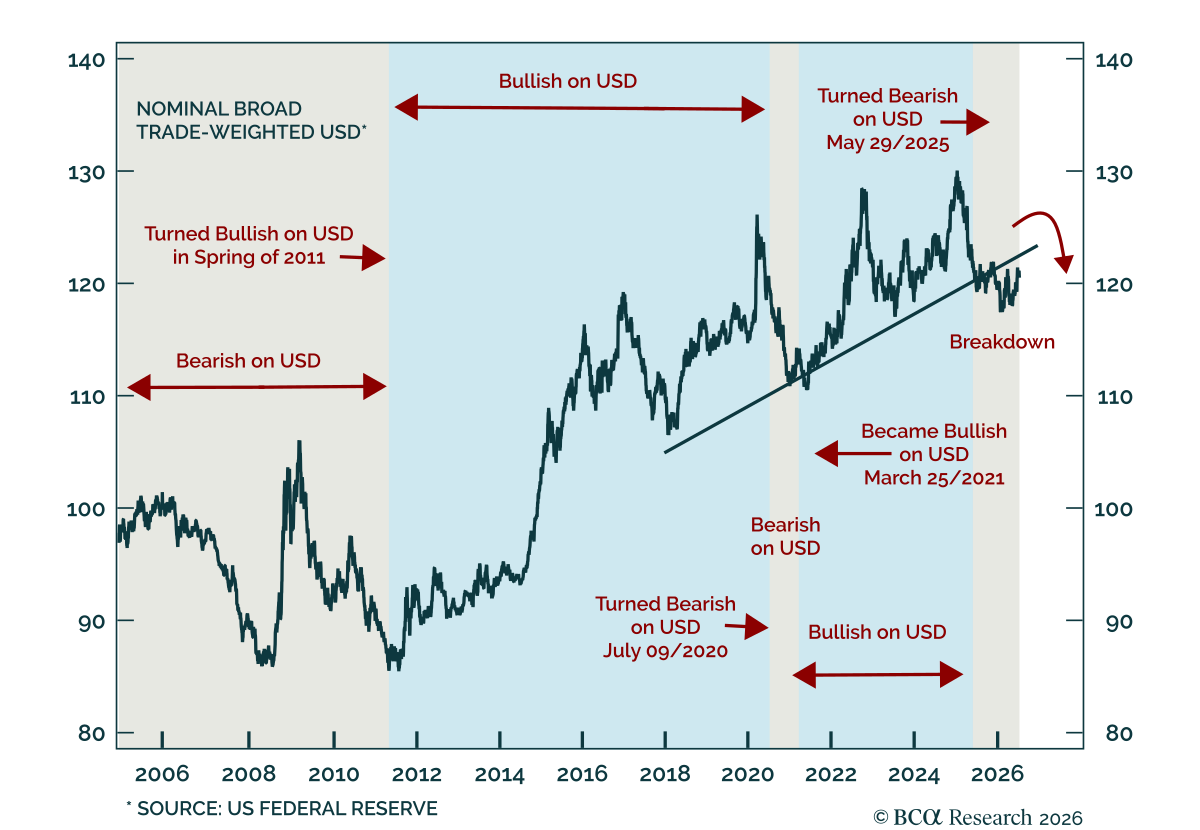

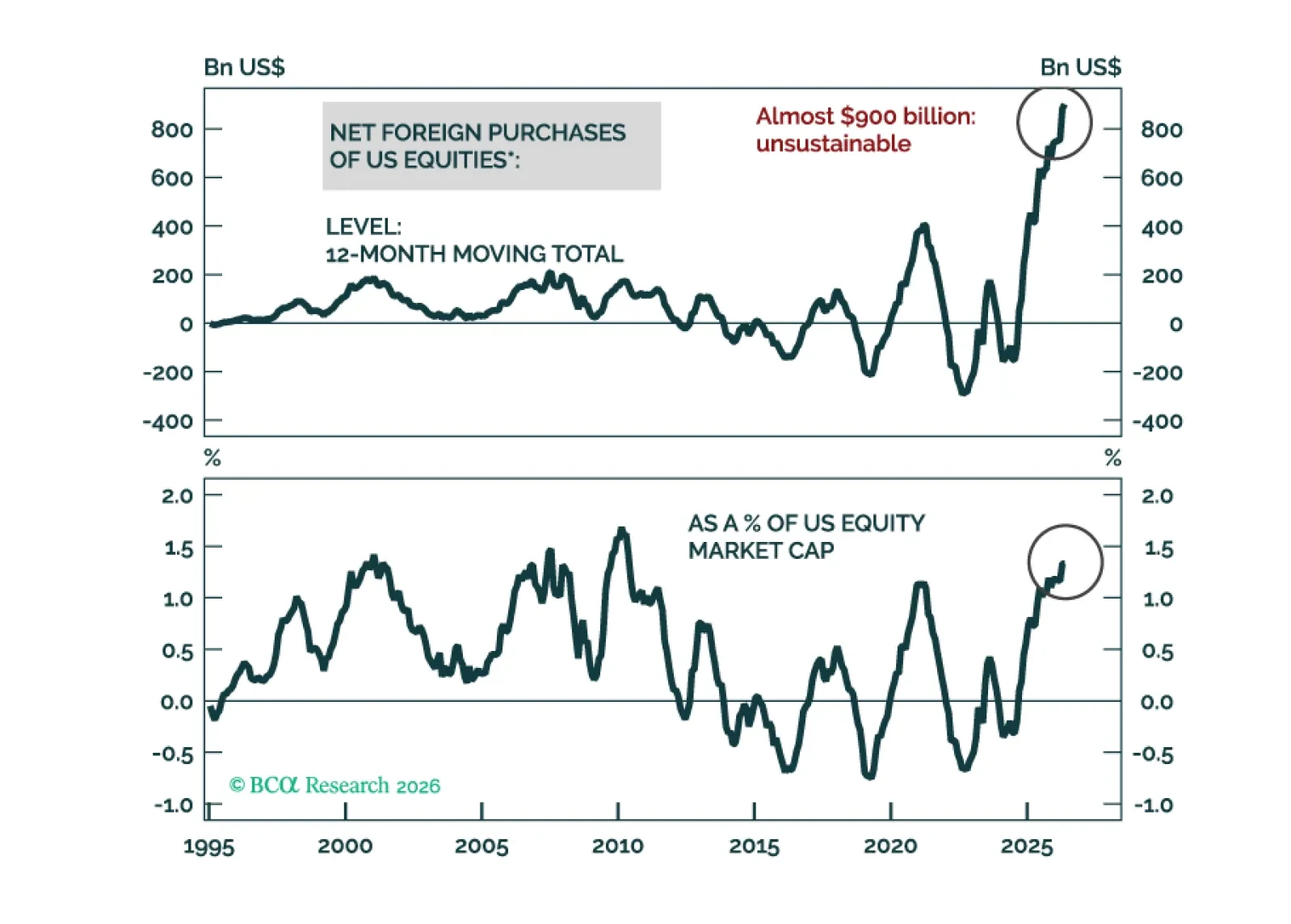

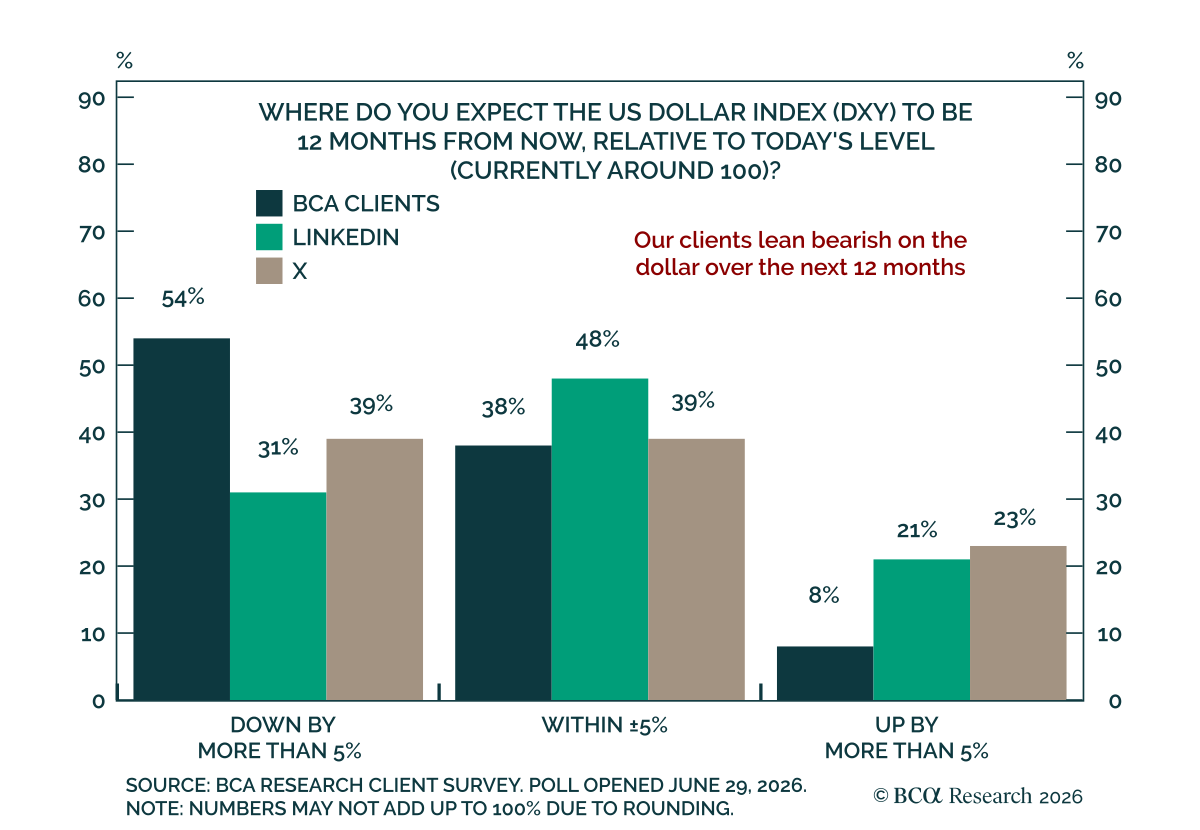

US Dollar

The US dollar will become a pro-cyclical currency going forward. This regime shift would upend financial market correlations, and most investment portfolios are not positioned for it. A great deal of money is made or lost during regime changes - and one is coming soon. That is why our message remains loud and clear: Get Out of the Dollar (G.O.D.).

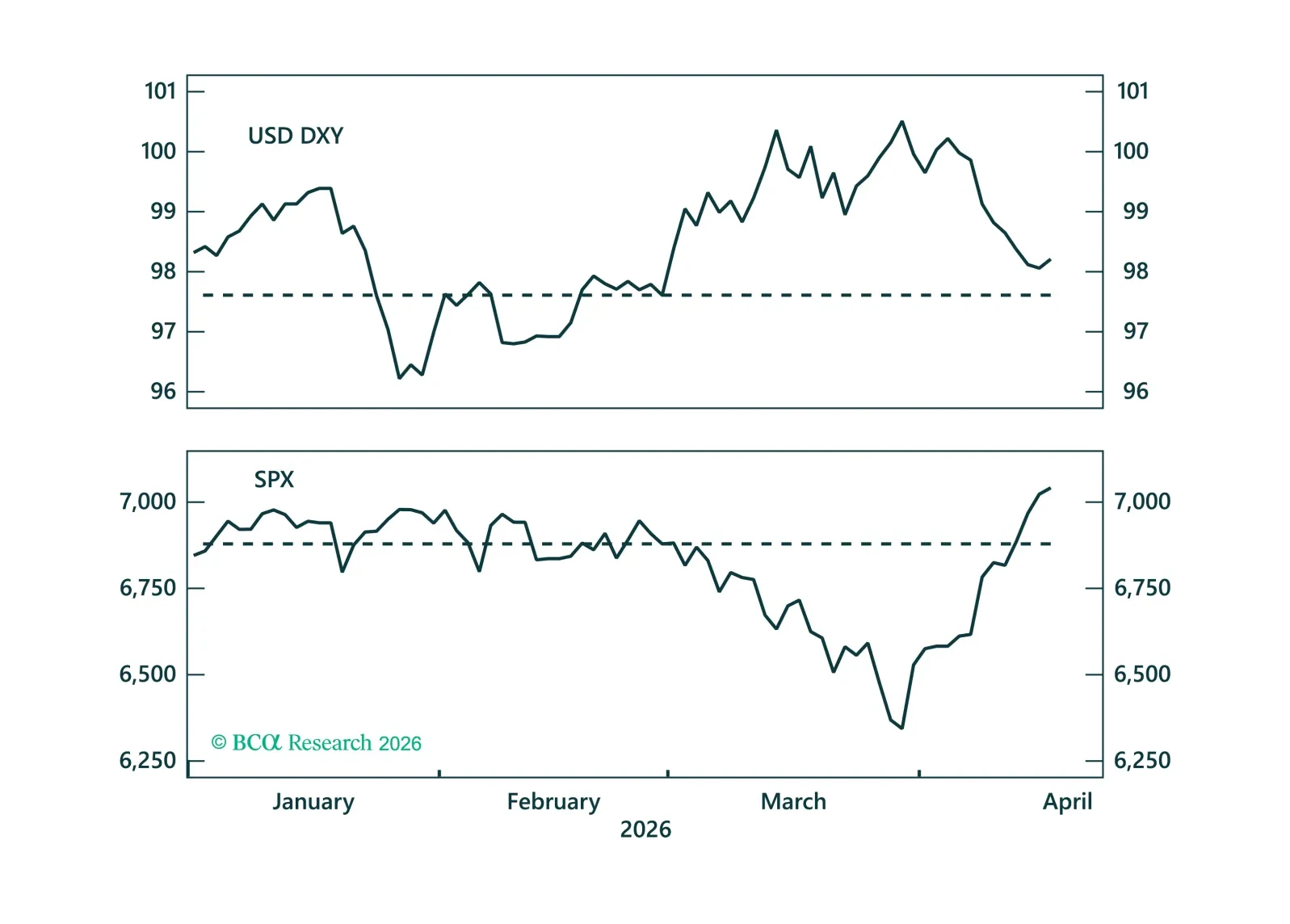

The dollar has had a strong run but its key supports from Fed repricing, positioning, and terms of trade are starting to fade. We close our tactical long USD positions and turn to short USD/JPY, where intervention risk makes yen shorts look increasingly dangerous.

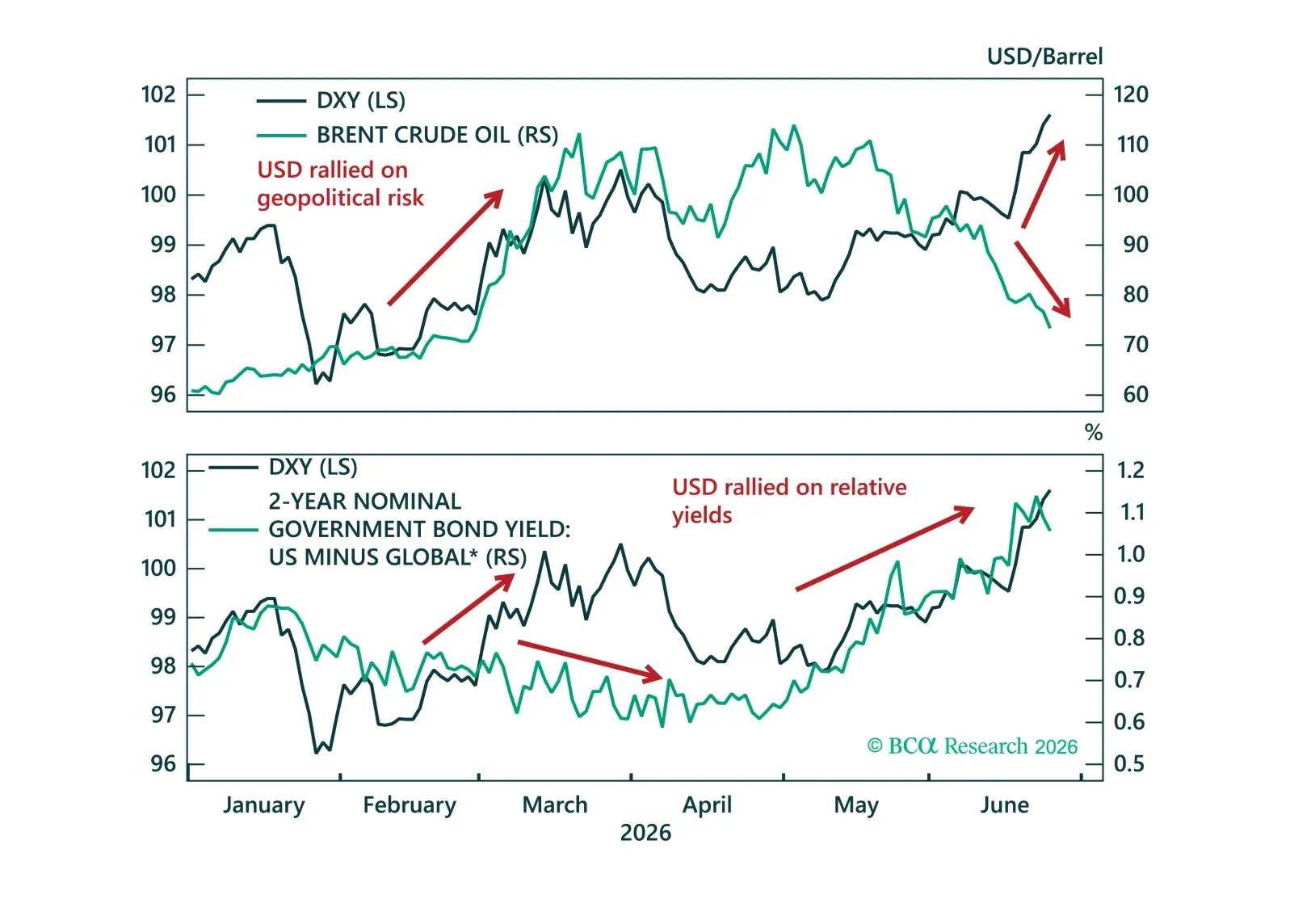

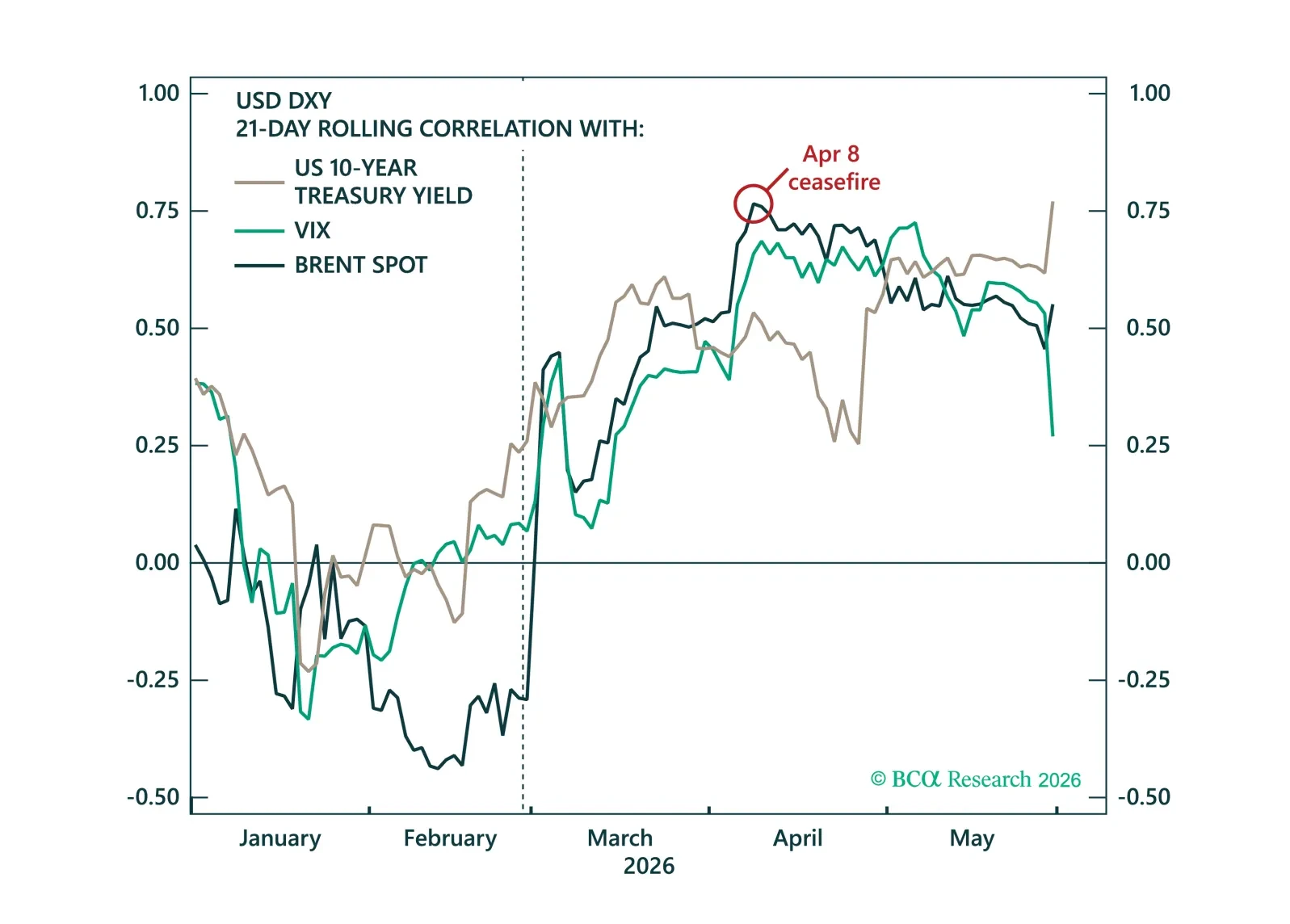

The dollar's muted response to the Iran conflict has led many to question its safe-haven appeal. We argue the opposite – the dollar's defensive properties have returned, while improving growth and rate dynamics should underpin further USD strength in the months ahead.

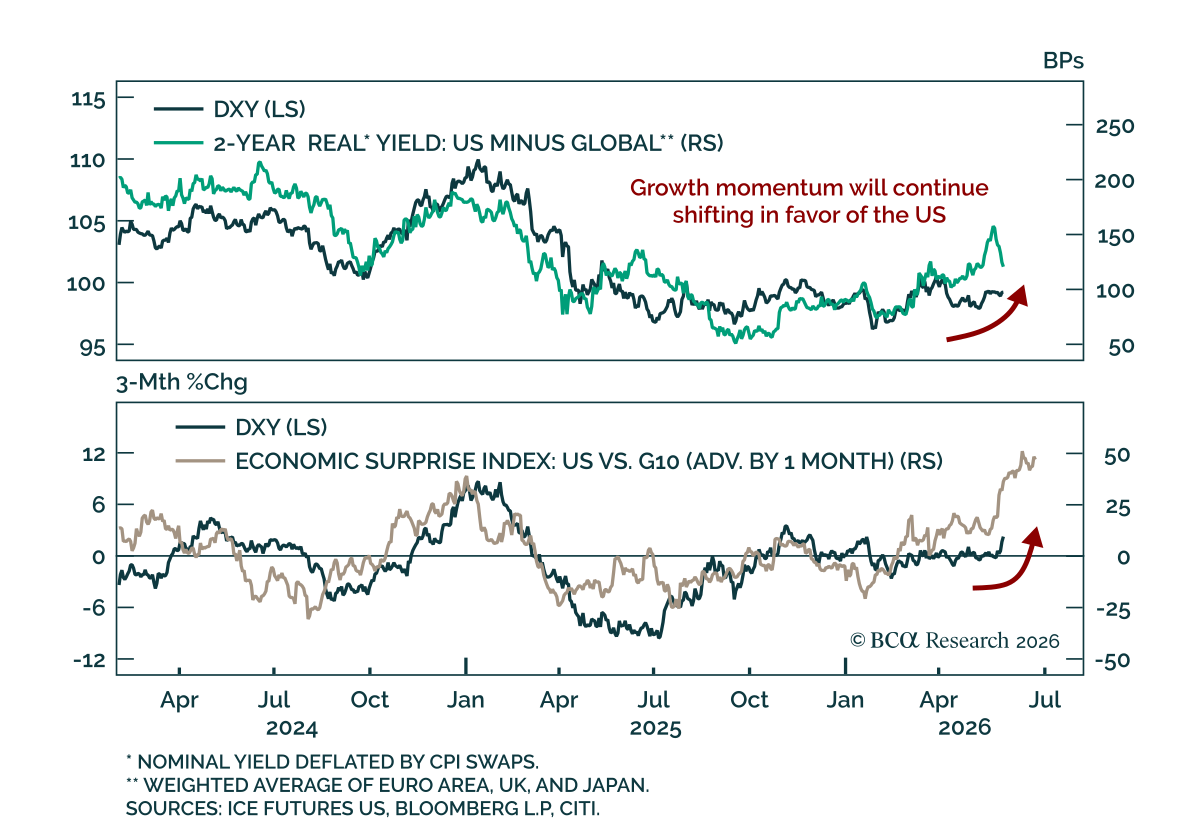

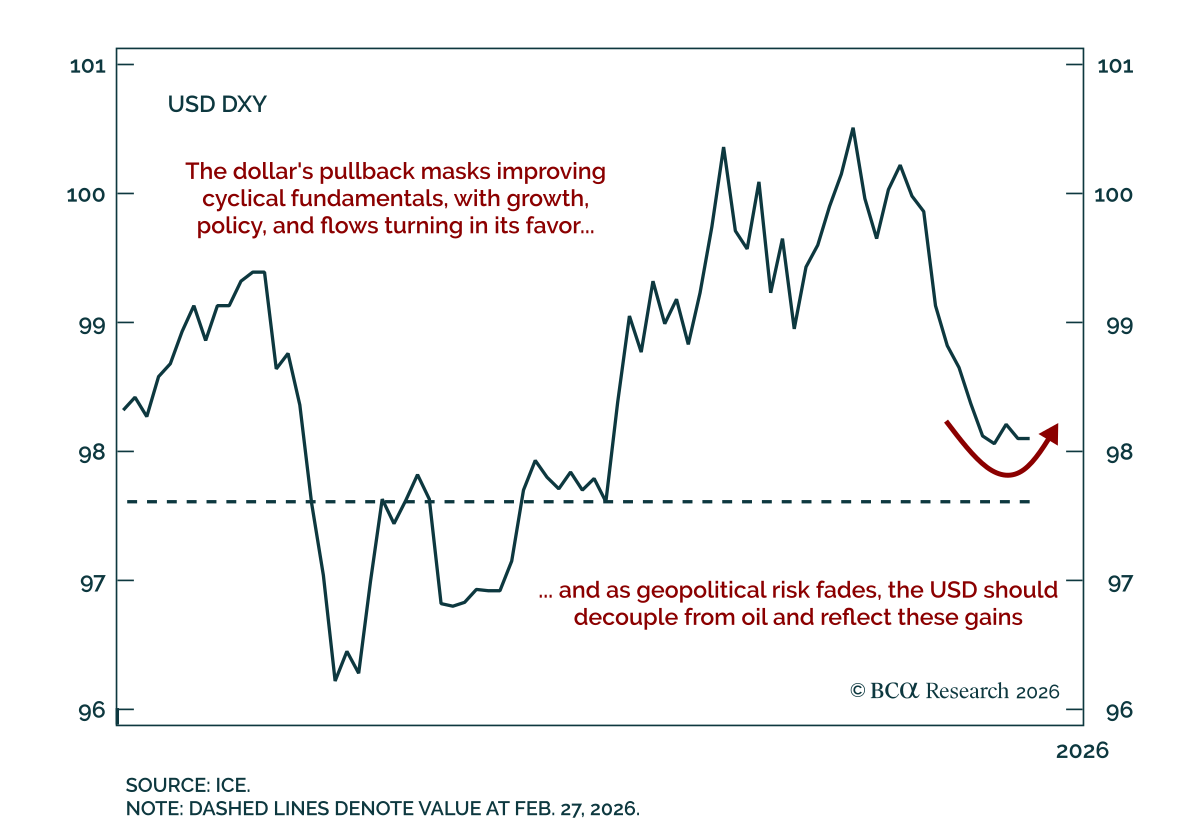

The dollar’s pullback masks a quiet improvement in its cyclical backdrop, with growth, monetary policy, and flows turning in its favor. As markets fully price out geopolitical risk, the USD should decouple from oil and better reflect these gains, despite lingering structural headwinds.