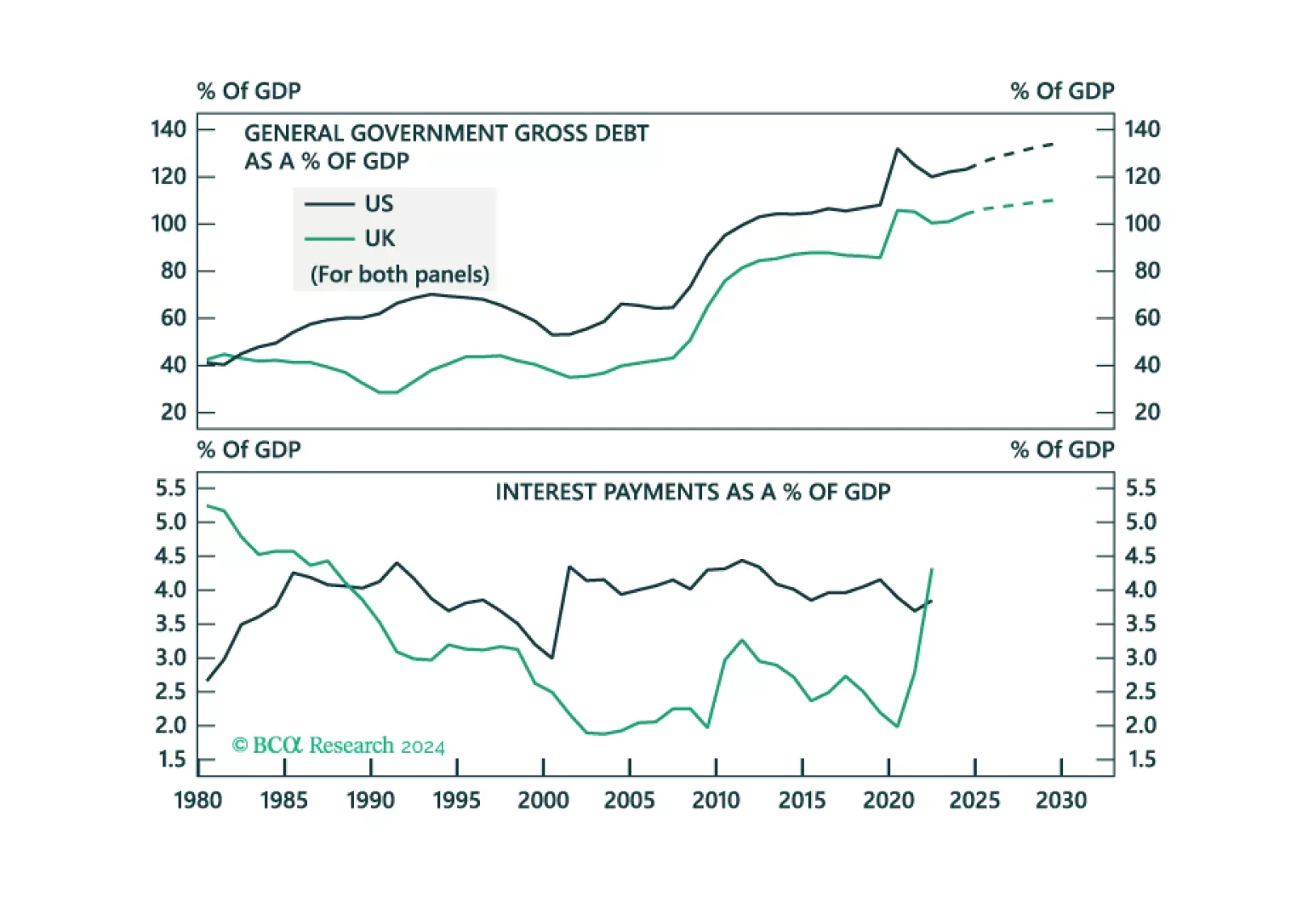

UK

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

In this Insight, we assess whether investors should expect fiscal turbulence in the UK, that will drive UK yields higher and the pound lower.

Our Q3 portfolio was defensive, which we believe will be the appropriate stance in the next six-to-twelve months. Data coming out of the US has remained robust which could cause US bond yields to temporarily overshoot. An overshoot in US bond yields will be an opportunity to dial up the portfolio’s defensive tilt. The average decline in 10-year Treasury yields 12 months after the first Fed rate cut is 100 bps. This time should be no different. There are not many changes to this quarter’s portfolio allocation. We have upgraded UK gilts to overweight and downgraded European credit to underweight. Portfolio duration remains the same. In terms of future changes, we are generally watching the trend in inflation given many central banks are delivering jumbo rate cuts. Any pause in the disinflationary trend we have seen will send bond yields soaring. This is a risk to our view. Otherwise, a recession in the first half of 2025 will cement our long duration stance.