UK

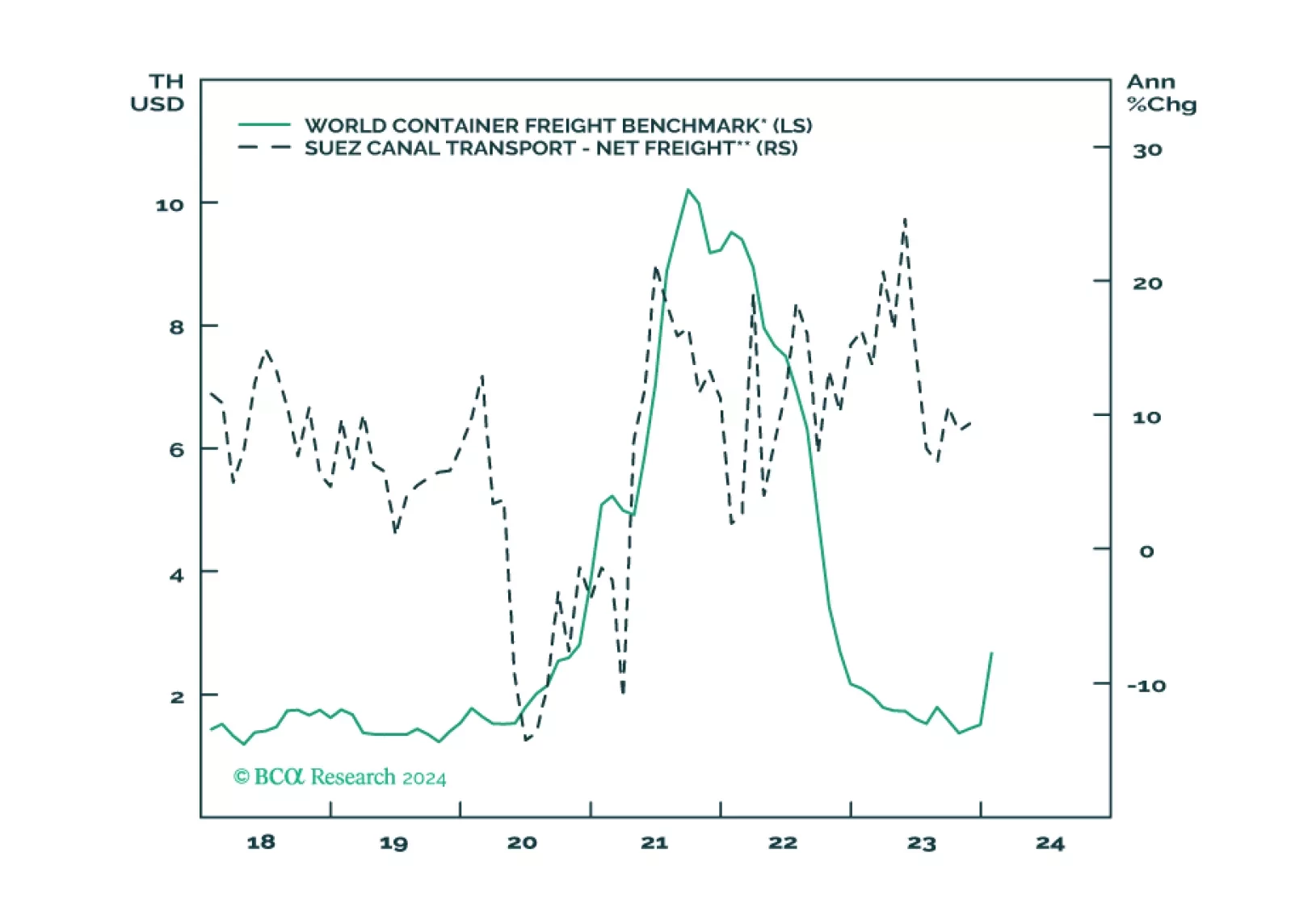

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

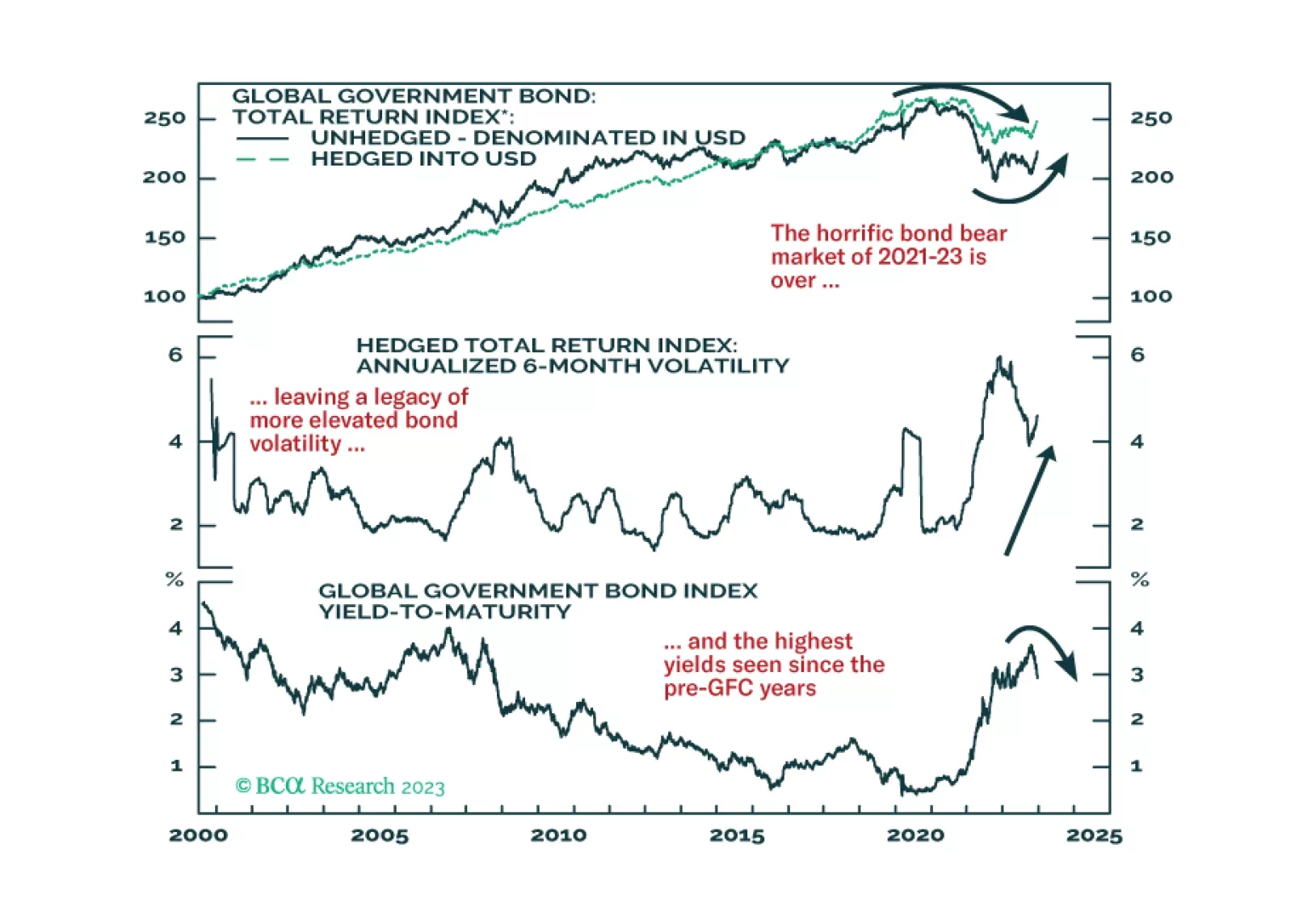

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

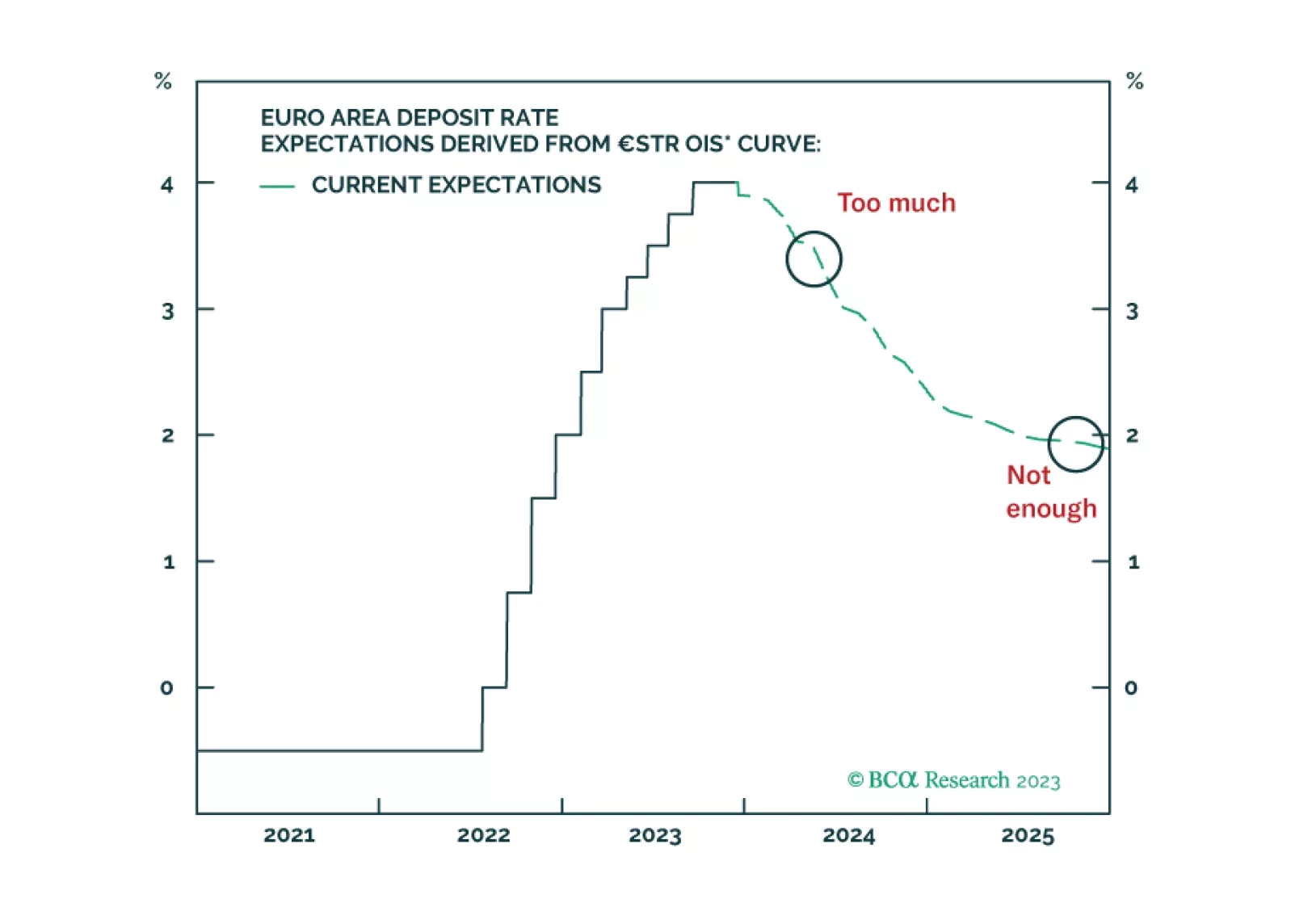

Explore the eight main themes that will drive the returns of European assets in 2024.

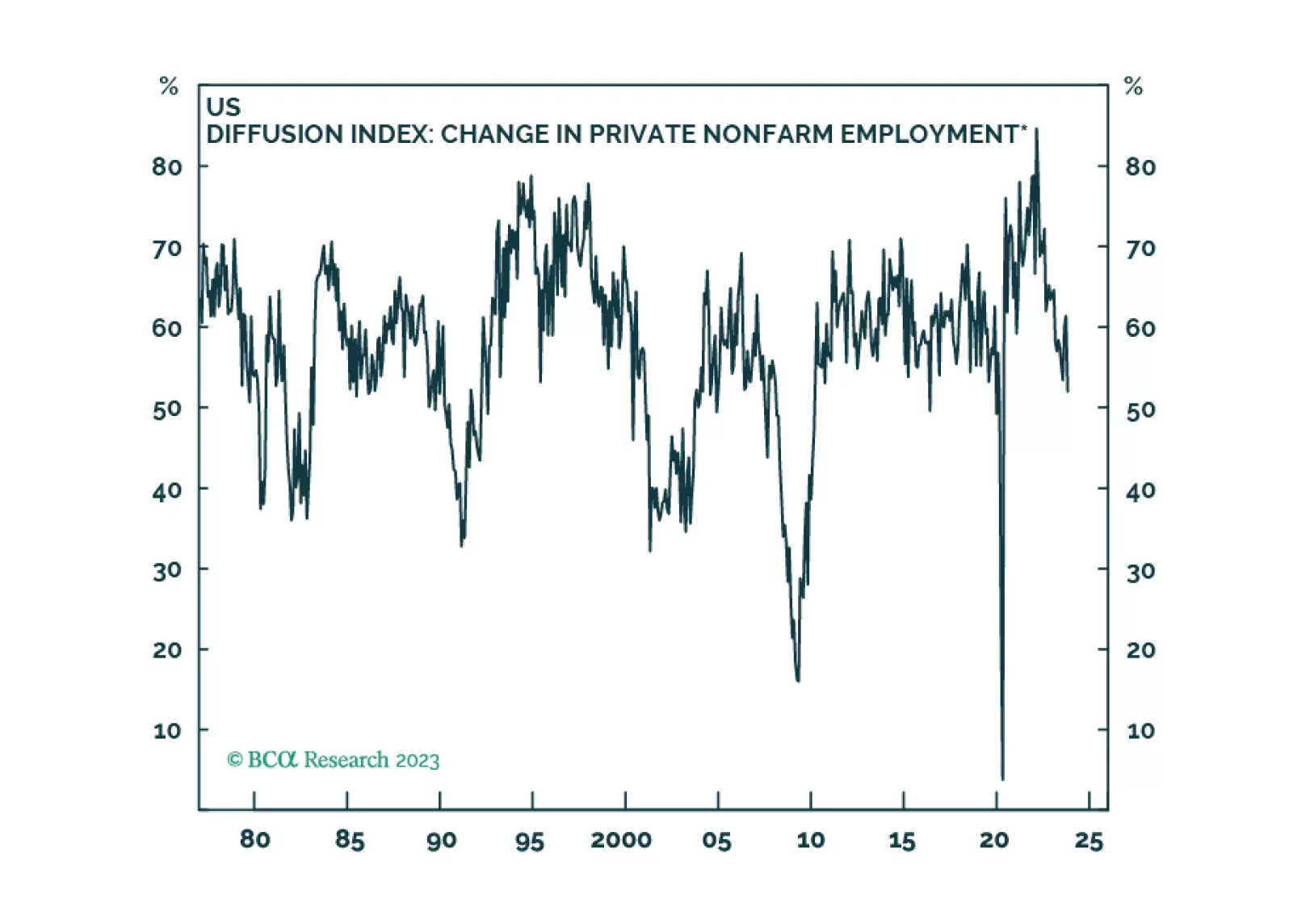

Labor markets are softening in most developed economies, as is usually the case in the lead-up to recessions. Our base case is that the global recession will begin in the second half of 2024, but we will be monitoring our MacroQuant model on a daily basis for confirmation.

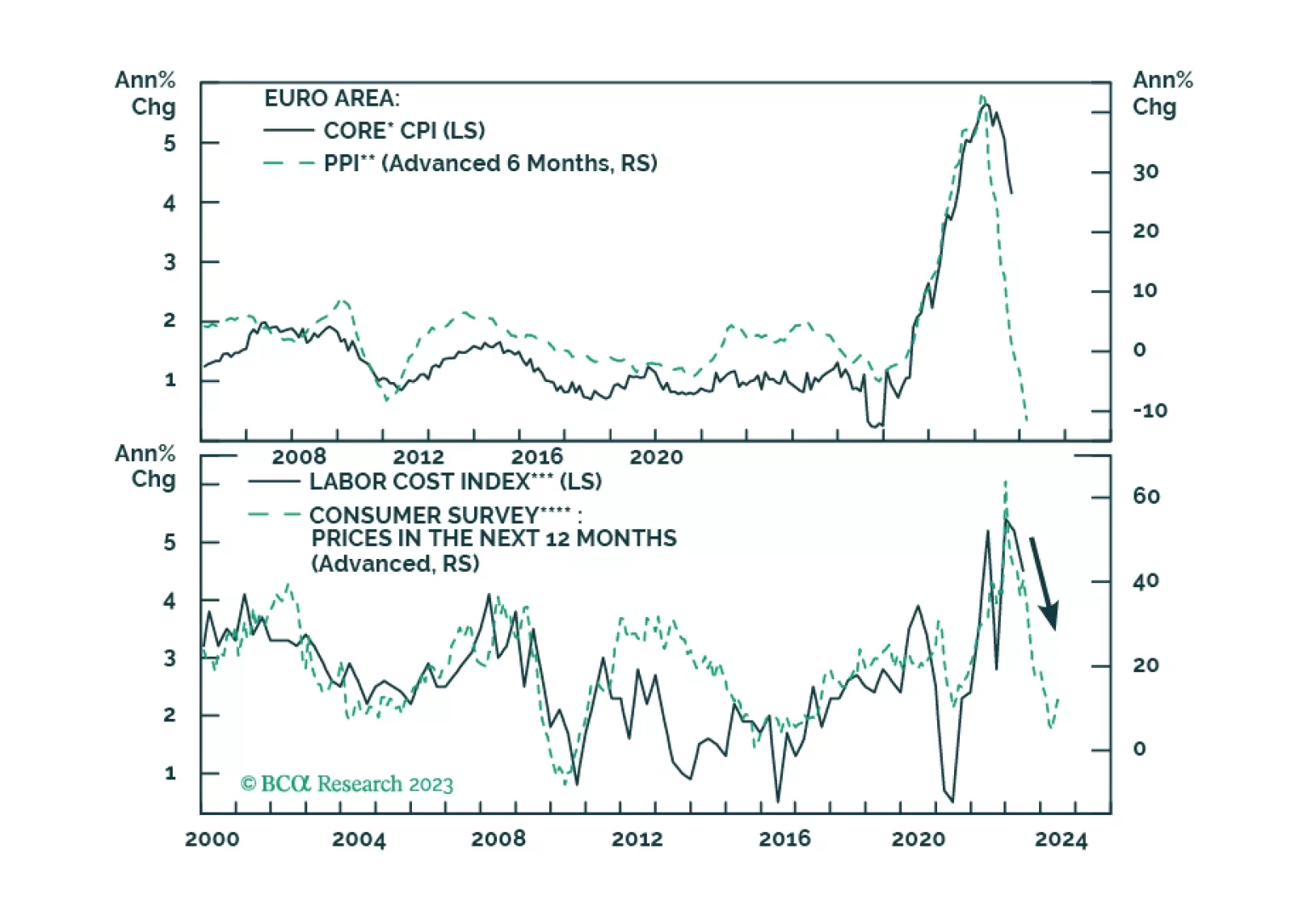

The Eurozone’s inflation will continue to slow over the coming months. While this trend will help Bund prices, will it boost the appeal of European equities?