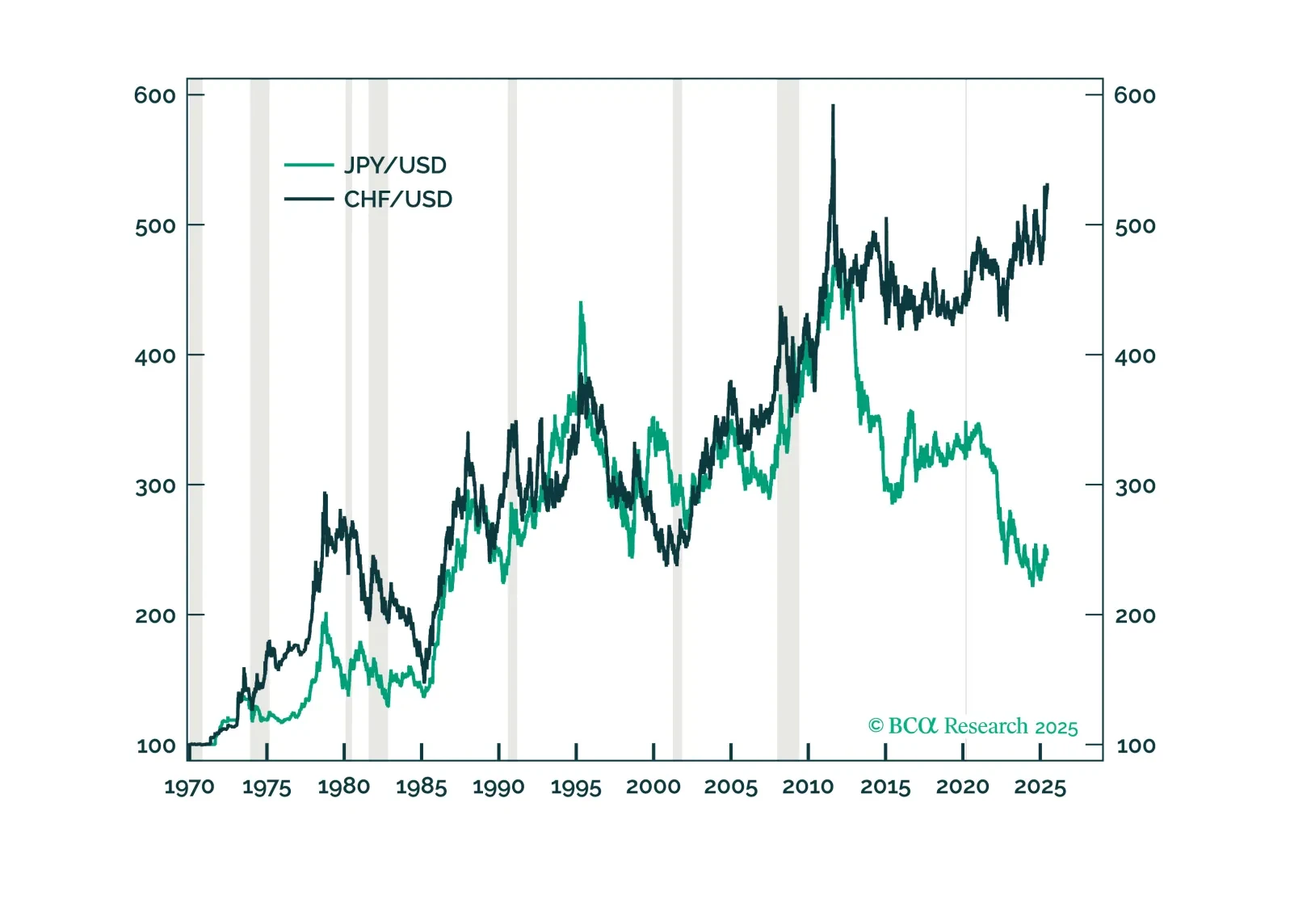

US Dollar

In this Insight, we highlight our strong conviction trades based on the central bank meetings held by the Bank of England, the Norges Bank, the Swiss National Bank and the Riksbank.

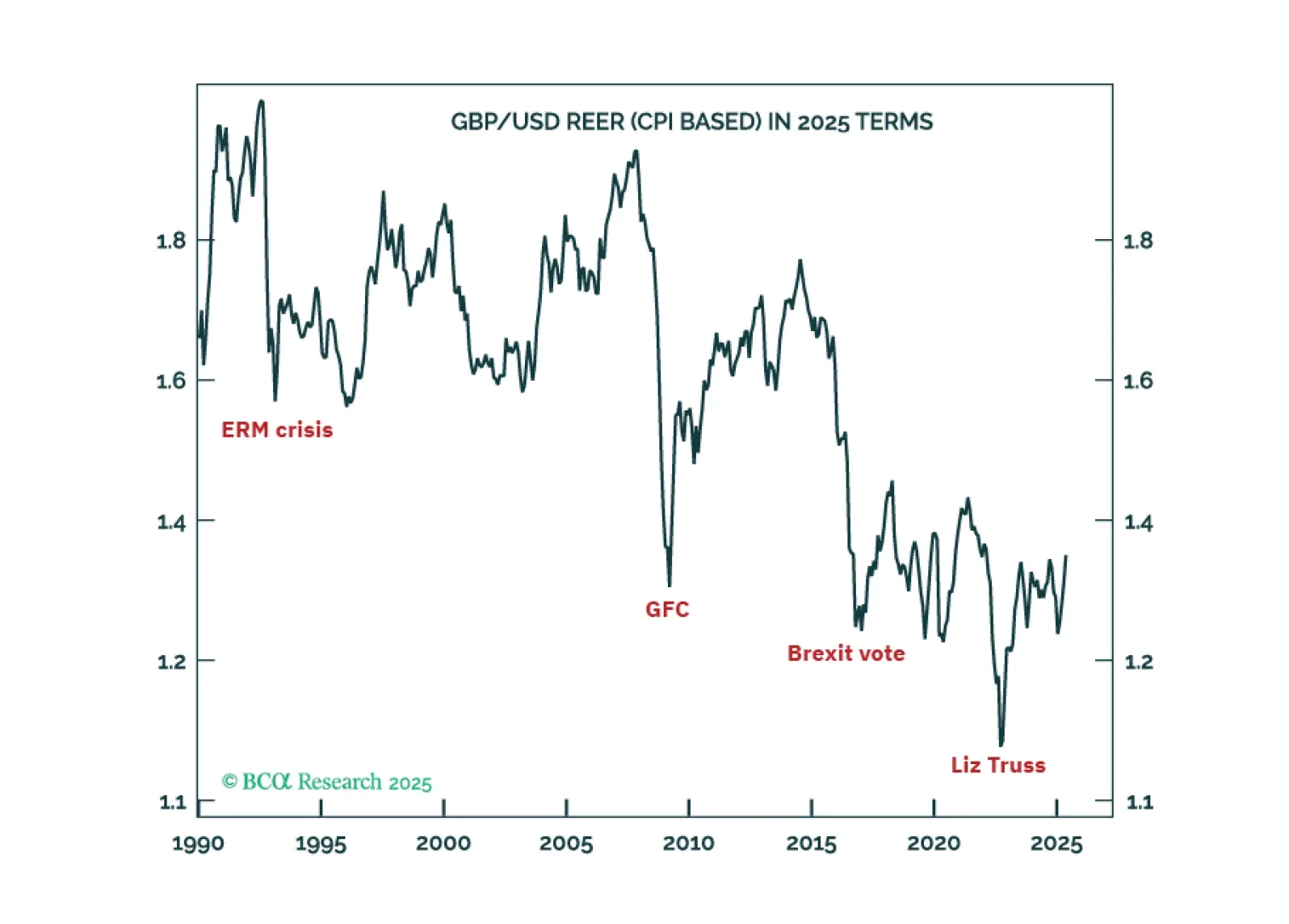

The pound will reach $1.60 if ‘America’s Brexit’ cancels out ‘Britain’s Brexit’. Meanwhile, the flight from the fiat dollar to non-fiat bitcoin will enable the preeminent cryptocurrency to reach $200,000+.

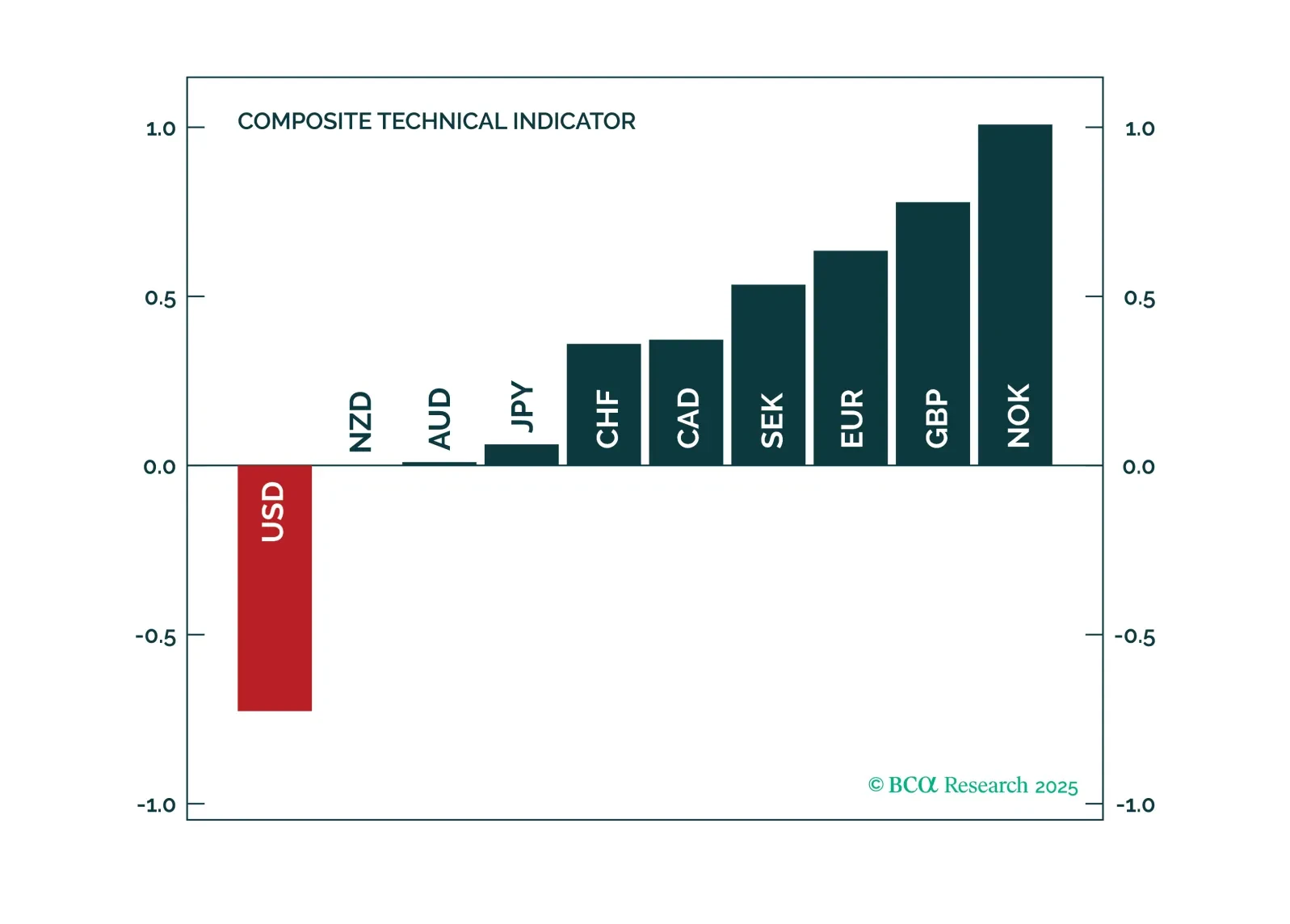

In this FX note, we provide a rationale for why it is important to pay attention to technical indicators, while still keeping your eyeball on the structural factors that drive currencies. This report answers the following questions: 1. Should you buy or sell the USD over a three-to-six month period from the pure lens of our proven technical indicators and 2. What are the best tactical cross trades among currencies.

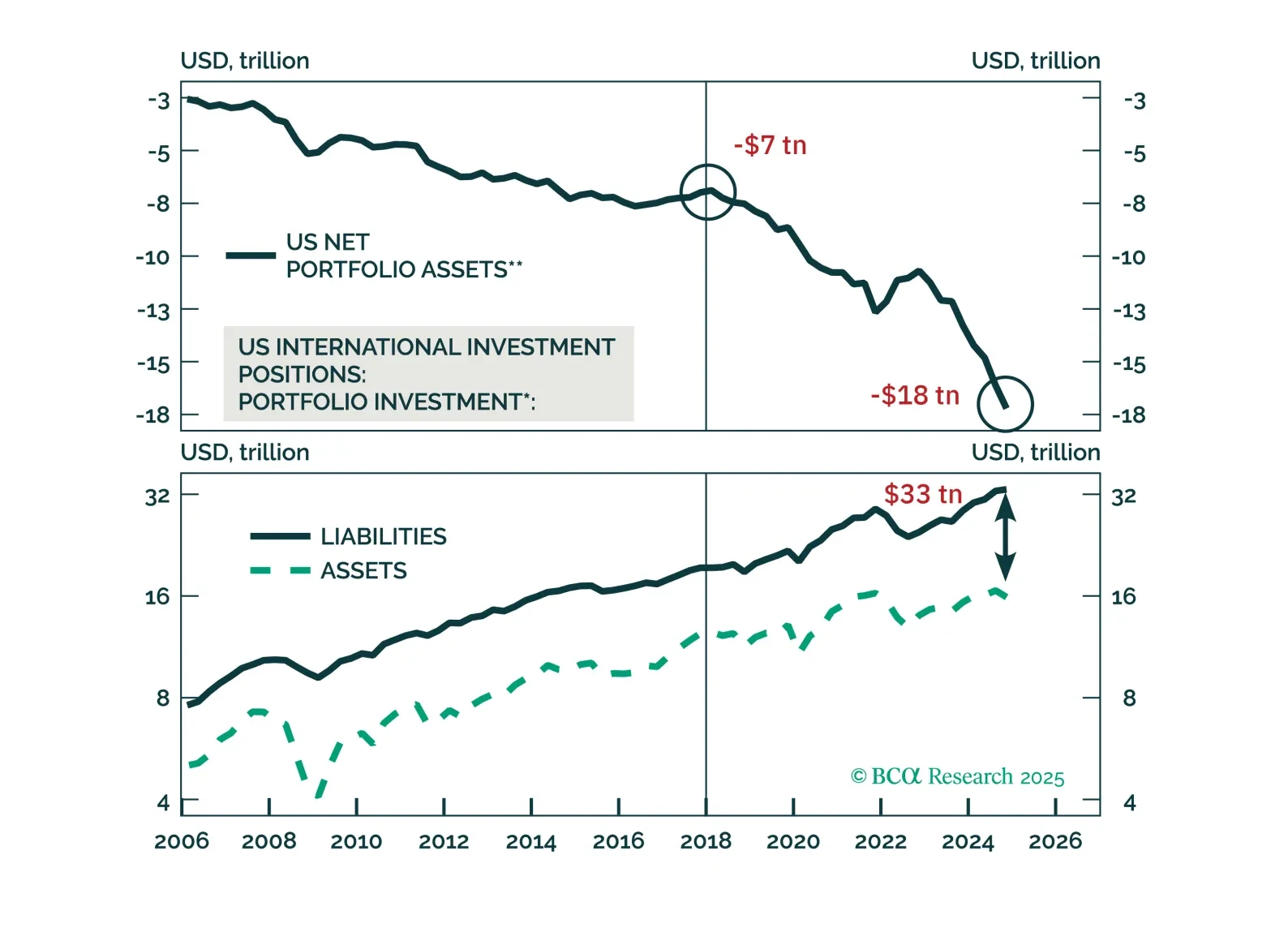

In our Beta report, we focus on our decade view. Many of our global allocator clients are scrambling to incorporate geopolitics into their strategic asset allocation. For most, this means thinking about war… or about future end-states. This is a mistake. We consider the next five years (maybe a decade) as the transition to the new era, a transition away from American unipolarity. And the transition itself is investment relevant. A transition to a multipolar world – which we think is occurring – will crush the USD and favor non-US assets. A transition to a bipolar world – not our base case, but still possible – would do the opposite.

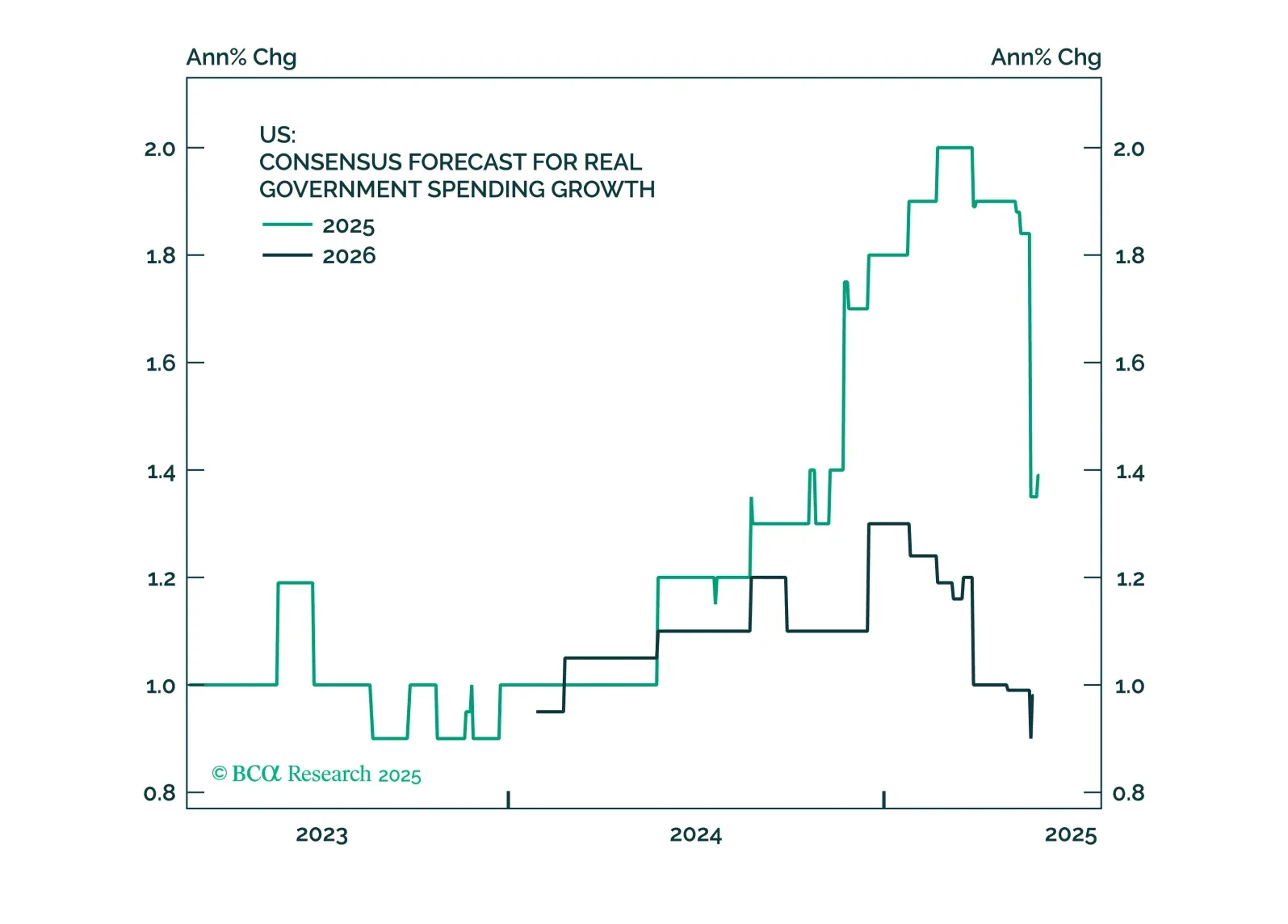

This month, we focus on the One Big Beautiful Bill Act (OBBBA). Our assessment in the Alpha report is that there won’t be any remaining alpha to harvest by shorting duration. The team that coined the “Human Steepener” moniker for President Trump is, effectively, throwing in the towel on looking for more upside to yields. There are many reasons for that view, but the main one is that the OBBBA legislation is just not that profligate, especially not relative to the investors’ expectations in the early days of the Trump 2.0 term.

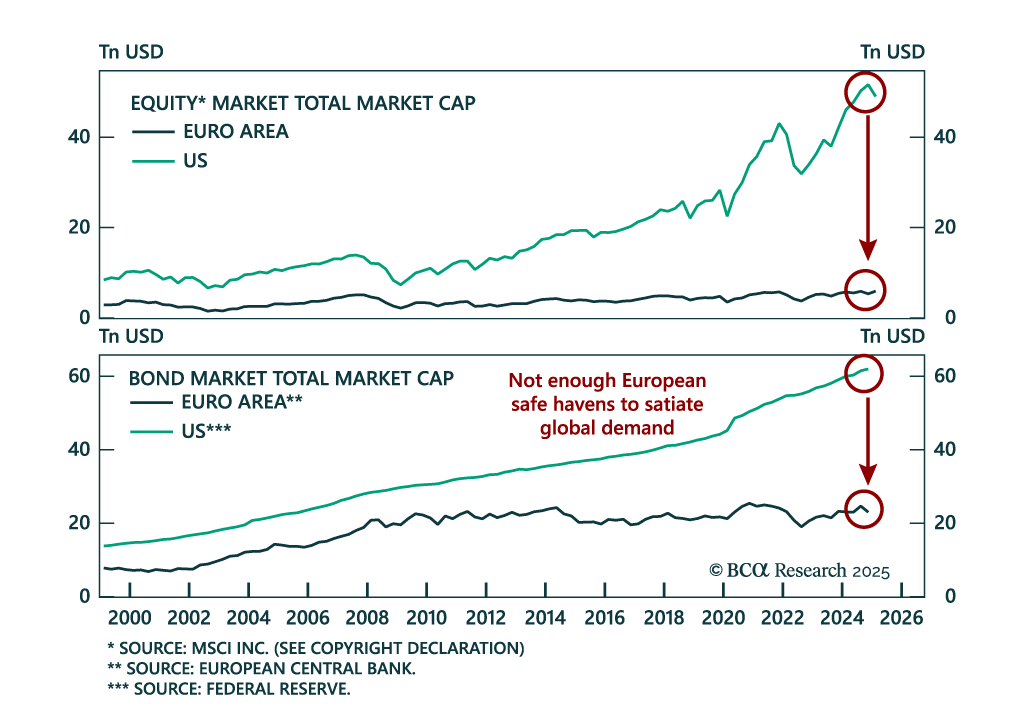

Global currency markets have entered a new era. This implies that the framework for analyzing exchange rates must also change. We introduce a new framework for analyzing EM currencies and classify them into resilient and vulnerable categories. Finally, we are adding more EM domestic bonds to our portfolio and making many changes to our currency trades.

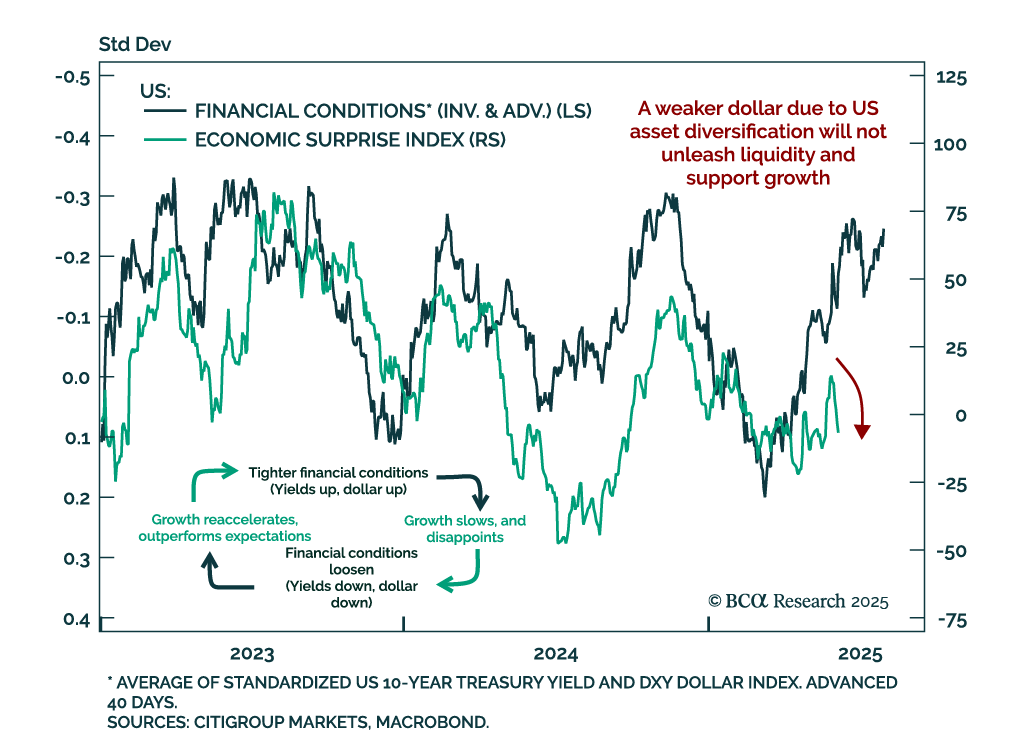

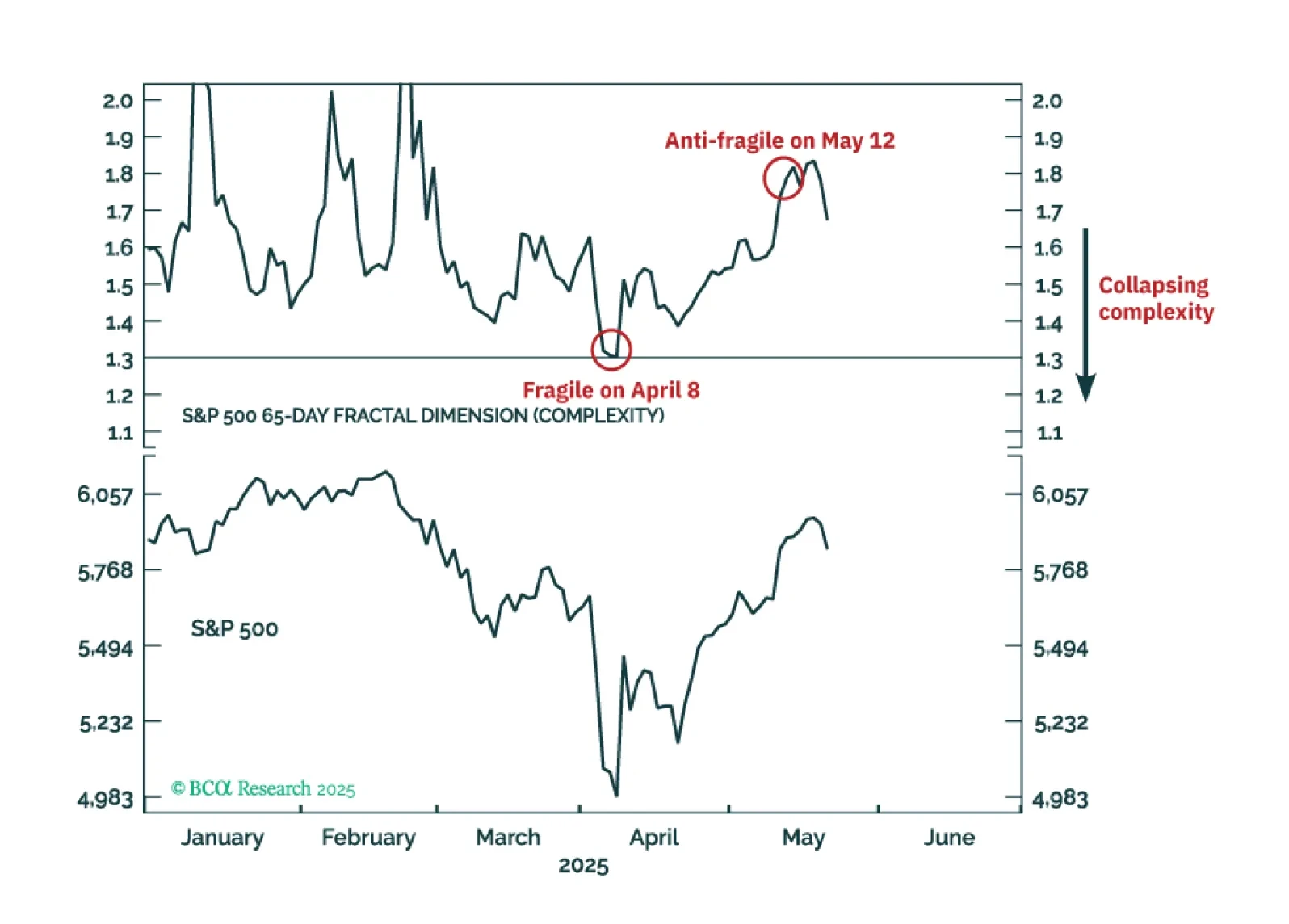

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

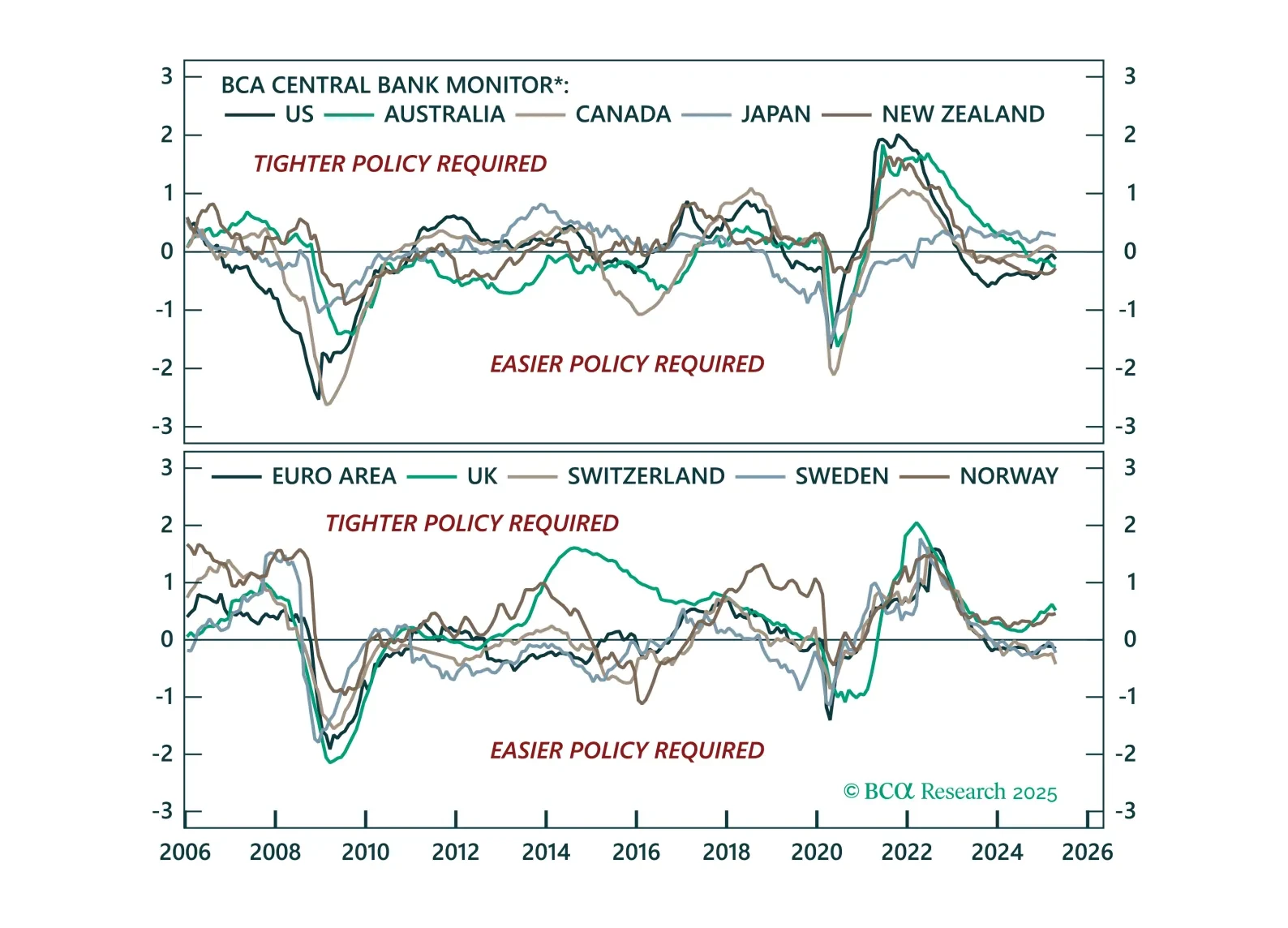

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.