US Dollar

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

In this report, we review our trade recommendations based on incoming data in the last month.

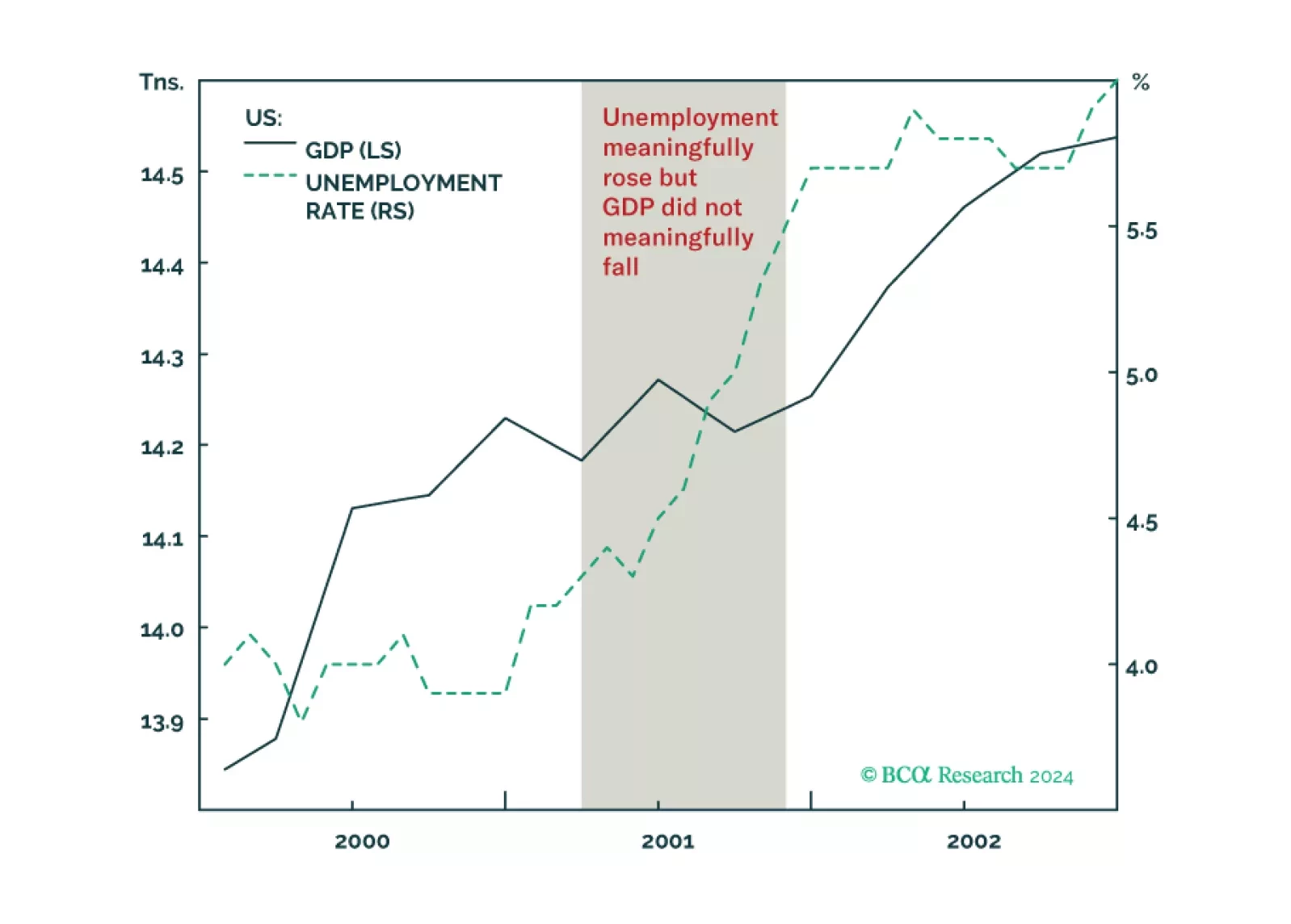

Why the US could get a jobs recession without a GDP recession, as happened in 2001, and what it means for stocks and bonds. Plus, an update on the Joshi rule.

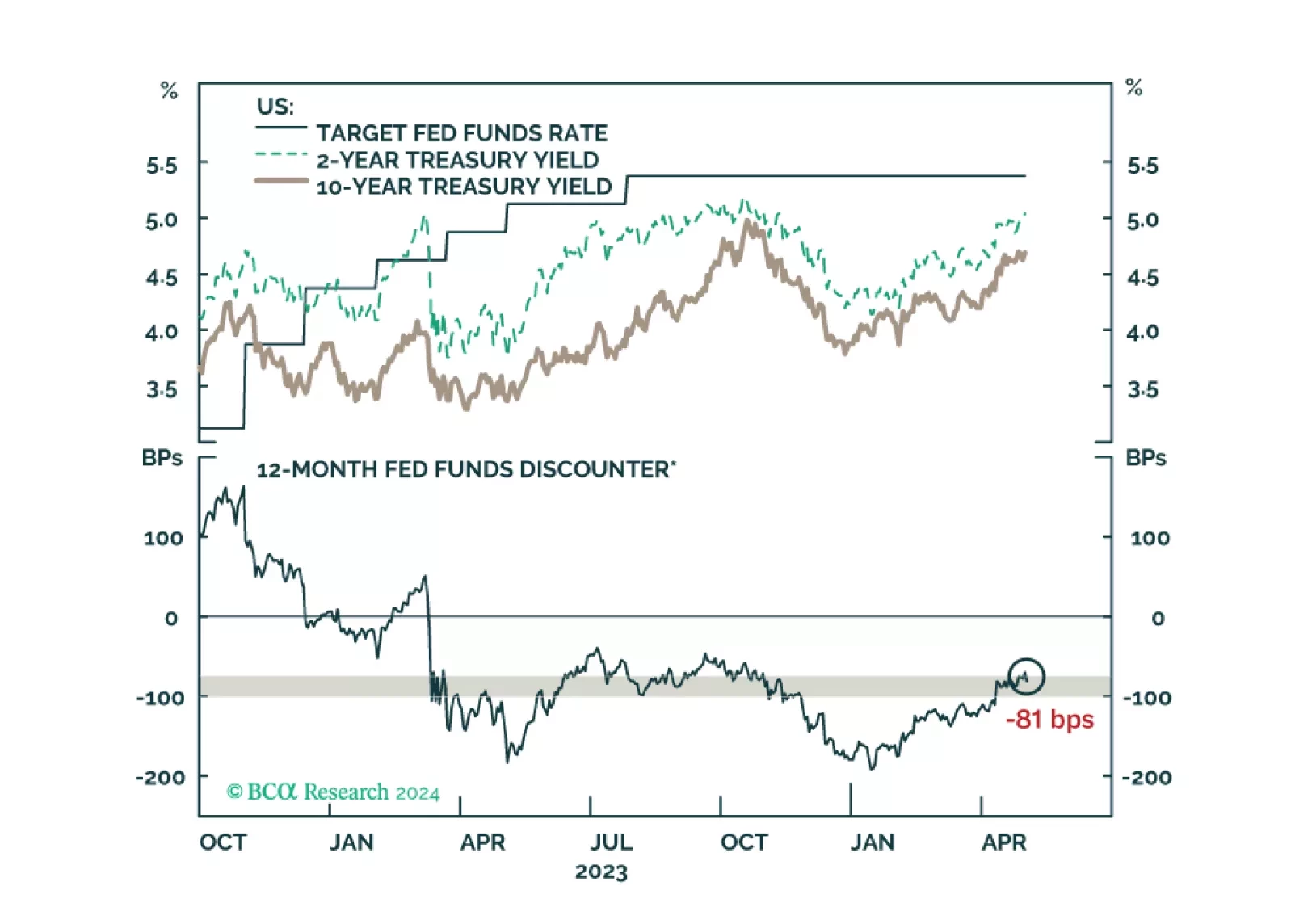

Updated views on US Treasury yields and the dollar following today’s FOMC meeting.

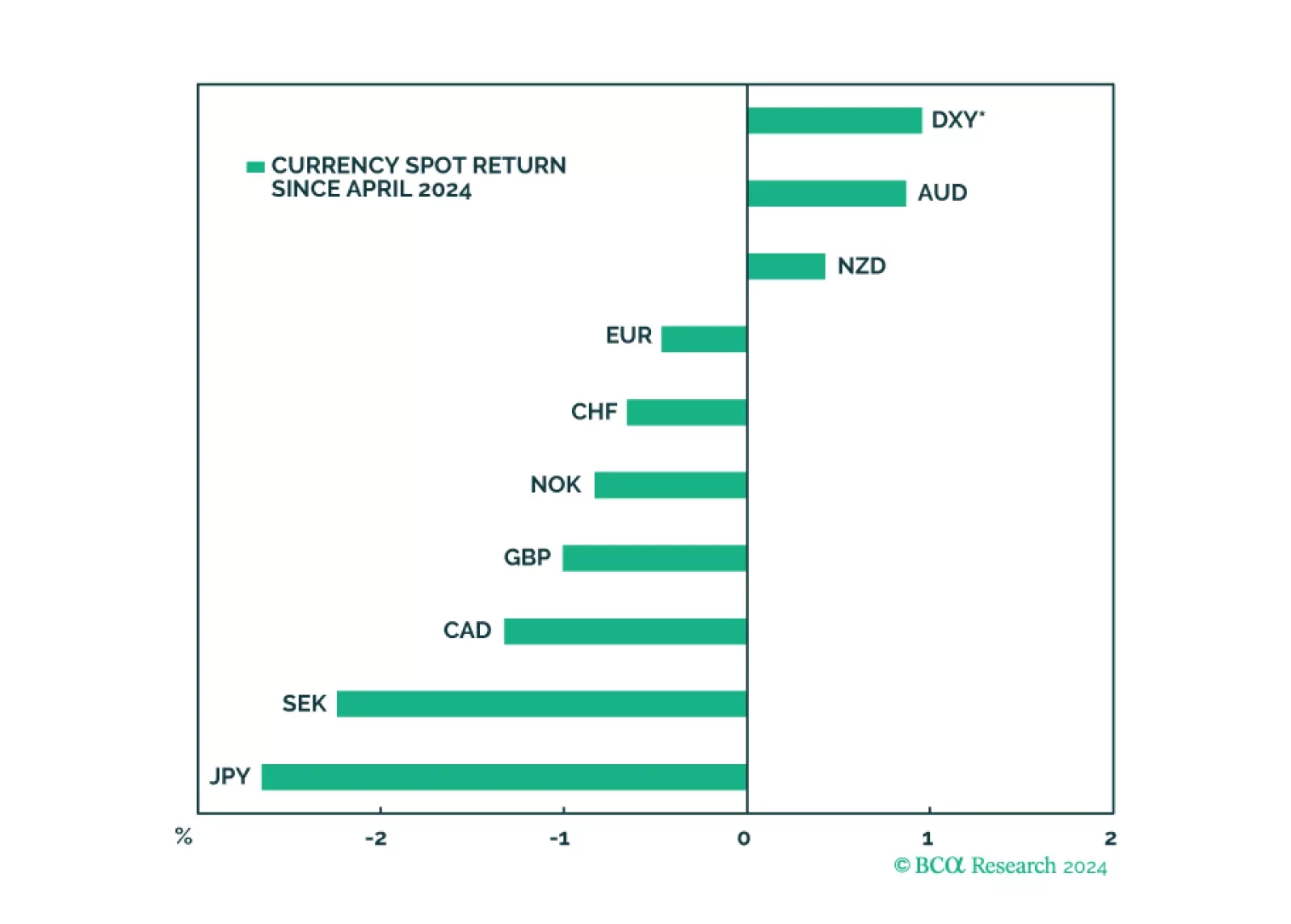

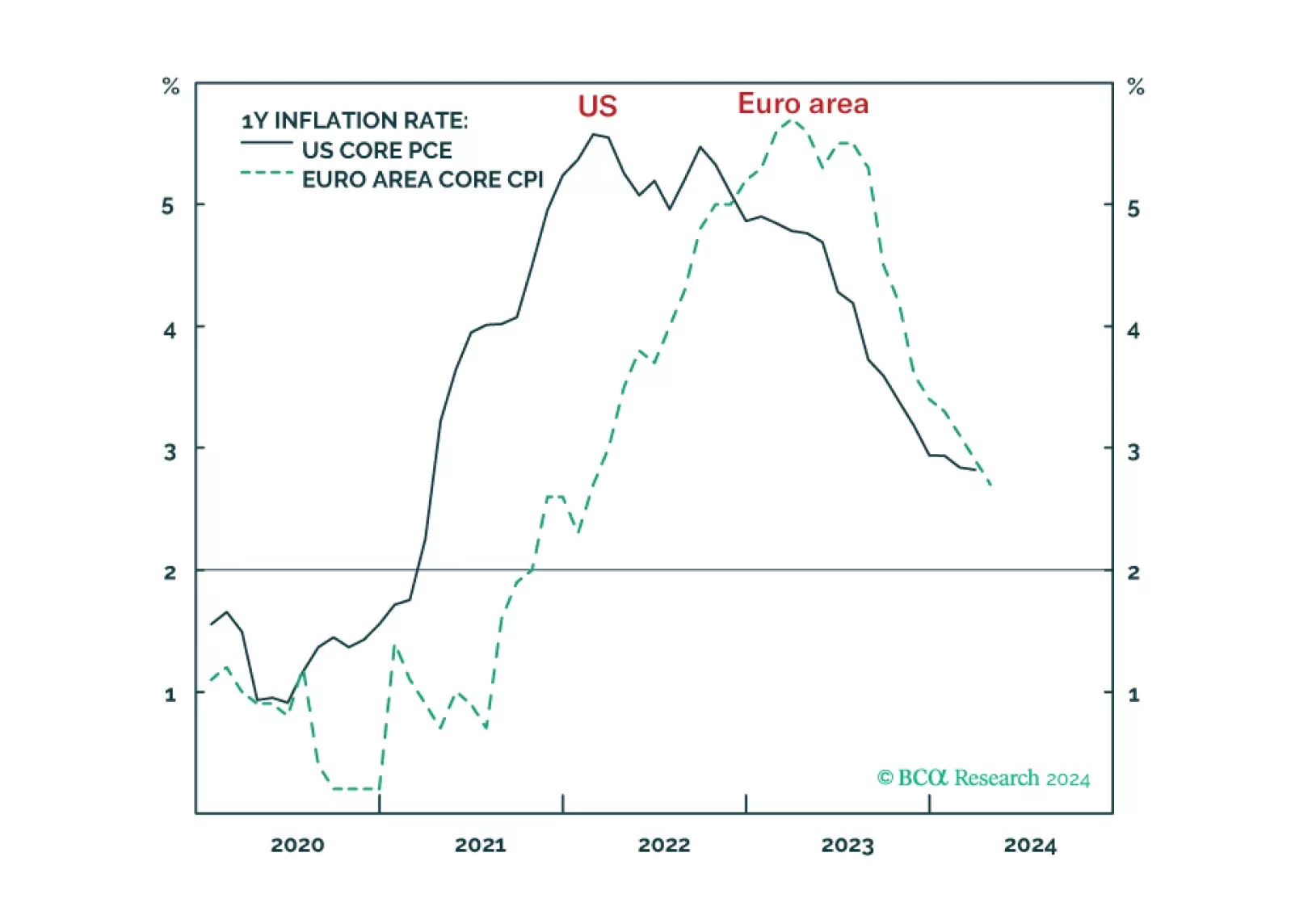

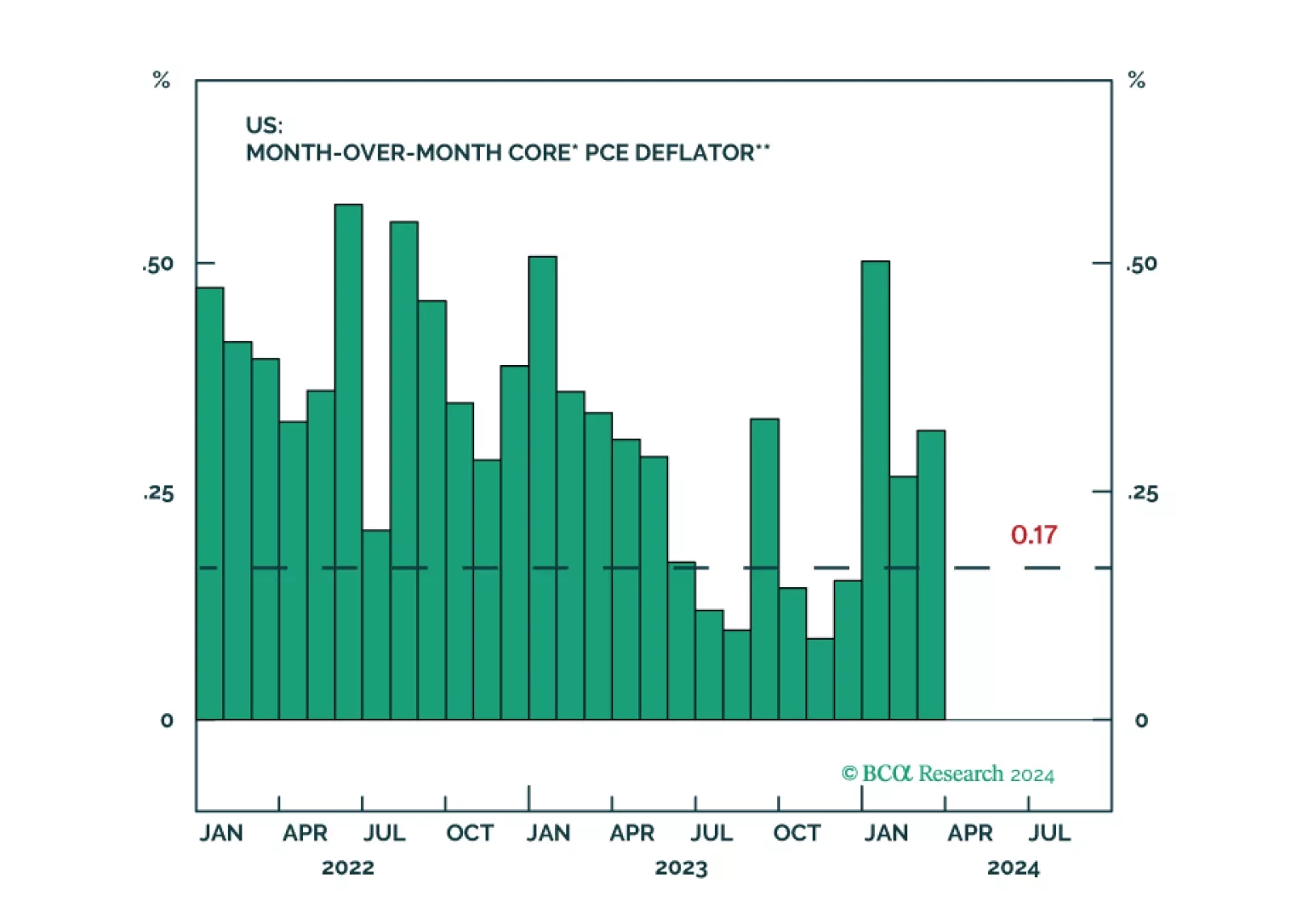

Wild hopes for US rate cuts got shattered, exactly as we predicted. But given the different incentives that the Fed and ECB now face, the relative pricing between the Fed and the ECB could widen further in the coming months. We discuss the implications for rates, the dollar, and the relative positioning in US versus European equities.

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

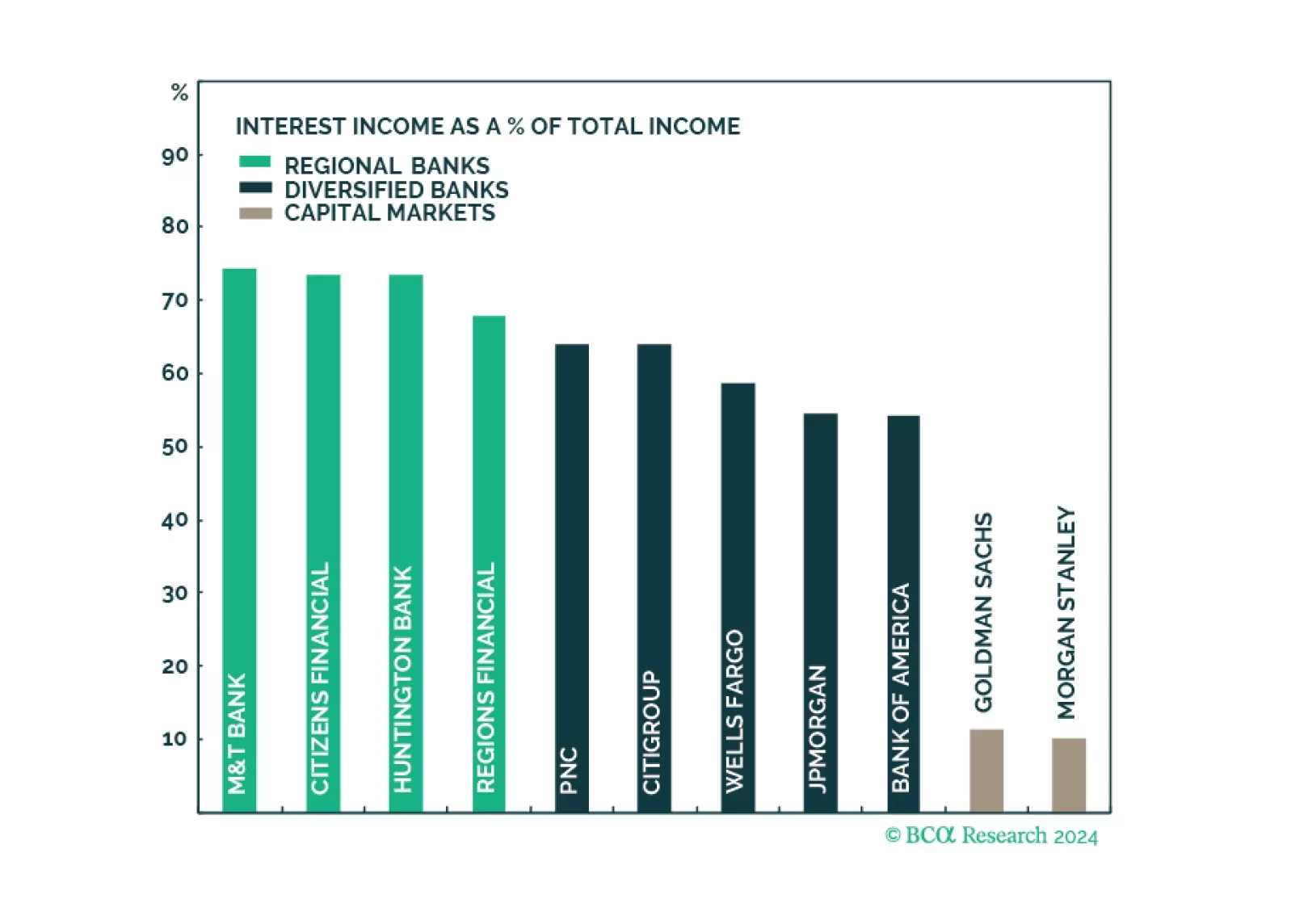

Q1 earnings results of the largest US banks have demonstrated that the engine of recent growth in profitability, NII, has faltered as funding costs are rising fast. However, the resurgence in non-NII thanks to a revival in corporate activity has been a saving grace. Earnings growth appears to have bottomed, while valuations are attractive. To play up portfolio exposure to an upcoming surge in capital markets activity, and minimize exposure to declining profitability in traditional banking services, overweight Diversified Banks and Capital Markets, and underweight Regional Banks.