US Dollar

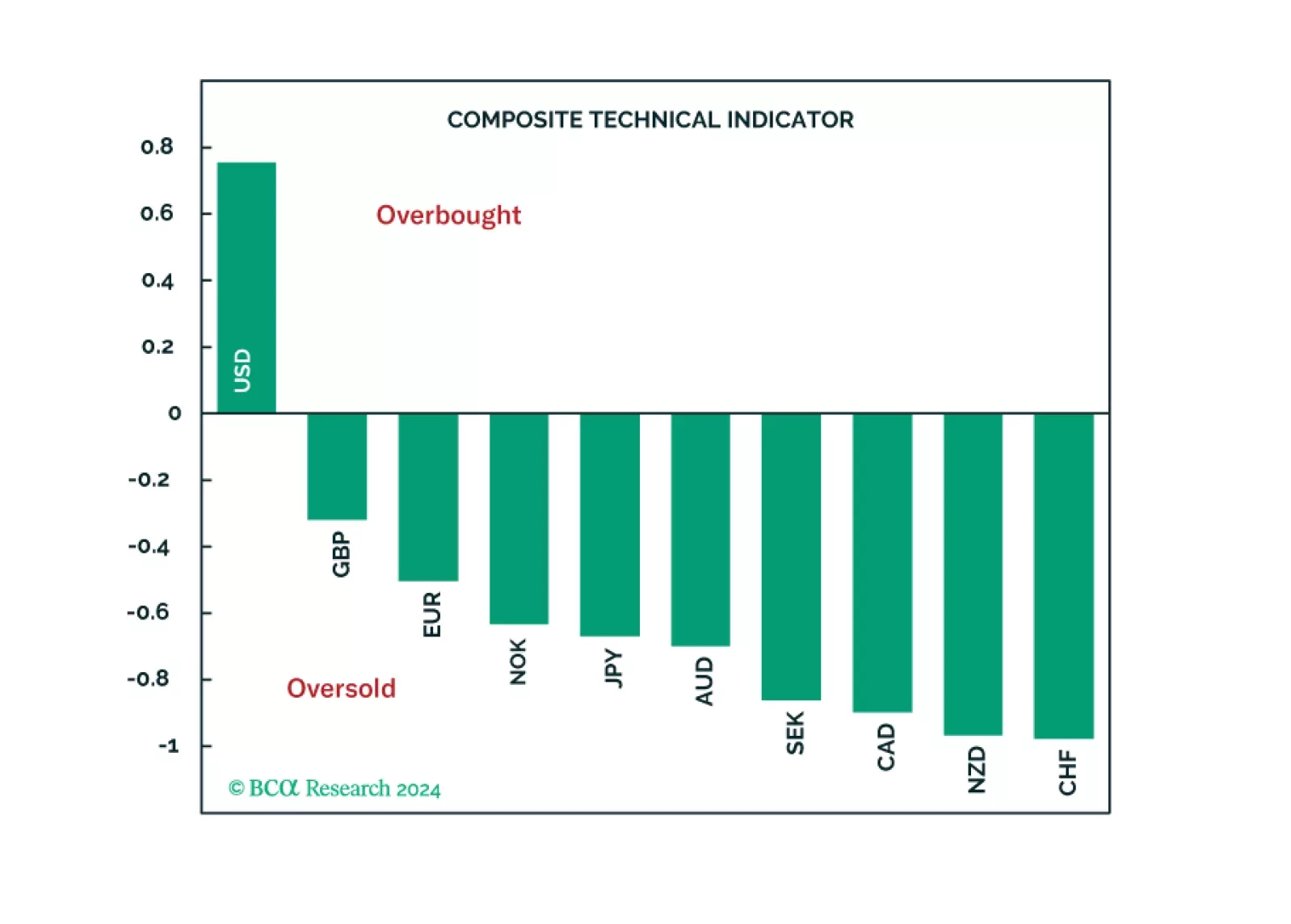

In this report, we review what our technical indicators are telling us about the G10 currencies.

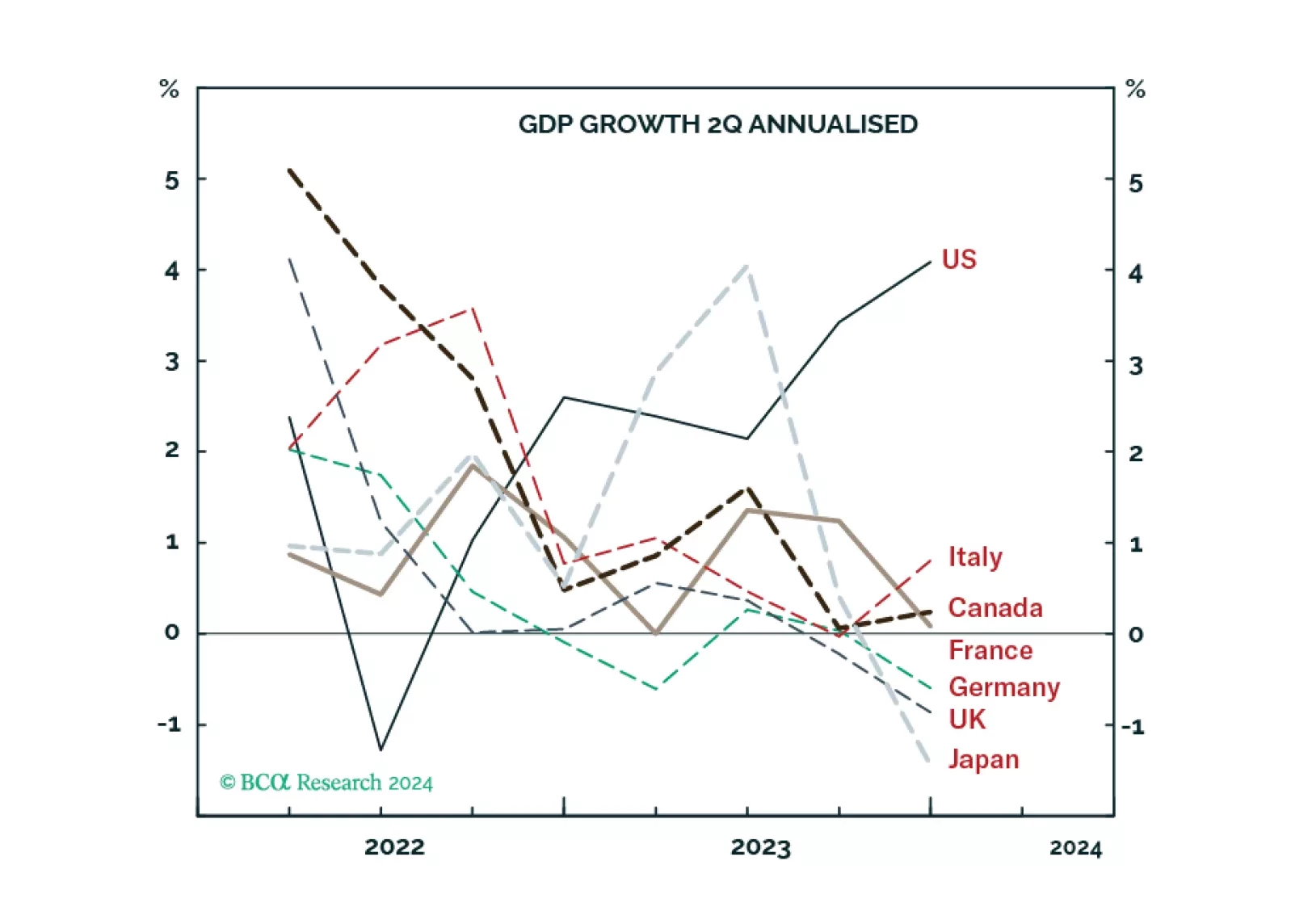

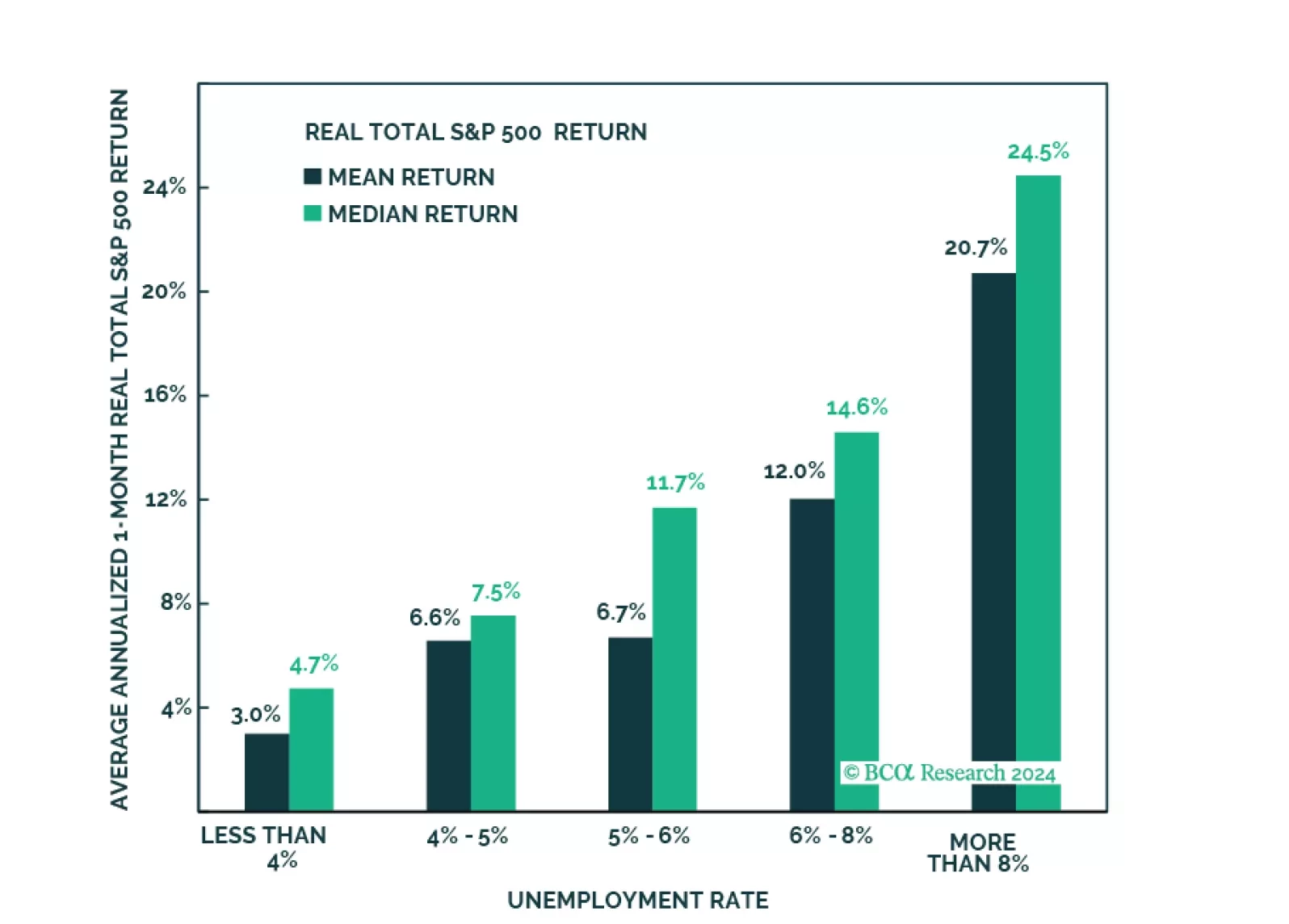

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

In this report, we review our trade recommendations based on incoming data in the last month.

MacroQuant downgraded equities from overweight to neutral on a 1-to-3 month horizon. The model maintains a negative view on stocks over a 12-month horizon.

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

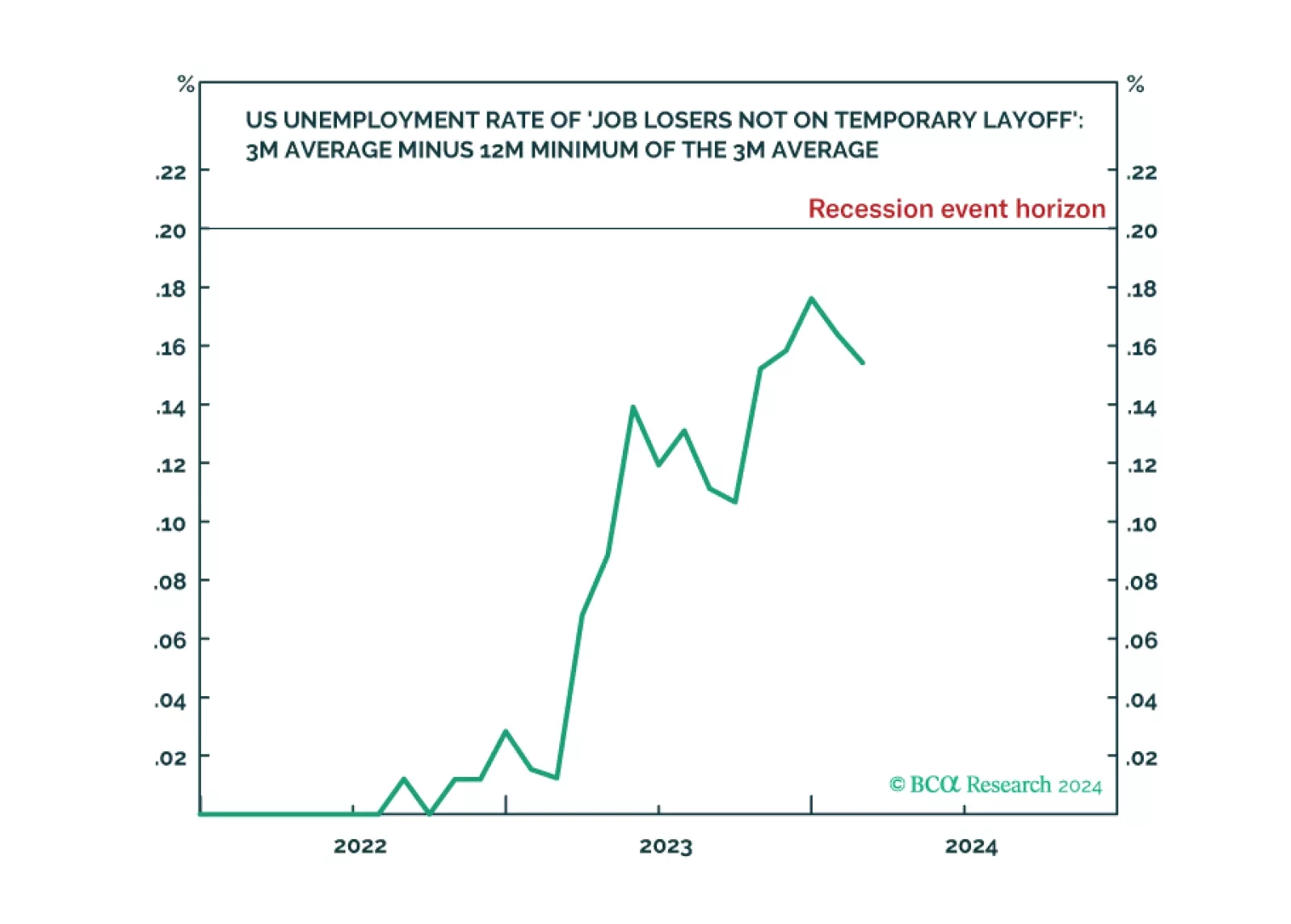

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).