Trade

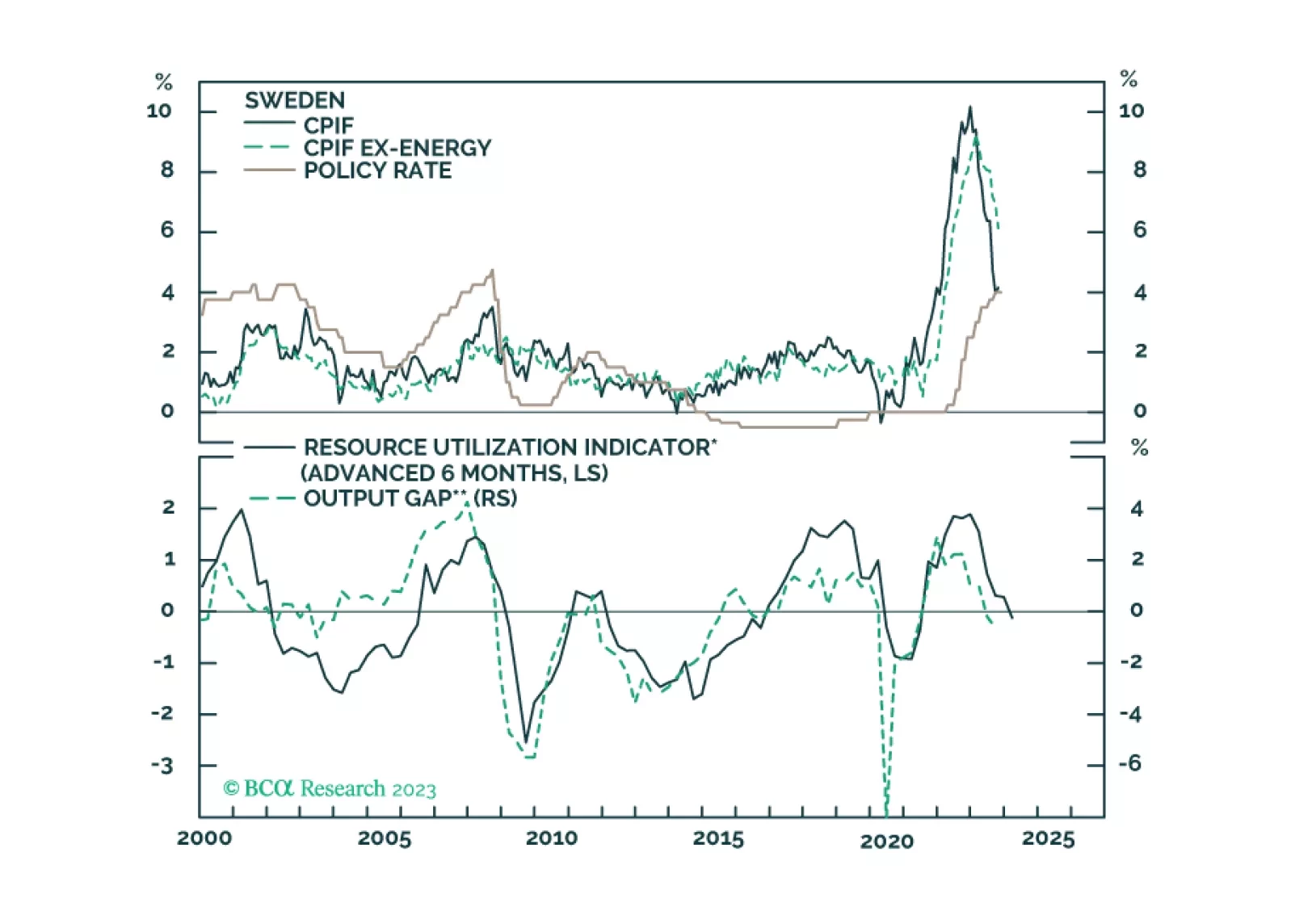

This report looks at the prospects for the Swedish krona, following the pause by the Riksbank.

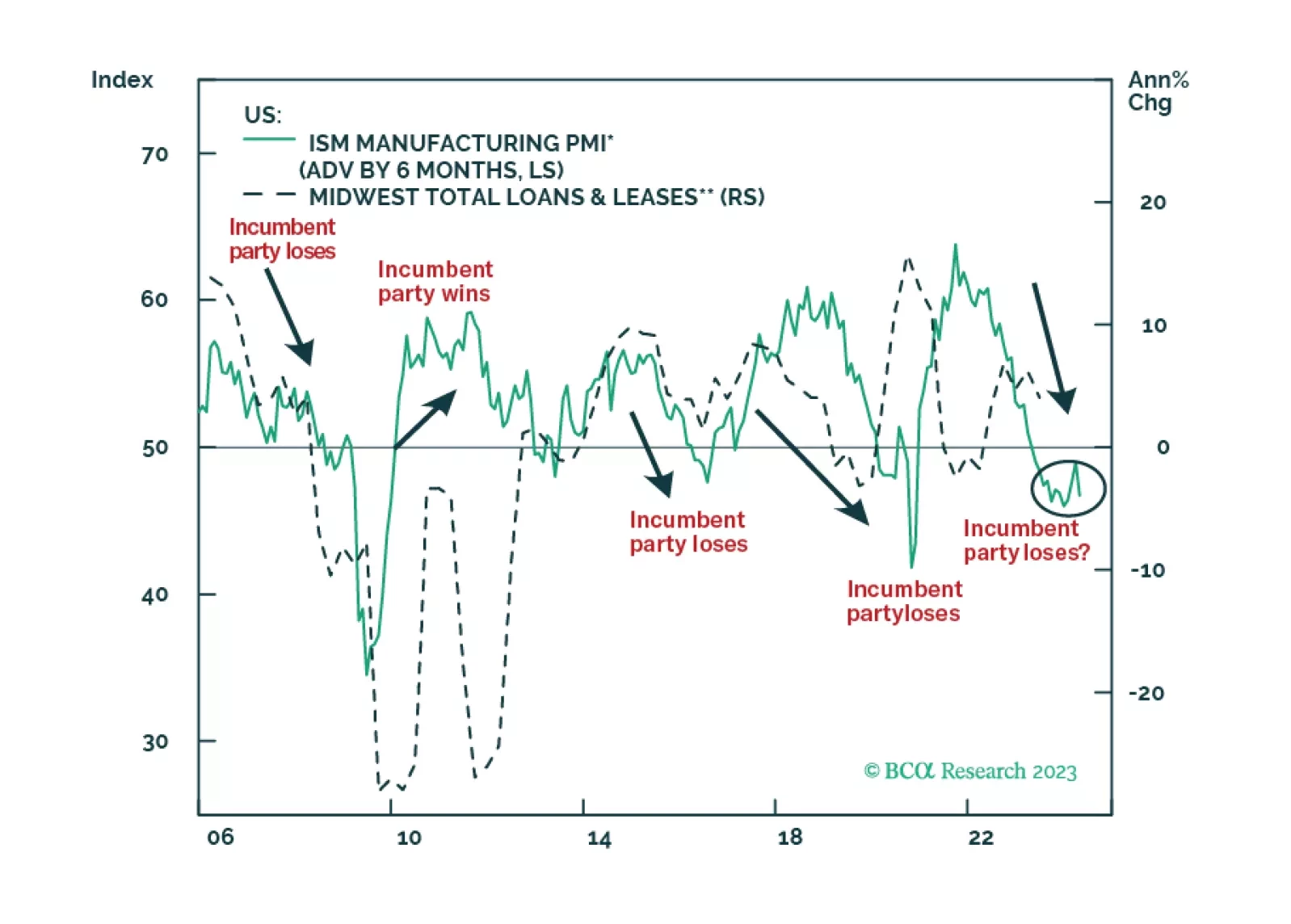

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

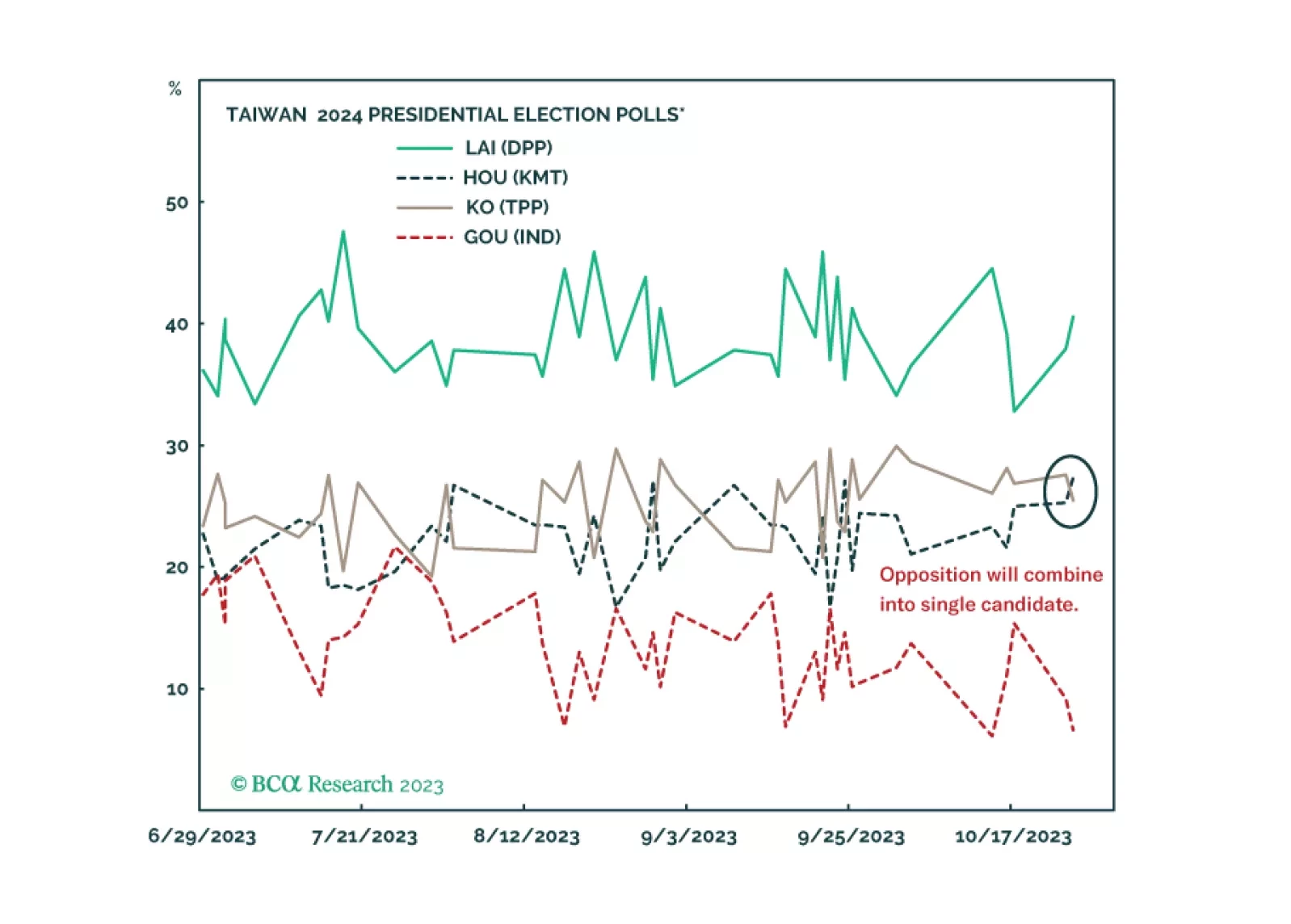

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.

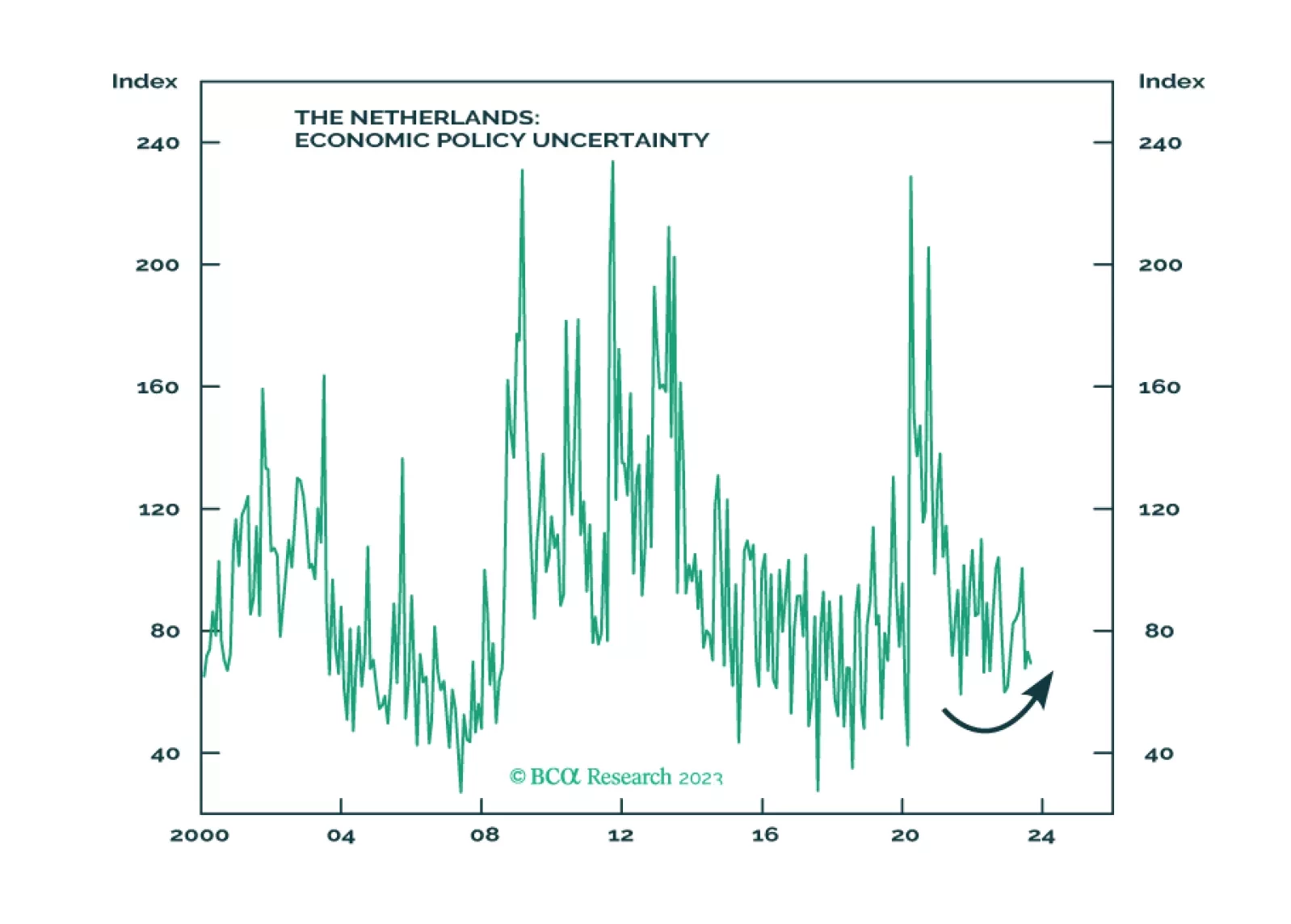

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

US fiscal, monetary, and foreign policies are unlikely to deliver any dovish surprises for investors in Q4, due to the impending government shutdown, persistent inflation, and instability among OPEC+ and China.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

Stocks perform worse in presidential election years than average years, especially in the first half of the year, and especially if the ruling party ends up falling from power. Investors should take risk off the table until the unemployment rate peaks.

The Fed and ECB talked a good game as they redoubled their commitments to returning core inflation to 2% p.a. at Jackson Hole. However, their outmoded inflation-fighting playbooks do not address supply tightness in commodity and energy markets, which keeps inflation risk elevated. The proposed expansion of the BRICS states seeks to capitalize on these trends, and supports efforts to weaken the centrality of the USD in global trade. We remain long commodity exposure via ETFs to retain exposure to energy and metals producers and refiners.