Trade

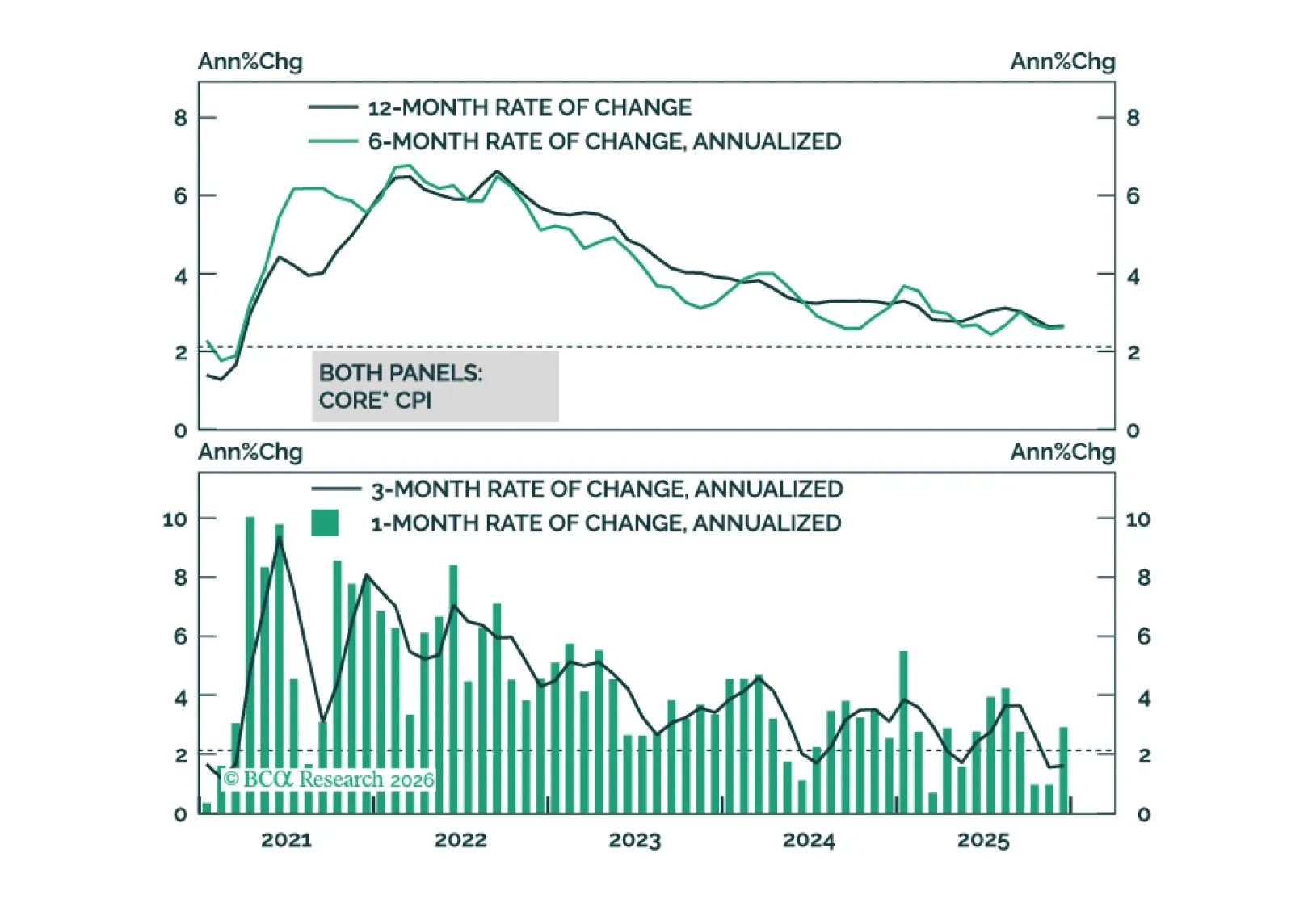

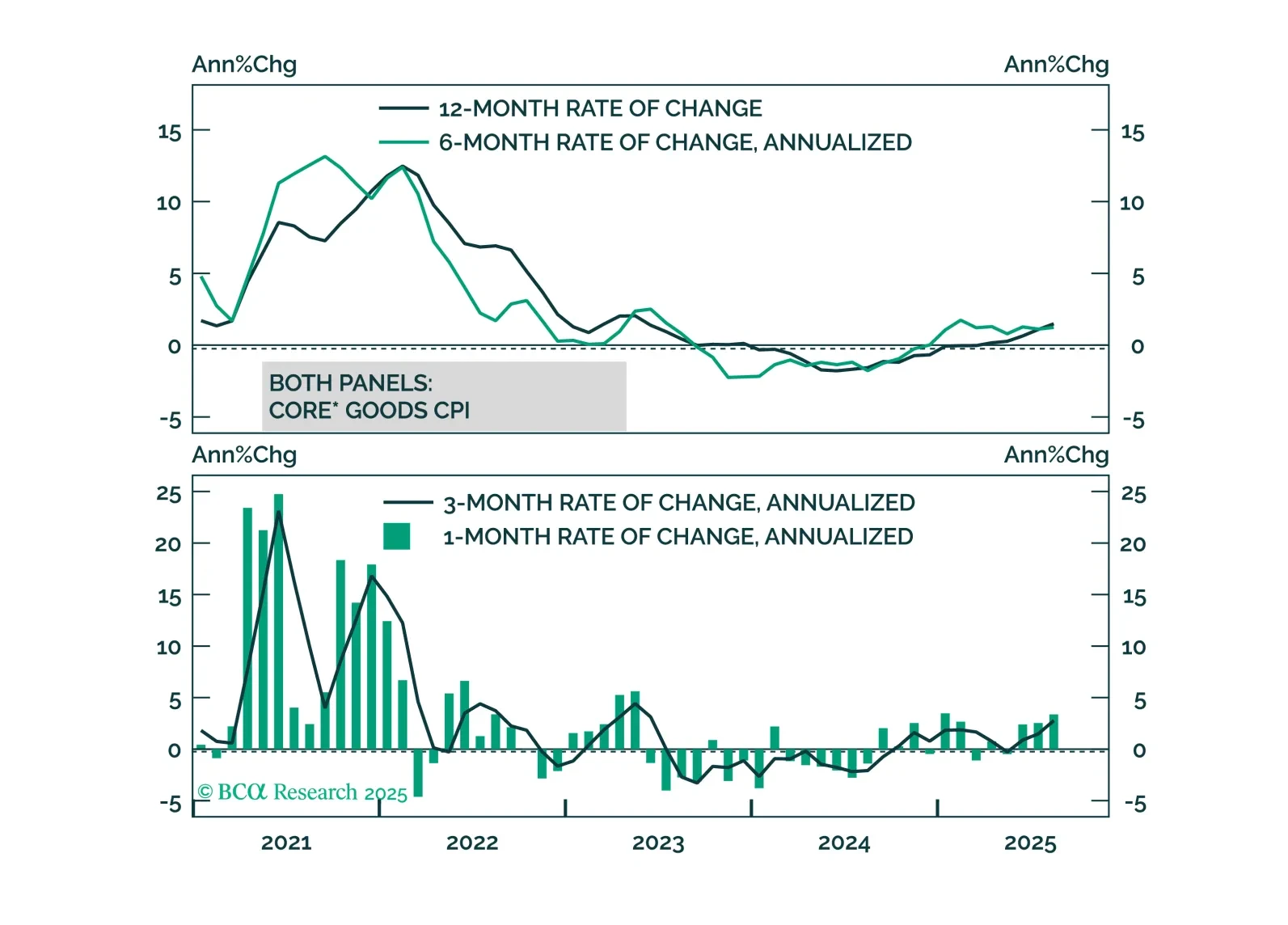

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

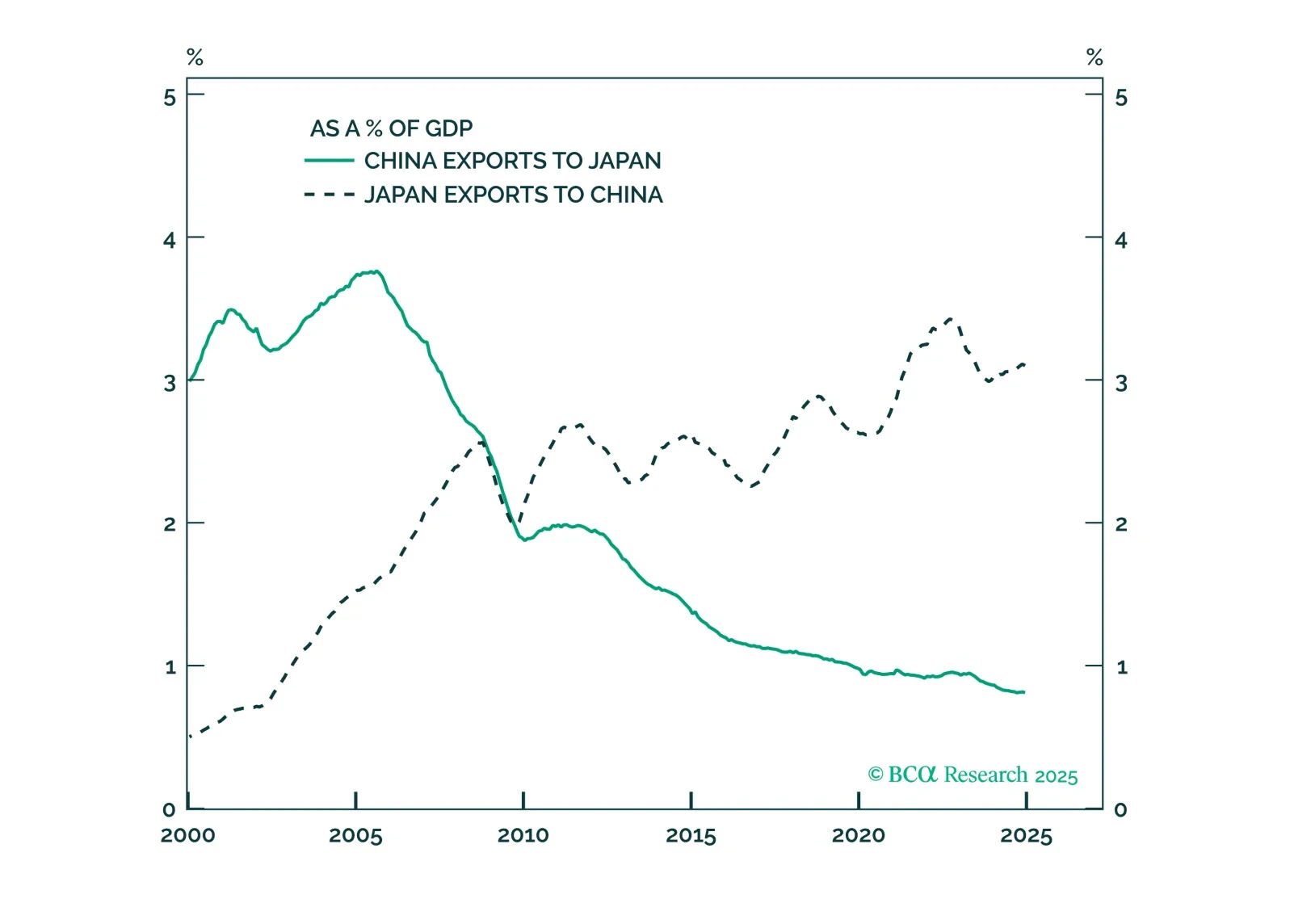

US talks with Russia and China coincide with rising EU-Russia and Japan-China tensions. Stay overweight US assets and long Japanese yen.

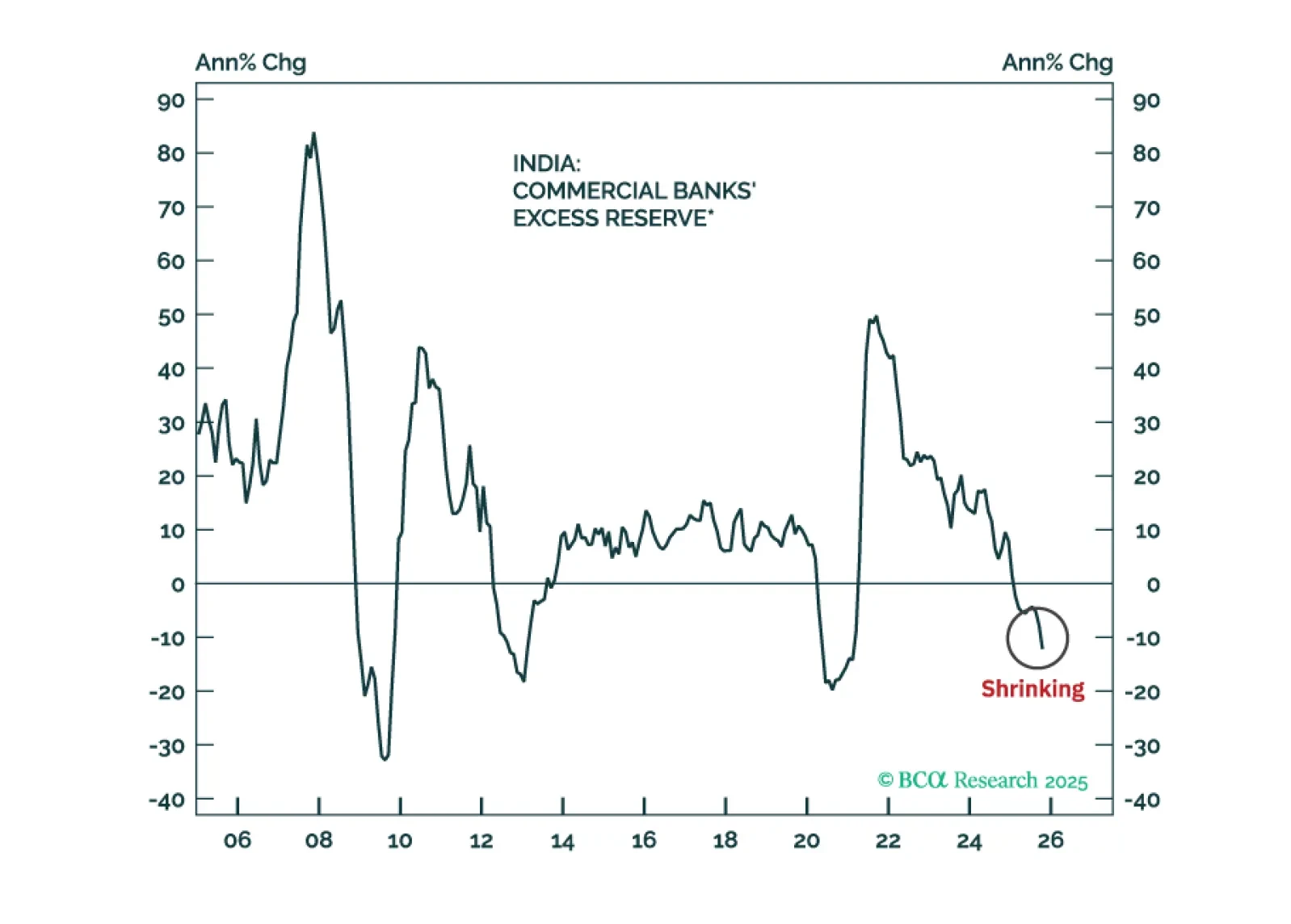

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

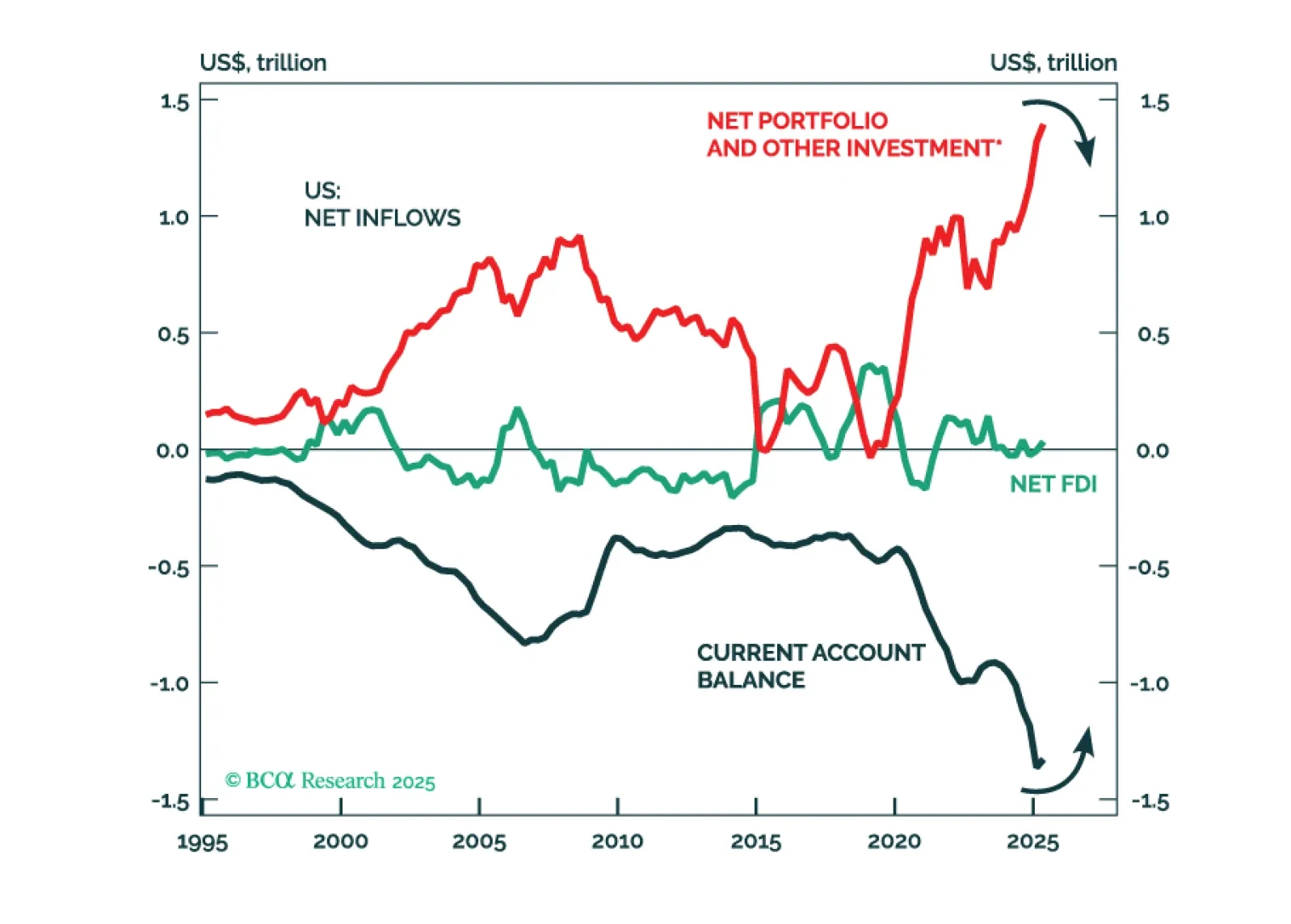

The belief that net portfolio outflows out of the US will fuel EM assets is a common but misguided narrative. If the US starts experiencing net capital outflows, it would need to run a current account surplus. A shift in the US current account from deficit to surplus would be devastating for the global economy in general and EM in particular.

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

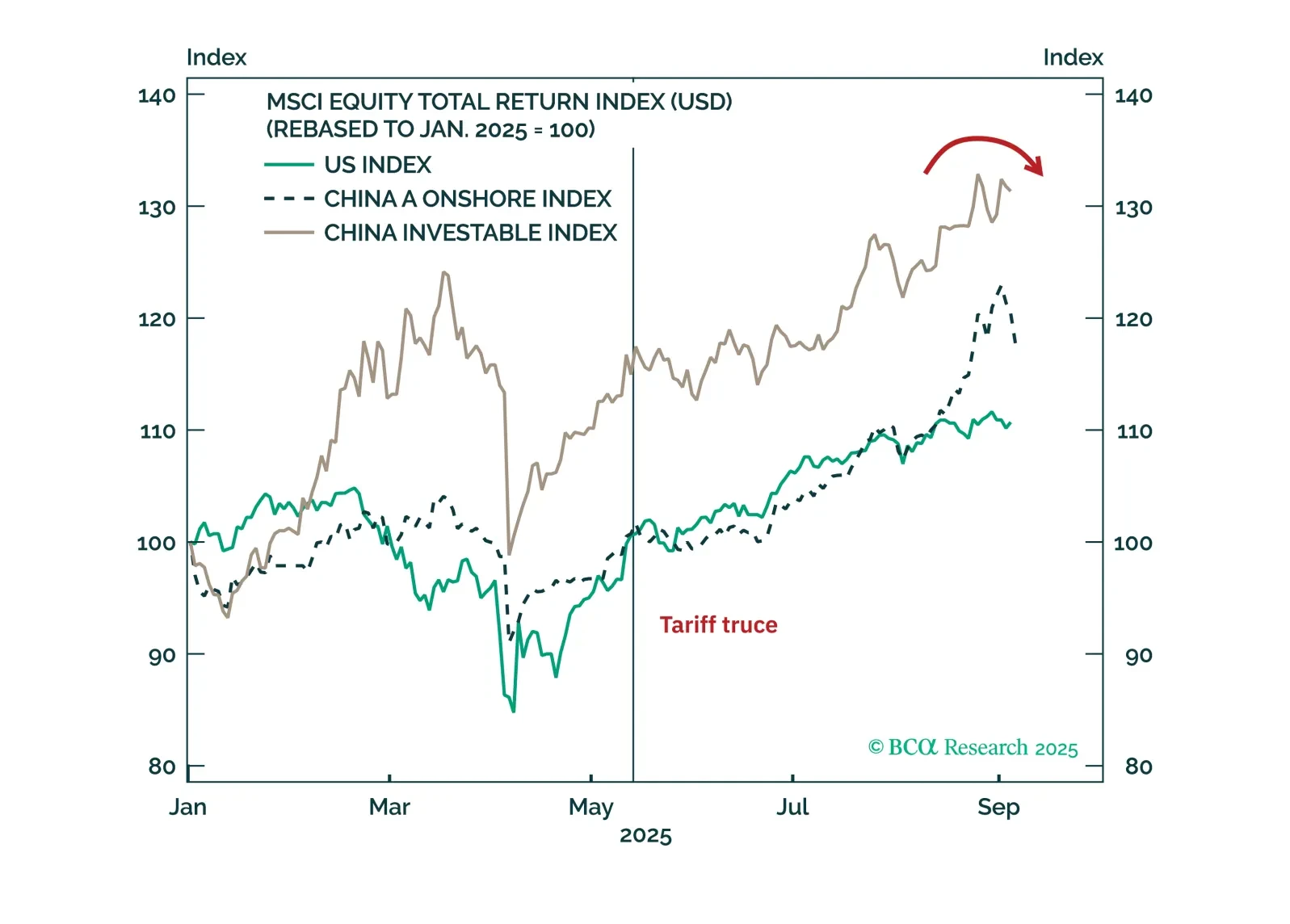

Investors will be disappointed if they buy into the China rally and then Russia escalates the war in Ukraine.

Our Portfolio Allocation Summary for September 2025.

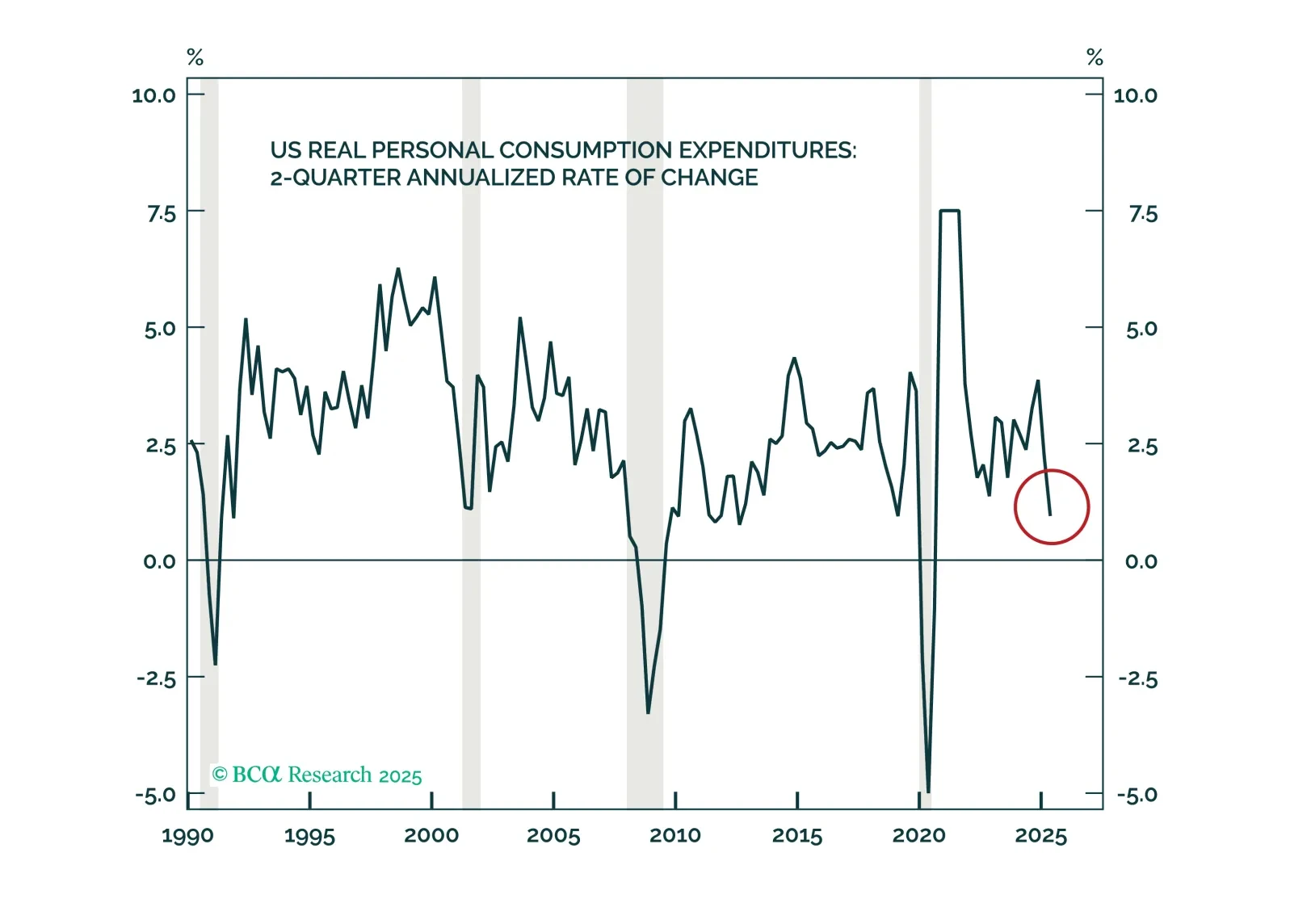

Economic activity plainly slowed in the first half, led by decelerating consumption and payrolls growth, but financial markets didn’t care. If the next two weeks of data don’t indicate that the May-June slowdown stretched into July and August, we will likely drop our defensive recommendations.

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.