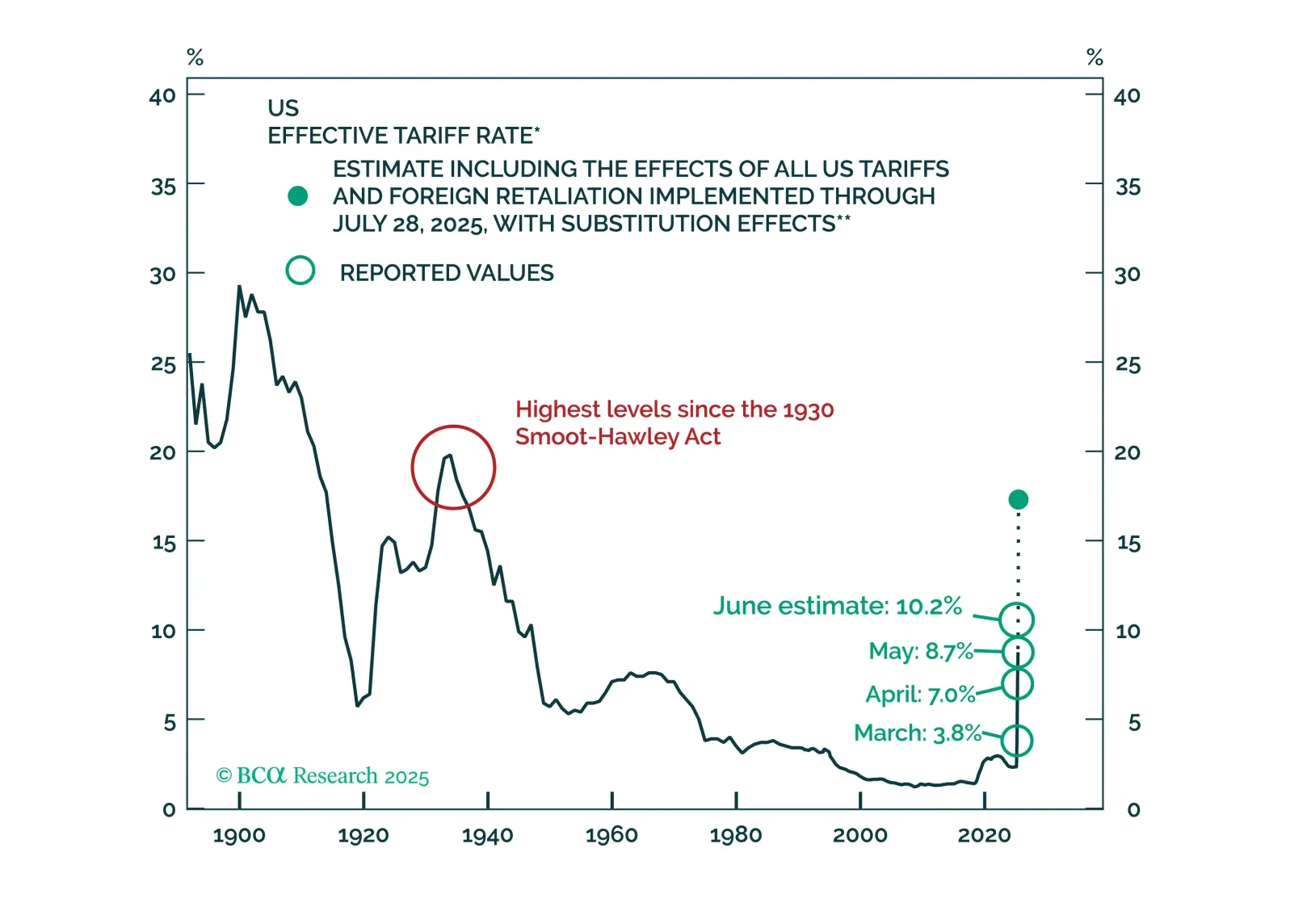

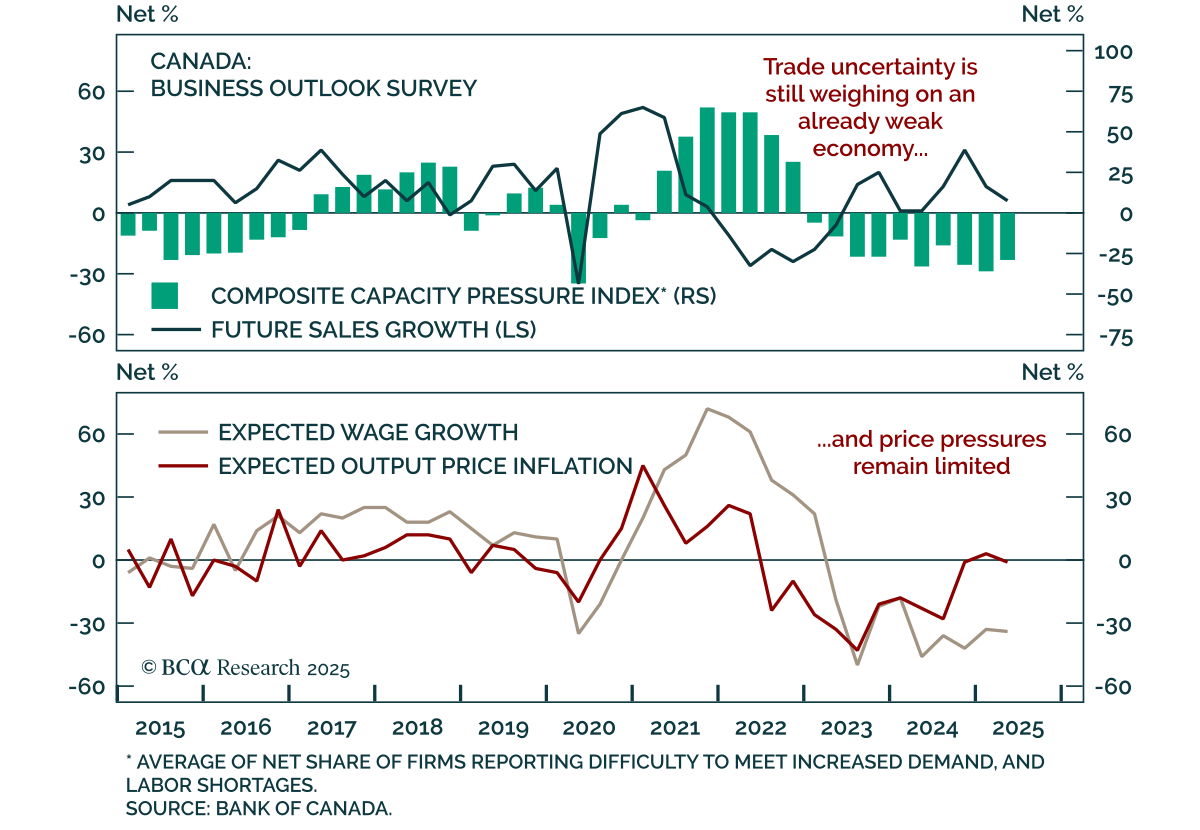

Trade

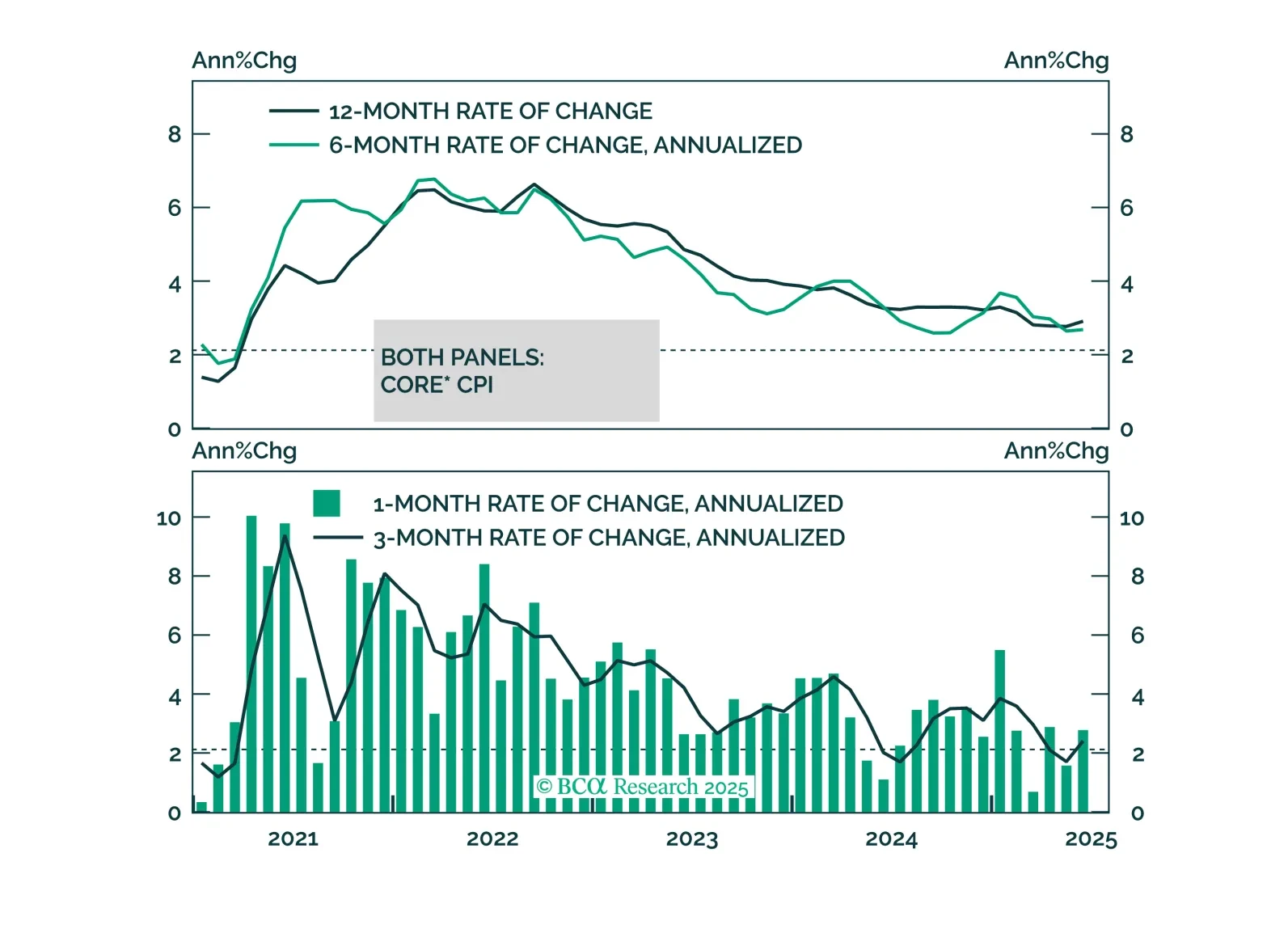

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

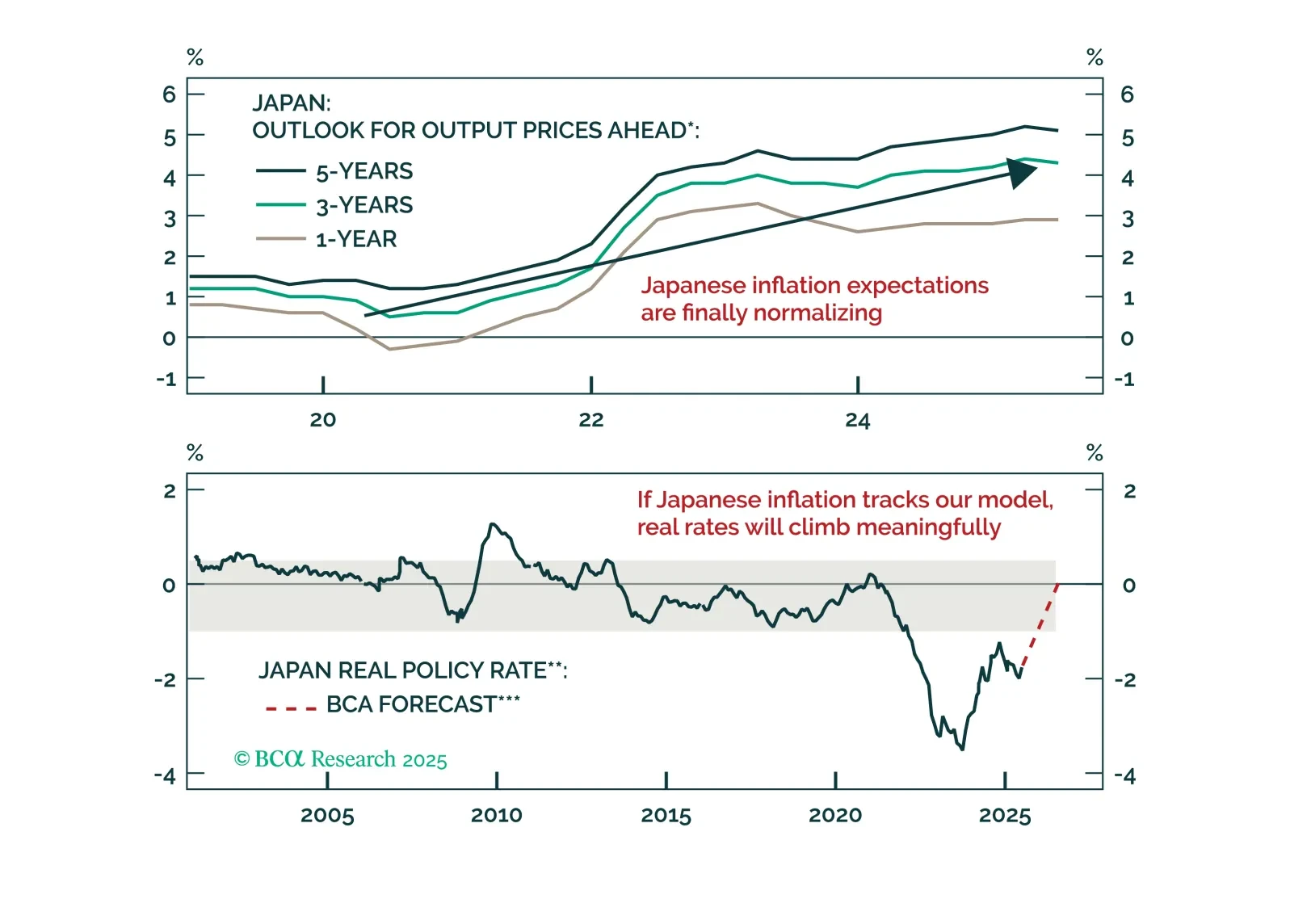

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

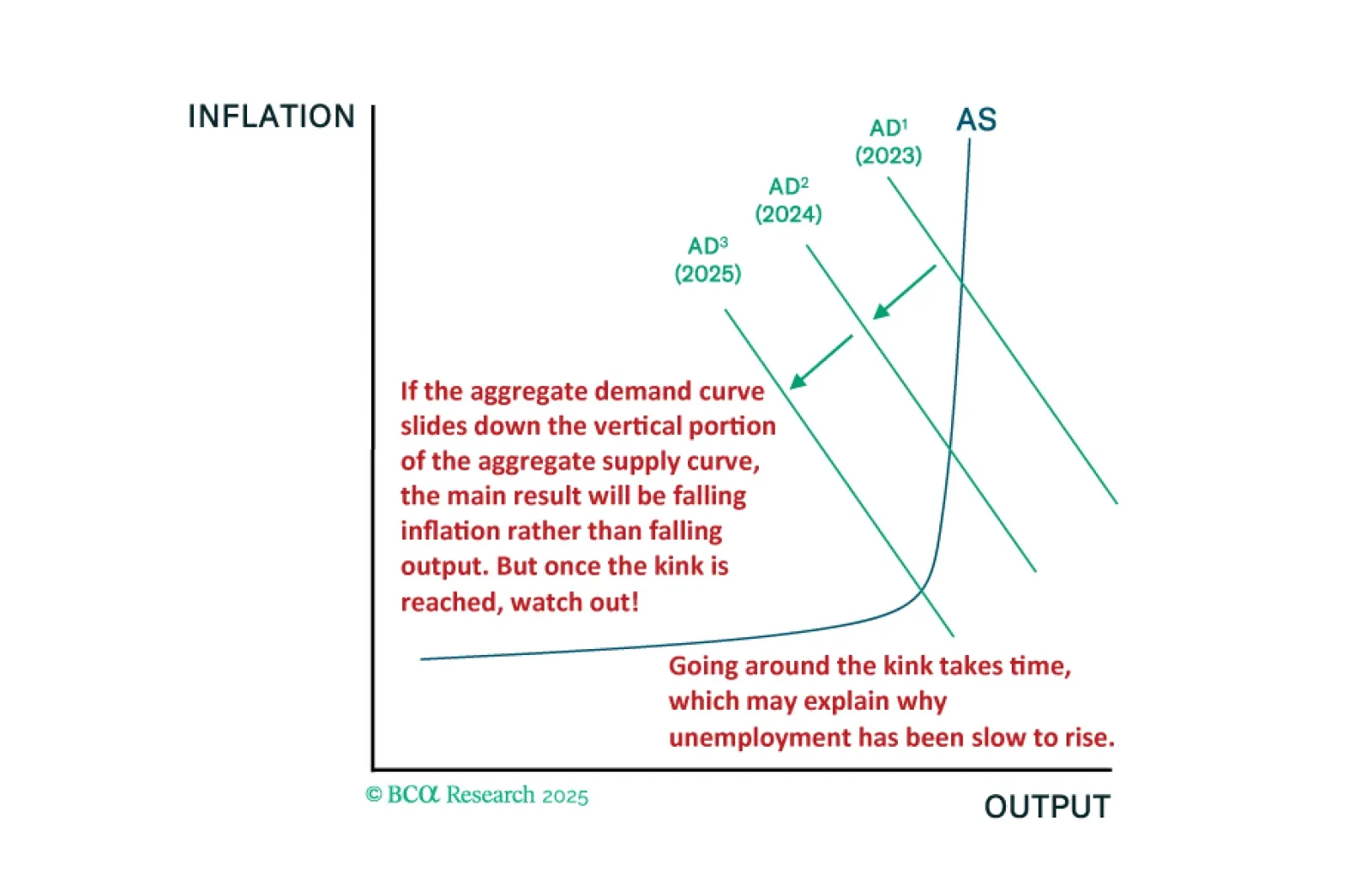

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

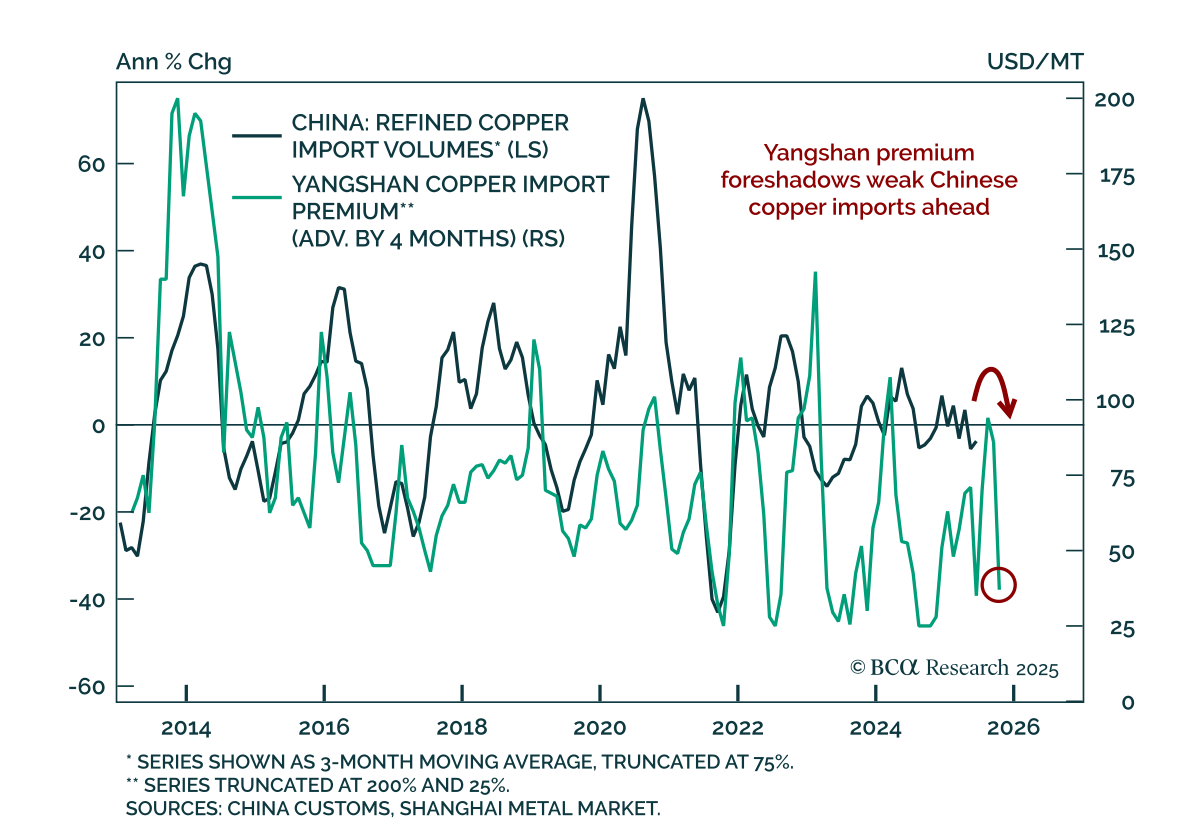

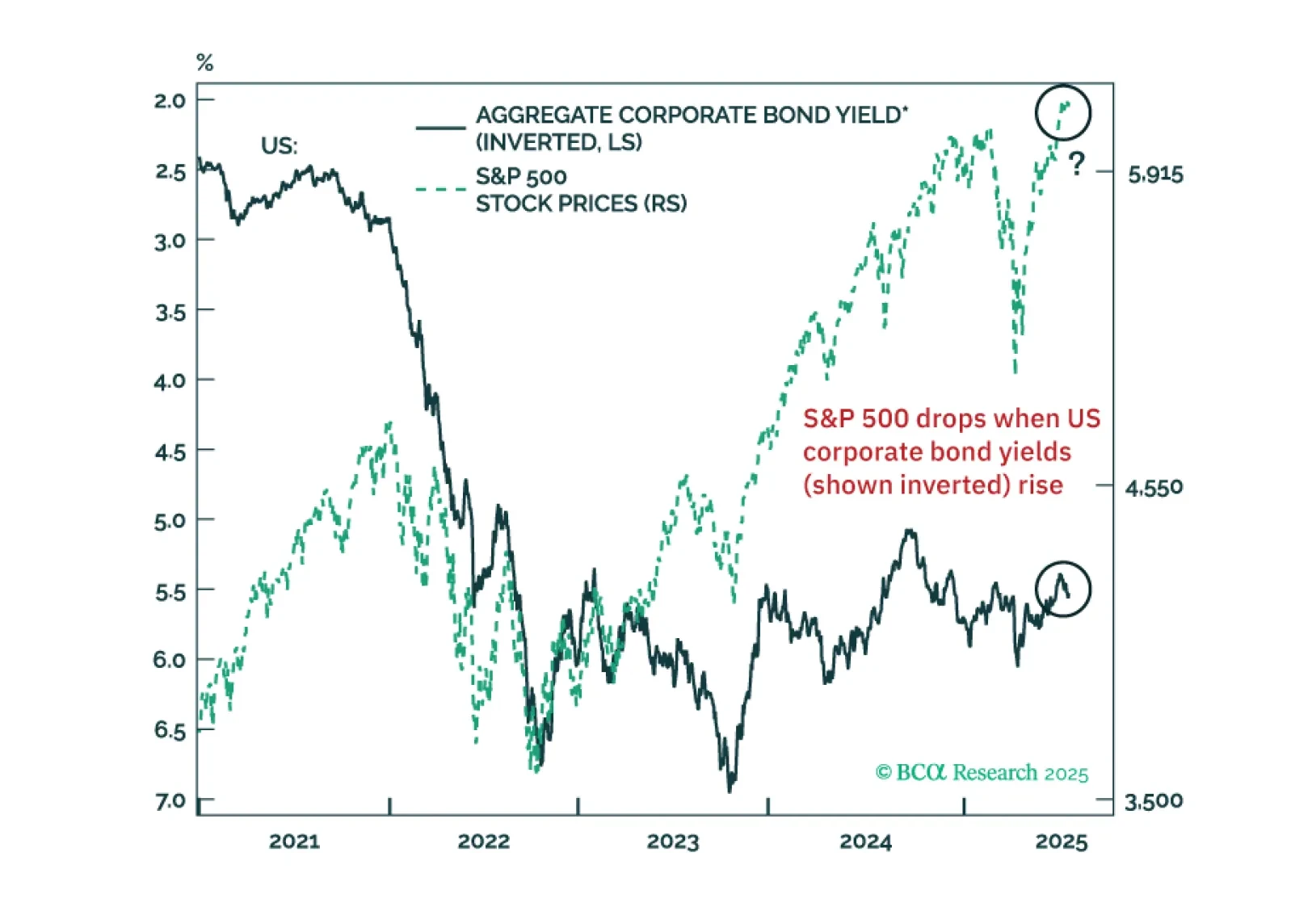

US equity investors should heed warning signals from US corporate bond yields. There are early red flags for EM share prices. Global trade will shrink in H2 2025. China’s economic tailwinds from H1 2025 – fiscal and export frontloading – are coming to an end.

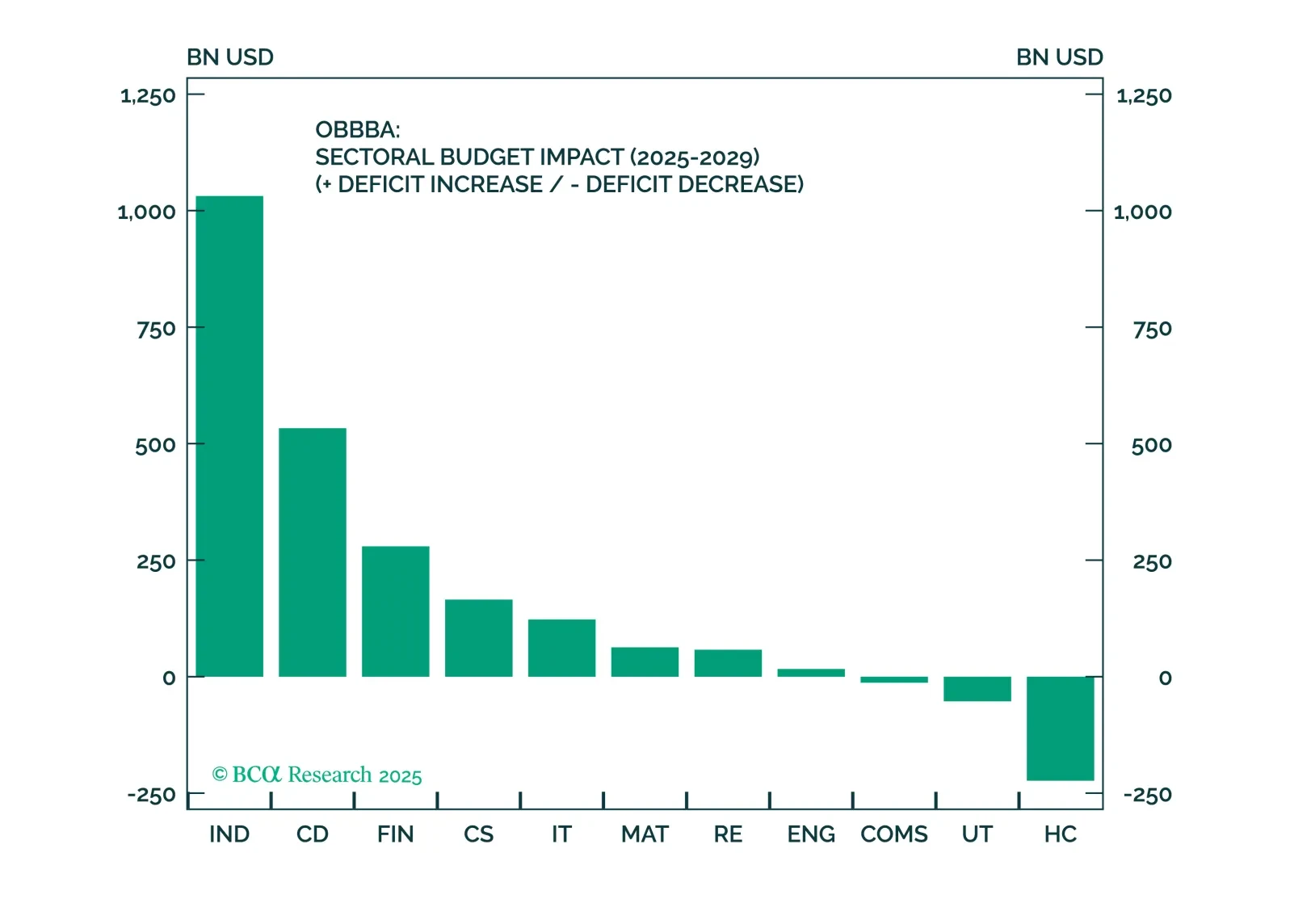

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.