concentration has been associated with future increases in the equity risk premium, underscoring that broadly-defined US tech sector concentration bodes poorly for future returns. Chart II-16The US Stock Market Is Now Extremely Concentrated

The US Stock Market Is Now Extremely Concentrated

The US Stock Market Is Now Extremely Concentrated

The Foreign Exchange EffectAs a final point, Chart II-17 illustrates the degree to which US relative performance has meaningfully benefitted from a rise in the US dollar since 2008. The chart highlights that an equity market-weighted dollar index has risen 20% from its late-2007 level, which has boosted US common currency relative performance.The US dollar was arguably modestly undervalued just prior to the 2008/2009 global financial crisis, but Chart II-18 highlights that it is now meaningfully overvalued versus other major currencies. Over a multi-year horizon, this argues against further relative common currency gains for US stocks from the foreign exchange effect. Chart II-17The US Dollar Has Helped US Common Currency Performance...

The US Dollar Has Helped US Common Currency Performance...

The US Dollar Has Helped US Common Currency Performance...

Chart II-18…And Is Now Expensive

October 2021

October 2021

The Absolute Secular Return Outlook For US StocksOver a secular horizon, the most common method for forecasting equity returns is to predict whether earnings are likely to grow faster or slower than nominal potential GDP growth, and whether equity multiples are likely to rise or fall.For the reasons described above, we have no plausible basis on which to forecast that US profit margins are inclined to rise further over time given how extended they have become. This suggests that a reasonable long-term earnings forecast should be closely linked to one’s forecast for revenue growth. Chart II-19S&P 500 Revenue Is Low Relative To US GDP, And May Rise Over The Next Decade

S&P 500 Revenue Is Low Relative To US GDP, And May Rise Over The Next Decade

S&P 500 Revenue Is Low Relative To US GDP, And May Rise Over The Next Decade

Chart II-19 presents S&P 500 revenue as a percent of nominal GDP, and underscores a fact that we noted above: revenue growth for US equities has underperformed US GDP since the global financial crisis. This undoubtedly has been linked to the fallout from the crisis and other exogenous shocks like the massive decline in energy prices in 2014/2015, which are unlikely to be repeated. Over the next ten years, the US Congressional Budget Office is forecasting nominal potential growth of roughly 4%; allowing for a potential rise in US equity revenue to GDP suggests that investors should expect earnings growth on the order of 4-5% per year over the coming decade, if extremely elevated profit margins are sustained. Chart II-20Multiples Seem To Predict Future Returns Well…

October 2021

October 2021

Unfortunately for equity investors, there are slim odds that US equity multiples will continue to rise or even stay at their current level. Equity valuation has been shown to have nearly zero ability to predict stock returns over a 6-12 month time horizon or even over the following 3-5 years, but 10-year regressions relating current valuations on future 10-year compound returns tend to be highly predictive (Chart II-20). Utilizing this approach, today’s 12-month forward P/E ratio would imply a 10-year future total return of just 2.9% (Chart II-21). That, in turn, would imply a annual drag of 3-4% from multiple contraction over the coming decade, given our 4-5% earnings growth forecast and a historically average dividend yield of roughly 2%.One problem with the method shown in Charts II-20 and II-21 is the fact that the relationship between today’s P/E ratio and 10-year future returns captures more than the impact of potentially mean-reverting multiples. It also includes any correlation between the starting point of valuation and subsequent earnings growth, which is likely to be spurious. This effect turns out to be important: we can see in Chart II-21 that the strong fit of the relationship is influenced by the fact that the global financial crisis occurred roughly 10-years after the equity market bubble of the late-1990s. Chart II-21...But That Depends Heavily On The Tech Bubble / GFC Relationship

...But That Depends Heavily On The Tech Bubble / GFC Relationship

...But That Depends Heavily On The Tech Bubble / GFC Relationship

Astute investors may infer a legitimate causal link between these two events, via too-easy monetary policy. But from the perspective of forecasting, predicting future returns based on prevailing equity multiples confusingly mixes together three effects: the relative timing of business cycles, the impact of changes in interest rates, and the potential mean-reverting nature of the equity risk premium.In order to disentangle these effects for the purposes of forecasting, we present a long-history estimate of the US equity risk premium based on Robert Shiller’s Irrational Exuberance dataset (Chart II-22). We define the equity risk premium as earnings per share (as reported) as a percent of the S&P 500, minus the real long-maturity interest rate. We calculate the real rate by subtracting the BCA adaptive inflation expectations model – essentially an exponentially smoothed version of actual inflation – from the nominal long-term bond yield. Chart II-22The US ERP Seems Normal Based On A Very Long Term History...

The US ERP Seems Normal Based On A Very Long Term History...

The US ERP Seems Normal Based On A Very Long Term History...

The chart highlights that this estimate of the ERP is currently exactly in line with its median value since 1872. Chart II-23 presents essentially the same conclusion, based on data since 1979, using the forward operating P/E ratio for the S&P 500 and the same definition for real bond yields.This implies that, if interest rates were at equilibrium levels, investors would have a reasonable basis to conclude that equity multiples would be unchanged over a secular investment horizon. However, as we have highlighted several times in previous reports, long-maturity government bond yields are likely well below equilibrium levels. Chart II-24 highlights that long-maturity US government bond yields have not been this low relative to trend growth since the late-1970s. Chart II-23...And Based On The Forward Earnings Yield Over The Past Four Decades

...And Based On The Forward Earnings Yield Over The Past Four Decades

...And Based On The Forward Earnings Yield Over The Past Four Decades

Chart II-24Interest Rates Are Well Below Equilibrium, And Are Likely To Rise Over Time

Interest Rates Are Well Below Equilibrium, And Are Likely To Rise Over Time

Interest Rates Are Well Below Equilibrium, And Are Likely To Rise Over Time

We presented in an April report why a gap between interest rates and trend rates of growth was indeed justified for a few years following the global financial crisis, but that a decline in the equilibrium real rate of interest (“r-star”) only appeared to be permanent due to persistent, non-monetary policy shocks to aggregate demand that occurred over the course of the last economic cycle.2In a scenario where the US output gap turns positive, inflation rises modestly above target, and where permanent damage to the labor market from the pandemic is relatively limited over the coming 6-18 months, it seems reasonable to conclude that the narrative of secular stagnation may ultimately be challenged and that investor expectations for the neutral rate may converge toward trend rates of economic growth. This would weigh on equity multiples, and thus lower equity total returns from the 6-7% implied by our earnings forecast and income return assumption. Chart II-25US Stocks Are Likely To Earn Annual Total Returns Between 1.8-4.7% Over The Next Decade

October 2021

October 2021

Were real long-maturity bond yields to rise by 100-200bps over the coming decade, this would imply annualized total returns of between 1.8 - 4.7% from US stocks, assuming 4-5% annual revenue growth, flat profit margins, a constant 2% dividend yield, and a constant ERP (Chart II-25). While this would beat the returns offered by bonds, implying that investors should still be structurally overweight equities versus fixed-income assets, it would also fall meaningfully short of the average pension fund return objective (Chart II-26), as well as the absolute return goals of many investors. Chart II-26Future Returns From US Stocks Will Greatly Disappoint Investors

Future Returns From US Stocks Will Greatly Disappoint Investors

Future Returns From US Stocks Will Greatly Disappoint Investors

Investment Conclusions Chart II-27Over The Coming Year, Favor Value And Global Ex-US Stocks

Over The Coming Year, Favor Value And Global Ex-US Stocks

Over The Coming Year, Favor Value And Global Ex-US Stocks

Over the coming 6-12 months, our view that 10-year US Treasury yields are likely to rise supports an overweight stance toward value versus growth stocks. Chart II-27 highlights that the underperformance of growth argues for an underweight stance toward US stocks within a global equity portfolio, especially versus developed markets ex-US.Over a longer-term horizon, there are two key investment implications from our research. First, the risks that we have highlighted to the sources of US outperformance over the past 14 years suggests that investors should not bank on a continuation of this trend over the next decade. We have not made the case in this report for the outperformance of global ex-US stocks, merely that the continued outperformance of US stocks now rests on an unreliable foundation. This may suggest that US relative performance will be flat over the structural horizon, arguing for a neutral strategic allocation. But even the cessation of US outperformance would be a significant development, as it would end the most consequential trend in regional equity performance in the post-GFC era.Second, investors should expect meaningfully lower absolute returns from US stocks over the next decade than what they have earned since 2008/2009, barring a continued rise in the already stretched profit margins of broadly-defined tech stocks. A structurally overweight stance is still warranted toward equities versus fixed-income, but even a 100% equity allocation is unlikely to meet investor return expectations in the high single-digits. As a consequence, global investors should be prepared to accept more volatility in order to reduce the gap between expected and desired returns, and should look towards riskier investments and asset classes (such as real estate and alternative investments) as potential portfolio return enhancements.Jonathan LaBerge, CFAVice PresidentThe Bank Credit AnalystFootnotes1 Please see US Political Strategy "Forget Biden's Budget," dated June 2, 2021, available at usps.bcaresearch.com2 Please see The Bank Credit Analyst “R-star, And The Structural Risk To Stocks,” dated March 31, 2021, available at bca.bcaresearch.com

Highlights The global fight against the Delta variant of COVID-19 continued to show progress in the month of September, but not without cost. Growth in services activity slowed meaningfully, which has likely delayed the return to potential output in the US until March of next year (at the earliest). However, even with this revised timeline, maximum employment remains a very possible outcome by next summer, barring a further extension of the pandemic in advanced economies. In this regard, the Fed’s likely decision at its next meeting to taper the rate of its asset purchases makes sense and is consistent with a first rate hike in the second half of 2022. The rise in long-maturity bond yields following this month’s Fed meeting is consistent with the view that 10-year Treasurys are overvalued and that yields will trend higher over the coming year. Fixed-income investors should stay short duration. The degree to which global shipping costs are being driven by the forces of supply versus demand will affect the Fed's criteria for liftoff next year, via changes in goods prices as well as consumer expectations for inflation. In our view, a detailed examination of shipping prices over the past 18 months points to a future pace of inflation that is not dangerously above-target, but does meet the Fed’s liftoff criteria. A mix-shift in consumer spending, away from goods and toward services, is not a threat to economic activity or S&P 500 earnings – so long as the decline in the former is not outsized relative to the rise in the latter. It will, however, disproportionately impact China, and could be the trigger for meaningful further easing by Chinese policymakers. In the interim, a catalyst for EM stocks may remain elusive. We continue to recommend an overweight stance toward value versus growth stocks and global ex-US versus the US, particularly in favor of developed markets ex-US. Investors should remain cyclically overweight stocks versus bonds, although it is possible that both assets will post negative returns for a short period at some point over the coming 12 months in response to higher long-maturity bond yields. Still, we expect both stock prices and the stock-to-bond ratio to be higher a year from today. Feature The global fight against the Delta variant of COVID-19 continued to show progress in the month of September. Chart I-1 highlights that an estimate of the reproduction rate of the disease in developed economies has fallen below one, and the weekly change in hospitalizations in both the US and UK – the two countries at the epicenter of the Delta wave that have not reintroduced widespread COVID-19 control measures – have fallen back into negative territory. In addition, we estimate that approximately 6% of the world’s population received vaccines against COVID-19 in September, with now 45% of the globe having received a first dose and 33% now fully vaccinated. Pfizer’s announcement last week that it has found a “favorable safety profile and robust neutralizing antibody responses” from its vaccine trial in children five to eleven years of age suggests that the FDA may grant emergency use authorization within weeks, which would likely raise the vaccination rate in the US (and ultimately other advanced economies) by at least 5 percentage points in fairly short order. This would also further reduce the impact of school/classroom closures on the labor market, via both an increased participation rate and increased hiring in the education sector. This fight, however, has not been without cost. US jobs growth slowed significantly in August, manufacturing and services PMIs continued to slow in September, and, as Chart I-2 highlights, the normalization in transportation use that was well underway in the first half of the year has clearly inflected in both the US and UK in response to the spread of Delta. Consensus market expectations for Q3 growth have been cut in the US, and to a lesser extent in the euro area, and the Fed reduced its forecast for 2021 real GDP growth from 7% to 5.9% following the September FOMC meeting. Chart I-1The Delta Wave Continues To Abate...

The Delta Wave Continues To Abate...

The Delta Wave Continues To Abate...

Chart I-2...But At A Cost To Economic Activity

...But At A Cost To Economic Activity

...But At A Cost To Economic Activity

The Path Toward Eventually Tighter Monetary Policy It has been surprising to some investors that the Fed has moved forward with their plans to taper the rate of its asset purchases against this backdrop of slowing near-term growth – an event that now seems likely to occur at its next meeting barring a disastrous September payroll report. In our view, this is not especially surprising, given that the Fed has expressed a desire for net purchases to reach zero before they raise interest rates for the first time. Chair Powell noted during last week’s press conference that FOMC participants felt a “gradual tapering process that concludes around the middle of next year is likely to be appropriate”, underscoring that the Fed wants the flexibility to raise interest rates in the second half of next year. The timing of the first Fed rate hike is entirely subject to the evolution of the economic data over the next year, and is not, in any way, calendar-based. But we presented in last month's Special Report why the Fed’s maximum employment criteria may be met as early as next summer,1 and the Fed’s projections for the pace of tapering are consistent with our analysis. Chart I-3Maximum Employment Remains A Very Possible Outcome By Next Summer

Maximum Employment Remains A Very Possible Outcome By Next Summer

Maximum Employment Remains A Very Possible Outcome By Next Summer

The Fed’s most recent Summary of Economic Projections (“SEP”) also seemingly confirmed Fed Vice Chair Richard Clarida’s view that a 3.8% unemployment rate is consistent with maximum employment, barring any issues with the “breadth and inclusivity” of the labor market recovery. We noted in last month’s report that these issues are unlikely in a scenario where jobs growth is sufficiently high to bring down the unemployment rate below 4%. Chart I-3 highlights that both the Fed’s forecast and Bloomberg consensus expectations imply a closed output gap by March, even after factoring in the near-term impact of the Delta variant. Consequently, maximum employment remains a very possible outcome by next summer, barring a further extension of the pandemic in advanced economies. Long-maturity bond yields rose following the Fed meeting, which is also not especially surprising given how low yields have fallen relative to the fair value implied by the Fed’s SEP forecasts even assuming a December 2022 initial rate hike. Chart I-4 highlights that the fair value of the 10-year Treasury yield today is roughly 2% using this approach, rising to 2.15% by next summer. Ironically, the September SEP update modestly lowered the fair value shown in Chart I-4 relative to what would otherwise have been the case, as it implied that the Fed is expecting to raise interest rates at a pace of approximately three hikes per year – rather than the four that prevailed prior to the pandemic. Investors should also note that the fair value for the 10-year yield is nontrivially lower based on market participant and primary dealer estimates of the terminal Fed funds rate (also shown in Chart I-4), although they still imply that long-maturity yields should trend higher over the coming year. Global Trade, Inflation, And The Fed A return to maximum employment will likely signal the onset of monetary policy tightening, as long as the Fed's inflation criteria for liftoff have been met. For now, inflation is signaling a green light for hikes next year, even after excluding the prices of COVID-impacted services and cars (Chart I-5). In fact, more recently, CPI ex-direct COVID effects has been pointing in the “non-transitory” direction, which continues to prompt questions from investors about whether the Fed will be forced to hike earlier than it currently expects for reasons other than a return to maximum employment. Chart I-4US Long-Maturity Bond Yields Are Set To Move Higher Over The Coming Year

US Long-Maturity Bond Yields Are Set To Move Higher Over The Coming Year

US Long-Maturity Bond Yields Are Set To Move Higher Over The Coming Year

Chart I-5For Now, Inflation Is Signaling A Green Light For Hikes Next Year

For Now, Inflation Is Signaling A Green Light For Hikes Next Year

For Now, Inflation Is Signaling A Green Light For Hikes Next Year

At least some portion of the current pace of increase in consumer goods prices is tied to surging import costs, which have run well in-excess of what would be predicted by the relationship with the US dollar (Chart I-6). This, in turn, is being driven by an explosion in shipping costs that has occurred since the onset of the pandemic, which is being driven both by demand and supply-side factors (Chart I-7). Chart I-6US CPI Is Being Affected By Surging Import Prices...

US CPI Is Being Affected By Surging Import Prices...

US CPI Is Being Affected By Surging Import Prices...

Chart I-7...Which Are Being Driven By An Explosion In Shipping Costs

...Which Are Being Driven By An Explosion In Shipping Costs

...Which Are Being Driven By An Explosion In Shipping Costs

The degree to which global shipping costs are being driven by the forces of supply versus demand will affect the Fed's criteria for liftoff next year, via changes in goods prices as well as consumer expectations for inflation. To the extent that demand side factors are mostly responsible, investors should have higher confidence that the recent surge in consumer prices is transitory, because a shift away from above-trend goods spending and toward below-trend services spending is likely over the coming year. If supply-side factors are mostly responsible, then it is conceivable that the global supply chain impact on consumer goods prices will persist for longer than would otherwise be the case, potentially raising the odds of a larger or more sustained rise in inflation expectations. In our view, a detailed examination of shipping prices over the past 18 months points to a mix of both demand and supply effects, even since the beginning of 2021. However, as we highlight below, several facts point toward the view that supply-side factors will be the dominant driver over the coming year, and that they are more likely to exert a disinflationary/deflationary rather than inflationary effect: Chart I-8 breaks down the cumulative change in the overall Freightos Baltic Index by route since December 2019. The chart makes it clear that shipping costs from China/East Asia to the West Coast of the US have risen far more than any other route, underscoring that US demand for goods has been an important part of the rise in shipping costs. Chart I-8US Demand For Goods Is An Important Part Of The Shipping Cost Story

October 2021

October 2021

Chart I-9US Goods Spending Has Clearly Been Boosted By US Fiscal Policy

US Goods Spending Has Clearly Been Boosted By US Fiscal Policy

US Goods Spending Has Clearly Been Boosted By US Fiscal Policy

Chart I-9 shows the level of real US personal consumption expenditures on goods relative to its pre-pandemic trendline, underscoring both that goods spending is currently well-above trend, and that there have been two distinct phases of rising goods spending: from May to October 2020 following the passage of the CARES act, and from January to March 2021 following the December 2020 extension of UI benefits and in anticipation of the passage of the American Rescue Plan. Since March, US real goods spending has trended lower, a pattern that we expect will continue over the coming year. Chart I-10 highlights that while the global supply chain struggled heavily last year in response to surging demand and the lagging effects of labor shortages and factory shutdowns during the earliest phase of the pandemic, there were some signs of supply-side normalization in the first half of 2021. The chart highlights that the number of ships at anchor at the Los Angeles and Long Beach ports declined meaningfully from February to June, and global shipping schedule reliability tentatively improved in March. The chart also shows that shipping costs from China/East Asia to the West Coast of the US continued to rise in Q2 seemingly as a lagged response to the Jan-Mar rise in goods spending, but they were still low at the end of June compared to today’s levels. Chart I-10Supply-Side Factors Seem To Have Driven A Majority Of This Year's Increase In Shipping Costs

Supply-Side Factors Seem To Have Driven A Majority Of This Year's Increase In Shipping Costs

Supply-Side Factors Seem To Have Driven A Majority Of This Year's Increase In Shipping Costs