Technology

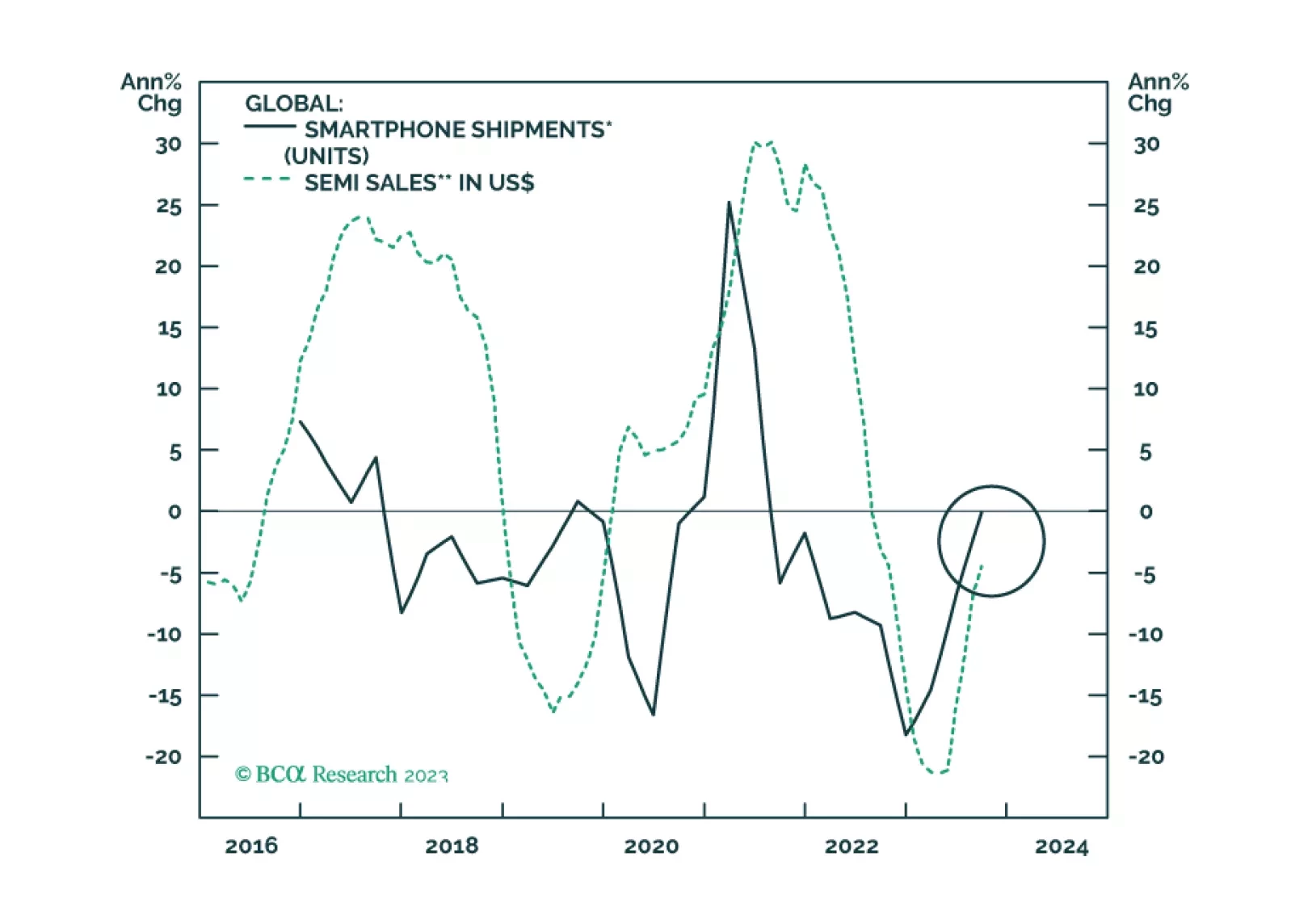

Global smartphone demand will likely find a bottom in 2024Q1 and rebound modestly between 2024Q2 and Q4. Competition in the global smartphone market will intensify. Chinese phone makers will gain market share from Apple and Samsung. Continue overweighting Taiwanese stocks, including tech, within the global equity benchmark.

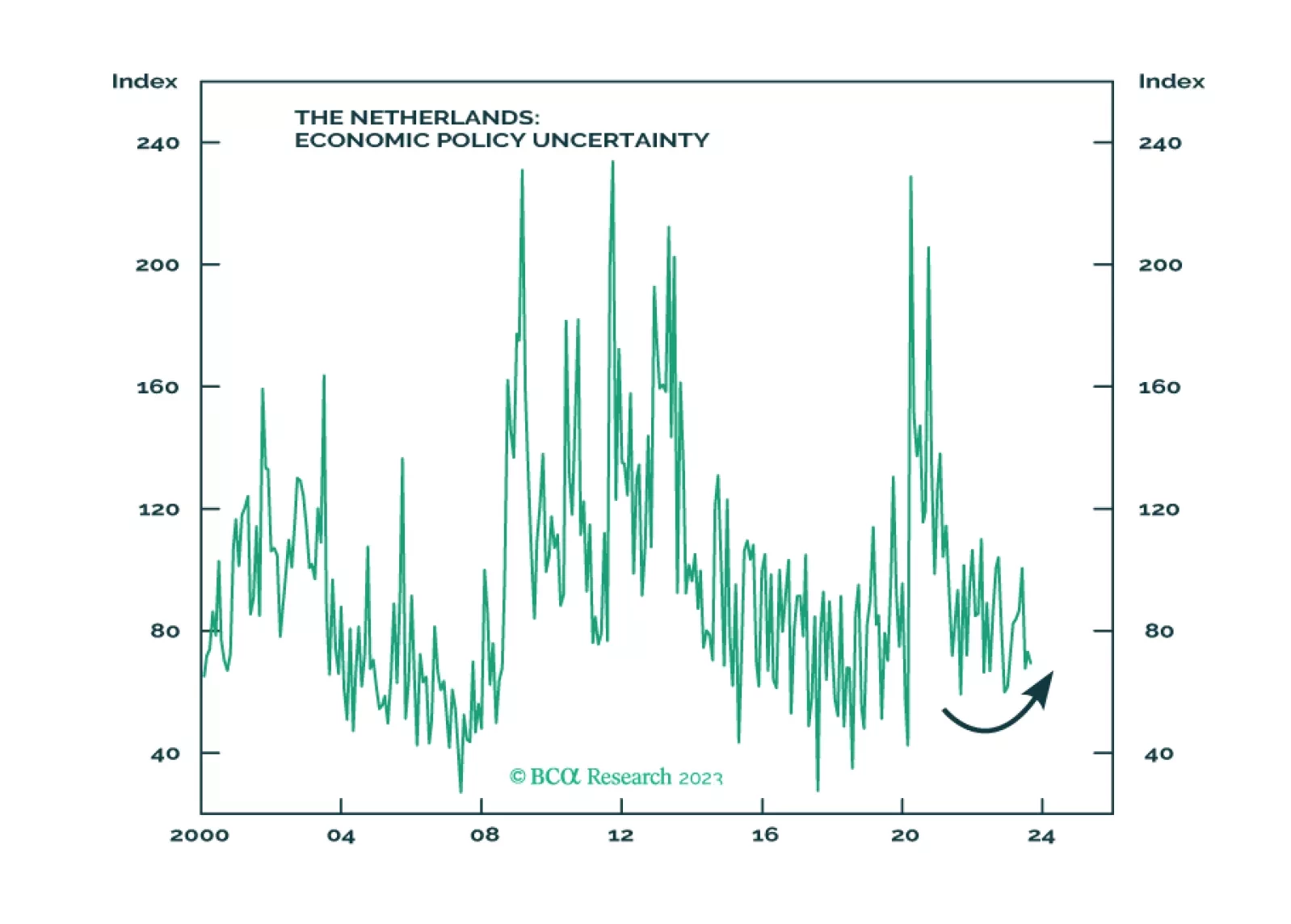

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

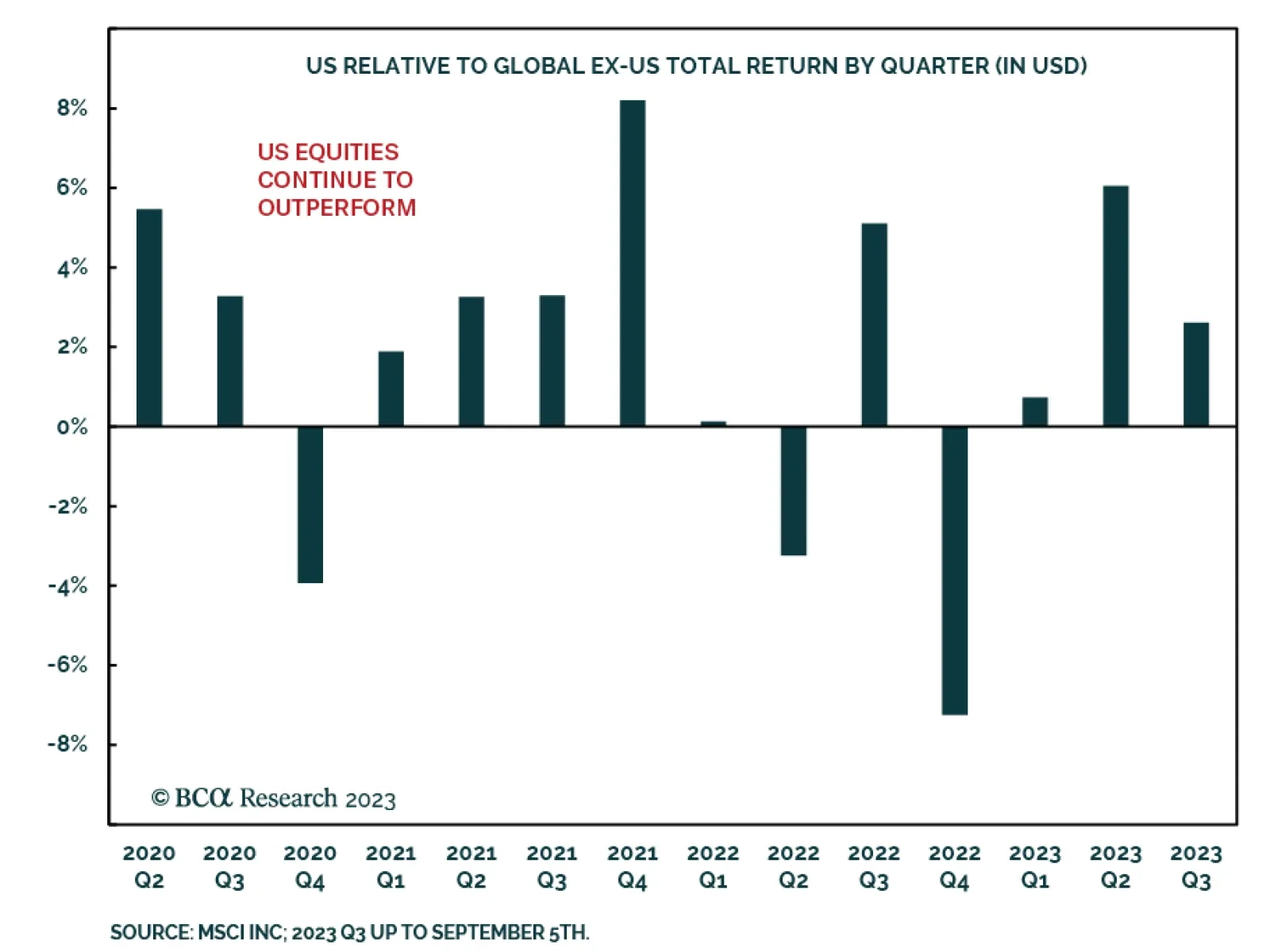

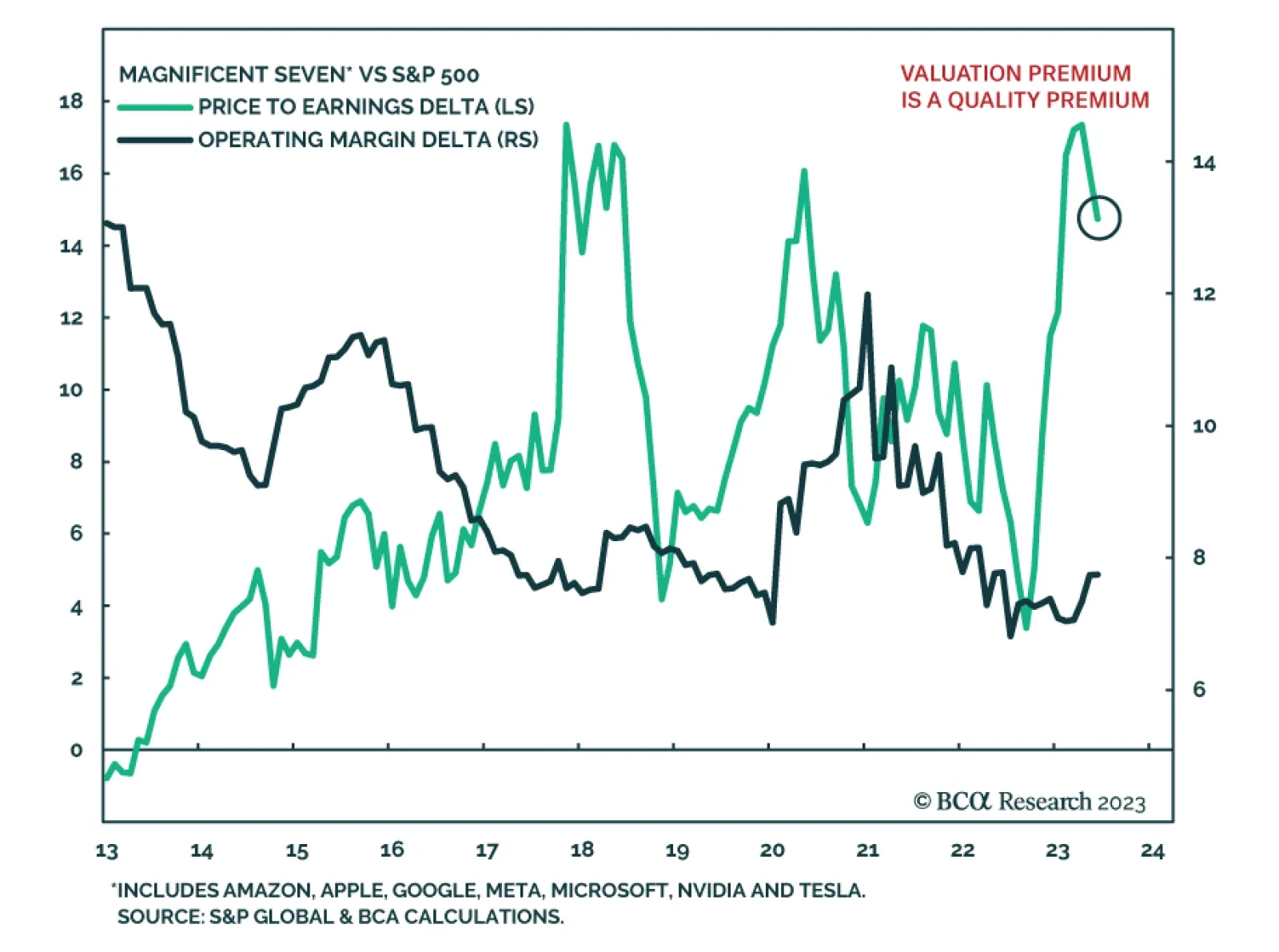

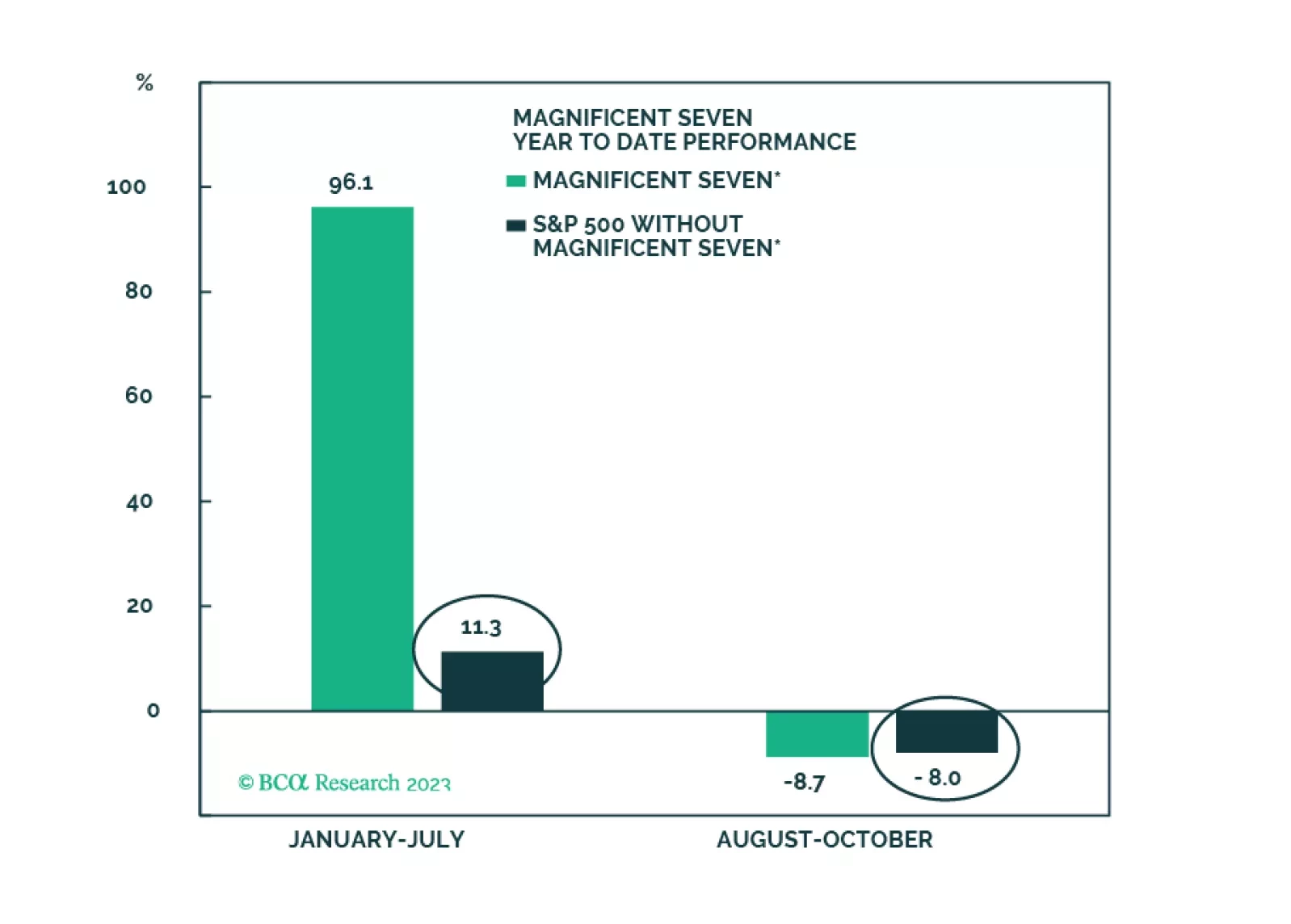

The Vicious Troika remains a long-term threat, but over the short term, rates will likely have another leg down on growth concerns, offering support to equities, which are now fairly valued and are no longer overbought. Longer-term outlook remains negative. The Magnificent Seven will likely lead a tactical rebound. Overweight Growth vs Value and FSemis.

Q3-2023 is expected to mark the end of the earnings recession for the past three quarters, opening the door to positive earnings growth. Whether that would be sustainable or will sputter once the recession settles in as expected in 2024 remains to be seen. However, much of earnings growth is already priced in.

Aggressive monetary tightening has always led to recession, although the timing is uncertain. The effects of high interest rates are starting to be felt. Investors should stay risk off and buy government bonds as a safe haven investment with carry.

Bulls and bears have capitulated, and the majority of the clients surveyed expect a rangebound market in the near term. Our fair value PE NTM indicates that the S&P 500 is only modestly overvalued. The continued outperformance of the Magnificent Seven faces multiple hurdles. Meanwhile, fiscal spending is unlikely to create an impetus for another leg up in equity performance.

This Special Report is a timely reprise of a speech that I gave at the London School of Economics on our understanding and misunderstanding of generative AI. In neurological terms, generative AI has a ‘super-neocortex’ which means that it can thrash humans in abstract thinking, or IQ. But crucially, generative AI does not have a ‘limbic system’ which means that it will lag well behind humans in emotional intelligence, or EQ. I hope you find the speech insightful and provocative, especially on how we might have completely misunderstood human intelligence and super-intelligence, and the economic and societal implications for the coming decade.