UK

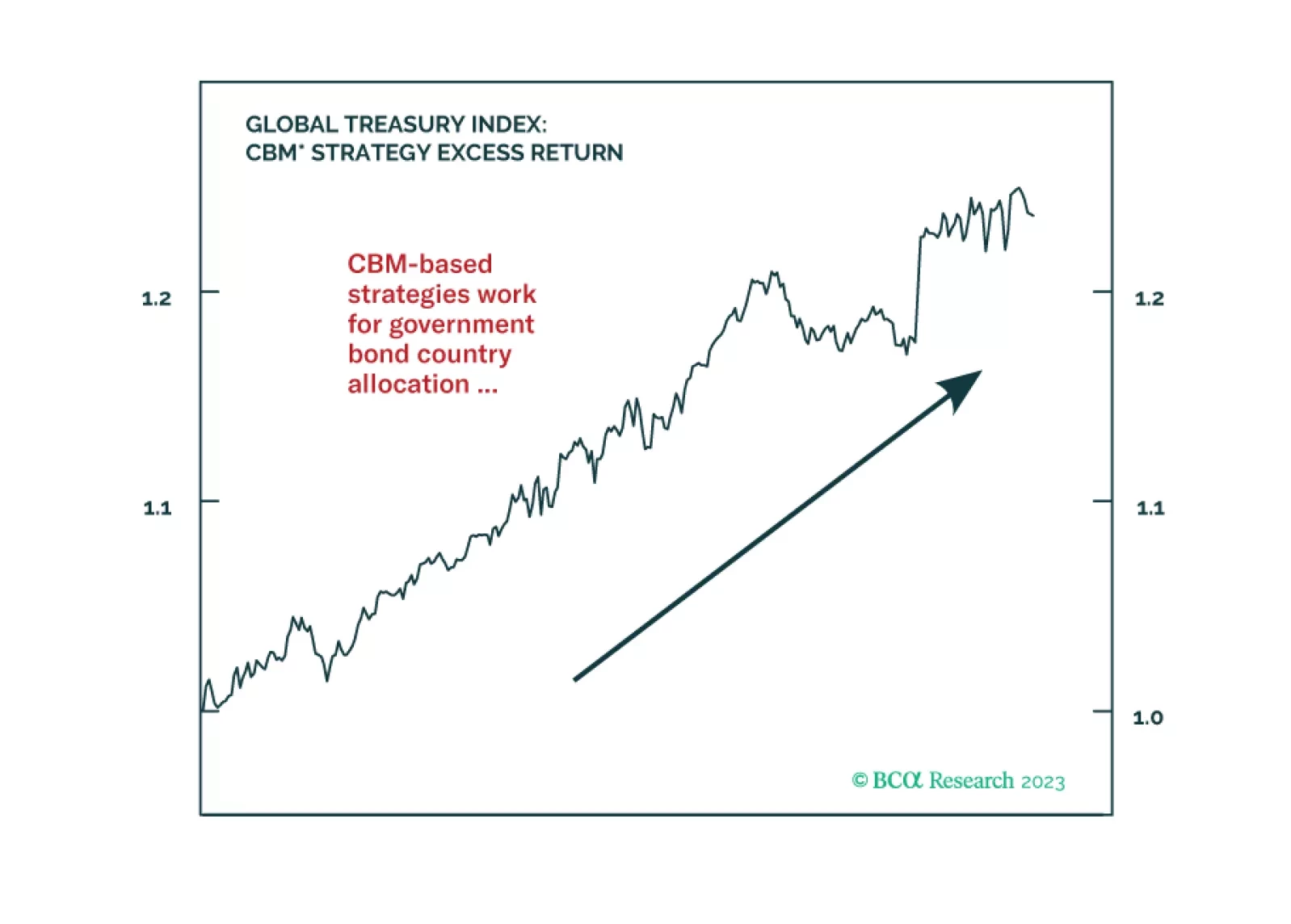

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

In this report, we present the quarterly review of the Global Fixed Income Strategy Model Bond Portfolio. The portfolio remains positioned for slower global growth momentum over the next 6-12 months, favoring government bonds over corporate debt. The portfolio also favors government bonds in countries flirting with recession where policy rates are too high (core Europe & the UK).

In this update to the two Special Reports on FX hedging of global equity portfolios with nine different home currencies, published in 2017, we show that BCA’s proprietary dynamic FX hedging strategies have consistently added value to global equity portfolios. We value quant models as an important input in our decision-making process, but we do not suggest any investor to slavishly follow them, because models cannot capture all the important fundamental changes, as demonstrated in the details of this report.