UK

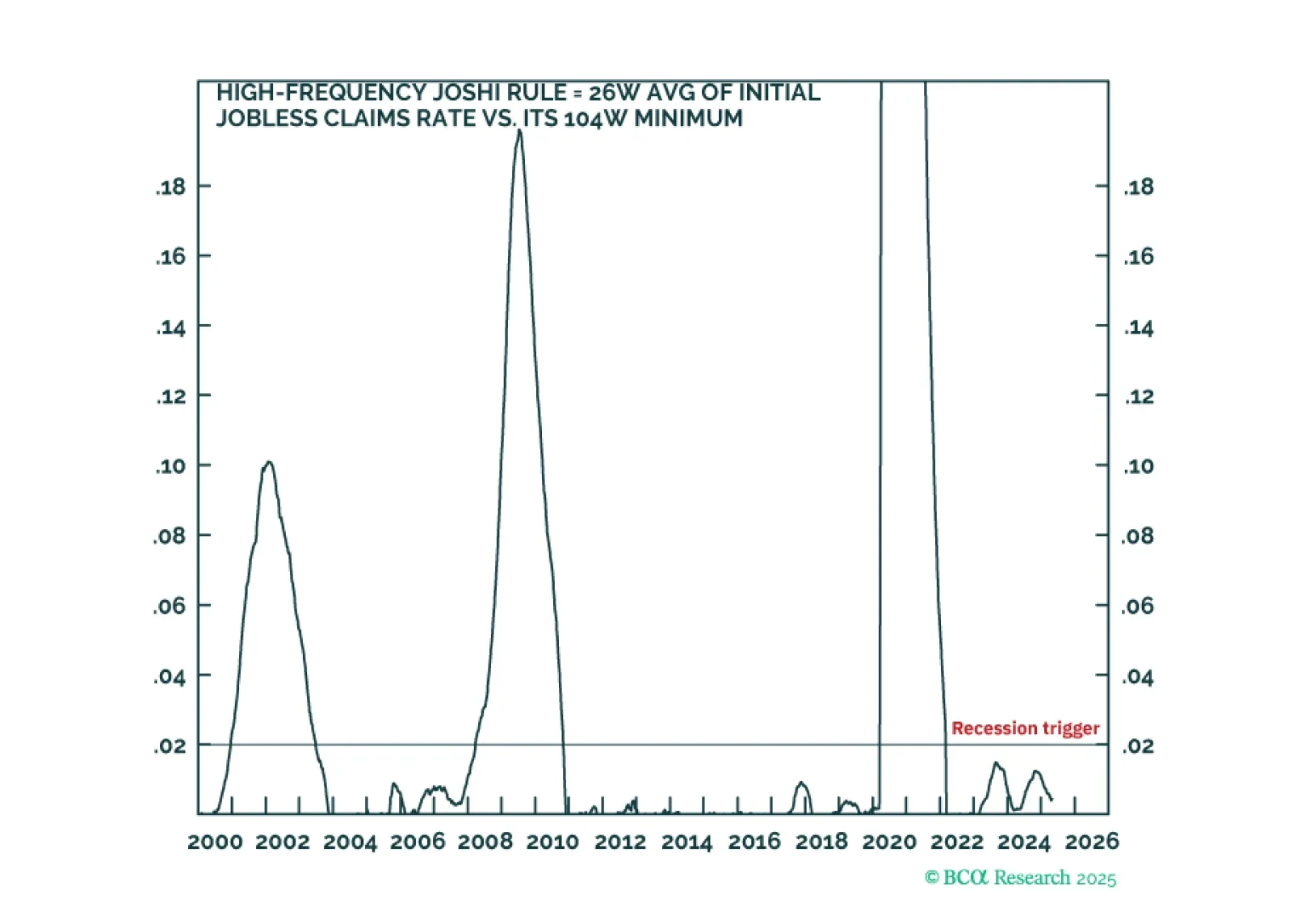

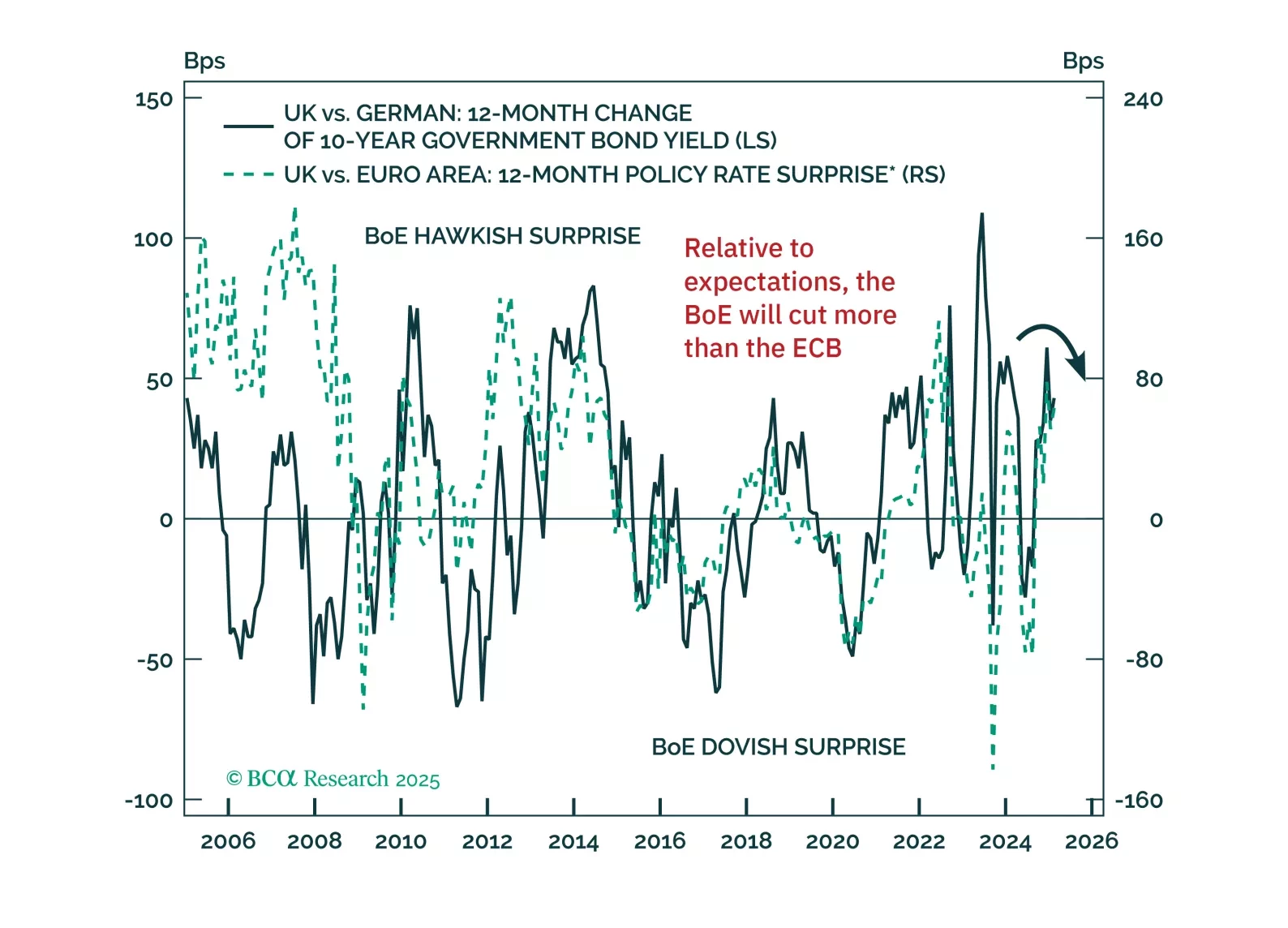

Today, we are introducing an additional ‘high-frequency Joshi rule’ which is updated weekly. The Joshi rules tell us that a US recession is not imminent. Until the Joshi rules are triggered, overweight non-US government bonds, and especially UK gilts, versus US T-bonds. And shift cyclical asset allocation from overweight to neutral-weight bonds. Plus: tactically long USD/GBP and tactically underweight global industrials (EXI).

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

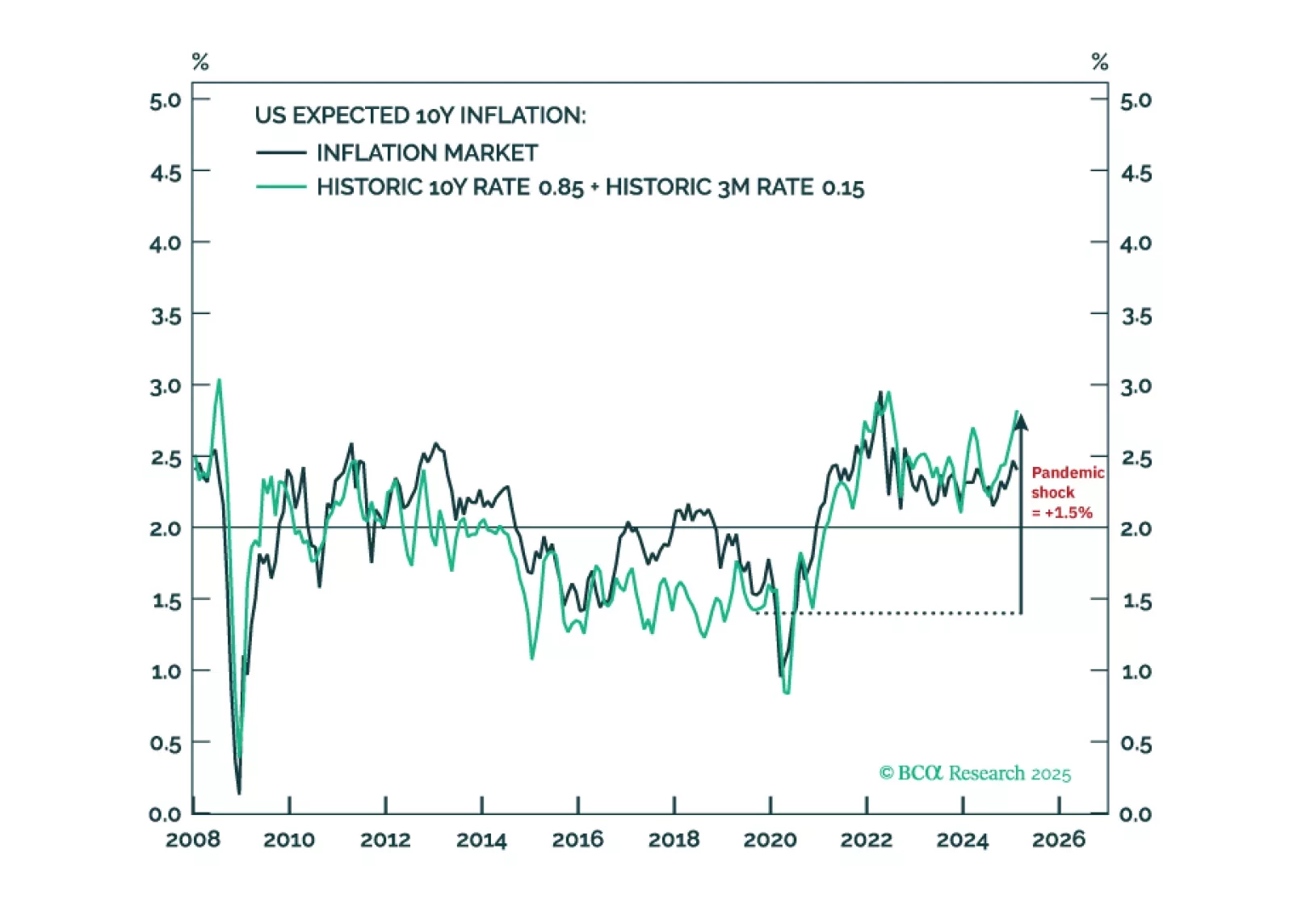

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

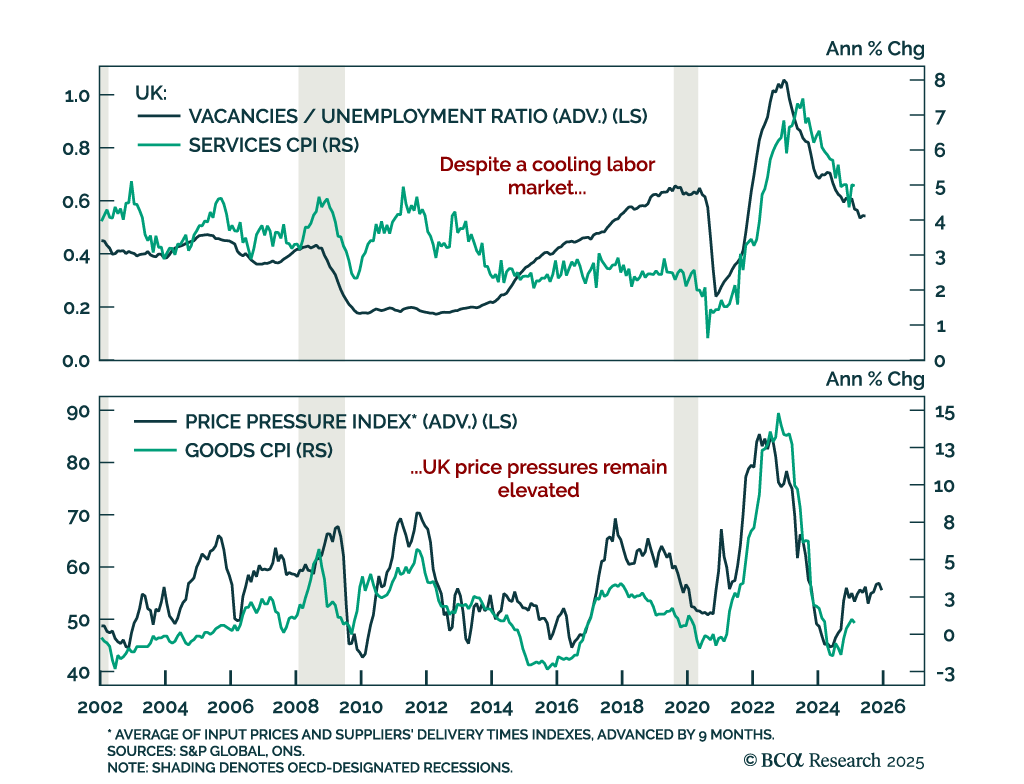

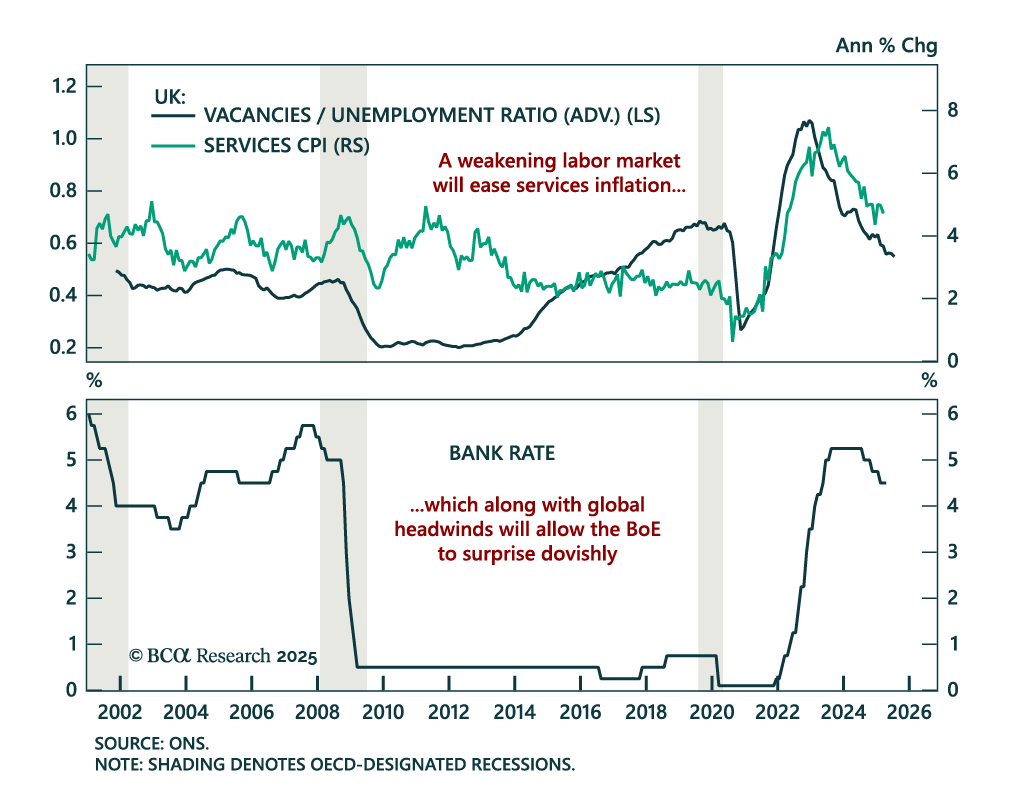

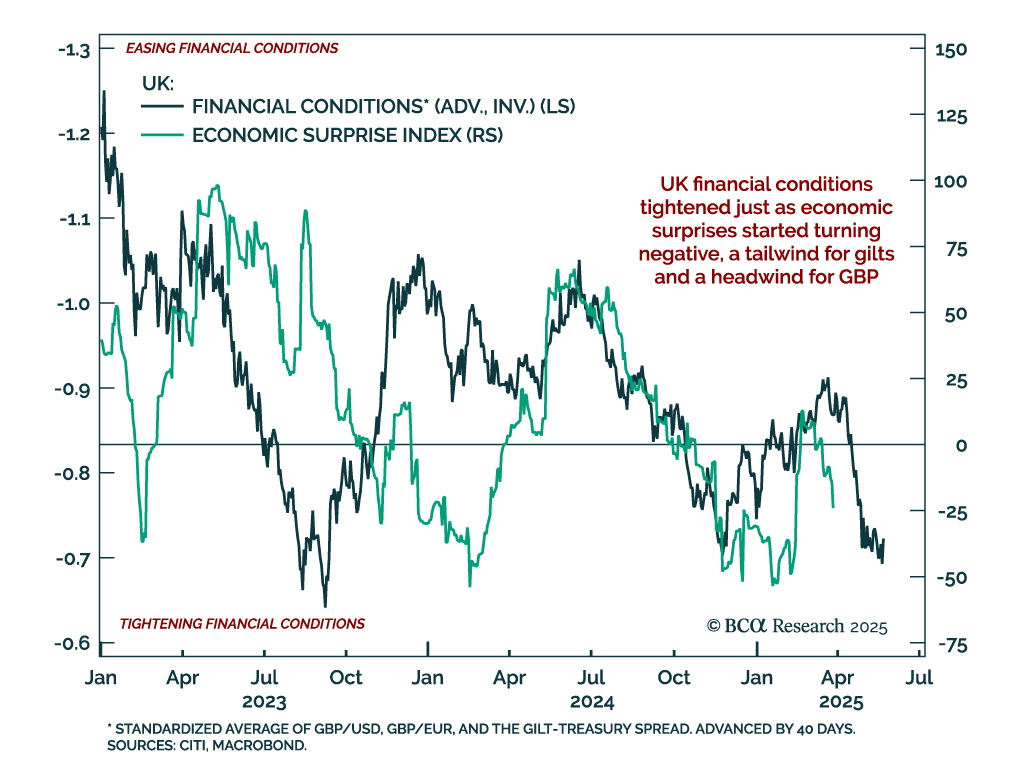

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

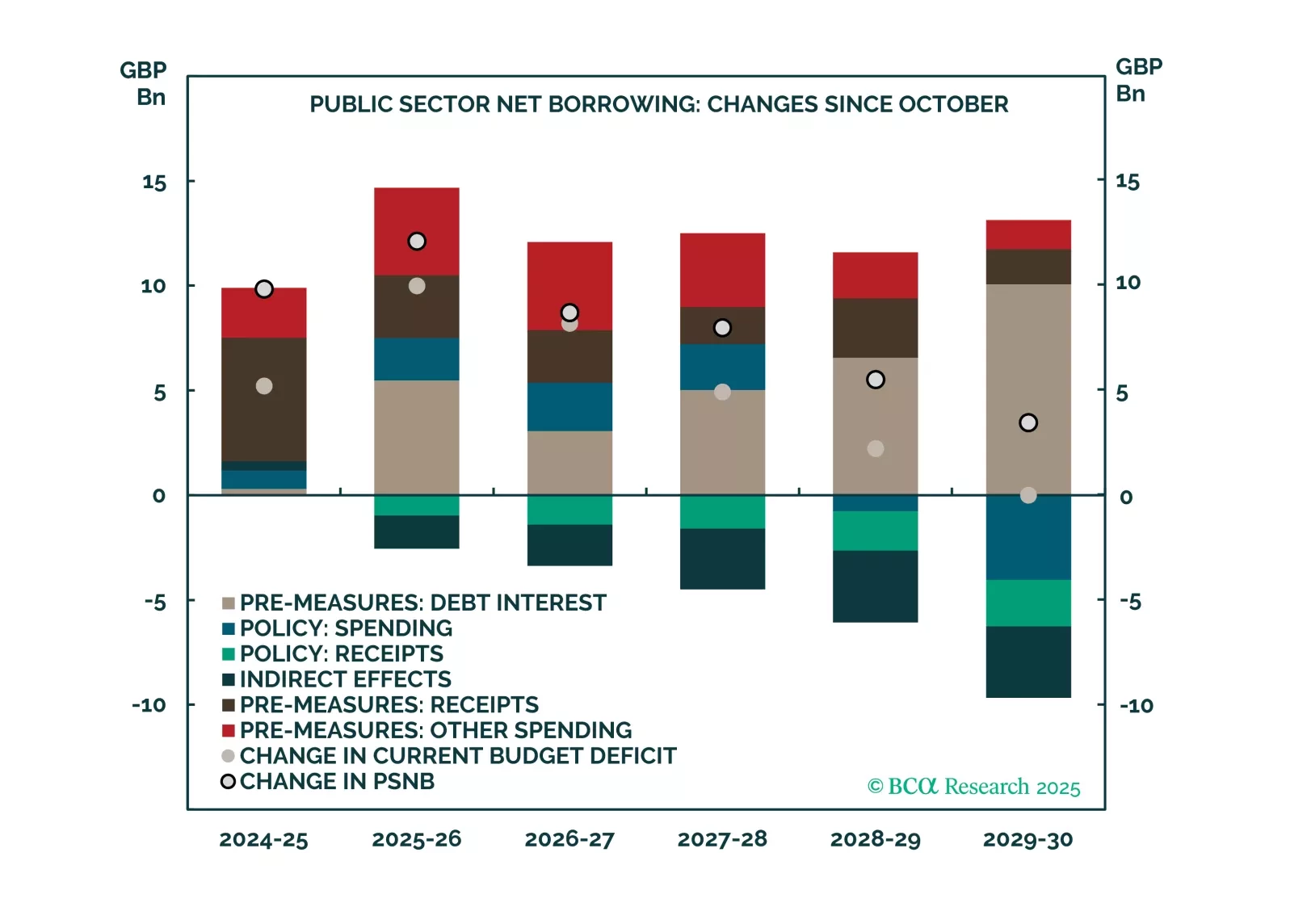

This report is a quick take on our views on UK bonds and FX, given the recent budget.