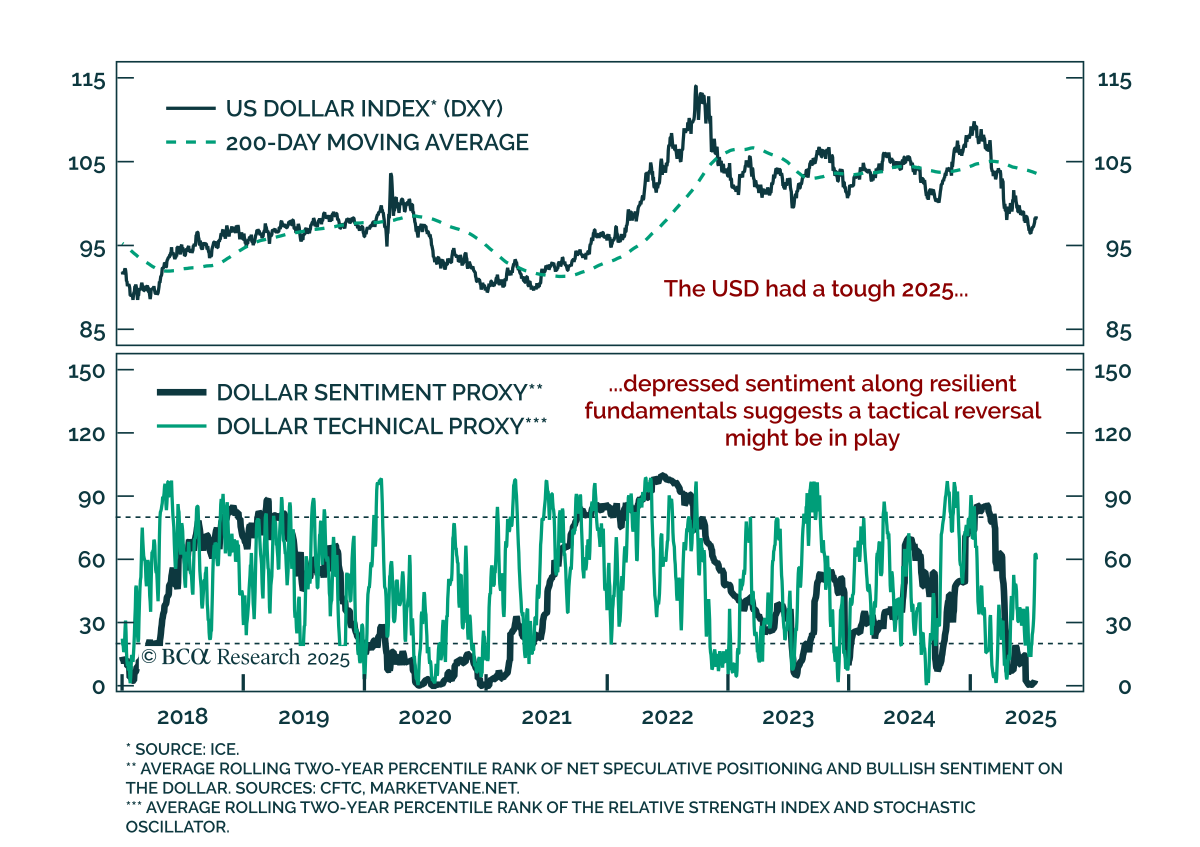

US Dollar

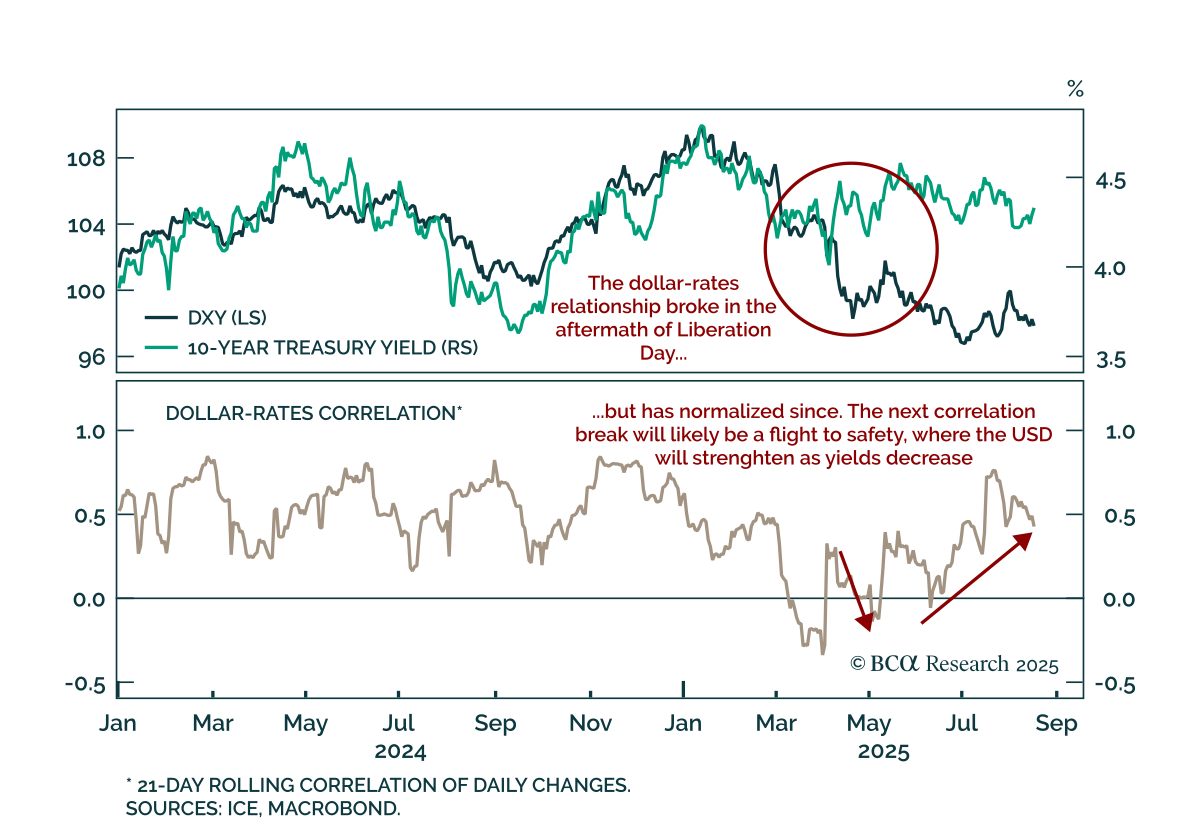

Trade tensions briefly broke the USD-rates link, but the dollar will remain a countercyclical currency for the near future. A key 2025 trend has been USD depreciation, driven by foreign investors reducing exposure to US assets. At the peak of stress,…

Our US Political Strategy team recommends staying long the US dollar, as Trump’s peak political capital drives near-term policy volatility and renewed support for US assets. Market optimism is underpinned by AI enthusiasm and the prospect of Fed easing,…

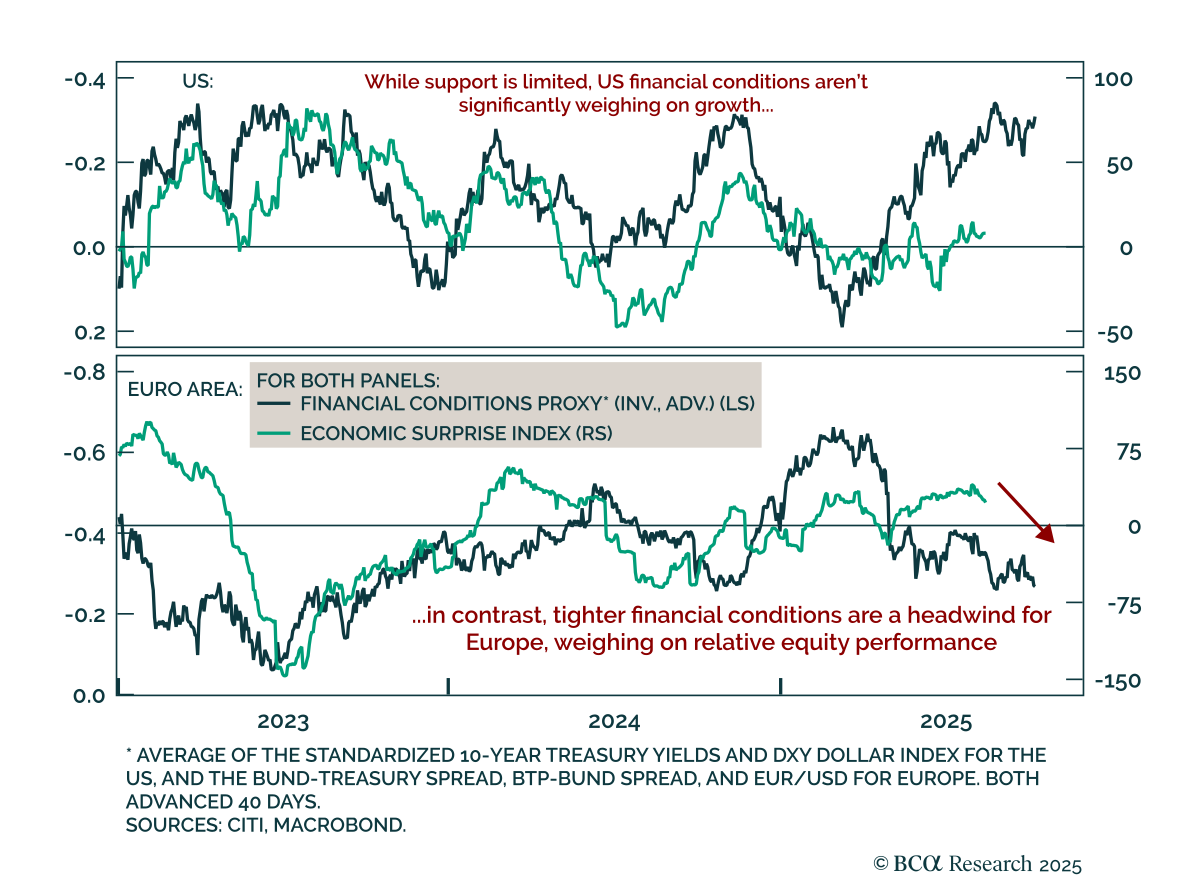

Dollar softness has had little growth impact, and European equities should keep lagging. A key 2025 trend has been USD depreciation, but the associated easing in financial conditions has offered minimal support to US growth, reflecting higher term premia…

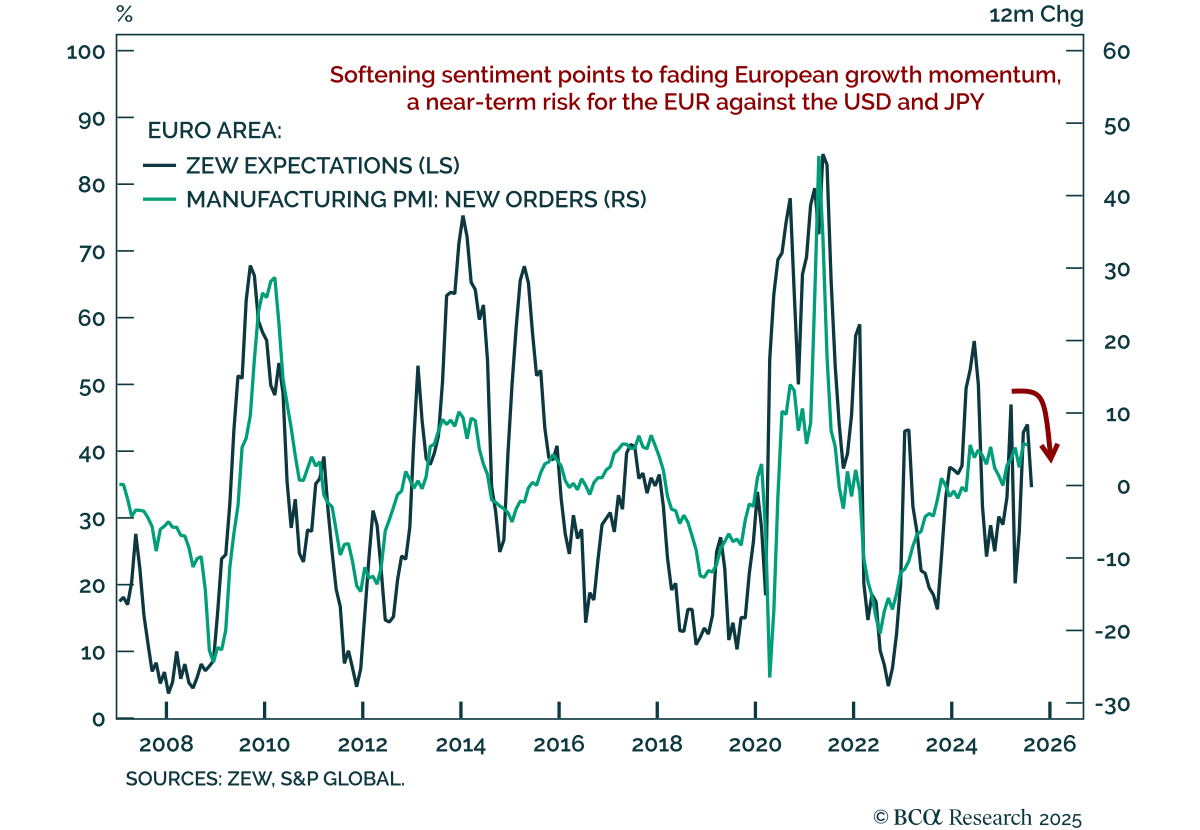

European sentiment has moderated, pointing to near-term downside risk for a technically-stretched Euro. The August Eurozone ZEW Expectations index fell to 25.1 from 36.1, with Germany’s reading missing estimates, dropping sharply to 34.7 from 52.7. The German…

Our DM ex. US strategists see the yen entering a multi-year rally and recommend shorting EUR/JPY now while preparing to short USD/JPY as Fed cuts approach. The yen remains deeply undervalued across PPP, unit labor cost, and real trade-weighted metrics, near…

Microsoft has gone up in a worryingly near-perfect straight line with dimension 1.098. Take August off before making a big commitment to stocks. Plus: a new tactical trade is to go long USD/HUF.

EUR/USD has broken below key support, and near-term risks justify a tactical bearish stance while longer-term investors should buy dips. The pair fell through its 50-day moving average, which, along with the 20-day, had provided steady support since…

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

The US-EU trade deal lifts uncertainty but imposes high tariffs, weighing on the EUR and supporting our long USD positioning. The agreement includes a 15% tariff on all EU exports to the US, including cars and potentially, pharmaceutical products,…

The USD remains structurally challenged, but near-term tactical conditions suggest a temporary bottom is in place. After a sustained selloff and rising concerns around its reserve status, the dollar has decoupled from rate differentials, a behavior more…