Technology

Highlights Taiwan’s semiconductor sector is facing both cyclical and structural headwinds. Semiconductor exports will continue to contract over the next six months or so, on retrenching global demand. In the long run, Taiwan is facing increasing competition from Korea in the high-end supply, and from mainland China in the medium- to low-end supply of the semiconductor market. The latest rebound in Taiwanese share prices is unsustainable, and they are about to relapse anew. Within an EM equity portfolio, we recommend staying neutral on Taiwanese stocks for now. Feature Taiwan’s exports and manufacturing are in full-blown recession. The equity market has rebounded after a major selloff last year. However, the overall manufacturing PMI and its export sub-component are extremely weak, and do not justify the latest share-price rebound (Chart I-1). Chart I-1Taiwanese Equities: Unsustainable Rally

Taiwanese Equities: Unsustainable Rally

Taiwanese Equities: Unsustainable Rally

Are manufacturing activity and exports about to recover? Or will the stock market rally fade? Our answer is the latter. There are currently no signs suggesting a recovery in exports is imminent. Moreover, the engine of the economy – the semiconductor sector – is facing both cyclical and structural headwinds. We remain negative on Taiwanese stocks in absolute terms. Within an EM equity portfolio, we recommend a market-weight allocation to Taiwanese stocks for now. Importance Of Semiconductors Over the past 15 years, the semiconductor sector has become the cornerstone of the Taiwanese economy. The Taiwanese economy is highly dependent on its external sector, as exports contribute to nearly 70% of GDP. As such, Taiwan’s business cycle has often been closely associated with its export sector. This means the region’s growth outlook relies on both external demand (a cyclical factor) and the competitiveness of its export sector (more of a structural factor). Over the past 15 years, the semiconductor sector has become the cornerstone of the Taiwanese economy. It contributes to over one-third of the region’s total exports, up from 22% in 2009 (Chart I-2). Chart I-2Semiconductor: Cornerstone Of Taiwanese Economy

Semiconductor: Cornerstone of Taiwanese Economy

Semiconductor: Cornerstone of Taiwanese Economy

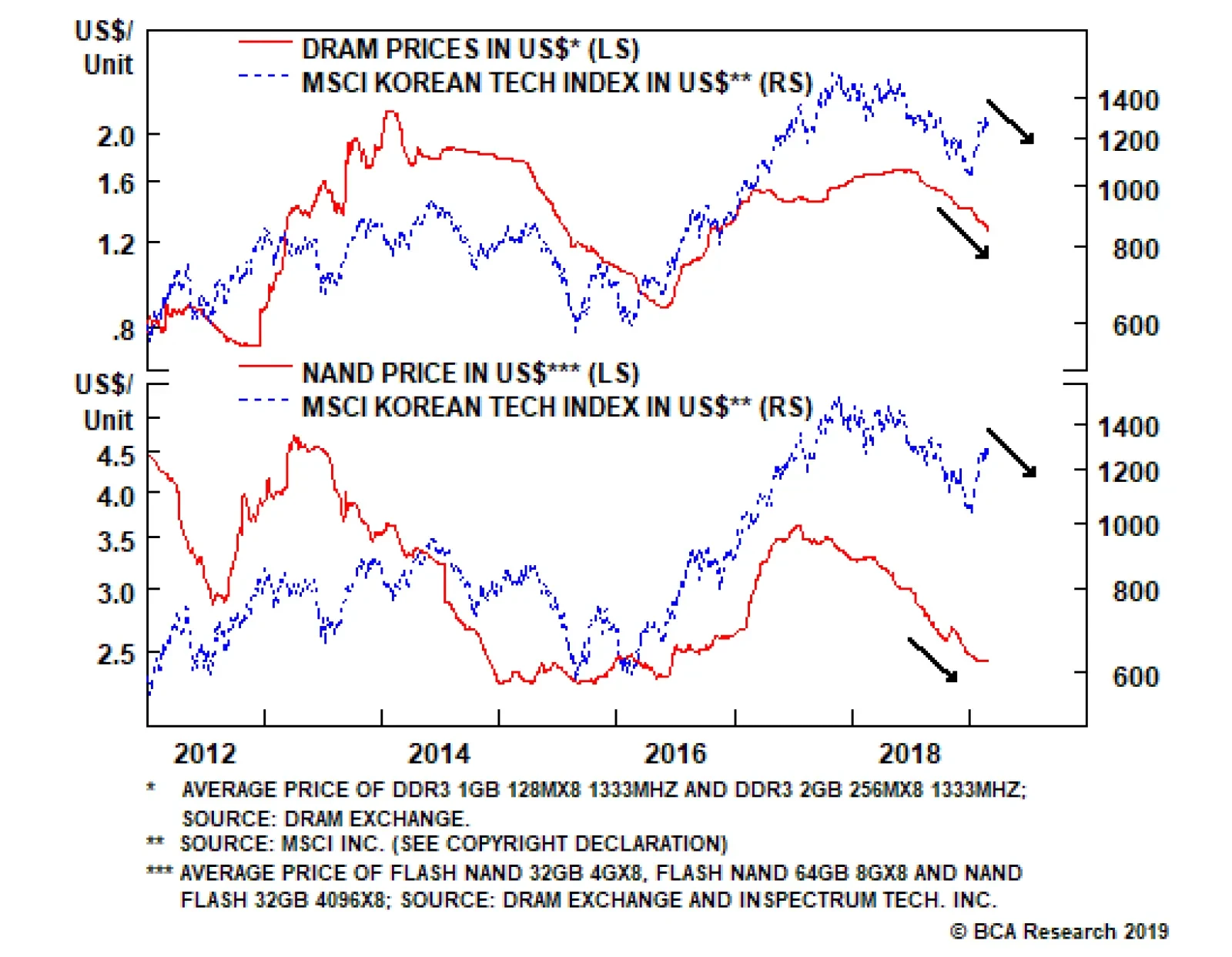

Consistently, tech stocks also account for the lion’s share of the Taiwanese stock market, representing nearly 60% of the MSCI Taiwan Index and 47% of the Taiwanese Stock Exchange (TSE) index in market-value terms. There have been two key forces behind the significant growth of Taiwan’s semiconductor sector: booming global demand for smartphones/tablets and increasing competitiveness among domestic semiconductor companies. However, looking forward, the Taiwanese manufacturing sector and its semiconductor exports are facing a double-whammy: cyclical weakness in global demand and a relative decline in Taiwan’s export ability. In the context of a negative structural outlook, a cyclical downtrend engenders substantial deterioration in manufacturing, and by extension corporate profitability. Cyclical Downturn In Global Semiconductor Demand The outlook for the Taiwanese semiconductor industry remains poor. The global semiconductor industry has already been in a cyclical downtrend since early 2018. Global smartphone sales are shrinking. Both DRAM and NAND prices have been falling (Chart I-3). Chart I-3Falling Memory Chips Prices

Falling Memory Chips Prices

Falling Memory Chips Prices

The freefall in Taiwan's new export orders seems to entail a further contraction in exports (Chart I-4). Chart I-4A Further Contraction In Exports Is Likely

A Further Contraction In Exports Is Likely

A Further Contraction In Exports Is Likely

Importantly, exports of electronics parts lead Taiwanese tech EPS growth, and currently point to an impending contraction in corporate earnings (Chart I-5). Chart I-5An Impending Contraction In Corporate Earnings

An Impending Contraction In Corporate Earnings

An Impending Contraction In Corporate Earnings

The outlook for the Taiwanese semiconductor industry remains poor. First, Taiwanese semiconductor producers are highly vulnerable to any further downside in global smartphone demand. There are two major pure-play wafer manufacturers in Taiwan: Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics (UMC). TSMC and UMC are the world’s largest and fourth-largest dedicated integrated circuit (IC) foundries, respectively. The smartphone sector has been the main revenue source for both companies, accounting for a 45% share for TSMC and 40% for UMC. Global smartphone demand is likely to decline further in 2019, as major markets such as mainland China and advanced economies have entered the saturation phase of mobile-phone demand. DRAMeXchange expects global smartphone production volume for 2019 to fall by 3.3% from last year following a 4% drop in 2018 (Chart I-6). Chart I-6Global Smartphone Demand Started A Downtrend

Global Smartphone Demand Started A Downtrend

Global Smartphone Demand Started A Downtrend

Smartphone sales in mainland China remain in deep contraction after two consecutive years of declines (Chart I-7). Odds are that smartphone shipments will remain sluggish amid the ongoing economic slump in the mainland’s economy. Chart I-7Smartphone Sales In Mainland China Are In A Deep Contraction

Smartphone Sales In Mainland China Are In A Deep Contraction

Smartphone Sales In Mainland China Are In A Deep Contraction

In addition, Taiwan’s TSMC is the sole chip supplier for Apple iPhones. A further decline in Apple smartphone shipments will reduce the company’s revenue and profits, damaging the region’s growth outlook. Mainland China now can produce top-notch quality smartphones at relatively cheaper selling prices. This will further crowd out higher-priced products from Apple, Samsung and others (Chart I-8). Chart I-8Apple Has Been Losing Market Share In Global Smartphone Market

Apple Has Been Losing Market Share In Global Smartphone Market

Apple Has Been Losing Market Share In Global Smartphone Market

Second, the significant surge in bitcoin prices greatly boosted cryptocurrency mining activity in 2016-‘17 as miners quickly expanded their computing power. This boosted demand for graphic process unit (GPU) chips and in turn brought higher revenue for Taiwan chipmakers between June 2016 and early 2018. However, with the bust in bitcoin prices (Chart I-3 on page 3), demand from cryptocurrency mining has vanished and is unlikely to revive soon. Indeed, Taiwan chipmakers have suffered from last year’s plunge in cryptocurrency mining activity. According to TSMC, revenue from the cryptocurrency mining-related high-performance computing (HPC) sector contracted by double digits in 2018. Given that HPC demand is the second-biggest source of revenue for TSMC, with 32% share, TSMC revenue will be curtailed as HPC chip demand will continue to decline on weak bitcoin prices. Last, developments in new technologies, such as foldable smartphones, artificial intelligence, fifth-generation (5G) mobile networks and the so-called Internet of Things (IoTs) could only produce a modest pick-up in semiconductor demand. Most of these developments are still in their infancy and early stages. Hence, their growth will not be large enough to make a cyclical difference in global semiconductor demand. For example, the foldable smartphone that Huawei recently announced is indeed appealing. However, a lack of stability in panel supply and quite-high selling prices will limit sales. WitsView, a division of TrendForce, predicts that the market penetration rate of the foldable phone will be only 0.1% in 2019, and could rise to 1% in 2020 if more panel providers join the game, enabling a significant reduction in panel costs. Moreover, these categories together account for only ~23% of TSMC’s revenue; their modest growth will not be able to make up for the losses from the smartphone and HPC sectors within Taiwan’s economy. Besides, there has been a slowdown in demand from high-growth areas such as data center servers, as well as the automotive and industrial sectors. Putting it all together, odds are that global semiconductor demand will only materially recover in 2020. By that time, more-mature 5G technology and the increasing adoption of the 5G network and 5G-related products may be able to shift global semiconductor demand from the current downturn to a cyclical uptrend. Hence, the cyclical weakness in global semiconductor demand is likely to persist over the next six months. Consequently, Taiwan’s major types of semiconductor production will likely remain in contraction, and inventory levels will stay elevated (Chart I-9 and Chart I-10). Chart I-9Taiwan: Semiconductor Output Contraction Will Likely Continue

Taiwan: Semiconductor Output Contraction Will Likely Continue

Taiwan: Semiconductor Output Contraction Will Likely Continue

Chart I-10Taiwan: Semiconductor Inventory Are Elevated

Taiwan: Semiconductor Inventory Are Elevated

Taiwan: Semiconductor Inventory Are Elevated

Bottom Line: There are no signs of an imminent recovery in exports. A Potential Decline In Taiwan’s Semiconductor Competitiveness Taiwan wafer manufacturers are facing an increasing threat from their Korean and mainland China competitors. Leadership in advanced process technologies has been a key factor in Taiwan’s strong market position in the global semiconductor industry. With cutting-edge technologies, Taiwan has been the global wafer capacity leader since 2015. As of last year, it held about 22% of global installed wafer capacity (Chart I-11).

Chart I-11

However, Taiwan wafer manufacturers are facing an increasing threat from their Korean and mainland China competitors. Korean Chipmakers While Taiwan will remain highly competitive in 7 nanometer (nm) and 10 nm wafer production, it is facing fierce competition from Korea. Manufacturing technologies designated by smaller nanometer numbers tend to have faster speeds and be more power-efficient than technologies designated by larger numbers. TSMC was the first company in the world to mass-produce 7 nm node wafers. Its 7 nm deep ultraviolet lithography (DUV) node has been in mass production since April 2018, producing chips for AMD, Apple, HiSilicon, and Xilinx. Beginning at the end of this month, TSMC will be ready to begin mass production of 7nm wafers using extreme ultraviolet lithography (EUV). The switch from 7nm DUV to 7nm EUV allows for fewer defects and fewer steps required during the production process. The company also aims to boost volume production of its 5 nm nodes in early 2020 and has a target of 3 nm wafers for 2022. Last year, wafer revenue from 7nm and 10nm chips accounted for 9% and 11% of TSMC’s total revenue, respectively (Chart I-12).

Chart I-12

Samsung has been closely following TSMC in terms of technological innovation. It started mass production of EUV-based 7nm chips last October, with a plan of risk production1 of 5nm wafers in 2019 and a target of 4nm wafers in 2022. Meanwhile, IBM announced last December that it signed an agreement with Samsung to produce its next-generation processors with Samsung’s 7nm technology. As Samsung seeks to diversify its revenue source away from memory chips, which last year contributed to about 80% of its operating profit, the company has been determined to ramp up the development of its foundry business. It aims to replace TSMC as the world’s largest foundry producer by 2030. In the near term, Samsung aims to secure a 25% market share in the global pure-play foundry market by 2023, a rise from 19% currently. Last year, Samsung surpassed Taiwan’s UMC to become the world’s second-largest dedicated chipmaker. Moreover, Samsung’s capital spending has been and will continue to be much higher than TSMC. Over the course of 2017 and 2018, Samsung spent about $46.9 billion on semiconductor capital expenditures, more than double TSMC’s $21 billion. Hence, the competition between TSMC and Samsung in the high-end chip market will intensify in the coming years. Chipmakers In Mainland China The competition between TSMC and chipmakers from mainland China is also escalating. Chart I-12 shows that 80% of TSMC’s wafer revenue comes from bigger node wafers (bigger than 10 nm). Taiwan’s second-biggest chipmaker, UMC, only produces wafers equal to or bigger than 28 nm. Therefore, the chip market using less-advanced technology than 10 nm will be the main battlefield between Taiwanese and mainland China’s chipmakers. Before 2014, there were few wafer manufacturers in mainland China, and those that did exist were too weak to compete with giant market players like TSMC. In 2014, the Chinese central government made a move to foster development within the local IC industry. Since then, the authorities have poured significant amounts of capital into semiconductor foundries, as well as companies focused on memory production, chip design and related equipment and materials. Semiconductor Manufacturing International Corporation (SMIC) is the world’s fourth-largest dedicated wafer manufacturer, and is the largest in mainland China. While 28nm will likely remain a large part of its business, SMIC plans to go into production on its 14 nm technology in the first half of 2019. The company is also working on 10nm and 7nm nodes with the use of EUV. SMIC currently counts HiSilicon and Qualcomm as customers, manufacturing smartphone chips with medium-to-low technology. As mainland China aims to increase its self-sufficiency rate for ICs significantly over the next five to 10 years, the nation’s producers will significantly expand their wafer capacity. Mainland China is likely to reduce its semiconductor imports from Taiwan considerably in the coming years, especially wafer imports. According to IC Insights, nine 300mm wafer fabs2 are scheduled to open worldwide in 2019, with five of them in mainland China. Based on another set of data from SEMI, the number of 200mm wafer fabs in the world will increase from 194 in 2017 to 203 by 2022, with an additional 56 established fabs planning to expand their manufacturing capacity. Mainland China is expected to account for 44% of the growth. In comparison, Taiwan only accounts for about 10% of the growth. Mainland China currently accounts for over 30% of Taiwanese electronic parts exports (wafers, PCBs, mainboards and others). As mainland China continues to build new wafer manufacturing capacity and gradually improve its existing technology, it will switch its consumption from imports to domestic production. Consequently, mainland China is likely to reduce its semiconductor imports from Taiwan considerably in the coming years, especially wafer imports (Chart I-13). This is structurally bearish for Taiwanese semiconductor companies. Chart I-13Mainland China’s Semiconductor Imports From Taiwan Will Drop

Mainland China’s Semiconductor Imports From Taiwan Will Drop

Mainland China’s Semiconductor Imports From Taiwan Will Drop

Bottom Line: Taiwan is facing increasing challenges from Korea in terms of defending its market share in the high-end wafer market. Meanwhile, Taiwan is also set to lose market share in the medium-to-low market to wafer producers from mainland China. What About The Rest Of The Economy? The rest of the economy is exhibiting mixed signals, with contracting major non-semiconductor export sectors but decent household consumption and property market. Table 1 shows Taiwan’s top 10 exported products, with the top three attributing to over half of total exports. Besides the semiconductor sector, exports of the other two major products – electrical machinery products and machinery – are beginning to contract (Chart I-14).

Chart I-

Chart I-14Taiwan: Contracting Non-Semiconductor Exports

Taiwan: Contracting Non-Semiconductor Exports

Taiwan: Contracting Non-Semiconductor Exports

However, the domestic economy seems to be running well at present. Production of construction materials in volume terms is growing rapidly, accompanied by a rebound in building permits granted (Chart I-15). While employment growth is decent, average wage growth has been quite strong (Chart I-16). With persistent contraction in exports and inflation very low, the central bank could cut rates in 2019. Chart I-15Decent Domestic Demand

Decent Domestic Demand

Decent Domestic Demand

Chart I-16Strong Wage Growth

Strong Wage Growth

Strong Wage Growth

Ongoing contraction in semiconductor exports will likely slow domestic demand with a time lag. In fact, the inverted 5-year/6-month yield curve is indeed signaling an economic slump in Taiwan (Chart I-17). Chart I-17Inverted Yield Curve Signals Continuing Economic Slump Ahead

Inverted Yield Curve Signals Continuing Economic Slump Ahead

Inverted Yield Curve Signals Continuing Economic Slump Ahead

Investment Recommendations The latest rebound in Taiwanese stocks is unsustainable and share prices will relapse again. Within an EM equity portfolio, we recommend maintaining a market-weight allocation to Taiwan for now. We are reluctant to downgrade Taiwan to underweight because some other emerging markets and sectors within the EM universe have a poorer outlook. In addition, Taiwanese shares have already underperformed the EM benchmark since last September (Chart I-18). Chart I-18Taiwanese Stocks: Staying Neutral Within EM

Taiwanese Stocks: Staying Neutral Within EM

Taiwanese Stocks: Staying Neutral Within EM

The Taiwanese currency is cheap (Chart I-19). The region has a massive current account surplus and foreigners do not hold any local bonds, which is very different from many other EM countries. Hence, Taiwan is less vulnerable to capital outflows than many current-account-deficit EM economies. The latter could be forced to raise rates, which will place pressure on their banks as well as on domestic demand. In contrast, Taiwan has the ability to cut rates. Chart I-19TWD Is Cheap

TWD Is Cheap

TWD Is Cheap

Ellen JingYuan He, Associate Vice President Emerging Markets Strategy ellenj@bcaresearch.com 1 "Risk Production" means that a particular silicon wafer fabrication process has established a baseline in terms of process recipes, device models, and design kits, and has passed standard wafer level reliability tests. 2 A fab, sometimes called foundry, is a semiconductor fabrication plant where devices such as integrated circuits are manufactured. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

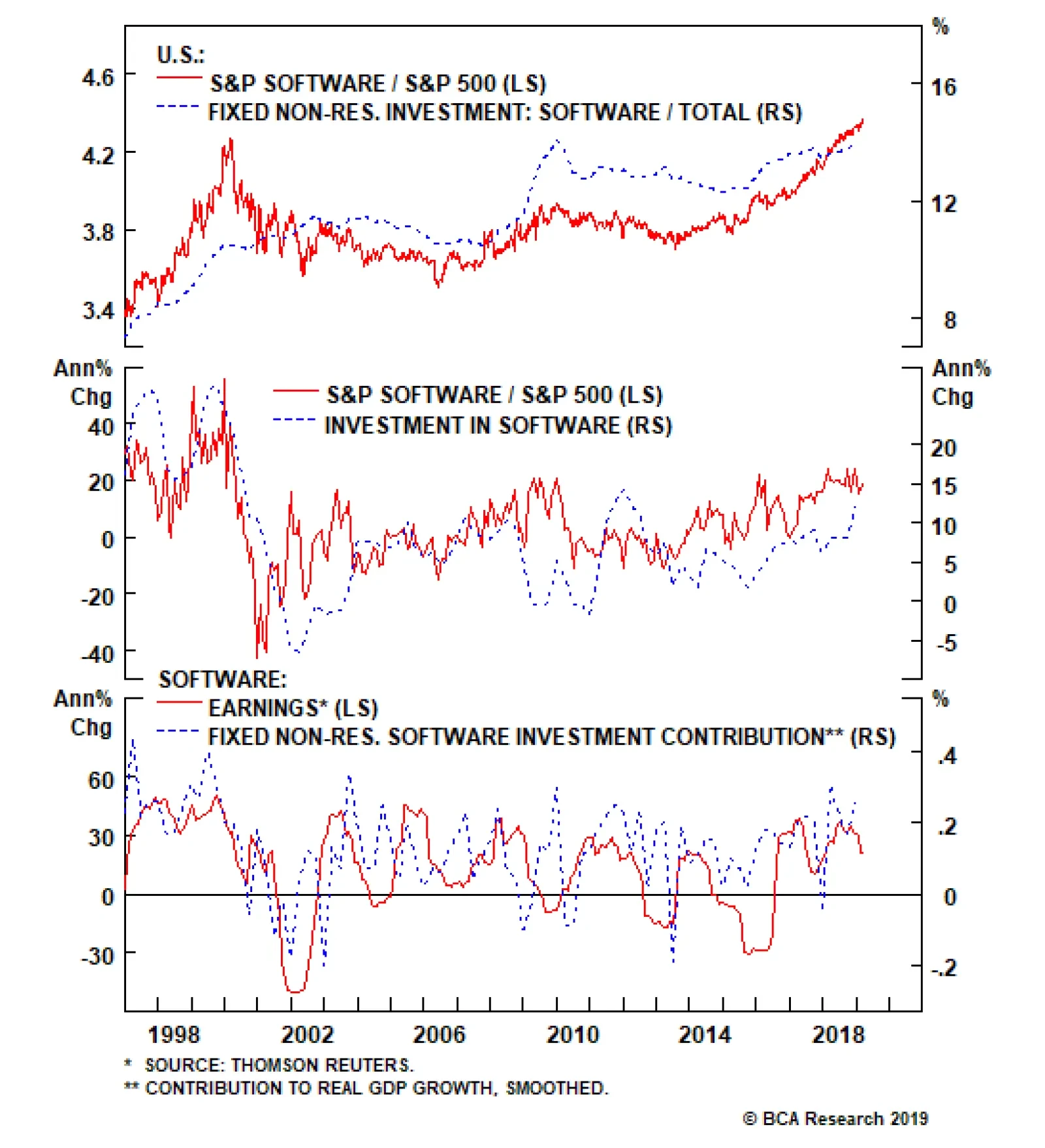

Buy The Software Breakout

Buy The Software Breakout

Overweight (High-Conviction) Software stocks are on fire and leading profit indicators suggest that more gains are in store in the coming months. Sustained capital outlays on software are a key driver of industry profits (bottom panel). In an otherwise muted Q4 GDP release, rising non-residential fixed investment in general and surging investment in software in particular suggest that our bullish software capex thesis is alive and kicking (middle panel). The move to cloud computing and SaaS, the proliferation of AI, machine learning and augmented reality are not fads but enjoy a secular growth profile, and signal that capital outlays on software are also in a structural uptrend. Not only private sector software capex is near all-time highs as a share of total outlays, but also government investment in software is reaccelerating at the fastest pace since the tech bubble. When productivity gains are anemic, both the business and government sectors resort to software upgrades in order to boost productivity. Bottom Line: We reiterated our high-conviction overweight recommendation on the S&P software index on Monday. Please see our Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S5SOFT – MSFT, ORCL, ADBE, CRM, INTU, ADSK, RHT, CDNS, SNPS, ANSS, SYMC, CTXS, FTNT.

While the broad tech sector is on an even keel with the SPX, software EPS are racing at twice the speed of the broad market, roughly 14%. The software profit juggernaut is intact and our U.S. Equity Strategy team reiterates its high-conviction overweight…

Highlights Portfolio Strategy Corporate sector selling price inflation is nil while leading wage inflation indicators signal additional labor cost increases in the coming months. The risk is that profit margins have already peaked for the cycle. We reiterate our tactically cautious overall equity market view. Galloping higher private and public sector software outlays, a structurally enticing software demand backdrop and ongoing industry M&A all signal that it still pays to be bullish software stocks Recent Changes Last Thursday we downgraded the S&P railroads index to underweight. Also last Thursday we trimmed the S&P air freight & logistics index to neutral. Table 1

Have SPX Margins Peaked?

Have SPX Margins Peaked?

Feature The SPX stalled last week, digesting the now-complete Fed pivot. Our sense is that the Fed’s dovish turn is now fully reflected in equities. Importantly, the longer and wider the dichotomy between stocks and bonds gets, the more painful the ramifications from the eventual snap will be, likely with equities yielding to the bond market (Chart 1). As we first posited on March 4, short-term equity market caution is still warranted.1 Chart 1Time To Get Back Together

Time To Get Back Together

Time To Get Back Together

While the Fed meeting and sharp decline in Treasury yields dominated headlines last week, it was the NFIB’s latest release that really caught our attention. Importantly, it revealed that taxes and big government are no longer the biggest problems facing small and medium business owners, but labor is: “Twenty-two percent of owners cited the difficulty of finding qualified workers as their Single Most Important Business Problem, only 3 points below the record high. Ten percent of owners find labor costs as their biggest problem, a record high for the 45-year survey.”2 Historically, such extreme tightness in the SME labor market is a precursor of a yield curve inversion (NFIB cost of labor shown inverted, Chart 2). The link is clearer if we show this same NFIB series with the Labor Department’s average hourly earnings monthly release that is currently running at a 3.4%/annum clip (Chart 3). In other words, a tight labor market is conducive to corporations bidding up the price of labor which in turn causes the Fed to raise interest rates, eventually inverting the yield curve. Chart 2Cycle Is Long In The Tooth

Cycle Is Long In The Tooth

Cycle Is Long In The Tooth

Chart 3Wage Growth...

Wage Growth...

Wage Growth...

This macro backdrop is slightly unnerving and our biggest concern is the S&P 500’s profit margins (Chart 4). Q3/2018 marked the all-time peak in SPX quarterly margins according to Standard & Poor’s,3 and in Q4/2018 margins have deflated from a high mark of 12.13% to 10.11%, or a 16.7% q/q drop. Chart 4...Denting Margins

...Denting Margins

...Denting Margins

Undoubtedly, last year’s fiscal easing-induced all-time highs in SPX margins is unsustainable, and a tight labor market is a warning shot. Using the same NFIB series on cost of labor being the most important problem SMEs face and subtracting it from our corporate pricing power proxy, we constructed an equity market margin proxy, shown as a Z-score in Chart 5. Historically, the y/y change in SPX profit margins move in lockstep with our margin proxy and the current message is grim (Chart 5). Chart 5Margin Trouble Ahead

Margin Trouble Ahead

Margin Trouble Ahead

Before getting too bearish though, we want to make three salient points: First, while the NFIB survey’s labor related indicators are disconcerting, unit labor costs – the best measure of wage growth – remain muted as productivity growth has ramped up recently. Second, using empirical evidence dating back to the 1960s, the ultimate SPX profit margin mean reversion occurs during recessions, when EPS suffer a major setback. The implication is that margins can move sideways or grind lower in the coming year. As a reminder, BCA’s review remains that the U.S. will avoid recession in the next 12 months. Third, the most important yield curve slope, the 10/2, has not yet inverted, and even when it does invert, investors will have time to start positioning defensively; we have shown in recent research that the S&P peaks after the yield curve inverts.4 On a related note, we use this opportunity to update our corporate pricing power proxy, and Table 2 summarizes the sectorial results. Table 2Industry Group Pricing Power

Have SPX Margins Peaked?

Have SPX Margins Peaked?

Corporate sector selling price inflation has ground to a halt at a time when wage inflation is rearing its ugly head. Worrisomely, our pricing power diffusion index’s breadth sunk below the 50% line, whereas our wage growth diffusion index spiked higher; 70% of the 44 industries we track are struggling with rising wages (second & third panels, Chart 6). Taken together, there is evidence that broad-based profit margin pressures are escalating, the mirror image of what our gauges were signaling in our last update late-last year.5 Chart 6Margins Have Likely Peaked

Margins Have Likely Peaked

Margins Have Likely Peaked

Digging beneath the surface of our corporate pricing power proxy is revealing. As a reminder, we calculate industry group pricing power from the relevant CPI, PPI, PCE and commodity growth rates for each of the 60 industry groups we track. Table 2 also highlights shorter term pricing power trends and each industry's spread to overall inflation. 57% of the industries we cover are lifting selling prices, but only 27% are raising prices at a faster clip than overall inflation. Both figures are lower than our early-November report. Outright deflating sectors increased by eight to twenty four since our last update, fifteen of which are deflating at 1%/annum pace or lower. One third of the industries we cover are experiencing a downtrend in selling price inflation, representing a 43% increase since our most recent report (Table 2). Deep cyclicals/commodity-related industries (ex-oil) continue to dominate the top ranks, occupying the top six slots (Table 2). Despite the ongoing global manufacturing deceleration and still unresolved U.S./China trade tussle, the commodity complex's ability to increase prices remains resilient. On the flip side, energy-related industries occupy the bottom of the ranks as WTI crude oil is still 22% lower than the most recent peak in October 2018. In sum, business sector selling price inflation is nil while leading wage inflation indicators signal additional labor cost increases in the coming months. The risk is that profit margins have already peaked for the cycle. We reiterate our tactically cautious overall equity market view. This week we update a high-conviction overweight tech subgroup and recap our transportation subsurface moves from last Thursday. Buy The Software Breakout Software stocks are on fire and leading profit indicators suggest that more gains are in store in the coming months. Last week, we published a table ranking all the sectors and subsectors by 12-month forward profit growth estimates (please refer to Table 2 from the March 18 Weekly Report). While the broad tech sector is on an even keel with the SPX, software EPS are racing at twice the speed of the broad market, roughly 14%. Keep in mind, when growth gets scarce, investors flock to industries with accelerating profit prospects. The software profit juggernaut is intact and we reiterate our high-conviction overweight recommendation. Sustained capital outlays on software are a key driver of industry profits (bottom panel, Chart 7). In an otherwise muted Q4 GDP release, rising non-residential fixed investment in general and surging investment in software in particular suggest that our bullish software capex thesis is alive and kicking (middle panel, Chart 7). Chart 7Software On A Tear

Software On A Tear

Software On A Tear

The move to cloud computing and SaaS, the proliferation of AI, machine learning and augmented reality are not fads but enjoy a secular growth profile, and signal that capital outlays on software are also in a structural uptrend. Not only private sector software capex is near all-time highs as a share of total outlays, but also government investment in software is reaccelerating at the fastest pace since the tech bubble. When productivity gains are anemic, both the business and government sectors resort to software upgrades in order to boost productivity. Cyber security is another more recent source of software related demand as governments are taking such risks extremely seriously the world over (second panel, Chart 8). Chart 8Earnings Led Advance

Earnings Led Advance

Earnings Led Advance

Meanwhile, fear of missing out has rekindled industry M&A and both the dollar amount and number of deals are sky high, with acquirers bidding up premia to the stratosphere (Chart 9). This supply reduction is bullish for industry pricing power. Chart 9M&A Frenzy

M&A Frenzy

M&A Frenzy

Granted the M&A frenzy has pushed relative valuations on the expensive side especially on a forward P/E basis, but on EV/EBITDA software stocks are trading below the historical mean and still significantly lower than the late-1990s peak valuation (bottom panel, Chart 8). If our bullish software profit thesis continues to pan out, then software stocks will grow into their pricey valuations. Finally, shareholder friendly activities are ongoing in this key tech subsector and buybacks in particular provide an added layer of artificial EPS growth (bottom panel, Chart 9). Adding it up, galloping higher private and public sector software outlays, a structurally enticing software demand backdrop and ongoing industry M&A, all signal that it still pays to be bullish software stocks. Bottom Line: Buy the software breakout. The S&P software index remains a high-conviction overweight. The ticker symbols for the stocks in this index are: BLBG: S5SOFT – MSFT, ORCL, ADBE, CRM, INTU, ADSK, RHT, CDNS, SNPS, ANSS, SYMC, CTXS, FTNT. Tweaking Transport Subgroup Positioning The S&P transports index’s recovery rally has stalled recently and is a cause for concern for the overall market. In more detail, the recent gulf between relative share prices and the SPX has widened and warns that the overall market is at a risk of suffering a pullback (Chart 10). Chart 10Engine Trouble

Engine Trouble

Engine Trouble

Thus on Thursday last week, we made two subsurface transport changes, downgrading a subgroup to underweight that commands lofty valuations at a time when leading profit indicators are flashing red, and also downgrading to neutral a globally exposed transport sub-index. Get Off The Rails In our downgrade of the S&P railroads index late last year to a benchmark allocation, we highlighted that two of our key industry Indicators, the Railroad Indicator and our Rail Shipment Diffusion Indicator, had turned negative.6 These indicators have continued to deteriorate, including total rail shipments which have now started to contract for the first time since the 2015-16 manufacturing recession (third panel, Chart 11). Intermodal shipments in particular have nosedived, likely a result of weak retail sales, as we highlighted earlier this month.7 Chart 11Downgrade Rails To...

Downgrade Rails To...

Downgrade Rails To...

This contraction would be far less concerning were it not for the rapid degradation of industry balance sheets as firms have sought to increase relatively cheap leverage in order to retire equity. Railroads are now significantly more indebted than the broad market which itself has not shown an aversion to adding leverage (bottom panel, Chart 11). Such a change in railroad capital structure has kept EPS growth rates artificially high while simultaneously adding an extra measure of equity risk premium that does not yet appear fully reflected in relative share prices. Moreover, when we downgraded the S&P railroads index to neutral last year, deteriorating Indicators were offset by exceptionally healthy pricing power.8 After a multi-year expansion, selling price inflation has now rolled over (second panel, Chart 12), taking away the remaining pillar supporting a neutral view which compelled us to move to an underweight allocation last week. Chart 12...Underweight

...Underweight

...Underweight

Pricing power is one of the key determinants in our earnings model that, when combined with the previously noted contracting volumes, is indicating the end to the industry’s above-trend earnings growth is nigh (third panel, Chart 12). With relative earnings growth slowing and rising leverage adding incremental risk, the S&P railroads index’s premium valuation multiple looks increasingly dicey (bottom panel, Chart 12). Bottom Line: Broad based declines in traffic volumes, falling pricing power and high leverage suggest that earnings will underwhelm. Accordingly, last Thursday we moved to an underweight recommendation on the S&P railroads index as we expect a de-rating phase to materialize. The ticker symbols for the stocks in this index are: BLBG: S5RAIL - UNP, CSX, NSC, KSU. Air Freight Had Its Wings Clipped We have been offside on the high-conviction overweight call on the S&P air freight & logistics index and the recent FedEx warning suggests that profits will come under pressure for this index for the rest of the year and will trail the SPX. As such, we trimmed exposure to neutral late-last week and removed it from the high-conviction overweight list for a loss of 14%. Chart 13 shows that all the profit drivers we had identified in early December last year have taken a sharp turn for the worse. Energy costs are no longer in deflation as oil prices have jumped from $42/bbl to near $60/bbl. Not only is global growth still decelerating, but also U.S. growth is in a softpatch: the manufacturing shipments-to-inventory ratio is on the verge of contraction, warning that delivery services’ selling prices are in for a turbulent ride (second panel, Chart 13). In addition, definitive news of Amazon becoming a formidable competitor in courier delivery services is structurally negative for the industry. Chart 13Air Freight: Move To The Sidelines

Air Freight: Move To The Sidelines

Air Freight: Move To The Sidelines

Nevertheless, we refrain from turning outright bearish as air freight stocks are technically oversold and valuations are trading at the steepest discount to the broad market since mid-2002. Bottom Line: Last Thursday we downgraded the S&P air freight & logistics index to neutral and also removed it from the high-conviction overweight list. The ticker symbols for the stocks in this index are: BLBG: S5AIRF - UPS, FDX, CHRW, EXPD. Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA U.S. Equity Strategy Weekly Report, “The Good, The Bad And The Ugly” dated March 4, 2019, available at uses.bcaresearch.com. 2https://www.nfib.com/assets/jobs0219hwwd.pdf 3https://ca.spindices.com/documents/additional-material/sp-500-eps-est.xlsx?force_download=true 4 Please see BCA U.S. Equity Strategy Weekly Report, “Signal Vs. Noise” dated December 17, 2018, available at uses.bcaresearch.com. 5 Please see BCA U.S. Equity Strategy Weekly Report, “Recuperating” dated November 5, 2018, available at uses.bcaresearch.com. 6 Please see BCA U.S. Equity Strategy Weekly Report, “Critical Reset“, dated October 29, 2018, available at uses.bcaresearch.com. 7 Please see BCA U.S. Equity Strategy Weekly Report, “The Good, The Bad And The Ugly“, dated March 4, 2019, available at uses.bcaresearch.com. 8 Please see BCA U.S. Equity Strategy Weekly Report, “Critical Reset“, dated October 29, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

A Reboot In Sentiment For Tech Hardware

A Reboot In Sentiment For Tech Hardware

Overweight The S&P tech hardware, storage & peripherals (THSP) index has been outperforming in the past few sessions as sell side sentiment has reversed course, principally on the dominant constituent firm, Apple. Net earnings revisions have bounced back strongly from the collapse following Apple’s repeated lowered forward guidance at the end of 2018 (second panel); it appears both the sell side and the market are looking forward from a new reset point. Optimism seems justified: Apple’s recent revamp of a number of product lines was well received and Monday’s upcoming launch of the company’s streaming service and its potential for deepening high-margin services revenue and cementing the company’s ecosystem has drawn a number of ratings upgrades this week. From a macro perspective we remain focused on valuation and leverage, both of which are encouraging. Despite the recent rally, the S&P THSP index continues to trade at a >10% discount to the broad market (third panel). Further, the still-pristine balance sheets reinforce some expectations that Apple could unveil a $100 billion share buyback program for the year to come. Bottom Line: A number of catalysts should propel the reasonably valued S&P THSP index higher; stay overweight. The ticker symbols for the stocks in the S&P THSP index are: BLBG: S5CMPE - HPQ, WDC, STX, XRX, AAPL, HPE, NTAP.

The Race To $1 Trillion

The Race To $1 Trillion

Overweight (High-Conviction) In last week’s GDP report, software was a clear standout. Investment in software as a ratio of total fixed non-residential investment has been on fire for much of the past four years and is on the cusp of surpassing the GFC highs when capex collapsed, but defensive outlays on software stood their ground (top panel). On a rate of change basis, growth in investment in software has breached the double-digit level for the first time in seven years; the last time this happened marked the beginning of software’s five year bull run. Further, the acute uptick in software investment’s contribution to GDP growth is an excellent herald for relative earnings performance. While the latter’s growth has been decelerating of late, the sharp divergence from the former suggests a resumption of outsized EPS growth in the S&P software index (bottom panel). Bottom Line: We reiterate our high-conviction overweight recommendation in the S&P software index. The ticker symbols for the stocks in this index are: BLBG: S5SOFT - MSFT, ORCL, ADBE, CRM, INTU, RHT, ADSK, SNPS, CTXS, ANSS, CDNS, FTNT and SYMC.

Korea’s dependence on the semiconductor sector has risen considerably in the past several years: Semiconductor exports have risen from under 10% to slightly above 20% of total goods exports. On the demand front, memory demand from the global smartphone…

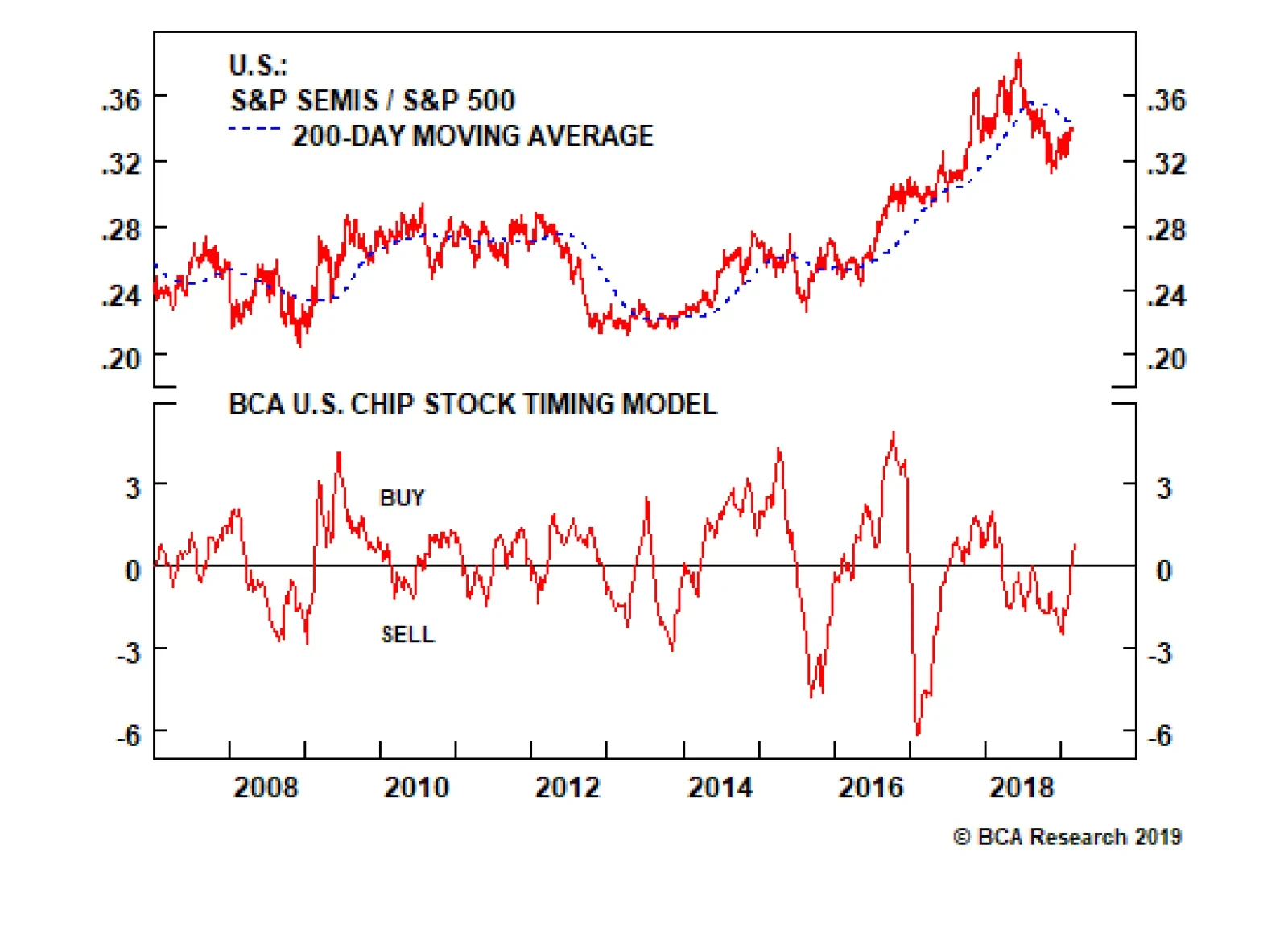

The Chip Cycle Is Turning

The Chip Cycle Is Turning

Neutral There are high odds that the chip cycle will soon take a turn for the better. Global chip sales have been decelerating for 17 months and are now on the cusp of contraction (middle panel). Over the past two decades, steep contractions have been associated with recession. Given that BCA’s view does not call for recession this year, it is highly unlikely for global semi sales to suffer a major setback. While we do not rule out a brief and shallow dip below zero similar to the 2011/12 and 2015/16 parallels, leading indicators of global semi sales suggest that a trough is near. Namely, BCA’s Global Leading Economic Indicator (GLEI) diffusion index is in a V-shaped recovery signaling that global growth is close to a nadir (middle panel). Similarly the U.S. dollar is decelerating which is a boon to global growth and conducive to higher global chip sales (trade-weighted U.S. dollar shown inverted, bottom panel). Bottom Line: In Monday’s Weekly Report, we lifted the S&P semiconductors index to neutral and added it to our upgrade watch list; we are looking for an opportunity to boost to overweight on a pullback, stay tuned. Finally, from a risk management perspective we increased our trailing stop to 15% in our tactical overweight in the S&P semi equipment index, in order to protect gains. The ticker symbols for the stocks in the S&P semiconductors index are: BLBG: S5SECO – INTC, AVGO, TXN, NVDA, QCOM, MU, ADI, XLNX, AMD, MCHP, MXIM, SWKS, QRVO.

Highlights Korean stocks are facing downside risks over the next several months. Exports will continue to contract on falling semiconductor prices and retrenching global demand. Growth deceleration and low inflation will lead the central bank to cut rates in 2019. Within an EM equity portfolio, we are downgrading Korean tech stocks from overweight to neutral but remain overweight the non-tech sector. We are booking gains on our strategic long positions in EM tech versus both the broader EM equity benchmark and materials. The KRW/USD exchange rate is at a critical technical juncture. Investors should wait to buy on a breakout and/or sell on a breakdown of the tapering wedge pattern. Feature Decelerating and lately contracting South Korean exports have been a major drag on the economy and stock market (Chart I-1). The country is heavily reliant on manufacturing, with exports of goods contributing to nearly half of real GDP. Chart I-1Korean Stocks: Unsustainable Rebound?

Korean Stocks: Unsustainable Rebound?

Korean Stocks: Unsustainable Rebound?

Although exports are currently shrinking, Korean domestic stock prices still rebounded. The rebound has mostly been driven by the information technology (tech) sector (Chart I-2).

Chart I-2

Is this recent rally justified by underlying fundamentals? Will share prices continue to rise in 2019? Our inclination is ‘no’ to both questions. There are still dark clouds on the horizon for both Korea’s business cycle and stock market. We are downgrading Korean tech stocks to neutral from overweight within a dedicated EM equity portfolio. However, we are maintaining our overweight in non-tech stocks relative to the EM equity benchmark. Lingering Risks In The Semiconductor Industry Korea’s dependence on the semiconductor sector has risen considerably in the past several years: Semiconductor exports have risen from under 10% to slightly above 20% of total goods exports (Chart I-3). As such, the outlook for semiconductor exports is a critical factor for future economic growth. Chart I-3Korea: Increasing Reliance On The Semiconductor Sector

Korea: Increasing Reliance On The Semiconductor Sector

Korea: Increasing Reliance On The Semiconductor Sector

Table 1 lists the top 10 major exported goods from Korea, together contributing about 72% of total exports. Semiconductors are by far the largest component. Last year, overseas sales of semiconductors alone contributed to some 90% of growth in Korean exports, and about one-third of the country’s nominal GDP growth.

Chart I-

Notably, Korea produces the largest quantity of DRAM and NAND memory chips in the world. Last year, Korean semiconductor companies accounted for about 70% of global DRAM and 50% of NAND flash global sales revenue. In 2019 Korean semiconductor exports will likely contract due to further deflation in DRAM and NAND memory prices (Chart I-4). Chart I-4Memory Prices Are Plunging

Memory Prices Are Plunging

Memory Prices Are Plunging

The 2016-2017 surge in DRAM and NAND flash prices was due to supply shortages relative to demand. Last year, NAND prices plunged and DRAM prices began to fall as their supply-demand balances shifted to oversupply. This year, the glut will worsen. Demand Global demand for DRAM and NAND memory is slowing. Memory demand from the global smartphone sector – one important end-user market for DRAM and NAND memory chips – is contracting. According to the International Data Corporation (IDC), the global mobile phone sector is the biggest end-market for both DRAM and NAND memory chips, with nearly 40% market share in each. As major markets like China and advanced economies have entered the saturation phase of mobile-phone demand, global smartphone shipments are likely to decline further in 2019 (Chart I-5, top panel). Chart I-5Global Memory Demand Is Slowing

Global Memory Demand Is Slowing

Global Memory Demand Is Slowing

DRAMeXchange1 expects global smartphone production volume for 2019 to fall by 3.3% from last year. In addition, the significant surge in bitcoin prices greatly boosted cryptocurrency mining activity in 2016-‘17 as miners quickly expanded their computing power. This contributed to strong DRAM demand and in turn higher semiconductor prices between June 2016 and May 2018. With the bust of bitcoin prices, this demand has vanished, which will further weigh on prices (Chart I-5, bottom panel). Supply High semiconductor prices in 2016-2017 boosted global production capacity expansion of DRAM and NAND memory chips. Based on data compiled by the IDC, global DRAM and NAND flash capacity expanded by 5.7% and 4.3% respectively in 2018 from a year earlier. As most of the global new capacity was added in the second half of 2018, the output of DRAM and NAND in 2019 will be higher than last year. Moreover, DRAM capacity will grow an additional 4% this year. Because of rising supply and slowing demand, both DRAM and NAND markets are in excess supply and have high inventories. DRAMeXchange forecasts that average DRAM prices will drop by at least another 20% in 2019, while NAND flash prices will fall another 10% from current levels. DRAM and NAND flash memory are the largest components of Korean tech producers. Yet they also sell many other tech products such as analog integrated circuits, LCD drivers, discrete circuits, sensors, actuators, and so on. Apart from the negative impact of declining global DRAM and NAND flash prices, the country’s semiconductor exports will also suffer from slowing demand in China in 2019. China, the biggest importer of Korean semiconductor products, has already shown waning demand. Its imports of electronic integrated circuits and micro-assemblies have contracted over the past two months in both value and volume terms (Chart I-6, top and middle panels). This mirrors a similar contraction in Korean semiconductor exports over the same period (Chart I-6, bottom panel). Chart I-6Weakening Chinese Semiconductor Demand

Weakening Chinese Semiconductor Demand

Weakening Chinese Semiconductor Demand

Bottom Line: Korean semiconductor producers will likely face a contraction in their sales in 2019 due to weakening demand and deflating semiconductor prices. Diminishing Competitive Advantage Korea has been losing its competitive edge in key sectors like automobiles and smartphones. Even though the country remains highly competitive in the global semiconductor industry, it is beginning to show early signs of losing competitiveness there too. Improving competitiveness among other producers as well as a slowing pace of technological improvement and rising production costs are major reasons underlying Korea’s diminishing global competitiveness. Automobiles Korean auto manufacturers have lost market share in the global auto market. In China, the world’s biggest auto market, Korean brands’ market share has declined significantly in the past four years, losing out to both Japanese and German brands (Chart I-7, top three panels). Chart I-7Korea: Losing Market Shares In China's Auto Market

Korea: Losing Market Shares In China's Auto Market

Korea: Losing Market Shares In China's Auto Market

Korean car companies have established auto manufacturing plants in China over the past decade. As a result, all Korean cars sold in China are produced within China, and automobile exports to China from Korea have fallen to zero (Chart I-7, bottom panel). Due to Korean auto manufacturers’ diminishing competitive advantage, Korean automobile production and exports peaked in 2012 in terms of volumes, and have been on a downtrend over the past seven years (Chart I-8, top panel). Chart I-8Further Decline In Korean Auto Output And Exports Is Possible

Further Decline In Korean Auto Output And Exports Is Possible

Further Decline In Korean Auto Output And Exports Is Possible

While demand for Korean cars in the EU remains resilient, sales volumes in the U.S., China and the rest of world have been on a downward trajectory (Chart I-8, bottom three panels). Smartphones In the global smartphone market, Korea’s major smartphone-producing company – Samsung – has been in fierce competition with Chinese brands, and it seems to be losing the battle. Chart I-9 shows that while Samsung’s smartphone sales declined 8% year-on-year last year, smartphone sales from major Chinese smartphone producers (Huawei, Xiaomi, Oppo and Vivo) continued to grow at a pace of 20%. Chart I-9Korea: Losing Market Shares In Global Smartphone Market

Korea: Losing Market Shares In Global Smartphone Market

Korea: Losing Market Shares In Global Smartphone Market

From 2012 to 2018, China’s share of global smartphone shipments rose from 6% to 39%. By comparison, Samsung’s share declined from 30% to 21% over the same period. Semiconductors Korean semiconductor companies – notably Samsung and SK Hynix – will likely remain the biggest producers in the memory market, given their advanced technology. However, there are still signs that Korean semiconductor companies will face increasing challenges in protecting their market share. Based on IDC data, Korean semiconductor companies’ share of global DRAM capacity will inch lower to 65% in 2019 from 65.4% in 2017, while their share of NAND capacity will decline to 53.8% from 57.5% during the same period. Meanwhile, China is focusing on boosting its self-sufficiency in terms of semiconductor production. At the moment there is still a three- to four-year technological gap between China and Korea in DRAM and NAND mass production, though the gap is likely to narrow. In the meantime, the U.S. will continue to create obstacles to prevent the rise of the Chinese semiconductor sector. However, these factors will only delay – not avert – the sector’s development and growth. We believe China will remain firmly committed to develop its semiconductor sector, particularly memory products, irrespective of the cost of investment necessary to do so. Similar to what has transpired in both automobile and smartphone production (Chart I-10), China will slowly increase its penetration in the semiconductor market with increasing capacity and a narrower technology gap over the next five to 10 years. After all, the world’s biggest semiconductor demand is in China. Chart I-10China: A Rising Star In Global Auto And Smartphone Market

China: A Rising Star In Global Auto And Smartphone Market

China: A Rising Star In Global Auto And Smartphone Market

Significant increase in labor costs = falling export competitiveness for all sectors Korean President Moon Jae-in’s flagship economic policy, “income-led growth,” has resulted in dramatic increases in minimum wages since he took office in 2017, further damaging Korea’s competitiveness. The nation’s minimum wage was hiked by 7.3% in 2017, 16.4% in 2018 and will rise by another 11% to 8,350 KRW or $7.40 an hour, in 2019. As the president remains committed to meeting his campaign pledge of lifting the minimum wage to 10,000 KRW an hour, or about $8.90, this would require a further 20% increase in the next year or two. In addition, the government has also limited the maximum workweek to 52 hours since last July for businesses with more than 300 workers. Last month, the Cabinet further approved a revision bill whereby workers are eligible to receive an additional eight hours of wages every weekend for 40 hours of work that week. The new wage regulations have become a substantial burden on employers in all industries. The impact is more severe on small- and medium-sized enterprises (SMEs). According a recent survey, about 30% of SMEs have been unable to pay workers due to the state-set minimum wage. It is also affecting large manufacturers. According to a joint statement released in late December by the Korea Automobile Manufacturers Association and the Korea Auto Industries Cooperative Association, local automakers’ annual labor cost burdens will increase by at least 700 billion won (US$630 million) a year. As for auto parts manufacturers, a skyrocketing financial burden due to the new policy may threaten their survival. In addition, despite the KORUS FTA agreement reached between Korea and the U.S. last September, Korean auto manufacturers still fear they will be subject to new tariffs in 2019. On February 17, the U.S. Commerce Department submitted a report about imposing tariffs on imported automobiles and auto parts to U.S. President Donald Trump, who will make a decision by May 18. Our Geopolitical Strategy Service (GPS) team believes the odds of U.S. administration imposing auto tariffs on imported cars from Korea are small as this will be against the KORUS FTA agreement.2 Our GPS team also believes Japan is less likely to suffer a tariff than the EU, and even if Japan suffers a tariff along with the EU, Japan will negotiate a waiver more quickly than the EU. In both cases, Korea is likely to sell more cars in the U.S., but it will continue to face strong competition from Japan. Bottom Line: In addition to weakening global demand, a deterioration in Korea’s competitive advantage, due in large part to improving competitiveness among other producers and rising domestic wages, will negatively affect Korean exports. What About Domestic Demand? Record fiscal spending in 2019 will boost public sector consumption considerably, offsetting weakening consumption in the private sector. As the new wage policy will likely result in more layoffs and additional shuttering of businesses, domestic retail sales growth will remain under pressure (Chart I-11). Hence, an unintended consequence of the government’s higher income policy will be weaker aggregate income and consumer spending growth. Chart I-11KOREA The New Wage Policy May Trigger More Layoffs And Weaken Retail Sales

KOREA The New Wage Policy May Trigger More Layoffs And Weaken Retail Sales

KOREA The New Wage Policy May Trigger More Layoffs And Weaken Retail Sales

Manufacturing and service sector jobs, including wholesale and retail trade and hotels and restaurants, account for 17% and 23% of total employment, respectively. Of all sectors, these two lost the most employees in January from a year ago. Meanwhile, due to the government’s deregulation of loans in 2014, Korean household debt has increased at a much faster pace than nominal income growth (Chart 12, top panel). As a result, Korea’s household debt has rapidly risen to 86% of its GDP as of the end of the third quarter of last year, from 72% four years ago – (Chart I-12, bottom panel). Elevated household debt at a time of rising layoffs will increase consumer anxiety and weigh on household spending. Chart I-12High Household Debt Will Weigh On Spending

High Household Debt Will Weigh On Spending

High Household Debt Will Weigh On Spending

In order to combat an economic downturn, the government last month approved a record 467 trillion won ($418 billion, 26.5% of the country’s 2018 GDP) budget for 2019, up 9.5% from last year. The last time the budget increased by such a big scale was in 2009, when spending rose 10.7% in the wake of the global financial crisis. In addition, the government will front-load spending – with 61% of the budget to be spent in the first half of 2019. Household spending and government expenditures account for 48% and 15% of real GDP, respectively, while exports equal about 50% of real GDP. Hence, the increase in fiscal spending will not entirely offset the contraction in exports and slowdown in consumer spending. This entails a considerable slowdown in economic growth in 2019. Bet On Monetary Easing With growth disappointing and both headline and core inflation well below 2% (Chart I-13), the central bank will cut rates in 2019. Chart I-13Bet On A Rate Cut

Bet On A Rate Cut

Bet On A Rate Cut

So far, economic growth has decelerated in the past 10 months, and recent data shows no signs of recovery. The country’s manufacturing sector is in contraction, with manufacturing PMI holding below the 50 boom-bust line in January (Chart I-14). Meanwhile, South Korea's unemployment rate rose to a nine-year high in January, with most of the job losses in the manufacturing and construction sectors. Chart I-14Manufacturing Sector: Still In Contraction

Manufacturing Sector: Still In Contraction

Manufacturing Sector: Still In Contraction

Saramin, a South Korean job search portal, surveyed 906 firms in South Korea last month, 77% of which expressed unwillingness to hire new employees due to higher labor costs and negative business sentiment. Retail sales volume growth recently tumbled to 2-3%, pointing to faltering domestic demand (Chart I-11 above, bottom panel). The fixed-income market is not pricing in a rate cut in 2019. Therefore, investors should consider betting on lower interest rates. Shrinking exports and rate cuts will likely undermine the Korean won. Bottom Line: Economic deceleration and low inflation will lead the central bank to cut interest rates in 2019. Investment Implications The following are our investment recommendations: Downgrade the Korean tech sector from overweight to neutral within the EM space. We are reluctant to downgrade to underweight because many other emerging markets and sectors within the EM universe have poorer structural fundamentals than Korean tech. The tech sector accounts for 38% of the MSCI Korea Index, and 27% of the KOSPI in terms of market value. The stock with the largest weight in the MSCI Korea equity index is Samsung Electronics, with a share of 25%, followed by SK Hynix, with a ~5% share. Both are very sensitive to semiconductor prices. Specifically, semiconductor sales accounted for 31% of Samsung’s revenue, but contributed 77% of Samsung’s operating profit last year (Table I-2).

Chart I-

Falling prices reduce producers’ profits by more than falling volumes.3 Hence, profits of semiconductor producers in Korea and globally will shrink in 2019. This will lead to a substantial selloff in Korean tech stocks (Chart I-15). Chart I-15Falling Memory Prices Will Trigger A Sell-Off In Korean Tech Stocks

Falling Memory Prices Will Trigger A Sell-Off In Korean Tech Stocks

Falling Memory Prices Will Trigger A Sell-Off In Korean Tech Stocks

Meanwhile, China accounts for 33% of Samsung’s revenue, making it the largest market (Chart I-16). The ongoing economic slump in China’s domestic demand implies weaker demand for Korean shipments to China, which account for 28% of its exports and 14% of its GDP.

Chart I-16

We are booking gains on our strategic long position in the Korean tech sector versus the EM benchmark index first instituted on January 27, 2010. This trade resulted in a 136% gain (Chart I-17, top panel). Chart I-16Taking Profits On Our Overweight Tech Positions

Taking Profits On Our Overweight Tech Positions

Taking Profits On Our Overweight Tech Positions

Consistently, we are also taking profits on our long EM tech / short EM materials stocks trade, a strategic recommendation initiated on February 23, 2010 that has yielded a 186% gain (Chart I-17, second panel). The basis for this strategic position was our broader theme for the decade of being long what Chinese consumers buy and short plays on Chinese construction, which we initiated on June 8, 2010.4 Stay overweight non-tech equities within the EM space. The fiscal stimulus will have a considerable positive impact on the economy. Besides, Korean non-tech stocks have been weak relative to the EM equity benchmark, and in a renewed EM selloff they could act as a low-beta play (Chart I-17, bottom panel). We initiated our long Korean non-tech sector versus the EM benchmark index on May 31, 2018, which has so far been flat. The KRW/USD exchange rate is at a critical technical juncture. Investors should wait and buy on a breakout or sell on a breakdown of the tapering wedge pattern. The KRW/USD has been in a tight trading range over the past eight months (Chart I-18) and is approaching a major breaking point – i.e., any move will be significant, which we expect will largely depend on the movement of the RMB/USD. Chart I-18Tapering Wedge Patterns

Tapering Wedge Patterns

Tapering Wedge Patterns

The natural path for the RMB would have been depreciation versus the U.S. dollar. However, China may opt for a flat exchange rate versus the U.S. dollar given its promises to the U.S. within the framework of forthcoming trade agreements. We have been shorting the KRW versus an equally weighted basket of USD and yen since February 14, 2018. We continue to hold this trade for the time being. Investors should augment their positions if the KRW/USD breaks down or close this trade and go long the won if the KRW/USD breaks out of its tapering wedge pattern. With respect to fixed income, we continue to receive Korean 10-year swap rates as we expect interest rates to fall meaningfully. Local investors should overweight bonds versus stocks. Ellen JingYuan He, Associate Vice President Emerging Markets Strategy ellenj@bcaresearch.com Footnotes 1 DRAMeXchange, the memory and storage division of a technology research firm TrendForce, has been conducting research on DRAM and NAND Flash since its creation in 2000. 2 Please see the Geopolitical Strategy Weekly Report, "Trump's Demands On China", published April 4, 2018. Available at gps.bcaresearch.com. 3 Please see the Emerging Markets Strategy Weekly Report “Corporate Profits: Recession Is Bad, Deflation Is Worse”, dated January 28, 2016, available at www.bcaresearch.com 4 Please see the Emerging Markets Strategy Special Report “How To Play Emerging Market Growth In The Coming Decade”, dated June 8, 2010, available at www.bcaresearch.com. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

There are high odds that the chip cycle will soon take a turn for the better. Global chip sales have been decelerating for 17 months and are now on the cusp of contracting. Over the past two decades, steep contractions have been associated with recessions.…