Trade Policy/Protectionism

The US-China trade truce is getting bigger and better, but a grand strategic bargain on Iran and Taiwan is not happening.

The Trump-Xi summit continued the trade truce and tentatively created a framework to contain tensions over 2026. That is not a trade deal but it is good enough for global financial markets, especially Chinese assets.

Reduce risk exposure in the very near term as President Trump's ceasefire effort falters, Russia tensions spike, and US-China trade prospects suffer.

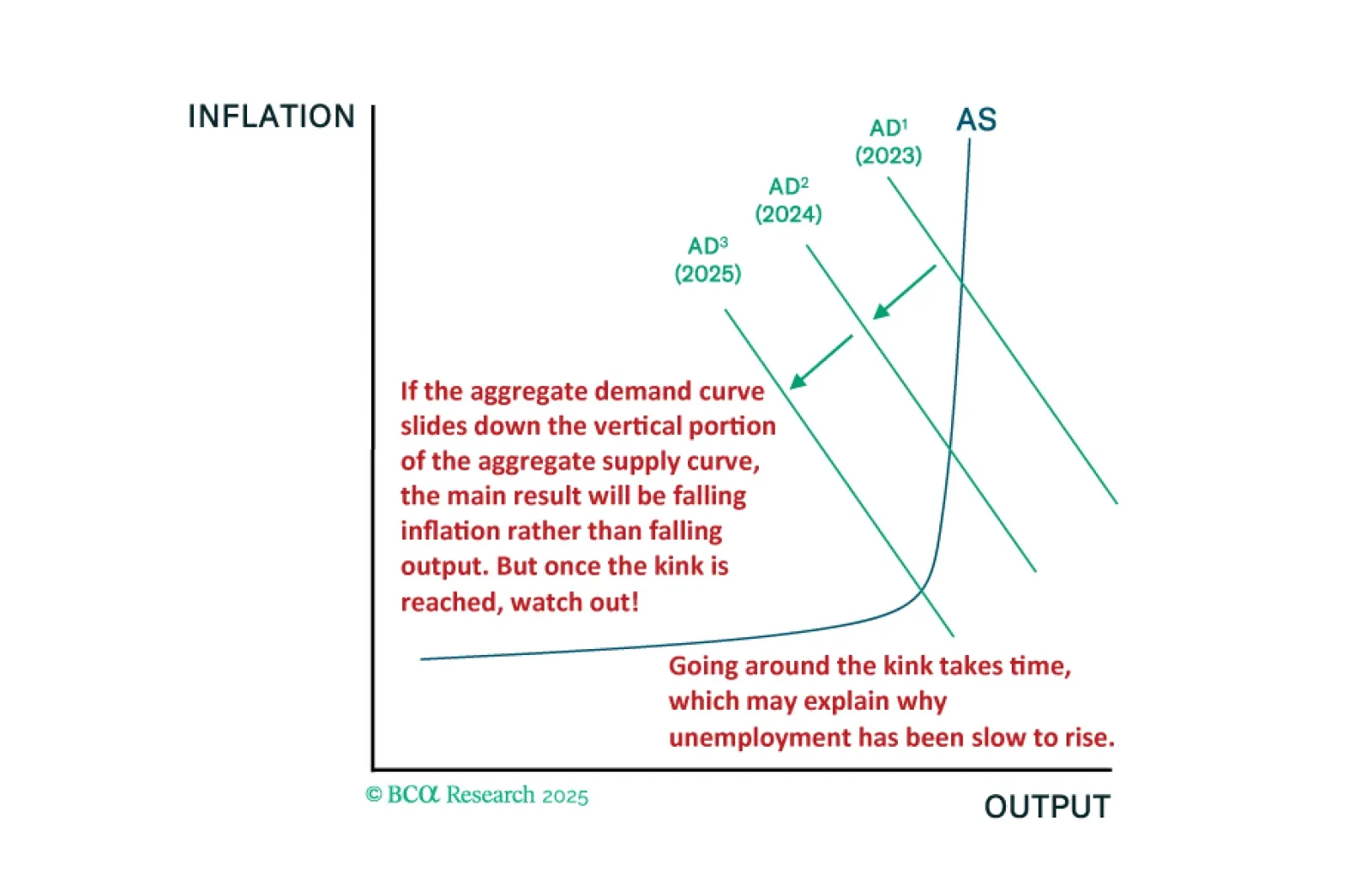

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

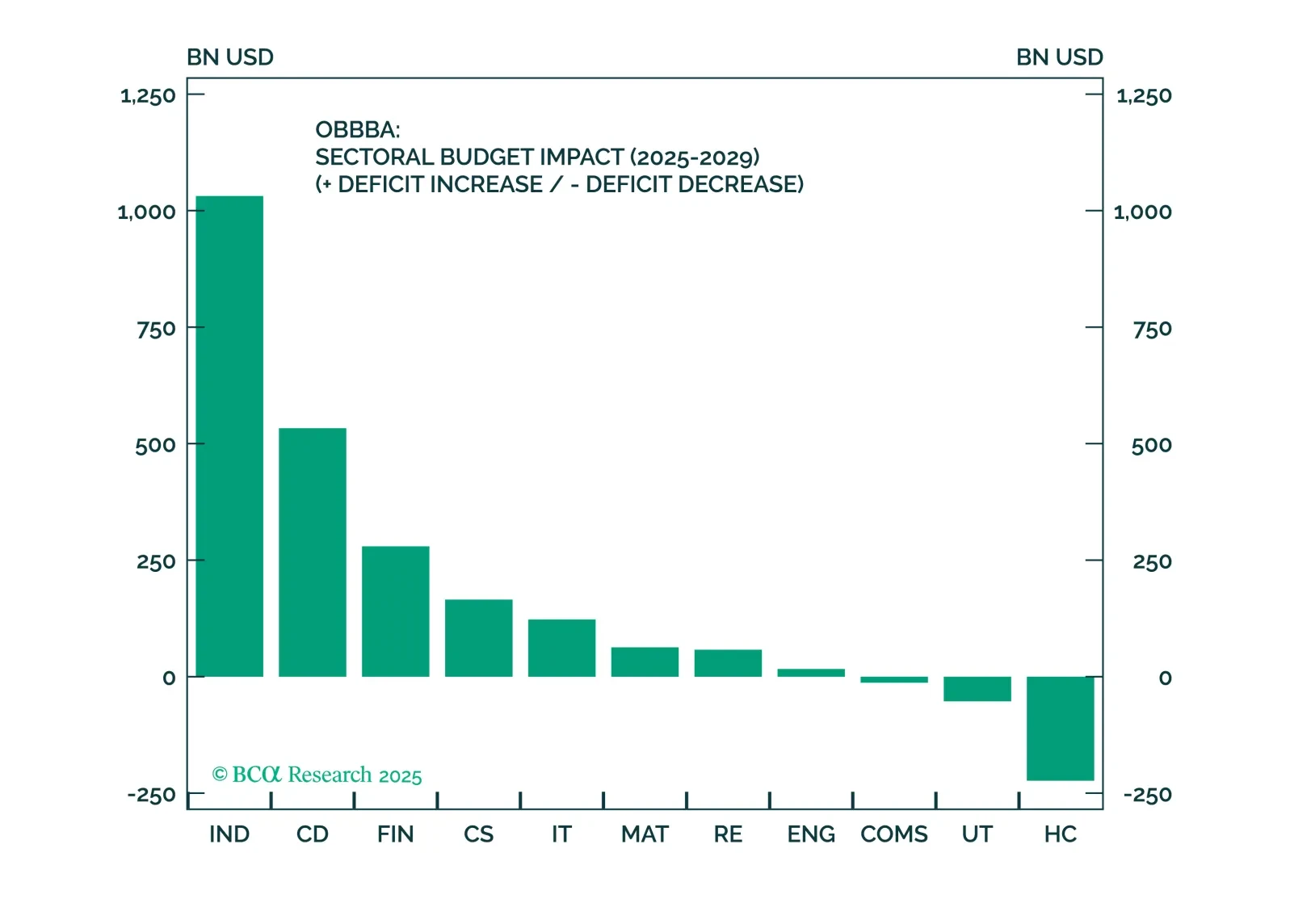

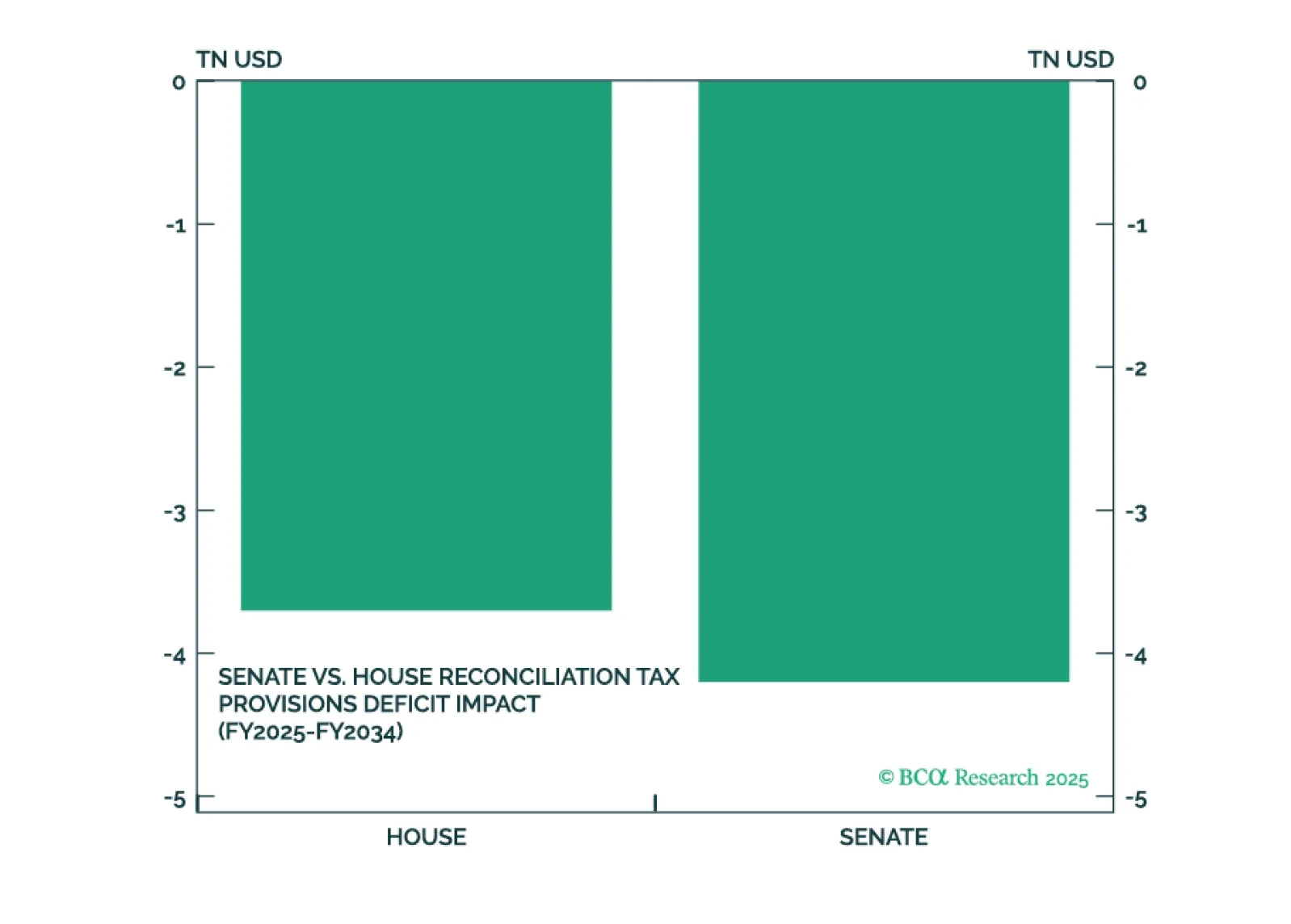

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

President Trump’s big beautiful bill will pass but faces near-term hurdles and will not tighten the government’s belt. It will combine with renewed tariff implementation to generate near-term risk for both the bond and stock market. The Iran crisis fizzled, saving Trump from a major oil shock that could have derailed his second term.