Trade / BOP

This week, we cover the main questions we fielded during our latest client trip in Europe. Among the many topics broached are Europe’s recession odds, the impact of China’s stimulus, and the outlook for European markets.

Regular readers are familiar with our expectations for a global recession over the cyclical investment timeframe. A global downturn is overwhelmingly bearish for oil demand. The supply side, on the other hand, is simultaneously facing the threat of supply…

The JPM Global manufacturing PMI declined at an accelerating pace in September (49.6 to 48.8). Moreover, international trade flows deteriorated notably with the new export orders component falling from 48.4 to 47.5. A sector breakdown underscores broad-based…

Export dynamics from small open economies are a good bellwether for global growth conditions. Taiwan export orders accelerated from 4.8% y/y to a faster-than-anticipated 9.1% in August. The faster pace of growth was also broad-based among the country’s…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. Overall exports, which are highly volatile on a month-on-month basis, decelerated at a…

Chinese export growth in USD terms accelerated from 7.0% y/y to a larger-than-expected 8.7% in August. China’s exports to its major trading partners (US, EU and ASEAN) were all growing in August on a year-on-year basis, though at a decelerating pace in the US…

According to BCA Research’s GeoMacro Strategy service, while the idea that Donald Trump would allow China to build factories in the US does not mesh with the contemporary media narrative, it would fit the historical track record. The last time that the US had…

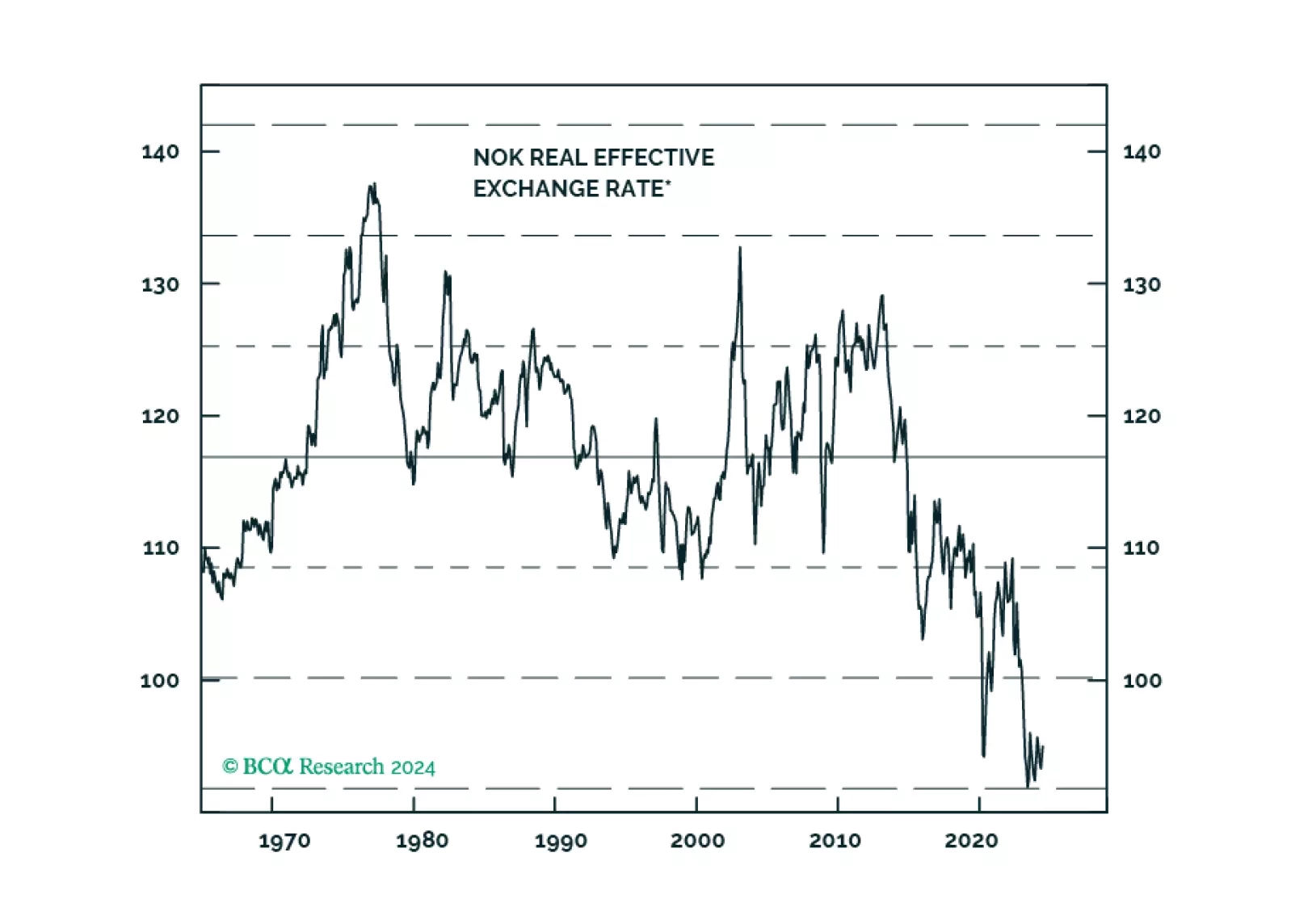

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

Indonesian stocks have sold off sharply and underperformed their EM and emerging Asian peers – both in local currency and in common currency terms – despite the nation’s 5.1% real GDP growth rate (the highest rate among G-20 countries, second only to India).…

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.