UK

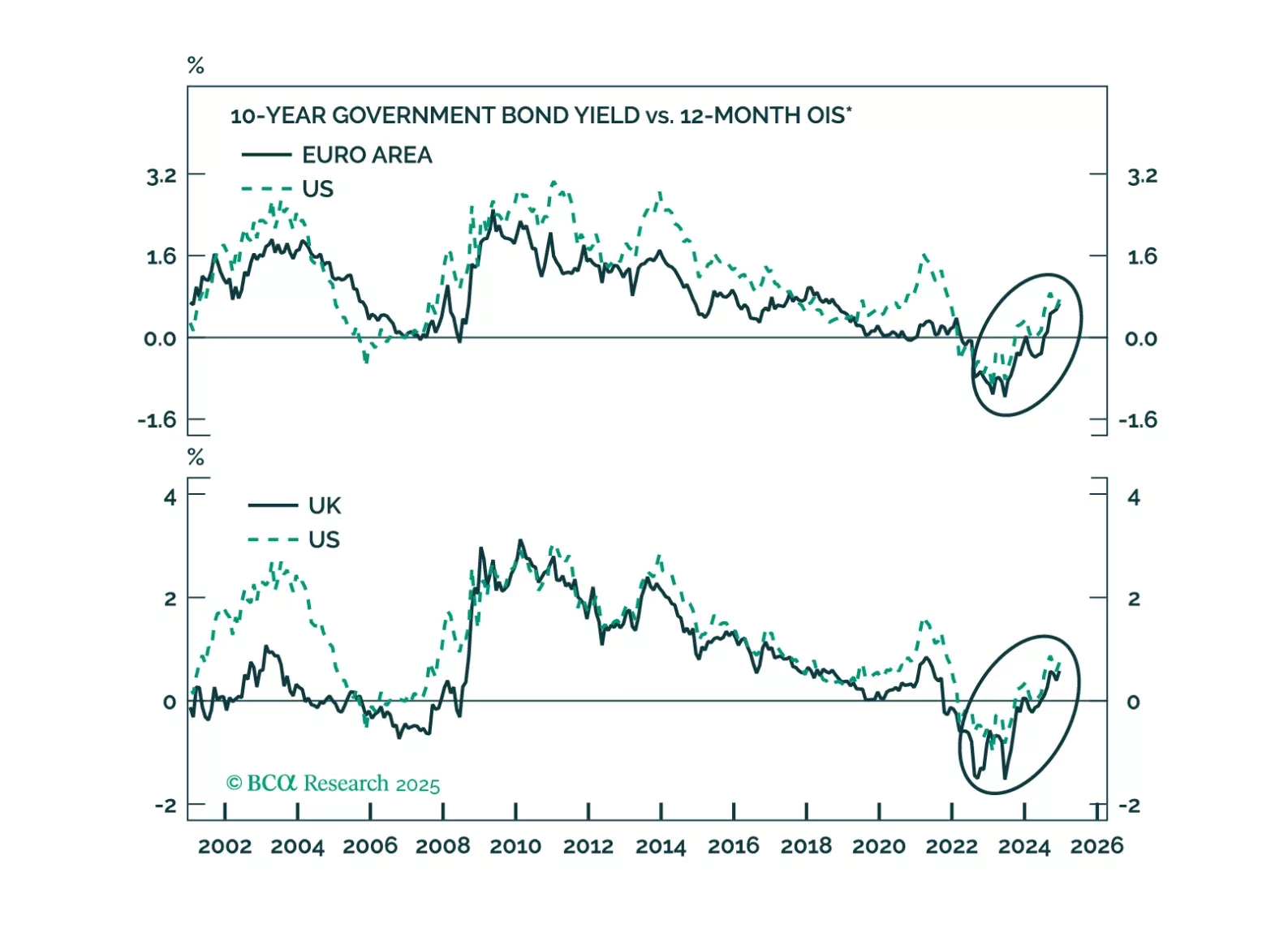

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.

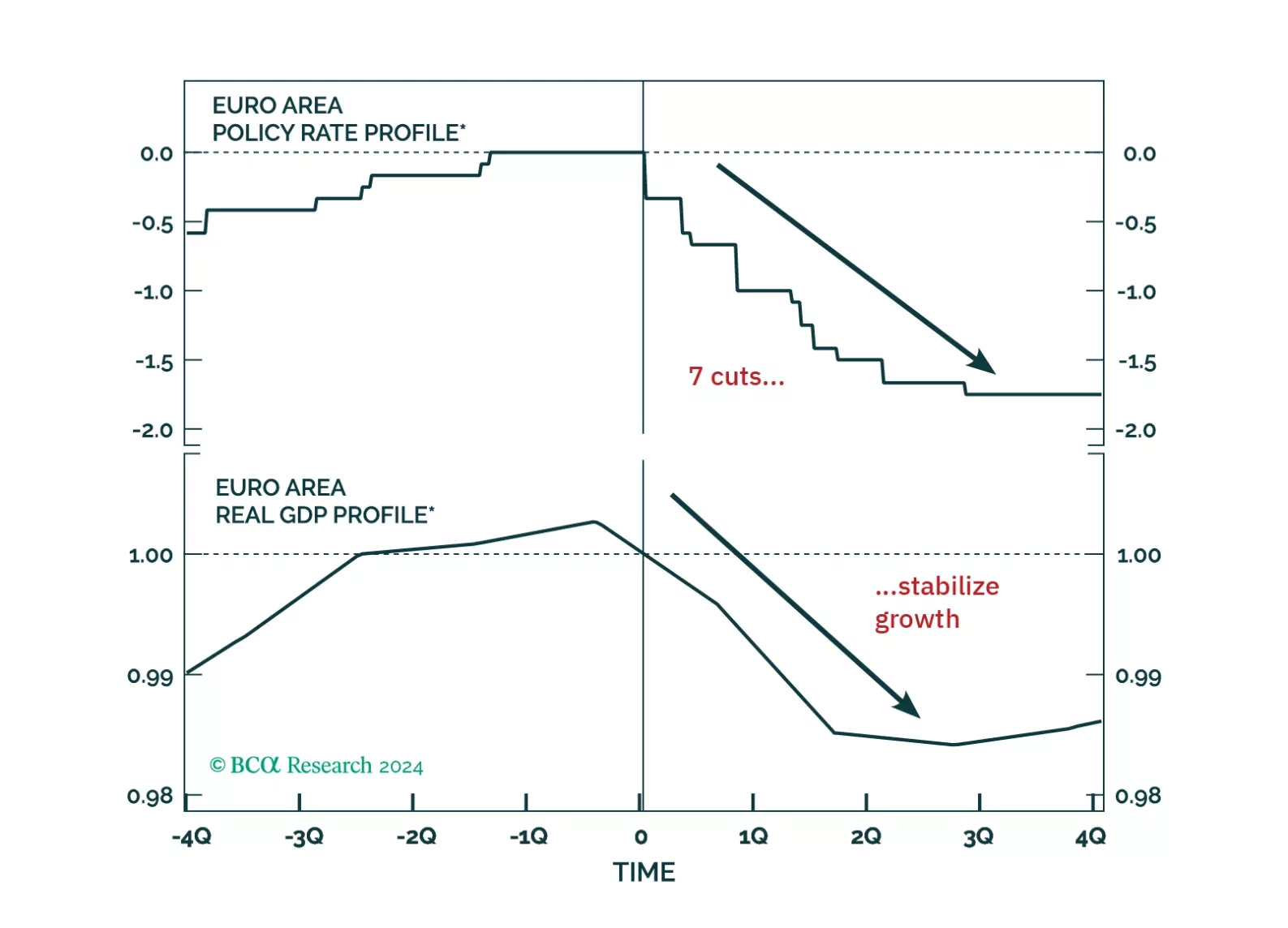

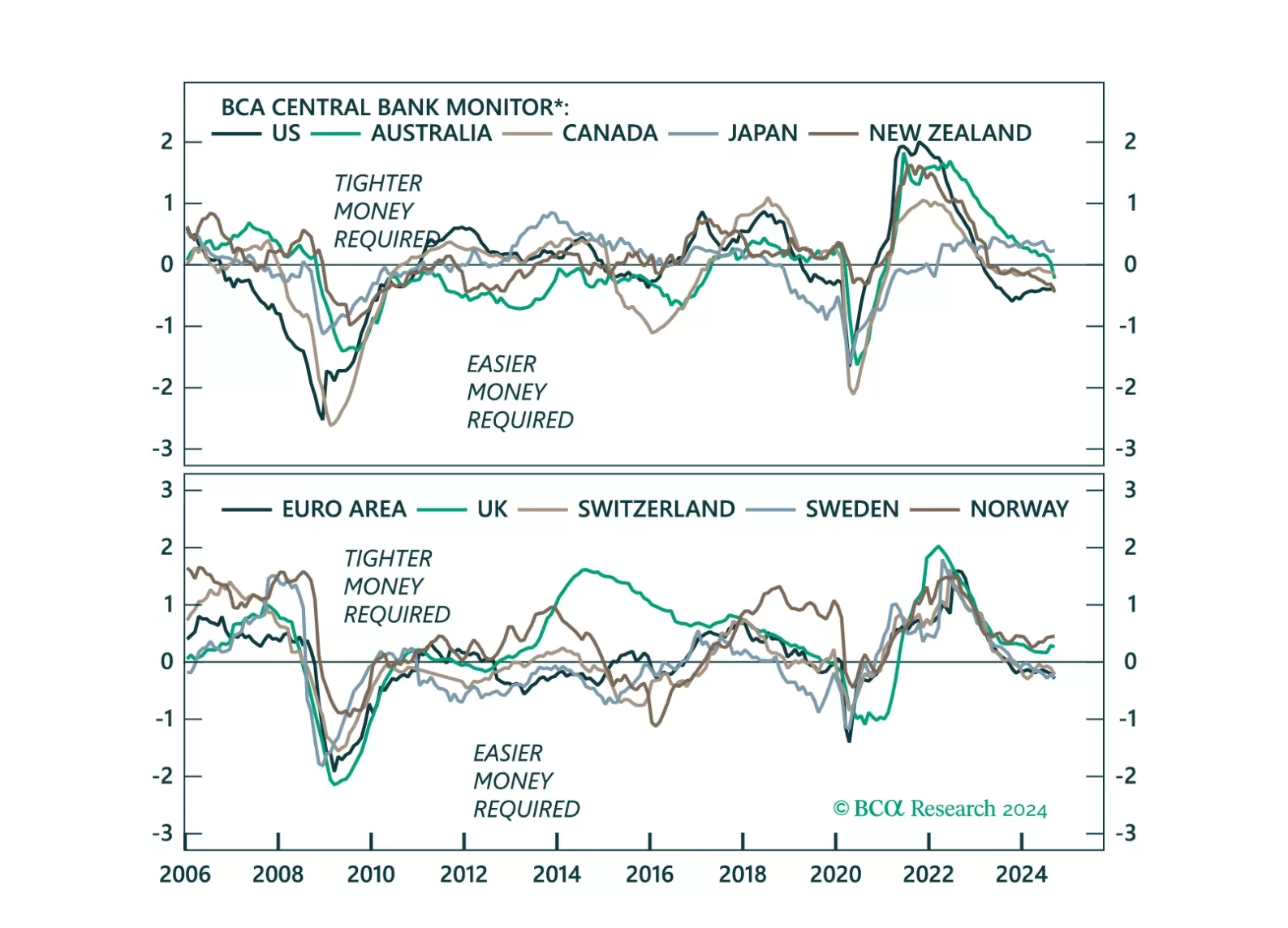

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

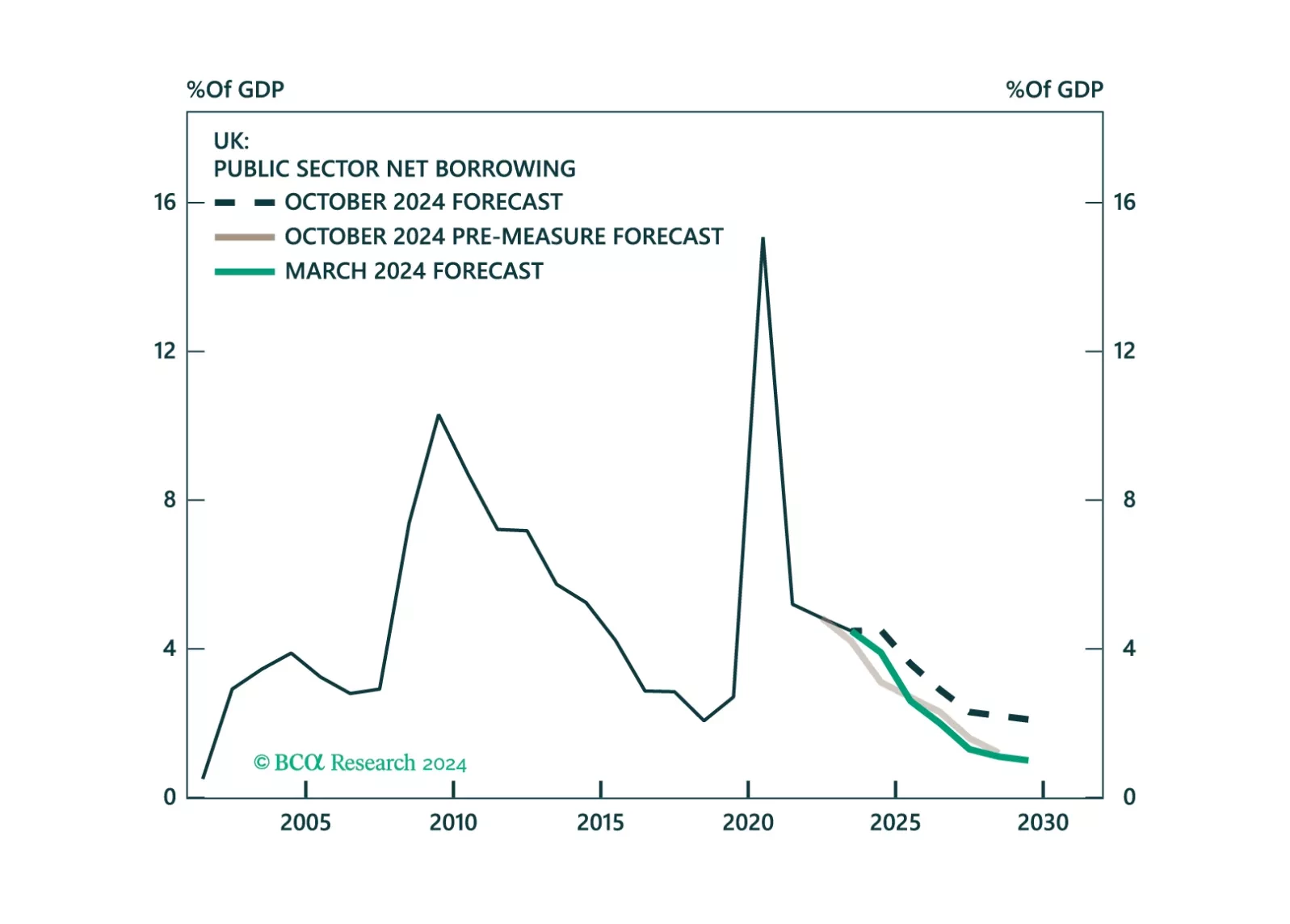

This Strategy Insight presents our view on today’s rate cut by the Bank of England as well as the budget announced by the UK government last week.